Comprehensive Report on Finance Leases Accounting and Impairment Loss

VerifiedAdded on 2023/03/30

|11

|2324

|398

Report

AI Summary

This report provides a detailed analysis of corporate accounting for finance leases and impairment loss. It explains the accounting treatment for finance leases by lessees, focusing on the recognition of right-to-use assets (RUA) and lease liabilities under AASB 16. The report covers the initial and subsequent measurement of RUA and lease liabilities, including the impact of lease modifications and remeasurements. It also discusses the financial statement presentation and disclosure requirements for lessees. Furthermore, the report includes a section on impairment loss, demonstrating the allocation of impairment losses across various assets like goodwill, plant, brand, and fittings, with calculations and pro-rata allocation provided. This document, contributed by a student, is available on Desklib, a platform offering a wide range of study resources for students.

Running head: CORPORATE ACCOUNTING

Corporate accounting

Name of the student

Name of the university

Student ID

Author note

Corporate accounting

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Part A

Accounting for finance leases by lessees

Lease is the arrangement where one party that is the lessor offers an asset

for the purpose of use by other party that is the lessee against periodic payment.

Accounting for any lease is made based on the type of lease. Finance lease is the

approach through which the finance is provided effectively by the leasing entity who

buys the asset for the purpose of providing it on lease for the agreed time period.

Lessee makes the rental payment that is sufficient to cover the asset’s original cost

during the primary period of the lease (Aasb.gov.au 2019). An obligation is there for

making such payment which sometime also includes the balloon payment while the

contract is over. Once all these payments are made, lessor is expected to recover

the investment made by lessor in the asset. The lessee is committed for paying the

rentals over the specified period and technically finance lease is considered as non-

cancellable though it can be terminated before the completion of lease term. Finance

lease leads to recognition of both the assets as well as liabilities by the lessee it its

books at commencement of lease. Further, it shall be reported at the value that is

equal to the PV of the MLP (minimum lease payments). It is likely that lease assets

as well as lease liabilities are reported by lessee and the lessor at different values

(Aasb.gov.au 2019).

Parties to the lease may go for negotiation of the lease before the assets

under the subject is available for the purpose of use by the lessee. The subjected

asset in some of the scenario required to be redesigned or reconstructed to make it

ready for the use by the lessee. Based on the conditions and the terms of contract

the lessee may require making payments associated with the design or construction

Accounting for finance leases by lessees

Lease is the arrangement where one party that is the lessor offers an asset

for the purpose of use by other party that is the lessee against periodic payment.

Accounting for any lease is made based on the type of lease. Finance lease is the

approach through which the finance is provided effectively by the leasing entity who

buys the asset for the purpose of providing it on lease for the agreed time period.

Lessee makes the rental payment that is sufficient to cover the asset’s original cost

during the primary period of the lease (Aasb.gov.au 2019). An obligation is there for

making such payment which sometime also includes the balloon payment while the

contract is over. Once all these payments are made, lessor is expected to recover

the investment made by lessor in the asset. The lessee is committed for paying the

rentals over the specified period and technically finance lease is considered as non-

cancellable though it can be terminated before the completion of lease term. Finance

lease leads to recognition of both the assets as well as liabilities by the lessee it its

books at commencement of lease. Further, it shall be reported at the value that is

equal to the PV of the MLP (minimum lease payments). It is likely that lease assets

as well as lease liabilities are reported by lessee and the lessor at different values

(Aasb.gov.au 2019).

Parties to the lease may go for negotiation of the lease before the assets

under the subject is available for the purpose of use by the lessee. The subjected

asset in some of the scenario required to be redesigned or reconstructed to make it

ready for the use by the lessee. Based on the conditions and the terms of contract

the lessee may require making payments associated with the design or construction

of the asset. If lessee incurs the cost with regard to design or construction of

subjected asset the lessee shall take into consideration those costs through

application of other associated standards (Barone, Birt and Moya 2014)

At the inception the lessee is required to recognise the lease liability and a

right-to-use asset (RUA) and the same shall be valued at cost. Cost of the RUA is

comprised of – (i) direct cost expensed by lessee initially (ii) lease payments made at

commencement of lease reduced by lease incentives received, if any (iii) amount

measured as lease liability initially (iv) cost estimates that is to be expensed by

lessee for dismantling as well as removing subjected asset, restoring the asset to the

condition which it is purported to be and restoring site where it is located. Lessee

must recognise all these costs as the integral part of while it expensed any obligation

for these costs (Wong and Joshi 2015)

For the contract that includes lease element and one or more than one

additional lease or the non lease component the lessee is required to allocate

consideration associated with the contract to each of the lease component and

aggregate stand alone price for the lease component. As the practical expedient, the

lessee has the option to select through the class of the underlying asset not for the

non-lease component and associated n on-lease component, if any (Aasb.gov.au

2019).

After the inception date lessee is required to value the RUA through

application of cost approach – (a) adjusting for measurement of lease liability and (b)

after deducting the amount of accumulated depreciation and accumulated

depreciation, if any. The lessee is required to apply AASB 16 – Property, plant and

equipment for the purpose of charging depreciation on RUA. If the subjected asset’s

subjected asset the lessee shall take into consideration those costs through

application of other associated standards (Barone, Birt and Moya 2014)

At the inception the lessee is required to recognise the lease liability and a

right-to-use asset (RUA) and the same shall be valued at cost. Cost of the RUA is

comprised of – (i) direct cost expensed by lessee initially (ii) lease payments made at

commencement of lease reduced by lease incentives received, if any (iii) amount

measured as lease liability initially (iv) cost estimates that is to be expensed by

lessee for dismantling as well as removing subjected asset, restoring the asset to the

condition which it is purported to be and restoring site where it is located. Lessee

must recognise all these costs as the integral part of while it expensed any obligation

for these costs (Wong and Joshi 2015)

For the contract that includes lease element and one or more than one

additional lease or the non lease component the lessee is required to allocate

consideration associated with the contract to each of the lease component and

aggregate stand alone price for the lease component. As the practical expedient, the

lessee has the option to select through the class of the underlying asset not for the

non-lease component and associated n on-lease component, if any (Aasb.gov.au

2019).

After the inception date lessee is required to value the RUA through

application of cost approach – (a) adjusting for measurement of lease liability and (b)

after deducting the amount of accumulated depreciation and accumulated

depreciation, if any. The lessee is required to apply AASB 16 – Property, plant and

equipment for the purpose of charging depreciation on RUA. If the subjected asset’s

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ownership is reassigned to lessee at the time when the lease period is completed or

if the cost of RUA reveals that the lessee will opt for the purchase option, the RUA

shall be depreciated since the commencement of the lease to the end of life of the

asset (Aasb.gov.au 2019). Otherwise, lessee is required to depreciate RUA from

inception of lease to completion of lease term or completion of the life of RUA,

whichever is earlier. Further, lessee is required to comply with AASB 136 –

Impairment of assets for determining whether the RUA is impaired and accounting

for acknowledged impairment loss. However, if the RUA related to any class of PPE

to which the revaluation model is used by lessee in accordance with AASB 116,

lessee has the option of applying the revaluation model for all the RUA that is related

to that class of PPE (Aasb.gov.au 2019).

After the date of inception the lessee is required to measure lease liability

through reducing carrying value for reflecting the lease payment made, increasing

the carrying value for reflecting the interest for lease liability, re-measurement of

carrying amount for reflecting the reassessment or the lease modification. Re-

measurement shall be carried out for the lease liability through discounting revised

lease payments applying the revised rate of discount if any change is there in

assessing the purchase option for the subjected asset that is assets with the

consideration of circumstances for purchase option or any change is there in the

term of lease where the lessee is required to determine revised payment for lease

based on the revised term of lease (Aasb.gov.au 2019).

In case of lease modification the lessee is required to judge the lease

modification as the separate lease if (a) the consideration of lease goes up by the

value of amount that is commensurate with the stand-alone value for increase in

scope and any applicable and appropriate adjustments to the stand-alone price for

if the cost of RUA reveals that the lessee will opt for the purchase option, the RUA

shall be depreciated since the commencement of the lease to the end of life of the

asset (Aasb.gov.au 2019). Otherwise, lessee is required to depreciate RUA from

inception of lease to completion of lease term or completion of the life of RUA,

whichever is earlier. Further, lessee is required to comply with AASB 136 –

Impairment of assets for determining whether the RUA is impaired and accounting

for acknowledged impairment loss. However, if the RUA related to any class of PPE

to which the revaluation model is used by lessee in accordance with AASB 116,

lessee has the option of applying the revaluation model for all the RUA that is related

to that class of PPE (Aasb.gov.au 2019).

After the date of inception the lessee is required to measure lease liability

through reducing carrying value for reflecting the lease payment made, increasing

the carrying value for reflecting the interest for lease liability, re-measurement of

carrying amount for reflecting the reassessment or the lease modification. Re-

measurement shall be carried out for the lease liability through discounting revised

lease payments applying the revised rate of discount if any change is there in

assessing the purchase option for the subjected asset that is assets with the

consideration of circumstances for purchase option or any change is there in the

term of lease where the lessee is required to determine revised payment for lease

based on the revised term of lease (Aasb.gov.au 2019).

In case of lease modification the lessee is required to judge the lease

modification as the separate lease if (a) the consideration of lease goes up by the

value of amount that is commensurate with the stand-alone value for increase in

scope and any applicable and appropriate adjustments to the stand-alone price for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

reflecting the contract’s circumstances and (b) modification enhances scope of lease

through adding the right to use one or more of the subjected assets. For lease

modification those are not taken into consideration for considering as the separate

lease on the date of lease modification the lessee is required to – (i) determine lease

term for modified lease (ii) assign consideration for modified contract (iii) re-measure

lease liability through discounting the revised payments for lease by applying the

revised rate of discount (Aasb.gov.au 2019). For the modification of lease that is not

taken into consideration as the distinct lease lessee is required to account for the re-

measurement of lease liability through – (i) making the corresponding adjustment to

RUA for all the modified lease and (ii) reducing carrying amount of RUA for reflecting

partial or the full termination of lease for the modified lease that reduce the scope of

lease. Further, the lessee is required to recognise the profit or loss for any gain or

loss associated to full or partial termination of lease (Spencer and Webb 2015)

A lease is placed in the financial statement or disclosed in the notes. When

the lessee is unable to provide RUA individually in the financial statement, the lessee

will incorporate RUA within similar category as that of the similar subjected assets

and will be reported if they were possessed and divulge which line unit in the

financial statement encompasses RUA (Müller, Riedl and Sellhorn 2015). When the

lessee does not present the liabilities of lease individually in the financial statement,

the lessee will divulge which line unit in the financial statement encompasses those

liabilities. The requirement in the above paragraph does not put in an application for

RUA that match the meaning of investment property that needs to be shown in the

financial report as investment property. Lessee needs to show current interest cost

towards lease liability individually from the depreciation charge for the RUA in the

profit or loss statement. Interest cost towards lease liability is a part of finance costs

through adding the right to use one or more of the subjected assets. For lease

modification those are not taken into consideration for considering as the separate

lease on the date of lease modification the lessee is required to – (i) determine lease

term for modified lease (ii) assign consideration for modified contract (iii) re-measure

lease liability through discounting the revised payments for lease by applying the

revised rate of discount (Aasb.gov.au 2019). For the modification of lease that is not

taken into consideration as the distinct lease lessee is required to account for the re-

measurement of lease liability through – (i) making the corresponding adjustment to

RUA for all the modified lease and (ii) reducing carrying amount of RUA for reflecting

partial or the full termination of lease for the modified lease that reduce the scope of

lease. Further, the lessee is required to recognise the profit or loss for any gain or

loss associated to full or partial termination of lease (Spencer and Webb 2015)

A lease is placed in the financial statement or disclosed in the notes. When

the lessee is unable to provide RUA individually in the financial statement, the lessee

will incorporate RUA within similar category as that of the similar subjected assets

and will be reported if they were possessed and divulge which line unit in the

financial statement encompasses RUA (Müller, Riedl and Sellhorn 2015). When the

lessee does not present the liabilities of lease individually in the financial statement,

the lessee will divulge which line unit in the financial statement encompasses those

liabilities. The requirement in the above paragraph does not put in an application for

RUA that match the meaning of investment property that needs to be shown in the

financial report as investment property. Lessee needs to show current interest cost

towards lease liability individually from the depreciation charge for the RUA in the

profit or loss statement. Interest cost towards lease liability is a part of finance costs

that is needed to be shown in the income statement and profit and loss statement

(Aasb.gov.au 2019). A lessee shall show under cash flow report the payment in cash

for the major segment of the lease liability in the financing activities, payment in cash

for the interest part of the lease liability putting use the needs in AASB107cash flow

statement for interest paid and payments for lease of low-value asset, uneven lease

payments and lease payments over short term lease payments not a part of

measurement of lease liability within operating activities (International Accounting

Standards Board (IASB) 2013).

The major reason behind declaration in the notes in addition to the details

provided in the cash flow statement, profit or loss statement and financial statement

is that it provides foundation for the users of these annual statements to gauge the

effect that leases have on the cash flows of the lessee, financial performance and

the financial position. A lessee needs to divulge information regarding ithe leases for

which the person is considered as lessee in one note or various segment under the

annual statements. But a lessee should not replicate the information that is present

beforehand in the financial statement, subjected to the fact that the information is

consolidated by cross reference in separate section or in one note about leases

(Financial Accounting Standards Board (FASB) 2016).

A lessee shall divulge the depreciation charge for RUA by class of subjected

assets, interest expense on lease liabilities, the expense related to short-term leases

that should not be included in the expense relating to leases with a lease term of 30

days or less, the expense related to leases of low-value assets that should not be

included in the expenses pertaining to short-term leases of low-value assets, the

expense pertaining to variable lease payment not part of calculating lease liabilities,

income from subleasing RUA, total value of cash outflow towards leases, in additions

(Aasb.gov.au 2019). A lessee shall show under cash flow report the payment in cash

for the major segment of the lease liability in the financing activities, payment in cash

for the interest part of the lease liability putting use the needs in AASB107cash flow

statement for interest paid and payments for lease of low-value asset, uneven lease

payments and lease payments over short term lease payments not a part of

measurement of lease liability within operating activities (International Accounting

Standards Board (IASB) 2013).

The major reason behind declaration in the notes in addition to the details

provided in the cash flow statement, profit or loss statement and financial statement

is that it provides foundation for the users of these annual statements to gauge the

effect that leases have on the cash flows of the lessee, financial performance and

the financial position. A lessee needs to divulge information regarding ithe leases for

which the person is considered as lessee in one note or various segment under the

annual statements. But a lessee should not replicate the information that is present

beforehand in the financial statement, subjected to the fact that the information is

consolidated by cross reference in separate section or in one note about leases

(Financial Accounting Standards Board (FASB) 2016).

A lessee shall divulge the depreciation charge for RUA by class of subjected

assets, interest expense on lease liabilities, the expense related to short-term leases

that should not be included in the expense relating to leases with a lease term of 30

days or less, the expense related to leases of low-value assets that should not be

included in the expenses pertaining to short-term leases of low-value assets, the

expense pertaining to variable lease payment not part of calculating lease liabilities,

income from subleasing RUA, total value of cash outflow towards leases, in additions

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to RUA, gains or losses coming from leaseback and sale transaction and the

carrying amount of RUA at the end of the reporting period by class of underlying

assets amounts for the reporting period. A lessee needs to provide disclosures only

in tabular format, unless other format is more relevant and the amounts should have

cost included in carrying amount of any other asset during the period under concern.

A lessee is required to provide the value of lease commitments towards short-term

leases if the portfolio of short term leases under which it is included at the completion

of reporting period is not similar to that of the expense disclosed (Chambers, Dooley

and Finger 2015). When RUA matches the meaning of investment property, a lessee

should apply the disclosure requirement in AASB 140.

Apart from the disclosures requirement mentioned above, lessee is required

to disclose additional qualitative plus quantitative information regarding the leasing

activities required for meeting objectives associated with disclosures. The said

additional information may inclusive of but not limited to the information that may

assist the users for assessing the financial statements in assessing – (i) covenants

or restrictions that is imposed by the leases (ii) leaseback and sales transactions (iii)

nature of leasing activities of lessee (iv) future cash outflows to which the lessee is

exposed and which is not reflected while measuring the lease liabilities. The

exposures may include – (i) lease that has not yet been commenced however, the

lessee is committed to the same (ii) termination as well as extension options (iii)

guarantees for residual values (iv) variable lease payments. Further, the lessee who

accounts for the short term lease or leases for low value asset must disclose the fact

related to approaches applied for the same (Bohušová 2015.)

carrying amount of RUA at the end of the reporting period by class of underlying

assets amounts for the reporting period. A lessee needs to provide disclosures only

in tabular format, unless other format is more relevant and the amounts should have

cost included in carrying amount of any other asset during the period under concern.

A lessee is required to provide the value of lease commitments towards short-term

leases if the portfolio of short term leases under which it is included at the completion

of reporting period is not similar to that of the expense disclosed (Chambers, Dooley

and Finger 2015). When RUA matches the meaning of investment property, a lessee

should apply the disclosure requirement in AASB 140.

Apart from the disclosures requirement mentioned above, lessee is required

to disclose additional qualitative plus quantitative information regarding the leasing

activities required for meeting objectives associated with disclosures. The said

additional information may inclusive of but not limited to the information that may

assist the users for assessing the financial statements in assessing – (i) covenants

or restrictions that is imposed by the leases (ii) leaseback and sales transactions (iii)

nature of leasing activities of lessee (iv) future cash outflows to which the lessee is

exposed and which is not reflected while measuring the lease liabilities. The

exposures may include – (i) lease that has not yet been commenced however, the

lessee is committed to the same (ii) termination as well as extension options (iii)

guarantees for residual values (iv) variable lease payments. Further, the lessee who

accounts for the short term lease or leases for low value asset must disclose the fact

related to approaches applied for the same (Bohušová 2015.)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Part B

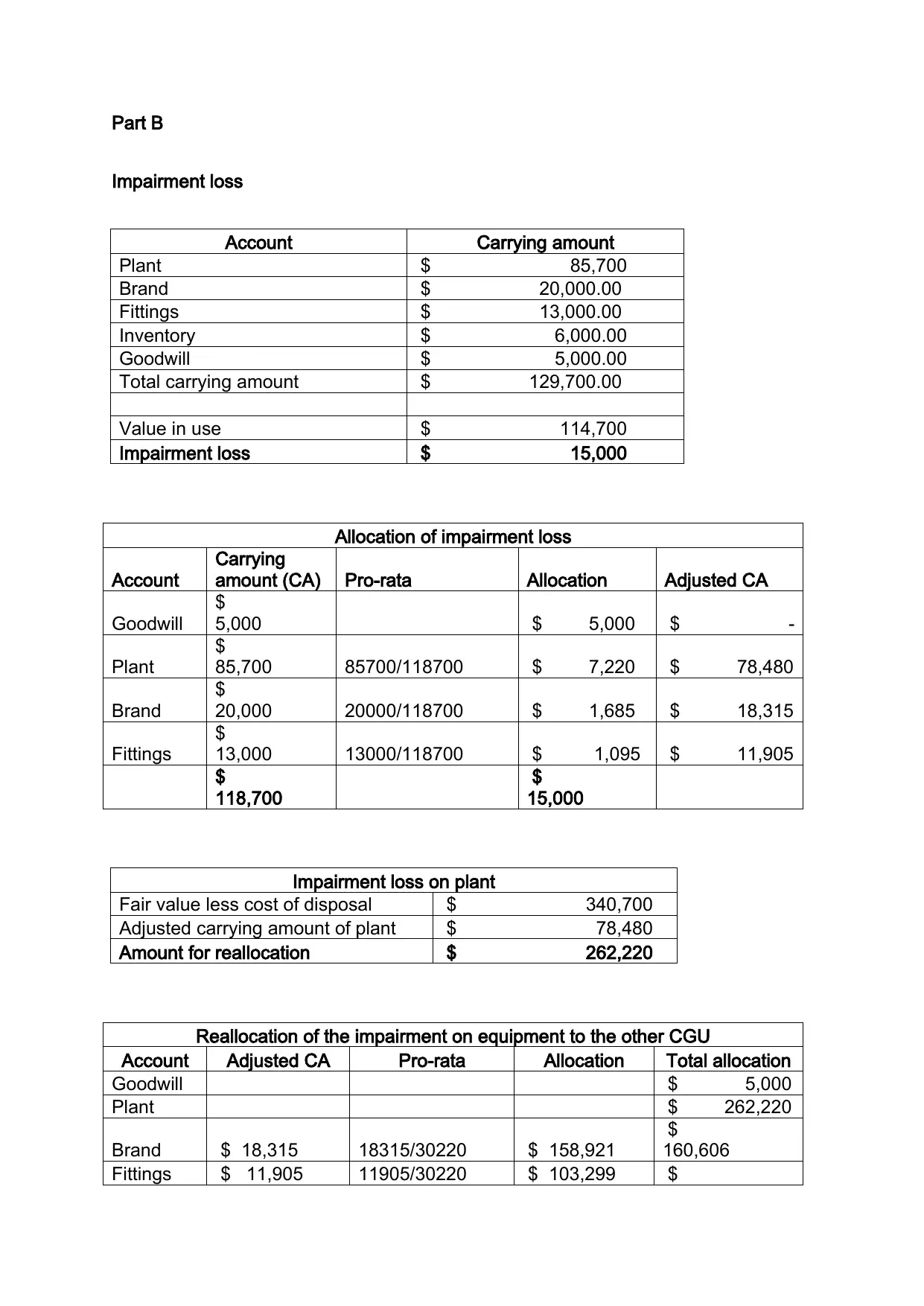

Impairment loss

Account Carrying amount

Plant $ 85,700

Brand $ 20,000.00

Fittings $ 13,000.00

Inventory $ 6,000.00

Goodwill $ 5,000.00

Total carrying amount $ 129,700.00

Value in use $ 114,700

Impairment loss $ 15,000

Allocation of impairment loss

Account

Carrying

amount (CA) Pro-rata Allocation Adjusted CA

Goodwill

$

5,000 $ 5,000 $ -

Plant

$

85,700 85700/118700 $ 7,220 $ 78,480

Brand

$

20,000 20000/118700 $ 1,685 $ 18,315

Fittings

$

13,000 13000/118700 $ 1,095 $ 11,905

$

118,700

$

15,000

Impairment loss on plant

Fair value less cost of disposal $ 340,700

Adjusted carrying amount of plant $ 78,480

Amount for reallocation $ 262,220

Reallocation of the impairment on equipment to the other CGU

Account Adjusted CA Pro-rata Allocation Total allocation

Goodwill $ 5,000

Plant $ 262,220

Brand $ 18,315 18315/30220 $ 158,921

$

160,606

Fittings $ 11,905 11905/30220 $ 103,299 $

Impairment loss

Account Carrying amount

Plant $ 85,700

Brand $ 20,000.00

Fittings $ 13,000.00

Inventory $ 6,000.00

Goodwill $ 5,000.00

Total carrying amount $ 129,700.00

Value in use $ 114,700

Impairment loss $ 15,000

Allocation of impairment loss

Account

Carrying

amount (CA) Pro-rata Allocation Adjusted CA

Goodwill

$

5,000 $ 5,000 $ -

Plant

$

85,700 85700/118700 $ 7,220 $ 78,480

Brand

$

20,000 20000/118700 $ 1,685 $ 18,315

Fittings

$

13,000 13000/118700 $ 1,095 $ 11,905

$

118,700

$

15,000

Impairment loss on plant

Fair value less cost of disposal $ 340,700

Adjusted carrying amount of plant $ 78,480

Amount for reallocation $ 262,220

Reallocation of the impairment on equipment to the other CGU

Account Adjusted CA Pro-rata Allocation Total allocation

Goodwill $ 5,000

Plant $ 262,220

Brand $ 18,315 18315/30220 $ 158,921

$

160,606

Fittings $ 11,905 11905/30220 $ 103,299 $

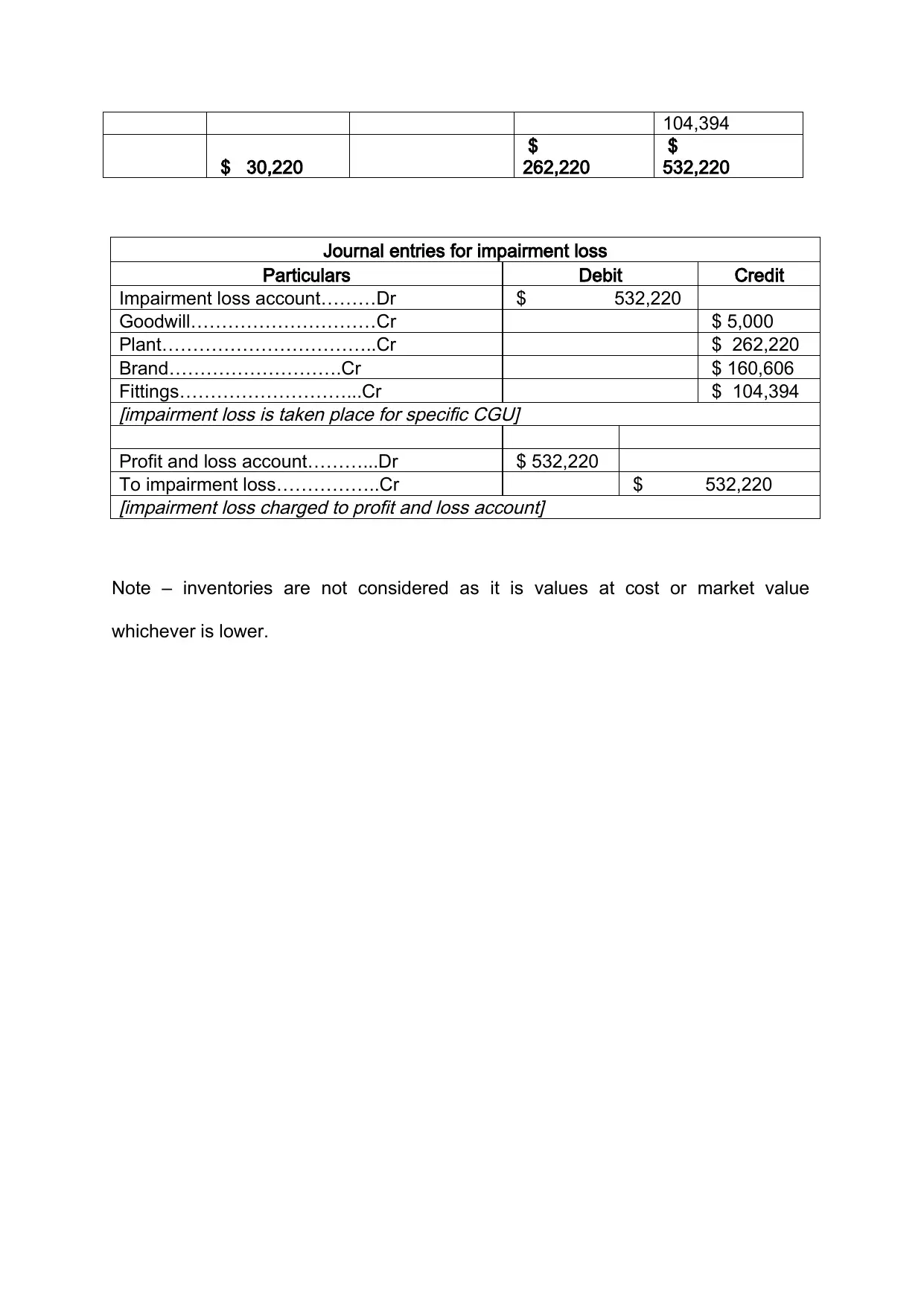

104,394

$ 30,220

$

262,220

$

532,220

Journal entries for impairment loss

Particulars Debit Credit

Impairment loss account………Dr $ 532,220

Goodwill…………………………Cr $ 5,000

Plant……………………………..Cr $ 262,220

Brand……………………….Cr $ 160,606

Fittings………………………...Cr $ 104,394[impairment loss is taken place for specific CGU]

Profit and loss account………...Dr $ 532,220

To impairment loss……………..Cr $ 532,220[impairment loss charged to profit and loss account]

Note – inventories are not considered as it is values at cost or market value

whichever is lower.

$ 30,220

$

262,220

$

532,220

Journal entries for impairment loss

Particulars Debit Credit

Impairment loss account………Dr $ 532,220

Goodwill…………………………Cr $ 5,000

Plant……………………………..Cr $ 262,220

Brand……………………….Cr $ 160,606

Fittings………………………...Cr $ 104,394[impairment loss is taken place for specific CGU]

Profit and loss account………...Dr $ 532,220

To impairment loss……………..Cr $ 532,220[impairment loss charged to profit and loss account]

Note – inventories are not considered as it is values at cost or market value

whichever is lower.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Reference

Aasb.gov.au. 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB16_02-16.pdf [Accessed 6

Jun. 2019].

Barone, E., Birt, J. and Moya, S., 2014. Lease accounting: a review of recent

literature.

Accounting in Europe,

11(1), pp.35-54.

Bohušová, H., 2015. Is Capitalization of Operating Lease Way to Increase of

Comparability of Financial Statements Prepared in Accordance with IFRS and US

GAAP?.

Acta Universitatis Agriculturae et Silviculturae Mendelianae

Brunensis,

63(2), pp.507-514.

Chambers, D., Dooley, J. and Finger, C.A., 2015. Preparing for the Looming

Changes in Lease Accounting.

The CPA Journal,

85(1), p.38.

Financial Accounting Standards Board (FASB). 2016. Accounting Standards

Codification (ASC) Topic 842, Leases. FASB

International Accounting Standards Board (IASB) 2013. Exposure Draft, Leases.

IASB.

International Accounting Standards Board (IASB) 2016. International Financial

Reporting Standards (IFRS) No. 16, Leases. IASB.

Müller, M.A., Riedl, E.J. and Sellhorn, T., 2015. Recognition versus disclosure of fair

values.

The Accounting Review,

90(6), pp.2411-2447.

Spencer, A. W., and Webb, T. Z. 2015. Leases: A review of contemporary academic

literature relating to lessees. Accounting Horizons, 29(4), 997–1023.

Aasb.gov.au. 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB16_02-16.pdf [Accessed 6

Jun. 2019].

Barone, E., Birt, J. and Moya, S., 2014. Lease accounting: a review of recent

literature.

Accounting in Europe,

11(1), pp.35-54.

Bohušová, H., 2015. Is Capitalization of Operating Lease Way to Increase of

Comparability of Financial Statements Prepared in Accordance with IFRS and US

GAAP?.

Acta Universitatis Agriculturae et Silviculturae Mendelianae

Brunensis,

63(2), pp.507-514.

Chambers, D., Dooley, J. and Finger, C.A., 2015. Preparing for the Looming

Changes in Lease Accounting.

The CPA Journal,

85(1), p.38.

Financial Accounting Standards Board (FASB). 2016. Accounting Standards

Codification (ASC) Topic 842, Leases. FASB

International Accounting Standards Board (IASB) 2013. Exposure Draft, Leases.

IASB.

International Accounting Standards Board (IASB) 2016. International Financial

Reporting Standards (IFRS) No. 16, Leases. IASB.

Müller, M.A., Riedl, E.J. and Sellhorn, T., 2015. Recognition versus disclosure of fair

values.

The Accounting Review,

90(6), pp.2411-2447.

Spencer, A. W., and Webb, T. Z. 2015. Leases: A review of contemporary academic

literature relating to lessees. Accounting Horizons, 29(4), 997–1023.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Wong, K. and Joshi, M., 2015. The impact of lease capitalisation on financial

statements and key ratios: Evidence from Australia.

Australasian Accounting

Business & Finance Journal,

9(3), p.27.

statements and key ratios: Evidence from Australia.

Australasian Accounting

Business & Finance Journal,

9(3), p.27.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.