Corporate Accounting Assignment: Trimester 3, 2019, Deakin University

VerifiedAdded on 2022/09/08

|11

|2086

|18

Homework Assignment

AI Summary

This assignment delves into key aspects of corporate accounting, addressing questions on carrying amounts, lease accounting, and the implications of new requirements. It examines why the carrying amount of a lease asset typically decreases faster than the liability, and explores how organizations might react to these changes. Furthermore, the assignment analyzes the concept of a 'true and fair view' of financial statements, outlining the conditions that must be met and the responsibilities of auditors and directors. It also discusses the challenges and advantages of a single set of global accounting standards, considering its impact on comparability, international expansion, and cost reduction. The assignment highlights the importance of accounting standards in providing transparent and reliable financial information for stakeholders.

Running Head: CORPORATE ACCOUNTING

Corporate accounting

Name of the Student:

Name of the University:

Author note:

Corporate accounting

Name of the Student:

Name of the University:

Author note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CORPORATE ACCOUNTING

Table of Contents

Part A...................................................................................................................................2

Answer to Question 1......................................................................................................2

Answer to question 2.......................................................................................................3

Part B...................................................................................................................................4

Part C...................................................................................................................................5

Answer to question 1.......................................................................................................5

Answer to question 2.......................................................................................................7

Reference list.......................................................................................................................9

CORPORATE ACCOUNTING

Table of Contents

Part A...................................................................................................................................2

Answer to Question 1......................................................................................................2

Answer to question 2.......................................................................................................3

Part B...................................................................................................................................4

Part C...................................................................................................................................5

Answer to question 1.......................................................................................................5

Answer to question 2.......................................................................................................7

Reference list.......................................................................................................................9

2

CORPORATE ACCOUNTING

Part A

Answer to Question 1

Carrying amount is the cost of assets or liability, which are recorded in the financial

statement as the net amount after deducting accumulated depreciation, or any impairment cost.

This cost is different from the current market value of the assets or liability as it shows the

market value of the assets or liability depending on the demand and supply of the market. It is

also known as the book value of the assets as the value of the assets are recorded in the books of

account which is calculated as historical cost after deducting accumulated depreciation and the

impairment cost. Its value is calculated by following the GAAP and IFRS accounting principle

(Schaltegger, Etxeberria and Ortas 2017). Carrying value is the measurement of value for the

company’s asset or liability. Usually carrying value is not recorded in the balance sheet and it is

always lower than the current market value. Assets and liabilities are recorded in the balance

sheet in their original cost rather than the market value as it is easy to trace. When a company

purchase any intangible assets then the formula to calculate the carrying amount will be the

original purchase cost minus the amortization expenses. On the other hand if tangible assets is

purchased then the formula to calculate the carrying amount is original purchase cost minus

depreciation.

Carrying amount of the assets is not the same as the market value and it differ in many ways. It

depends on the gradual depreciation of the assets which shows the declined value with the time

pass. The carrying amount of lease assets will reduce more quickly than the carrying amount of

the lease liability because in each period of lease asset the asset value will be depreciating in

straight-line method. The lease liability is reduced by the value of the lease payments which is

increased by the interest, with the reduction of the life of the lease. Amount of the both lease

CORPORATE ACCOUNTING

Part A

Answer to Question 1

Carrying amount is the cost of assets or liability, which are recorded in the financial

statement as the net amount after deducting accumulated depreciation, or any impairment cost.

This cost is different from the current market value of the assets or liability as it shows the

market value of the assets or liability depending on the demand and supply of the market. It is

also known as the book value of the assets as the value of the assets are recorded in the books of

account which is calculated as historical cost after deducting accumulated depreciation and the

impairment cost. Its value is calculated by following the GAAP and IFRS accounting principle

(Schaltegger, Etxeberria and Ortas 2017). Carrying value is the measurement of value for the

company’s asset or liability. Usually carrying value is not recorded in the balance sheet and it is

always lower than the current market value. Assets and liabilities are recorded in the balance

sheet in their original cost rather than the market value as it is easy to trace. When a company

purchase any intangible assets then the formula to calculate the carrying amount will be the

original purchase cost minus the amortization expenses. On the other hand if tangible assets is

purchased then the formula to calculate the carrying amount is original purchase cost minus

depreciation.

Carrying amount of the assets is not the same as the market value and it differ in many ways. It

depends on the gradual depreciation of the assets which shows the declined value with the time

pass. The carrying amount of lease assets will reduce more quickly than the carrying amount of

the lease liability because in each period of lease asset the asset value will be depreciating in

straight-line method. The lease liability is reduced by the value of the lease payments which is

increased by the interest, with the reduction of the life of the lease. Amount of the both lease

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CORPORATE ACCOUNTING

asset and liability are the same in the beginning but the amount of the asset stays lower than the

amount of the liability during the lease period. This effect can be seen in all type of lease of the

company by considering the portfolio effect.

Answer to question 2

New requirement for the lease will be required for the organization who want to report

their lease of both the asset and liabilities on their balance sheet. With the effective adoption of

the new lease accounting standard helps the companies to develop a strategic way for the growth.

New lease are expected to provide the investors and the stakeholders more transparent picture of

the company. This change will make a significant change in the technology, media and

communication industry (Watson 2015).

Every company uses the lease as their only way to obtain the access of the assets so they are

going too effected by the new lease. The new requirement will eliminate all the balance sheet

accounting for the lessee as it is used for the financial metrics. It will affect the credit rating,

borrowing costs and other stakeholders. Lessor business model may be effected as their will be

new need of lease with behavioral change of the lessee. Business process and system are also get

impacted as it requires more data than before. A company has to perform new implementation

like cross-functional approach other than the accounting process. Organization must be prepared

for all potential issues, cost and risk that may arise. Balance sheets of the companies are going to

increase while the gearing ratio will increase and the capital ratio will decreases. Both lessee and

lessor will need to again negotiate and restructure their lease agreement. Business and legal

structure need to reassess with the new lease requirement structure. Lessors are more affected

then the lessor as per the changes required which impacts their business model and the lease

items.

CORPORATE ACCOUNTING

asset and liability are the same in the beginning but the amount of the asset stays lower than the

amount of the liability during the lease period. This effect can be seen in all type of lease of the

company by considering the portfolio effect.

Answer to question 2

New requirement for the lease will be required for the organization who want to report

their lease of both the asset and liabilities on their balance sheet. With the effective adoption of

the new lease accounting standard helps the companies to develop a strategic way for the growth.

New lease are expected to provide the investors and the stakeholders more transparent picture of

the company. This change will make a significant change in the technology, media and

communication industry (Watson 2015).

Every company uses the lease as their only way to obtain the access of the assets so they are

going too effected by the new lease. The new requirement will eliminate all the balance sheet

accounting for the lessee as it is used for the financial metrics. It will affect the credit rating,

borrowing costs and other stakeholders. Lessor business model may be effected as their will be

new need of lease with behavioral change of the lessee. Business process and system are also get

impacted as it requires more data than before. A company has to perform new implementation

like cross-functional approach other than the accounting process. Organization must be prepared

for all potential issues, cost and risk that may arise. Balance sheets of the companies are going to

increase while the gearing ratio will increase and the capital ratio will decreases. Both lessee and

lessor will need to again negotiate and restructure their lease agreement. Business and legal

structure need to reassess with the new lease requirement structure. Lessors are more affected

then the lessor as per the changes required which impacts their business model and the lease

items.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CORPORATE ACCOUNTING

Part B

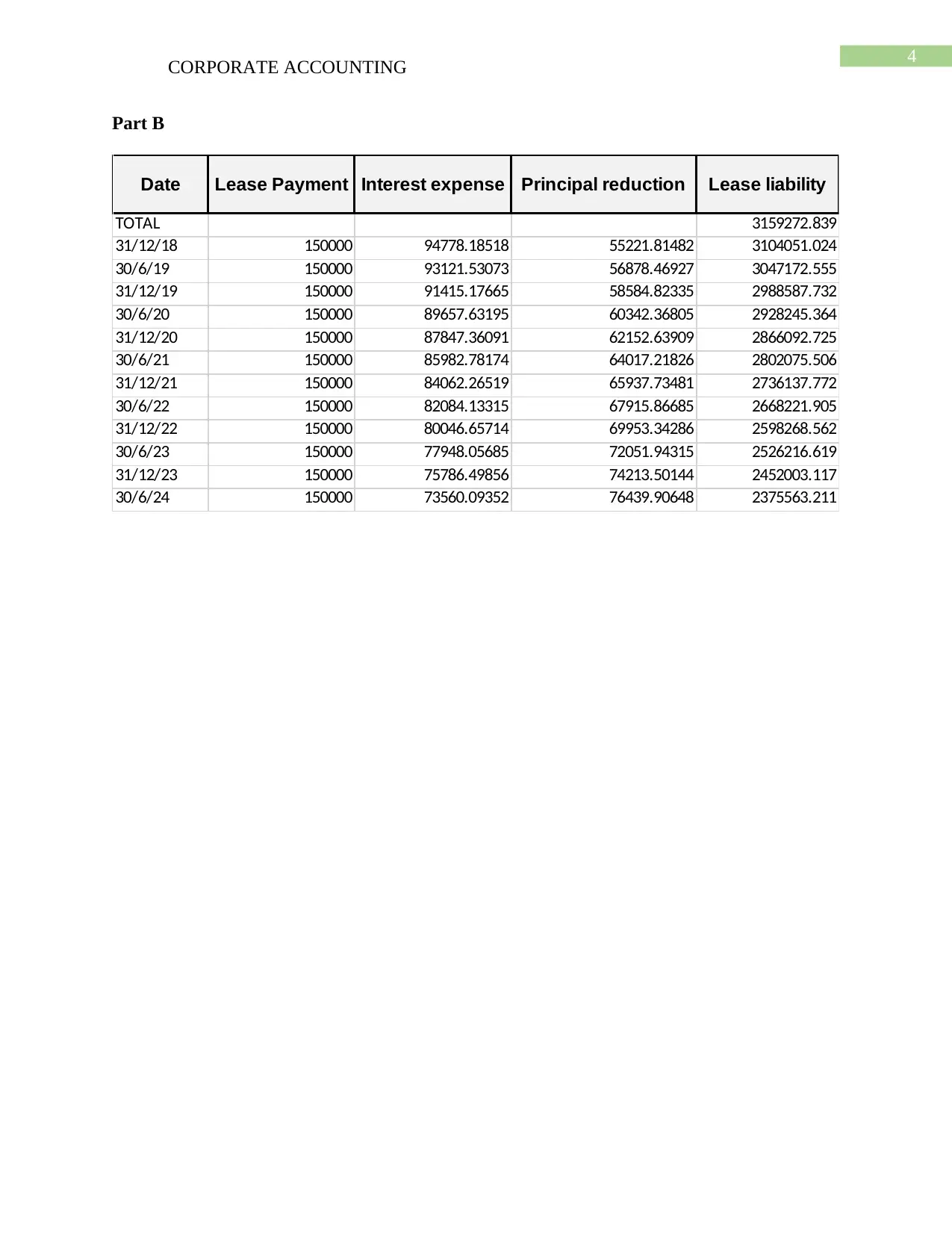

Date Lease Payment Interest expense Principal reduction Lease liability

TOTAL 3159272.839

31/12/18 150000 94778.18518 55221.81482 3104051.024

30/6/19 150000 93121.53073 56878.46927 3047172.555

31/12/19 150000 91415.17665 58584.82335 2988587.732

30/6/20 150000 89657.63195 60342.36805 2928245.364

31/12/20 150000 87847.36091 62152.63909 2866092.725

30/6/21 150000 85982.78174 64017.21826 2802075.506

31/12/21 150000 84062.26519 65937.73481 2736137.772

30/6/22 150000 82084.13315 67915.86685 2668221.905

31/12/22 150000 80046.65714 69953.34286 2598268.562

30/6/23 150000 77948.05685 72051.94315 2526216.619

31/12/23 150000 75786.49856 74213.50144 2452003.117

30/6/24 150000 73560.09352 76439.90648 2375563.211

CORPORATE ACCOUNTING

Part B

Date Lease Payment Interest expense Principal reduction Lease liability

TOTAL 3159272.839

31/12/18 150000 94778.18518 55221.81482 3104051.024

30/6/19 150000 93121.53073 56878.46927 3047172.555

31/12/19 150000 91415.17665 58584.82335 2988587.732

30/6/20 150000 89657.63195 60342.36805 2928245.364

31/12/20 150000 87847.36091 62152.63909 2866092.725

30/6/21 150000 85982.78174 64017.21826 2802075.506

31/12/21 150000 84062.26519 65937.73481 2736137.772

30/6/22 150000 82084.13315 67915.86685 2668221.905

31/12/22 150000 80046.65714 69953.34286 2598268.562

30/6/23 150000 77948.05685 72051.94315 2526216.619

31/12/23 150000 75786.49856 74213.50144 2452003.117

30/6/24 150000 73560.09352 76439.90648 2375563.211

5

CORPORATE ACCOUNTING

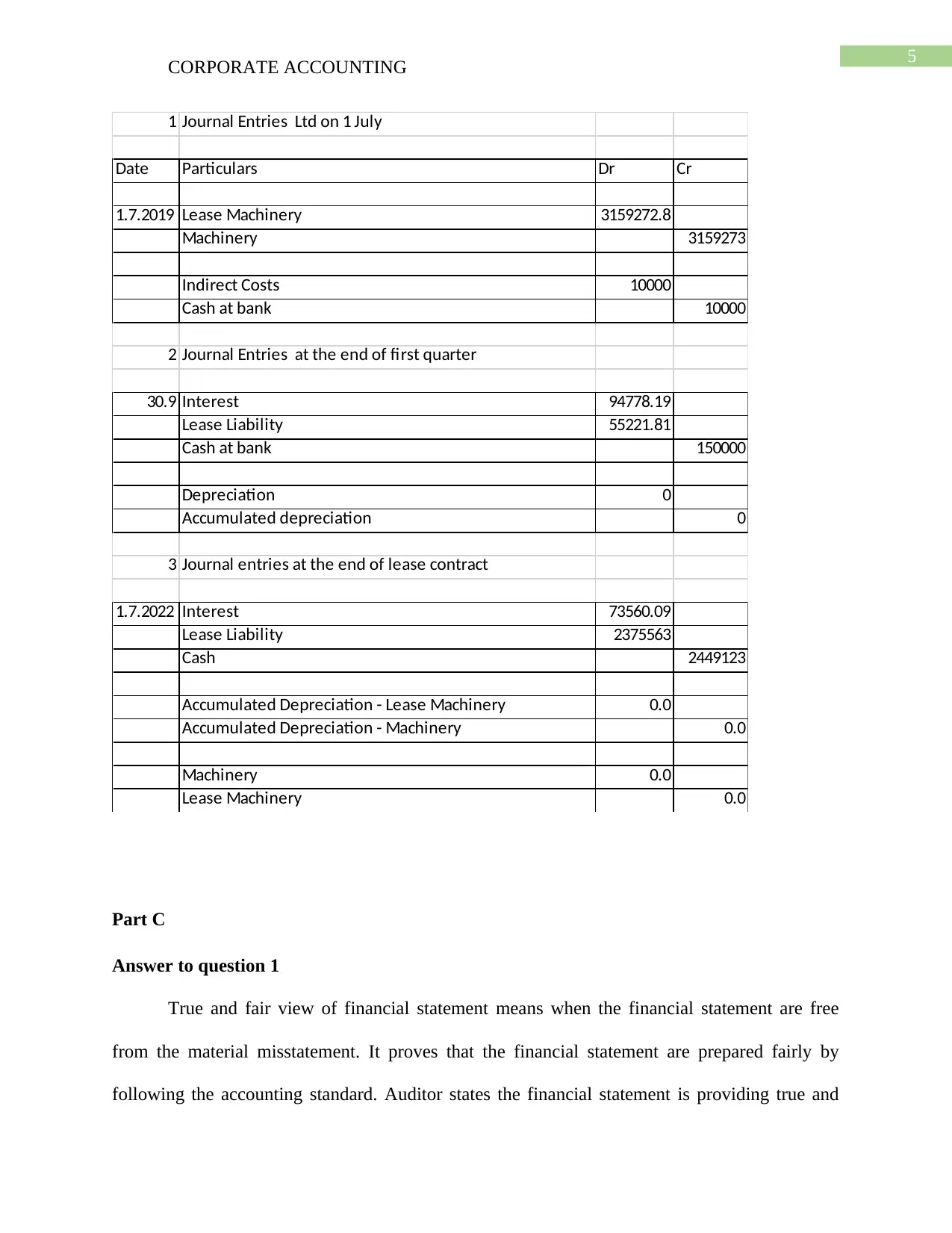

1 Journal Entries Ltd on 1 July

Date Particulars Dr Cr

1.7.2019 Lease Machinery 3159272.8

Machinery 3159273

Indirect Costs 10000

Cash at bank 10000

2 Journal Entries at the end of first quarter

30.9 Interest 94778.19

Lease Liability 55221.81

Cash at bank 150000

Depreciation 0

Accumulated depreciation 0

3 Journal entries at the end of lease contract

1.7.2022 Interest 73560.09

Lease Liability 2375563

Cash 2449123

Accumulated Depreciation - Lease Machinery 0.0

Accumulated Depreciation - Machinery 0.0

Machinery 0.0

Lease Machinery 0.0

Part C

Answer to question 1

True and fair view of financial statement means when the financial statement are free

from the material misstatement. It proves that the financial statement are prepared fairly by

following the accounting standard. Auditor states the financial statement is providing true and

CORPORATE ACCOUNTING

1 Journal Entries Ltd on 1 July

Date Particulars Dr Cr

1.7.2019 Lease Machinery 3159272.8

Machinery 3159273

Indirect Costs 10000

Cash at bank 10000

2 Journal Entries at the end of first quarter

30.9 Interest 94778.19

Lease Liability 55221.81

Cash at bank 150000

Depreciation 0

Accumulated depreciation 0

3 Journal entries at the end of lease contract

1.7.2022 Interest 73560.09

Lease Liability 2375563

Cash 2449123

Accumulated Depreciation - Lease Machinery 0.0

Accumulated Depreciation - Machinery 0.0

Machinery 0.0

Lease Machinery 0.0

Part C

Answer to question 1

True and fair view of financial statement means when the financial statement are free

from the material misstatement. It proves that the financial statement are prepared fairly by

following the accounting standard. Auditor states the financial statement is providing true and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CORPORATE ACCOUNTING

fair view when they found no financial misstatement and are correctly prepared. Auditor uses

this in their report but they use this very carefully after proper examination. The word true states

that the financial statements are correct and prepared according to the IFRS framework without

any material misstatement (Maas, Schaltegger and Crutzen 2016). Whereas the fair means that, the

financial statement provides the faithful information without any bias. It shows the economic

substance of the transaction rather than the legal form. A financial statement is said to be the true

and fair when it satisfy some conditions like books of accounts has recorded all the business

transaction correctly, there is no error or fraud in the financial statement, all the provisions under

the companies act laws has been followed and the books of accounts has been prepared

according to the accepted accounting policies. When all this condition satisfies then the financial

statement is said to be true and fair.

True and fair view financial statement is mostly recognized and its preparation is one of the

responsibility of the directors of the company. Directors mainly prefer the audited financial

statement which are approved by them. It is more appropriate than any other financial statement.

Auditor is required to exercise the audit opinion which is sufficient for the directors to reach the

conclusion solely. So, auditors must consider the directors points while fulfilling their

responsibility during the preparation of the true and fair financial statement. Director of the

company does not approves the accounts unless he is satisfied with the true and fair of the

financial statement consisting of the company’s asset and liabilities. Accounts are expected to

give true and fair view if it complies with the relevant regulatory legislation, comply with the

relevant accounting standard, providing an unbiased report, providing report with sufficient

accuracy with all the materiality and underlying the substances of the legal forms.

CORPORATE ACCOUNTING

fair view when they found no financial misstatement and are correctly prepared. Auditor uses

this in their report but they use this very carefully after proper examination. The word true states

that the financial statements are correct and prepared according to the IFRS framework without

any material misstatement (Maas, Schaltegger and Crutzen 2016). Whereas the fair means that, the

financial statement provides the faithful information without any bias. It shows the economic

substance of the transaction rather than the legal form. A financial statement is said to be the true

and fair when it satisfy some conditions like books of accounts has recorded all the business

transaction correctly, there is no error or fraud in the financial statement, all the provisions under

the companies act laws has been followed and the books of accounts has been prepared

according to the accepted accounting policies. When all this condition satisfies then the financial

statement is said to be true and fair.

True and fair view financial statement is mostly recognized and its preparation is one of the

responsibility of the directors of the company. Directors mainly prefer the audited financial

statement which are approved by them. It is more appropriate than any other financial statement.

Auditor is required to exercise the audit opinion which is sufficient for the directors to reach the

conclusion solely. So, auditors must consider the directors points while fulfilling their

responsibility during the preparation of the true and fair financial statement. Director of the

company does not approves the accounts unless he is satisfied with the true and fair of the

financial statement consisting of the company’s asset and liabilities. Accounts are expected to

give true and fair view if it complies with the relevant regulatory legislation, comply with the

relevant accounting standard, providing an unbiased report, providing report with sufficient

accuracy with all the materiality and underlying the substances of the legal forms.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE ACCOUNTING

Answer to question 2

With the diversified accounting practice across the countries has make it difficult for the

companies involved in the foreign operation to prepare the financial statement. Users of the

financial statement found it difficult in comparing the financial information of different

companies, as they are prepared according to their accounting standard followed in their

countries (Atanasov and Black 2016). In recent years, the demand in the international business has

increased a lot which forced the accounting users to record their transaction and financial report

according to the international market. It created a lot of pressure and more time consuming for

the accountant to keep the record. Even the small companies has to consider the international

accounting standard which has not only created work pressure but also increase the cost. All of

this caused the major reason for the establishment of the single set of global accounting standard.

Some of the advantages of single set of global accounting standard are as follows:

Comparability – It is one of the biggest advantage of the single global accounting

standard. It helps to compare the business on basis of the same accounting standard.

International expansion – With the Single set of global accounting standard it will

remove the barriers of expansion for companies. Companies who want to expand in the

overseas business need to consider the international standards by completely adopting the

new set of accounting. In some cases, the cost of accounts maintenance of the company

also increases specially in the small organization.

Central authoritative body – This single standard rule helps to build a single policy which

is the only authority body to rule the standard. Currently there are different sets of

accounting standard in different country. With this new standard it will reduce the

disagreement between the countries and international regulators.

CORPORATE ACCOUNTING

Answer to question 2

With the diversified accounting practice across the countries has make it difficult for the

companies involved in the foreign operation to prepare the financial statement. Users of the

financial statement found it difficult in comparing the financial information of different

companies, as they are prepared according to their accounting standard followed in their

countries (Atanasov and Black 2016). In recent years, the demand in the international business has

increased a lot which forced the accounting users to record their transaction and financial report

according to the international market. It created a lot of pressure and more time consuming for

the accountant to keep the record. Even the small companies has to consider the international

accounting standard which has not only created work pressure but also increase the cost. All of

this caused the major reason for the establishment of the single set of global accounting standard.

Some of the advantages of single set of global accounting standard are as follows:

Comparability – It is one of the biggest advantage of the single global accounting

standard. It helps to compare the business on basis of the same accounting standard.

International expansion – With the Single set of global accounting standard it will

remove the barriers of expansion for companies. Companies who want to expand in the

overseas business need to consider the international standards by completely adopting the

new set of accounting. In some cases, the cost of accounts maintenance of the company

also increases specially in the small organization.

Central authoritative body – This single standard rule helps to build a single policy which

is the only authority body to rule the standard. Currently there are different sets of

accounting standard in different country. With this new standard it will reduce the

disagreement between the countries and international regulators.

8

CORPORATE ACCOUNTING

Cost reduction – By adopting the single set of accounting standard the cost of marinating

accounting standard will reduce as the workload will reduce. It may not affect the large

organization but small organization will be largely benefited from it.

Easy transition – With the global standard the transition will get easier as it developed as

self-contained guide for all small and medium size organization. It will remove many

level of complexity which is faced due to the accounting standard (Balakrishnan, Watts and

Zuo 2016).

Convergence – Some of the small organization may adopt the change slowly according to

their accounting practice while some may move gradually to reduce their financial

impact. Both generally accepted accounting policy and international financial reporting

standard helps the international accounting standard. Both of them are considered to

adopt, reject or modify any new rules as it provides the basis of decision making for the

new single set of global accounting standard.

CORPORATE ACCOUNTING

Cost reduction – By adopting the single set of accounting standard the cost of marinating

accounting standard will reduce as the workload will reduce. It may not affect the large

organization but small organization will be largely benefited from it.

Easy transition – With the global standard the transition will get easier as it developed as

self-contained guide for all small and medium size organization. It will remove many

level of complexity which is faced due to the accounting standard (Balakrishnan, Watts and

Zuo 2016).

Convergence – Some of the small organization may adopt the change slowly according to

their accounting practice while some may move gradually to reduce their financial

impact. Both generally accepted accounting policy and international financial reporting

standard helps the international accounting standard. Both of them are considered to

adopt, reject or modify any new rules as it provides the basis of decision making for the

new single set of global accounting standard.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CORPORATE ACCOUNTING

Reference list

Agrawal, A. and Cooper, T., 2017. Corporate governance consequences of accounting scandals:

Evidence from top management, CFO and auditor turnover. Quarterly Journal of Finance, 7(01),

p.1650014.

Atanasov, V.A. and Black, B.S., 2016. Shock-based causal inference in corporate finance and

accounting research. Critical Finance Review, 5, pp.207-304.

Balakrishnan, K., Watts, R. and Zuo, L., 2016. The effect of accounting conservatism on

corporate investment during the global financial crisis. Journal of Business Finance &

Accounting, 43(5-6), pp.513-542.

Guenther, E., Jasch, C., Schmidt, M., Wagner, B. and Ilg, P., 2015. Material Flow Cost

Accounting–looking back and ahead.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production, 136, pp.237-

248.

Mitchell, R.K., Van Buren III, H.J., Greenwood, M. and Freeman, R.E., 2015. Stakeholder

inclusion and accounting for stakeholders. Journal of Management Studies, 52(7), pp.851-877.

Mokhtar, N., Jusoh, R. and Zulkifli, N., 2016. Corporate characteristics and environmental

management accounting (EMA) implementation: evidence from Malaysian public listed

companies (PLCs). Journal of Cleaner Production, 136, pp.111-122.

O'Dwyer, B. and Unerman, J., 2016. Fostering rigour in accounting for social

sustainability. Accounting, Organizations and Society, 49, pp.32-40.

CORPORATE ACCOUNTING

Reference list

Agrawal, A. and Cooper, T., 2017. Corporate governance consequences of accounting scandals:

Evidence from top management, CFO and auditor turnover. Quarterly Journal of Finance, 7(01),

p.1650014.

Atanasov, V.A. and Black, B.S., 2016. Shock-based causal inference in corporate finance and

accounting research. Critical Finance Review, 5, pp.207-304.

Balakrishnan, K., Watts, R. and Zuo, L., 2016. The effect of accounting conservatism on

corporate investment during the global financial crisis. Journal of Business Finance &

Accounting, 43(5-6), pp.513-542.

Guenther, E., Jasch, C., Schmidt, M., Wagner, B. and Ilg, P., 2015. Material Flow Cost

Accounting–looking back and ahead.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production, 136, pp.237-

248.

Mitchell, R.K., Van Buren III, H.J., Greenwood, M. and Freeman, R.E., 2015. Stakeholder

inclusion and accounting for stakeholders. Journal of Management Studies, 52(7), pp.851-877.

Mokhtar, N., Jusoh, R. and Zulkifli, N., 2016. Corporate characteristics and environmental

management accounting (EMA) implementation: evidence from Malaysian public listed

companies (PLCs). Journal of Cleaner Production, 136, pp.111-122.

O'Dwyer, B. and Unerman, J., 2016. Fostering rigour in accounting for social

sustainability. Accounting, Organizations and Society, 49, pp.32-40.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CORPORATE ACCOUNTING

Saeidi, S.P., Sofian, S., Saeidi, P., Saeidi, S.P. and Saaeidi, S.A., 2015. How does corporate

social responsibility contribute to firm financial performance? The mediating role of competitive

advantage, reputation, and customer satisfaction. Journal of business research, 68(2), pp.341-

350.

Schaltegger, S., Etxeberria, I.Á. and Ortas, E., 2017. Innovating corporate accounting and

reporting for sustainability–attributes and challenges. Sustainable Development, 25(2), pp.113-

122.

Waniak-Michalak, H., Macuda, M. and Krasodomskac, J., 2016. Corporate social responsibility

and accounting in Poland: A literature review. Accounting and Management Information

Systems, 15(2), p.255.

Watson, L., 2015. Corporate social responsibility research in accounting. Journal of Accounting

Literature, 34, pp.1-16.

CORPORATE ACCOUNTING

Saeidi, S.P., Sofian, S., Saeidi, P., Saeidi, S.P. and Saaeidi, S.A., 2015. How does corporate

social responsibility contribute to firm financial performance? The mediating role of competitive

advantage, reputation, and customer satisfaction. Journal of business research, 68(2), pp.341-

350.

Schaltegger, S., Etxeberria, I.Á. and Ortas, E., 2017. Innovating corporate accounting and

reporting for sustainability–attributes and challenges. Sustainable Development, 25(2), pp.113-

122.

Waniak-Michalak, H., Macuda, M. and Krasodomskac, J., 2016. Corporate social responsibility

and accounting in Poland: A literature review. Accounting and Management Information

Systems, 15(2), p.255.

Watson, L., 2015. Corporate social responsibility research in accounting. Journal of Accounting

Literature, 34, pp.1-16.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.