Corporate Accounting and Reporting: Impairment Analysis Report

VerifiedAdded on 2020/04/07

|8

|1685

|62

Report

AI Summary

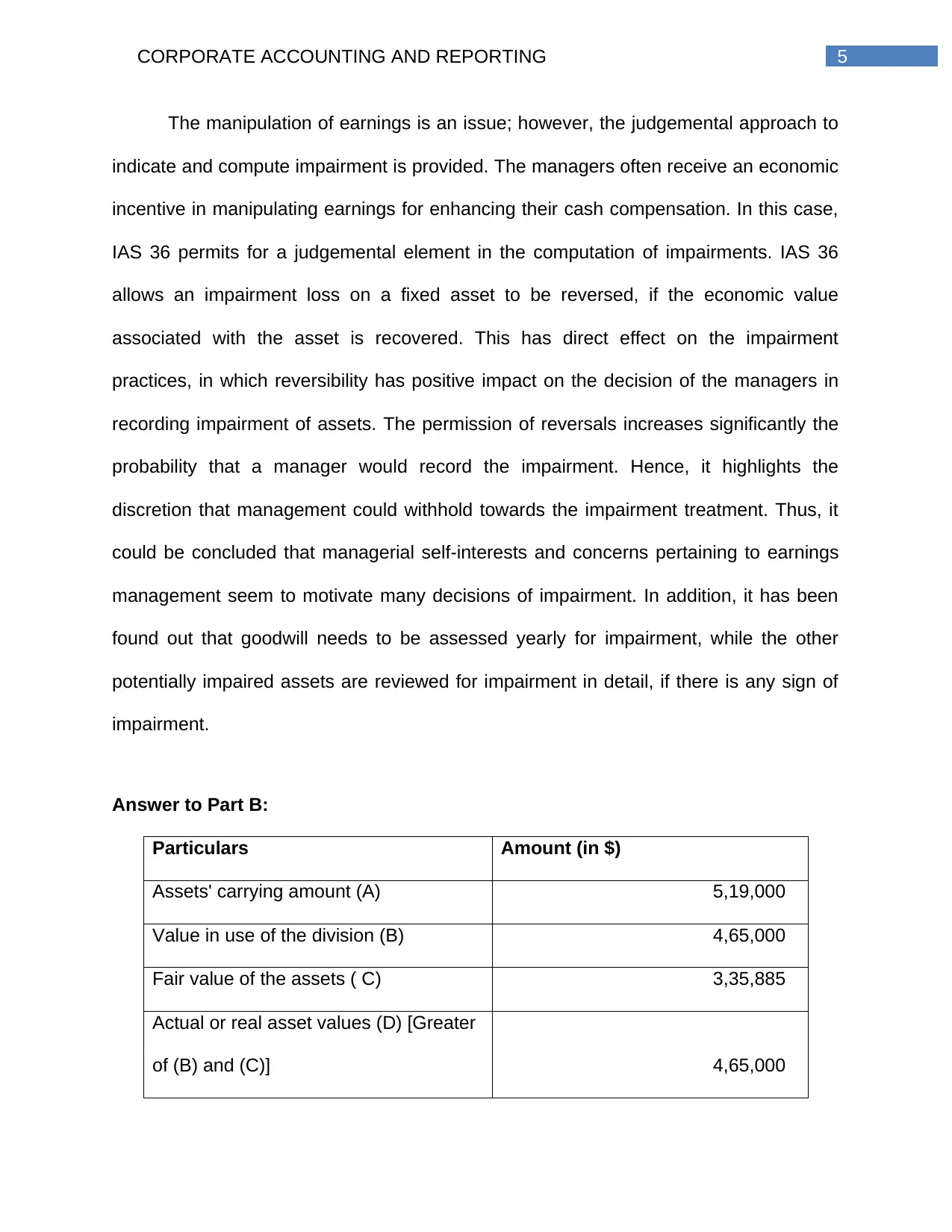

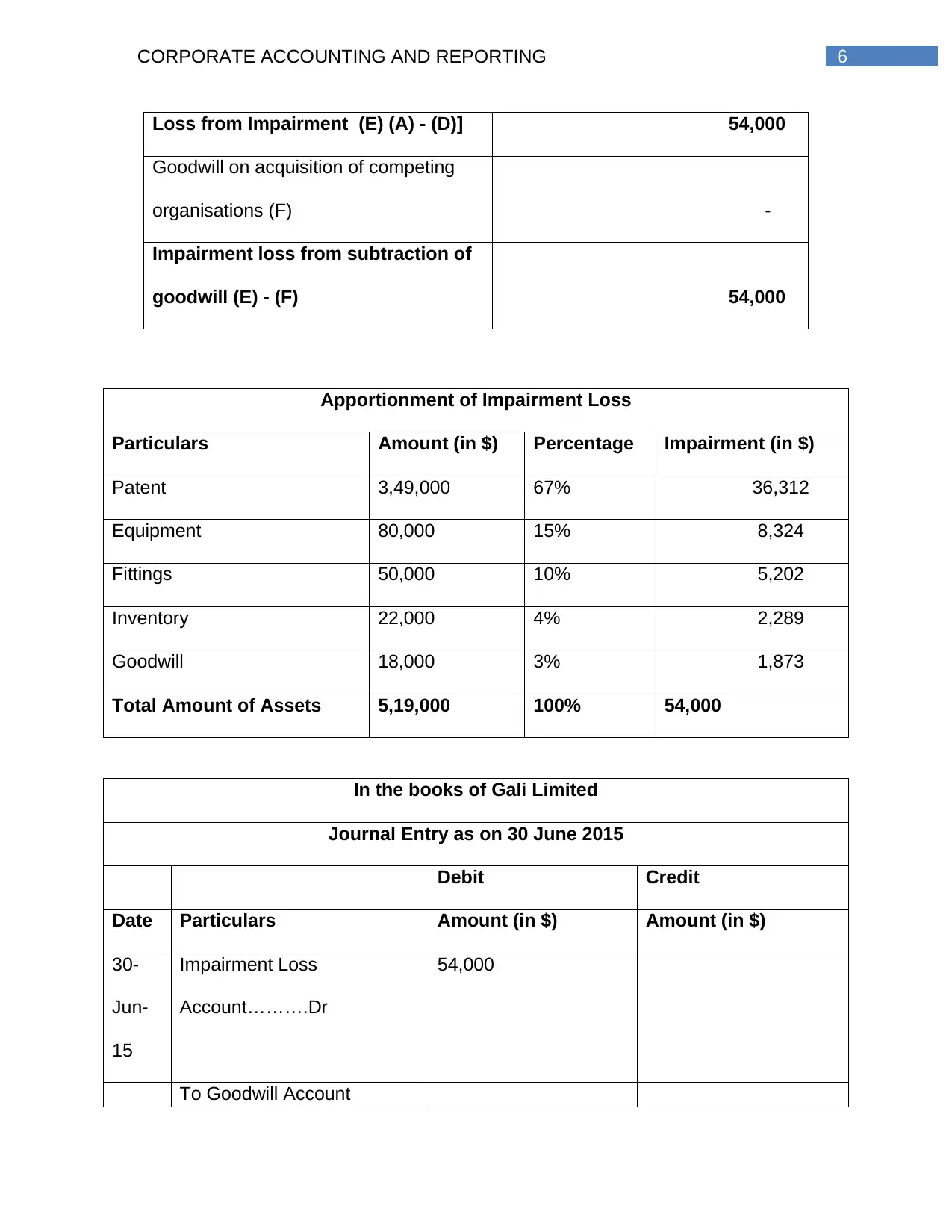

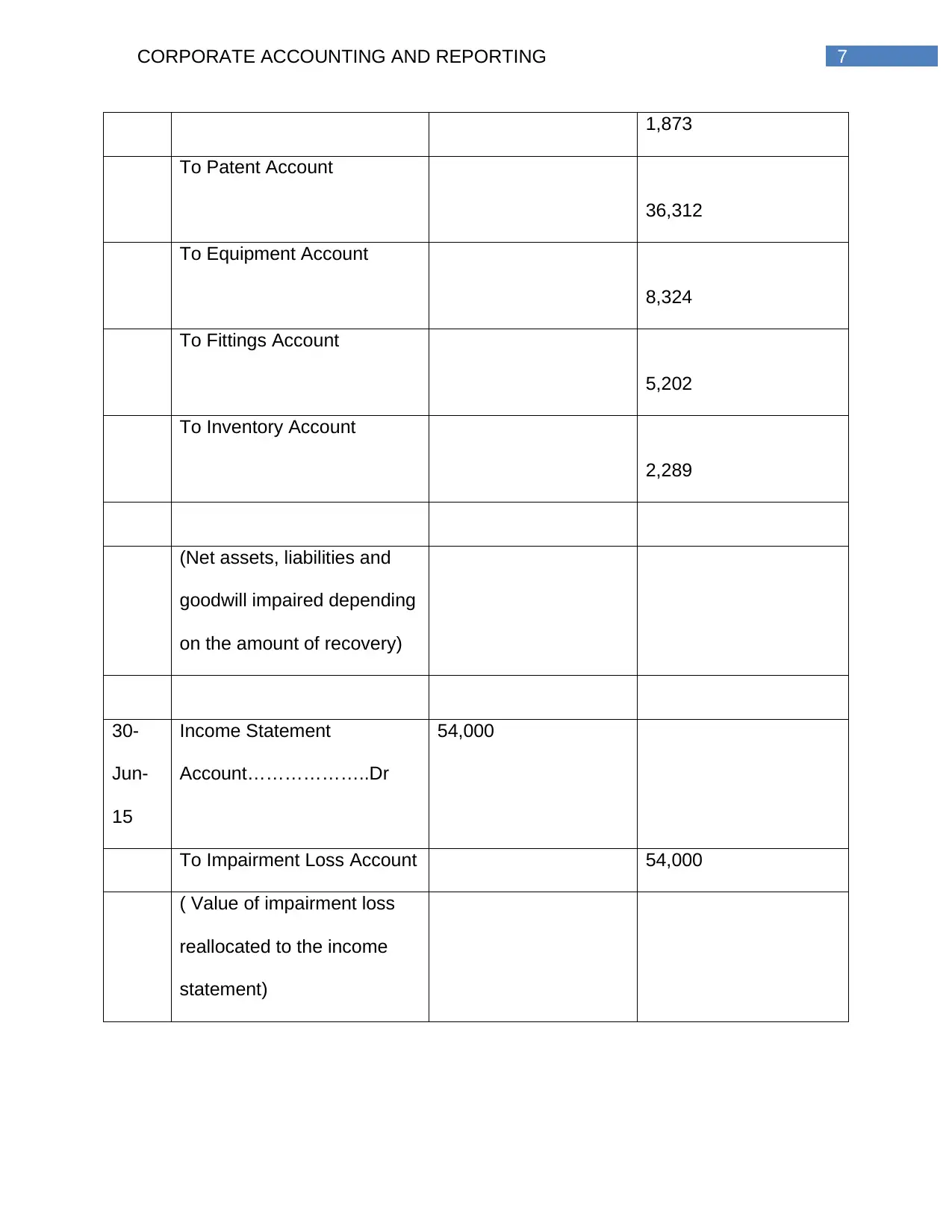

This report provides an in-depth analysis of corporate accounting, with a specific focus on asset impairment according to IAS 36. The report explains the concept of impairment loss, detailing the situations in which it occurs and the assessment of asset values compared to their recoverable amounts. It examines the role of impairment indicators, both internal and external, and the process of determining the recoverable amount. The report also includes a practical application of these principles through a case study, presenting a scenario involving asset impairment and providing a journal entry to reflect the financial impact. It also includes a detailed breakdown of the impairment loss apportionment across different asset types, such as patents, equipment, and goodwill, demonstrating the practical application of accounting standards. The report also touches upon the challenges associated with impairment testing, including the subjectivity in valuation models and the potential for managerial discretion in earnings management, which can impact the comparability of financial statements.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.