HI5020 Corporate Accounting Report: ASX Companies Performance

VerifiedAdded on 2020/10/22

|41

|5234

|286

Report

AI Summary

This report provides a detailed analysis of the financial performance of three Australian Securities Exchange (ASX) listed companies operating in the retailing industry: Breville Group, Accent Group, and Joyce Corporation. The report examines key aspects of corporate accounting, including equity and liability positions, cash flow statements, other comprehensive income statements, and accounting for corporate income tax. It lists and analyzes the alterations in equity and liability items over three years, provides comparative analyses of debt and equity, and assesses the changes in cash flow from operating, investing, and financing activities. Additionally, the report explores items of comprehensive income, tax expenses, effective tax rates, and deferred tax assets and liabilities. The analysis is supported by data extracted from the companies' financial statements, offering insights into their financial health and performance over the specified period.

CORPORATE ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Corporate accounting sets a new standard and referred as recording, measurements along with

interpretation of financial information and data of limited organization. The present report is

related to retailing industry and companies listed on ASX. The accent retail business in

integrated with Hype business in its operating environment of Apparel. The other company is

Breville Group which sells electrical consumer products and home goods and Joyce corporation

retails wardrobe and kitchen products. It had shown that retailing industry is having various ups

and down which could be resolved by following appropriate strategy.

Corporate accounting sets a new standard and referred as recording, measurements along with

interpretation of financial information and data of limited organization. The present report is

related to retailing industry and companies listed on ASX. The accent retail business in

integrated with Hype business in its operating environment of Apparel. The other company is

Breville Group which sells electrical consumer products and home goods and Joyce corporation

retails wardrobe and kitchen products. It had shown that retailing industry is having various ups

and down which could be resolved by following appropriate strategy.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................5

EQUITY & LIABILITY..................................................................................................................5

1. Listing item of equity with its alteration over last three years................................................5

2. Listing item of liability with its change over 3 years..............................................................6

3. Comparative analysis of debt and equity position of three business....................................10

CASH FLOW STATEMENT .......................................................................................................10

4. Listing items of cash flow with its changes..........................................................................10

5. Comparative analysis of broad categories of cash flow........................................................11

6. Comparative analysis of three companies.............................................................................13

OTHER COMPREHENSIVE INCOME STATEMENT .............................................................13

7. Stating items of comprehensive income statement for each organisation............................13

8. Reason of these items not stated in income statement..........................................................14

9. Comparative analysis of other comprehensive income statements.......................................14

10. OCI must be used for evaluating performance of managers of organization.....................15

ACCOUNTING FOR CORPORATE INCOME TAX..................................................................15

11. Tax expenses in the latest financial statements...................................................................15

12. Calculating effective tax rate..............................................................................................15

13. Commenting on deferred tax assets and liability................................................................16

14. Increment or decrement in deferred tax asset and liability.................................................16

15. Calculating cash tax amount...............................................................................................17

16. Calculating cash tax rate.....................................................................................................18

17. Reason of differing cash tax rate from book tax rate..........................................................19

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................21

APPENDIX....................................................................................................................................22

Breville group- 2018.................................................................................................................22

Breville group- 2017.................................................................................................................24

Accent Group 2017...................................................................................................................28

........................................................................................................................................................32

INTRODUCTION...........................................................................................................................5

EQUITY & LIABILITY..................................................................................................................5

1. Listing item of equity with its alteration over last three years................................................5

2. Listing item of liability with its change over 3 years..............................................................6

3. Comparative analysis of debt and equity position of three business....................................10

CASH FLOW STATEMENT .......................................................................................................10

4. Listing items of cash flow with its changes..........................................................................10

5. Comparative analysis of broad categories of cash flow........................................................11

6. Comparative analysis of three companies.............................................................................13

OTHER COMPREHENSIVE INCOME STATEMENT .............................................................13

7. Stating items of comprehensive income statement for each organisation............................13

8. Reason of these items not stated in income statement..........................................................14

9. Comparative analysis of other comprehensive income statements.......................................14

10. OCI must be used for evaluating performance of managers of organization.....................15

ACCOUNTING FOR CORPORATE INCOME TAX..................................................................15

11. Tax expenses in the latest financial statements...................................................................15

12. Calculating effective tax rate..............................................................................................15

13. Commenting on deferred tax assets and liability................................................................16

14. Increment or decrement in deferred tax asset and liability.................................................16

15. Calculating cash tax amount...............................................................................................17

16. Calculating cash tax rate.....................................................................................................18

17. Reason of differing cash tax rate from book tax rate..........................................................19

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................21

APPENDIX....................................................................................................................................22

Breville group- 2018.................................................................................................................22

Breville group- 2017.................................................................................................................24

Accent Group 2017...................................................................................................................28

........................................................................................................................................................32

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Joyce Corporation 2016-...........................................................................................................35

Joyce corporation 2017-2018....................................................................................................37

Joyce corporation 2017-2018....................................................................................................37

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

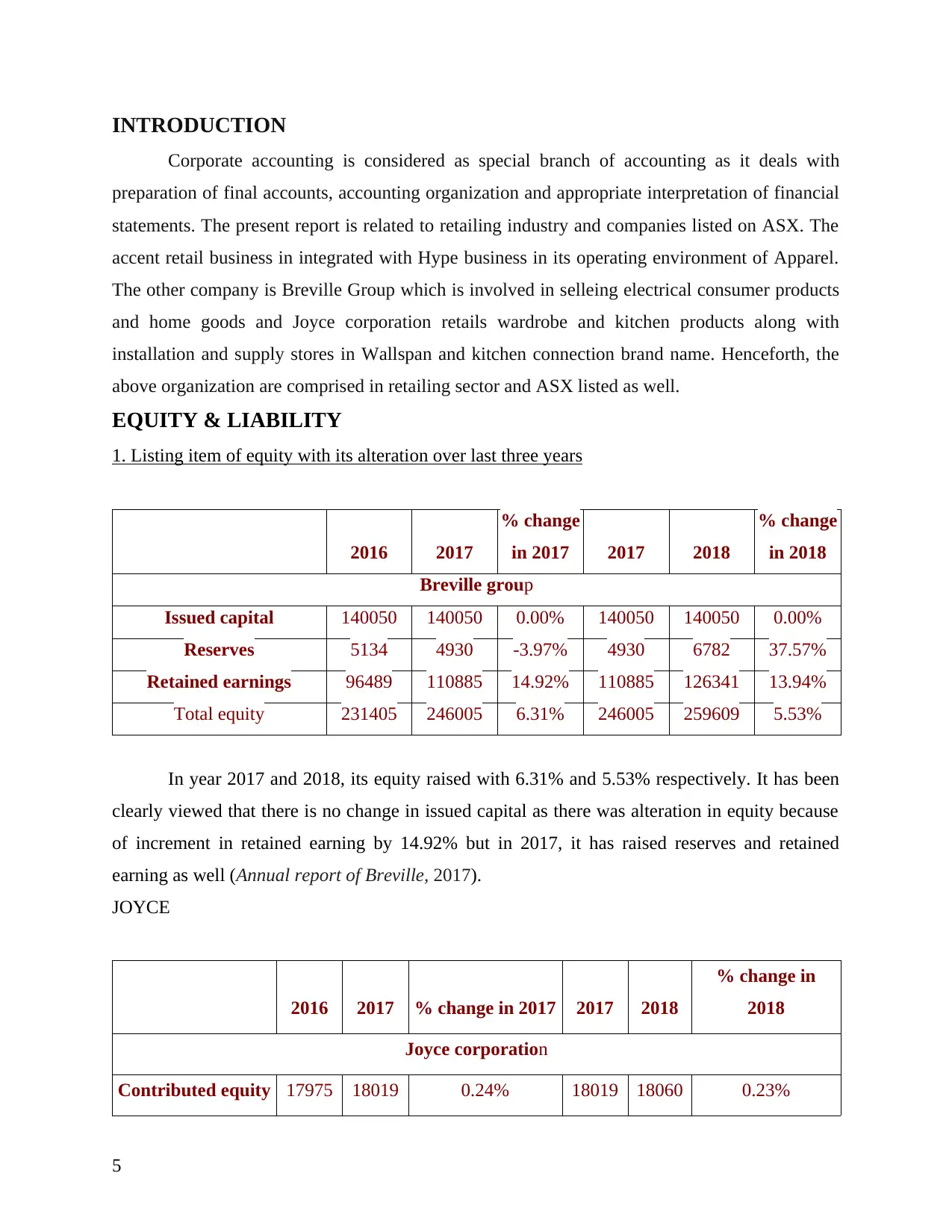

INTRODUCTION

Corporate accounting is considered as special branch of accounting as it deals with

preparation of final accounts, accounting organization and appropriate interpretation of financial

statements. The present report is related to retailing industry and companies listed on ASX. The

accent retail business in integrated with Hype business in its operating environment of Apparel.

The other company is Breville Group which is involved in selleing electrical consumer products

and home goods and Joyce corporation retails wardrobe and kitchen products along with

installation and supply stores in Wallspan and kitchen connection brand name. Henceforth, the

above organization are comprised in retailing sector and ASX listed as well.

EQUITY & LIABILITY

1. Listing item of equity with its alteration over last three years

2016 2017

% change

in 2017 2017 2018

% change

in 2018

Breville group

Issued capital 140050 140050 0.00% 140050 140050 0.00%

Reserves 5134 4930 -3.97% 4930 6782 37.57%

Retained earnings 96489 110885 14.92% 110885 126341 13.94%

Total equity 231405 246005 6.31% 246005 259609 5.53%

In year 2017 and 2018, its equity raised with 6.31% and 5.53% respectively. It has been

clearly viewed that there is no change in issued capital as there was alteration in equity because

of increment in retained earning by 14.92% but in 2017, it has raised reserves and retained

earning as well (Annual report of Breville, 2017).

JOYCE

2016 2017 % change in 2017 2017 2018

% change in

2018

Joyce corporation

Contributed equity 17975 18019 0.24% 18019 18060 0.23%

5

Corporate accounting is considered as special branch of accounting as it deals with

preparation of final accounts, accounting organization and appropriate interpretation of financial

statements. The present report is related to retailing industry and companies listed on ASX. The

accent retail business in integrated with Hype business in its operating environment of Apparel.

The other company is Breville Group which is involved in selleing electrical consumer products

and home goods and Joyce corporation retails wardrobe and kitchen products along with

installation and supply stores in Wallspan and kitchen connection brand name. Henceforth, the

above organization are comprised in retailing sector and ASX listed as well.

EQUITY & LIABILITY

1. Listing item of equity with its alteration over last three years

2016 2017

% change

in 2017 2017 2018

% change

in 2018

Breville group

Issued capital 140050 140050 0.00% 140050 140050 0.00%

Reserves 5134 4930 -3.97% 4930 6782 37.57%

Retained earnings 96489 110885 14.92% 110885 126341 13.94%

Total equity 231405 246005 6.31% 246005 259609 5.53%

In year 2017 and 2018, its equity raised with 6.31% and 5.53% respectively. It has been

clearly viewed that there is no change in issued capital as there was alteration in equity because

of increment in retained earning by 14.92% but in 2017, it has raised reserves and retained

earning as well (Annual report of Breville, 2017).

JOYCE

2016 2017 % change in 2017 2017 2018

% change in

2018

Joyce corporation

Contributed equity 17975 18019 0.24% 18019 18060 0.23%

5

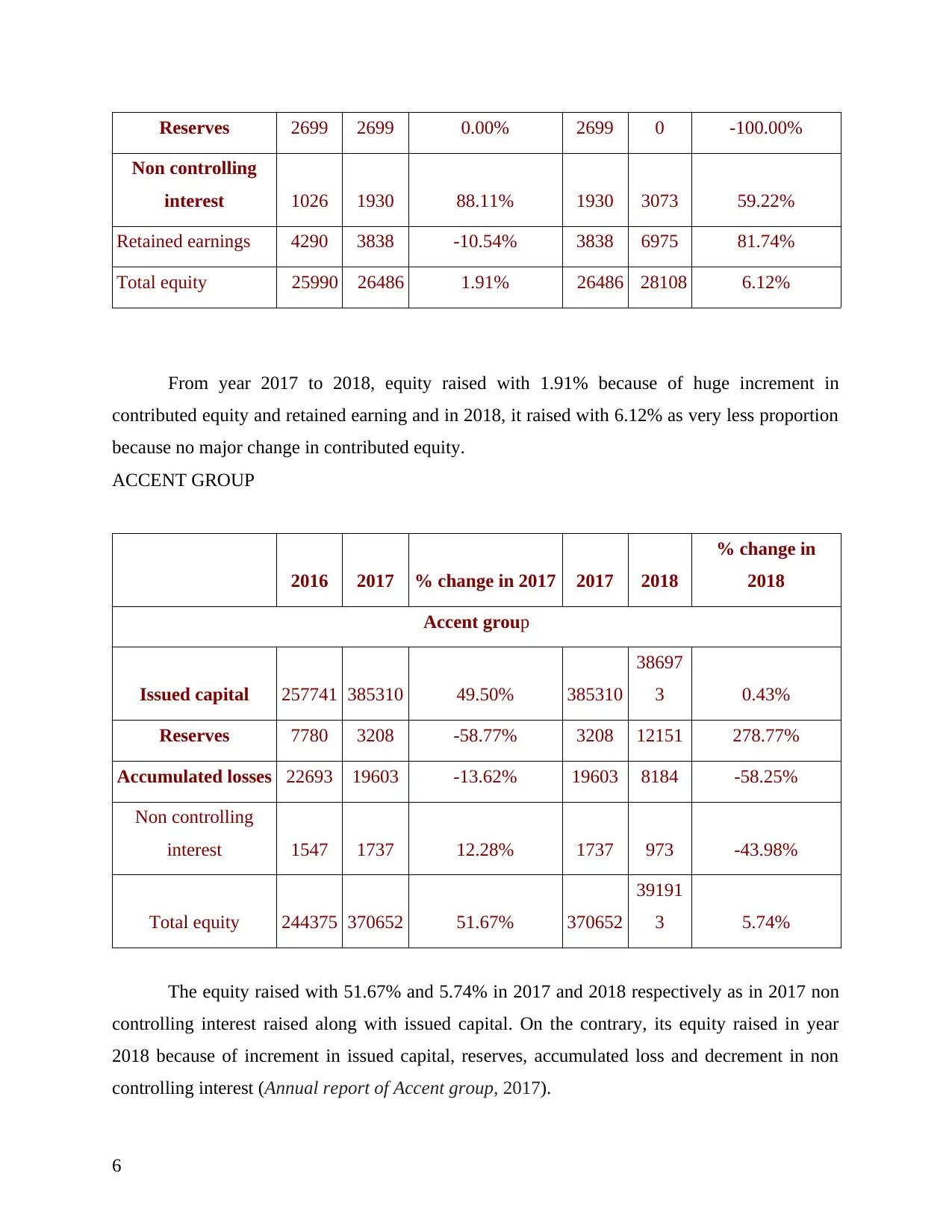

Reserves 2699 2699 0.00% 2699 0 -100.00%

Non controlling

interest 1026 1930 88.11% 1930 3073 59.22%

Retained earnings 4290 3838 -10.54% 3838 6975 81.74%

Total equity 25990 26486 1.91% 26486 28108 6.12%

From year 2017 to 2018, equity raised with 1.91% because of huge increment in

contributed equity and retained earning and in 2018, it raised with 6.12% as very less proportion

because no major change in contributed equity.

ACCENT GROUP

2016 2017 % change in 2017 2017 2018

% change in

2018

Accent group

Issued capital 257741 385310 49.50% 385310

38697

3 0.43%

Reserves 7780 3208 -58.77% 3208 12151 278.77%

Accumulated losses 22693 19603 -13.62% 19603 8184 -58.25%

Non controlling

interest 1547 1737 12.28% 1737 973 -43.98%

Total equity 244375 370652 51.67% 370652

39191

3 5.74%

The equity raised with 51.67% and 5.74% in 2017 and 2018 respectively as in 2017 non

controlling interest raised along with issued capital. On the contrary, its equity raised in year

2018 because of increment in issued capital, reserves, accumulated loss and decrement in non

controlling interest (Annual report of Accent group, 2017).

6

Non controlling

interest 1026 1930 88.11% 1930 3073 59.22%

Retained earnings 4290 3838 -10.54% 3838 6975 81.74%

Total equity 25990 26486 1.91% 26486 28108 6.12%

From year 2017 to 2018, equity raised with 1.91% because of huge increment in

contributed equity and retained earning and in 2018, it raised with 6.12% as very less proportion

because no major change in contributed equity.

ACCENT GROUP

2016 2017 % change in 2017 2017 2018

% change in

2018

Accent group

Issued capital 257741 385310 49.50% 385310

38697

3 0.43%

Reserves 7780 3208 -58.77% 3208 12151 278.77%

Accumulated losses 22693 19603 -13.62% 19603 8184 -58.25%

Non controlling

interest 1547 1737 12.28% 1737 973 -43.98%

Total equity 244375 370652 51.67% 370652

39191

3 5.74%

The equity raised with 51.67% and 5.74% in 2017 and 2018 respectively as in 2017 non

controlling interest raised along with issued capital. On the contrary, its equity raised in year

2018 because of increment in issued capital, reserves, accumulated loss and decrement in non

controlling interest (Annual report of Accent group, 2017).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

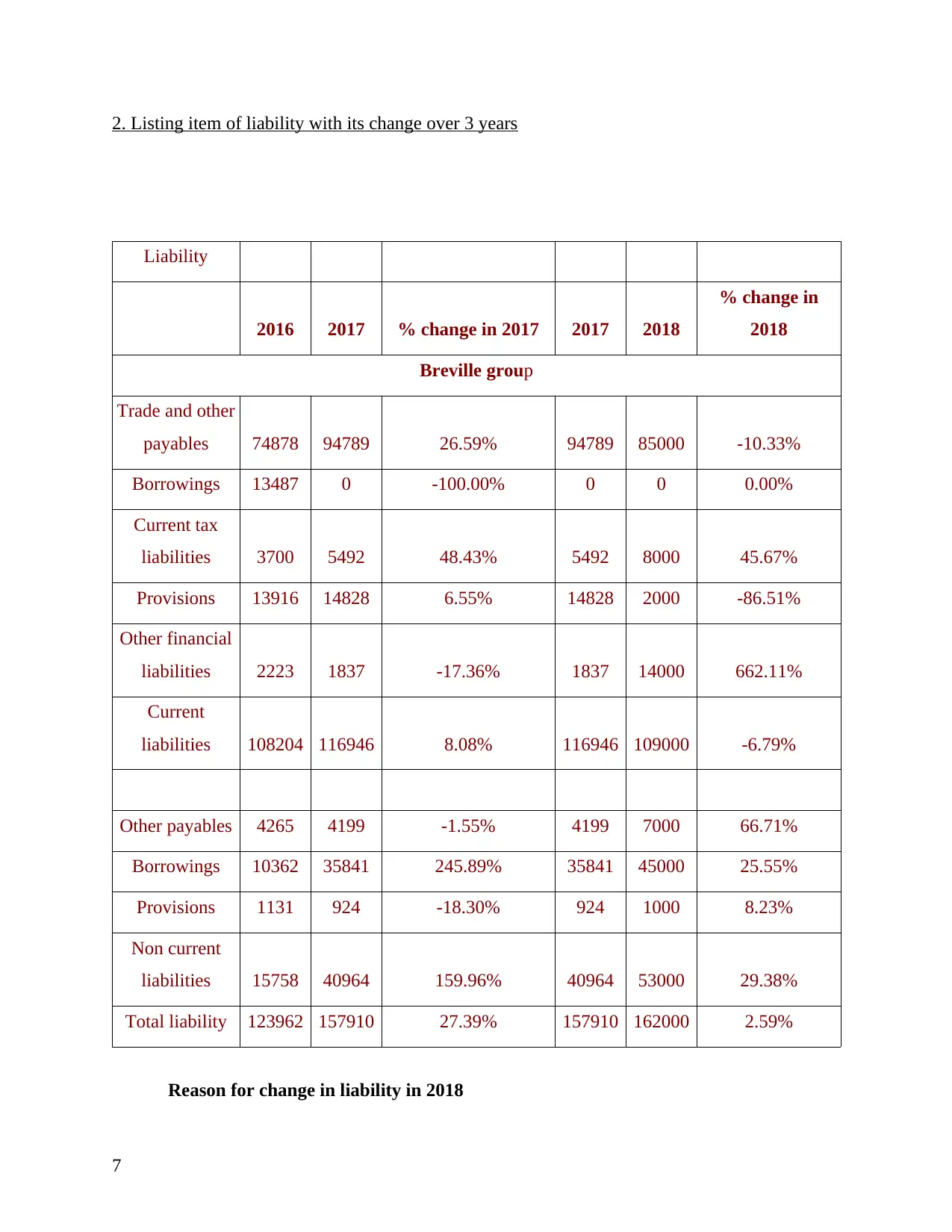

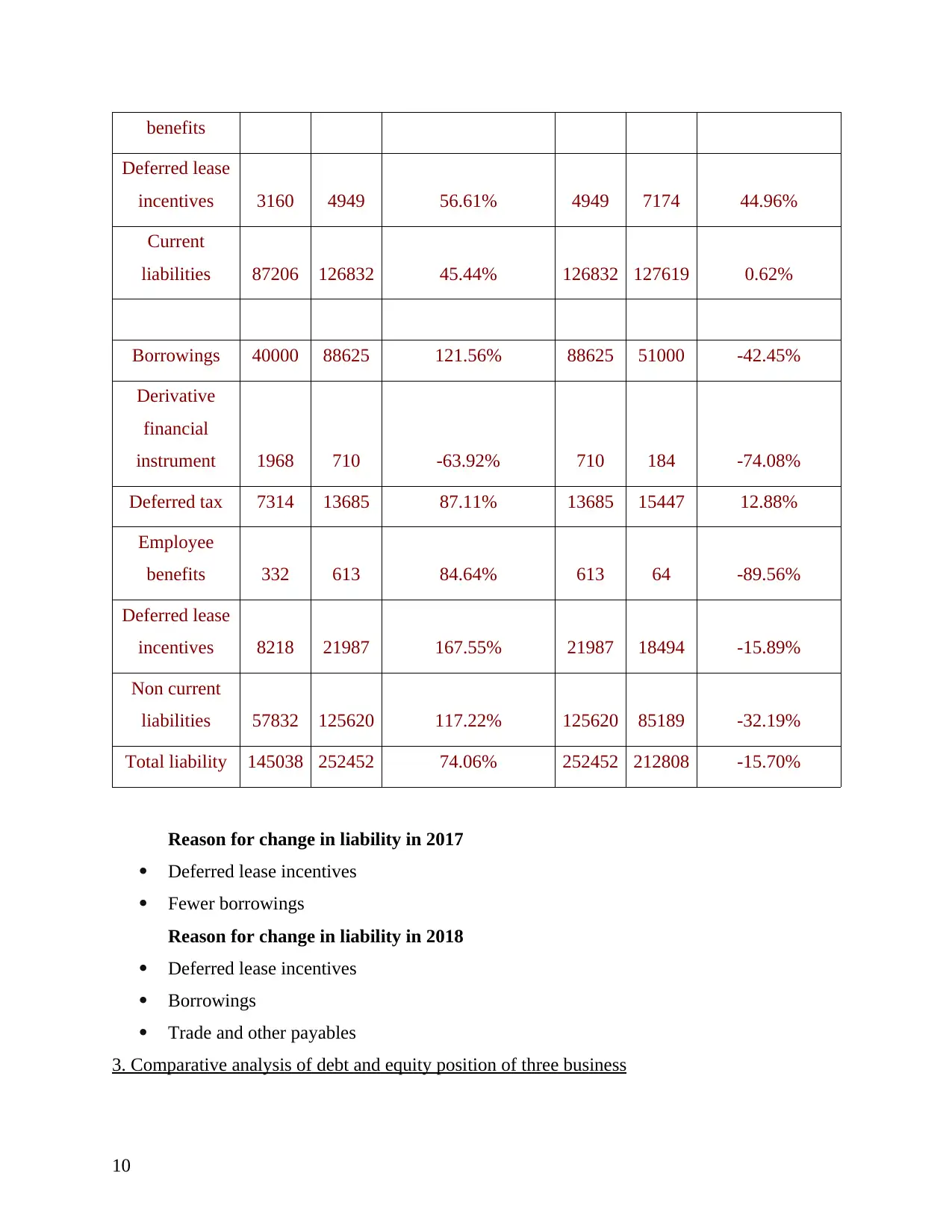

2. Listing item of liability with its change over 3 years

Liability

2016 2017 % change in 2017 2017 2018

% change in

2018

Breville group

Trade and other

payables 74878 94789 26.59% 94789 85000 -10.33%

Borrowings 13487 0 -100.00% 0 0 0.00%

Current tax

liabilities 3700 5492 48.43% 5492 8000 45.67%

Provisions 13916 14828 6.55% 14828 2000 -86.51%

Other financial

liabilities 2223 1837 -17.36% 1837 14000 662.11%

Current

liabilities 108204 116946 8.08% 116946 109000 -6.79%

Other payables 4265 4199 -1.55% 4199 7000 66.71%

Borrowings 10362 35841 245.89% 35841 45000 25.55%

Provisions 1131 924 -18.30% 924 1000 8.23%

Non current

liabilities 15758 40964 159.96% 40964 53000 29.38%

Total liability 123962 157910 27.39% 157910 162000 2.59%

Reason for change in liability in 2018

7

Liability

2016 2017 % change in 2017 2017 2018

% change in

2018

Breville group

Trade and other

payables 74878 94789 26.59% 94789 85000 -10.33%

Borrowings 13487 0 -100.00% 0 0 0.00%

Current tax

liabilities 3700 5492 48.43% 5492 8000 45.67%

Provisions 13916 14828 6.55% 14828 2000 -86.51%

Other financial

liabilities 2223 1837 -17.36% 1837 14000 662.11%

Current

liabilities 108204 116946 8.08% 116946 109000 -6.79%

Other payables 4265 4199 -1.55% 4199 7000 66.71%

Borrowings 10362 35841 245.89% 35841 45000 25.55%

Provisions 1131 924 -18.30% 924 1000 8.23%

Non current

liabilities 15758 40964 159.96% 40964 53000 29.38%

Total liability 123962 157910 27.39% 157910 162000 2.59%

Reason for change in liability in 2018

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Trade and other payables: Amount owned through suppliers and not paid on immediate

basis in form of cash are not replicated as trade payable is decreased.

Other payables

Borrowings: The total amount of collateral against lender will lend funds related to

business. Breville group reduced its borrowing in year 2018

Provisions

Reason for change in liability in 2017

Huge borrowings

JOYCE

2016 2017 % change in 2017 2017 2018

% change in

2018

Joyce Corporation

Trade and other

payables 8864 10073 13.64% 10073 11779 16.94%

Provisions 1000 1361 36.10% 1361 1528 12.27%

Interest bearing

loans 0 0 0.00% 0 435 0.00%

Provisions for

income tax 1153 1153 0.00% 1153 820 -28.88%

Current

liabilities 11017 12587 14.25% 12587 14562 15.69%

Interest bearing 0 8600 0.00% 8600 10056 16.93%

8

basis in form of cash are not replicated as trade payable is decreased.

Other payables

Borrowings: The total amount of collateral against lender will lend funds related to

business. Breville group reduced its borrowing in year 2018

Provisions

Reason for change in liability in 2017

Huge borrowings

JOYCE

2016 2017 % change in 2017 2017 2018

% change in

2018

Joyce Corporation

Trade and other

payables 8864 10073 13.64% 10073 11779 16.94%

Provisions 1000 1361 36.10% 1361 1528 12.27%

Interest bearing

loans 0 0 0.00% 0 435 0.00%

Provisions for

income tax 1153 1153 0.00% 1153 820 -28.88%

Current

liabilities 11017 12587 14.25% 12587 14562 15.69%

Interest bearing 0 8600 0.00% 8600 10056 16.93%

8

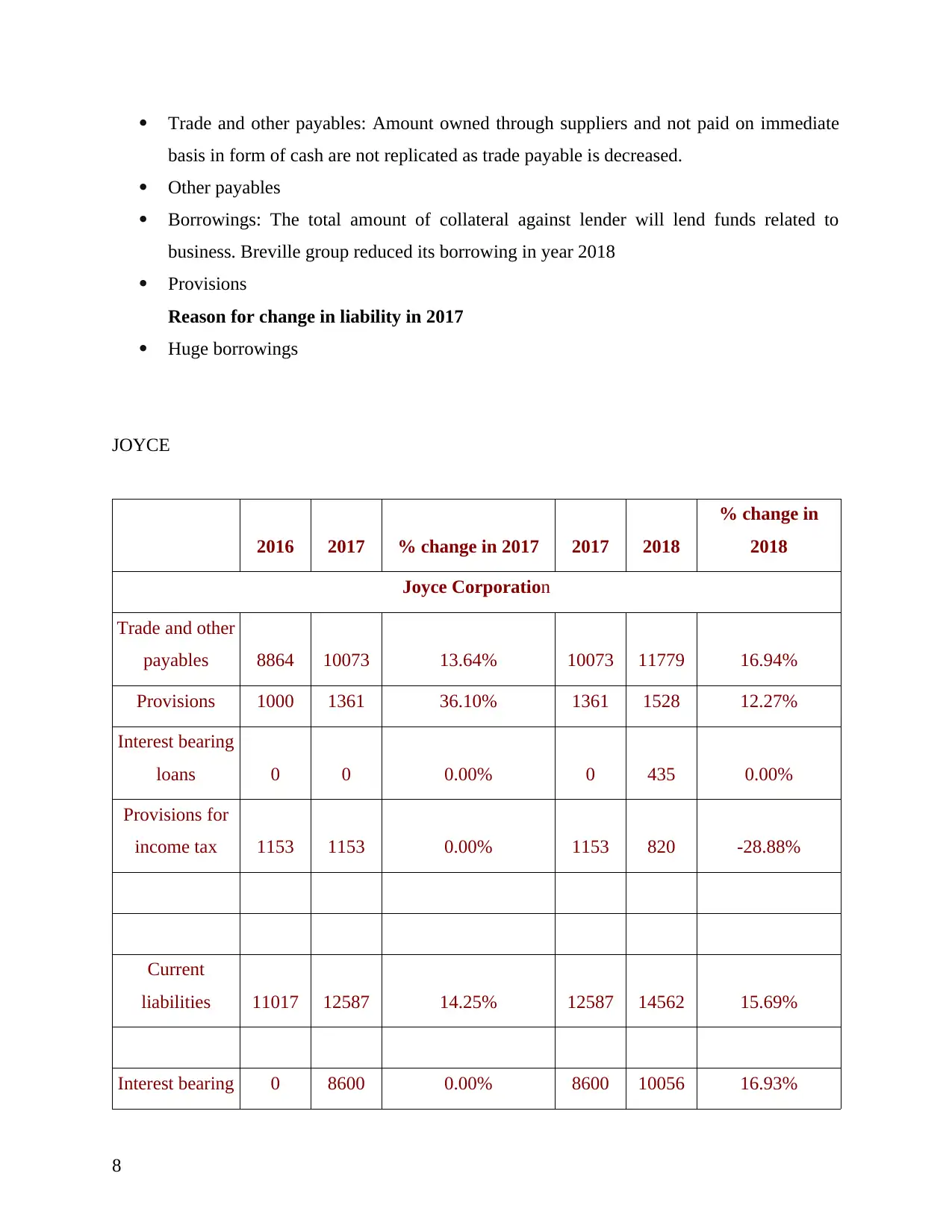

loans

Deferred tax

liabilities 317 262 -17.35% 262 554 111.45%

Provisions 962 712 -25.99% 712 818 14.89%

Non current

liabilities 1279 9574 648.55% 9574 11428 19.36%

Total liability 12296 22161 80.23% 22161 25990 17.28%

Reason for change in liability in 2018

Huge provisions

Reason for change in liability in 2017

Decrement in derivative financial instrument

Trade and other payables (increase)

2016 2017 % change in 2017 2017 2018

% change in

2018

Accent group

Trade and other

payables 58986 88849 50.63% 88849 80965 -8.87%

Borrowings 10013 15097 50.77% 15097 22625 49.86%

Derivative

financial

instrument 6608 5054 -23.52% 5054 251 -95.03%

Income tax 5236 7990 52.60% 7990 10497 31.38%

Employee 3203 4893 52.76% 4893 6107 24.81%

9

Deferred tax

liabilities 317 262 -17.35% 262 554 111.45%

Provisions 962 712 -25.99% 712 818 14.89%

Non current

liabilities 1279 9574 648.55% 9574 11428 19.36%

Total liability 12296 22161 80.23% 22161 25990 17.28%

Reason for change in liability in 2018

Huge provisions

Reason for change in liability in 2017

Decrement in derivative financial instrument

Trade and other payables (increase)

2016 2017 % change in 2017 2017 2018

% change in

2018

Accent group

Trade and other

payables 58986 88849 50.63% 88849 80965 -8.87%

Borrowings 10013 15097 50.77% 15097 22625 49.86%

Derivative

financial

instrument 6608 5054 -23.52% 5054 251 -95.03%

Income tax 5236 7990 52.60% 7990 10497 31.38%

Employee 3203 4893 52.76% 4893 6107 24.81%

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

benefits

Deferred lease

incentives 3160 4949 56.61% 4949 7174 44.96%

Current

liabilities 87206 126832 45.44% 126832 127619 0.62%

Borrowings 40000 88625 121.56% 88625 51000 -42.45%

Derivative

financial

instrument 1968 710 -63.92% 710 184 -74.08%

Deferred tax 7314 13685 87.11% 13685 15447 12.88%

Employee

benefits 332 613 84.64% 613 64 -89.56%

Deferred lease

incentives 8218 21987 167.55% 21987 18494 -15.89%

Non current

liabilities 57832 125620 117.22% 125620 85189 -32.19%

Total liability 145038 252452 74.06% 252452 212808 -15.70%

Reason for change in liability in 2017

Deferred lease incentives

Fewer borrowings

Reason for change in liability in 2018

Deferred lease incentives

Borrowings

Trade and other payables

3. Comparative analysis of debt and equity position of three business

10

Deferred lease

incentives 3160 4949 56.61% 4949 7174 44.96%

Current

liabilities 87206 126832 45.44% 126832 127619 0.62%

Borrowings 40000 88625 121.56% 88625 51000 -42.45%

Derivative

financial

instrument 1968 710 -63.92% 710 184 -74.08%

Deferred tax 7314 13685 87.11% 13685 15447 12.88%

Employee

benefits 332 613 84.64% 613 64 -89.56%

Deferred lease

incentives 8218 21987 167.55% 21987 18494 -15.89%

Non current

liabilities 57832 125620 117.22% 125620 85189 -32.19%

Total liability 145038 252452 74.06% 252452 212808 -15.70%

Reason for change in liability in 2017

Deferred lease incentives

Fewer borrowings

Reason for change in liability in 2018

Deferred lease incentives

Borrowings

Trade and other payables

3. Comparative analysis of debt and equity position of three business

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

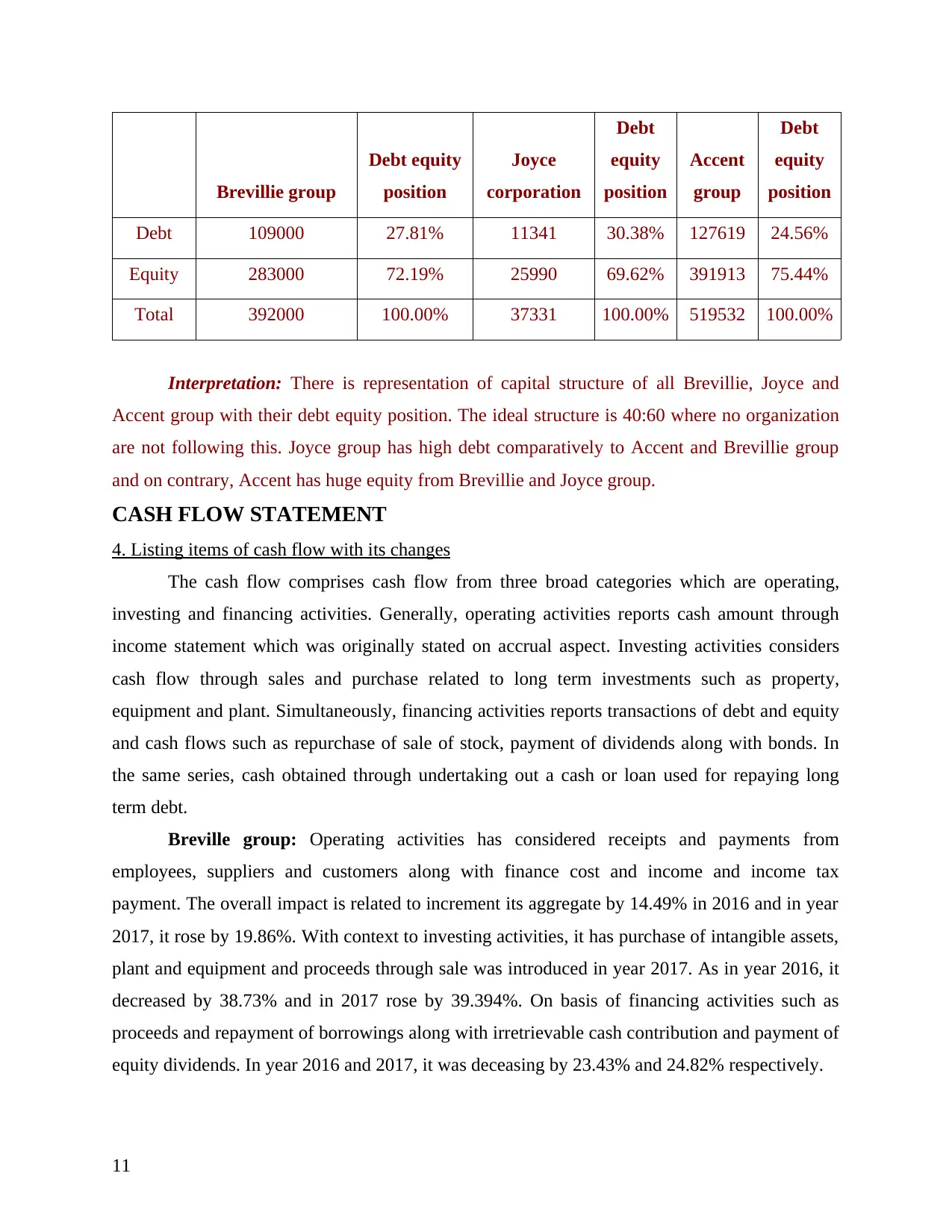

Brevillie group

Debt equity

position

Joyce

corporation

Debt

equity

position

Accent

group

Debt

equity

position

Debt 109000 27.81% 11341 30.38% 127619 24.56%

Equity 283000 72.19% 25990 69.62% 391913 75.44%

Total 392000 100.00% 37331 100.00% 519532 100.00%

Interpretation: There is representation of capital structure of all Brevillie, Joyce and

Accent group with their debt equity position. The ideal structure is 40:60 where no organization

are not following this. Joyce group has high debt comparatively to Accent and Brevillie group

and on contrary, Accent has huge equity from Brevillie and Joyce group.

CASH FLOW STATEMENT

4. Listing items of cash flow with its changes

The cash flow comprises cash flow from three broad categories which are operating,

investing and financing activities. Generally, operating activities reports cash amount through

income statement which was originally stated on accrual aspect. Investing activities considers

cash flow through sales and purchase related to long term investments such as property,

equipment and plant. Simultaneously, financing activities reports transactions of debt and equity

and cash flows such as repurchase of sale of stock, payment of dividends along with bonds. In

the same series, cash obtained through undertaking out a cash or loan used for repaying long

term debt.

Breville group: Operating activities has considered receipts and payments from

employees, suppliers and customers along with finance cost and income and income tax

payment. The overall impact is related to increment its aggregate by 14.49% in 2016 and in year

2017, it rose by 19.86%. With context to investing activities, it has purchase of intangible assets,

plant and equipment and proceeds through sale was introduced in year 2017. As in year 2016, it

decreased by 38.73% and in 2017 rose by 39.394%. On basis of financing activities such as

proceeds and repayment of borrowings along with irretrievable cash contribution and payment of

equity dividends. In year 2016 and 2017, it was deceasing by 23.43% and 24.82% respectively.

11

Debt equity

position

Joyce

corporation

Debt

equity

position

Accent

group

Debt

equity

position

Debt 109000 27.81% 11341 30.38% 127619 24.56%

Equity 283000 72.19% 25990 69.62% 391913 75.44%

Total 392000 100.00% 37331 100.00% 519532 100.00%

Interpretation: There is representation of capital structure of all Brevillie, Joyce and

Accent group with their debt equity position. The ideal structure is 40:60 where no organization

are not following this. Joyce group has high debt comparatively to Accent and Brevillie group

and on contrary, Accent has huge equity from Brevillie and Joyce group.

CASH FLOW STATEMENT

4. Listing items of cash flow with its changes

The cash flow comprises cash flow from three broad categories which are operating,

investing and financing activities. Generally, operating activities reports cash amount through

income statement which was originally stated on accrual aspect. Investing activities considers

cash flow through sales and purchase related to long term investments such as property,

equipment and plant. Simultaneously, financing activities reports transactions of debt and equity

and cash flows such as repurchase of sale of stock, payment of dividends along with bonds. In

the same series, cash obtained through undertaking out a cash or loan used for repaying long

term debt.

Breville group: Operating activities has considered receipts and payments from

employees, suppliers and customers along with finance cost and income and income tax

payment. The overall impact is related to increment its aggregate by 14.49% in 2016 and in year

2017, it rose by 19.86%. With context to investing activities, it has purchase of intangible assets,

plant and equipment and proceeds through sale was introduced in year 2017. As in year 2016, it

decreased by 38.73% and in 2017 rose by 39.394%. On basis of financing activities such as

proceeds and repayment of borrowings along with irretrievable cash contribution and payment of

equity dividends. In year 2016 and 2017, it was deceasing by 23.43% and 24.82% respectively.

11

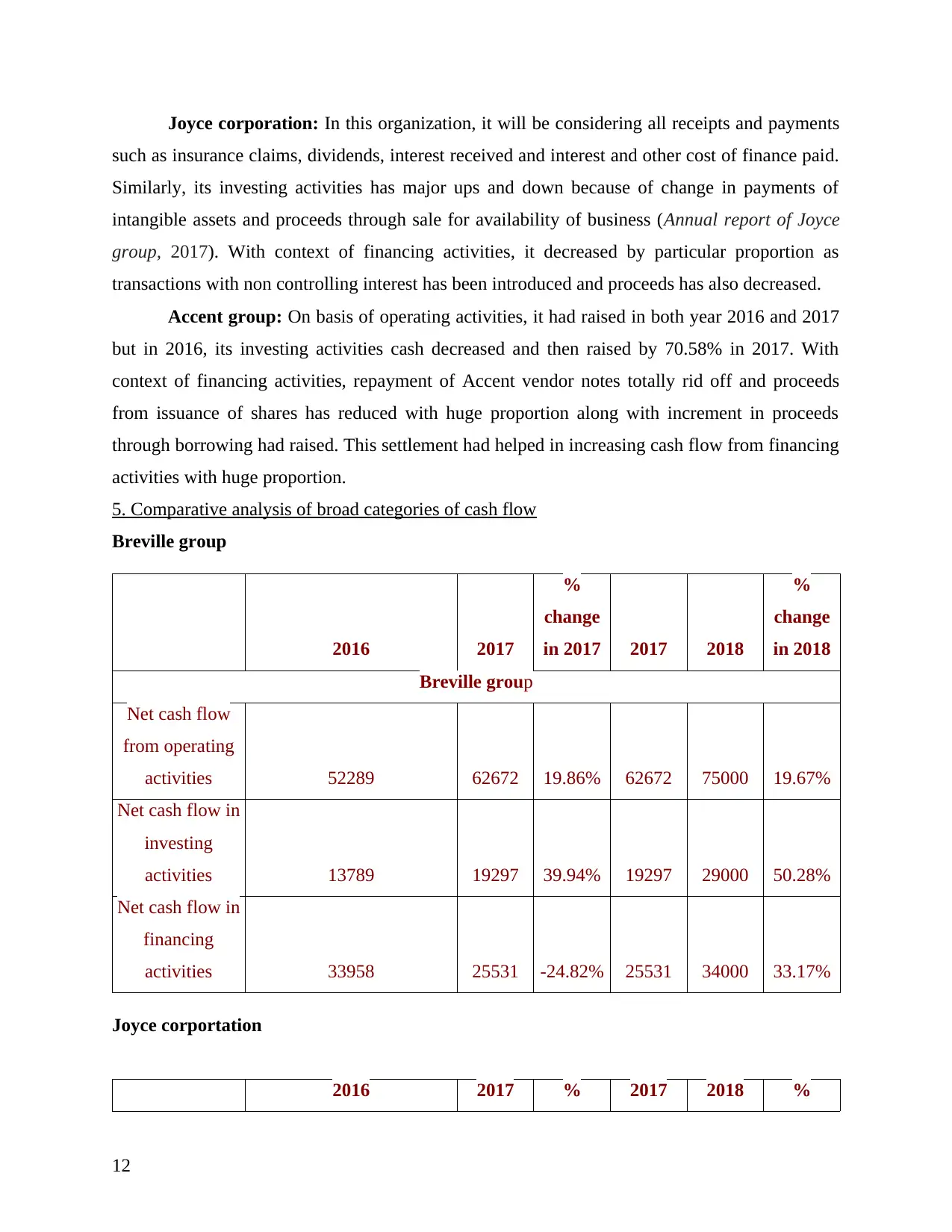

Joyce corporation: In this organization, it will be considering all receipts and payments

such as insurance claims, dividends, interest received and interest and other cost of finance paid.

Similarly, its investing activities has major ups and down because of change in payments of

intangible assets and proceeds through sale for availability of business (Annual report of Joyce

group, 2017). With context of financing activities, it decreased by particular proportion as

transactions with non controlling interest has been introduced and proceeds has also decreased.

Accent group: On basis of operating activities, it had raised in both year 2016 and 2017

but in 2016, its investing activities cash decreased and then raised by 70.58% in 2017. With

context of financing activities, repayment of Accent vendor notes totally rid off and proceeds

from issuance of shares has reduced with huge proportion along with increment in proceeds

through borrowing had raised. This settlement had helped in increasing cash flow from financing

activities with huge proportion.

5. Comparative analysis of broad categories of cash flow

Breville group

2016 2017

%

change

in 2017 2017 2018

%

change

in 2018

Breville group

Net cash flow

from operating

activities 52289 62672 19.86% 62672 75000 19.67%

Net cash flow in

investing

activities 13789 19297 39.94% 19297 29000 50.28%

Net cash flow in

financing

activities 33958 25531 -24.82% 25531 34000 33.17%

Joyce corportation

2016 2017 % 2017 2018 %

12

such as insurance claims, dividends, interest received and interest and other cost of finance paid.

Similarly, its investing activities has major ups and down because of change in payments of

intangible assets and proceeds through sale for availability of business (Annual report of Joyce

group, 2017). With context of financing activities, it decreased by particular proportion as

transactions with non controlling interest has been introduced and proceeds has also decreased.

Accent group: On basis of operating activities, it had raised in both year 2016 and 2017

but in 2016, its investing activities cash decreased and then raised by 70.58% in 2017. With

context of financing activities, repayment of Accent vendor notes totally rid off and proceeds

from issuance of shares has reduced with huge proportion along with increment in proceeds

through borrowing had raised. This settlement had helped in increasing cash flow from financing

activities with huge proportion.

5. Comparative analysis of broad categories of cash flow

Breville group

2016 2017

%

change

in 2017 2017 2018

%

change

in 2018

Breville group

Net cash flow

from operating

activities 52289 62672 19.86% 62672 75000 19.67%

Net cash flow in

investing

activities 13789 19297 39.94% 19297 29000 50.28%

Net cash flow in

financing

activities 33958 25531 -24.82% 25531 34000 33.17%

Joyce corportation

2016 2017 % 2017 2018 %

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 41

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.