Corporate Accounting Report: Standard Setting and Analysis

VerifiedAdded on 2023/06/07

|15

|2892

|148

Report

AI Summary

This report delves into the realm of corporate accounting, emphasizing the significance of voluntary financial information disclosure and the role of regulation in ensuring accurate and reliable financial reporting. It highlights the importance of aligning debt and equity components for an optimal capital structure, thereby reducing financial leverage and cost of capital. The report explores the role of the Australian Accounting Standards Board (AASB) in the global accounting standard-setting process, including its collaboration with the IASB and the challenges faced by companies in implementing IFRS. Furthermore, it provides an equity analysis of four ASX-listed companies, examining their debt and equity positions over a four-year period. The analysis covers key financial aspects such as share capital, retained earnings, and reserves. The report concludes with key findings related to corporate accounting practices, financial reporting, and the financial performance of the selected companies.

RUNNING HEAD: CORPORATE ACCOUNTING

Corporate accounting

Corporate accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate accounting 2

Executive summary

The report outlines the importance of voluntarily disclosing the financial accounting information

to the users. It recommended that managers must uncover all the data on their own so that true

position of the organization can be identified. Additionally it likewise gives bits of knowledge

about the regulation of corporate financial reporting which is important for avoiding the mistakes

and errors. In the later part, equity analysis of the four listed organizations of Australia is done in

which their debt and equity proportion are analysed for the past four years. The findings of the

report are provided in conclusion in a nutshell.

Executive summary

The report outlines the importance of voluntarily disclosing the financial accounting information

to the users. It recommended that managers must uncover all the data on their own so that true

position of the organization can be identified. Additionally it likewise gives bits of knowledge

about the regulation of corporate financial reporting which is important for avoiding the mistakes

and errors. In the later part, equity analysis of the four listed organizations of Australia is done in

which their debt and equity proportion are analysed for the past four years. The findings of the

report are provided in conclusion in a nutshell.

Corporate accounting 3

Contents

Introduction.................................................................................................................................................4

Corporate Regulation...................................................................................................................................5

Part 1.......................................................................................................................................................5

Accounting standard setting........................................................................................................................7

Part 2.......................................................................................................................................................7

Owners’ equity............................................................................................................................................9

Part 3.......................................................................................................................................................9

Part 4.....................................................................................................................................................11

Conclusion.................................................................................................................................................12

References.................................................................................................................................................14

Contents

Introduction.................................................................................................................................................4

Corporate Regulation...................................................................................................................................5

Part 1.......................................................................................................................................................5

Accounting standard setting........................................................................................................................7

Part 2.......................................................................................................................................................7

Owners’ equity............................................................................................................................................9

Part 3.......................................................................................................................................................9

Part 4.....................................................................................................................................................11

Conclusion.................................................................................................................................................12

References.................................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate accounting 4

Introduction

This report focuses on the execution of IFRS for the presentation of financial reports of the

organization. It also laid more emphasis on establishing equal alignment the debt and equity

component of the firm so as to have preferred capital structure which will automatically drop the

financial leverage and cost of capital of the organization. It set out the significance of

deliberately revealing the financial data and recommends that the same is especially vital for

reflecting the fair and true perspective of the organization's performance and position in

monetary angles. Further, it talks about the significance of managing and regulating corporate

financial reporting procedures so as to avoid problems like misstatements, manipulation of

figures, falsification of accounts and other voluntarily done misconducts on the part of

management.

In the later part, the report highlights the AASB’s role in setting accounting standards at global

level. It states that IASB has collaborated with various domestic standard setting bodies so as to

formulate relevant and appropriate global accounting benchmarks. The board identifies few

problems and asked IASB for feedback in order to get approval for building up bookkeeping

benchmarks. Also, it features the reasons why a few individuals from IASB has not yet move

towards the implementation of IFRS and the same isn't obligatory for them. The report

additionally gives bits of knowledge about the capital structure of four ASX recorded

organizations for the past four years. It looks at their debt and equity position and outlines all the

findings under the head conclusion at the end.

Introduction

This report focuses on the execution of IFRS for the presentation of financial reports of the

organization. It also laid more emphasis on establishing equal alignment the debt and equity

component of the firm so as to have preferred capital structure which will automatically drop the

financial leverage and cost of capital of the organization. It set out the significance of

deliberately revealing the financial data and recommends that the same is especially vital for

reflecting the fair and true perspective of the organization's performance and position in

monetary angles. Further, it talks about the significance of managing and regulating corporate

financial reporting procedures so as to avoid problems like misstatements, manipulation of

figures, falsification of accounts and other voluntarily done misconducts on the part of

management.

In the later part, the report highlights the AASB’s role in setting accounting standards at global

level. It states that IASB has collaborated with various domestic standard setting bodies so as to

formulate relevant and appropriate global accounting benchmarks. The board identifies few

problems and asked IASB for feedback in order to get approval for building up bookkeeping

benchmarks. Also, it features the reasons why a few individuals from IASB has not yet move

towards the implementation of IFRS and the same isn't obligatory for them. The report

additionally gives bits of knowledge about the capital structure of four ASX recorded

organizations for the past four years. It looks at their debt and equity position and outlines all the

findings under the head conclusion at the end.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate accounting 5

Corporate Regulation

Part 1

It is a fact that disclosure of accounting data has turned out to be fundamental piece of

administration work and the same has been demonstrated by numerous analysts who conducted

several researches led in the field of accounting. The researches proposed that the directors and

officials ought to voluntarily uncover all the pertinent and reliable fiscal information in order to

give bits of knowledge about the financial performance and position of the organizations. The

managers and executives communicate all the financial data to its stakeholders through the

annual report of the company. The report comprises both the financial and non-financial

information which assist the stakeholders to take correct and suitable decisions regarding the

future prospectus of the organization. In particular, introduction of bookkeeping data is

especially valuable for the outside stakeholders as they don't take an interest in the everyday

exercises of the firm and don't know about its internal working (Christensen, Nikolaev and

WITTENBERG‐MOERMAN, 2016). These outside users of report includes government,

lenders, investors and other people who simply put their cash in the business and earn a return on

their investment. They don't have any significant interest in the activities and operations of the

company. Unveiling the financial data will provide such people about the working and monetary

execution of the organization for the present and past years. They can undoubtedly take vital and

fitting choices with respect to their interest in a specific organization and can evaluate the

profitability and liquidity position of the same. The investors keep different viewpoints in their

psyche while ascertaining and measuring the performance of a firm. The points of view

incorporate liquidity, productivity, efficiency and solvency which assess the quantitative

information and give dependable results. As far as qualitative factors or non financial perspective

Corporate Regulation

Part 1

It is a fact that disclosure of accounting data has turned out to be fundamental piece of

administration work and the same has been demonstrated by numerous analysts who conducted

several researches led in the field of accounting. The researches proposed that the directors and

officials ought to voluntarily uncover all the pertinent and reliable fiscal information in order to

give bits of knowledge about the financial performance and position of the organizations. The

managers and executives communicate all the financial data to its stakeholders through the

annual report of the company. The report comprises both the financial and non-financial

information which assist the stakeholders to take correct and suitable decisions regarding the

future prospectus of the organization. In particular, introduction of bookkeeping data is

especially valuable for the outside stakeholders as they don't take an interest in the everyday

exercises of the firm and don't know about its internal working (Christensen, Nikolaev and

WITTENBERG‐MOERMAN, 2016). These outside users of report includes government,

lenders, investors and other people who simply put their cash in the business and earn a return on

their investment. They don't have any significant interest in the activities and operations of the

company. Unveiling the financial data will provide such people about the working and monetary

execution of the organization for the present and past years. They can undoubtedly take vital and

fitting choices with respect to their interest in a specific organization and can evaluate the

profitability and liquidity position of the same. The investors keep different viewpoints in their

psyche while ascertaining and measuring the performance of a firm. The points of view

incorporate liquidity, productivity, efficiency and solvency which assess the quantitative

information and give dependable results. As far as qualitative factors or non financial perspective

Corporate accounting 6

is concerned, company’s sustainability reports, corporate governance statement, GRI

compliance, statement of corporate social responsibility and others are properly analysed and by

the investors and other users to enhance and strengthen their decisions or judgement in context of

a particular entity (Collier, 2015).

As it is clear that the disclosure of financial accounting information is necessary for the

managers and other users, the company should also focus on regulating the procedure of

preparing the financial reports. The principle motive of preparing such reports is to demonstrate

the genuine and fair view of organization's position and performance amid the particular

timeframe. These reports mirror the general working of the organization in a summarized manner

and therefore it is necessary to properly direct and control the process preparing the same.

Setting up the directions will result in harmonization and consistency in the method of planning

corporate financial reports. It gets consistency in the information and makes comparable with

other data, in a way helping the investors and different clients to legitimately comprehend it and

make an appropriate decision (Kaya and Koch, 2015). Each business applies such accounting

benchmarks as per its nature, size and kinds of activities it undertakes. The consistency will

evade the control of records and blunders on part of calculating figures. In addition, it will expel

the likelihood of misrepresentation of records and evacuate the complexity between the adoption

of national and international standards. Overall, it tends to be said that deliberate revelation and

corporate direction is the key component of management as it will enhance the quality of

financial reporting and reduce the chances of establishing internal control for the accounting

purposes. The regulatory framework will assists the accountants in representing all the financial

data in an understandable manner and require the companies to prepare their reports within a

legal framework. The implementation of IFRS standards will create harmony and uniformity in

is concerned, company’s sustainability reports, corporate governance statement, GRI

compliance, statement of corporate social responsibility and others are properly analysed and by

the investors and other users to enhance and strengthen their decisions or judgement in context of

a particular entity (Collier, 2015).

As it is clear that the disclosure of financial accounting information is necessary for the

managers and other users, the company should also focus on regulating the procedure of

preparing the financial reports. The principle motive of preparing such reports is to demonstrate

the genuine and fair view of organization's position and performance amid the particular

timeframe. These reports mirror the general working of the organization in a summarized manner

and therefore it is necessary to properly direct and control the process preparing the same.

Setting up the directions will result in harmonization and consistency in the method of planning

corporate financial reports. It gets consistency in the information and makes comparable with

other data, in a way helping the investors and different clients to legitimately comprehend it and

make an appropriate decision (Kaya and Koch, 2015). Each business applies such accounting

benchmarks as per its nature, size and kinds of activities it undertakes. The consistency will

evade the control of records and blunders on part of calculating figures. In addition, it will expel

the likelihood of misrepresentation of records and evacuate the complexity between the adoption

of national and international standards. Overall, it tends to be said that deliberate revelation and

corporate direction is the key component of management as it will enhance the quality of

financial reporting and reduce the chances of establishing internal control for the accounting

purposes. The regulatory framework will assists the accountants in representing all the financial

data in an understandable manner and require the companies to prepare their reports within a

legal framework. The implementation of IFRS standards will create harmony and uniformity in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate accounting 7

firm’s accounting practices. It will naturally build up control on the strategies and make the

accountants work as per the correct principles and directions (Naranjo, Saavedra and Verdi,

2017).

Accounting standard setting

Part 2

Accounting standards are the guidelines and principles which are put to use at time of preparing

reports that contain money related explanations and financial data. They are the definitive gauges

created by board like AASB and IASB and are the essential wellspring of Generally Accepted

Accounting Principles (GAAP). These guidelines set out the treatment of some particular

business transactions and events that has occurred amid a particular timeframe. Each and every

company working across the world is required to present their financial accounting information

in a manner suggested by international accounting standards.

With a thought process of making harmonization and standardization IASB has worked together

with AASB keeping in mind the end goal to build up the bookkeeping norms at worldwide level.

Australian Accounting Standard Board is an administration specialist which was formed with a

motive of setting out the accounting benchmarks that must be embraced by each publically and

privately owned business listed on ASX and working in Australia. To the extent the job of

AASB has concerned, it has assumed that the board has played an imperative job in building up

the reporting standards. The approved body in charge of setting the principles at worldwide level

is International accounting standard board (IASB) which has been authorized to plan accounting

measures and benchmarks on the global level. The benchmarks set by IASB must be trailed by

every organization working in different parts of the world at time of preparing their annual and

firm’s accounting practices. It will naturally build up control on the strategies and make the

accountants work as per the correct principles and directions (Naranjo, Saavedra and Verdi,

2017).

Accounting standard setting

Part 2

Accounting standards are the guidelines and principles which are put to use at time of preparing

reports that contain money related explanations and financial data. They are the definitive gauges

created by board like AASB and IASB and are the essential wellspring of Generally Accepted

Accounting Principles (GAAP). These guidelines set out the treatment of some particular

business transactions and events that has occurred amid a particular timeframe. Each and every

company working across the world is required to present their financial accounting information

in a manner suggested by international accounting standards.

With a thought process of making harmonization and standardization IASB has worked together

with AASB keeping in mind the end goal to build up the bookkeeping norms at worldwide level.

Australian Accounting Standard Board is an administration specialist which was formed with a

motive of setting out the accounting benchmarks that must be embraced by each publically and

privately owned business listed on ASX and working in Australia. To the extent the job of

AASB has concerned, it has assumed that the board has played an imperative job in building up

the reporting standards. The approved body in charge of setting the principles at worldwide level

is International accounting standard board (IASB) which has been authorized to plan accounting

measures and benchmarks on the global level. The benchmarks set by IASB must be trailed by

every organization working in different parts of the world at time of preparing their annual and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate accounting 8

other financial reports. IASB has hold hands with AASB and other domestic bodies to

incorporate the benchmarks that will get harmonization and consistency. Thinking about the job

of AASB as a standard setter, the board has made a few strategies which legitimize its job in the

changing and dynamic condition. It figures its arrangements and systems in such a way, that they

properly align with the requirements and necessities of IASB. AASB identifies some specialized

issues and got feedback from the Australian organizations which are considered by IASB at the

time of setting principles. The problems faced by Australian companies while presenting their

accounting data are identified which eventually help IASB in making relevant and appropriate

standards for every type of business and entities (AASB. 2018). Australian accounting board also

gather the feedback of the entities working in the country so as to know about the reliability of

the existing standards and the need for bringing the new ones. AASB has presented formal

archives and articulations with IASB in order to got the input and remarks from the international

board so to get the approval for formulating reliable accounting standards (AASB. 2018).

Nonetheless, even after the overall acknowledgment of IFRS there are some members of IASB

which don't have any significant bearing to the same. Also, it isn't mandatory for them to go for

the same. For example, USA has not yet received IFRS in their bookkeeping practices and still

tails US GAAP. One reason is that execution of IFRS will be expensive affair for the nation.

Additionally, settling on GAAP and IFRS is a questionable choice and the nation will confront

issues while looking at the financial information of the organizations working in different areas

of the world. Quality factor is additionally the explanation behind not receiving IFRS. Every

such reason legitimizes that for a few individuals from IASB, it isn't necessary to go for IFRS

(Lam, 2015).

other financial reports. IASB has hold hands with AASB and other domestic bodies to

incorporate the benchmarks that will get harmonization and consistency. Thinking about the job

of AASB as a standard setter, the board has made a few strategies which legitimize its job in the

changing and dynamic condition. It figures its arrangements and systems in such a way, that they

properly align with the requirements and necessities of IASB. AASB identifies some specialized

issues and got feedback from the Australian organizations which are considered by IASB at the

time of setting principles. The problems faced by Australian companies while presenting their

accounting data are identified which eventually help IASB in making relevant and appropriate

standards for every type of business and entities (AASB. 2018). Australian accounting board also

gather the feedback of the entities working in the country so as to know about the reliability of

the existing standards and the need for bringing the new ones. AASB has presented formal

archives and articulations with IASB in order to got the input and remarks from the international

board so to get the approval for formulating reliable accounting standards (AASB. 2018).

Nonetheless, even after the overall acknowledgment of IFRS there are some members of IASB

which don't have any significant bearing to the same. Also, it isn't mandatory for them to go for

the same. For example, USA has not yet received IFRS in their bookkeeping practices and still

tails US GAAP. One reason is that execution of IFRS will be expensive affair for the nation.

Additionally, settling on GAAP and IFRS is a questionable choice and the nation will confront

issues while looking at the financial information of the organizations working in different areas

of the world. Quality factor is additionally the explanation behind not receiving IFRS. Every

such reason legitimizes that for a few individuals from IASB, it isn't necessary to go for IFRS

(Lam, 2015).

Corporate accounting 9

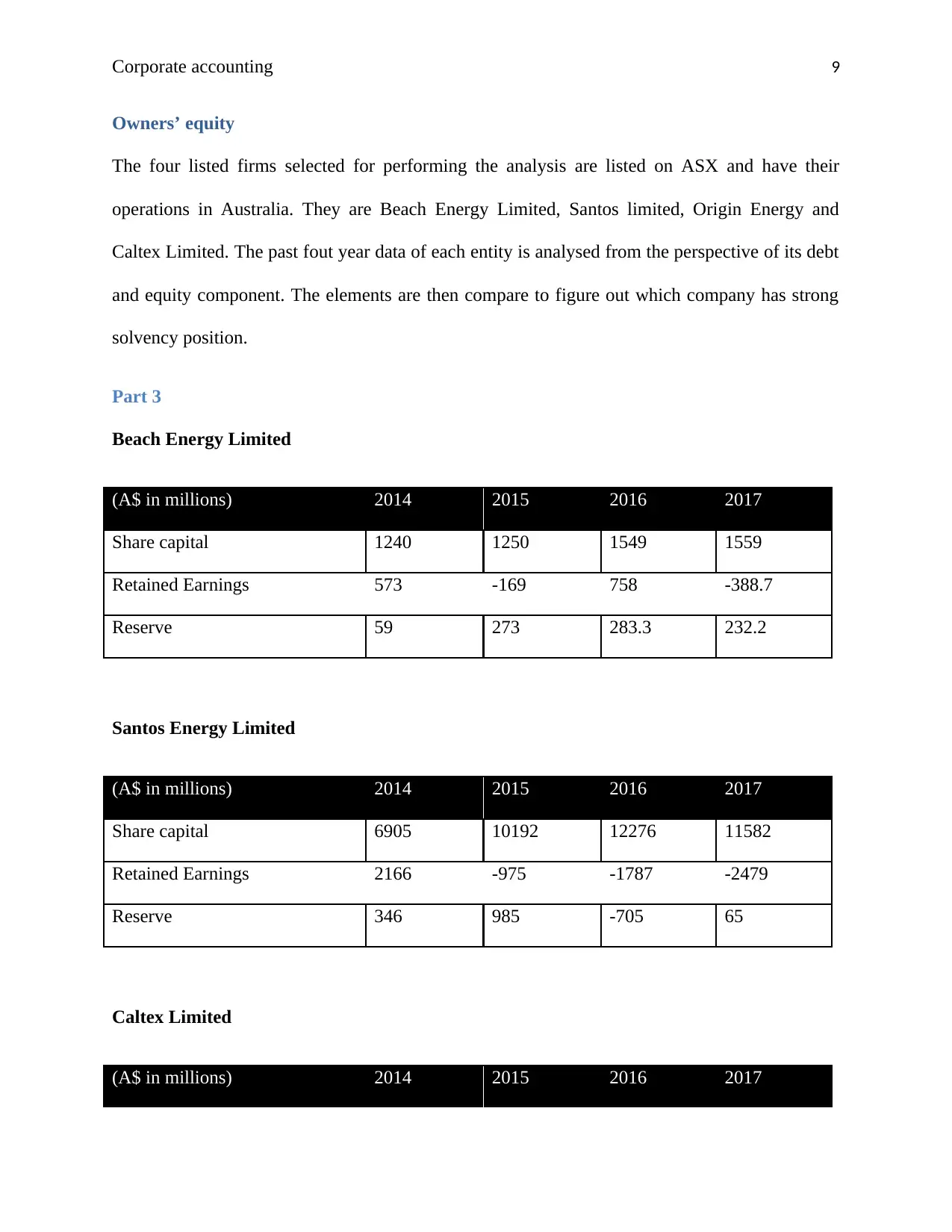

Owners’ equity

The four listed firms selected for performing the analysis are listed on ASX and have their

operations in Australia. They are Beach Energy Limited, Santos limited, Origin Energy and

Caltex Limited. The past fout year data of each entity is analysed from the perspective of its debt

and equity component. The elements are then compare to figure out which company has strong

solvency position.

Part 3

Beach Energy Limited

(A$ in millions) 2014 2015 2016 2017

Share capital 1240 1250 1549 1559

Retained Earnings 573 -169 758 -388.7

Reserve 59 273 283.3 232.2

Santos Energy Limited

(A$ in millions) 2014 2015 2016 2017

Share capital 6905 10192 12276 11582

Retained Earnings 2166 -975 -1787 -2479

Reserve 346 985 -705 65

Caltex Limited

(A$ in millions) 2014 2015 2016 2017

Owners’ equity

The four listed firms selected for performing the analysis are listed on ASX and have their

operations in Australia. They are Beach Energy Limited, Santos limited, Origin Energy and

Caltex Limited. The past fout year data of each entity is analysed from the perspective of its debt

and equity component. The elements are then compare to figure out which company has strong

solvency position.

Part 3

Beach Energy Limited

(A$ in millions) 2014 2015 2016 2017

Share capital 1240 1250 1549 1559

Retained Earnings 573 -169 758 -388.7

Reserve 59 273 283.3 232.2

Santos Energy Limited

(A$ in millions) 2014 2015 2016 2017

Share capital 6905 10192 12276 11582

Retained Earnings 2166 -975 -1787 -2479

Reserve 346 985 -705 65

Caltex Limited

(A$ in millions) 2014 2015 2016 2017

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate accounting 10

Share capital 543 543 525 524

Retained Earnings 1981 2242 2281 2610

Reserve -4 -9 -8 -40

Origin Energy

(A$ in millions) 2014 2015 2016 2017

Share capital 4520 4599 7150 7150

Retained Earnings 8754 7548 6502 3807

Reserve 160 576 857 439

Ordinary Share Capital: It is the amount raised by the company by issuing the number of

shares. It represents the capital invested by the owners or shareholders in the business.

Santos has the highest share capital which reflects the increased market value of the company

and its enhanced performance. Following it is the Origin Energy whose share capital has also

increased in the past four years. This reflected that company has increased its returns to attract

more investors towards the business (Morningstar. 2018).

Reserves: They represent the amount which is kept aside for the purpose of meeting

liabilities that might occur in future.

High reserves are maintained by Origin Energy and Santos Limited as compare to the other two

companies. Caltex reported negative reserves in the past years which mean the value of the

company has degraded due to its low profits.

Share capital 543 543 525 524

Retained Earnings 1981 2242 2281 2610

Reserve -4 -9 -8 -40

Origin Energy

(A$ in millions) 2014 2015 2016 2017

Share capital 4520 4599 7150 7150

Retained Earnings 8754 7548 6502 3807

Reserve 160 576 857 439

Ordinary Share Capital: It is the amount raised by the company by issuing the number of

shares. It represents the capital invested by the owners or shareholders in the business.

Santos has the highest share capital which reflects the increased market value of the company

and its enhanced performance. Following it is the Origin Energy whose share capital has also

increased in the past four years. This reflected that company has increased its returns to attract

more investors towards the business (Morningstar. 2018).

Reserves: They represent the amount which is kept aside for the purpose of meeting

liabilities that might occur in future.

High reserves are maintained by Origin Energy and Santos Limited as compare to the other two

companies. Caltex reported negative reserves in the past years which mean the value of the

company has degraded due to its low profits.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate accounting 11

Retained Earnings: It is the amount which is left after paying all the financial obligations

and liabilities. It reflects the figure retained by the company for making dividend

payments to its shareholders.

Caltex and Origin has high and positive RE in past years reflecting the improved profitability of

the companies. However, Santos reported negative earnings in 2016 and 2017 along with the

Beach Energy’s negative RE in 2017. This was due to the losses made by the companies in last

few years (Morningstar. 2018).

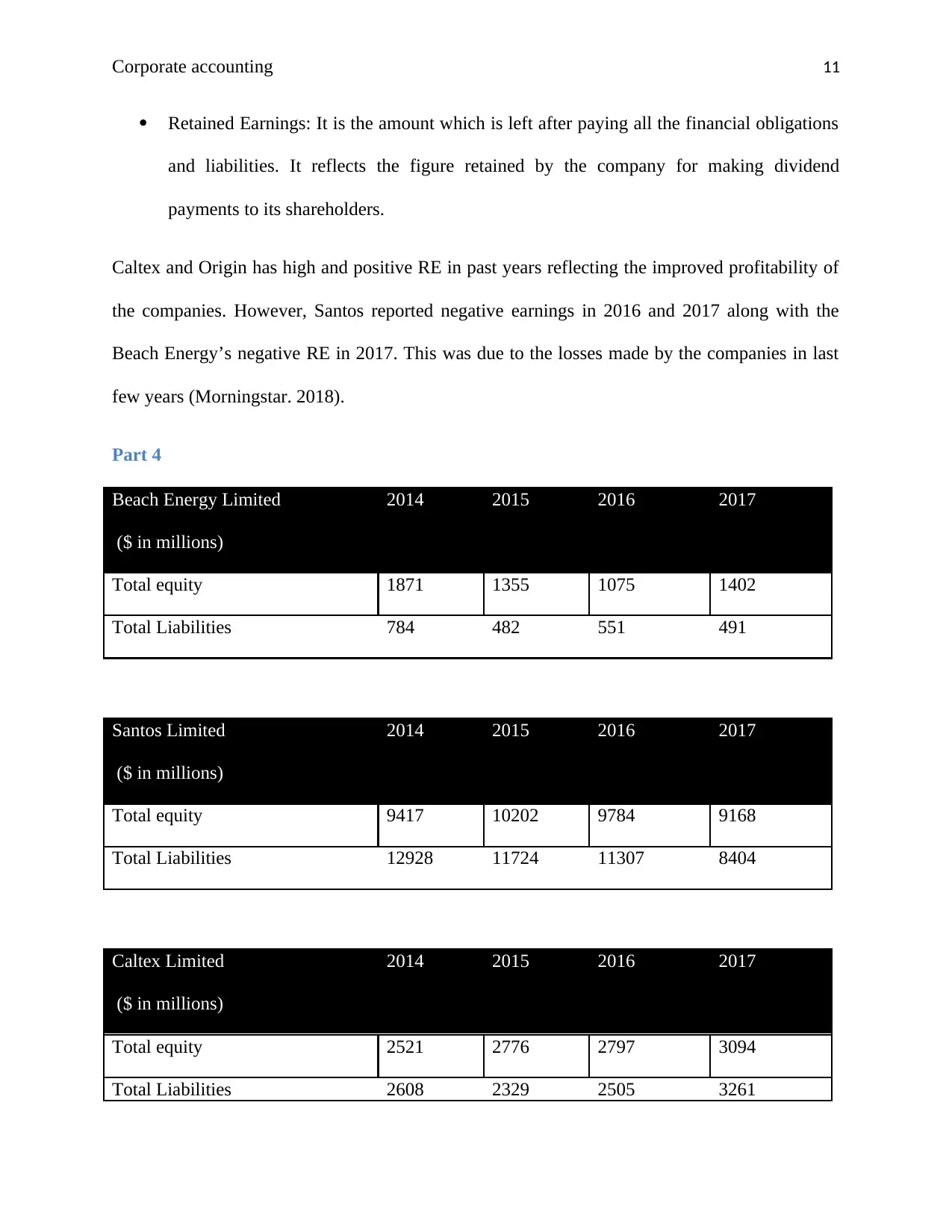

Part 4

Beach Energy Limited

($ in millions)

2014 2015 2016 2017

Total equity 1871 1355 1075 1402

Total Liabilities 784 482 551 491

Santos Limited

($ in millions)

2014 2015 2016 2017

Total equity 9417 10202 9784 9168

Total Liabilities 12928 11724 11307 8404

Caltex Limited

($ in millions)

2014 2015 2016 2017

Total equity 2521 2776 2797 3094

Total Liabilities 2608 2329 2505 3261

Retained Earnings: It is the amount which is left after paying all the financial obligations

and liabilities. It reflects the figure retained by the company for making dividend

payments to its shareholders.

Caltex and Origin has high and positive RE in past years reflecting the improved profitability of

the companies. However, Santos reported negative earnings in 2016 and 2017 along with the

Beach Energy’s negative RE in 2017. This was due to the losses made by the companies in last

few years (Morningstar. 2018).

Part 4

Beach Energy Limited

($ in millions)

2014 2015 2016 2017

Total equity 1871 1355 1075 1402

Total Liabilities 784 482 551 491

Santos Limited

($ in millions)

2014 2015 2016 2017

Total equity 9417 10202 9784 9168

Total Liabilities 12928 11724 11307 8404

Caltex Limited

($ in millions)

2014 2015 2016 2017

Total equity 2521 2776 2797 3094

Total Liabilities 2608 2329 2505 3261

Corporate accounting 12

Origin Energy

($ in millions)

2014 2015 2016 2017

Total equity 13444 12723 14509 11396

Total Liabilities 17695 20644 14389 13803

The analysis of debt and equity states the degree of financial leverage taken by the firm. It can be

observed that Beach energy has very low D/E ratio of 11% in 2017 as compare to the ratio of

Santos Limited which stands at 52% (Morningstar. 2018). Origin energy also has a high and

increased ratio of 74% whereas Caltex reported the ratio of 19% only. Among all it can be said

that Caltex has low financial leverage and a preferred mix of equity and debt as proportionate

increase in both has reduced its degree of financial leverage. Also, the low ratio of Beach energy

determines that company relies heavily on equity financing (Morningstar. 2018).

Conclusion

The above report concludes that from view point of financial risk, Beach energy and Caltex

limited has low risk as compare to the other companies. They are focused on reducing their debt

and increasing their equity component. However, from profitability point of view Caltex and

Origin has performed well in past years. The report also suggested that it is very much important

for the companies to properly comply with all the international accounting standards in order to

show a true and fair view of their performance and position.

Origin Energy

($ in millions)

2014 2015 2016 2017

Total equity 13444 12723 14509 11396

Total Liabilities 17695 20644 14389 13803

The analysis of debt and equity states the degree of financial leverage taken by the firm. It can be

observed that Beach energy has very low D/E ratio of 11% in 2017 as compare to the ratio of

Santos Limited which stands at 52% (Morningstar. 2018). Origin energy also has a high and

increased ratio of 74% whereas Caltex reported the ratio of 19% only. Among all it can be said

that Caltex has low financial leverage and a preferred mix of equity and debt as proportionate

increase in both has reduced its degree of financial leverage. Also, the low ratio of Beach energy

determines that company relies heavily on equity financing (Morningstar. 2018).

Conclusion

The above report concludes that from view point of financial risk, Beach energy and Caltex

limited has low risk as compare to the other companies. They are focused on reducing their debt

and increasing their equity component. However, from profitability point of view Caltex and

Origin has performed well in past years. The report also suggested that it is very much important

for the companies to properly comply with all the international accounting standards in order to

show a true and fair view of their performance and position.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.