Corporate Accounting: Integrated Reporting Analysis Report

VerifiedAdded on 2021/06/17

|12

|2808

|96

Report

AI Summary

This report provides a comprehensive overview of integrated reporting (IR), examining its core concepts, objectives, and the framework established by the International Integrated Reporting Council (IIRC). The report delves into the benefits of IR, such as enhanced management insights, improved stakeholder relations, and increased employee engagement, supported by findings from ACCA and IFAC reports. It also explores the limitations, including difficulties in merging traditional annual reports, complexities in understanding the concept, lack of clarity, challenges in managing high-volume data, and issues related to assurance. The report concludes by emphasizing the importance of addressing these limitations to successfully implement IR and leverage its advantages for improved corporate performance and value creation. The report highlights the importance of integrated thinking and the value creation process for all sizes of organizations. Furthermore, the report also addresses the importance of stakeholders, risks and opportunities associated with the business organization.

RUNNING HEAD: CORPORATE ACCOUNTING

Integrated reporting

Integrated reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate accounting 1

Abstract

This report reviews the benefits and limitations of integrated reports prepared by the

organization. These reports covers both financial and non-financial aspects of an

organization. In the first section of report, a brief introduction of IR is been given which

describes the concept of integrated reporting. This section provides the information about the

needs and objectives of IR in a nutshell.

The second section deals with the benefits of IR to the companies. It is concerned with the

several advantages available to the organization who has applied integrated reporting in their

framework. Such as, IR provides greater insights to the management and make the thinking

integrated. Employee engagement and stakeholder’s relation has also improved due to this.

The third part of the report throw some lights on limitations of integrated reporting practices.

It highlights some points such as difficulty in merging the annual reports, understanding the

concept of IR, lack of clarity and complexity, issues related to dealing with high volume data

and many more. All such limitations are explained in this section.

The last part of the report includes a conclusion that contains the overall outcome of the

report. It suggested that there are many benefits of IR as well as the same has some

limitations also. In order to eliminate those drawbacks, proper steps should be taken by the

organization so that the implementation of integrated reporting can become successful.

Abstract

This report reviews the benefits and limitations of integrated reports prepared by the

organization. These reports covers both financial and non-financial aspects of an

organization. In the first section of report, a brief introduction of IR is been given which

describes the concept of integrated reporting. This section provides the information about the

needs and objectives of IR in a nutshell.

The second section deals with the benefits of IR to the companies. It is concerned with the

several advantages available to the organization who has applied integrated reporting in their

framework. Such as, IR provides greater insights to the management and make the thinking

integrated. Employee engagement and stakeholder’s relation has also improved due to this.

The third part of the report throw some lights on limitations of integrated reporting practices.

It highlights some points such as difficulty in merging the annual reports, understanding the

concept of IR, lack of clarity and complexity, issues related to dealing with high volume data

and many more. All such limitations are explained in this section.

The last part of the report includes a conclusion that contains the overall outcome of the

report. It suggested that there are many benefits of IR as well as the same has some

limitations also. In order to eliminate those drawbacks, proper steps should be taken by the

organization so that the implementation of integrated reporting can become successful.

Corporate accounting 2

Contents

Introduction...........................................................................................................................................3

Benefits of integrated reporting.............................................................................................................3

Limitations of Integrated Reporting.......................................................................................................6

Conclusion.............................................................................................................................................9

References...........................................................................................................................................10

Contents

Introduction...........................................................................................................................................3

Benefits of integrated reporting.............................................................................................................3

Limitations of Integrated Reporting.......................................................................................................6

Conclusion.............................................................................................................................................9

References...........................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate accounting 3

Introduction

In corporate terms, the process of representing company’s performance both in financial and

other relevant factors is known as integrated reporting. An integrated report is a brief

communication of company’s strategies, performances and governance employed or creating

short, medium and long term values within the organization (Ey.com. 2018).

The International Integrated Reporting Council (IIRC) is responsible for establishing this

framework. The council aims at bringing integrity in financial reporting and promoting value

creation in the enterprise. The need for IR arises when corporate reporting fails to reflects the

financial stability and economic sustainability in one go. Therefore in order to clearly

communicate the value, integrated reports are been prepared which clearly reflects the short

and long term consequences of the decision making process of the organisation

(Integratedreporting.org. 2018).

However, just like every coin has two faces, preparation of integrated reports also has some

benefits and limitations, which are been discussed below.

Benefits of integrated reporting

According to the report published by Association of Chartered Certified Accountants

(ACCA), there are several benefits of IR which are been enjoyed by the individuals who have

experienced and adopted IR within their organization. The findings of the report are based on

the review of 41 corporate reports. The benefits include making the thinking and management

more integrated, providing more clarity about the issues and performance of business,

enhancing the relations with stakeholders and improves corporate reputation. Furthermore,

the report stated that integrated reporting offer more insights to the management in assessing

the factors that drives the business performance. IR is the most appropriate and efficient

reporting method for both the users and prepares. It also promotes employee engagement.

Introduction

In corporate terms, the process of representing company’s performance both in financial and

other relevant factors is known as integrated reporting. An integrated report is a brief

communication of company’s strategies, performances and governance employed or creating

short, medium and long term values within the organization (Ey.com. 2018).

The International Integrated Reporting Council (IIRC) is responsible for establishing this

framework. The council aims at bringing integrity in financial reporting and promoting value

creation in the enterprise. The need for IR arises when corporate reporting fails to reflects the

financial stability and economic sustainability in one go. Therefore in order to clearly

communicate the value, integrated reports are been prepared which clearly reflects the short

and long term consequences of the decision making process of the organisation

(Integratedreporting.org. 2018).

However, just like every coin has two faces, preparation of integrated reports also has some

benefits and limitations, which are been discussed below.

Benefits of integrated reporting

According to the report published by Association of Chartered Certified Accountants

(ACCA), there are several benefits of IR which are been enjoyed by the individuals who have

experienced and adopted IR within their organization. The findings of the report are based on

the review of 41 corporate reports. The benefits include making the thinking and management

more integrated, providing more clarity about the issues and performance of business,

enhancing the relations with stakeholders and improves corporate reputation. Furthermore,

the report stated that integrated reporting offer more insights to the management in assessing

the factors that drives the business performance. IR is the most appropriate and efficient

reporting method for both the users and prepares. It also promotes employee engagement.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate accounting 4

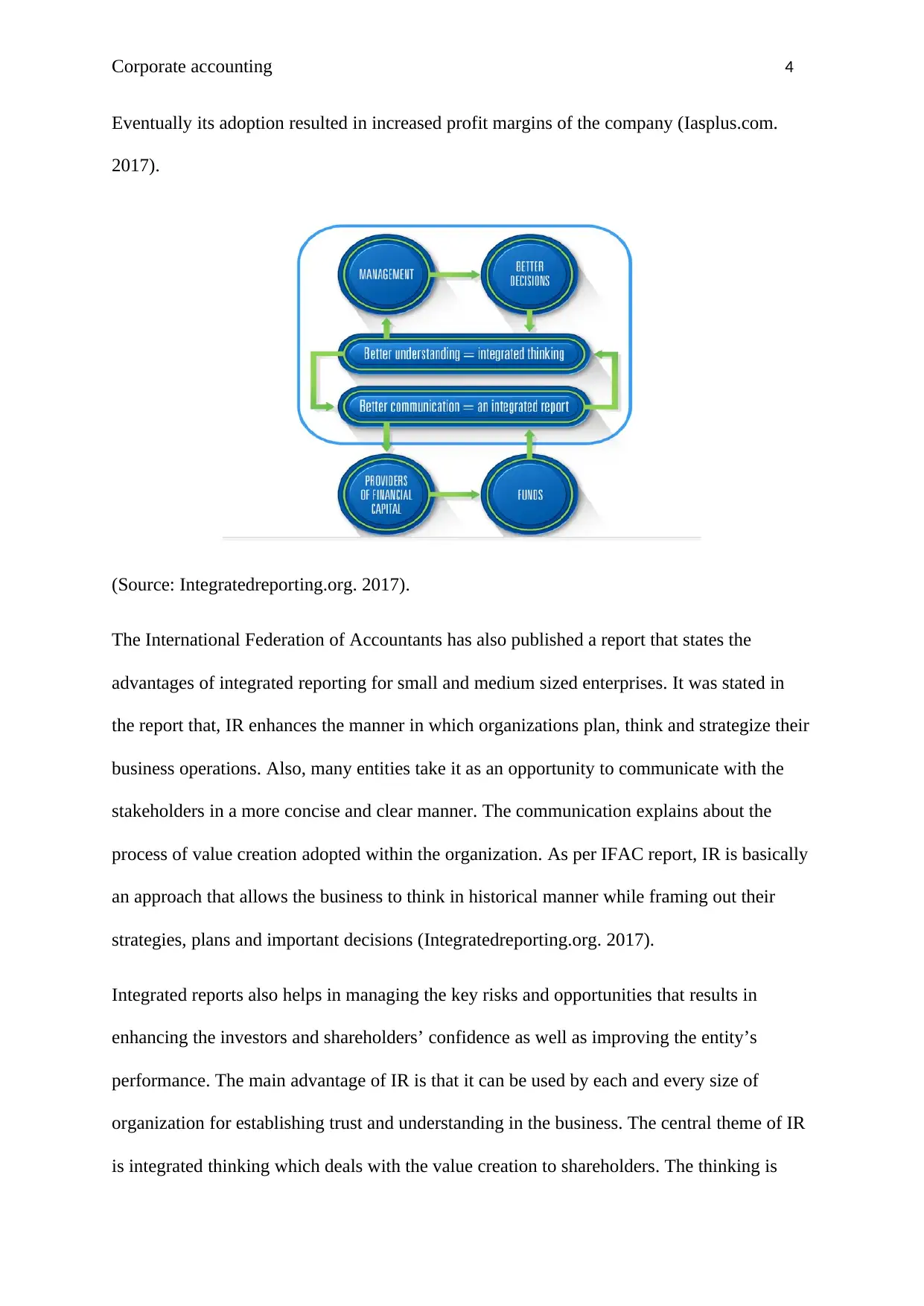

Eventually its adoption resulted in increased profit margins of the company (Iasplus.com.

2017).

(Source: Integratedreporting.org. 2017).

The International Federation of Accountants has also published a report that states the

advantages of integrated reporting for small and medium sized enterprises. It was stated in

the report that, IR enhances the manner in which organizations plan, think and strategize their

business operations. Also, many entities take it as an opportunity to communicate with the

stakeholders in a more concise and clear manner. The communication explains about the

process of value creation adopted within the organization. As per IFAC report, IR is basically

an approach that allows the business to think in historical manner while framing out their

strategies, plans and important decisions (Integratedreporting.org. 2017).

Integrated reports also helps in managing the key risks and opportunities that results in

enhancing the investors and shareholders’ confidence as well as improving the entity’s

performance. The main advantage of IR is that it can be used by each and every size of

organization for establishing trust and understanding in the business. The central theme of IR

is integrated thinking which deals with the value creation to shareholders. The thinking is

Eventually its adoption resulted in increased profit margins of the company (Iasplus.com.

2017).

(Source: Integratedreporting.org. 2017).

The International Federation of Accountants has also published a report that states the

advantages of integrated reporting for small and medium sized enterprises. It was stated in

the report that, IR enhances the manner in which organizations plan, think and strategize their

business operations. Also, many entities take it as an opportunity to communicate with the

stakeholders in a more concise and clear manner. The communication explains about the

process of value creation adopted within the organization. As per IFAC report, IR is basically

an approach that allows the business to think in historical manner while framing out their

strategies, plans and important decisions (Integratedreporting.org. 2017).

Integrated reports also helps in managing the key risks and opportunities that results in

enhancing the investors and shareholders’ confidence as well as improving the entity’s

performance. The main advantage of IR is that it can be used by each and every size of

organization for establishing trust and understanding in the business. The central theme of IR

is integrated thinking which deals with the value creation to shareholders. The thinking is

Corporate accounting 5

based on the fact that there should be proper delegation of authority, roles and responsibilities

between people and departments so that a collective and better understating of business’s key

elements can be developed (Iasplus.com. 2018).

However, in order to improve the internal management process. IR has some significant

benefits such as establishment of high level of trust and credibility with the customers,

suppliers, society and other stakeholders. This can be very useful for the non-profit

organizations as they are constantly searching for commercial partners. IR maximizes the

ability to transfer and sell the business by providing a greater value for it. Based on a good

strategy and well defined plan, business can secure its finances at reasonable cost

(Integratedreporting.org. 2017).

Talking about SMEs, through IR they can easily create a better understanding of the factors

that measures its capability of value generation over short and long term. It also improves the

business planning and leads to the overall development of SMEs. It helps in better

understanding, improved communication, generating multiple capitals and enhanced decision

making process. Also it allows SMEs to summarize their reports and create a strategic focus

that will lead to future growth and development (Integratedreporting.org. 2017).

It was observed that many multinational companies has faced problems related to the

information disclosure in their financial reports. Such as there were inconsistent definitions of

some particular terms such as full-time equivalent, sick days and many others. The data

represented does not reflect the true picture of the company and thus making it difficult for

the financial executives to deal with the risk and uncertainties. However, in order to deal with

such situations, framework of Integrated reporting was introduced which was accepted and

adopted by several organizations operating at large and small scale (Pwc.blogs.com. 2011).

based on the fact that there should be proper delegation of authority, roles and responsibilities

between people and departments so that a collective and better understating of business’s key

elements can be developed (Iasplus.com. 2018).

However, in order to improve the internal management process. IR has some significant

benefits such as establishment of high level of trust and credibility with the customers,

suppliers, society and other stakeholders. This can be very useful for the non-profit

organizations as they are constantly searching for commercial partners. IR maximizes the

ability to transfer and sell the business by providing a greater value for it. Based on a good

strategy and well defined plan, business can secure its finances at reasonable cost

(Integratedreporting.org. 2017).

Talking about SMEs, through IR they can easily create a better understanding of the factors

that measures its capability of value generation over short and long term. It also improves the

business planning and leads to the overall development of SMEs. It helps in better

understanding, improved communication, generating multiple capitals and enhanced decision

making process. Also it allows SMEs to summarize their reports and create a strategic focus

that will lead to future growth and development (Integratedreporting.org. 2017).

It was observed that many multinational companies has faced problems related to the

information disclosure in their financial reports. Such as there were inconsistent definitions of

some particular terms such as full-time equivalent, sick days and many others. The data

represented does not reflect the true picture of the company and thus making it difficult for

the financial executives to deal with the risk and uncertainties. However, in order to deal with

such situations, framework of Integrated reporting was introduced which was accepted and

adopted by several organizations operating at large and small scale (Pwc.blogs.com. 2011).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate accounting 6

The main advantage of IR is that it gives a complete view of the data which is relevant to the

companies as well as it value creation strategies (Adams, 2017). According to the report by

Eccles and Krzus, IR approach stimulates a wider standpoint of the data which is necessary

for the company’s goals and decisions. As a result of which, financial executives can easily

create value and enhances its corporate processes (Eccles and Krzus, 2014). The

comprehensive approach of integrated reporting yield many advantages such as bringing

greater transparency in the information, improving short term and long term analysis. It

makes the review process more automated and streamlined by eliminating the manual errors.

Furthermore, IR makes the information more relevant and useful for the company as well as

for its shareholders. It provides a clear disclosure on the concepts suggested by IIRC and

World Intellectual.

Overall, it can be said that the reports prepared through integrated reporting approach helps in

increasing the overall performance of the business. It clearly lay down the process of creating

value, both internally and externally and also the measures to gain the trust of the

stakeholders. Along with this, IR discloses the important or key risk associated with the

business organization as well as the opportunities related to it. This enables the management

and investors to determine or measure the short, medium and long term impact of such risk

on the organization.

Limitations of Integrated Reporting

However, despite of having several benefits IR also has some disadvantages. One of the key

challenges faced by the organizations while adopting IR in their financial reporting practices

is that bring changes in the traditional annual report. The problems was related to

modification of a report which was focused on key financial areas and disclosures, to a

broader one that tells each and everything about the value creation process of the company.

The main advantage of IR is that it gives a complete view of the data which is relevant to the

companies as well as it value creation strategies (Adams, 2017). According to the report by

Eccles and Krzus, IR approach stimulates a wider standpoint of the data which is necessary

for the company’s goals and decisions. As a result of which, financial executives can easily

create value and enhances its corporate processes (Eccles and Krzus, 2014). The

comprehensive approach of integrated reporting yield many advantages such as bringing

greater transparency in the information, improving short term and long term analysis. It

makes the review process more automated and streamlined by eliminating the manual errors.

Furthermore, IR makes the information more relevant and useful for the company as well as

for its shareholders. It provides a clear disclosure on the concepts suggested by IIRC and

World Intellectual.

Overall, it can be said that the reports prepared through integrated reporting approach helps in

increasing the overall performance of the business. It clearly lay down the process of creating

value, both internally and externally and also the measures to gain the trust of the

stakeholders. Along with this, IR discloses the important or key risk associated with the

business organization as well as the opportunities related to it. This enables the management

and investors to determine or measure the short, medium and long term impact of such risk

on the organization.

Limitations of Integrated Reporting

However, despite of having several benefits IR also has some disadvantages. One of the key

challenges faced by the organizations while adopting IR in their financial reporting practices

is that bring changes in the traditional annual report. The problems was related to

modification of a report which was focused on key financial areas and disclosures, to a

broader one that tells each and everything about the value creation process of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate accounting 7

Generally, traditional annual reports are of 1000 pages which involves both the relevant and

irrelevant information. Reports prepared on the basis of integrated reporting approach are

concise in nature and reflects only the relevant and useful information. It anyhow reduces the

quantity of data and enhance the understandability of company’s goals and strategies. The

unique features of IR related to the structure of report has confused many entities on how to

structure and prepare integrated reports.

The Association of Charted Certified Accountant has carried out a research based on the

challenges to assuring integrated reporting. The research interviewed a Big Four audit partner

and the findings shows that although the assurance of IR can add value by improving the

credibility of the report and helps the board of directors in monitoring and reviewing the

functions, but there are number of technical issues which makes it difficult to assure the

entire report. These issues include difficulty in developing appropriate base for assuring the

IR, traditional audit team has limited skills and inadequacy in client’s records. Along with

this, there are inappropriate systems and controls.

As result of which, only some part of the integrated reporting are exposed to assurance

engagement, which includes only realistic disclosures without any evaluation. Moreover, in

order to cope up with this problem, a process based audit was suggested. But the idea failed

due to the inappropriate documentation of systems and controls for many clients. Also the

suitable criteria for evaluating and controlling was not present there. The absence of such

criteria was the major hindrance in the assurance of integrated reports and also in the risk of

auditor liability (Accaglobal.com. 2015).

As per these findings, it can be said that there were many problems regarding the assurance

of integrated reports and also many members of IIRC were also disappointed with this fact as

they believed that assurance must cover the entire report (Accaglobal.com. 2015).

Generally, traditional annual reports are of 1000 pages which involves both the relevant and

irrelevant information. Reports prepared on the basis of integrated reporting approach are

concise in nature and reflects only the relevant and useful information. It anyhow reduces the

quantity of data and enhance the understandability of company’s goals and strategies. The

unique features of IR related to the structure of report has confused many entities on how to

structure and prepare integrated reports.

The Association of Charted Certified Accountant has carried out a research based on the

challenges to assuring integrated reporting. The research interviewed a Big Four audit partner

and the findings shows that although the assurance of IR can add value by improving the

credibility of the report and helps the board of directors in monitoring and reviewing the

functions, but there are number of technical issues which makes it difficult to assure the

entire report. These issues include difficulty in developing appropriate base for assuring the

IR, traditional audit team has limited skills and inadequacy in client’s records. Along with

this, there are inappropriate systems and controls.

As result of which, only some part of the integrated reporting are exposed to assurance

engagement, which includes only realistic disclosures without any evaluation. Moreover, in

order to cope up with this problem, a process based audit was suggested. But the idea failed

due to the inappropriate documentation of systems and controls for many clients. Also the

suitable criteria for evaluating and controlling was not present there. The absence of such

criteria was the major hindrance in the assurance of integrated reports and also in the risk of

auditor liability (Accaglobal.com. 2015).

As per these findings, it can be said that there were many problems regarding the assurance

of integrated reports and also many members of IIRC were also disappointed with this fact as

they believed that assurance must cover the entire report (Accaglobal.com. 2015).

Corporate accounting 8

From another research conducted, it was identified that there are some shortcomings of

integrated reporting. These generally include complexity, lack of clarity and a general lack of

perception that IR will achieve all its objectives are all existed. When the framework was

introduced, there were debates and arguments related to the structure and looks of IR.

Another related problem was lack of accepted standards, which was decided to be overcome

through the framework prepared by IIRC. But still the framework has some gaps and need to

be field tested. One key problems that still exists is the relationship between integrated report

and other report such as sustainability report. This issue may result in duplication of the data

and it is very necessary for IR to figure out a suitable way for complying with other reporting

requirements. According to The Journal of the Global Accounting Alliance one of the

practical challenges faced by the preparers is implanting the process of forming a report in

order to get a balanced view that represents the essence of an organization and the various

forward looking perspectives of it (Gaaaccounting.com. 2014).

In addition to this, the biggest challenge faced was the high volume of information that is

required to be managed within the tight deadlines, specifically for the reporters who has not

prepared sustainability reports. Other problems are related to the contents of report and

simply compiling the annual and sustainability reports is the another major issue as it makes

the report larger. Also if some information is omitted, it may result in a material risk.

Moreover, the matter of sustainability report will be sacrificed because of the financial

content that is regulated and is tended to be preferred more. Merging of both the reports in a

meaningful way is considered to be a complex challenge (Vancity.com. 2005). Initially, IR

was not considered as a part of business process, but when it has become compulsory,

prepares has faced many problems and were also not convinced by the fact that these are been

taken seriously by the investors (Gürtürk, 2017).

From another research conducted, it was identified that there are some shortcomings of

integrated reporting. These generally include complexity, lack of clarity and a general lack of

perception that IR will achieve all its objectives are all existed. When the framework was

introduced, there were debates and arguments related to the structure and looks of IR.

Another related problem was lack of accepted standards, which was decided to be overcome

through the framework prepared by IIRC. But still the framework has some gaps and need to

be field tested. One key problems that still exists is the relationship between integrated report

and other report such as sustainability report. This issue may result in duplication of the data

and it is very necessary for IR to figure out a suitable way for complying with other reporting

requirements. According to The Journal of the Global Accounting Alliance one of the

practical challenges faced by the preparers is implanting the process of forming a report in

order to get a balanced view that represents the essence of an organization and the various

forward looking perspectives of it (Gaaaccounting.com. 2014).

In addition to this, the biggest challenge faced was the high volume of information that is

required to be managed within the tight deadlines, specifically for the reporters who has not

prepared sustainability reports. Other problems are related to the contents of report and

simply compiling the annual and sustainability reports is the another major issue as it makes

the report larger. Also if some information is omitted, it may result in a material risk.

Moreover, the matter of sustainability report will be sacrificed because of the financial

content that is regulated and is tended to be preferred more. Merging of both the reports in a

meaningful way is considered to be a complex challenge (Vancity.com. 2005). Initially, IR

was not considered as a part of business process, but when it has become compulsory,

prepares has faced many problems and were also not convinced by the fact that these are been

taken seriously by the investors (Gürtürk, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate accounting 9

Conclusion

The above report concludes that in order to provide greater insights to the management and

investors, it is very necessary for the organizations to have integrity in their financial

reporting processes. The integrated reports help in creating better understanding of the

financial and non- financial information as well as clearly displays the process of value

creation. However, along with the benefits, IR also has some limitations which are also

discussed in the above report. There are some loop holes in the framework established by

IIRC which created many problems for the preparers, reporters, users and for other related

people (Mio, C. ed. (2016). To cope up with such limitations, several steps are been taken by

IIRC for the same. Overall, it is concluded that now Integrated Reports has become a major

part of the business process and is followed in the internal procedure of the organizations.

Despite of having some disadvantages, it is compulsory for the companies to prepare

integrated reports and reflect all the necessary information and data in it.

Conclusion

The above report concludes that in order to provide greater insights to the management and

investors, it is very necessary for the organizations to have integrity in their financial

reporting processes. The integrated reports help in creating better understanding of the

financial and non- financial information as well as clearly displays the process of value

creation. However, along with the benefits, IR also has some limitations which are also

discussed in the above report. There are some loop holes in the framework established by

IIRC which created many problems for the preparers, reporters, users and for other related

people (Mio, C. ed. (2016). To cope up with such limitations, several steps are been taken by

IIRC for the same. Overall, it is concluded that now Integrated Reports has become a major

part of the business process and is followed in the internal procedure of the organizations.

Despite of having some disadvantages, it is compulsory for the companies to prepare

integrated reports and reflect all the necessary information and data in it.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate accounting 10

References

Accaglobal.com. (2015). The Challenges of Assuring Integrated Reports: Views from the

South African Auditing Community. [Online] Available at:

http://www.accaglobal.com/content/dam/ACCA_Global/Technical/integrate/ea-south-africa-

IR-assurance.pdf [Accessed 6 May 2018].

Adams, C. (2017). Understanding integrated reporting: The concise guide to integrated

thinking and the future of corporate reporting. USA: Routledge.

Eccles, R.G. and Krzus, M.P. (2014). The integrated reporting movement: Meaning,

momentum, motives, and materiality. New Jersey: John Wiley & Sons.

Ey.com. (2018). Integrated reporting Elevating value. [Online] Available at:

http://www.ey.com/Publication/vwLUAssets/EY-Integrated-reporting/$FILE/EY-Integrated-

reporting.pdf [Accessed 6 May 2018].

Gaaaccounting.com. (2014). The Practical Challenges of Integrated Reporting – GAA

Accounting. [Online] Available at: http://www.gaaaccounting.com/the-practical-challenges-

of-integrated-reporting/ [Accessed 6 May 2018].

Gürtürk, A., (2017). Integrated reporting and sustainability-related assurance: Effects,

current practice and future directions. Kassel: kassel university press GmbH.

Iasplus.com. (2017). ACCA report highlights benefits and challenges of adopting Integrated

Reporting. [Online] Available at: https://www.iasplus.com/en-gb/news/2017/04/acca-

integrated-reporting [Accessed 6 May 2018].

Iasplus.com. (2018). Integrated Reporting - A better review. [Online] Available at:

https://www.iasplus.com/en/binary/sustain/1109integratedreportingview.pdf [Accessed 6

May 2018].

References

Accaglobal.com. (2015). The Challenges of Assuring Integrated Reports: Views from the

South African Auditing Community. [Online] Available at:

http://www.accaglobal.com/content/dam/ACCA_Global/Technical/integrate/ea-south-africa-

IR-assurance.pdf [Accessed 6 May 2018].

Adams, C. (2017). Understanding integrated reporting: The concise guide to integrated

thinking and the future of corporate reporting. USA: Routledge.

Eccles, R.G. and Krzus, M.P. (2014). The integrated reporting movement: Meaning,

momentum, motives, and materiality. New Jersey: John Wiley & Sons.

Ey.com. (2018). Integrated reporting Elevating value. [Online] Available at:

http://www.ey.com/Publication/vwLUAssets/EY-Integrated-reporting/$FILE/EY-Integrated-

reporting.pdf [Accessed 6 May 2018].

Gaaaccounting.com. (2014). The Practical Challenges of Integrated Reporting – GAA

Accounting. [Online] Available at: http://www.gaaaccounting.com/the-practical-challenges-

of-integrated-reporting/ [Accessed 6 May 2018].

Gürtürk, A., (2017). Integrated reporting and sustainability-related assurance: Effects,

current practice and future directions. Kassel: kassel university press GmbH.

Iasplus.com. (2017). ACCA report highlights benefits and challenges of adopting Integrated

Reporting. [Online] Available at: https://www.iasplus.com/en-gb/news/2017/04/acca-

integrated-reporting [Accessed 6 May 2018].

Iasplus.com. (2018). Integrated Reporting - A better review. [Online] Available at:

https://www.iasplus.com/en/binary/sustain/1109integratedreportingview.pdf [Accessed 6

May 2018].

Corporate accounting 11

Integratedreporting.org. (2017). CREATING VALUE FOR SMEs THROUGH INTEGRATED

THINKING. [Online] Available at:

http://integratedreporting.org/wp-content/uploads/2017/08/IFAC_CreatingValueforSMEs.pdf

[Accessed 6 May 2018].

Integratedreporting.org. (2018). The IIRC | Integrated Reporting. [Online] Available at:

https://integratedreporting.org/the-iirc-2/ [Accessed 6 May 2018].

Mio, C. ed. (2016). Integrated Reporting: A New Accounting Disclosure. London: Springer.

Pwc.blogs.com. (2011). Benefits of Comprehensive Integrated Reporting. [Online] Available

at: http://pwc.blogs.com/files/benefits-of-comprehensive-integrated-reporting.pdf [Accessed

6 May 2018].

Vancity.com. (2005). Integrated reporting issues and implications for reporters. [Online]

Available at: https://www.vancity.com/SharedContent/documents/IntegratedReporting.pdf

[Accessed 6 May 2018].

Integratedreporting.org. (2017). CREATING VALUE FOR SMEs THROUGH INTEGRATED

THINKING. [Online] Available at:

http://integratedreporting.org/wp-content/uploads/2017/08/IFAC_CreatingValueforSMEs.pdf

[Accessed 6 May 2018].

Integratedreporting.org. (2018). The IIRC | Integrated Reporting. [Online] Available at:

https://integratedreporting.org/the-iirc-2/ [Accessed 6 May 2018].

Mio, C. ed. (2016). Integrated Reporting: A New Accounting Disclosure. London: Springer.

Pwc.blogs.com. (2011). Benefits of Comprehensive Integrated Reporting. [Online] Available

at: http://pwc.blogs.com/files/benefits-of-comprehensive-integrated-reporting.pdf [Accessed

6 May 2018].

Vancity.com. (2005). Integrated reporting issues and implications for reporters. [Online]

Available at: https://www.vancity.com/SharedContent/documents/IntegratedReporting.pdf

[Accessed 6 May 2018].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.