University Corporate Accounting & Reporting Assignment Solution

VerifiedAdded on 2019/10/31

|10

|2294

|143

Homework Assignment

AI Summary

This assignment solution addresses corporate accounting and reporting, focusing on the concept of impairment as per IAS 36. It defines impairment, the calculation of recoverable value, and the allocation of impairment losses across different assets, including goodwill. The solution explains the concepts of Cash Generating Units (CGUs), internal and external indicators of impairment, and the process of impairment reversal. The assignment includes a detailed solution to a question involving the impairment assessment of a CGU, including the calculation of impairment loss and journal entries. The solution also provides a conclusion on the implications of impairment and the necessary disclosures in financial statements. References to relevant academic sources are included.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 16 Spetember 2017.

1 | P a g e

By student name

Professor

University

Date: 16 Spetember 2017.

1 | P a g e

2

Contents

Introduction...…………………………………………………………………………………………….......3

Concepts on Impairment of CGU and its reversal……………………………………………..........

……………………………..……………………...4

Solution to Question 2……………………………………………….....…………………………………6

Conclusion and Disclosure..……………………………………….....…………………………………8

Refrences.....……………………………………………………………….......................................9

2 | P a g e

Contents

Introduction...…………………………………………………………………………………………….......3

Concepts on Impairment of CGU and its reversal……………………………………………..........

……………………………..……………………...4

Solution to Question 2……………………………………………….....…………………………………6

Conclusion and Disclosure..……………………………………….....…………………………………8

Refrences.....……………………………………………………………….......................................9

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Introduction – Impairment

As per IAS 36 and AS 28, impairment of the assets is described as write down in the

value of the assets of an entity based on the regular assessments. It should not be carried in the

books at more than the recoverable value, i.e., higher of the fair value of the asset less cost of

disposal and value in use. The difference between net carrying value in the books and the

recoverable value is called the impairment loss. The company needs to check on the impairment

of the assets if the relevant conditions exist and thereby make necessary adjustments in the value

of the asset in the financials.Goodwill and other intangible assets are being reviewed annually

and separately for impairment through an impairment test as per the standard. In case the single

asset is identifiable and is independent of other units in terms of generating the revenue for the

company, it should be assessed individually for impairment else the smallest possible group or

class of assets which is capable of generating the revenue independently known as the cash

generating unit needs to be assessed for impairment. It is not necessary the asset once impaired

will be as it is and can never be appreciated based on the relevant factors but there can be the

reversal of impairment loss recorded earlier based on the improved and positive business

conditions and other factors. Therefore, it can also be reversed based on the existence of the

relevant indicators. IAS 36 applies to land, building, plant and machinery, intangible assets,

goodwill, investments in subsidiaries or other companies as well. However, it does not applies to

inventories, deferred tax assets, financial assets, assets from construction contracts and assets

which arise out of employee benefits, agricultural assets and non current assets held for sale

purposes. (Buchanan, et al., 2017)

3 | P a g e

Introduction – Impairment

As per IAS 36 and AS 28, impairment of the assets is described as write down in the

value of the assets of an entity based on the regular assessments. It should not be carried in the

books at more than the recoverable value, i.e., higher of the fair value of the asset less cost of

disposal and value in use. The difference between net carrying value in the books and the

recoverable value is called the impairment loss. The company needs to check on the impairment

of the assets if the relevant conditions exist and thereby make necessary adjustments in the value

of the asset in the financials.Goodwill and other intangible assets are being reviewed annually

and separately for impairment through an impairment test as per the standard. In case the single

asset is identifiable and is independent of other units in terms of generating the revenue for the

company, it should be assessed individually for impairment else the smallest possible group or

class of assets which is capable of generating the revenue independently known as the cash

generating unit needs to be assessed for impairment. It is not necessary the asset once impaired

will be as it is and can never be appreciated based on the relevant factors but there can be the

reversal of impairment loss recorded earlier based on the improved and positive business

conditions and other factors. Therefore, it can also be reversed based on the existence of the

relevant indicators. IAS 36 applies to land, building, plant and machinery, intangible assets,

goodwill, investments in subsidiaries or other companies as well. However, it does not applies to

inventories, deferred tax assets, financial assets, assets from construction contracts and assets

which arise out of employee benefits, agricultural assets and non current assets held for sale

purposes. (Buchanan, et al., 2017)

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Concepts on Impairment of CGU and its reversal

A company needs to do the periodic evalauation of the assets whether the same can be

impaired given the circumstances of the case of else if it can be reversed if the impairment loss

on a particular asset has already been recognised. In case the indicators for impairment do exist,

the same needs to be identified and also the recoverable value of the assets. Indicators can be of

two types: internal and external indicators. Internal indiactors includes specifically the factosr

inside the company and on which the company exercises the control like physical damange to the

asset or its obsolescence, or asset is kept idle and held for sale, or the esset is expected to give

worst economic performance or the investment in subsidiary or the joint ventures is more than

the investee’s actual assets. (Das, 2017) There can also be external factors or indicators which

are not inside the control of the company but affects every company or industry as a whole like

the value of the assets lying in the books is higher than the market capitalization, or the market

value has declined considerably, or there is a negative change in the taste, preferences or

technology in the market or the market interest rates have increased. The list is just a few

examples of the factors and not the exhaustive one. Together with the impairment assessment the

company also needs to check on the depreciation method, the estimated useful life or even the

residual value of the asset at the end of certain period.

The question now is how to reverse the impairment value of the asset? It is to be done in

the same way as the impairment is done such that the above mentioned factors are on the positive

side. Post that the recoverable value needs to be ascertained. In case the fair value less cost of

disposal as well as the value in use is more than the carrying value the question of impairment

subsumes as it iis not required in this case. However, in case the opposite happens, the

recoverable value has to be determined and carrying value needs to be written off or charged to

profit and loss account for the differential amount. In case the fair value is not determinable, the

value in use becomes the recoverable value and in case of the disposable assets, the recoverable

value is the fair value less the cost of disposal. The determination of fair value has to be done in

accordance with the IFRS 13 which is on Fair value measurement. The cost of disposal includes

only the direct costs related to it. The other factor being value in use is detrmined through a

number of variables like the time value of money, the expected future cash flow generation

ability of the asset, the time lag in between the receipt of the amount from the use of the asset,

4 | P a g e

Concepts on Impairment of CGU and its reversal

A company needs to do the periodic evalauation of the assets whether the same can be

impaired given the circumstances of the case of else if it can be reversed if the impairment loss

on a particular asset has already been recognised. In case the indicators for impairment do exist,

the same needs to be identified and also the recoverable value of the assets. Indicators can be of

two types: internal and external indicators. Internal indiactors includes specifically the factosr

inside the company and on which the company exercises the control like physical damange to the

asset or its obsolescence, or asset is kept idle and held for sale, or the esset is expected to give

worst economic performance or the investment in subsidiary or the joint ventures is more than

the investee’s actual assets. (Das, 2017) There can also be external factors or indicators which

are not inside the control of the company but affects every company or industry as a whole like

the value of the assets lying in the books is higher than the market capitalization, or the market

value has declined considerably, or there is a negative change in the taste, preferences or

technology in the market or the market interest rates have increased. The list is just a few

examples of the factors and not the exhaustive one. Together with the impairment assessment the

company also needs to check on the depreciation method, the estimated useful life or even the

residual value of the asset at the end of certain period.

The question now is how to reverse the impairment value of the asset? It is to be done in

the same way as the impairment is done such that the above mentioned factors are on the positive

side. Post that the recoverable value needs to be ascertained. In case the fair value less cost of

disposal as well as the value in use is more than the carrying value the question of impairment

subsumes as it iis not required in this case. However, in case the opposite happens, the

recoverable value has to be determined and carrying value needs to be written off or charged to

profit and loss account for the differential amount. In case the fair value is not determinable, the

value in use becomes the recoverable value and in case of the disposable assets, the recoverable

value is the fair value less the cost of disposal. The determination of fair value has to be done in

accordance with the IFRS 13 which is on Fair value measurement. The cost of disposal includes

only the direct costs related to it. The other factor being value in use is detrmined through a

number of variables like the time value of money, the expected future cash flow generation

ability of the asset, the time lag in between the receipt of the amount from the use of the asset,

4 | P a g e

5

and many more including accounting for uncertainity, if any. (Fay & Negangard, 2017) Assets

cash flow generation projections should always be made on the most recent or current data and

not of the past years and in case the time period is more than 5 years, extrapolation can be used

as per the IAS. The projection should be exclusive of any future expenditure which is expected

to be incurred on the asset. The interest rate to be used in the calculation of the value in use

should be pre tax rate such that it includes the effect of time value of money and the market

conditions. It should be the rate which the investors would have asked for in return on investing

in the company or any specific asset. Further, the discount rate used should be the one which

would have borrowed from the market in order to buy a particular asset.

From all the above inputs, impairment loss to be reversed can be calculated and then

credited to the profit and loss account of the entity. It would generally be done in case the

recoverable value is more than the carrying value of the asset and we can utilise the asset and

derive the future economic benefit from the asset which was already impaired earlier (Meroño-

Cerdán, et al., 2017) Based on all this, the future depreciation amount also needs to be adjusted

on the prospective basis.

When we talk about CGU or a cash generating unit, it is not the single asset but the

smallest possible group of assets or a class of asset from which revenue for the business can be

generated and which has an identity which is independent of the other group or class of assets.

The calculation for impairment of goodwill is completely different as the goodwill of the entity

is generally allocated to all the CGUs proporatioately and then each CGU is assessed separately

for impairment. The amount is first decreaed to the extent of the goodwill and then the amount is

decreased form the other assets. The carrying amount of the assets should be be reduced below

zero. The amount of goodwill once impaired cannot be reversed in any circumstance whatsoever.

While reversal of impairement loss, which again needs to be done on periodical basis

whenever the positive internal or external factors are available, is to be seen alongwith the

impairment. (Mahapatra, et al., 2017) However, there are a few exceptions to be followed while

accounting for reversal of impairment loss like goodwill impairment non reversal, the amount of

reversal should not exceed the amount of impairment in any case, reversal of the the impairment

loss is to be recognised in the profit and loss account unless it relates to the revalued asset, the

amount of depreciation also needs to be adjusted for the future periods, etc.

5 | P a g e

and many more including accounting for uncertainity, if any. (Fay & Negangard, 2017) Assets

cash flow generation projections should always be made on the most recent or current data and

not of the past years and in case the time period is more than 5 years, extrapolation can be used

as per the IAS. The projection should be exclusive of any future expenditure which is expected

to be incurred on the asset. The interest rate to be used in the calculation of the value in use

should be pre tax rate such that it includes the effect of time value of money and the market

conditions. It should be the rate which the investors would have asked for in return on investing

in the company or any specific asset. Further, the discount rate used should be the one which

would have borrowed from the market in order to buy a particular asset.

From all the above inputs, impairment loss to be reversed can be calculated and then

credited to the profit and loss account of the entity. It would generally be done in case the

recoverable value is more than the carrying value of the asset and we can utilise the asset and

derive the future economic benefit from the asset which was already impaired earlier (Meroño-

Cerdán, et al., 2017) Based on all this, the future depreciation amount also needs to be adjusted

on the prospective basis.

When we talk about CGU or a cash generating unit, it is not the single asset but the

smallest possible group of assets or a class of asset from which revenue for the business can be

generated and which has an identity which is independent of the other group or class of assets.

The calculation for impairment of goodwill is completely different as the goodwill of the entity

is generally allocated to all the CGUs proporatioately and then each CGU is assessed separately

for impairment. The amount is first decreaed to the extent of the goodwill and then the amount is

decreased form the other assets. The carrying amount of the assets should be be reduced below

zero. The amount of goodwill once impaired cannot be reversed in any circumstance whatsoever.

While reversal of impairement loss, which again needs to be done on periodical basis

whenever the positive internal or external factors are available, is to be seen alongwith the

impairment. (Mahapatra, et al., 2017) However, there are a few exceptions to be followed while

accounting for reversal of impairment loss like goodwill impairment non reversal, the amount of

reversal should not exceed the amount of impairment in any case, reversal of the the impairment

loss is to be recognised in the profit and loss account unless it relates to the revalued asset, the

amount of depreciation also needs to be adjusted for the future periods, etc.

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

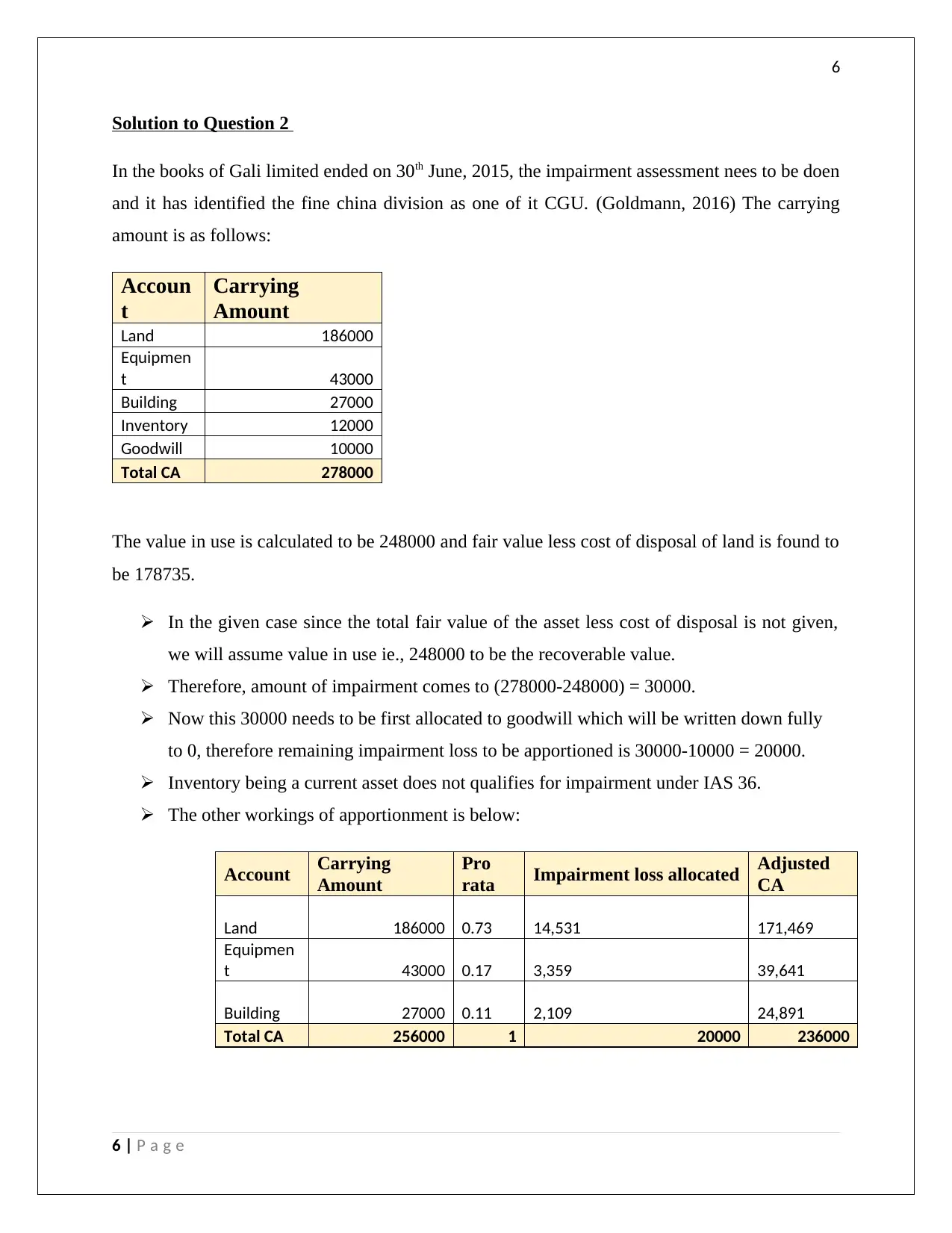

Solution to Question 2

In the books of Gali limited ended on 30th June, 2015, the impairment assessment nees to be doen

and it has identified the fine china division as one of it CGU. (Goldmann, 2016) The carrying

amount is as follows:

Accoun

t

Carrying

Amount

Land 186000

Equipmen

t 43000

Building 27000

Inventory 12000

Goodwill 10000

Total CA 278000

The value in use is calculated to be 248000 and fair value less cost of disposal of land is found to

be 178735.

In the given case since the total fair value of the asset less cost of disposal is not given,

we will assume value in use ie., 248000 to be the recoverable value.

Therefore, amount of impairment comes to (278000-248000) = 30000.

Now this 30000 needs to be first allocated to goodwill which will be written down fully

to 0, therefore remaining impairment loss to be apportioned is 30000-10000 = 20000.

Inventory being a current asset does not qualifies for impairment under IAS 36.

The other workings of apportionment is below:

Account Carrying

Amount

Pro

rata Impairment loss allocated Adjusted

CA

Land 186000 0.73 14,531 171,469

Equipmen

t 43000 0.17 3,359 39,641

Building 27000 0.11 2,109 24,891

Total CA 256000 1 20000 236000

6 | P a g e

Solution to Question 2

In the books of Gali limited ended on 30th June, 2015, the impairment assessment nees to be doen

and it has identified the fine china division as one of it CGU. (Goldmann, 2016) The carrying

amount is as follows:

Accoun

t

Carrying

Amount

Land 186000

Equipmen

t 43000

Building 27000

Inventory 12000

Goodwill 10000

Total CA 278000

The value in use is calculated to be 248000 and fair value less cost of disposal of land is found to

be 178735.

In the given case since the total fair value of the asset less cost of disposal is not given,

we will assume value in use ie., 248000 to be the recoverable value.

Therefore, amount of impairment comes to (278000-248000) = 30000.

Now this 30000 needs to be first allocated to goodwill which will be written down fully

to 0, therefore remaining impairment loss to be apportioned is 30000-10000 = 20000.

Inventory being a current asset does not qualifies for impairment under IAS 36.

The other workings of apportionment is below:

Account Carrying

Amount

Pro

rata Impairment loss allocated Adjusted

CA

Land 186000 0.73 14,531 171,469

Equipmen

t 43000 0.17 3,359 39,641

Building 27000 0.11 2,109 24,891

Total CA 256000 1 20000 236000

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

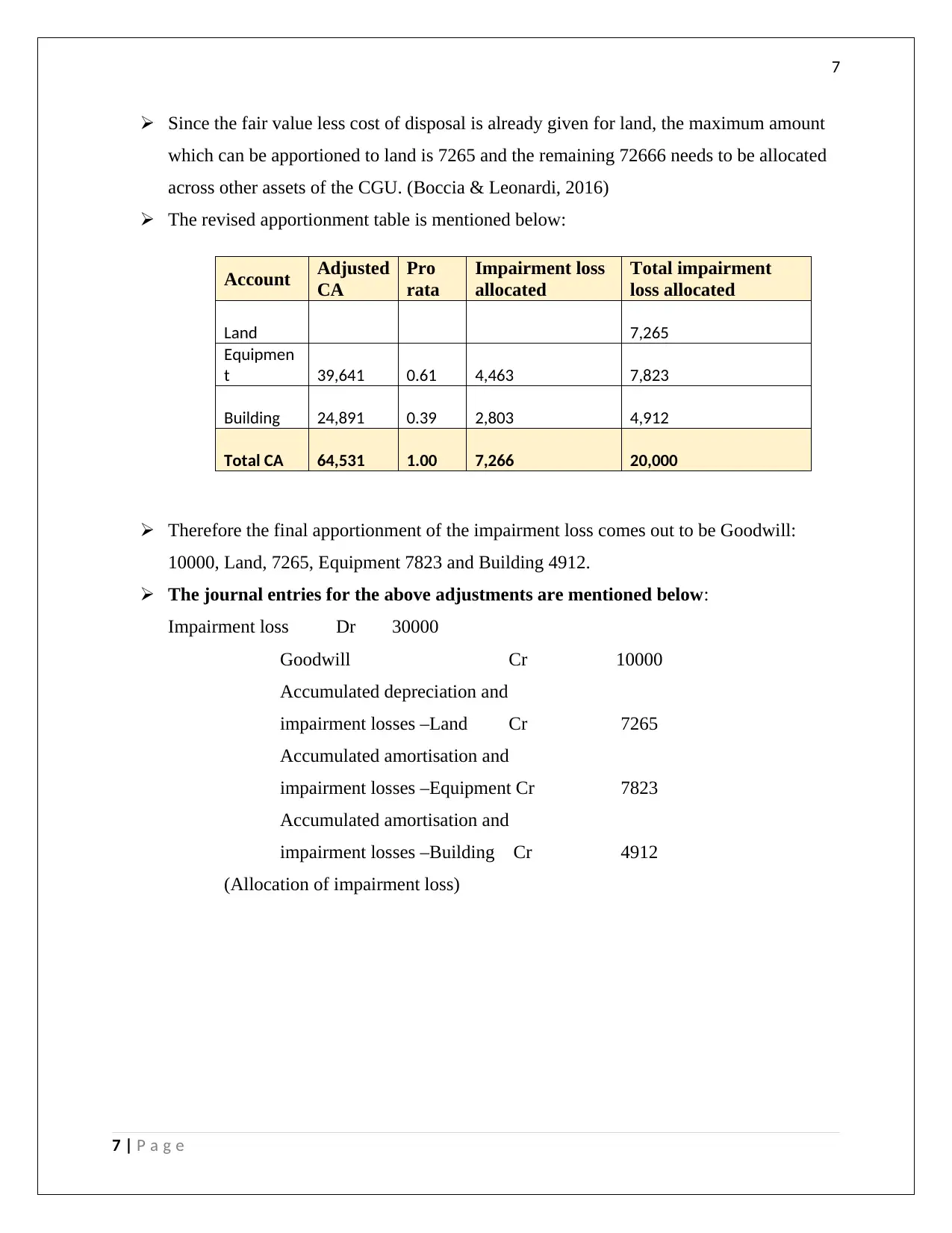

Since the fair value less cost of disposal is already given for land, the maximum amount

which can be apportioned to land is 7265 and the remaining 72666 needs to be allocated

across other assets of the CGU. (Boccia & Leonardi, 2016)

The revised apportionment table is mentioned below:

Account Adjusted

CA

Pro

rata

Impairment loss

allocated

Total impairment

loss allocated

Land 7,265

Equipmen

t 39,641 0.61 4,463 7,823

Building 24,891 0.39 2,803 4,912

Total CA 64,531 1.00 7,266 20,000

Therefore the final apportionment of the impairment loss comes out to be Goodwill:

10000, Land, 7265, Equipment 7823 and Building 4912.

The journal entries for the above adjustments are mentioned below:

Impairment loss Dr 30000

Goodwill Cr 10000

Accumulated depreciation and

impairment losses –Land Cr 7265

Accumulated amortisation and

impairment losses –Equipment Cr 7823

Accumulated amortisation and

impairment losses –Building Cr 4912

(Allocation of impairment loss)

7 | P a g e

Since the fair value less cost of disposal is already given for land, the maximum amount

which can be apportioned to land is 7265 and the remaining 72666 needs to be allocated

across other assets of the CGU. (Boccia & Leonardi, 2016)

The revised apportionment table is mentioned below:

Account Adjusted

CA

Pro

rata

Impairment loss

allocated

Total impairment

loss allocated

Land 7,265

Equipmen

t 39,641 0.61 4,463 7,823

Building 24,891 0.39 2,803 4,912

Total CA 64,531 1.00 7,266 20,000

Therefore the final apportionment of the impairment loss comes out to be Goodwill:

10000, Land, 7265, Equipment 7823 and Building 4912.

The journal entries for the above adjustments are mentioned below:

Impairment loss Dr 30000

Goodwill Cr 10000

Accumulated depreciation and

impairment losses –Land Cr 7265

Accumulated amortisation and

impairment losses –Equipment Cr 7823

Accumulated amortisation and

impairment losses –Building Cr 4912

(Allocation of impairment loss)

7 | P a g e

8

Conclusion and disclosures

Impairment is a very broad and judgementall topic which depends on the management

estrimate and judgements and how the situation is perceived given the cicrcumstances. (kabir, et

al., 2017) The valuation of the asset can vary from one value to another based on the

assumptions being considered. It has been a matter of discussion to provide the supporting facts

and figures on the impairment assessment and to disclose the transparency in the calculation.

Also, how the selection of cash generating unit is being done is based on an assumption and

needs to be justified and therefore the following disclosure become necessary in the financial

statements:

1. The basis of impairment, the loss recognised and reversed in P&L account

2. Impairment loss being recognised or reversed on the revalued assets in OCI.

3. The amount of reversal

4. The internal and external factors leading to it

5. The cash gereating unit and the classes of asset in it.

6. Other critical circumstances and events.

8 | P a g e

Conclusion and disclosures

Impairment is a very broad and judgementall topic which depends on the management

estrimate and judgements and how the situation is perceived given the cicrcumstances. (kabir, et

al., 2017) The valuation of the asset can vary from one value to another based on the

assumptions being considered. It has been a matter of discussion to provide the supporting facts

and figures on the impairment assessment and to disclose the transparency in the calculation.

Also, how the selection of cash generating unit is being done is based on an assumption and

needs to be justified and therefore the following disclosure become necessary in the financial

statements:

1. The basis of impairment, the loss recognised and reversed in P&L account

2. Impairment loss being recognised or reversed on the revalued assets in OCI.

3. The amount of reversal

4. The internal and external factors leading to it

5. The cash gereating unit and the classes of asset in it.

6. Other critical circumstances and events.

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

References

Boccia, F. & Leonardi, R., 2016. The Challenge of the Digital Economy. Markets, Taxation and

Appropriate Economic Models, pp. 1-16.

Buchanan, B., Cao, C., Liljeblom, E. & Weihrich, S., 2017. Taxation and Dividend Policy: The Muting Effect

of Agency Issues and Shareholder Conflicts. Journal of Corporate Finance, Volume 42, pp. 179-197.

Das, P., 2017. Financing Pattern and Utilization of Fixed Assets - A Study. Asian Journal of Social Science

Studies, 2(2), pp. 10-17.

Fay, R. & Negangard, E., 2017. Manual journal entry testing : Data analytics and the risk of fraud. Journal

of Accounting Education, Volume 38, pp. 37-49.

Goldmann, K., 2016. Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, Volume 4, pp. 103-112.

kabir, H., Rahman, A. & Su, L., 2017. The Association between Goodwill Impairment Loss and Goodwill

Impairment Test-Related Disclosures in Australia. 8th Conference on Financial Markets and Corporate

Governance (FMCG) 2017, pp. 1-32.

Mahapatra, S., Levental, S. & Narasimhan, R., 2017. Market price uncertainty, risk aversion and

procurement: Combining contracts and open market sourcing alternatives. International Journal of

Production Economics, pp. 34-51.

Meroño-Cerdán, A., Lopez-Nicolas, C. & Molina-Castillo, F., 2017. Risk aversion, innovation and

performance in family firms. Economics of Innovation and new technology, pp. 1-15.

9 | P a g e

References

Boccia, F. & Leonardi, R., 2016. The Challenge of the Digital Economy. Markets, Taxation and

Appropriate Economic Models, pp. 1-16.

Buchanan, B., Cao, C., Liljeblom, E. & Weihrich, S., 2017. Taxation and Dividend Policy: The Muting Effect

of Agency Issues and Shareholder Conflicts. Journal of Corporate Finance, Volume 42, pp. 179-197.

Das, P., 2017. Financing Pattern and Utilization of Fixed Assets - A Study. Asian Journal of Social Science

Studies, 2(2), pp. 10-17.

Fay, R. & Negangard, E., 2017. Manual journal entry testing : Data analytics and the risk of fraud. Journal

of Accounting Education, Volume 38, pp. 37-49.

Goldmann, K., 2016. Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, Volume 4, pp. 103-112.

kabir, H., Rahman, A. & Su, L., 2017. The Association between Goodwill Impairment Loss and Goodwill

Impairment Test-Related Disclosures in Australia. 8th Conference on Financial Markets and Corporate

Governance (FMCG) 2017, pp. 1-32.

Mahapatra, S., Levental, S. & Narasimhan, R., 2017. Market price uncertainty, risk aversion and

procurement: Combining contracts and open market sourcing alternatives. International Journal of

Production Economics, pp. 34-51.

Meroño-Cerdán, A., Lopez-Nicolas, C. & Molina-Castillo, F., 2017. Risk aversion, innovation and

performance in family firms. Economics of Innovation and new technology, pp. 1-15.

9 | P a g e

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.