Corporate Financial Accounting Analysis of Myer Limited, Australia

VerifiedAdded on 2023/06/12

|13

|2550

|373

Report

AI Summary

This report provides a comprehensive financial analysis of Myer Limited, an Australian departmental store company, focusing on its tax position, cash flow, and financial statements. It examines the company's cash flow statement, comparing operating, investing, and financing activities across multiple years, and analyzes the comprehensive income statement, highlighting items like exchange rate differences and cash flow hedges. The report also delves into the company's tax expenses, deferred tax items, and the differences between accounting profit and taxable income, referencing AASB 112 rules. Furthermore, it explores the discrepancies between income tax amounts in the income statement, balance sheet, and cash flow statement, offering insights into their recording and treatment. The analysis reveals that the company's cash inflow position is decreasing and that various non-deductible losses and asset impairments impact its taxation figures.

RUNNING HEAD: Corporate Financial Accounting

1

Name of the student-

Topic-Corporate Financial Accounting

University name

1

Name of the student-

Topic-Corporate Financial Accounting

University name

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Financial Accounting

2

Contents

Introduction................................................................................................................................3

Answer to question-1.................................................................................................................3

Answer to question-2.................................................................................................................4

Comparative analysis of the all three main flow of activities................................................4

Answer to question no-3............................................................................................................5

Answer to question no-4............................................................................................................6

Answer to question no-5............................................................................................................6

Answer to question no-6............................................................................................................6

Answer to question no-7............................................................................................................7

Answer to question no-8............................................................................................................8

Answer to question no-9..........................................................................................................10

Answer to question no-10........................................................................................................10

Answer to question no-11........................................................................................................10

References................................................................................................................................12

2

Contents

Introduction................................................................................................................................3

Answer to question-1.................................................................................................................3

Answer to question-2.................................................................................................................4

Comparative analysis of the all three main flow of activities................................................4

Answer to question no-3............................................................................................................5

Answer to question no-4............................................................................................................6

Answer to question no-5............................................................................................................6

Answer to question no-6............................................................................................................6

Answer to question no-7............................................................................................................7

Answer to question no-8............................................................................................................8

Answer to question no-9..........................................................................................................10

Answer to question no-10........................................................................................................10

Answer to question no-11........................................................................................................10

References................................................................................................................................12

Corporate Financial Accounting

3

Introduction

The report has been prepared to evaluate the tax amount, deferred tax amount,

financial statement, tax provisions and various other tax activities and the figures of an

Australian company, Myer limited. The economy and the industry of Australian market has

changed a lot and it explains that with the changes, it becomes important for an auditor as

well as an accountant to measure the changes and apply it while preparing and auditing the

annual report of the company.

Myer limited is a departmental store company in Australian market; the company offers

the services and the products through its 60 stores all over the Australia. The company has

launched 11 categories of clothes for woman, man and child. It has also diversified into

toiletry produces (Reuters, 2018). The company’s annual report (2017) explains that the

performance of the company has been altered due to changes into the industry and the

economical changes in the company.

Answer to question-1

Analysis of the Cash flow statement

Analysis over the cash flow statement is a crucial process as it evaluates all the factors

of the company related to the cash outflow and cash inflow of the company and it measures

that whether the recordings of all the cash activities of the company have been done by the

company in better way or not. Operating cash flows, investing cash flows and operating cash

flows of the company are main segment which explains about the different cash outflows and

inflows of the company (McKee, 2005).

The operating cash flows, investing cash flows and operating cash flows of the

company are evaluated to recognize the changes which have occurred. The cash flow

statement explains that the investments and the purchase of new assets for the business and

the operations of the company have reduced the cash flow of the company. The statement

3

Introduction

The report has been prepared to evaluate the tax amount, deferred tax amount,

financial statement, tax provisions and various other tax activities and the figures of an

Australian company, Myer limited. The economy and the industry of Australian market has

changed a lot and it explains that with the changes, it becomes important for an auditor as

well as an accountant to measure the changes and apply it while preparing and auditing the

annual report of the company.

Myer limited is a departmental store company in Australian market; the company offers

the services and the products through its 60 stores all over the Australia. The company has

launched 11 categories of clothes for woman, man and child. It has also diversified into

toiletry produces (Reuters, 2018). The company’s annual report (2017) explains that the

performance of the company has been altered due to changes into the industry and the

economical changes in the company.

Answer to question-1

Analysis of the Cash flow statement

Analysis over the cash flow statement is a crucial process as it evaluates all the factors

of the company related to the cash outflow and cash inflow of the company and it measures

that whether the recordings of all the cash activities of the company have been done by the

company in better way or not. Operating cash flows, investing cash flows and operating cash

flows of the company are main segment which explains about the different cash outflows and

inflows of the company (McKee, 2005).

The operating cash flows, investing cash flows and operating cash flows of the

company are evaluated to recognize the changes which have occurred. The cash flow

statement explains that the investments and the purchase of new assets for the business and

the operations of the company have reduced the cash flow of the company. The statement

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Financial Accounting

4

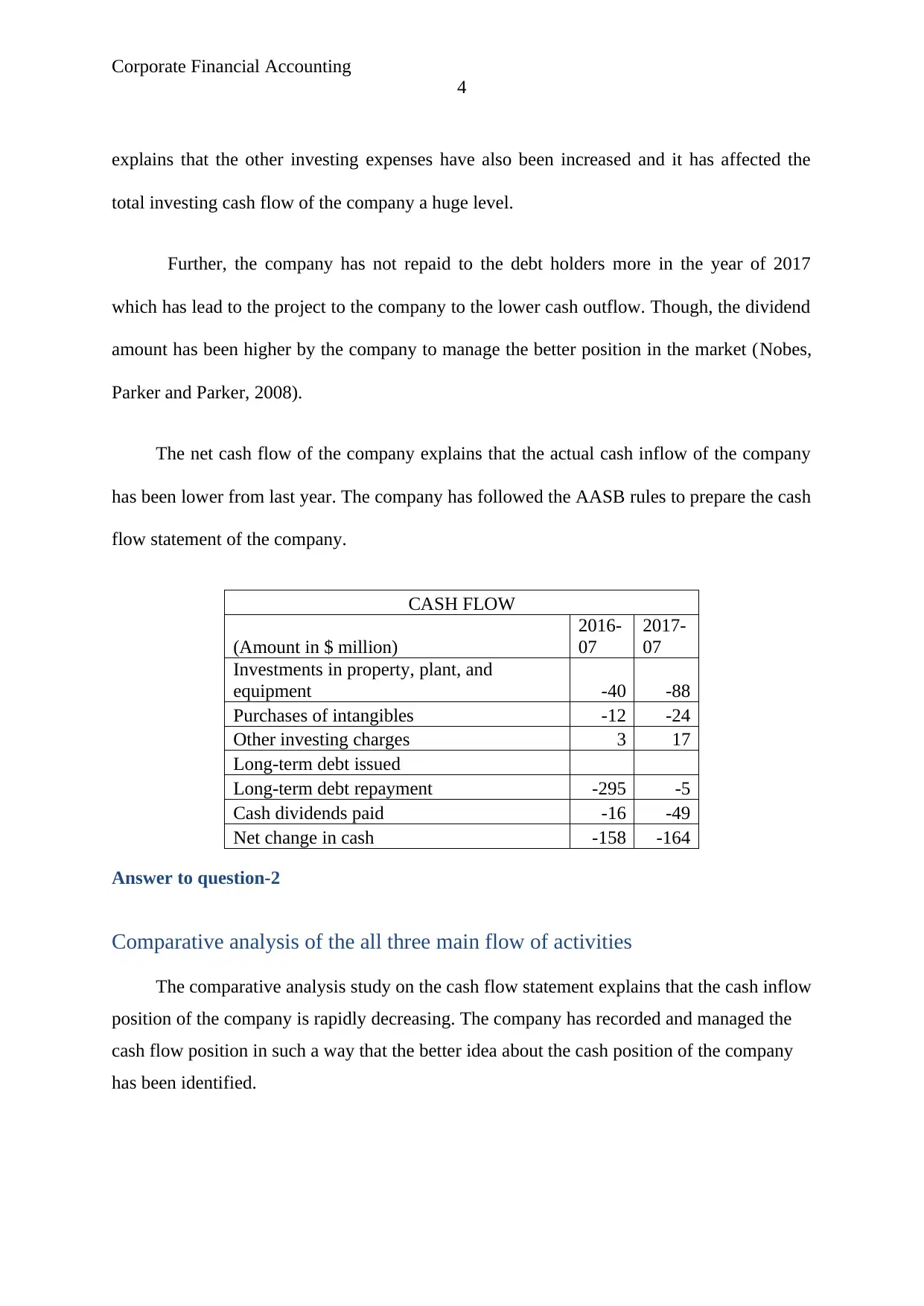

explains that the other investing expenses have also been increased and it has affected the

total investing cash flow of the company a huge level.

Further, the company has not repaid to the debt holders more in the year of 2017

which has lead to the project to the company to the lower cash outflow. Though, the dividend

amount has been higher by the company to manage the better position in the market (Nobes,

Parker and Parker, 2008).

The net cash flow of the company explains that the actual cash inflow of the company

has been lower from last year. The company has followed the AASB rules to prepare the cash

flow statement of the company.

CASH FLOW

(Amount in $ million)

2016-

07

2017-

07

Investments in property, plant, and

equipment -40 -88

Purchases of intangibles -12 -24

Other investing charges 3 17

Long-term debt issued

Long-term debt repayment -295 -5

Cash dividends paid -16 -49

Net change in cash -158 -164

Answer to question-2

Comparative analysis of the all three main flow of activities

The comparative analysis study on the cash flow statement explains that the cash inflow

position of the company is rapidly decreasing. The company has recorded and managed the

cash flow position in such a way that the better idea about the cash position of the company

has been identified.

4

explains that the other investing expenses have also been increased and it has affected the

total investing cash flow of the company a huge level.

Further, the company has not repaid to the debt holders more in the year of 2017

which has lead to the project to the company to the lower cash outflow. Though, the dividend

amount has been higher by the company to manage the better position in the market (Nobes,

Parker and Parker, 2008).

The net cash flow of the company explains that the actual cash inflow of the company

has been lower from last year. The company has followed the AASB rules to prepare the cash

flow statement of the company.

CASH FLOW

(Amount in $ million)

2016-

07

2017-

07

Investments in property, plant, and

equipment -40 -88

Purchases of intangibles -12 -24

Other investing charges 3 17

Long-term debt issued

Long-term debt repayment -295 -5

Cash dividends paid -16 -49

Net change in cash -158 -164

Answer to question-2

Comparative analysis of the all three main flow of activities

The comparative analysis study on the cash flow statement explains that the cash inflow

position of the company is rapidly decreasing. The company has recorded and managed the

cash flow position in such a way that the better idea about the cash position of the company

has been identified.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Financial Accounting

5

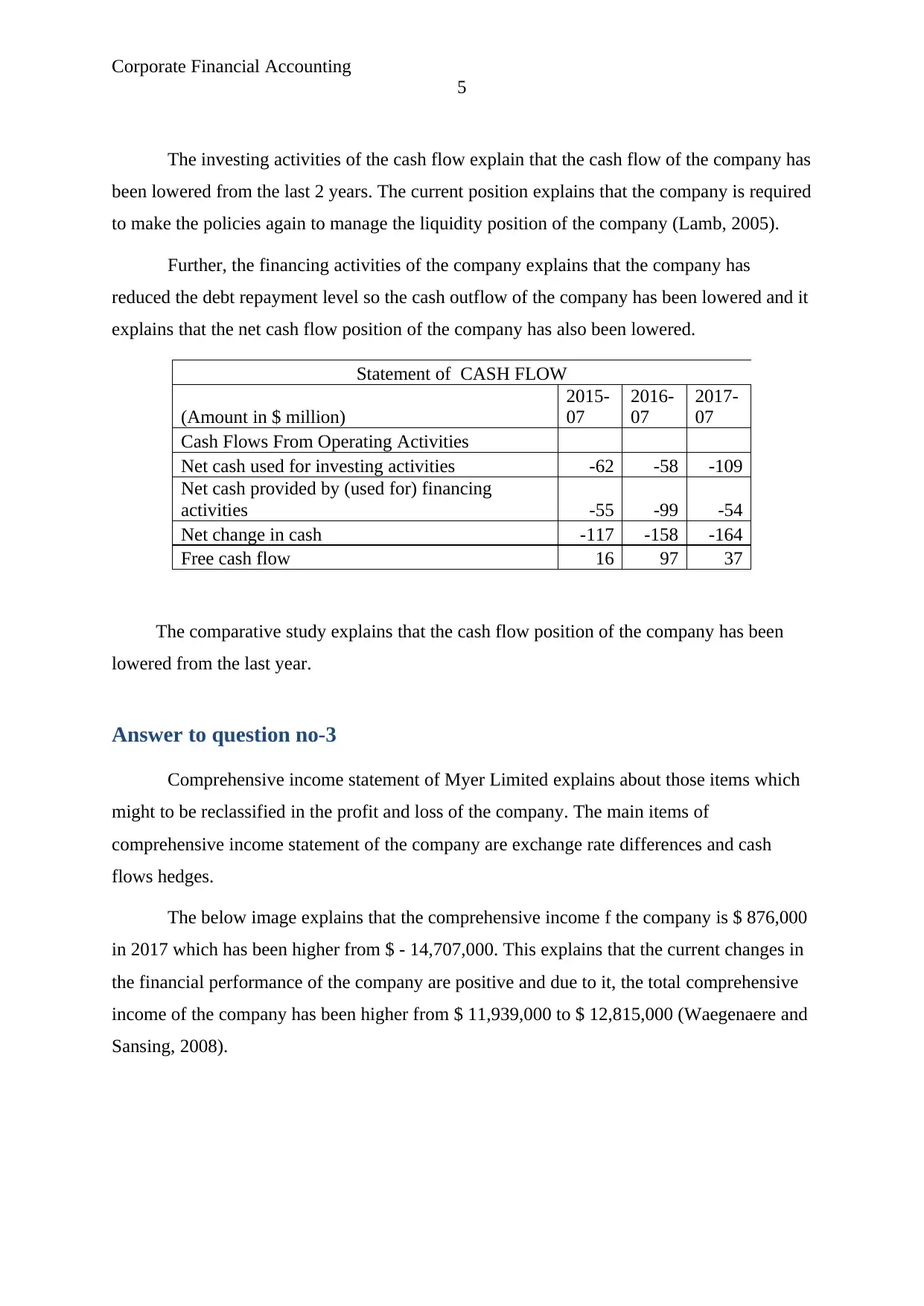

The investing activities of the cash flow explain that the cash flow of the company has

been lowered from the last 2 years. The current position explains that the company is required

to make the policies again to manage the liquidity position of the company (Lamb, 2005).

Further, the financing activities of the company explains that the company has

reduced the debt repayment level so the cash outflow of the company has been lowered and it

explains that the net cash flow position of the company has also been lowered.

Statement of CASH FLOW

(Amount in $ million)

2015-

07

2016-

07

2017-

07

Cash Flows From Operating Activities

Net cash used for investing activities -62 -58 -109

Net cash provided by (used for) financing

activities -55 -99 -54

Net change in cash -117 -158 -164

Free cash flow 16 97 37

The comparative study explains that the cash flow position of the company has been

lowered from the last year.

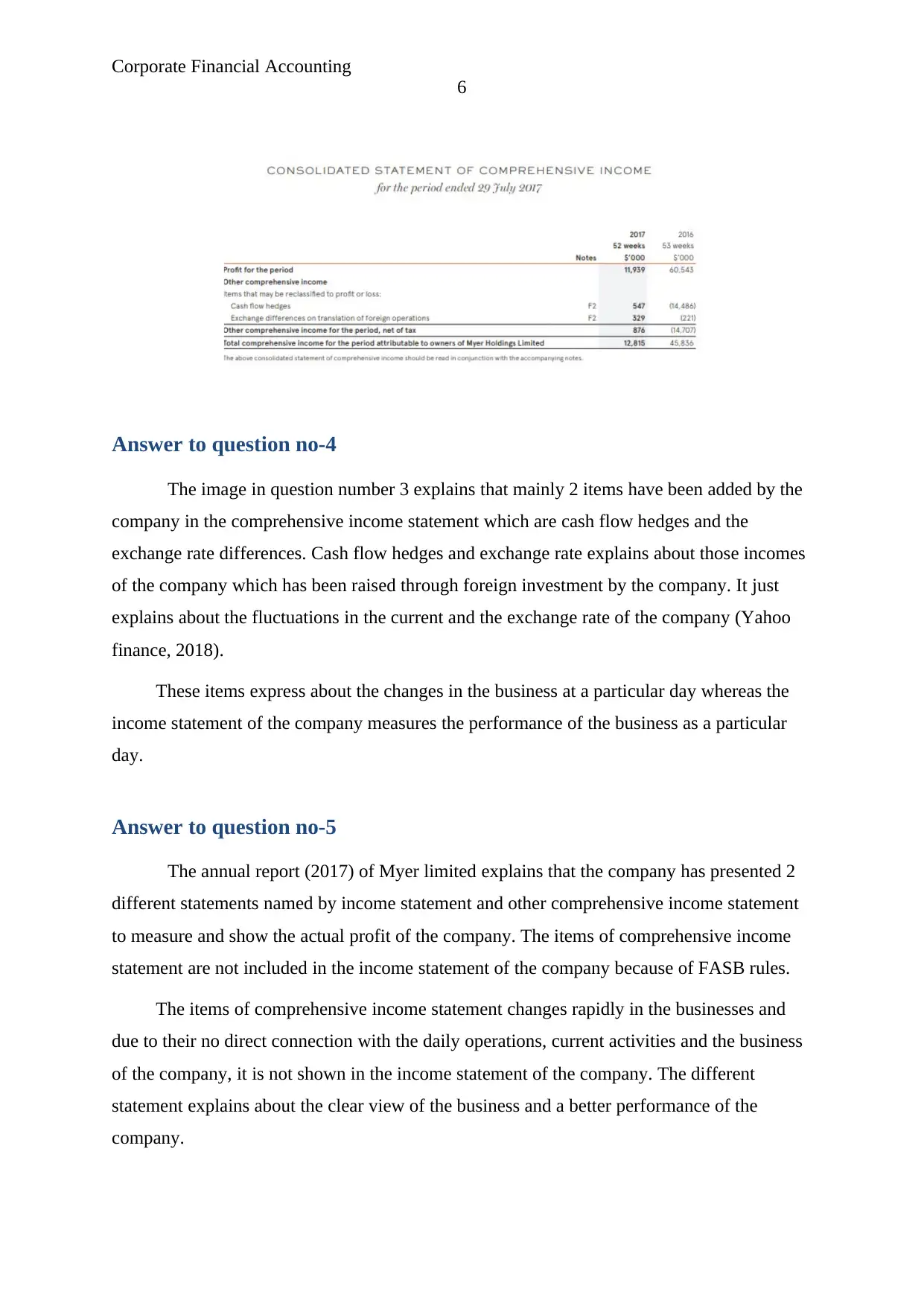

Answer to question no-3

Comprehensive income statement of Myer Limited explains about those items which

might to be reclassified in the profit and loss of the company. The main items of

comprehensive income statement of the company are exchange rate differences and cash

flows hedges.

The below image explains that the comprehensive income f the company is $ 876,000

in 2017 which has been higher from $ - 14,707,000. This explains that the current changes in

the financial performance of the company are positive and due to it, the total comprehensive

income of the company has been higher from $ 11,939,000 to $ 12,815,000 (Waegenaere and

Sansing, 2008).

5

The investing activities of the cash flow explain that the cash flow of the company has

been lowered from the last 2 years. The current position explains that the company is required

to make the policies again to manage the liquidity position of the company (Lamb, 2005).

Further, the financing activities of the company explains that the company has

reduced the debt repayment level so the cash outflow of the company has been lowered and it

explains that the net cash flow position of the company has also been lowered.

Statement of CASH FLOW

(Amount in $ million)

2015-

07

2016-

07

2017-

07

Cash Flows From Operating Activities

Net cash used for investing activities -62 -58 -109

Net cash provided by (used for) financing

activities -55 -99 -54

Net change in cash -117 -158 -164

Free cash flow 16 97 37

The comparative study explains that the cash flow position of the company has been

lowered from the last year.

Answer to question no-3

Comprehensive income statement of Myer Limited explains about those items which

might to be reclassified in the profit and loss of the company. The main items of

comprehensive income statement of the company are exchange rate differences and cash

flows hedges.

The below image explains that the comprehensive income f the company is $ 876,000

in 2017 which has been higher from $ - 14,707,000. This explains that the current changes in

the financial performance of the company are positive and due to it, the total comprehensive

income of the company has been higher from $ 11,939,000 to $ 12,815,000 (Waegenaere and

Sansing, 2008).

Corporate Financial Accounting

6

Answer to question no-4

The image in question number 3 explains that mainly 2 items have been added by the

company in the comprehensive income statement which are cash flow hedges and the

exchange rate differences. Cash flow hedges and exchange rate explains about those incomes

of the company which has been raised through foreign investment by the company. It just

explains about the fluctuations in the current and the exchange rate of the company (Yahoo

finance, 2018).

These items express about the changes in the business at a particular day whereas the

income statement of the company measures the performance of the business as a particular

day.

Answer to question no-5

The annual report (2017) of Myer limited explains that the company has presented 2

different statements named by income statement and other comprehensive income statement

to measure and show the actual profit of the company. The items of comprehensive income

statement are not included in the income statement of the company because of FASB rules.

The items of comprehensive income statement changes rapidly in the businesses and

due to their no direct connection with the daily operations, current activities and the business

of the company, it is not shown in the income statement of the company. The different

statement explains about the clear view of the business and a better performance of the

company.

6

Answer to question no-4

The image in question number 3 explains that mainly 2 items have been added by the

company in the comprehensive income statement which are cash flow hedges and the

exchange rate differences. Cash flow hedges and exchange rate explains about those incomes

of the company which has been raised through foreign investment by the company. It just

explains about the fluctuations in the current and the exchange rate of the company (Yahoo

finance, 2018).

These items express about the changes in the business at a particular day whereas the

income statement of the company measures the performance of the business as a particular

day.

Answer to question no-5

The annual report (2017) of Myer limited explains that the company has presented 2

different statements named by income statement and other comprehensive income statement

to measure and show the actual profit of the company. The items of comprehensive income

statement are not included in the income statement of the company because of FASB rules.

The items of comprehensive income statement changes rapidly in the businesses and

due to their no direct connection with the daily operations, current activities and the business

of the company, it is not shown in the income statement of the company. The different

statement explains about the clear view of the business and a better performance of the

company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Financial Accounting

7

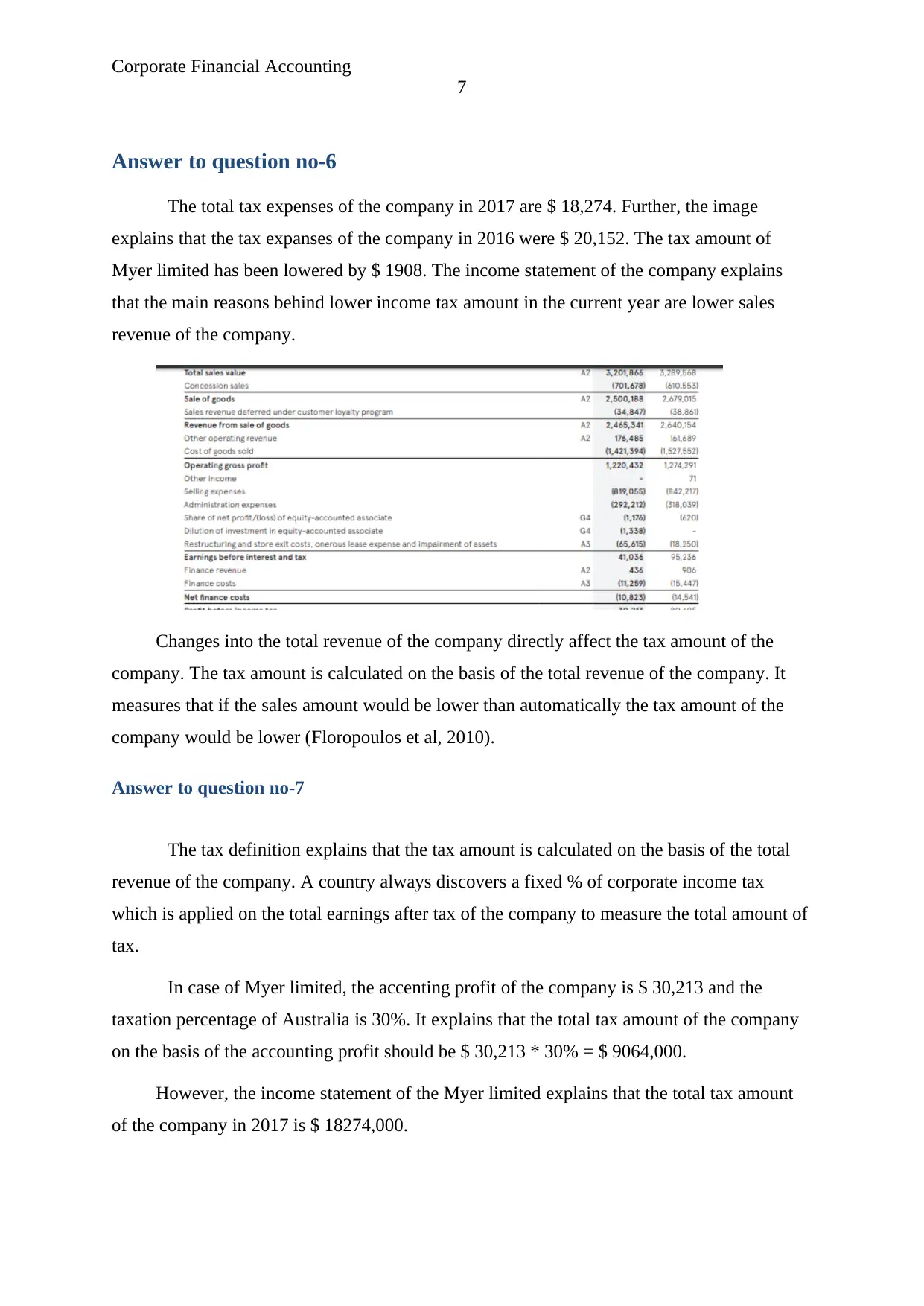

Answer to question no-6

The total tax expenses of the company in 2017 are $ 18,274. Further, the image

explains that the tax expanses of the company in 2016 were $ 20,152. The tax amount of

Myer limited has been lowered by $ 1908. The income statement of the company explains

that the main reasons behind lower income tax amount in the current year are lower sales

revenue of the company.

Changes into the total revenue of the company directly affect the tax amount of the

company. The tax amount is calculated on the basis of the total revenue of the company. It

measures that if the sales amount would be lower than automatically the tax amount of the

company would be lower (Floropoulos et al, 2010).

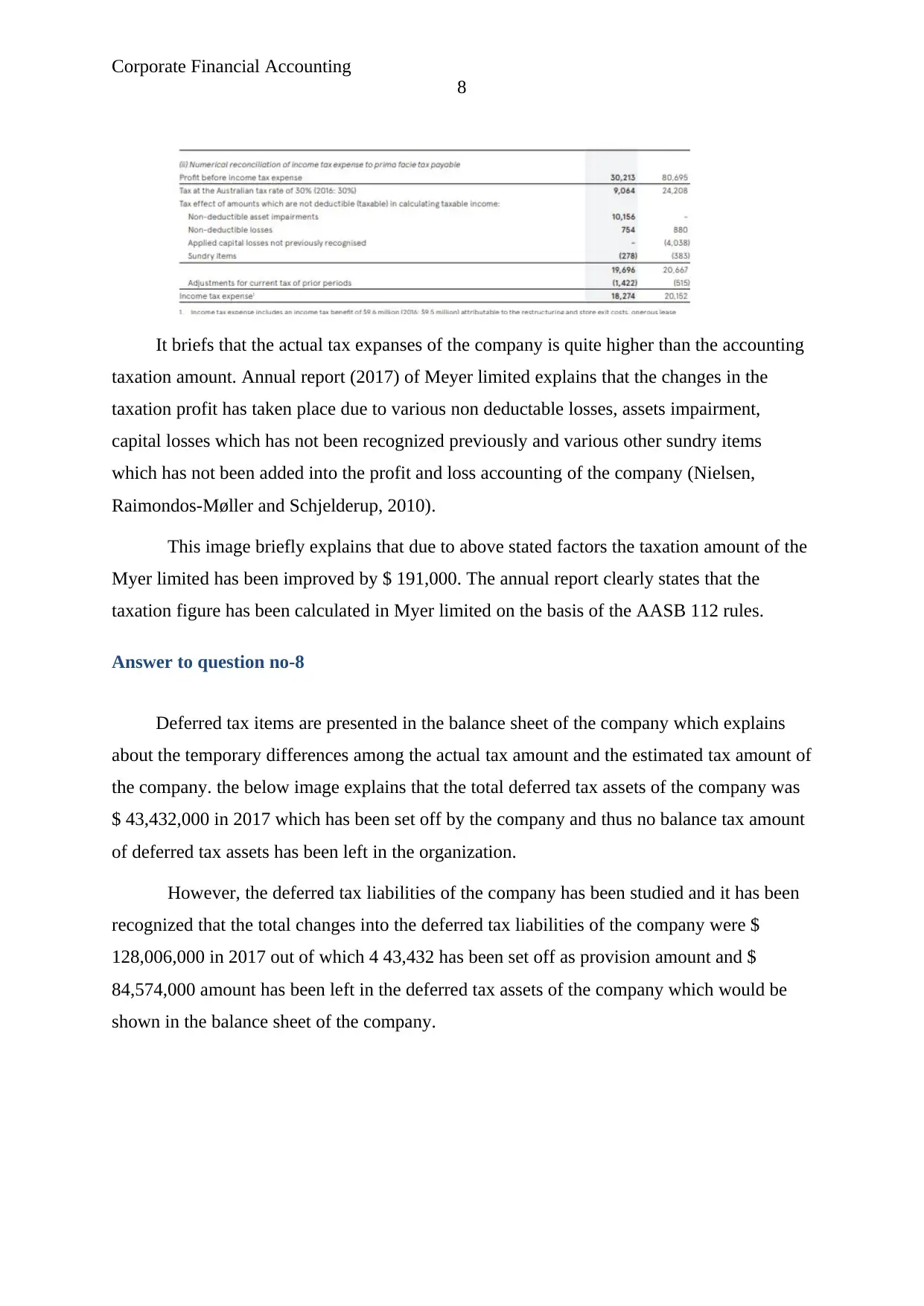

Answer to question no-7

The tax definition explains that the tax amount is calculated on the basis of the total

revenue of the company. A country always discovers a fixed % of corporate income tax

which is applied on the total earnings after tax of the company to measure the total amount of

tax.

In case of Myer limited, the accenting profit of the company is $ 30,213 and the

taxation percentage of Australia is 30%. It explains that the total tax amount of the company

on the basis of the accounting profit should be $ 30,213 * 30% = $ 9064,000.

However, the income statement of the Myer limited explains that the total tax amount

of the company in 2017 is $ 18274,000.

7

Answer to question no-6

The total tax expenses of the company in 2017 are $ 18,274. Further, the image

explains that the tax expanses of the company in 2016 were $ 20,152. The tax amount of

Myer limited has been lowered by $ 1908. The income statement of the company explains

that the main reasons behind lower income tax amount in the current year are lower sales

revenue of the company.

Changes into the total revenue of the company directly affect the tax amount of the

company. The tax amount is calculated on the basis of the total revenue of the company. It

measures that if the sales amount would be lower than automatically the tax amount of the

company would be lower (Floropoulos et al, 2010).

Answer to question no-7

The tax definition explains that the tax amount is calculated on the basis of the total

revenue of the company. A country always discovers a fixed % of corporate income tax

which is applied on the total earnings after tax of the company to measure the total amount of

tax.

In case of Myer limited, the accenting profit of the company is $ 30,213 and the

taxation percentage of Australia is 30%. It explains that the total tax amount of the company

on the basis of the accounting profit should be $ 30,213 * 30% = $ 9064,000.

However, the income statement of the Myer limited explains that the total tax amount

of the company in 2017 is $ 18274,000.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Financial Accounting

8

It briefs that the actual tax expanses of the company is quite higher than the accounting

taxation amount. Annual report (2017) of Meyer limited explains that the changes in the

taxation profit has taken place due to various non deductable losses, assets impairment,

capital losses which has not been recognized previously and various other sundry items

which has not been added into the profit and loss accounting of the company (Nielsen,

Raimondos-Møller and Schjelderup, 2010).

This image briefly explains that due to above stated factors the taxation amount of the

Myer limited has been improved by $ 191,000. The annual report clearly states that the

taxation figure has been calculated in Myer limited on the basis of the AASB 112 rules.

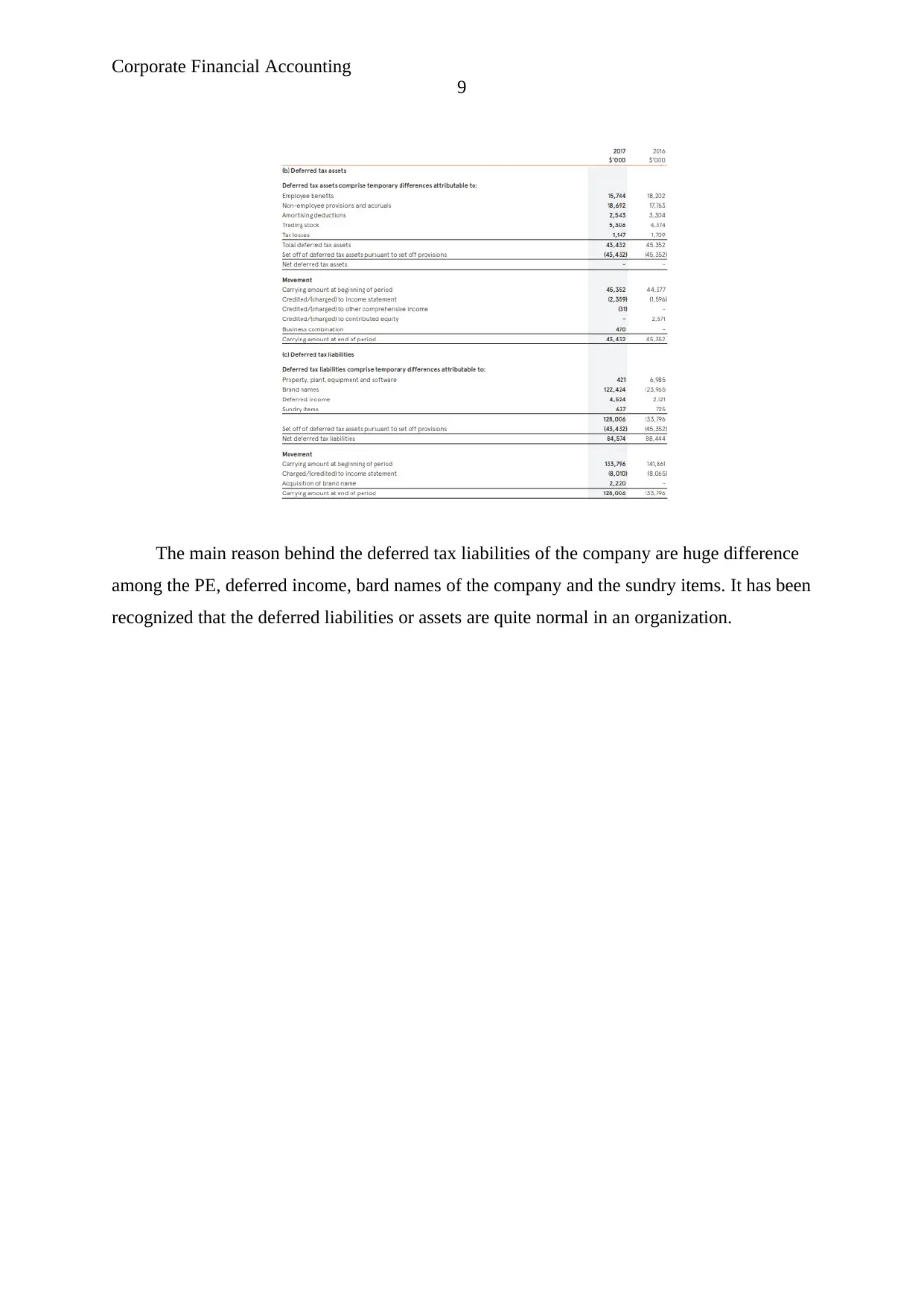

Answer to question no-8

Deferred tax items are presented in the balance sheet of the company which explains

about the temporary differences among the actual tax amount and the estimated tax amount of

the company. the below image explains that the total deferred tax assets of the company was

$ 43,432,000 in 2017 which has been set off by the company and thus no balance tax amount

of deferred tax assets has been left in the organization.

However, the deferred tax liabilities of the company has been studied and it has been

recognized that the total changes into the deferred tax liabilities of the company were $

128,006,000 in 2017 out of which 4 43,432 has been set off as provision amount and $

84,574,000 amount has been left in the deferred tax assets of the company which would be

shown in the balance sheet of the company.

8

It briefs that the actual tax expanses of the company is quite higher than the accounting

taxation amount. Annual report (2017) of Meyer limited explains that the changes in the

taxation profit has taken place due to various non deductable losses, assets impairment,

capital losses which has not been recognized previously and various other sundry items

which has not been added into the profit and loss accounting of the company (Nielsen,

Raimondos-Møller and Schjelderup, 2010).

This image briefly explains that due to above stated factors the taxation amount of the

Myer limited has been improved by $ 191,000. The annual report clearly states that the

taxation figure has been calculated in Myer limited on the basis of the AASB 112 rules.

Answer to question no-8

Deferred tax items are presented in the balance sheet of the company which explains

about the temporary differences among the actual tax amount and the estimated tax amount of

the company. the below image explains that the total deferred tax assets of the company was

$ 43,432,000 in 2017 which has been set off by the company and thus no balance tax amount

of deferred tax assets has been left in the organization.

However, the deferred tax liabilities of the company has been studied and it has been

recognized that the total changes into the deferred tax liabilities of the company were $

128,006,000 in 2017 out of which 4 43,432 has been set off as provision amount and $

84,574,000 amount has been left in the deferred tax assets of the company which would be

shown in the balance sheet of the company.

Corporate Financial Accounting

9

The main reason behind the deferred tax liabilities of the company are huge difference

among the PE, deferred income, bard names of the company and the sundry items. It has been

recognized that the deferred liabilities or assets are quite normal in an organization.

9

The main reason behind the deferred tax liabilities of the company are huge difference

among the PE, deferred income, bard names of the company and the sundry items. It has been

recognized that the deferred liabilities or assets are quite normal in an organization.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Financial Accounting

10

Answer to question no-9

Income tax payable and income tax receivable are also recognized as current tax

liabilities and current tax assets respectively. The current tax assets and current tax liabilities

figure explains about those items which have been added into the balance sheet of the

company due to the differences among the income tax amount and the tax paid amount.

The balance sheet express that the current tax liabilities of the company are $

1992000. It explains that the company has not paid 1,992,000 amounts to the government,

And in very next year, company has to pay the amount to reduce the liabilities of the

company (Istrate, 2011).

The main reason behind occur the current tax liabilities of the company is the less

taxation amount has been paid by the company from the estimated taxation amount.

Answer to question no-10

Income tax paid amount in the cash flow statement explains about the $ 27,759,000.

And the income tax amount in the income statement explains about $ 18,274,000. It briefs

that the company has paid more than the tax amount of the company.

The main reason behind the difference is the last year tax expenses which have been

paid by the company in the current year to manage the performance and the position of the

company. The cash flow statement only focuses on the current yea cash flow of the company

whereas the income statement explains about current year expenses liability of the company

(Radebaugh, Gray and Black, 2006).

Answer to question no-11

Interesting thing

10

Answer to question no-9

Income tax payable and income tax receivable are also recognized as current tax

liabilities and current tax assets respectively. The current tax assets and current tax liabilities

figure explains about those items which have been added into the balance sheet of the

company due to the differences among the income tax amount and the tax paid amount.

The balance sheet express that the current tax liabilities of the company are $

1992000. It explains that the company has not paid 1,992,000 amounts to the government,

And in very next year, company has to pay the amount to reduce the liabilities of the

company (Istrate, 2011).

The main reason behind occur the current tax liabilities of the company is the less

taxation amount has been paid by the company from the estimated taxation amount.

Answer to question no-10

Income tax paid amount in the cash flow statement explains about the $ 27,759,000.

And the income tax amount in the income statement explains about $ 18,274,000. It briefs

that the company has paid more than the tax amount of the company.

The main reason behind the difference is the last year tax expenses which have been

paid by the company in the current year to manage the performance and the position of the

company. The cash flow statement only focuses on the current yea cash flow of the company

whereas the income statement explains about current year expenses liability of the company

(Radebaugh, Gray and Black, 2006).

Answer to question no-11

Interesting thing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Financial Accounting

11

the interesting thing about the study was different income tax amount in the income

statement, balance sheet and cash flow statement. Theire recording and treatment notes were

also interesting.

Surprising thing

The surprising thing of the study is evaluation and the differences among such income

tax figures. The company has recorded all the taxation data with working notes to offers a

clear view.

Difficulty

The difficult part explains that the performance and recording process of the company

is quite better. It briefs about better position of the company, Myer limited.

Conclusion

To conclude, Myer limited has followed the AASB 112 rules to measure and record

all the taxation figures of the company.

11

the interesting thing about the study was different income tax amount in the income

statement, balance sheet and cash flow statement. Theire recording and treatment notes were

also interesting.

Surprising thing

The surprising thing of the study is evaluation and the differences among such income

tax figures. The company has recorded all the taxation data with working notes to offers a

clear view.

Difficulty

The difficult part explains that the performance and recording process of the company

is quite better. It briefs about better position of the company, Myer limited.

Conclusion

To conclude, Myer limited has followed the AASB 112 rules to measure and record

all the taxation figures of the company.

Corporate Financial Accounting

12

References

Annual report. 2017. Myer limited. [online]. Available at:

http://investor.myer.com.au/FormBuilder/_Resource/_module/dGngnzELxUikQxL5gb1cgA/

file/Myer_Annual_Report_2017.pdf (accessed 25/5/18).

Floropoulos, J., Spathis, C., Halvatzis, D. and Tsipouridou, M., 2010. Measuring the success

of the Greek taxation information system. International Journal of Information

Management, 30(1), pp.47-56.

Istrate, C., 2011. Evolutions in the Accounting–Taxation (Dis) connection in Romania, After

1990. Review of Economic & Business Studies, 4(2), pp.43-61.

Lamb, M. 2005. Taxation: An interdisciplinary approach to research. Oxford University

Press on Demand.

McKEE, T.E., 2005. Earnings management: an executive perspective. South-Western Pub.

Nielsen, S.B., Raimondos-Møller, P. and Schjelderup, G., 2010. Company taxation and tax

spillovers: Separate accounting versus formula apportionment. European Economic

Review, 54(1), pp.121-132.

Nobes, C., Parker, R.B. and Parker, R.H., 2008. Comparative international accounting.

Pearson Education.

Radebaugh, L.H., Gray, S.J. and Black, E.L., 2006. International accounting and

multinational enterprises. New York, NY: John Wiley & Sons.

Reuters. 2017. Myer limited. [online]. Available at:

https://www.reuters.com/finance/stocks/company-profile/MYR.AX (accessed 25/5/18).

Waegenaere, A. and Sansing, R.C., 2008. Taxation of international investment and

accounting valuation. Contemporary Accounting Research, 25(4), pp.1045-1066.

Yahoo Finance. 2017. Myer limited. [online]. Available at:

https://finance.yahoo.com/quote/MYR.AX/financials?p=MYR.AX (accessed 25/5/18).

12

References

Annual report. 2017. Myer limited. [online]. Available at:

http://investor.myer.com.au/FormBuilder/_Resource/_module/dGngnzELxUikQxL5gb1cgA/

file/Myer_Annual_Report_2017.pdf (accessed 25/5/18).

Floropoulos, J., Spathis, C., Halvatzis, D. and Tsipouridou, M., 2010. Measuring the success

of the Greek taxation information system. International Journal of Information

Management, 30(1), pp.47-56.

Istrate, C., 2011. Evolutions in the Accounting–Taxation (Dis) connection in Romania, After

1990. Review of Economic & Business Studies, 4(2), pp.43-61.

Lamb, M. 2005. Taxation: An interdisciplinary approach to research. Oxford University

Press on Demand.

McKEE, T.E., 2005. Earnings management: an executive perspective. South-Western Pub.

Nielsen, S.B., Raimondos-Møller, P. and Schjelderup, G., 2010. Company taxation and tax

spillovers: Separate accounting versus formula apportionment. European Economic

Review, 54(1), pp.121-132.

Nobes, C., Parker, R.B. and Parker, R.H., 2008. Comparative international accounting.

Pearson Education.

Radebaugh, L.H., Gray, S.J. and Black, E.L., 2006. International accounting and

multinational enterprises. New York, NY: John Wiley & Sons.

Reuters. 2017. Myer limited. [online]. Available at:

https://www.reuters.com/finance/stocks/company-profile/MYR.AX (accessed 25/5/18).

Waegenaere, A. and Sansing, R.C., 2008. Taxation of international investment and

accounting valuation. Contemporary Accounting Research, 25(4), pp.1045-1066.

Yahoo Finance. 2017. Myer limited. [online]. Available at:

https://finance.yahoo.com/quote/MYR.AX/financials?p=MYR.AX (accessed 25/5/18).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.