Corporate Accounting: Impairment Loss Calculation and Distribution

VerifiedAdded on 2023/06/12

|8

|1594

|123

Report

AI Summary

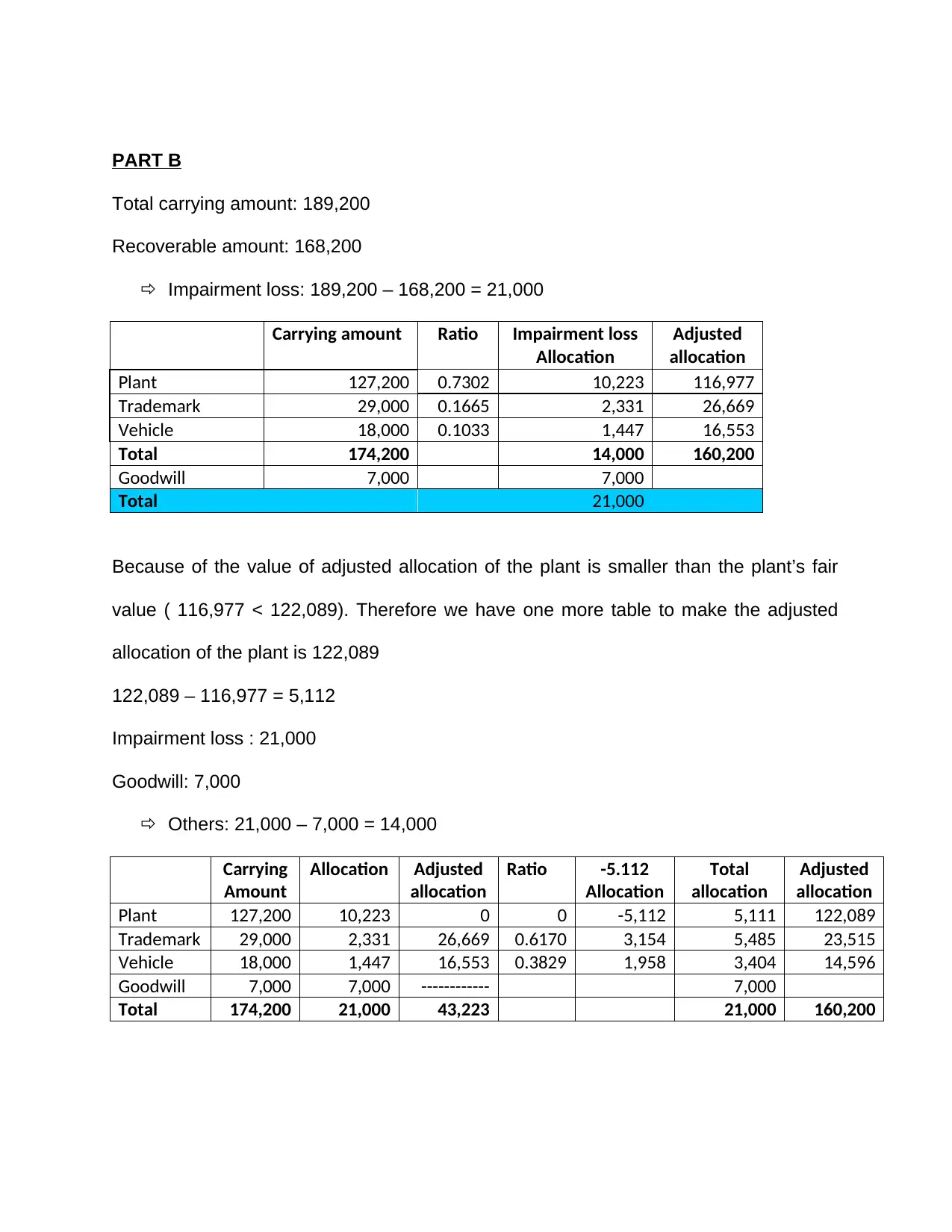

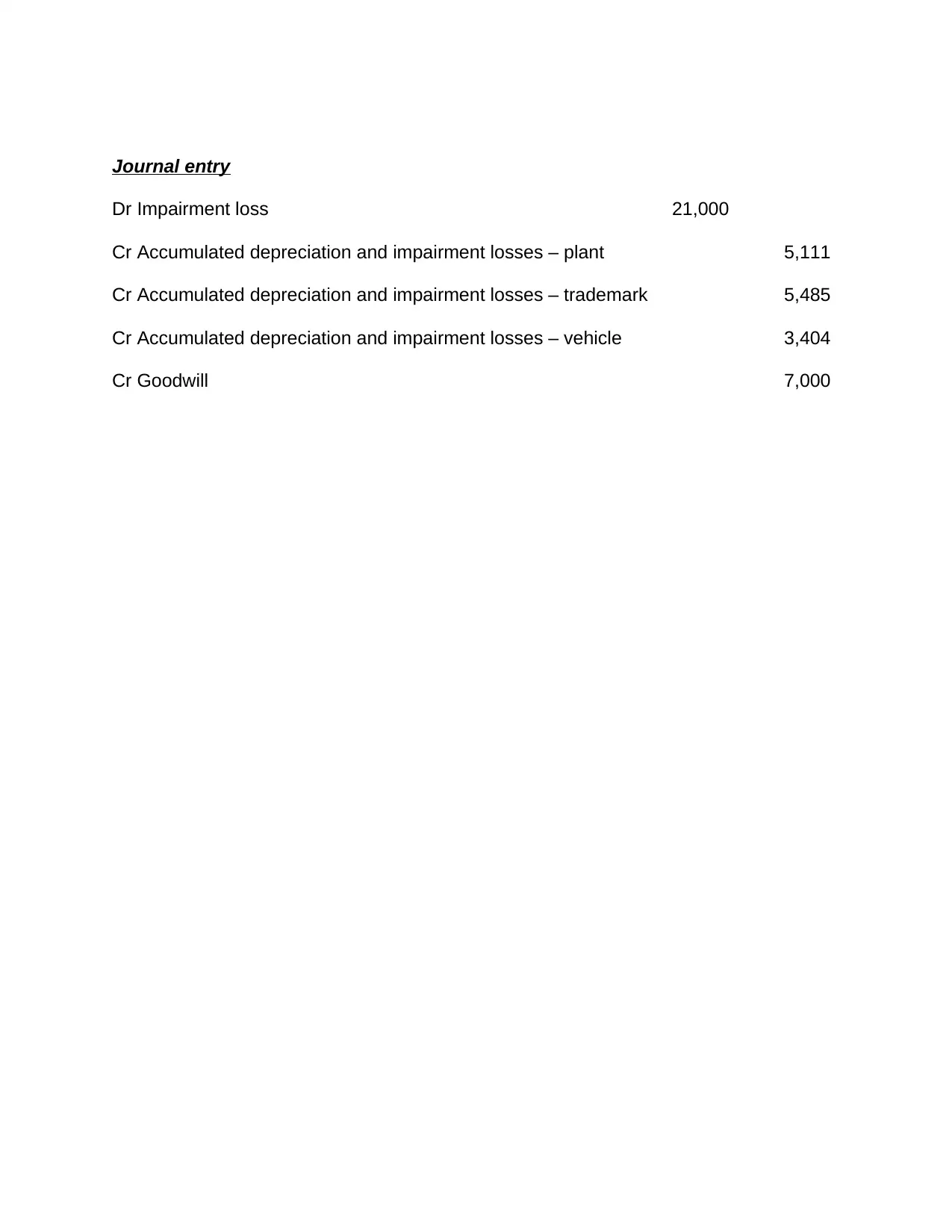

This report provides a comprehensive analysis of impairment loss for cash-generating units within the context of corporate accounting and reporting, referencing AASB 136 standards. It discusses the principles of impairment, emphasizing that assets cannot be carried above their recoverable amount, defined as the higher of fair value less selling costs and value-in-use. The report details the process of identifying impairment indications, conducting annual impairment tests for assets like goodwill, and calculating recoverable amounts. It explains how impairment losses are distributed within cash-generating units, initially reducing goodwill and then other assets on a pro-rata basis, ensuring that carrying values are not reduced below certain thresholds like value-in-use or fair value less disposal costs. A practical example involving a damaged machine illustrates the application of these principles, highlighting scenarios where impairment loss is recognized versus when reassessment of depreciation is more appropriate. The report includes a numerical example demonstrating the calculation and allocation of impairment loss across different assets, including plant, trademark, vehicle, and goodwill, along with the corresponding journal entries. It concludes by emphasizing the importance of proper accounting for impairment losses in accordance with accounting standards.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.