Corporate Accounting Report: Freedom Food Group Financial Analysis

VerifiedAdded on 2020/05/16

|11

|2020

|77

Report

AI Summary

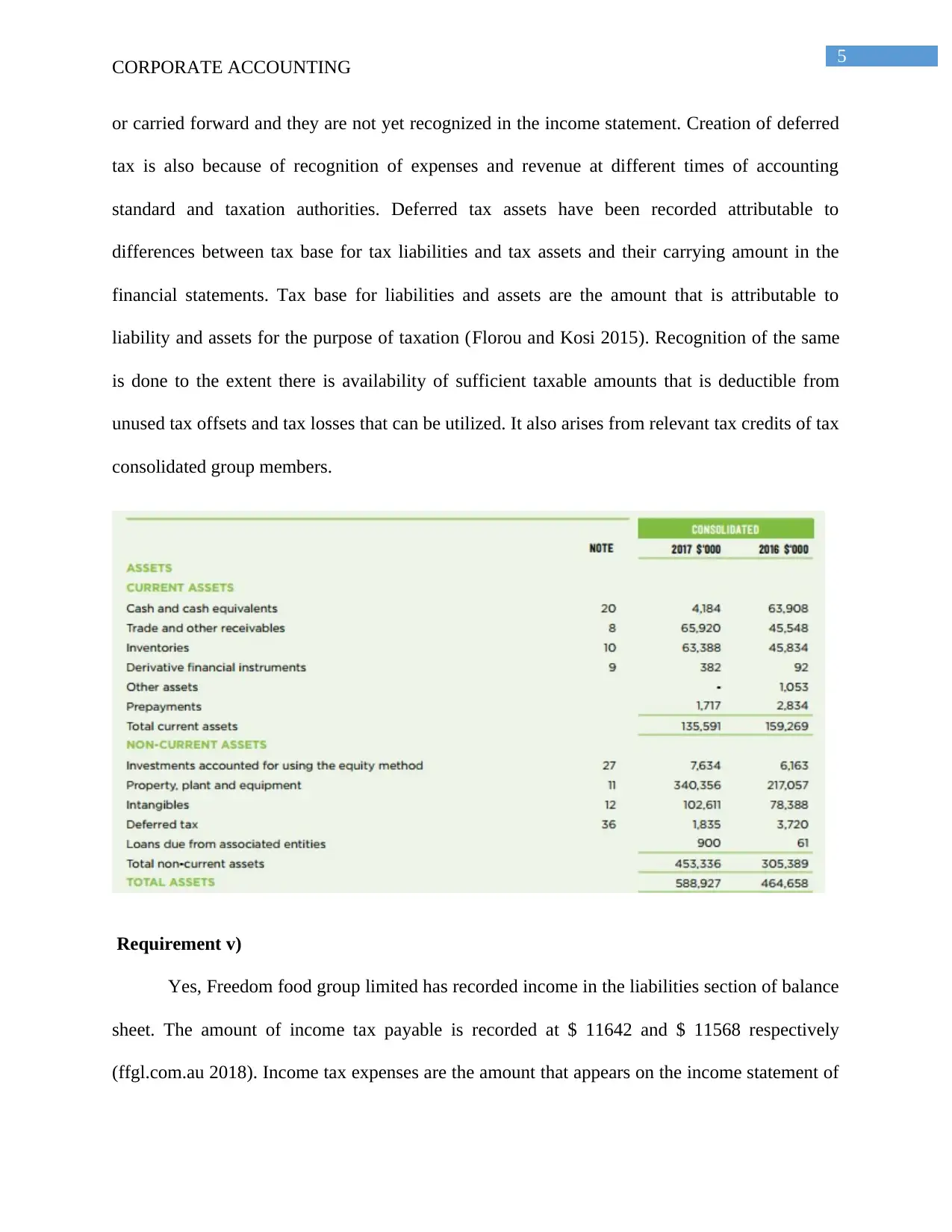

This report provides a detailed analysis of the corporate accounting practices of Freedom Food Group Limited. It examines various aspects of the company's financial statements, including items of equity, income tax expense, effective tax rates, deferred tax, and income tax payable. The analysis covers the years 2017 and 2016, highlighting changes in equity capital, non-controlling interest, reserves, and retained earnings. The report also compares income tax expenses with accounting income times the tax rate, explaining the differences due to varying accounting treatments. Furthermore, it explores the creation and recording of deferred tax assets and liabilities, the presentation of income tax payable in the liabilities section, and the treatment of income tax paid in the cash flow statement. The report concludes with insights into Freedom Food Group's taxation treatment and its effective tax rate, offering a comprehensive understanding of the company's financial performance and accounting practices. The document is contributed by a student to be published on the website Desklib, a platform which provides all the necessary AI based study tools for students.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.