Corporate Accounting and Reporting: Impairment Loss Analysis, Finance

VerifiedAdded on 2023/06/06

|6

|1457

|361

Homework Assignment

AI Summary

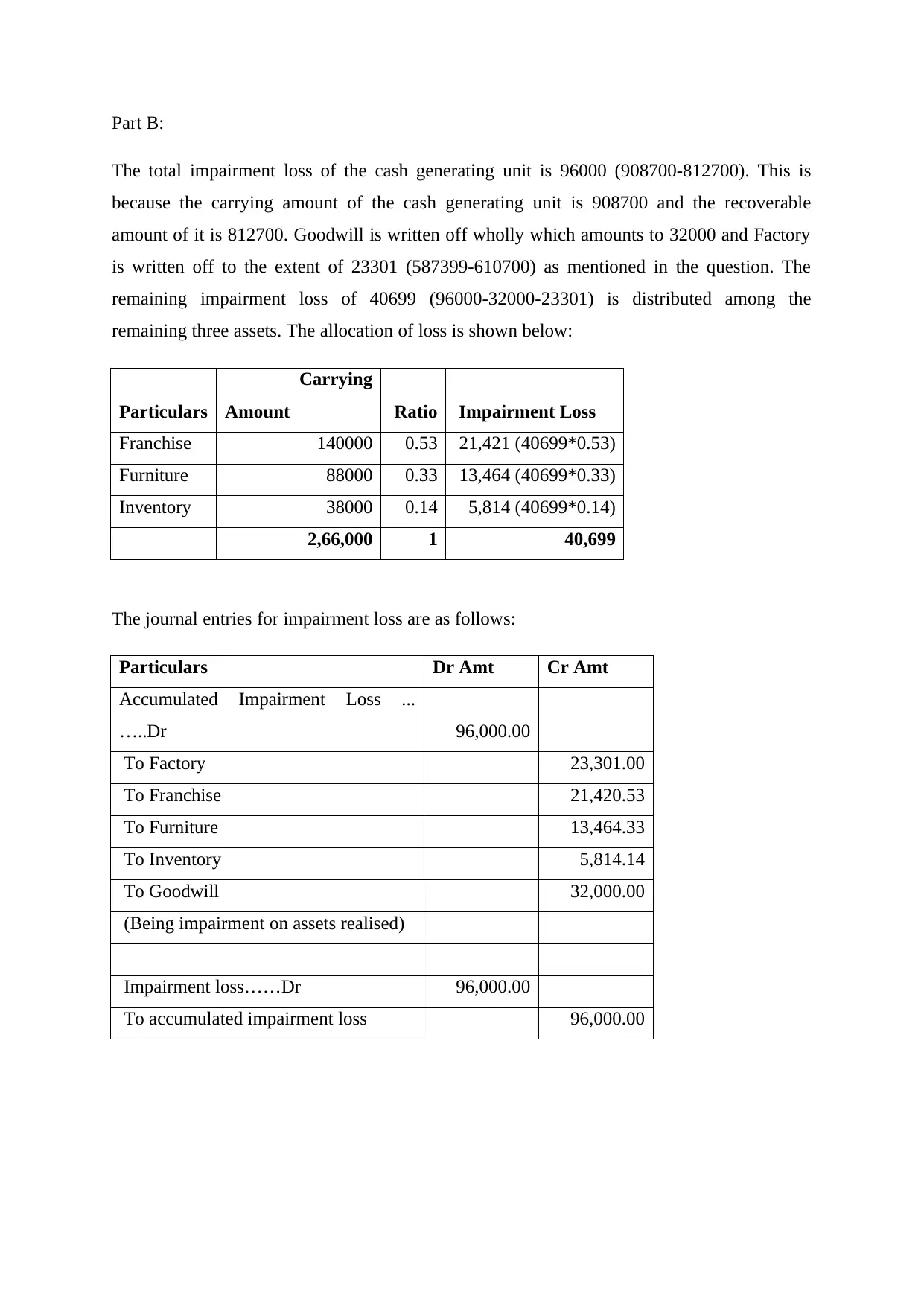

This document presents a comprehensive solution to a corporate accounting assignment focusing on impairment analysis and financial reporting. The assignment addresses the basic principles of asset impairment, emphasizing that assets should not be recorded above their recoverable amount, which is the higher of value in use and fair value less costs. It details the comparison between carrying amount and recoverable amount, the calculation and treatment of impairment loss, and the specific handling of goodwill and intangible assets. The solution includes a breakdown of impairment indicators, both external and internal, and the disclosure requirements for companies. Part B of the solution provides a practical application of the concepts, calculating the total impairment loss for a cash generating unit, allocating the loss among various assets including goodwill, and providing the corresponding journal entries. The document references relevant accounting literature and emphasizes the importance of professional knowledge and skills in business forecasting and modeling within the finance department.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.