Corporate Accounting Project: Impairment and Consolidation

VerifiedAdded on 2022/11/23

|14

|921

|414

Project

AI Summary

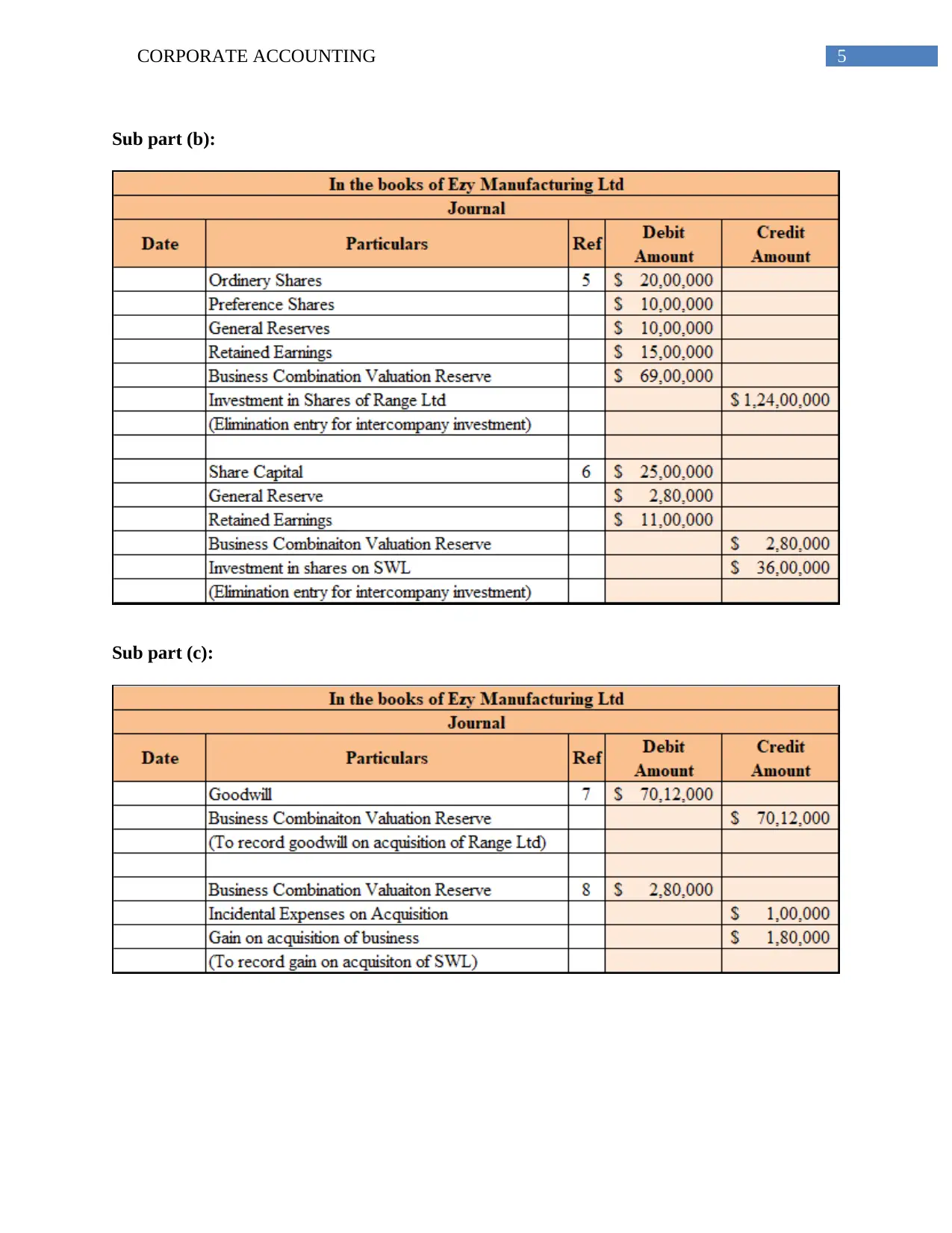

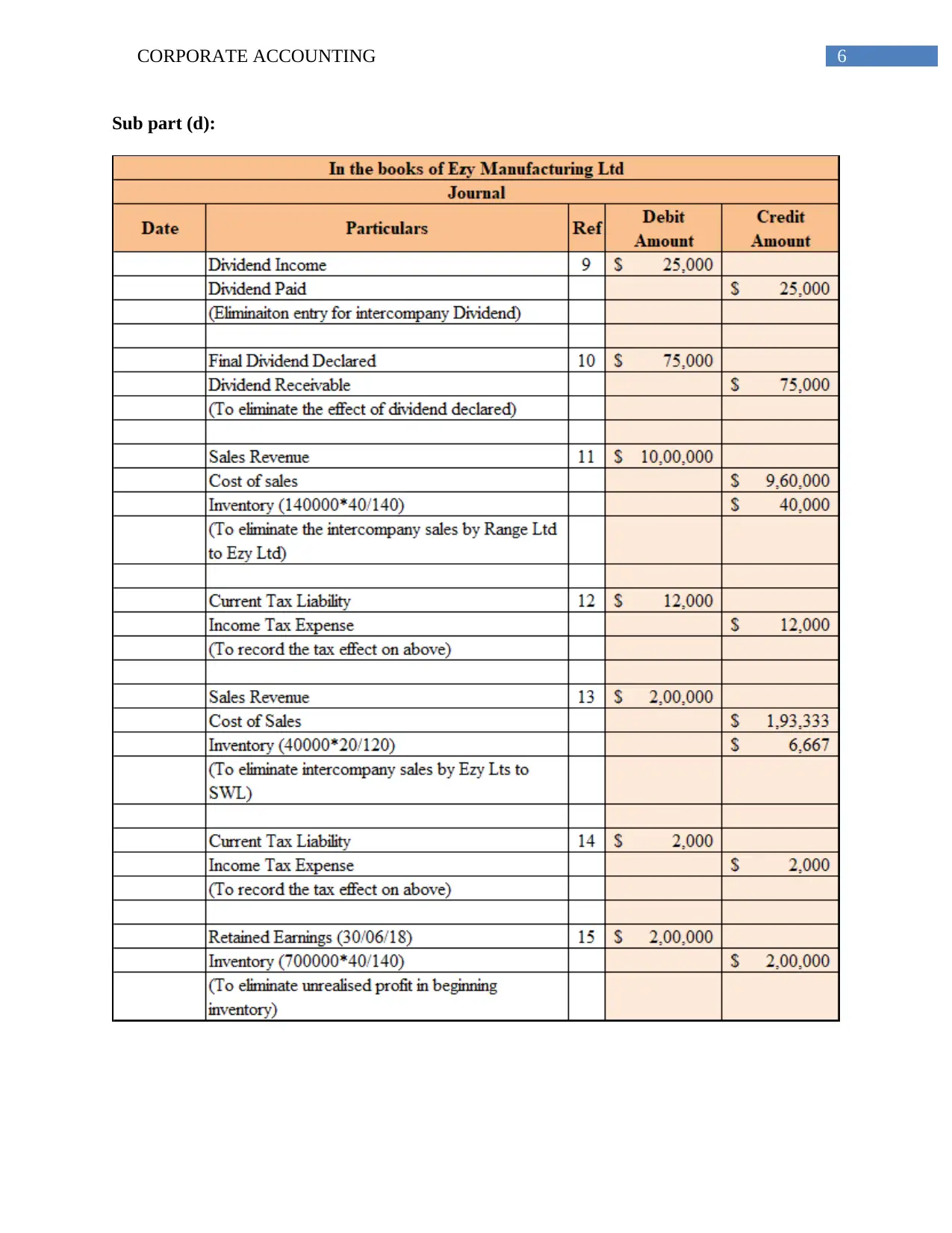

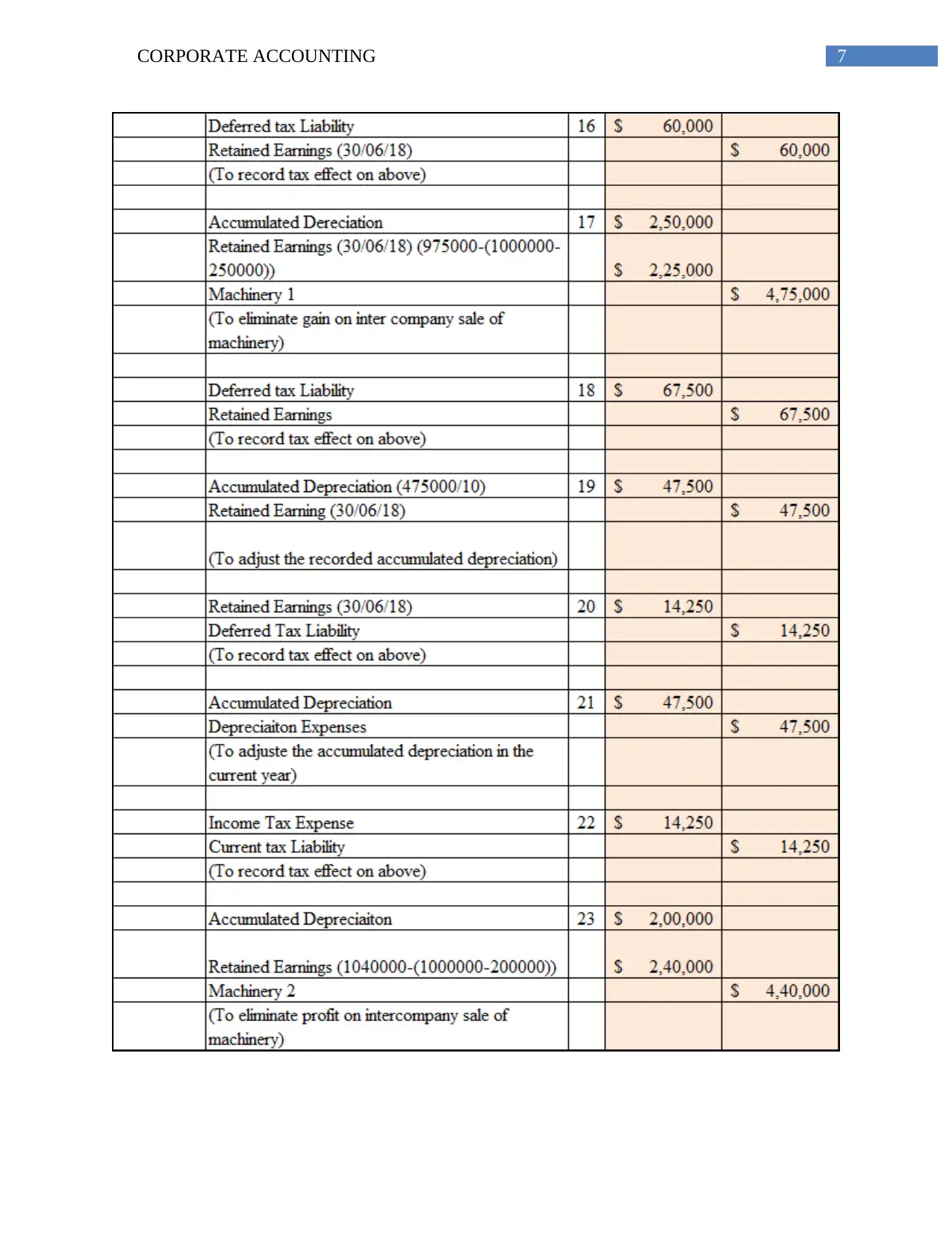

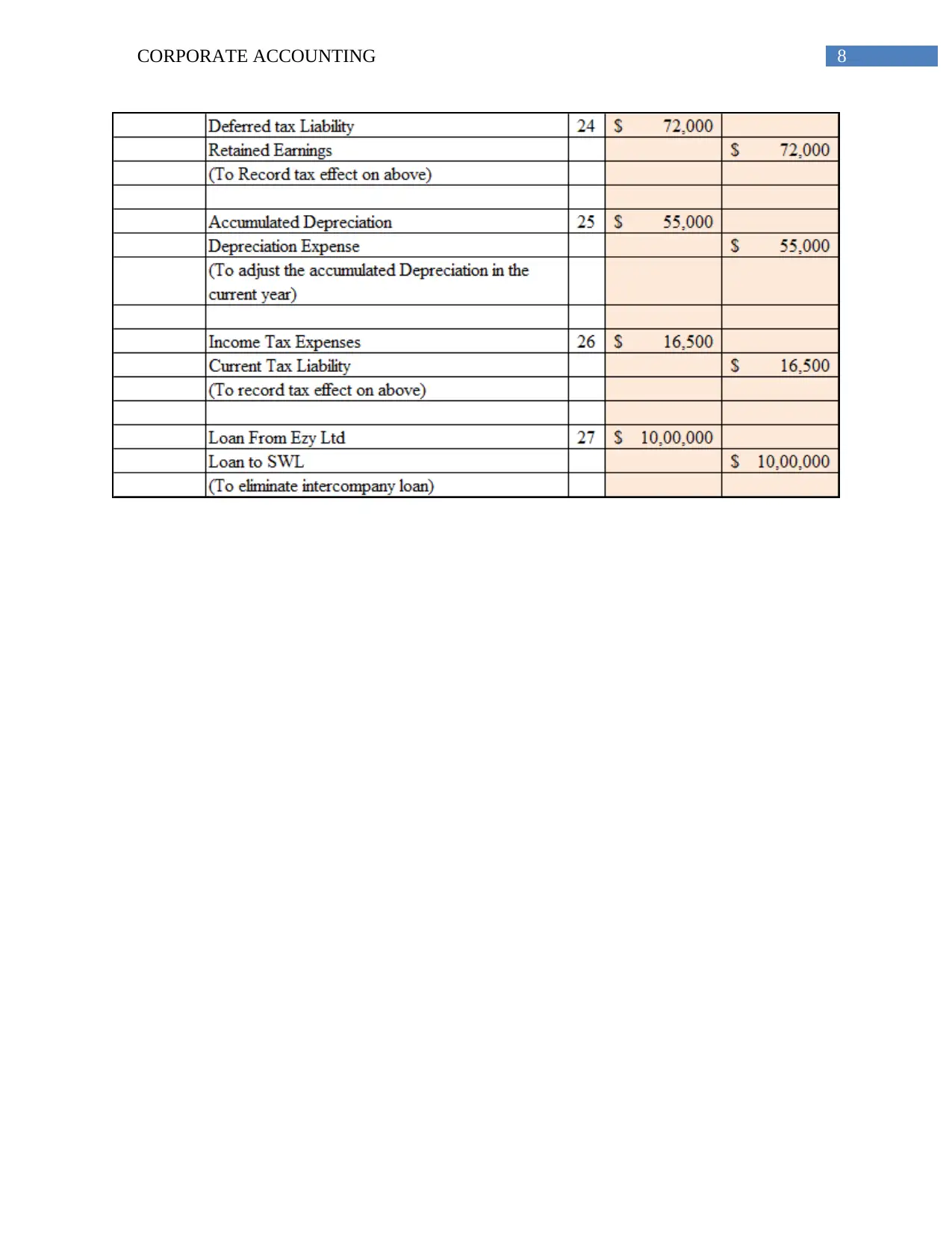

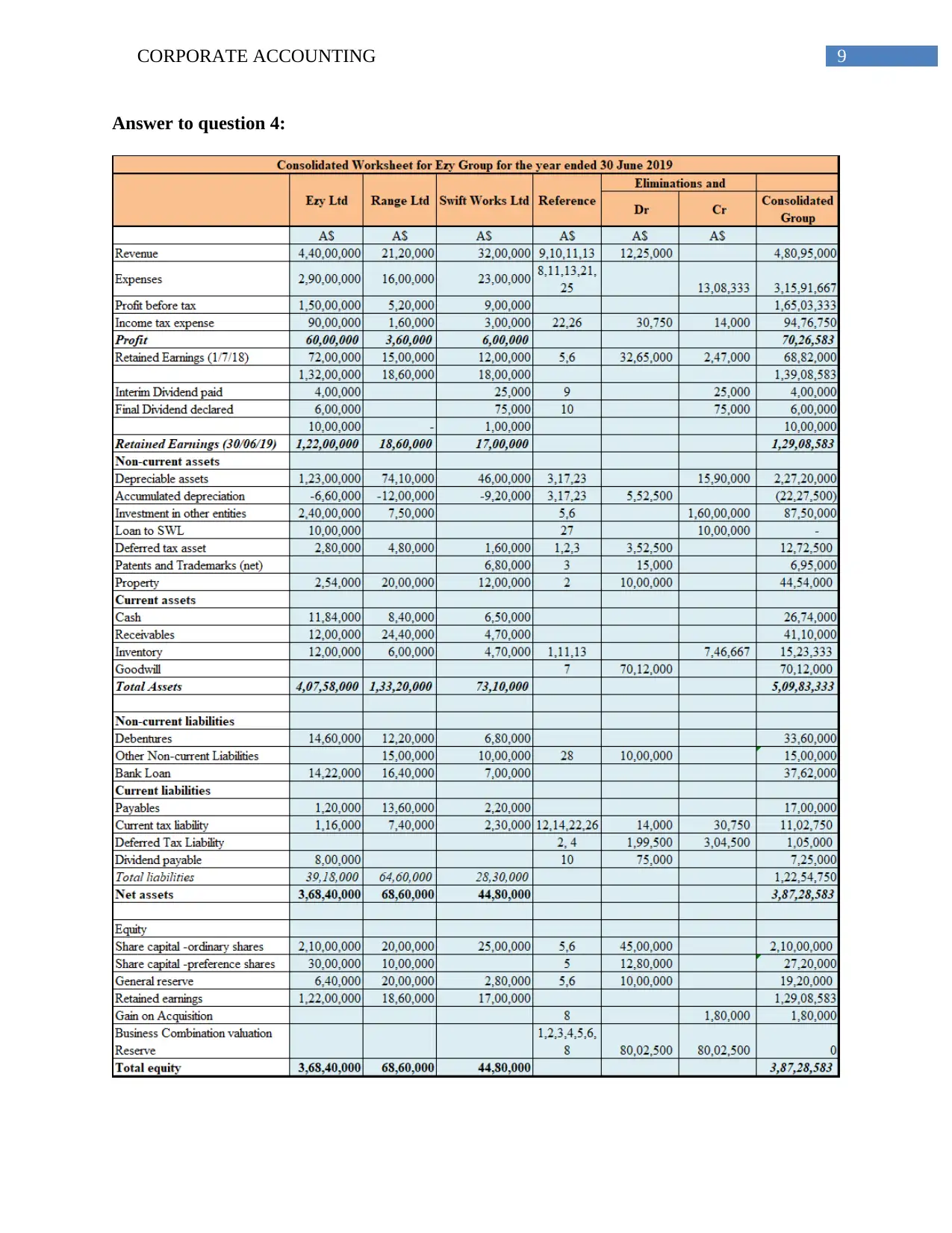

This assignment is a comprehensive project on corporate accounting, focusing on impairment of assets and consolidation. Part I involves an analysis of Ezy Manufacturing Ltd's investments in Range Pty Ltd and SWL, requiring the student to address specific accounting questions related to these entities. The assignment delves into the concepts of impairment testing, including the valuation of goodwill and other intangible assets, and the impact of discount rates. Part II focuses on impairment testing, exploring its process, application to tangible and intangible assets, and the impact of revaluation. The project examines impairment testing, the value of goodwill, and the effects of amortization and impairment on financial reporting. It also addresses the reversal of impairment and relevant accounting standards, such as IAS 36. The solution also includes journal entries and a consolidation worksheet. The assignment is based on Chapter 25 of Deegan's Financial Accounting, 8th edition.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.