Corporate Accounting Report: Woolworths, Spotless, and Orion Analysis

VerifiedAdded on 2020/07/22

|15

|3486

|31

Report

AI Summary

This report delves into various aspects of corporate accounting, using Woolworths Ltd, Spotless Group Holdings, and Orion Ltd as case studies. The analysis begins with an examination of Woolworths' board composition, including director qualifications, experience, and other board affiliations. It then evaluates Woolworths' financial performance, assessing profitability, equity growth, and opportunities for future expansion, while also identifying current business challenges and contributions to social and environmental sustainability. The report further explores lease accounting, differentiating between operating and financial leases used by Woolworths, and analyzing the reasons behind these choices. It examines how leases are recorded in the company's annual report and discusses the advantages and disadvantages of different lease types. The report also addresses the introduction of lease standard AASB 117. Finally, the report investigates the lease arrangements undertaken by Orion Ltd and consolidations, explaining the need for adjustments related to intra-group transactions and their tax effects. The report provides a comprehensive overview of key corporate accounting concepts and their practical application.

Corporate Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

QUESTION 1..................................................................................................................................1

PART1. BOARD COMPOSITION.................................................................................................1

1. Stating the number of independent directors in Woolworths Ltd............................................1

2. Assessing the number of directors as per gender.....................................................................1

3. Presenting the qualifications of 3 directors.............................................................................1

4. Presenting the experience of three directors............................................................................2

5. Other boards of the directors in Woolworths Ltd....................................................................3

PART 2: REPORT...........................................................................................................................4

1. Evaluating the current profitability aspect of Woolworths Holding Ltd.................................4

2. Assessing the extent to which company’s equity is growing as compared to the past years. .6

3. Identifying the opportunities for future growth.......................................................................7

4. Stating challenges pertaining to the current business activities...............................................7

5. Presenting company’s contribution in social and environment sustainability.........................8

QUESTION 2: LEASE....................................................................................................................8

1...................................................................................................................................................8

a. Assessing the kind of lease that Spotless Group Holdings use for their offices......................8

b. Stating the kind of lease undertaken by Spotless Group Holdings for equipments.................9

2. Presenting the reasons behind undertaking each kind of lease................................................9

3. Stating the manner in which leases recorded in the Annual Report of Spotless.....................9

4. Advantages and disadvantages of using different types of lease agreements..........................9

5. Giving reasons behind the introduction of lease standard (AASB 117)................................10

PART 2: CLASSIFICATION OF LEASES..................................................................................11

1. Stating the lease arrangement undertaken by Orion Ltd.......................................................11

INTRODUCTION...........................................................................................................................1

QUESTION 1..................................................................................................................................1

PART1. BOARD COMPOSITION.................................................................................................1

1. Stating the number of independent directors in Woolworths Ltd............................................1

2. Assessing the number of directors as per gender.....................................................................1

3. Presenting the qualifications of 3 directors.............................................................................1

4. Presenting the experience of three directors............................................................................2

5. Other boards of the directors in Woolworths Ltd....................................................................3

PART 2: REPORT...........................................................................................................................4

1. Evaluating the current profitability aspect of Woolworths Holding Ltd.................................4

2. Assessing the extent to which company’s equity is growing as compared to the past years. .6

3. Identifying the opportunities for future growth.......................................................................7

4. Stating challenges pertaining to the current business activities...............................................7

5. Presenting company’s contribution in social and environment sustainability.........................8

QUESTION 2: LEASE....................................................................................................................8

1...................................................................................................................................................8

a. Assessing the kind of lease that Spotless Group Holdings use for their offices......................8

b. Stating the kind of lease undertaken by Spotless Group Holdings for equipments.................9

2. Presenting the reasons behind undertaking each kind of lease................................................9

3. Stating the manner in which leases recorded in the Annual Report of Spotless.....................9

4. Advantages and disadvantages of using different types of lease agreements..........................9

5. Giving reasons behind the introduction of lease standard (AASB 117)................................10

PART 2: CLASSIFICATION OF LEASES..................................................................................11

1. Stating the lease arrangement undertaken by Orion Ltd.......................................................11

2. Critically evaluating the accounting treatment undertaken by Orion Ltd.............................11

QUESTION 3: CONSOLIDATIONS...........................................................................................11

1. Explaining the need for making adjustments related to intra-group transactions in

consolidated financial statements..............................................................................................11

2. Presenting tax effects arising from intra-group transactions.................................................11

3. Explaining the manner through which unrealized profit of intra-group transaction become

realized.......................................................................................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

QUESTION 3: CONSOLIDATIONS...........................................................................................11

1. Explaining the need for making adjustments related to intra-group transactions in

consolidated financial statements..............................................................................................11

2. Presenting tax effects arising from intra-group transactions.................................................11

3. Explaining the manner through which unrealized profit of intra-group transaction become

realized.......................................................................................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Corporate accounting is highly concerned with the rules which are undertaken by the

firms for the preparation of balance sheet, income and cash flow statements. Aspects of corporate

accounting are highly significant which in turn helps in interpreting financial results and

accounting related to the events such as amalgamation, absorption and consolidation. The present

report is based on different case situations which will provide deeper insight about the areas of

accounting. For the present report, Woolworths Holding Ltd has been selected which is one of

the leading retailers operating throughout in Australia and New Zealand. In this, report will

highlight the information pertaining to directors and financial position as well as performance of

the firm. It also depicts different types of leasing used by the firm for the purpose of office and

equipments. Further, it will shed light on AASB 117 and AASB 10 that is highly associated with

the field of accounting.

QUESTION 1

PART1. BOARD COMPOSITION

1. Stating the number of independent directors in Woolworths Ltd

Annual report of Woolworths Ltd related to 2016 clearly shows that during such period

number of independent director was 6.

2. Assessing the number of directors as per gender

In the Woolworth Limited company, total 7 directors are there where proportion of male

and female is 3 and 4 respectively.

3. Presenting the qualifications of 3 directors

Directors Qualifications

Jillian Broadbent, AO BA (Maths & Economics)

Corporate accounting is highly concerned with the rules which are undertaken by the

firms for the preparation of balance sheet, income and cash flow statements. Aspects of corporate

accounting are highly significant which in turn helps in interpreting financial results and

accounting related to the events such as amalgamation, absorption and consolidation. The present

report is based on different case situations which will provide deeper insight about the areas of

accounting. For the present report, Woolworths Holding Ltd has been selected which is one of

the leading retailers operating throughout in Australia and New Zealand. In this, report will

highlight the information pertaining to directors and financial position as well as performance of

the firm. It also depicts different types of leasing used by the firm for the purpose of office and

equipments. Further, it will shed light on AASB 117 and AASB 10 that is highly associated with

the field of accounting.

QUESTION 1

PART1. BOARD COMPOSITION

1. Stating the number of independent directors in Woolworths Ltd

Annual report of Woolworths Ltd related to 2016 clearly shows that during such period

number of independent director was 6.

2. Assessing the number of directors as per gender

In the Woolworth Limited company, total 7 directors are there where proportion of male

and female is 3 and 4 respectively.

3. Presenting the qualifications of 3 directors

Directors Qualifications

Jillian Broadbent, AO BA (Maths & Economics)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Independent non-executive director)

Holly Kramer

(Independent non-executive director)

BA (Hons), MBA

Brad Banducci

(MD and CEO)

MBA, LLB, BComm (Annual report of

Woolworth Holding, 2016)

4. Presenting the experience of three directors

Directors Experiences

Jillian Broadbent, AO

(Independent non-executive director)

Jillian has experience in corporate banking and

finance sector in both Australia and global

level.

Holly Kramer

(Independent non-executive director)

Ms Kramer has experience of more than 20

years in the field of general management,

marketing and sales. She also worked with the

leading companies namely Ford Motors,

Telstra etc.

Brad Banducci

(MD and CEO)

He worked as a CEO of Cellarmasters from the

period of 2007 to 2011. Further, prior to this,

Brad was acted as CEO, director and non-

executive director in Tyro Payments (Annual

report of Woolworth Holding, 2016). In

addition to this, Brad was vice president and

director of Boston Consultancy Group. All

such aspects clearly show that he was the core

member of retail group from 15 years and

Holly Kramer

(Independent non-executive director)

BA (Hons), MBA

Brad Banducci

(MD and CEO)

MBA, LLB, BComm (Annual report of

Woolworth Holding, 2016)

4. Presenting the experience of three directors

Directors Experiences

Jillian Broadbent, AO

(Independent non-executive director)

Jillian has experience in corporate banking and

finance sector in both Australia and global

level.

Holly Kramer

(Independent non-executive director)

Ms Kramer has experience of more than 20

years in the field of general management,

marketing and sales. She also worked with the

leading companies namely Ford Motors,

Telstra etc.

Brad Banducci

(MD and CEO)

He worked as a CEO of Cellarmasters from the

period of 2007 to 2011. Further, prior to this,

Brad was acted as CEO, director and non-

executive director in Tyro Payments (Annual

report of Woolworth Holding, 2016). In

addition to this, Brad was vice president and

director of Boston Consultancy Group. All

such aspects clearly show that he was the core

member of retail group from 15 years and

having great experiences in such sector.

5. Other boards of the directors in Woolworths Ltd

Directors Other boards & kinds

Jillian Broadbent, AO

(Independent non-executive director)

Chancellor of the University of

Wollongong

Member of the Board of the Reserve

Bank of Australia (1998 to 2013)

Director of ASX Limited, Coca-Cola

Amatil Limited

Director of Qantas Airways Limited

Director of Westfield Property Trusts

and Woodside Petroleum Ltd

Holly Kramer

(Independent non-executive director)

Non-executive Director of Nine

Entertainment Corporation (from May

2015)

Non-executive Director of AMP

Limited (since October 2015)

Member of Chief Executive Women

Group Managing Director at Telstra

Chief Executive Officer of Best & Less

(South African retail group Pepkor)

Brad Banducci

(MD and CEO)

Managing Director of Woolworths

Food Group (March 2015 – February

2016)

Director of Liquor (2012 – March

5. Other boards of the directors in Woolworths Ltd

Directors Other boards & kinds

Jillian Broadbent, AO

(Independent non-executive director)

Chancellor of the University of

Wollongong

Member of the Board of the Reserve

Bank of Australia (1998 to 2013)

Director of ASX Limited, Coca-Cola

Amatil Limited

Director of Qantas Airways Limited

Director of Westfield Property Trusts

and Woodside Petroleum Ltd

Holly Kramer

(Independent non-executive director)

Non-executive Director of Nine

Entertainment Corporation (from May

2015)

Non-executive Director of AMP

Limited (since October 2015)

Member of Chief Executive Women

Group Managing Director at Telstra

Chief Executive Officer of Best & Less

(South African retail group Pepkor)

Brad Banducci

(MD and CEO)

Managing Director of Woolworths

Food Group (March 2015 – February

2016)

Director of Liquor (2012 – March

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2015)

Chief Executive Officer of

Cellarmasters (2007 – 2011)

Chief Financial Officer and Director,

and later a Non-Executive Director at

Tyro Payments

Vice President and Director in The

Boston Consulting Group (15 years)

PART 2: REPORT

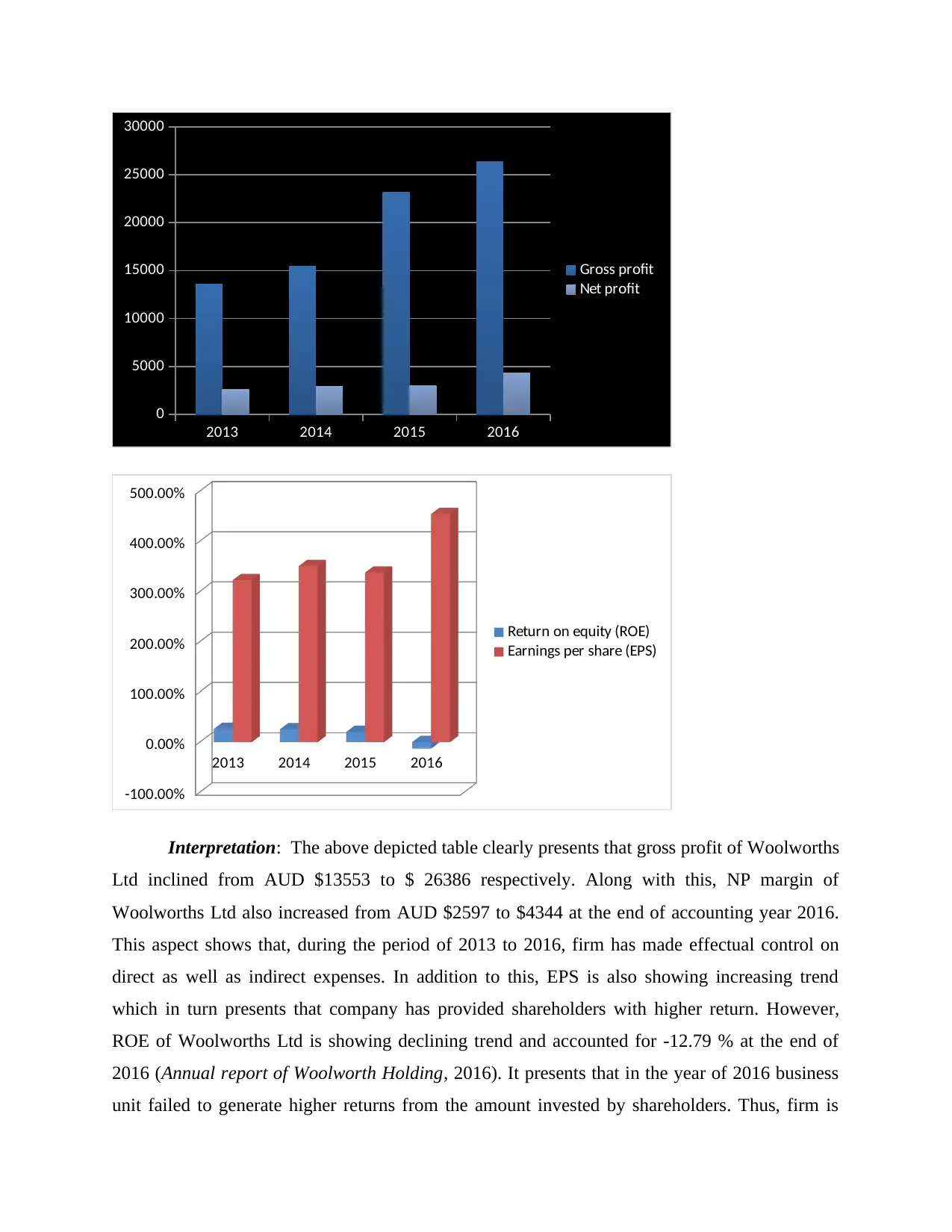

1. Evaluating the current profitability aspect of Woolworths Holding Ltd

Years Gross profit Net profit Return on

equity (ROE)

Earnings per

share (EPS)

2013 13553 2597 26.25% 3.22

2014 15498 2888 25.43% 3.50

2015 23150 3017 20.35% 3.37

2016 26386 4344 -12.79% 4.54

Chief Executive Officer of

Cellarmasters (2007 – 2011)

Chief Financial Officer and Director,

and later a Non-Executive Director at

Tyro Payments

Vice President and Director in The

Boston Consulting Group (15 years)

PART 2: REPORT

1. Evaluating the current profitability aspect of Woolworths Holding Ltd

Years Gross profit Net profit Return on

equity (ROE)

Earnings per

share (EPS)

2013 13553 2597 26.25% 3.22

2014 15498 2888 25.43% 3.50

2015 23150 3017 20.35% 3.37

2016 26386 4344 -12.79% 4.54

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2013 2014 2015 2016

0

5000

10000

15000

20000

25000

30000

Gross profit

Net profit

2013 2014 2015 2016

-100.00%

0.00%

100.00%

200.00%

300.00%

400.00%

500.00%

Return on equity (ROE)

Earnings per share (EPS)

Interpretation: The above depicted table clearly presents that gross profit of Woolworths

Ltd inclined from AUD $13553 to $ 26386 respectively. Along with this, NP margin of

Woolworths Ltd also increased from AUD $2597 to $4344 at the end of accounting year 2016.

This aspect shows that, during the period of 2013 to 2016, firm has made effectual control on

direct as well as indirect expenses. In addition to this, EPS is also showing increasing trend

which in turn presents that company has provided shareholders with higher return. However,

ROE of Woolworths Ltd is showing declining trend and accounted for -12.79 % at the end of

2016 (Annual report of Woolworth Holding, 2016). It presents that in the year of 2016 business

unit failed to generate higher returns from the amount invested by shareholders. Thus, firm is

0

5000

10000

15000

20000

25000

30000

Gross profit

Net profit

2013 2014 2015 2016

-100.00%

0.00%

100.00%

200.00%

300.00%

400.00%

500.00%

Return on equity (ROE)

Earnings per share (EPS)

Interpretation: The above depicted table clearly presents that gross profit of Woolworths

Ltd inclined from AUD $13553 to $ 26386 respectively. Along with this, NP margin of

Woolworths Ltd also increased from AUD $2597 to $4344 at the end of accounting year 2016.

This aspect shows that, during the period of 2013 to 2016, firm has made effectual control on

direct as well as indirect expenses. In addition to this, EPS is also showing increasing trend

which in turn presents that company has provided shareholders with higher return. However,

ROE of Woolworths Ltd is showing declining trend and accounted for -12.79 % at the end of

2016 (Annual report of Woolworth Holding, 2016). It presents that in the year of 2016 business

unit failed to generate higher returns from the amount invested by shareholders. Thus, firm is

required to develop sound strategic framework that helps in enhancing margin and thereby

contributes in the organizational success. On the basis of the outcome of overall evaluation, it

can be stated that profitability aspect of the company is good and increased over the past years.

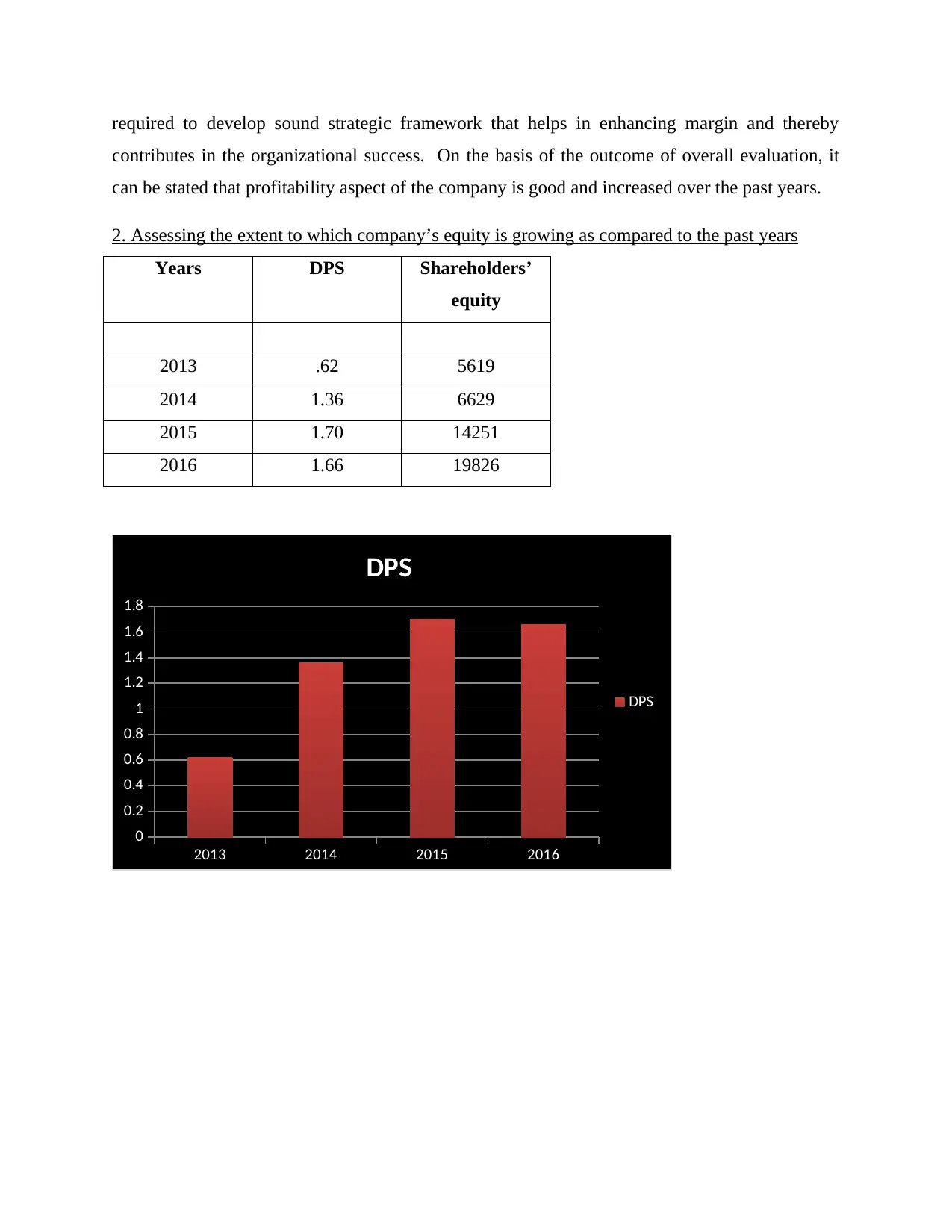

2. Assessing the extent to which company’s equity is growing as compared to the past years

Years DPS Shareholders’

equity

2013 .62 5619

2014 1.36 6629

2015 1.70 14251

2016 1.66 19826

2013 2014 2015 2016

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

DPS

DPS

contributes in the organizational success. On the basis of the outcome of overall evaluation, it

can be stated that profitability aspect of the company is good and increased over the past years.

2. Assessing the extent to which company’s equity is growing as compared to the past years

Years DPS Shareholders’

equity

2013 .62 5619

2014 1.36 6629

2015 1.70 14251

2016 1.66 19826

2013 2014 2015 2016

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

DPS

DPS

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

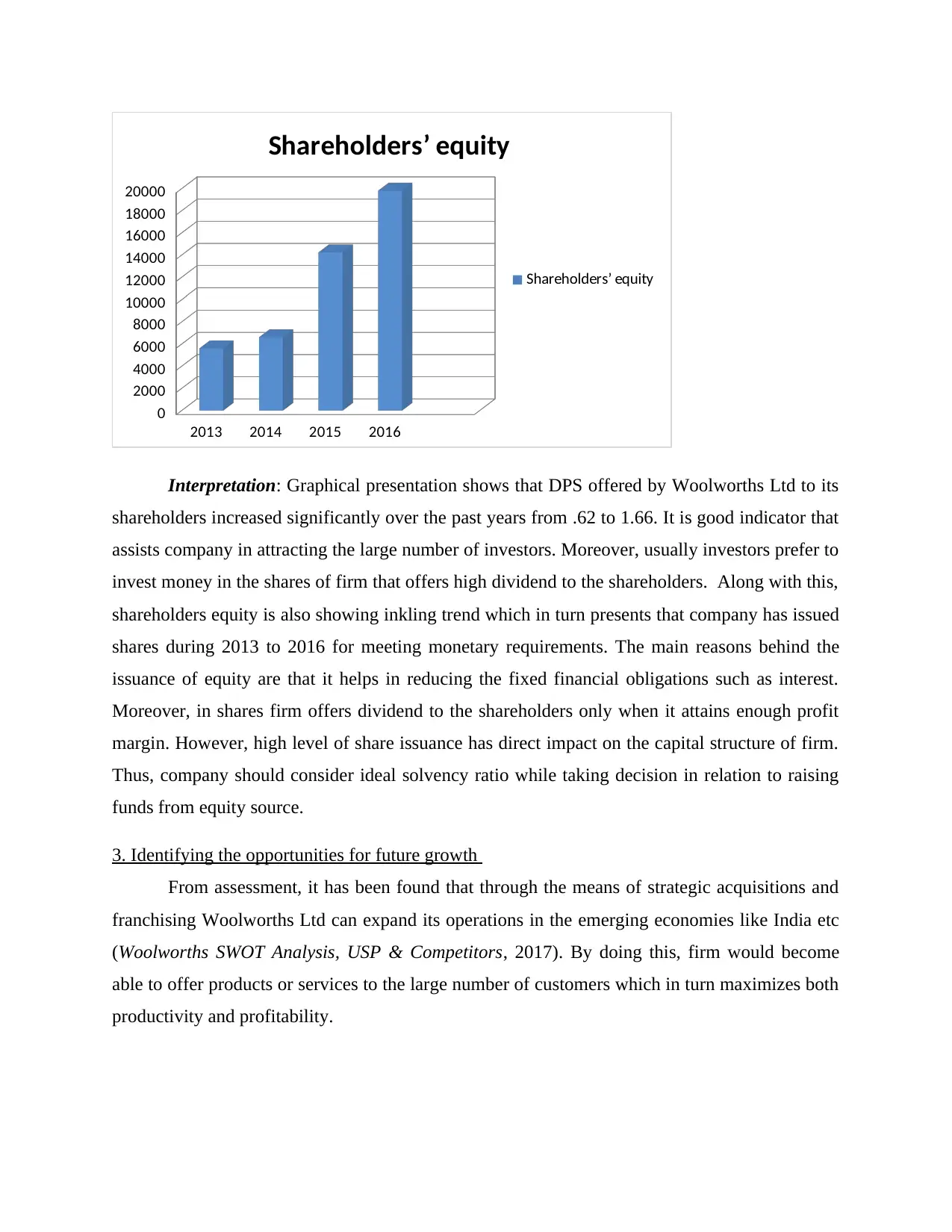

2013 2014 2015 2016

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

Shareholders’ equity

Shareholders’ equity

Interpretation: Graphical presentation shows that DPS offered by Woolworths Ltd to its

shareholders increased significantly over the past years from .62 to 1.66. It is good indicator that

assists company in attracting the large number of investors. Moreover, usually investors prefer to

invest money in the shares of firm that offers high dividend to the shareholders. Along with this,

shareholders equity is also showing inkling trend which in turn presents that company has issued

shares during 2013 to 2016 for meeting monetary requirements. The main reasons behind the

issuance of equity are that it helps in reducing the fixed financial obligations such as interest.

Moreover, in shares firm offers dividend to the shareholders only when it attains enough profit

margin. However, high level of share issuance has direct impact on the capital structure of firm.

Thus, company should consider ideal solvency ratio while taking decision in relation to raising

funds from equity source.

3. Identifying the opportunities for future growth

From assessment, it has been found that through the means of strategic acquisitions and

franchising Woolworths Ltd can expand its operations in the emerging economies like India etc

(Woolworths SWOT Analysis, USP & Competitors, 2017). By doing this, firm would become

able to offer products or services to the large number of customers which in turn maximizes both

productivity and profitability.

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

Shareholders’ equity

Shareholders’ equity

Interpretation: Graphical presentation shows that DPS offered by Woolworths Ltd to its

shareholders increased significantly over the past years from .62 to 1.66. It is good indicator that

assists company in attracting the large number of investors. Moreover, usually investors prefer to

invest money in the shares of firm that offers high dividend to the shareholders. Along with this,

shareholders equity is also showing inkling trend which in turn presents that company has issued

shares during 2013 to 2016 for meeting monetary requirements. The main reasons behind the

issuance of equity are that it helps in reducing the fixed financial obligations such as interest.

Moreover, in shares firm offers dividend to the shareholders only when it attains enough profit

margin. However, high level of share issuance has direct impact on the capital structure of firm.

Thus, company should consider ideal solvency ratio while taking decision in relation to raising

funds from equity source.

3. Identifying the opportunities for future growth

From assessment, it has been found that through the means of strategic acquisitions and

franchising Woolworths Ltd can expand its operations in the emerging economies like India etc

(Woolworths SWOT Analysis, USP & Competitors, 2017). By doing this, firm would become

able to offer products or services to the large number of customers which in turn maximizes both

productivity and profitability.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4. Stating challenges pertaining to the current business activities

Retail sector of Australia is filled up with the high level of competition which in turn

imposes challenge in front of Telstra. Moreover, with the motive to attract more customers’

competitors such as Tesco, Aldi, Walmart, Macro Wholefoods Ltd etc are offering high

discounts which in turn create difficulty for Woolworths Ltd. Moreover, if company will not

make changes in its own pricing policies as per competitors then it may result into loss of

customer base. Along with this, increasing cost of raw material and economic recession also has

significant influence on the current business practices as well as growth of Woolworths ltd.

5. Presenting company’s contribution in social and environment sustainability

Annual report of Woolworth Holding ltd shows that in the year of 2016 it has taken

several initiatives for making contribution in social and environmental sustainability. Corporate

and sustainability report presented by Woolworth clearly exhibits that its solar power generation

accounts for 1560 MWH. In addition to this, company recycled 247930 tones waste material or

diverted the wastage from landfill. Further, by offering employment opportunity to 805000

people company indirectly contributed in Australian economy. Along with this, Woolworth has

introduced or offered its own 1300 branded products with health starrating. It presents company

makes focus on providing customers with healthy and high quality food. Apart from this, direct

community investment of the company implies for AUD $ 31 million, whereas customers

fundraising implies for $19.49 m. In addition to this, total shareholders dividend payout is $1

billion which entails that firm has fulfilled its responsibility towards the society or shareholders

to a great extent (Corporate sustainability report of Woolworth, 2017). All the above depicted

aspects clearly show that contribution made by Woolworth Holding Ltd for the welfare of others

is highly significant and commendable.

Retail sector of Australia is filled up with the high level of competition which in turn

imposes challenge in front of Telstra. Moreover, with the motive to attract more customers’

competitors such as Tesco, Aldi, Walmart, Macro Wholefoods Ltd etc are offering high

discounts which in turn create difficulty for Woolworths Ltd. Moreover, if company will not

make changes in its own pricing policies as per competitors then it may result into loss of

customer base. Along with this, increasing cost of raw material and economic recession also has

significant influence on the current business practices as well as growth of Woolworths ltd.

5. Presenting company’s contribution in social and environment sustainability

Annual report of Woolworth Holding ltd shows that in the year of 2016 it has taken

several initiatives for making contribution in social and environmental sustainability. Corporate

and sustainability report presented by Woolworth clearly exhibits that its solar power generation

accounts for 1560 MWH. In addition to this, company recycled 247930 tones waste material or

diverted the wastage from landfill. Further, by offering employment opportunity to 805000

people company indirectly contributed in Australian economy. Along with this, Woolworth has

introduced or offered its own 1300 branded products with health starrating. It presents company

makes focus on providing customers with healthy and high quality food. Apart from this, direct

community investment of the company implies for AUD $ 31 million, whereas customers

fundraising implies for $19.49 m. In addition to this, total shareholders dividend payout is $1

billion which entails that firm has fulfilled its responsibility towards the society or shareholders

to a great extent (Corporate sustainability report of Woolworth, 2017). All the above depicted

aspects clearly show that contribution made by Woolworth Holding Ltd for the welfare of others

is highly significant and commendable.

QUESTION 2: LEASE

PART 1

1.

a. Assessing the kind of lease that Woolworths Holding Ltd use for their offices

In order to uses offices of the company, the cited firm Woolworths Ltd considers

operating lease. In this method, assets are generally given on rent to the another party and not

transacted in the books of financial position of the firm. Further, ownership of the asset is not to

be transferred to another party because it works for the short period of time (Rohan, 2016.).

b. Stating the kind of lease undertaken by Woolworths Ltd for equipments

The Woolworths Ltd enterprise considers financial lease with respect to the equipments

and machinery within workplace. It works in the firm as a loan where residual value of the risks

is not applicable. Apart from this, transactions of financial lease are mandatory to show in the

balance sheet. In this ownership remains with the company itself and not transfer to another

party.

2. Presenting the reasons behind undertaking each kind of lease

The Woolworths Limited entity considers operating lease because option of renew is

available with it. When talking about the reason of using financial lease then it has chance to buy

the equipment while taking decisions at the market price. Another justification is for using such

leasing kinds is that, ownership of both office and equipment remains with the company itself

rather than transferring to another party (Dou, Hu and Wu, 2017). The financial leasing under

equipments is supportive for the cited firm in order to preserve cash flows in the profitable

direction. Along with this, facilities of tax deductible are also allowed in this case.

3. Stating the manner in which leases recorded in the Annual Report of Woolworths Ltd

In the annual report of Woolworths Ltd, operating lease is recorded as an expenses and

financial lease as the liabilities. Further, straight-line method is taken into account by the

company after considering to the lease term. On the other side, operating lease is not recorded in

the statement of financial position at the end of year of the company (Galina, 2017). Further, as

PART 1

1.

a. Assessing the kind of lease that Woolworths Holding Ltd use for their offices

In order to uses offices of the company, the cited firm Woolworths Ltd considers

operating lease. In this method, assets are generally given on rent to the another party and not

transacted in the books of financial position of the firm. Further, ownership of the asset is not to

be transferred to another party because it works for the short period of time (Rohan, 2016.).

b. Stating the kind of lease undertaken by Woolworths Ltd for equipments

The Woolworths Ltd enterprise considers financial lease with respect to the equipments

and machinery within workplace. It works in the firm as a loan where residual value of the risks

is not applicable. Apart from this, transactions of financial lease are mandatory to show in the

balance sheet. In this ownership remains with the company itself and not transfer to another

party.

2. Presenting the reasons behind undertaking each kind of lease

The Woolworths Limited entity considers operating lease because option of renew is

available with it. When talking about the reason of using financial lease then it has chance to buy

the equipment while taking decisions at the market price. Another justification is for using such

leasing kinds is that, ownership of both office and equipment remains with the company itself

rather than transferring to another party (Dou, Hu and Wu, 2017). The financial leasing under

equipments is supportive for the cited firm in order to preserve cash flows in the profitable

direction. Along with this, facilities of tax deductible are also allowed in this case.

3. Stating the manner in which leases recorded in the Annual Report of Woolworths Ltd

In the annual report of Woolworths Ltd, operating lease is recorded as an expenses and

financial lease as the liabilities. Further, straight-line method is taken into account by the

company after considering to the lease term. On the other side, operating lease is not recorded in

the statement of financial position at the end of year of the company (Galina, 2017). Further, as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.