Corporate Accounting and Reporting: Measurement of Impairment Loss

VerifiedAdded on 2020/06/04

|9

|1544

|199

Report

AI Summary

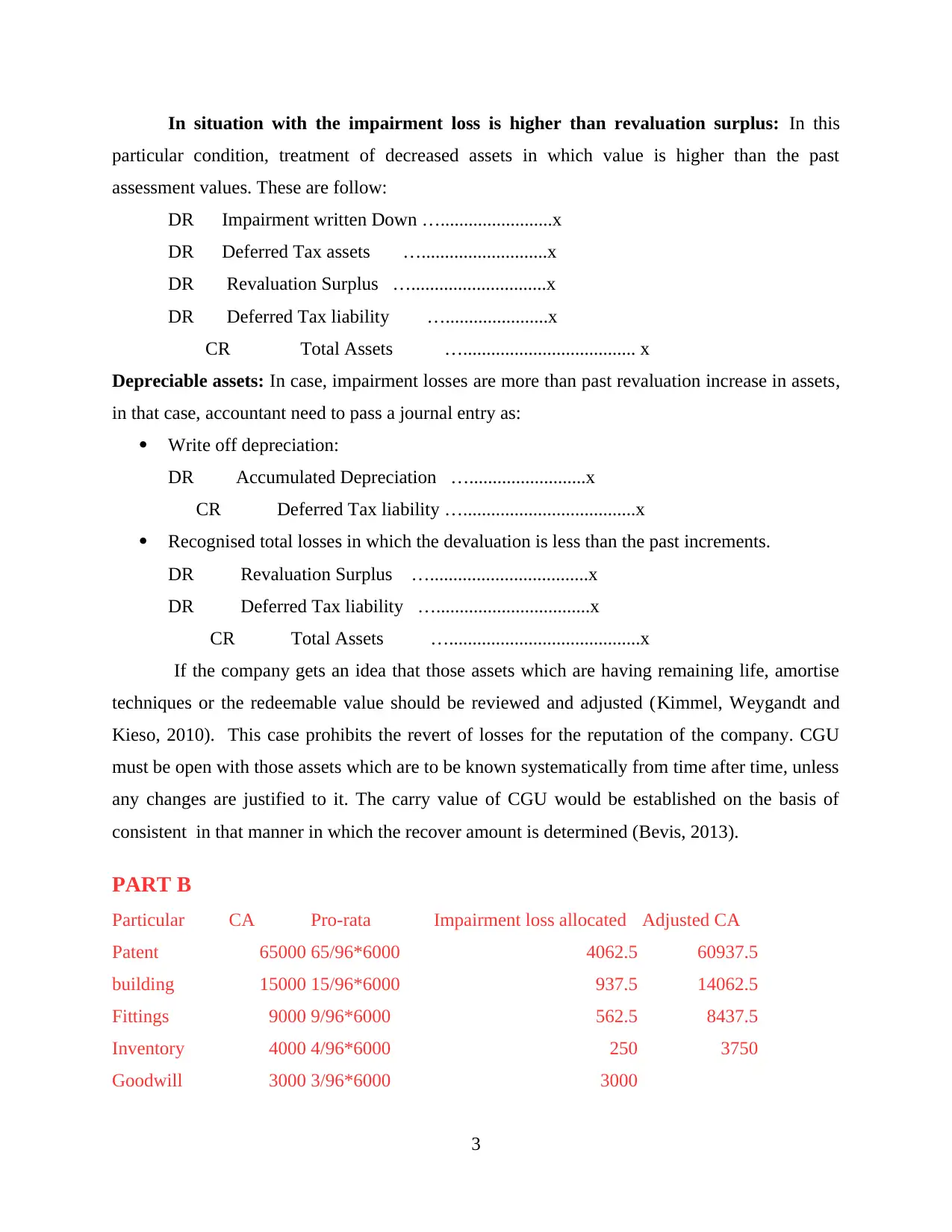

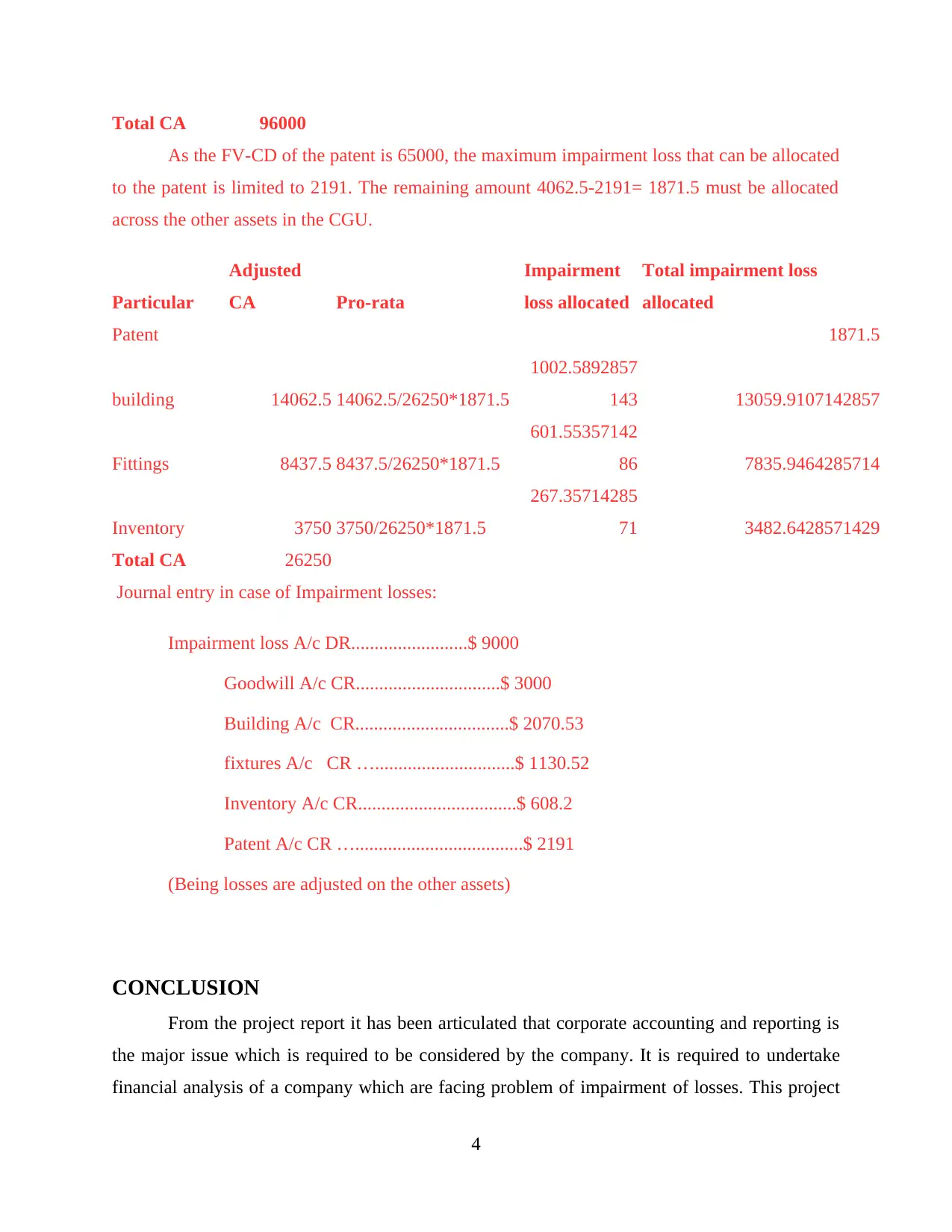

This report delves into the critical aspects of corporate accounting and reporting, specifically focusing on the measurement and recognition of impairment loss for assets. The report begins by defining corporate accounting and its role in financial statement analysis. It then explores the concept of impairment loss, explaining its occurrence when asset values decline and the need for testing. The report details the two methods for measuring impairment losses, including the recoverability test, and provides journal entries for various scenarios, such as assets carried at cost, asset decreases, and revaluation of assets. Furthermore, the report analyzes a practical example, allocating impairment losses across different assets within a cash-generating unit (CGU). The conclusion emphasizes the significance of understanding impairment loss in financial analysis and reporting, summarizing the key concepts and accounting treatments discussed throughout the report. The report also includes a table that illustrates the allocation of impairment loss across various assets within a CGU, providing a clear and practical application of the concepts discussed.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.