Analysis of Consolidated Financial Statements for Griffin Ltd

VerifiedAdded on 2021/02/20

|10

|2353

|54

Report

AI Summary

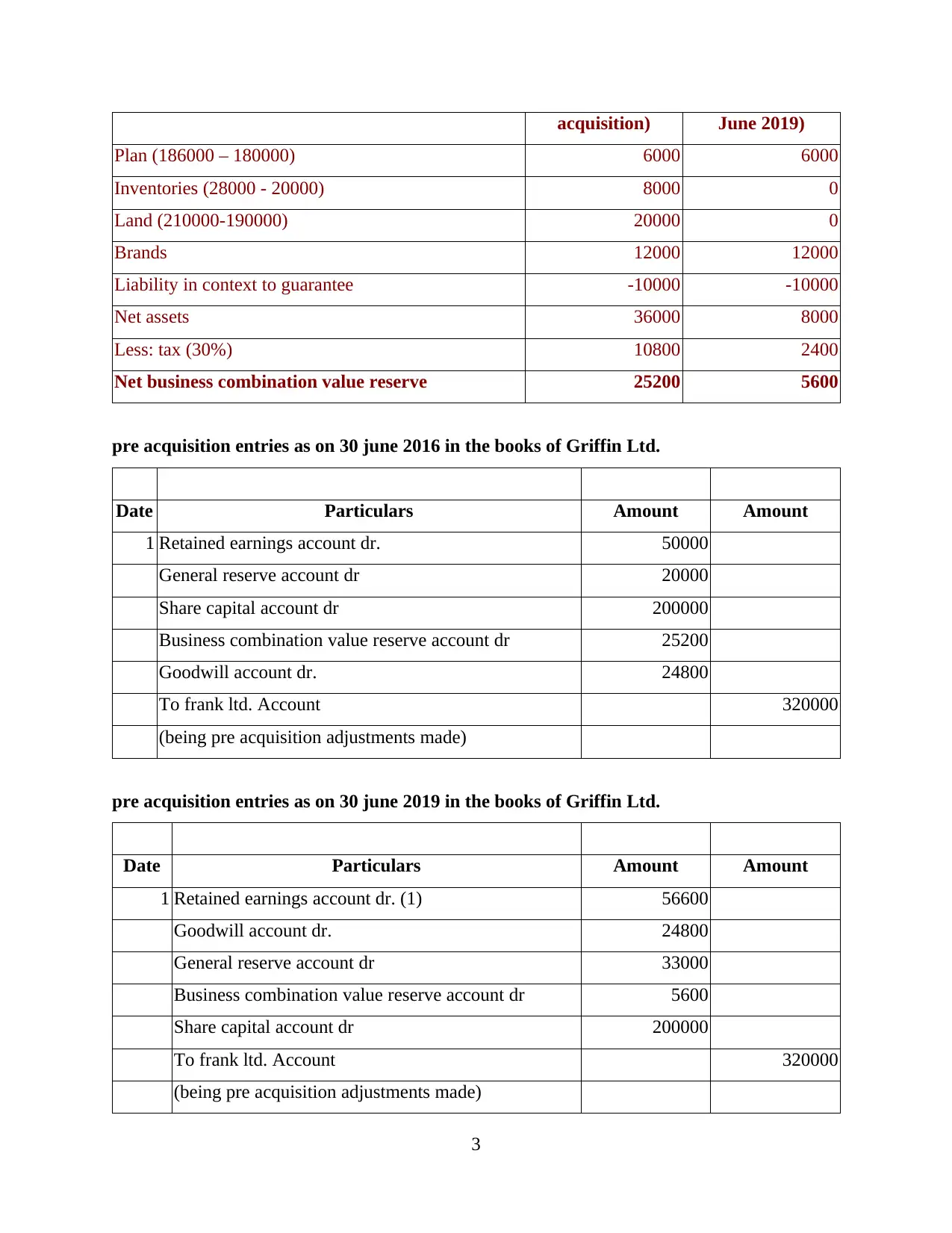

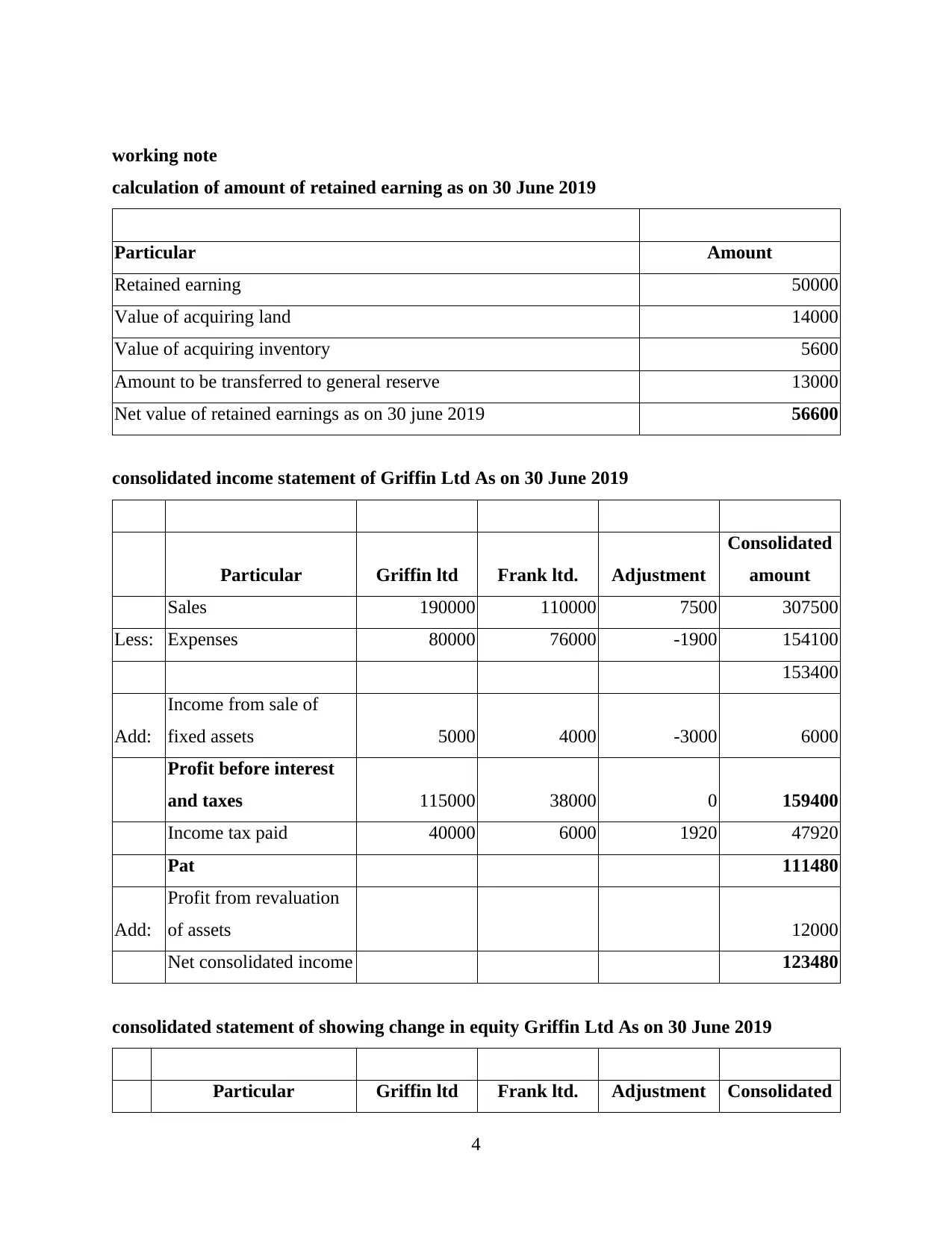

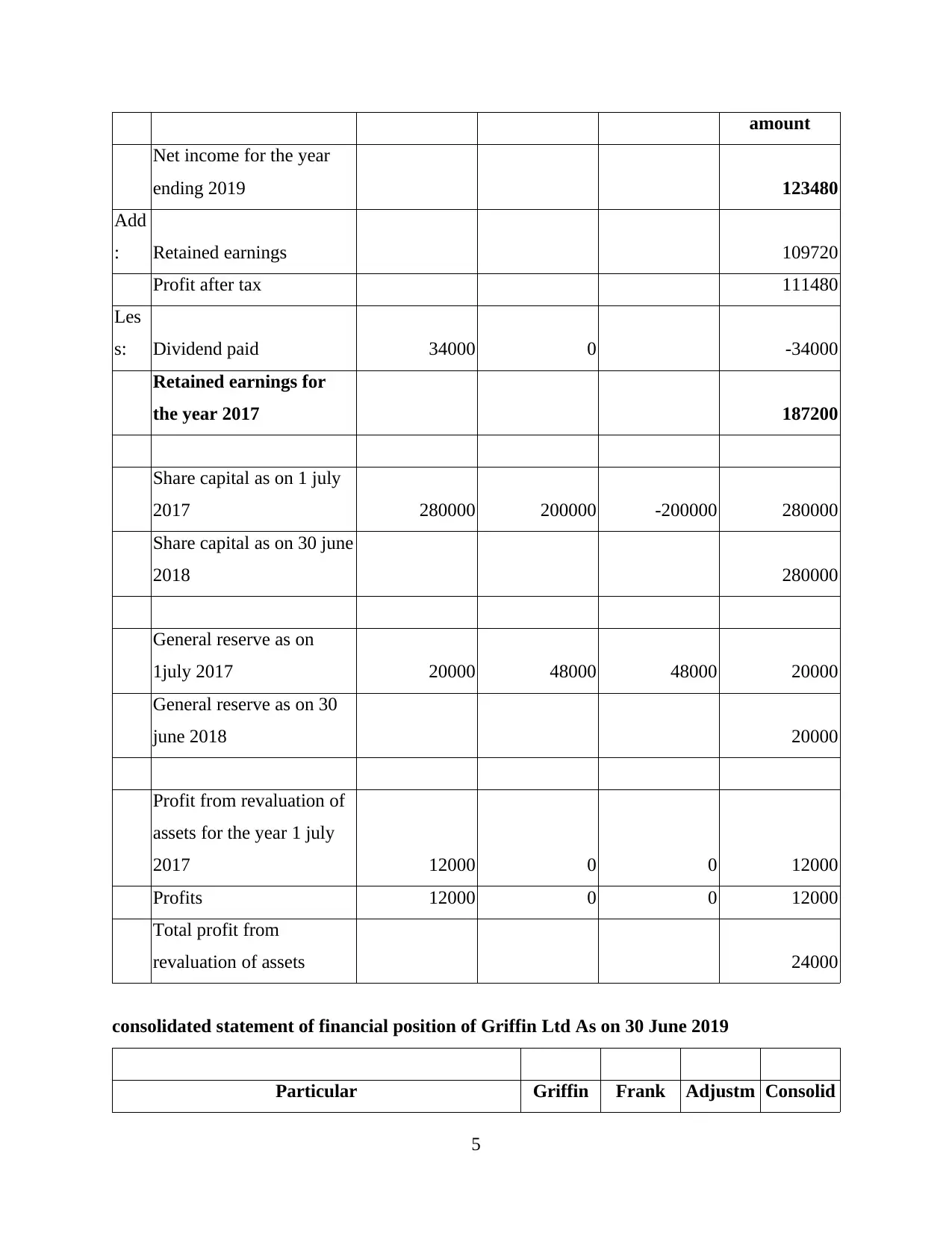

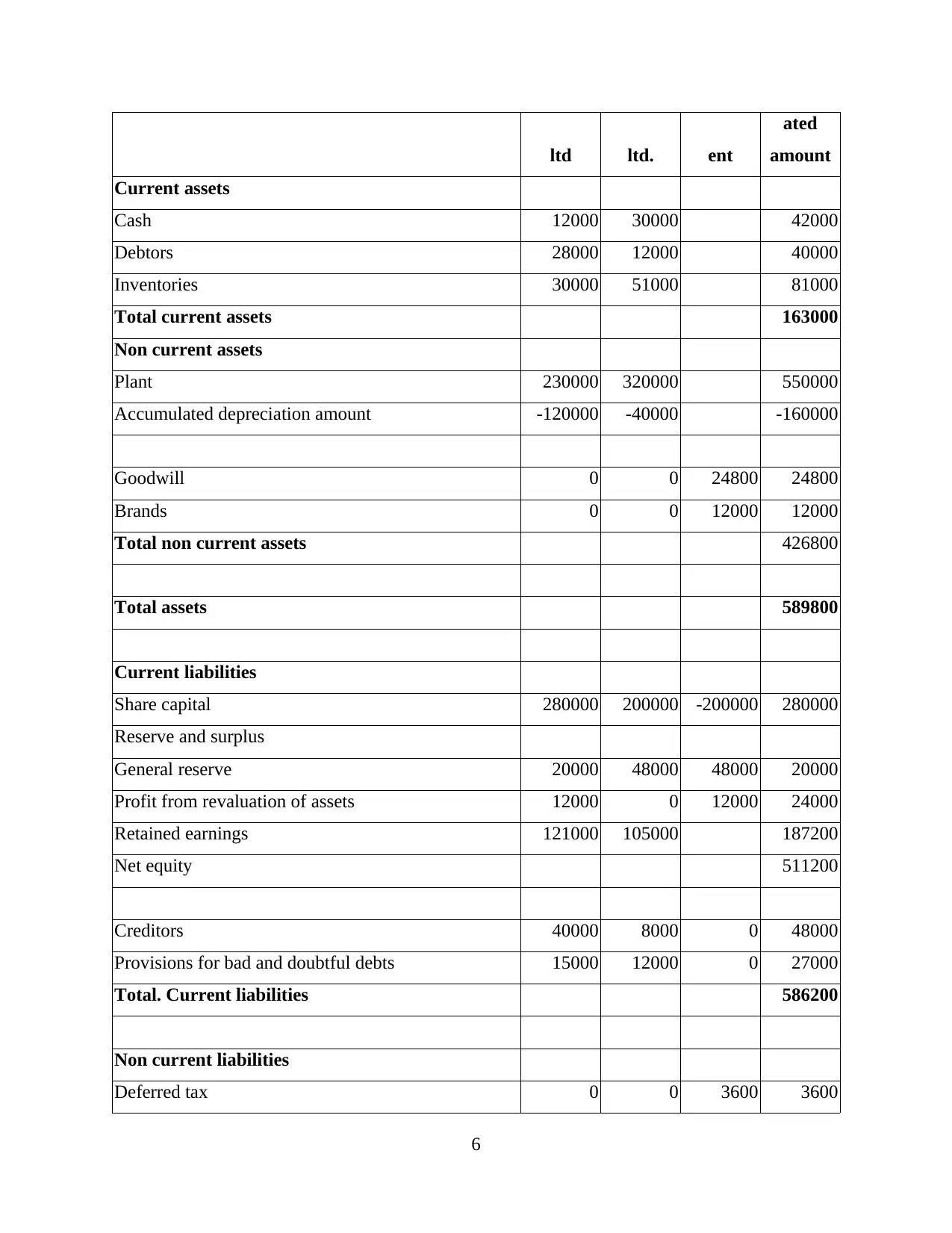

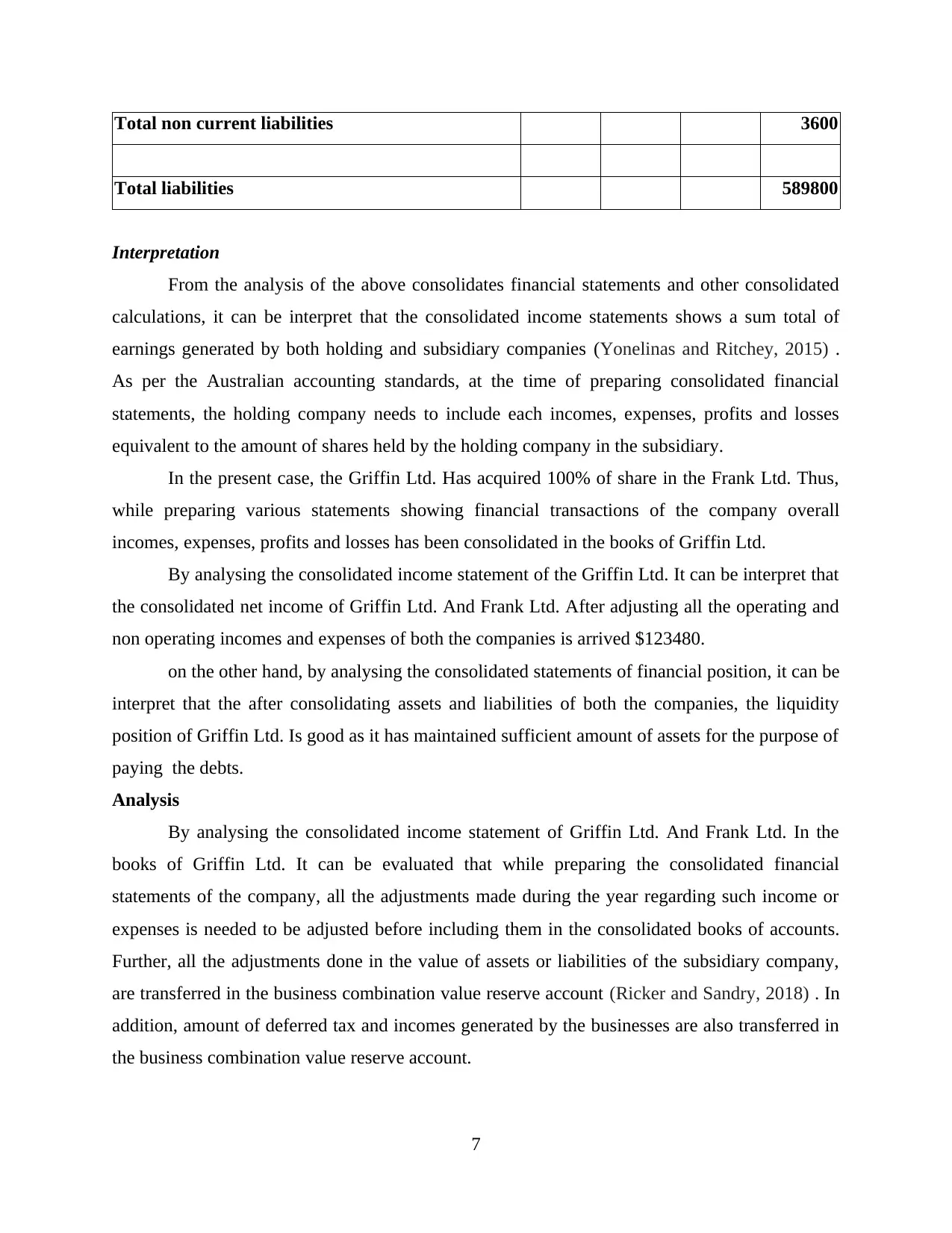

This report provides a comprehensive analysis of the consolidated financial statements of Griffin Ltd. The assignment focuses on the preparation and interpretation of these statements, including the income statement, statement of financial position, and statement of changes in equity. The report details the consolidation process, acquisition adjustments, and pre-acquisition entries. It includes working notes for calculations, such as retained earnings. The analysis covers key financial metrics and interpretations of the company's performance, considering the acquisition of Frank Ltd. The report also discusses assumptions made during the consolidation process and concludes with an overview of the company's financial position. This report is designed to provide a clear understanding of corporate accounting and financial reporting.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.