Corporate Accounting and Financial Reporting - Impairment Assessment

VerifiedAdded on 2020/05/28

|8

|1500

|50

Report

AI Summary

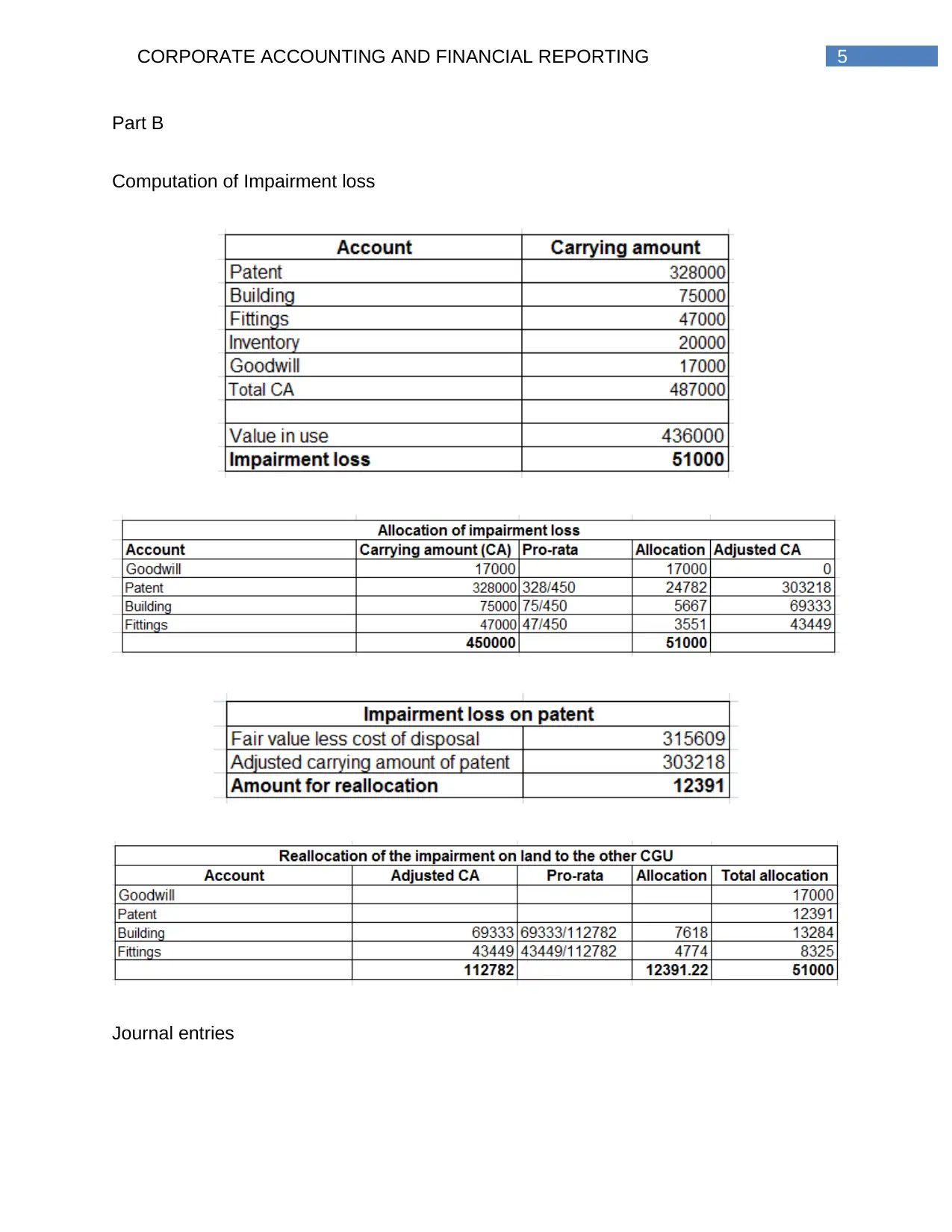

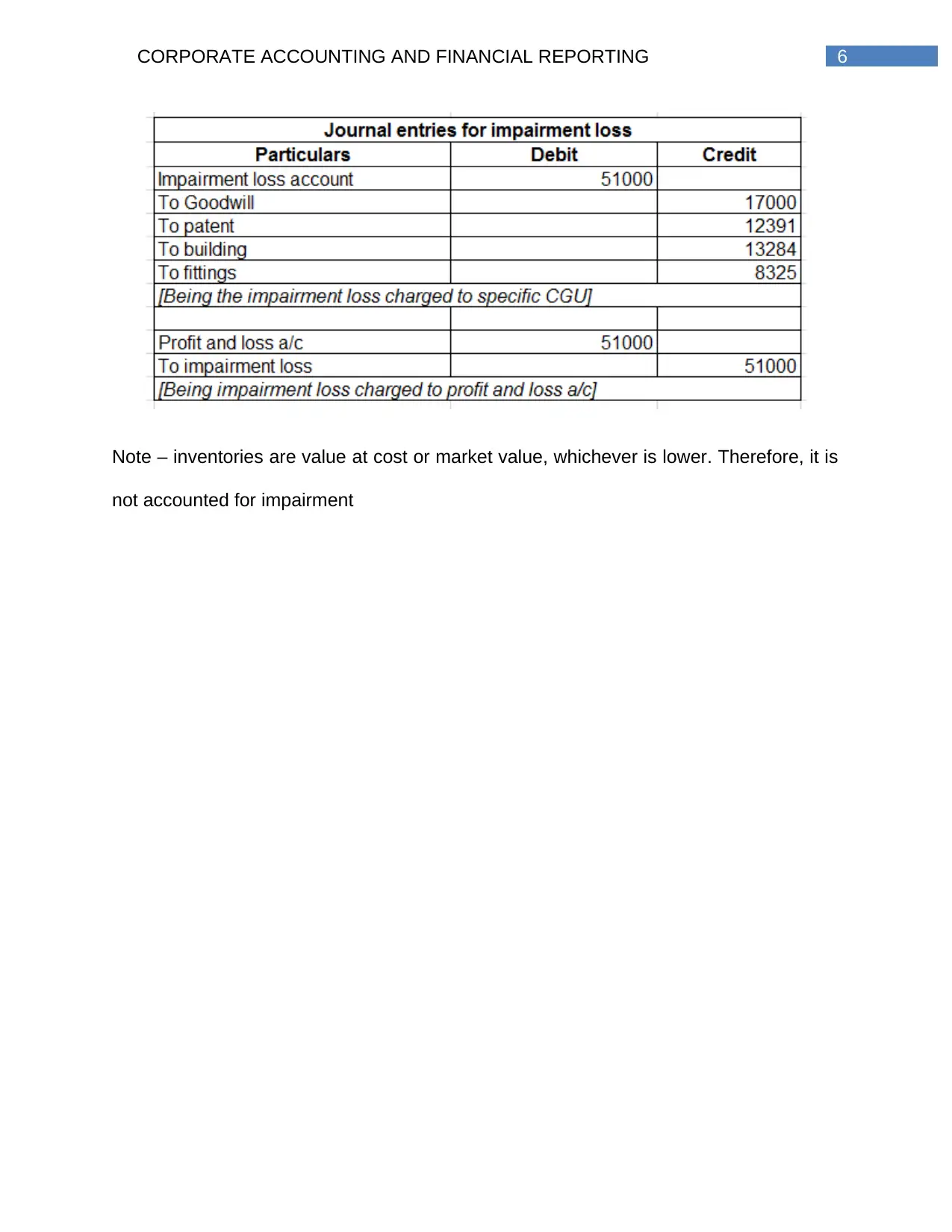

This report delves into the intricacies of corporate accounting and financial reporting, with a specific emphasis on asset impairment. It meticulously explains the concepts of recoverable value, value in use, and fair value less cost of disposal, as defined by AASB 136. The report outlines the methods for measuring these values and determining whether an asset is impaired. It includes a discussion on impairment tests for intangible assets, the estimation of fair value, and the computation of impairment loss, offering a comprehensive understanding of the accounting treatment of impaired assets. The report also covers the journal entries for impairment losses, providing a practical application of the theoretical concepts discussed. The references provided offer additional resources for further study on the topic.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.