Analysis of Corporate Accounting and Reporting Principles

VerifiedAdded on 2020/05/28

|9

|1483

|34

Report

AI Summary

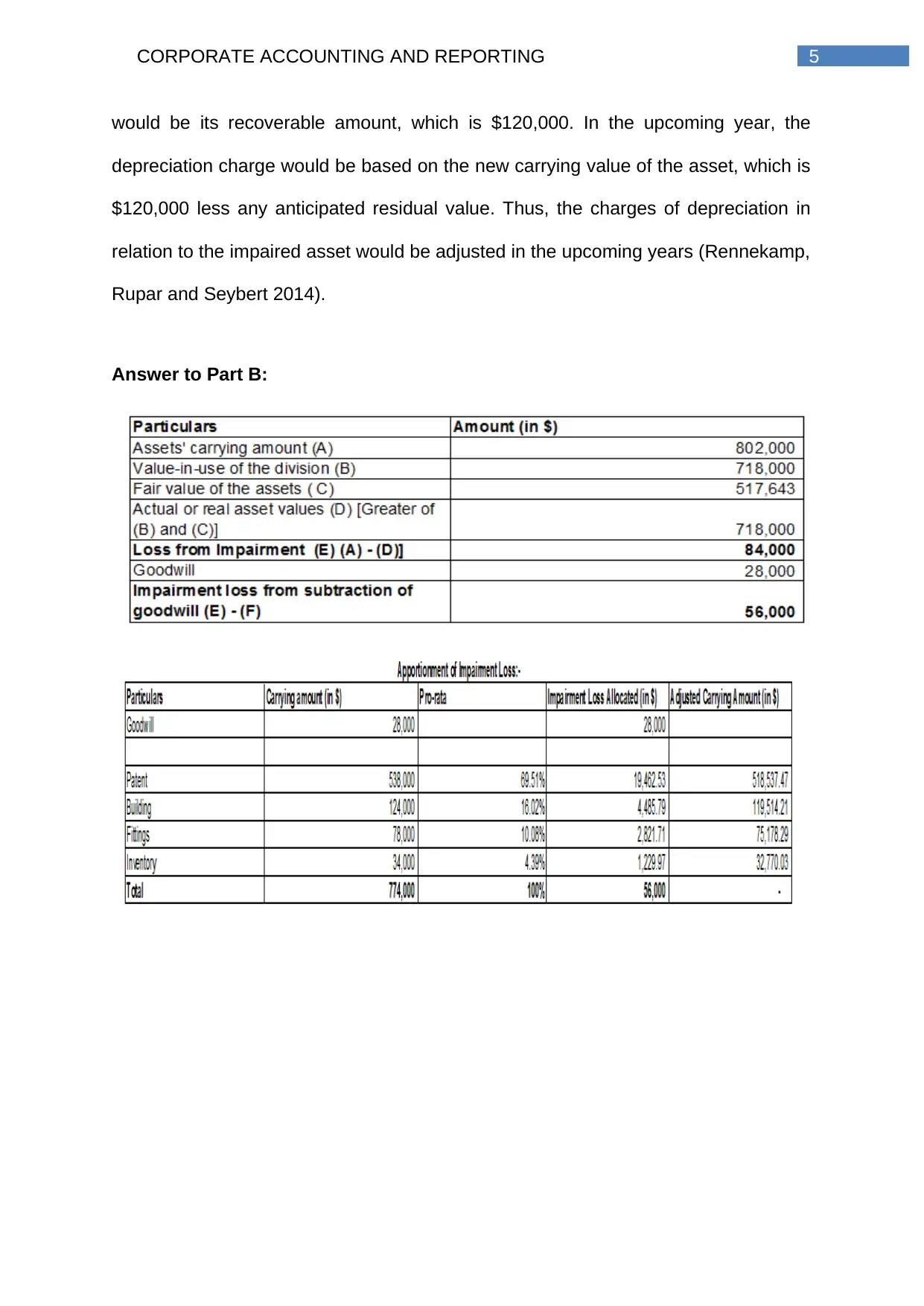

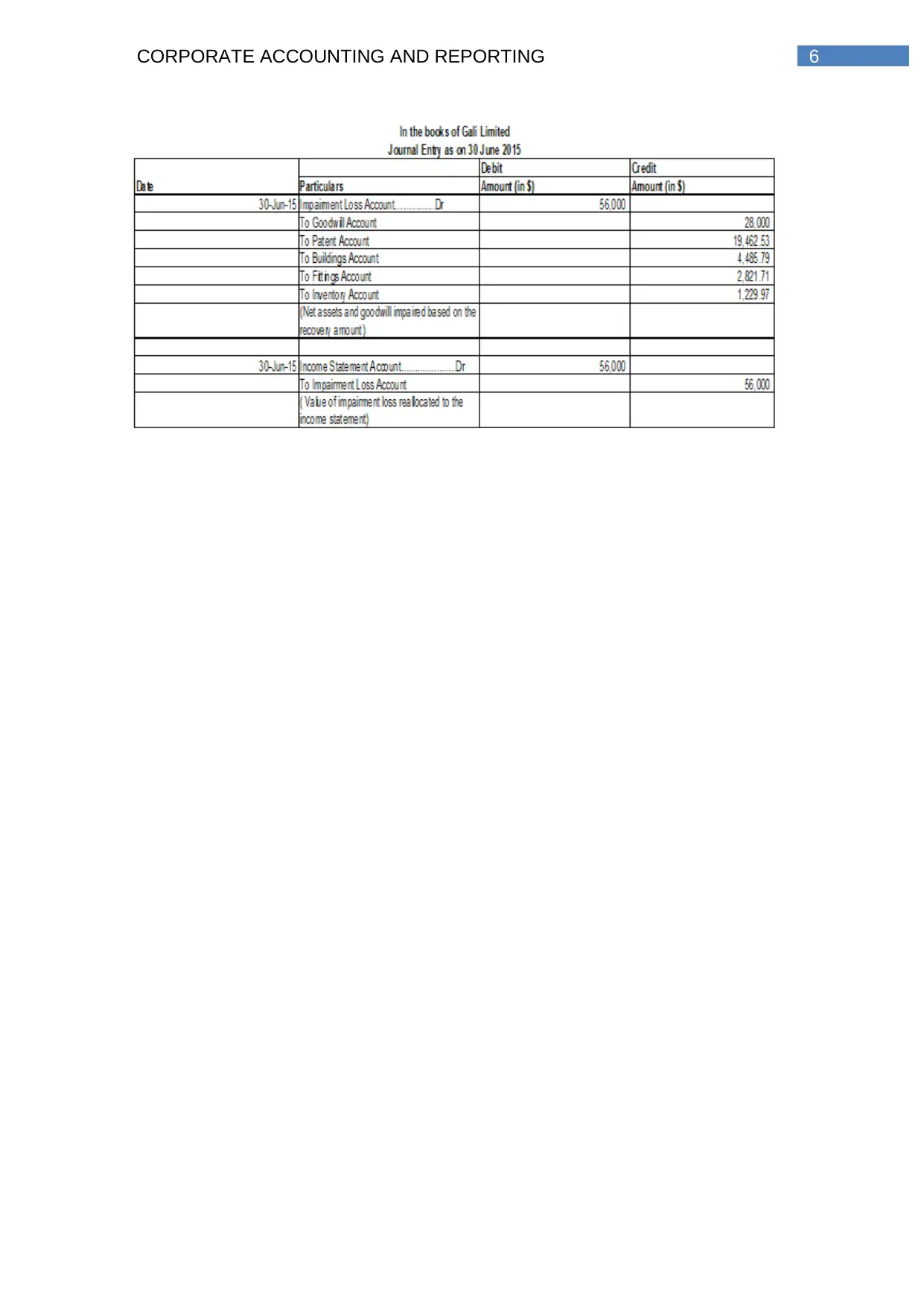

This report provides an in-depth analysis of corporate accounting and reporting, focusing on the concept of impairment loss and its implications on asset valuation. It explores the factors leading to asset impairment, the process of determining recoverable amounts, and the recognition of impairment losses in financial statements. The report references key accounting standards like AASB 136, detailing the requirements for measuring and recognizing impairment losses for individual assets. It includes examples to illustrate the practical application of these principles, such as the impact of asset damage on depreciation charges and revaluation surpluses. The report also discusses the accounting treatment of impairment losses for re-valued assets and non-revalued assets, and the adjustments required in subsequent periods. Finally, the report provides a comprehensive overview of corporate accounting principles related to asset impairment and valuation. This report is available on Desklib, a platform that provides students with AI-based study tools and resources, including past papers and solved assignments.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.