HI5020 Corporate Accounting Assignment: Orica Limited Analysis

VerifiedAdded on 2023/06/12

|10

|2169

|347

Report

AI Summary

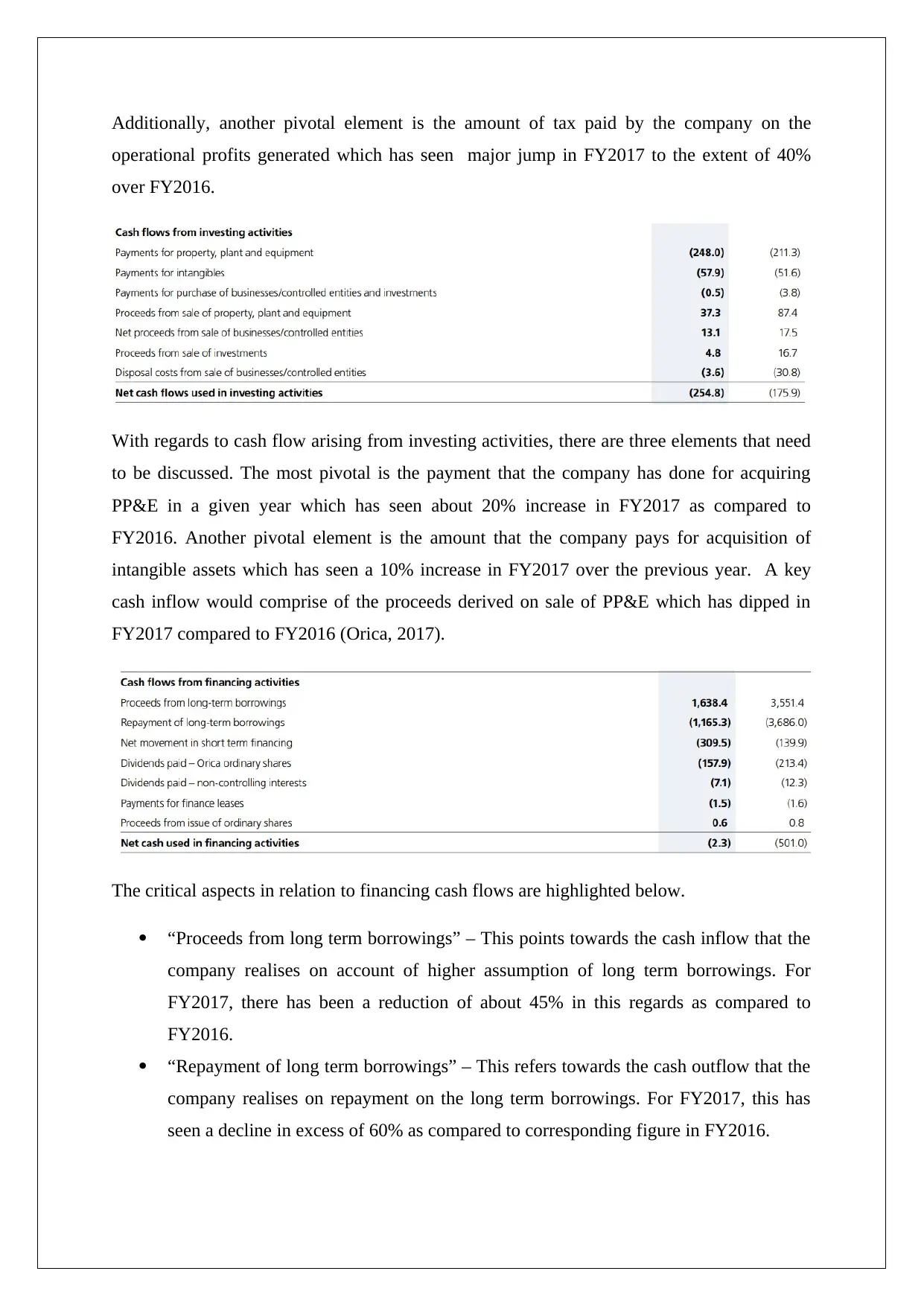

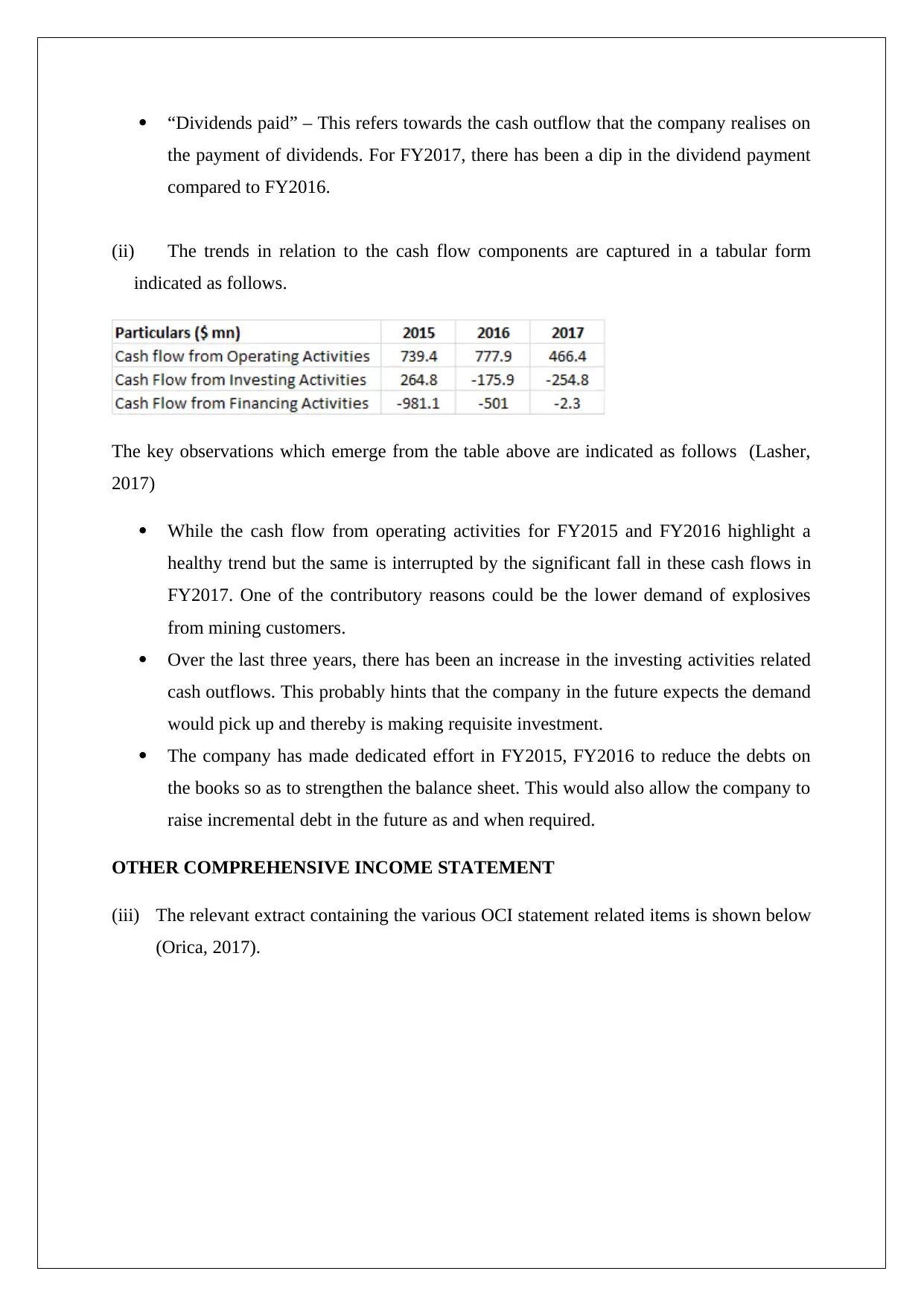

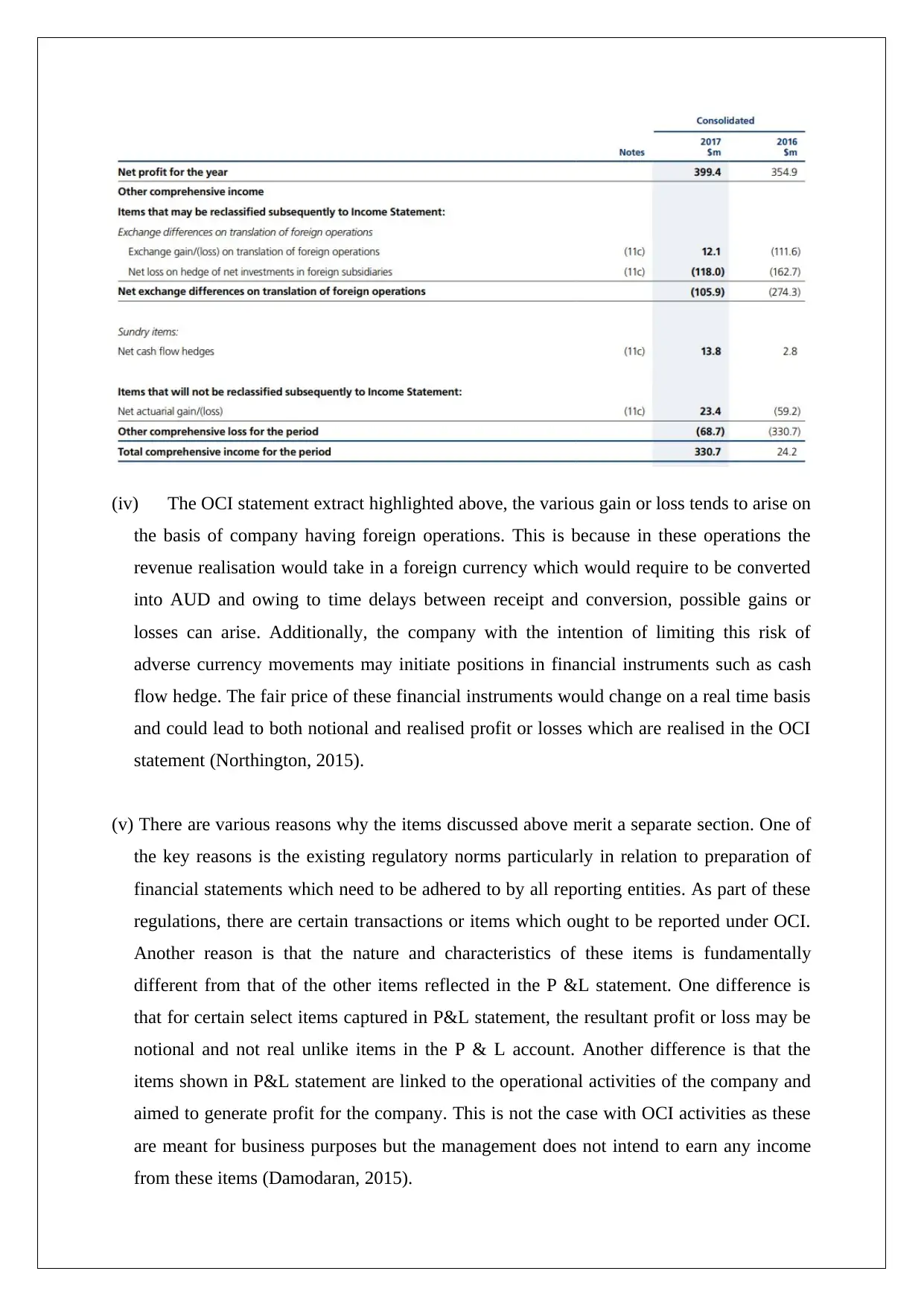

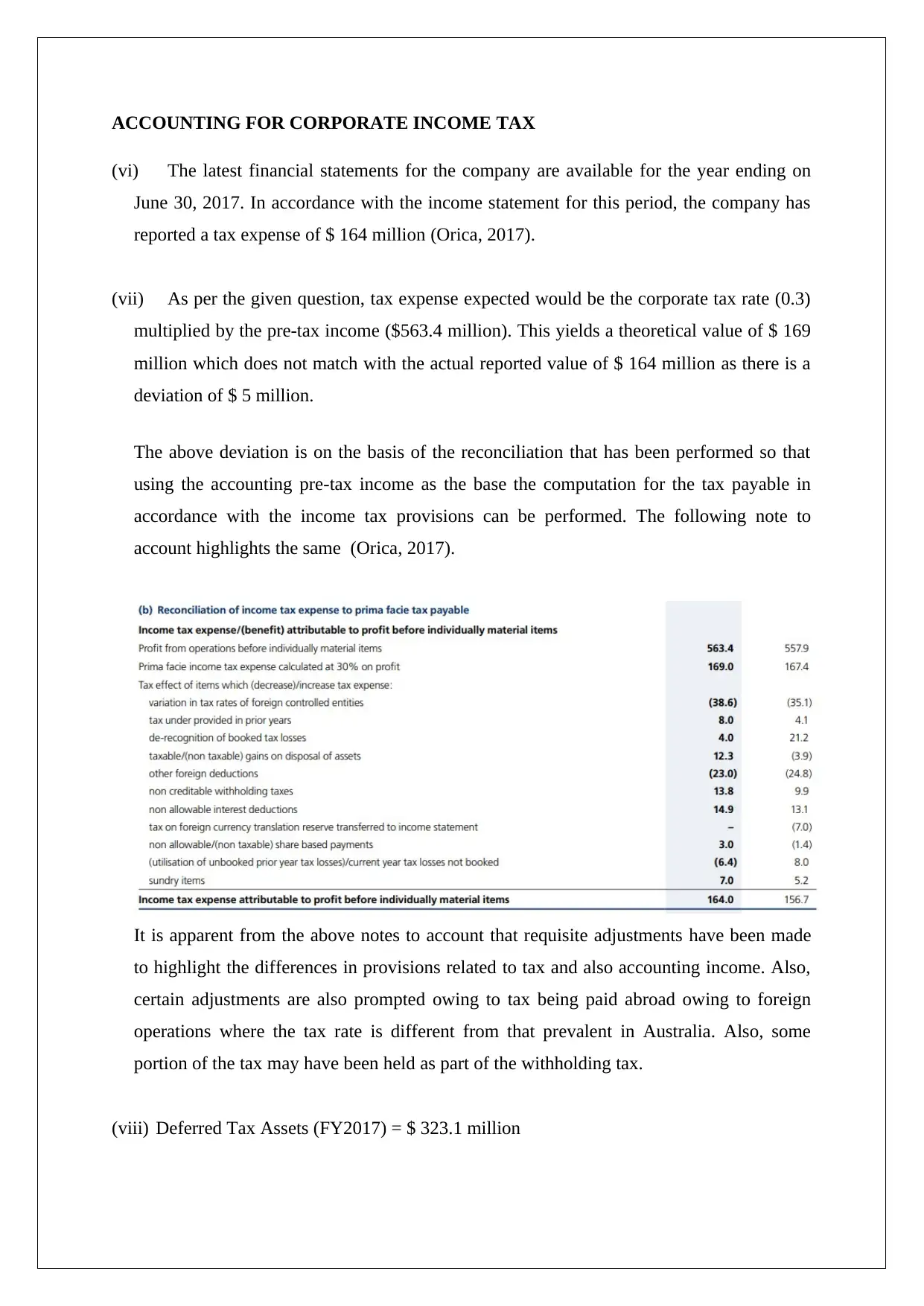

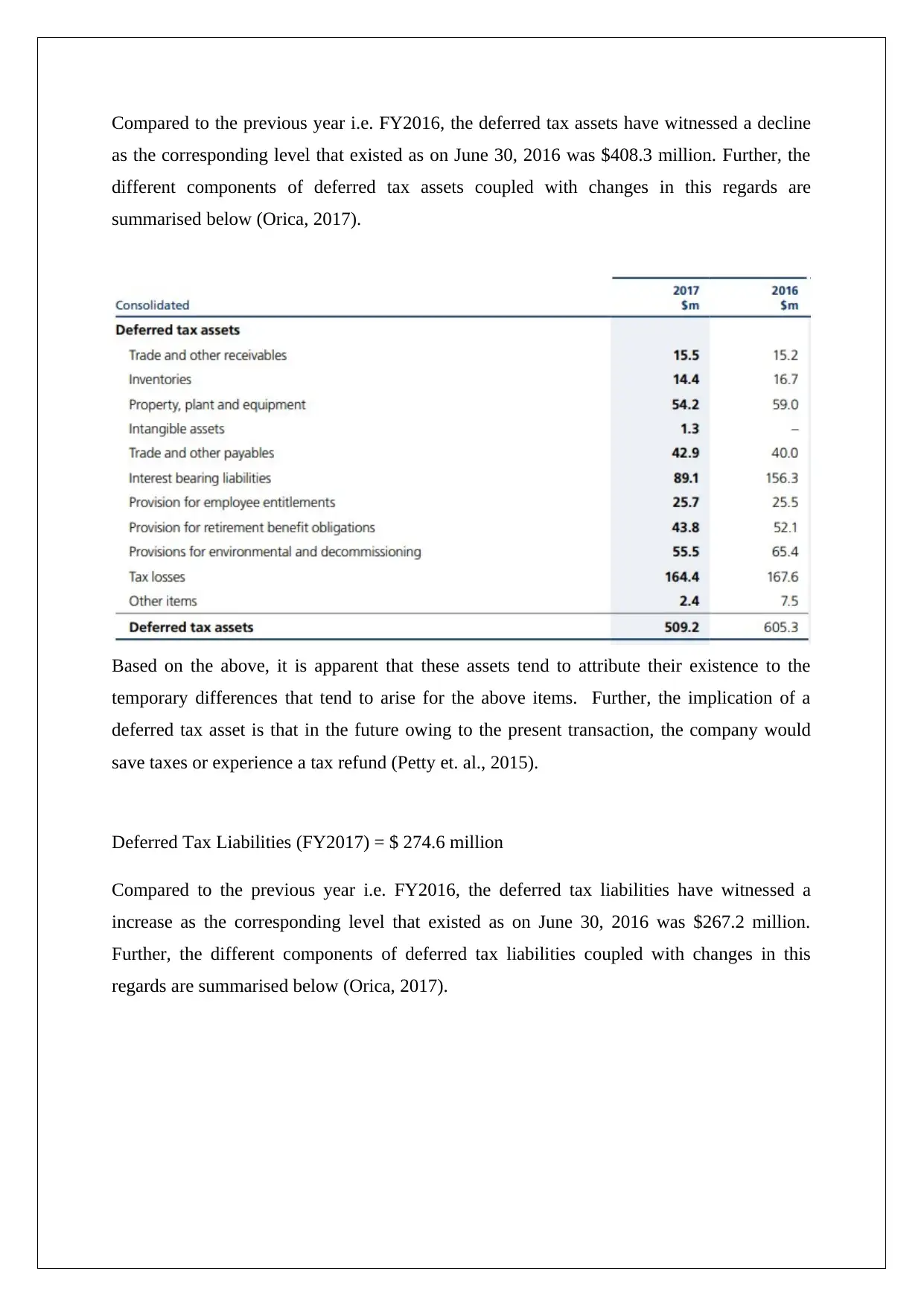

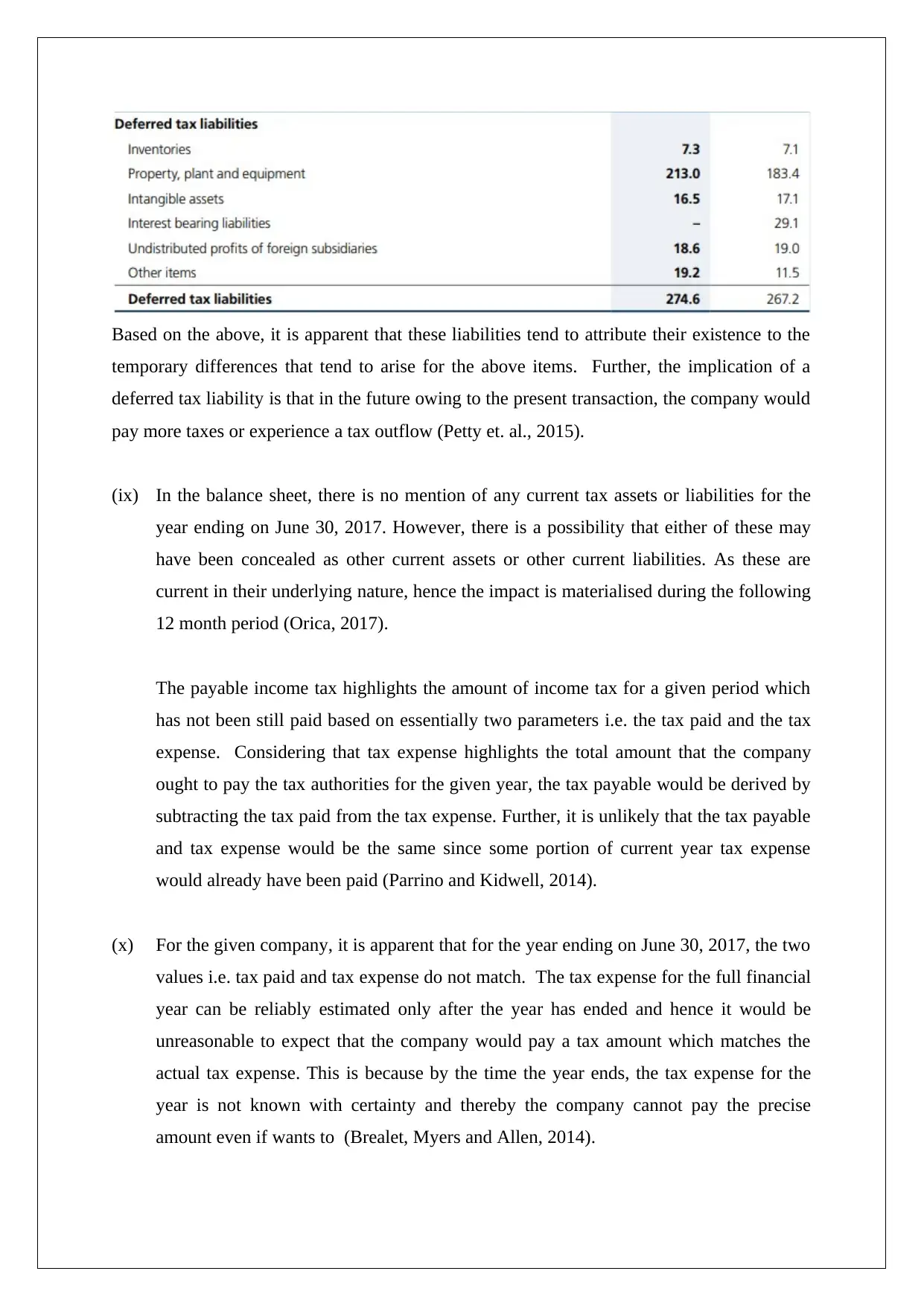

This report provides a comprehensive analysis of Orica Limited's financial statements, focusing on the cash flow statement, other comprehensive income (OCI), and corporate income tax accounting for the fiscal year 2017. It examines key operational, investing, and financing cash flow components, highlighting trends and potential drivers behind changes in receipts from customers, payments to suppliers and employees, and long-term borrowings. The analysis extends to OCI, explaining gains or losses arising from foreign operations and the use of financial instruments like cash flow hedges. Furthermore, the report delves into the reconciliation of tax expense, deferred tax assets, and liabilities, emphasizing the impact of temporary differences and adjustments related to foreign tax rates. The report also addresses the challenges in interpreting deferred tax assets and the reconciliation process for tax expenses, providing a detailed overview of Orica's financial position and tax strategies.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.