Corporate Accounting Analysis: Financial Performance Report

VerifiedAdded on 2020/10/22

|21

|4390

|420

Report

AI Summary

This report provides a detailed analysis of corporate accounting practices, focusing on two prominent Australian companies: Wesfarmers Ltd and Woolworths Group Ltd. The project begins with an executive summary and table of contents, setting the stage for an in-depth examination of key financial statements. The analysis encompasses owners' equity, comparing items such as common stock, retained earnings, and reserves, and conducting a comparative analysis using the debt-to-equity ratio. The report then delves into cash flow statements, examining interest received, borrowing costs, and income tax received, with comparative insights for both companies. The study also covers other comprehensive income statements, identifying items within comprehensive profit and loss statements and their significance in reporting income statements. Furthermore, the project explores accounting for corporate income tax, including tax expenses, effective tax rates, deferred tax assets and liabilities, and the calculation of cash tax rates, providing reasons for variations between cash tax rates and book rates. The report concludes with an overall evaluation, drawing conclusions from the analysis to aid in effective future decision-making, and includes references and an appendix for further information.

Corporate Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

This project is being summaries by taking specific information about the corporate

accounting. It consists of various rules and regulation that can help accounting in analysing the

overall performance of the both the company. In order to get more reliable results two of the

main companies is taken for this particular analysis such as Wesfarmers ltd and Woolworths

group ltd. Different types of accounting statements, comprehensive incomes report and other

accounting statements are discussed under this report. Understanding of accounting for corporate

income tax is also being covered under this project so that specific knowledge about tax paid by

both the companies can easily be analysed. Overall evaluation is done to reach at specific

outcomes so the effective decisions can be made in near future.

This project is being summaries by taking specific information about the corporate

accounting. It consists of various rules and regulation that can help accounting in analysing the

overall performance of the both the company. In order to get more reliable results two of the

main companies is taken for this particular analysis such as Wesfarmers ltd and Woolworths

group ltd. Different types of accounting statements, comprehensive incomes report and other

accounting statements are discussed under this report. Understanding of accounting for corporate

income tax is also being covered under this project so that specific knowledge about tax paid by

both the companies can easily be analysed. Overall evaluation is done to reach at specific

outcomes so the effective decisions can be made in near future.

TABLE OF CONTENTS

EXECUTIVE SUMMARY.............................................................................................................2

Table of Contents.............................................................................................................................3

INTRODUCTION...........................................................................................................................1

OWNERS’ EQUITY.......................................................................................................................1

(i): Listing item of equity and associated information about the companies.........................1

(ii): Comparative analysis.......................................................................................................2

CASH FLOW STATEMENT..........................................................................................................3

(iii): Listing of cash flow statements......................................................................................3

(iv): Comparative analysis......................................................................................................3

(v): Comparative analysis along with proper insight.............................................................4

OTHER COMPREHENSIVE INCOME STATEMENT................................................................5

(vi): Items in comprehensive profit and loss statements of both company............................5

(vii): Essential for reporting income statements.....................................................................8

(viii): Comparative analysis...................................................................................................9

(ix): Comprehensive income be included in evaluating the performance of manager...........9

ACCOUNTING FOR CORPORATE INCOME TAX....................................................................9

(x): Tax expenses shown in financial statements of both the companies...............................9

(xi): Effective tax rate...........................................................................................................10

(xii): Deferred tax assets / liabilities.....................................................................................11

(xiii): Evaluation on Deferred tax liabilities.........................................................................12

(xiv): Cash tax amount using in book tax amount................................................................12

(xv): Calculation of cash tax rate for both the company......................................................12

(Xvi): Reasons of variation in cash tax rate and book rate...................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

Appendix........................................................................................................................................15

EXECUTIVE SUMMARY.............................................................................................................2

Table of Contents.............................................................................................................................3

INTRODUCTION...........................................................................................................................1

OWNERS’ EQUITY.......................................................................................................................1

(i): Listing item of equity and associated information about the companies.........................1

(ii): Comparative analysis.......................................................................................................2

CASH FLOW STATEMENT..........................................................................................................3

(iii): Listing of cash flow statements......................................................................................3

(iv): Comparative analysis......................................................................................................3

(v): Comparative analysis along with proper insight.............................................................4

OTHER COMPREHENSIVE INCOME STATEMENT................................................................5

(vi): Items in comprehensive profit and loss statements of both company............................5

(vii): Essential for reporting income statements.....................................................................8

(viii): Comparative analysis...................................................................................................9

(ix): Comprehensive income be included in evaluating the performance of manager...........9

ACCOUNTING FOR CORPORATE INCOME TAX....................................................................9

(x): Tax expenses shown in financial statements of both the companies...............................9

(xi): Effective tax rate...........................................................................................................10

(xii): Deferred tax assets / liabilities.....................................................................................11

(xiii): Evaluation on Deferred tax liabilities.........................................................................12

(xiv): Cash tax amount using in book tax amount................................................................12

(xv): Calculation of cash tax rate for both the company......................................................12

(Xvi): Reasons of variation in cash tax rate and book rate...................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

Appendix........................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Corporate accounting is a specialized branch of accounting that deals with the accounting

for companies, formulation of final accounts and cash flow statements. The actions that

managers take to increase the value of their firm to the shareholders and techniques as well as

analysis used to allocate financial resources within an organisation. In accordance to analyse the

significance of this concepts, the two companies are selected which are listed on ASX

(Australian securities Exchange). The first company is chosen is “Wesfarmers Ltd” which is

having one of the largest business operations in chemicals, fertilisers and coal mining. While the

another one is “Woolworths group limited” which is more trusted brands in retailing, serving

millions of customer every day. This project covers various information about owners’ equity,

cash flow statements of the mentioned two companies under this report. Apart from this,

accounting for corporate income tax is also being illustrated effectively in this project

(Etxeberria and Ortas, 2017).

OWNERS’ EQUITY

(i): Listing item of equity and associated information about the companies

Equity items: These are said to be owner capital worth that is being derived among total

assets and liabilities they are carrying with them. The data is taken from both Woolworths group

limited and Wesfarmers ltd. There are various types of equity accounts that combine to make up

total shareholders’ equity. It consists of common stock, preferred stock, contribution surplus,

additional paid up capital and retained earnings. These are mentioned as per the financial

statement prepared by the company. some of them are discussed underneath:

Common stock: It is said to be the security that represent ownerships within an

organisation. Common stock is considered as securities, shares, bonds and debentures

retain by organisation of other companies. The main reason of fluctuation in the value of

stocks occurs due to fluctuations in dividends or interest income received by

organisation. For example, Wesfarmers and Woolworths group retain the common stocks

and the fluctuation will be based upon change in dividends and interest income. Holders

of common stock exercise control by electing a board of directors and making vote on

corporate policy. (Zadek, Evans and Pruzan, 2013).

Retain earnings: These are said to be net revenue after dividends that are present with

the company to reinvestment in the company’s core business or to pay their all-time

1

Corporate accounting is a specialized branch of accounting that deals with the accounting

for companies, formulation of final accounts and cash flow statements. The actions that

managers take to increase the value of their firm to the shareholders and techniques as well as

analysis used to allocate financial resources within an organisation. In accordance to analyse the

significance of this concepts, the two companies are selected which are listed on ASX

(Australian securities Exchange). The first company is chosen is “Wesfarmers Ltd” which is

having one of the largest business operations in chemicals, fertilisers and coal mining. While the

another one is “Woolworths group limited” which is more trusted brands in retailing, serving

millions of customer every day. This project covers various information about owners’ equity,

cash flow statements of the mentioned two companies under this report. Apart from this,

accounting for corporate income tax is also being illustrated effectively in this project

(Etxeberria and Ortas, 2017).

OWNERS’ EQUITY

(i): Listing item of equity and associated information about the companies

Equity items: These are said to be owner capital worth that is being derived among total

assets and liabilities they are carrying with them. The data is taken from both Woolworths group

limited and Wesfarmers ltd. There are various types of equity accounts that combine to make up

total shareholders’ equity. It consists of common stock, preferred stock, contribution surplus,

additional paid up capital and retained earnings. These are mentioned as per the financial

statement prepared by the company. some of them are discussed underneath:

Common stock: It is said to be the security that represent ownerships within an

organisation. Common stock is considered as securities, shares, bonds and debentures

retain by organisation of other companies. The main reason of fluctuation in the value of

stocks occurs due to fluctuations in dividends or interest income received by

organisation. For example, Wesfarmers and Woolworths group retain the common stocks

and the fluctuation will be based upon change in dividends and interest income. Holders

of common stock exercise control by electing a board of directors and making vote on

corporate policy. (Zadek, Evans and Pruzan, 2013).

Retain earnings: These are said to be net revenue after dividends that are present with

the company to reinvestment in the company’s core business or to pay their all-time

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

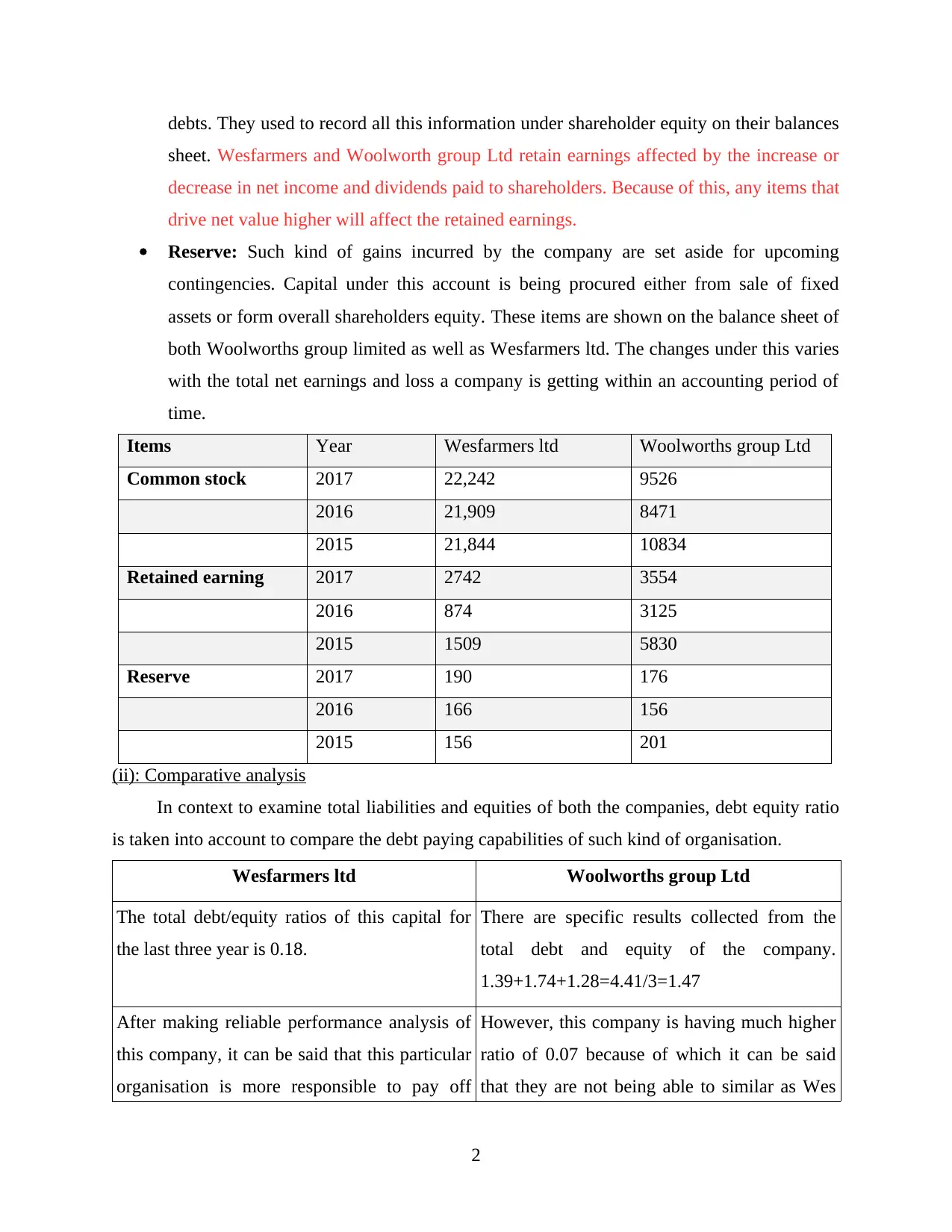

debts. They used to record all this information under shareholder equity on their balances

sheet. Wesfarmers and Woolworth group Ltd retain earnings affected by the increase or

decrease in net income and dividends paid to shareholders. Because of this, any items that

drive net value higher will affect the retained earnings.

Reserve: Such kind of gains incurred by the company are set aside for upcoming

contingencies. Capital under this account is being procured either from sale of fixed

assets or form overall shareholders equity. These items are shown on the balance sheet of

both Woolworths group limited as well as Wesfarmers ltd. The changes under this varies

with the total net earnings and loss a company is getting within an accounting period of

time.

Items Year Wesfarmers ltd Woolworths group Ltd

Common stock 2017 22,242 9526

2016 21,909 8471

2015 21,844 10834

Retained earning 2017 2742 3554

2016 874 3125

2015 1509 5830

Reserve 2017 190 176

2016 166 156

2015 156 201

(ii): Comparative analysis

In context to examine total liabilities and equities of both the companies, debt equity ratio

is taken into account to compare the debt paying capabilities of such kind of organisation.

Wesfarmers ltd Woolworths group Ltd

The total debt/equity ratios of this capital for

the last three year is 0.18.

There are specific results collected from the

total debt and equity of the company.

1.39+1.74+1.28=4.41/3=1.47

After making reliable performance analysis of

this company, it can be said that this particular

organisation is more responsible to pay off

However, this company is having much higher

ratio of 0.07 because of which it can be said

that they are not being able to similar as Wes

2

sheet. Wesfarmers and Woolworth group Ltd retain earnings affected by the increase or

decrease in net income and dividends paid to shareholders. Because of this, any items that

drive net value higher will affect the retained earnings.

Reserve: Such kind of gains incurred by the company are set aside for upcoming

contingencies. Capital under this account is being procured either from sale of fixed

assets or form overall shareholders equity. These items are shown on the balance sheet of

both Woolworths group limited as well as Wesfarmers ltd. The changes under this varies

with the total net earnings and loss a company is getting within an accounting period of

time.

Items Year Wesfarmers ltd Woolworths group Ltd

Common stock 2017 22,242 9526

2016 21,909 8471

2015 21,844 10834

Retained earning 2017 2742 3554

2016 874 3125

2015 1509 5830

Reserve 2017 190 176

2016 166 156

2015 156 201

(ii): Comparative analysis

In context to examine total liabilities and equities of both the companies, debt equity ratio

is taken into account to compare the debt paying capabilities of such kind of organisation.

Wesfarmers ltd Woolworths group Ltd

The total debt/equity ratios of this capital for

the last three year is 0.18.

There are specific results collected from the

total debt and equity of the company.

1.39+1.74+1.28=4.41/3=1.47

After making reliable performance analysis of

this company, it can be said that this particular

organisation is more responsible to pay off

However, this company is having much higher

ratio of 0.07 because of which it can be said

that they are not being able to similar as Wes

2

their liabilities in coming future time. farmer in accordance with debt payment

system.

CASH FLOW STATEMENT

(iii): Listing of cash flow statements

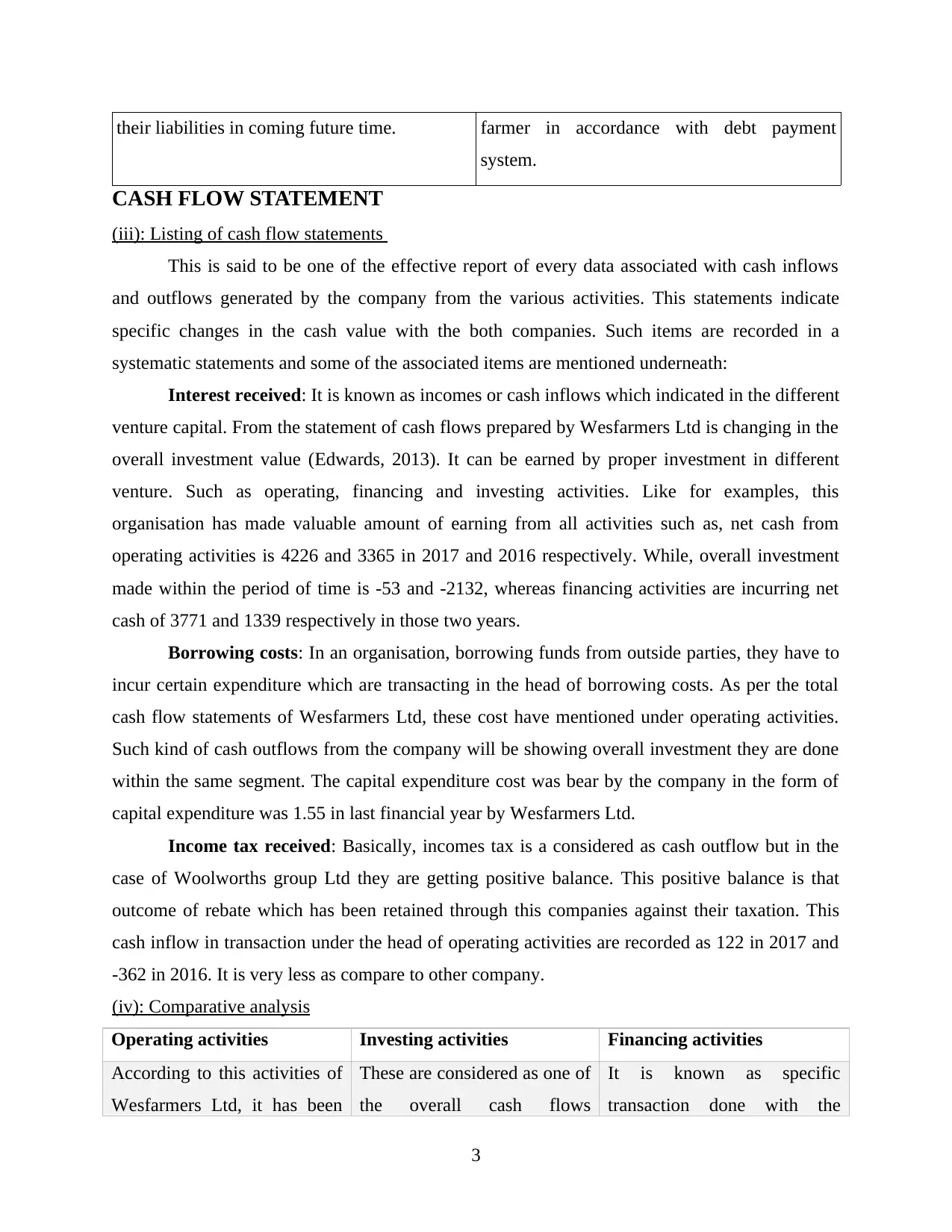

This is said to be one of the effective report of every data associated with cash inflows

and outflows generated by the company from the various activities. This statements indicate

specific changes in the cash value with the both companies. Such items are recorded in a

systematic statements and some of the associated items are mentioned underneath:

Interest received: It is known as incomes or cash inflows which indicated in the different

venture capital. From the statement of cash flows prepared by Wesfarmers Ltd is changing in the

overall investment value (Edwards, 2013). It can be earned by proper investment in different

venture. Such as operating, financing and investing activities. Like for examples, this

organisation has made valuable amount of earning from all activities such as, net cash from

operating activities is 4226 and 3365 in 2017 and 2016 respectively. While, overall investment

made within the period of time is -53 and -2132, whereas financing activities are incurring net

cash of 3771 and 1339 respectively in those two years.

Borrowing costs: In an organisation, borrowing funds from outside parties, they have to

incur certain expenditure which are transacting in the head of borrowing costs. As per the total

cash flow statements of Wesfarmers Ltd, these cost have mentioned under operating activities.

Such kind of cash outflows from the company will be showing overall investment they are done

within the same segment. The capital expenditure cost was bear by the company in the form of

capital expenditure was 1.55 in last financial year by Wesfarmers Ltd.

Income tax received: Basically, incomes tax is a considered as cash outflow but in the

case of Woolworths group Ltd they are getting positive balance. This positive balance is that

outcome of rebate which has been retained through this companies against their taxation. This

cash inflow in transaction under the head of operating activities are recorded as 122 in 2017 and

-362 in 2016. It is very less as compare to other company.

(iv): Comparative analysis

Operating activities Investing activities Financing activities

According to this activities of

Wesfarmers Ltd, it has been

These are considered as one of

the overall cash flows

It is known as specific

transaction done with the

3

system.

CASH FLOW STATEMENT

(iii): Listing of cash flow statements

This is said to be one of the effective report of every data associated with cash inflows

and outflows generated by the company from the various activities. This statements indicate

specific changes in the cash value with the both companies. Such items are recorded in a

systematic statements and some of the associated items are mentioned underneath:

Interest received: It is known as incomes or cash inflows which indicated in the different

venture capital. From the statement of cash flows prepared by Wesfarmers Ltd is changing in the

overall investment value (Edwards, 2013). It can be earned by proper investment in different

venture. Such as operating, financing and investing activities. Like for examples, this

organisation has made valuable amount of earning from all activities such as, net cash from

operating activities is 4226 and 3365 in 2017 and 2016 respectively. While, overall investment

made within the period of time is -53 and -2132, whereas financing activities are incurring net

cash of 3771 and 1339 respectively in those two years.

Borrowing costs: In an organisation, borrowing funds from outside parties, they have to

incur certain expenditure which are transacting in the head of borrowing costs. As per the total

cash flow statements of Wesfarmers Ltd, these cost have mentioned under operating activities.

Such kind of cash outflows from the company will be showing overall investment they are done

within the same segment. The capital expenditure cost was bear by the company in the form of

capital expenditure was 1.55 in last financial year by Wesfarmers Ltd.

Income tax received: Basically, incomes tax is a considered as cash outflow but in the

case of Woolworths group Ltd they are getting positive balance. This positive balance is that

outcome of rebate which has been retained through this companies against their taxation. This

cash inflow in transaction under the head of operating activities are recorded as 122 in 2017 and

-362 in 2016. It is very less as compare to other company.

(iv): Comparative analysis

Operating activities Investing activities Financing activities

According to this activities of

Wesfarmers Ltd, it has been

These are considered as one of

the overall cash flows

It is known as specific

transaction done with the

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

found that net cash inflows

from operating actives is 4226

and 3365 in 2016-17.

Whereas, Woolworths group

Ltd 3126 and 2361

respectively.

investments made on payment

of fixed assets and net

proceeds from sale of

businesses. In Wesfarmers

Ltd, they are getting net cash

of 53 and 2132. While, in case

of Woolworths group Ltd,

they are getting 1435 and

1270 respectively.

creditors and shareholders to

funds either company’s overall

operations or expansions.

These are transactions are

third set of cash activities

displayed on the overall

statements of cash flows. Cash

flow from operation was

recorded as $4266 billion and

102.1 percent (excluding non-

trading items) by Wesfarmers

and the net cash flow for the

year 2017 was $234 million.

From the above comparison made on the basis of various activities of both companies has

been analyse their performance by taken into account the net income and losses incurred by the

during the period of time.

(v): Comparative analysis along with proper insight

Woolworths group Ltd Wesfarmers Ltd

On the basis of income statement prepared

from all three activities are showing maximum

amount as compare to Wesfarmers. Free cash

flow for the 2015, 2016 and 2017 was found

respectively $2265 million, $2545 million and

$1466 million.

In this particular company, it has been analysed

that they are having low income and loss but

there is consistency in their entire value.

Because of this consistency the company is

more capable and high in turnover. The free

cash flow for the year 2015, 2016 and 2017

was found respectively $1212 million, $375

million and $1172 million.

OTHER COMPREHENSIVE INCOME STATEMENT

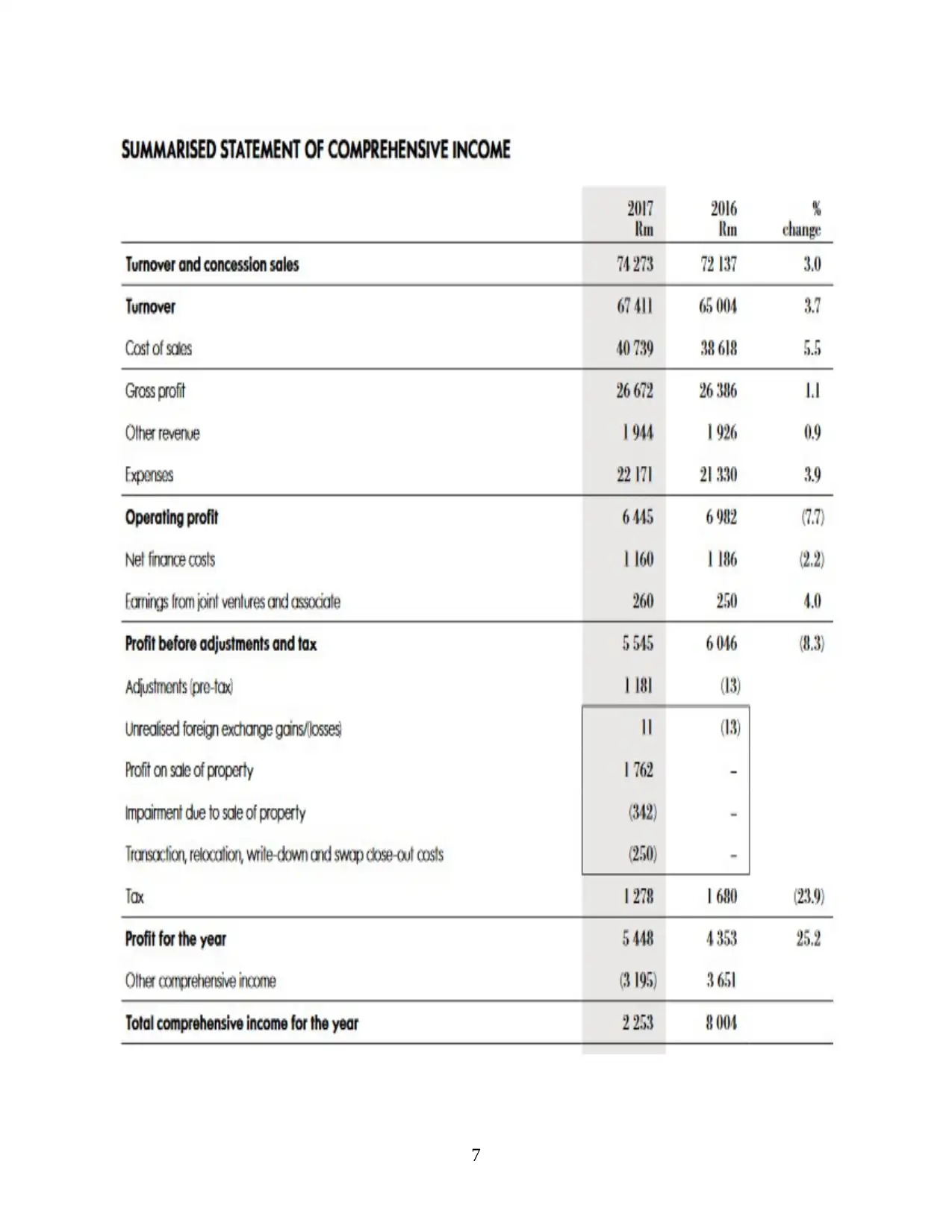

(vi): Items in comprehensive profit and loss statements of both company

Comprehensive income is said to be the sum total of net profit and other items that must be

go through the incomes statement. Because they have not been realized including products

4

from operating actives is 4226

and 3365 in 2016-17.

Whereas, Woolworths group

Ltd 3126 and 2361

respectively.

investments made on payment

of fixed assets and net

proceeds from sale of

businesses. In Wesfarmers

Ltd, they are getting net cash

of 53 and 2132. While, in case

of Woolworths group Ltd,

they are getting 1435 and

1270 respectively.

creditors and shareholders to

funds either company’s overall

operations or expansions.

These are transactions are

third set of cash activities

displayed on the overall

statements of cash flows. Cash

flow from operation was

recorded as $4266 billion and

102.1 percent (excluding non-

trading items) by Wesfarmers

and the net cash flow for the

year 2017 was $234 million.

From the above comparison made on the basis of various activities of both companies has

been analyse their performance by taken into account the net income and losses incurred by the

during the period of time.

(v): Comparative analysis along with proper insight

Woolworths group Ltd Wesfarmers Ltd

On the basis of income statement prepared

from all three activities are showing maximum

amount as compare to Wesfarmers. Free cash

flow for the 2015, 2016 and 2017 was found

respectively $2265 million, $2545 million and

$1466 million.

In this particular company, it has been analysed

that they are having low income and loss but

there is consistency in their entire value.

Because of this consistency the company is

more capable and high in turnover. The free

cash flow for the year 2015, 2016 and 2017

was found respectively $1212 million, $375

million and $1172 million.

OTHER COMPREHENSIVE INCOME STATEMENT

(vi): Items in comprehensive profit and loss statements of both company

Comprehensive income is said to be the sum total of net profit and other items that must be

go through the incomes statement. Because they have not been realized including products

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

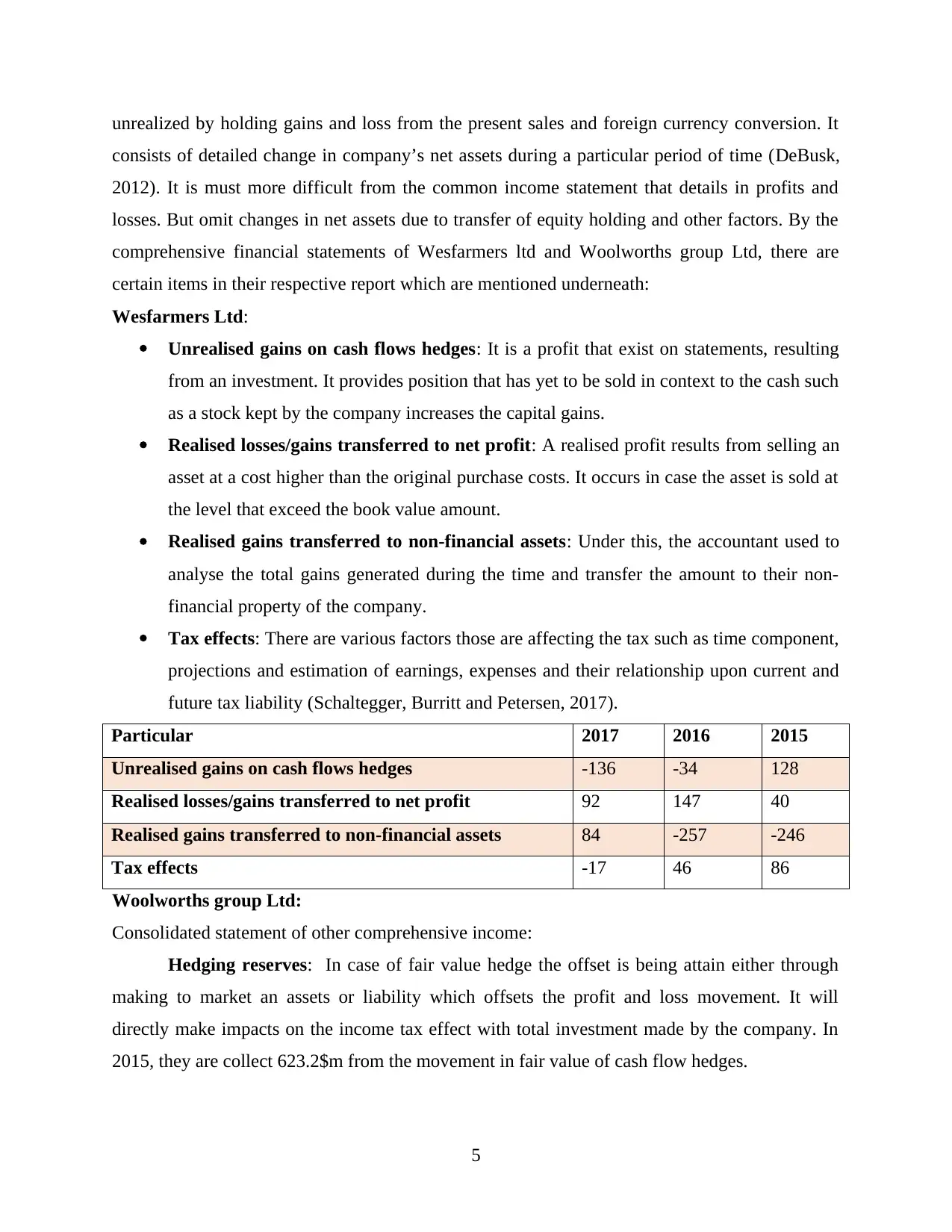

unrealized by holding gains and loss from the present sales and foreign currency conversion. It

consists of detailed change in company’s net assets during a particular period of time (DeBusk,

2012). It is must more difficult from the common income statement that details in profits and

losses. But omit changes in net assets due to transfer of equity holding and other factors. By the

comprehensive financial statements of Wesfarmers ltd and Woolworths group Ltd, there are

certain items in their respective report which are mentioned underneath:

Wesfarmers Ltd:

Unrealised gains on cash flows hedges: It is a profit that exist on statements, resulting

from an investment. It provides position that has yet to be sold in context to the cash such

as a stock kept by the company increases the capital gains.

Realised losses/gains transferred to net profit: A realised profit results from selling an

asset at a cost higher than the original purchase costs. It occurs in case the asset is sold at

the level that exceed the book value amount.

Realised gains transferred to non-financial assets: Under this, the accountant used to

analyse the total gains generated during the time and transfer the amount to their non-

financial property of the company.

Tax effects: There are various factors those are affecting the tax such as time component,

projections and estimation of earnings, expenses and their relationship upon current and

future tax liability (Schaltegger, Burritt and Petersen, 2017).

Particular 2017 2016 2015

Unrealised gains on cash flows hedges -136 -34 128

Realised losses/gains transferred to net profit 92 147 40

Realised gains transferred to non-financial assets 84 -257 -246

Tax effects -17 46 86

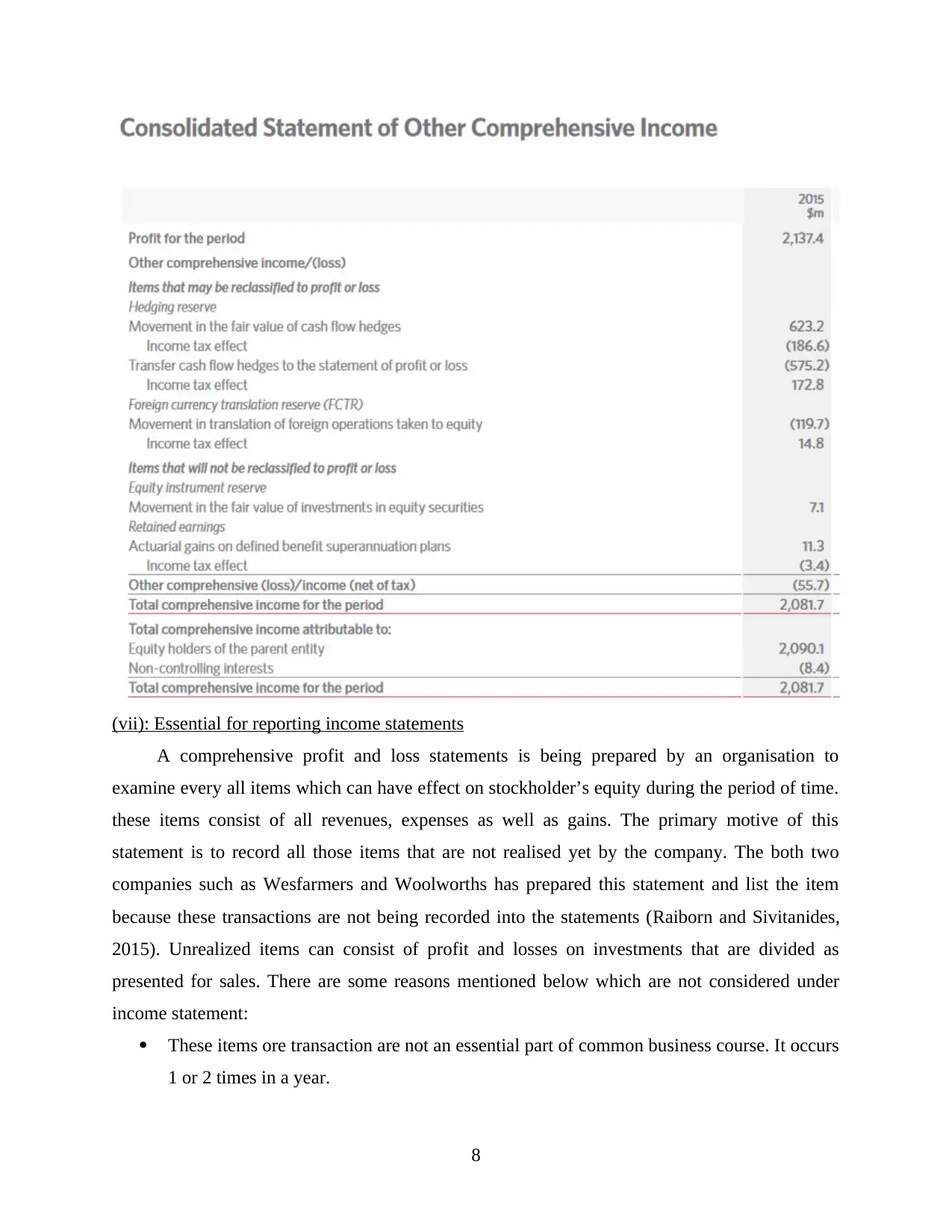

Woolworths group Ltd:

Consolidated statement of other comprehensive income:

Hedging reserves: In case of fair value hedge the offset is being attain either through

making to market an assets or liability which offsets the profit and loss movement. It will

directly make impacts on the income tax effect with total investment made by the company. In

2015, they are collect 623.2$m from the movement in fair value of cash flow hedges.

5

consists of detailed change in company’s net assets during a particular period of time (DeBusk,

2012). It is must more difficult from the common income statement that details in profits and

losses. But omit changes in net assets due to transfer of equity holding and other factors. By the

comprehensive financial statements of Wesfarmers ltd and Woolworths group Ltd, there are

certain items in their respective report which are mentioned underneath:

Wesfarmers Ltd:

Unrealised gains on cash flows hedges: It is a profit that exist on statements, resulting

from an investment. It provides position that has yet to be sold in context to the cash such

as a stock kept by the company increases the capital gains.

Realised losses/gains transferred to net profit: A realised profit results from selling an

asset at a cost higher than the original purchase costs. It occurs in case the asset is sold at

the level that exceed the book value amount.

Realised gains transferred to non-financial assets: Under this, the accountant used to

analyse the total gains generated during the time and transfer the amount to their non-

financial property of the company.

Tax effects: There are various factors those are affecting the tax such as time component,

projections and estimation of earnings, expenses and their relationship upon current and

future tax liability (Schaltegger, Burritt and Petersen, 2017).

Particular 2017 2016 2015

Unrealised gains on cash flows hedges -136 -34 128

Realised losses/gains transferred to net profit 92 147 40

Realised gains transferred to non-financial assets 84 -257 -246

Tax effects -17 46 86

Woolworths group Ltd:

Consolidated statement of other comprehensive income:

Hedging reserves: In case of fair value hedge the offset is being attain either through

making to market an assets or liability which offsets the profit and loss movement. It will

directly make impacts on the income tax effect with total investment made by the company. In

2015, they are collect 623.2$m from the movement in fair value of cash flow hedges.

5

Foreign currency translation reserve(FCTR): It used during the time of preparing the

financial statements of forging operations which is transferred to the FCTR which forms

associated part of other comprehensive statements. With 119.7$m is found as movement in

translation of forging operations that is taken into equity (Watson, 2015).

Income tax effect: It is acceptable to either all report element of other comprehensive net

income related tax, or before related tax effects with an individual aggregate income tax expense.

The overall income tax paid by the company during 2015 is 14.8$m.

Earning from joint venture: Profit from Woolworths financial services increase from

4.4% from last year. The performance impacted through rate adjustments and wide impairment

charged in a challenging collection environment can provide great chance of growth opportunity

for the Woolworths.

6

financial statements of forging operations which is transferred to the FCTR which forms

associated part of other comprehensive statements. With 119.7$m is found as movement in

translation of forging operations that is taken into equity (Watson, 2015).

Income tax effect: It is acceptable to either all report element of other comprehensive net

income related tax, or before related tax effects with an individual aggregate income tax expense.

The overall income tax paid by the company during 2015 is 14.8$m.

Earning from joint venture: Profit from Woolworths financial services increase from

4.4% from last year. The performance impacted through rate adjustments and wide impairment

charged in a challenging collection environment can provide great chance of growth opportunity

for the Woolworths.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(vii): Essential for reporting income statements

A comprehensive profit and loss statements is being prepared by an organisation to

examine every all items which can have effect on stockholder’s equity during the period of time.

these items consist of all revenues, expenses as well as gains. The primary motive of this

statement is to record all those items that are not realised yet by the company. The both two

companies such as Wesfarmers and Woolworths has prepared this statement and list the item

because these transactions are not being recorded into the statements (Raiborn and Sivitanides,

2015). Unrealized items can consist of profit and losses on investments that are divided as

presented for sales. There are some reasons mentioned below which are not considered under

income statement:

These items ore transaction are not an essential part of common business course. It occurs

1 or 2 times in a year.

8

A comprehensive profit and loss statements is being prepared by an organisation to

examine every all items which can have effect on stockholder’s equity during the period of time.

these items consist of all revenues, expenses as well as gains. The primary motive of this

statement is to record all those items that are not realised yet by the company. The both two

companies such as Wesfarmers and Woolworths has prepared this statement and list the item

because these transactions are not being recorded into the statements (Raiborn and Sivitanides,

2015). Unrealized items can consist of profit and losses on investments that are divided as

presented for sales. There are some reasons mentioned below which are not considered under

income statement:

These items ore transaction are not an essential part of common business course. It occurs

1 or 2 times in a year.

8

These gains and losses are gained by an organisation but not yet being realised through

proper business management.

(viii): Comparative analysis

Wesfarmers Ltd Woolworths group ltd

In case of comprehensive income items such as

overall sales of stock and income tax effect

appear in usual income statements then profit

for the year. It will increase eventually which

can further reflect non-accurate as well as

undependable fiscal position of the company.

Profit generated from comprehensive income

continues and discontinued operation are not

being recorded in profit and loss account. But,

if these items were concluded in this account

then value of net income would increase

because of their investment made by the

investors and shareholders.

(ix): Comprehensive income be included in evaluating the performance of manager

It is said to be sum total of net income and other items that must bypass the overall income

statement because they have not been realised. It consists of all items that are unrealised holding

profit or losses from available for sale securities and international currency translation gains.

Managers are associated with internal operations of an organisation that develop this statement

which cannot concern performance of a manager. In accordance to measure and analyse manager

performance different appraisal methods are taken into account but comprehensive profit and

loss statements cannot assist in this particular process (Hoskin, Fizzell and Cherry, 2014).

ACCOUNTING FOR CORPORATE INCOME TAX

(x): Tax expenses shown in financial statements of both the companies

Wesfarmers Ltd:

Tax expenditure is said to be the compulsory cost that are charged by government in

context to the income earned by an organisation during an accounting period. As per the balance

sheet of Wesfarmers ltd, it has been analysed that the company is paying annual tax of

$1.9billion and royalties in 2017. Because of unrecognised temporary difference and tax losses.

There is no balance of income tax on their company and their break down are mentioned

underneath:

9

proper business management.

(viii): Comparative analysis

Wesfarmers Ltd Woolworths group ltd

In case of comprehensive income items such as

overall sales of stock and income tax effect

appear in usual income statements then profit

for the year. It will increase eventually which

can further reflect non-accurate as well as

undependable fiscal position of the company.

Profit generated from comprehensive income

continues and discontinued operation are not

being recorded in profit and loss account. But,

if these items were concluded in this account

then value of net income would increase

because of their investment made by the

investors and shareholders.

(ix): Comprehensive income be included in evaluating the performance of manager

It is said to be sum total of net income and other items that must bypass the overall income

statement because they have not been realised. It consists of all items that are unrealised holding

profit or losses from available for sale securities and international currency translation gains.

Managers are associated with internal operations of an organisation that develop this statement

which cannot concern performance of a manager. In accordance to measure and analyse manager

performance different appraisal methods are taken into account but comprehensive profit and

loss statements cannot assist in this particular process (Hoskin, Fizzell and Cherry, 2014).

ACCOUNTING FOR CORPORATE INCOME TAX

(x): Tax expenses shown in financial statements of both the companies

Wesfarmers Ltd:

Tax expenditure is said to be the compulsory cost that are charged by government in

context to the income earned by an organisation during an accounting period. As per the balance

sheet of Wesfarmers ltd, it has been analysed that the company is paying annual tax of

$1.9billion and royalties in 2017. Because of unrecognised temporary difference and tax losses.

There is no balance of income tax on their company and their break down are mentioned

underneath:

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.