A Detailed Report on Corporate Accounting and Reporting of Leases

VerifiedAdded on 2023/06/05

|7

|1597

|378

Report

AI Summary

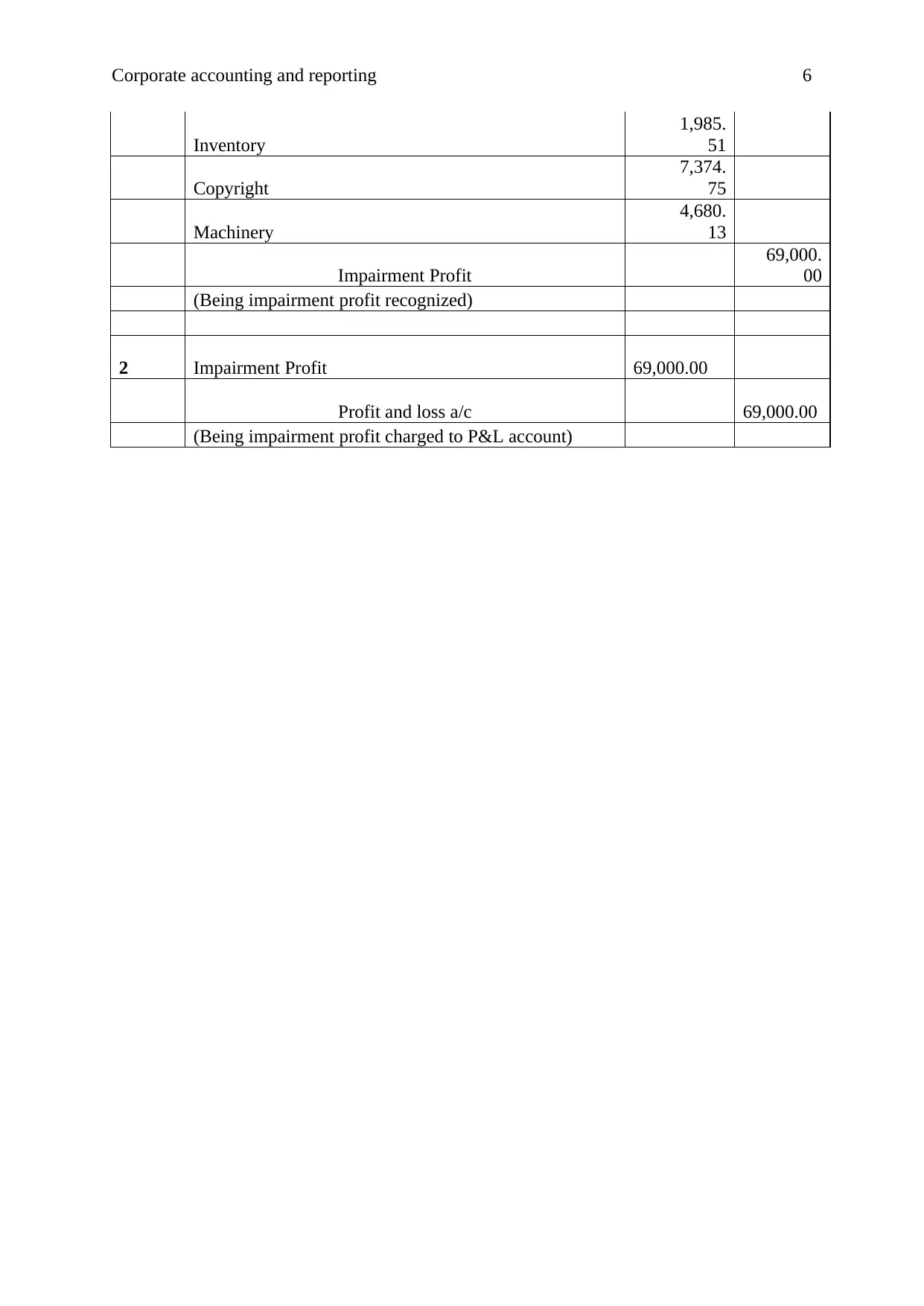

This report evaluates the treatment of leases from the lessee's perspective, emphasizing the importance of accurate record-keeping for financial transparency. It delves into AASB 16, which governs lease recognition, measurement, presentation, and disclosure. The report outlines the accounting process for both finance and operating leases, detailing how they impact the balance sheet, income statement, and cash flow statement. It provides a practical example with journal entries to illustrate the accounting treatment. Additionally, the report includes a computation of impairment loss, offering a comprehensive overview of lease accounting and reporting requirements under AASB guidelines. Desklib provides access to this and other solved assignments to aid students in their studies.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.