Financial Report: Corporate Accounting Analysis of Myer & Kathmandu

VerifiedAdded on 2023/06/04

|18

|4140

|468

Report

AI Summary

This report provides a detailed analysis of the corporate accounting practices of Myer Limited and Kathmandu Limited, two companies listed on the Australian Securities Exchange (ASX) within the same industry. The analysis focuses on key aspects of their financial statements, including owner's equity, cash flow statements, and the relationship between debt and equity. The report identifies and explains the various equity items for both companies, such as contributed equity, retained earnings, and reserves, discussing changes in these items from 2016 to 2017. Furthermore, it conducts a comparative analysis of the debt and equity positions of the two firms, calculating their debt-to-equity ratios to assess their capital structures. The cash flow statements are examined to understand the companies' cash inflows and outflows from operating, investing, and financing activities, with a comparative analysis highlighting the changes in cash flow positions between the years. The report concludes by summarizing the key findings and providing insights into the corporate accounting practices of Myer and Kathmandu Limited.

Running Head: Corporate Accounting

1

Project Report: Corporate Accounting

1

Project Report: Corporate Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

2

Executive summary

This report has been prepared in order to identify the process and the importance of

the corporate accounting in an organization. This report mainly concentrates on the recording

and the presentation of various accounting transaction and the figures in the annual report of

the company. In this report, the Myer limited and Kathmandu limited has been taken into

context to measure and identify their corporate accounting process. If an organization does

not focus on the corporate accounting process than the social accountability of the business

becomes lower. All the main figures and the recording has been studied and evaluated in the

report.

2

Executive summary

This report has been prepared in order to identify the process and the importance of

the corporate accounting in an organization. This report mainly concentrates on the recording

and the presentation of various accounting transaction and the figures in the annual report of

the company. In this report, the Myer limited and Kathmandu limited has been taken into

context to measure and identify their corporate accounting process. If an organization does

not focus on the corporate accounting process than the social accountability of the business

becomes lower. All the main figures and the recording has been studied and evaluated in the

report.

Corporate Accounting

3

Contents

Introduction.......................................................................................................................5

Company overview...........................................................................................................5

Myer limited.................................................................................................................5

Kathmandu limited.......................................................................................................5

Owner’s equity..................................................................................................................6

i. List of the equity items.........................................................................................6

ii. Debt and equity position......................................................................................7

Cash flow statement..........................................................................................................8

iii. List of the cash flow items...................................................................................8

iv. Comparative analysis.........................................................................................10

v. Comparison........................................................................................................10

Comprehensive income statement..................................................................................11

vi. List of the comprehensive income statement items...........................................11

vii. Why not added in the P&L a/c.......................................................................12

viii. Comparative analysis......................................................................................13

ix. Performance of manager’s evaluation................................................................13

Accounting for corporate income tax.............................................................................13

x. Taxation expenses of the company....................................................................13

xi. Effective tax rate calculations and analysis.......................................................14

xii. Deferred tax assets and liabilities...................................................................14

xiii. Changes in DTA and DTL.............................................................................14

xiv. Calculate of cash tax amount..........................................................................15

xv. Cash tax rate...................................................................................................15

3

Contents

Introduction.......................................................................................................................5

Company overview...........................................................................................................5

Myer limited.................................................................................................................5

Kathmandu limited.......................................................................................................5

Owner’s equity..................................................................................................................6

i. List of the equity items.........................................................................................6

ii. Debt and equity position......................................................................................7

Cash flow statement..........................................................................................................8

iii. List of the cash flow items...................................................................................8

iv. Comparative analysis.........................................................................................10

v. Comparison........................................................................................................10

Comprehensive income statement..................................................................................11

vi. List of the comprehensive income statement items...........................................11

vii. Why not added in the P&L a/c.......................................................................12

viii. Comparative analysis......................................................................................13

ix. Performance of manager’s evaluation................................................................13

Accounting for corporate income tax.............................................................................13

x. Taxation expenses of the company....................................................................13

xi. Effective tax rate calculations and analysis.......................................................14

xii. Deferred tax assets and liabilities...................................................................14

xiii. Changes in DTA and DTL.............................................................................14

xiv. Calculate of cash tax amount..........................................................................15

xv. Cash tax rate...................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting

4

xvi. Book and cash tax rate....................................................................................16

Conclusion......................................................................................................................16

References.......................................................................................................................17

4

xvi. Book and cash tax rate....................................................................................16

Conclusion......................................................................................................................16

References.......................................................................................................................17

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

5

Introduction:

The corporate accounting process is the part of accounting. The main focus of

corporate accounting is on the accounting treatment of all the financial figures and the

activities of the business. The corporate accounting is mainly inspired by the accounting

standards and the accounting policies. It explains that an organization is required to manage

and record all the financial figures and the accounting transactions of the business in better

and described way so that it becomes easier for the managers, employs, customers, suppliers,

investors and the other stakeholders of the business to measure the overall performance of the

business (Gorry, Hassett, Hubbard and Mathur, 2017).

Corporate accounting keeps a track on the financial statement and recording process

of the company in order to follow the proper accounting guidelines. In this report, the Myer

limited and Kathmandu limited has been taken into context to measure and identify their

corporate accounting process. The financial items of the business and the relevant financial

notes of the business have been studied in the report to evaluate the performance of corporate

accounting in an organization.

Company overview:

The brief description of both the companies is as follows:

Myer limited:

Myer limited is a retail company. The head market of the company is Australia. It is

an upmarket departmental store in the Australian states. The company is also a self governing

territory among the two territories of Australia. The main product and services of the business

includes variety of products such as children’s clothing, footwear, accessories, electrical

products etc. the company also deals in the home products, electronic products etc. the

company has been funded 118 years back in 1900. Total 14000 people are working with the

company to help and run the business (Home, 2018).

Kathmandu limited:

Kathmandu limited is also a retail company. The company is operating its business in

the Australian and New Zealand market. It is a transactional chain in the Australian states.

The company is one of the transactional chains in Australia. The main product and services of

5

Introduction:

The corporate accounting process is the part of accounting. The main focus of

corporate accounting is on the accounting treatment of all the financial figures and the

activities of the business. The corporate accounting is mainly inspired by the accounting

standards and the accounting policies. It explains that an organization is required to manage

and record all the financial figures and the accounting transactions of the business in better

and described way so that it becomes easier for the managers, employs, customers, suppliers,

investors and the other stakeholders of the business to measure the overall performance of the

business (Gorry, Hassett, Hubbard and Mathur, 2017).

Corporate accounting keeps a track on the financial statement and recording process

of the company in order to follow the proper accounting guidelines. In this report, the Myer

limited and Kathmandu limited has been taken into context to measure and identify their

corporate accounting process. The financial items of the business and the relevant financial

notes of the business have been studied in the report to evaluate the performance of corporate

accounting in an organization.

Company overview:

The brief description of both the companies is as follows:

Myer limited:

Myer limited is a retail company. The head market of the company is Australia. It is

an upmarket departmental store in the Australian states. The company is also a self governing

territory among the two territories of Australia. The main product and services of the business

includes variety of products such as children’s clothing, footwear, accessories, electrical

products etc. the company also deals in the home products, electronic products etc. the

company has been funded 118 years back in 1900. Total 14000 people are working with the

company to help and run the business (Home, 2018).

Kathmandu limited:

Kathmandu limited is also a retail company. The company is operating its business in

the Australian and New Zealand market. It is a transactional chain in the Australian states.

The company is one of the transactional chains in Australia. The main product and services of

Corporate Accounting

6

the business includes variety of products such as apparel, equipment etc. the company also

deals in the outdoor product etc. the company has been funded 31 years back in 1987 (Home,

2018). Total 2000 people are working with the company to help and run the business.

Owner’s equity:

The owner’s equity is a financial head which is shown in the balance sheet of an

organization under the liability and shareholder head. It describes about the total fund which

has been generated and managed by the business through selling the ownership and the profit

amount of the business.

i. List of the equity items:

The equity items describe the funds which are managed by the business to run the

business and invest into the long term projects to improve the return level of the business. On

the basis of the study on annual report (2017) of Myer limited and Kathmandu limited, it has

been found that the equity items of the companies are contributed equity, reserves and

retained earnings. The contributed equity defines the investment done by the shareholders in

the company. The equity position of Myer and Kathmandu limited has been changed by

0.00% and 0.01% from 2016 in 2017.

In addition, the retained earnings stand for the few % from the net profit of an

organization which is kept by the company and not paid to the shareholder as dividend. This

amount is kept for the business activities. The retained earnings position of Myer limited has

been reduced by 9.84% and in case of Kathmandu limited, the retained earnings have been

improved by 10.19%. Lastly, the reserve is the amount which is maintained for the business

to compensate the sudden loss of the business (Gorry, Hassett, Hubbard and Mathur, 2017).

The reserve level of both the companies depict about the reduction from last year. The below

table represent the equity items and the changes which has occurred into the performance of

the business.

Equity Items

Myer Limited Kathmandu Limited

AUD in '000 2017 2016 Changes 2017 2016 Changes

Stockholders' equity

Contributed equity 739329 739338 0.00% 200209 200191 0.01%

Retained earnings 342146 379483 -9.84% 149893 136033 10.19%

Reserves -8607 -11056 -22.15% -23002 -24541 -6.27%

6

the business includes variety of products such as apparel, equipment etc. the company also

deals in the outdoor product etc. the company has been funded 31 years back in 1987 (Home,

2018). Total 2000 people are working with the company to help and run the business.

Owner’s equity:

The owner’s equity is a financial head which is shown in the balance sheet of an

organization under the liability and shareholder head. It describes about the total fund which

has been generated and managed by the business through selling the ownership and the profit

amount of the business.

i. List of the equity items:

The equity items describe the funds which are managed by the business to run the

business and invest into the long term projects to improve the return level of the business. On

the basis of the study on annual report (2017) of Myer limited and Kathmandu limited, it has

been found that the equity items of the companies are contributed equity, reserves and

retained earnings. The contributed equity defines the investment done by the shareholders in

the company. The equity position of Myer and Kathmandu limited has been changed by

0.00% and 0.01% from 2016 in 2017.

In addition, the retained earnings stand for the few % from the net profit of an

organization which is kept by the company and not paid to the shareholder as dividend. This

amount is kept for the business activities. The retained earnings position of Myer limited has

been reduced by 9.84% and in case of Kathmandu limited, the retained earnings have been

improved by 10.19%. Lastly, the reserve is the amount which is maintained for the business

to compensate the sudden loss of the business (Gorry, Hassett, Hubbard and Mathur, 2017).

The reserve level of both the companies depict about the reduction from last year. The below

table represent the equity items and the changes which has occurred into the performance of

the business.

Equity Items

Myer Limited Kathmandu Limited

AUD in '000 2017 2016 Changes 2017 2016 Changes

Stockholders' equity

Contributed equity 739329 739338 0.00% 200209 200191 0.01%

Retained earnings 342146 379483 -9.84% 149893 136033 10.19%

Reserves -8607 -11056 -22.15% -23002 -24541 -6.27%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting

7

Total stockholder's

equity

1072868 1107765 -3.15% 327100 311683 4.95%

ii. Debt and equity position:

Debt and equity position describe the capital structure position of a company. A

business is always required to manage the optimal capital structure of the business where the

risk position and the cost position of the business is lower in order to improve the investment

position and reduce the financial risk position of the business. The debt and equity weight

must be maintained by the business in such a way that the cost of capital of the business

could be reduced and the financial leverage position of the business could also be lowered

(Rees and Shane, 2012).

In order to evaluate the debt and equity position of Myer limited and Kathmandu

limited, the long term debt and equity worth of both the business has been calculated from the

annual report of the business to evaluate the capital structure position of the business.

Through the calculations on Myer limited, the debt equity position of the company is 29.70%

which expresses that the financial gearing ratio of the business is lower. Though the cost

position of the company is higher and still, in the industry the position of the company is

competitive (Annual report, 2017).

Further, in case of Kathmandu limited, the debt weight of the company against the

total equity amount is 13.67%. It describes that the main focus of the company is on the

equity level only in order to reduce the risk position of the company. But along with this, the

cost of the company has been higher. The annual report (2017) explains that the director has

depicted to make improvements in the capital structure to maintain the overall position of risk

and cost of the business.

Debt / Equity calculations

Myer

Limited

Kathmandu

Limited

AUD in '000 2017 2017

Long term

debt 318647 44723

Equity 1072868 327100

Debt / Equity 29.70% 13.67%

7

Total stockholder's

equity

1072868 1107765 -3.15% 327100 311683 4.95%

ii. Debt and equity position:

Debt and equity position describe the capital structure position of a company. A

business is always required to manage the optimal capital structure of the business where the

risk position and the cost position of the business is lower in order to improve the investment

position and reduce the financial risk position of the business. The debt and equity weight

must be maintained by the business in such a way that the cost of capital of the business

could be reduced and the financial leverage position of the business could also be lowered

(Rees and Shane, 2012).

In order to evaluate the debt and equity position of Myer limited and Kathmandu

limited, the long term debt and equity worth of both the business has been calculated from the

annual report of the business to evaluate the capital structure position of the business.

Through the calculations on Myer limited, the debt equity position of the company is 29.70%

which expresses that the financial gearing ratio of the business is lower. Though the cost

position of the company is higher and still, in the industry the position of the company is

competitive (Annual report, 2017).

Further, in case of Kathmandu limited, the debt weight of the company against the

total equity amount is 13.67%. It describes that the main focus of the company is on the

equity level only in order to reduce the risk position of the company. But along with this, the

cost of the company has been higher. The annual report (2017) explains that the director has

depicted to make improvements in the capital structure to maintain the overall position of risk

and cost of the business.

Debt / Equity calculations

Myer

Limited

Kathmandu

Limited

AUD in '000 2017 2017

Long term

debt 318647 44723

Equity 1072868 327100

Debt / Equity 29.70% 13.67%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

8

(Annual report, 2017)

Cash flow statement:

The cash flow statement is a financial statement which is shown in annual report and

prepared after the statement of financial position and financial performance. It describes

about the total cash outflows and inflows of the company which has been generated and paid

by the business in a particular time period.

iii. List of the cash flow items:

The cash flow items describe the funds which has been either paid or received by the

business in a particular time period and these transactions are related to the business, its

activities and the financial position. On the basis of the study on annual report (2017) of

Myer limited and Kathmandu limited, it has been found that the cash flow items of the

companies are investment into the PPE, subsidiary businesses, amount received from the

customers and paid to the suppliers, dividend amount paid, issues of shares, proceed of

borrowings, buy back of shares etc. The cash flow statement defines the cash position of the

company.

Figure 1: Cash flow statement of Myer

On the basis of the figure 1, it has been measured that the receipts from the customer

defines the cash inflows which has been received by the business. The reduction has been

8

(Annual report, 2017)

Cash flow statement:

The cash flow statement is a financial statement which is shown in annual report and

prepared after the statement of financial position and financial performance. It describes

about the total cash outflows and inflows of the company which has been generated and paid

by the business in a particular time period.

iii. List of the cash flow items:

The cash flow items describe the funds which has been either paid or received by the

business in a particular time period and these transactions are related to the business, its

activities and the financial position. On the basis of the study on annual report (2017) of

Myer limited and Kathmandu limited, it has been found that the cash flow items of the

companies are investment into the PPE, subsidiary businesses, amount received from the

customers and paid to the suppliers, dividend amount paid, issues of shares, proceed of

borrowings, buy back of shares etc. The cash flow statement defines the cash position of the

company.

Figure 1: Cash flow statement of Myer

On the basis of the figure 1, it has been measured that the receipts from the customer

defines the cash inflows which has been received by the business. The reduction has been

Corporate Accounting

9

seen in that level and along with that, the payment of the company has also been reduced.

Though, it has been found that the overall position of the operating cash flow of the company

has been reduced.

Further, the investing cash flow contains the activities which are related to the

investment into the new plants, building, fixed assets and the subsidiaries of the business. The

investing cash position of Myer limited has been reduced because of the higher investment

into PPE and intangible assets of the business (Annual report, 2017). Lastly, the investing

cash flow contains the activities which are related to the investment into the new plants,

building, fixed assets and the subsidiaries of the business. The investing cash position of

Myer limited has been reduced because of the higher investment into PPE and intangible

assets of the business.

Figure 2: Cash flow statement of Kathmandu

On the basis of the figure 2, the improvement has been seen in the receipts from

customers and along with that, the payment of the company has also been increased. Though,

it has been found that the overall position of the operating cash flow of the company has been

reduced (Bardley, 2007).

9

seen in that level and along with that, the payment of the company has also been reduced.

Though, it has been found that the overall position of the operating cash flow of the company

has been reduced.

Further, the investing cash flow contains the activities which are related to the

investment into the new plants, building, fixed assets and the subsidiaries of the business. The

investing cash position of Myer limited has been reduced because of the higher investment

into PPE and intangible assets of the business (Annual report, 2017). Lastly, the investing

cash flow contains the activities which are related to the investment into the new plants,

building, fixed assets and the subsidiaries of the business. The investing cash position of

Myer limited has been reduced because of the higher investment into PPE and intangible

assets of the business.

Figure 2: Cash flow statement of Kathmandu

On the basis of the figure 2, the improvement has been seen in the receipts from

customers and along with that, the payment of the company has also been increased. Though,

it has been found that the overall position of the operating cash flow of the company has been

reduced (Bardley, 2007).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting

10

Further, the investing cash flow has been improved from the last year because of the

reduction into the investment position of the business. Lastly, the financial cash flow contains

the higher expenses of the business. It explains that the overall cash position of the business

has been changed.

iv. Comparative analysis:

The main cash flows of both the companies have been evaluated further. On the basis

of the below table, it has been recognized that the operating activities of both the companies

have been improved by 54.03% and 127.07%. Along with that the cash outflow from the

investing activities of Myer limited has been improved and the cash outflow of Kathmandu

limited has been reduced (Gorry, Hassett, Hubbard and Mathur, 2017). Lastly, the cash

outflow from the financing activities of Myer limited has been reduced and the cash outflow

of Kathmandu limited has been improved. It explains that the changes have seen in both the

companies.

Myer Limited Kathmandu Limited

AUD in '000 2017 2016 2015 Changes 2017 2016 2015 Changes

Net cash used for operating

activities 149278 149490 96915 54.03% 67273 69080 29627 127.07%

Net cash used for investing

activities -109456 -58251 -62350 75.55% -13275 -23191 -19980 -33.56%

Net cash provided by (used

for) financing activities -54438 -99355 -54806 -0.67% -57382 -40730 -14898 285.17%

(Annual report, 2017)

v. Comparison:

The cash position of both the companies has been compared with each other. On the

basis of the evaluation, it has been recognized that the Kathmandu limited has made better

changes into its cash inflow position and due to which the cash position of the business has

been improved. The below table better explains the changes and the comparison of both the

companies:

Myer Limited Kathmandu Limited

AUD in '000 2017 2016 Changes 2017 2016 Changes

Net cash used for operating

activities 149278 149490 -0.14% 67273 69080 -2.62%

Net cash used for investing

activities

-

109456 -58251 87.90%

-

13275

-

23191 -42.76%

10

Further, the investing cash flow has been improved from the last year because of the

reduction into the investment position of the business. Lastly, the financial cash flow contains

the higher expenses of the business. It explains that the overall cash position of the business

has been changed.

iv. Comparative analysis:

The main cash flows of both the companies have been evaluated further. On the basis

of the below table, it has been recognized that the operating activities of both the companies

have been improved by 54.03% and 127.07%. Along with that the cash outflow from the

investing activities of Myer limited has been improved and the cash outflow of Kathmandu

limited has been reduced (Gorry, Hassett, Hubbard and Mathur, 2017). Lastly, the cash

outflow from the financing activities of Myer limited has been reduced and the cash outflow

of Kathmandu limited has been improved. It explains that the changes have seen in both the

companies.

Myer Limited Kathmandu Limited

AUD in '000 2017 2016 2015 Changes 2017 2016 2015 Changes

Net cash used for operating

activities 149278 149490 96915 54.03% 67273 69080 29627 127.07%

Net cash used for investing

activities -109456 -58251 -62350 75.55% -13275 -23191 -19980 -33.56%

Net cash provided by (used

for) financing activities -54438 -99355 -54806 -0.67% -57382 -40730 -14898 285.17%

(Annual report, 2017)

v. Comparison:

The cash position of both the companies has been compared with each other. On the

basis of the evaluation, it has been recognized that the Kathmandu limited has made better

changes into its cash inflow position and due to which the cash position of the business has

been improved. The below table better explains the changes and the comparison of both the

companies:

Myer Limited Kathmandu Limited

AUD in '000 2017 2016 Changes 2017 2016 Changes

Net cash used for operating

activities 149278 149490 -0.14% 67273 69080 -2.62%

Net cash used for investing

activities

-

109456 -58251 87.90%

-

13275

-

23191 -42.76%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

11

Net cash provided by (used for)

financing activities -54438 -99355 -45.21%

-

57382

-

40730 40.88%

(Annual report, 2017)

Comprehensive income statement:

The comprehensive income statement is a one of the financial statement which is

prepared and shown in the annual report of a company. It describes about those items which

is not added in the profit and loss statement even though they affect the profit position of an

organization. It describes about the total fund and profit which has been affected due to other

factors of the business.

vi. List of the comprehensive income statement items:

The item list is as follows:

Figure 3: Comprehensive income statement of Myer limited

11

Net cash provided by (used for)

financing activities -54438 -99355 -45.21%

-

57382

-

40730 40.88%

(Annual report, 2017)

Comprehensive income statement:

The comprehensive income statement is a one of the financial statement which is

prepared and shown in the annual report of a company. It describes about those items which

is not added in the profit and loss statement even though they affect the profit position of an

organization. It describes about the total fund and profit which has been affected due to other

factors of the business.

vi. List of the comprehensive income statement items:

The item list is as follows:

Figure 3: Comprehensive income statement of Myer limited

Corporate Accounting

12

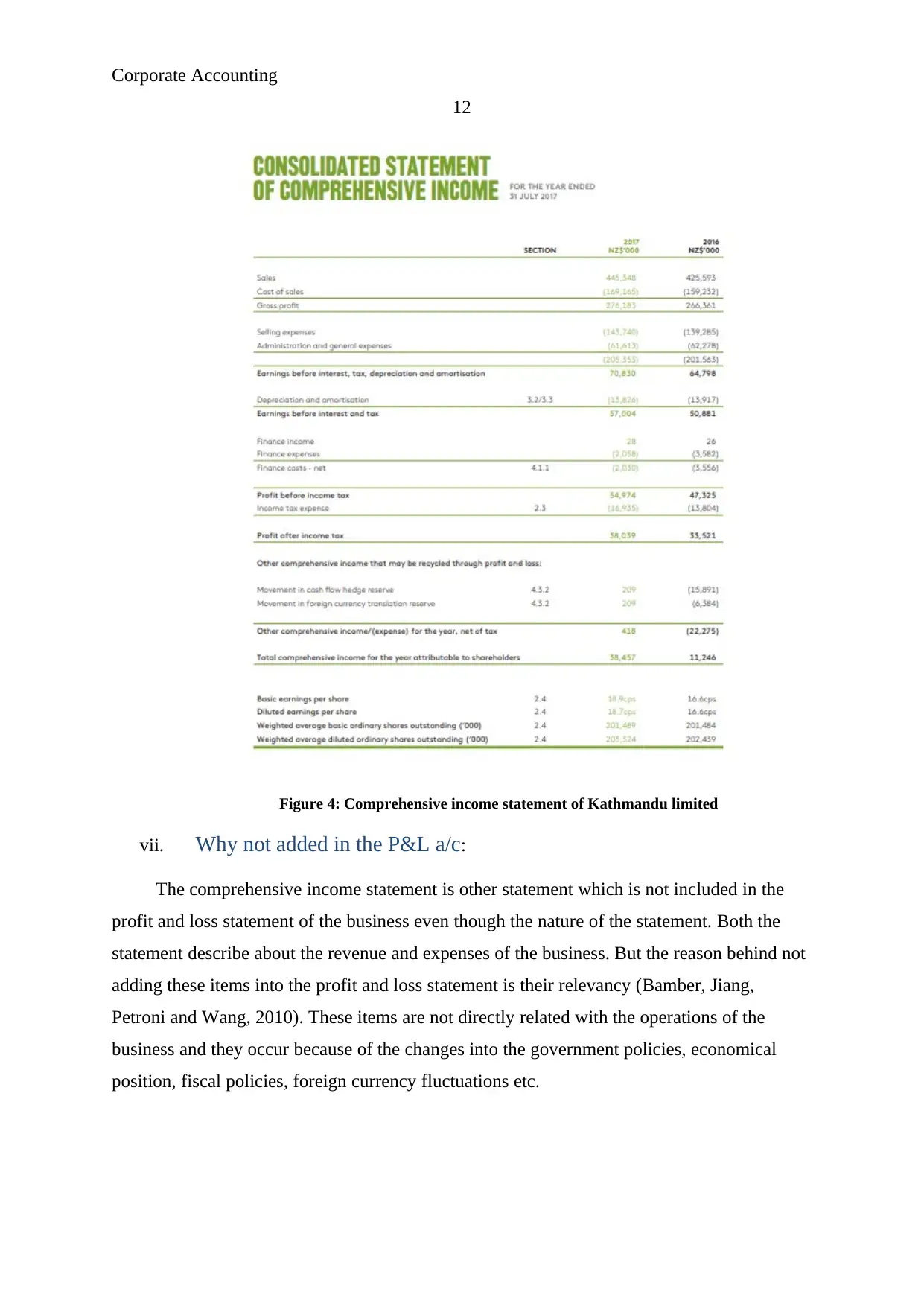

Figure 4: Comprehensive income statement of Kathmandu limited

vii. Why not added in the P&L a/c:

The comprehensive income statement is other statement which is not included in the

profit and loss statement of the business even though the nature of the statement. Both the

statement describe about the revenue and expenses of the business. But the reason behind not

adding these items into the profit and loss statement is their relevancy (Bamber, Jiang,

Petroni and Wang, 2010). These items are not directly related with the operations of the

business and they occur because of the changes into the government policies, economical

position, fiscal policies, foreign currency fluctuations etc.

12

Figure 4: Comprehensive income statement of Kathmandu limited

vii. Why not added in the P&L a/c:

The comprehensive income statement is other statement which is not included in the

profit and loss statement of the business even though the nature of the statement. Both the

statement describe about the revenue and expenses of the business. But the reason behind not

adding these items into the profit and loss statement is their relevancy (Bamber, Jiang,

Petroni and Wang, 2010). These items are not directly related with the operations of the

business and they occur because of the changes into the government policies, economical

position, fiscal policies, foreign currency fluctuations etc.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.