Corporate Accounting: Impairment Loss Calculation and AASB 136

VerifiedAdded on 2023/06/07

|5

|1372

|338

Homework Assignment

AI Summary

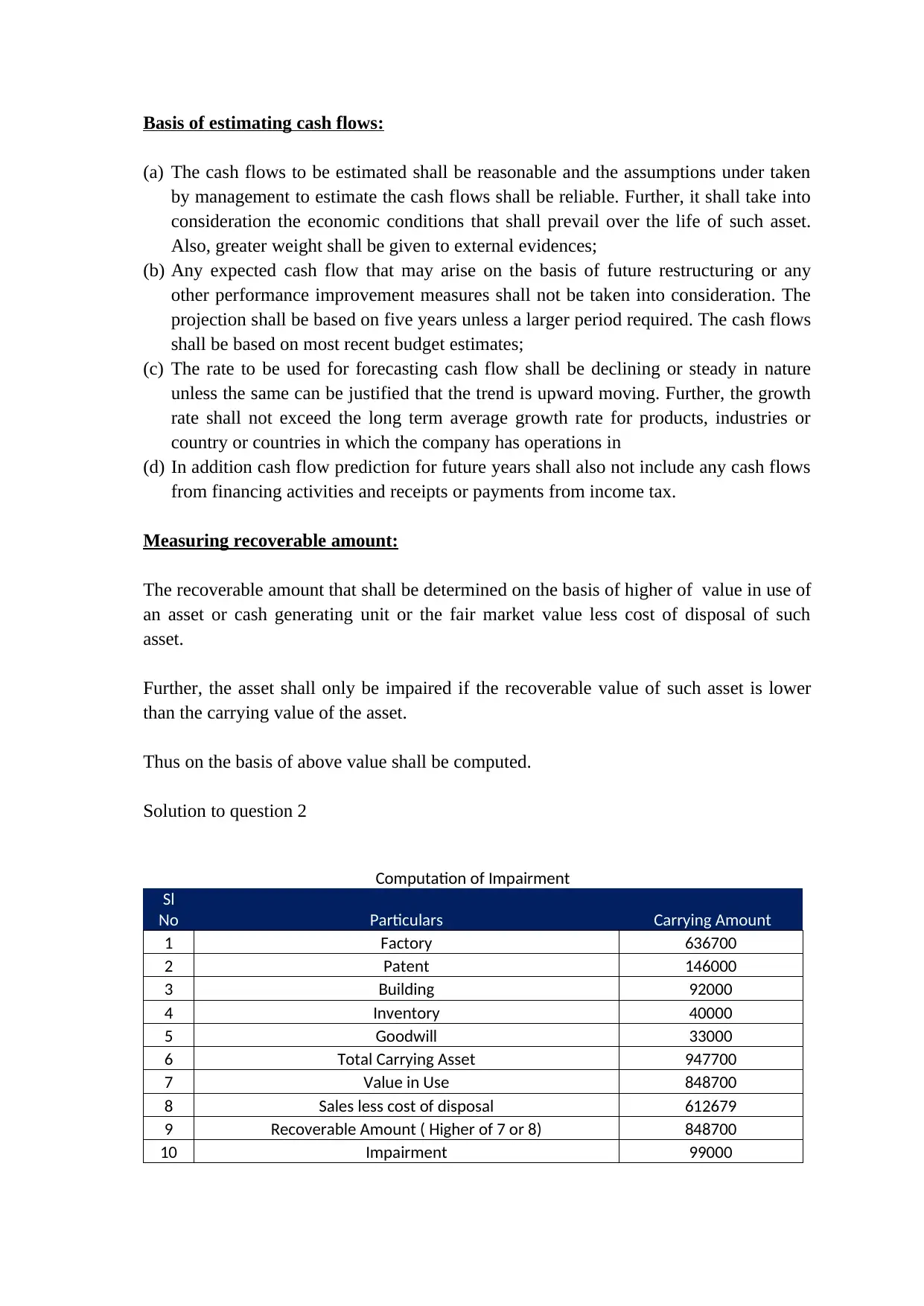

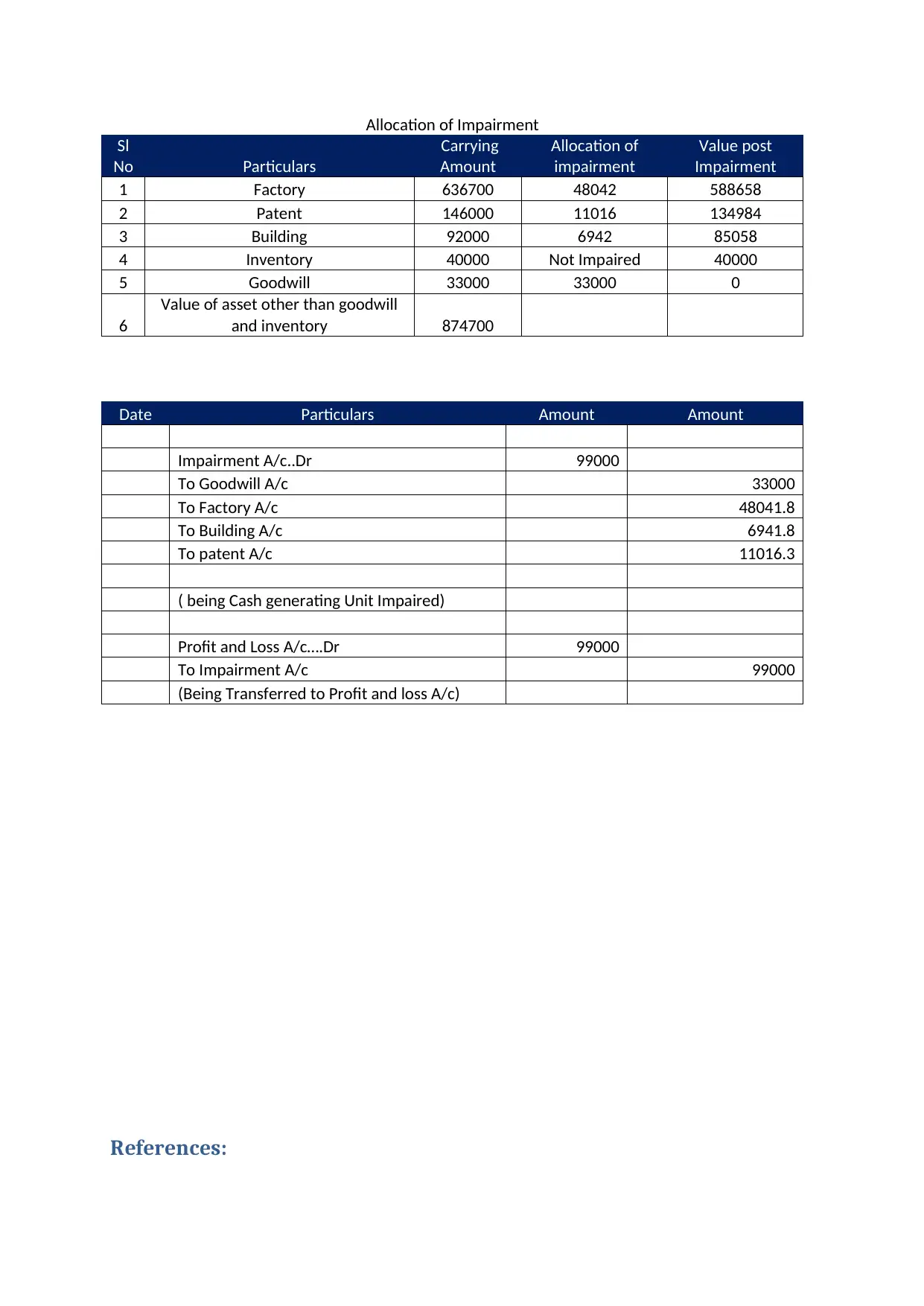

This assignment solution delves into the intricacies of corporate accounting and reporting, focusing on the definition of key terms such as value-in-use, useful life, cash generating unit, depreciable amount, fair value, impairment loss, and recoverable amount as per accounting standards. It provides a detailed explanation of how to calculate recoverable amount, value in use, and fair value less cost of disposal in accordance with AASB 136 - Impairment of Assets, including considerations for fair market value determination and cash flow estimation. The solution includes a practical example demonstrating the computation of impairment, allocation of impairment across various assets (factory, patent, building, inventory, and goodwill), and the corresponding journal entries. The assignment concludes with a list of references to support the analysis and calculations presented.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.