Corporate Accounting: IFRS3, Acquisition Analysis and Consolidation

VerifiedAdded on 2023/01/13

|13

|2355

|25

Report

AI Summary

This report delves into the realm of corporate accounting, providing a comprehensive analysis of key concepts and practical applications. It begins with an introduction to corporate accounting and its significance, followed by a detailed examination of International Financial Reporting Standard 3 (IFRS 3) and its implications for business combinations. The report then explores the process of identifying business combinations, the recognition and measurement principles, and the exceptions to these principles. Furthermore, the report applies these concepts to a case study involving the acquisition of Davis Ltd by Alma Corporation Ltd, including acquisition analysis and consolidation worksheet entries. The analysis includes calculating the net fair value of identifiable assets and liabilities, determining the net consideration transferred, and calculating gain from the acquisition. Finally, the report concludes by summarizing the key findings and emphasizing the importance of corporate accounting in ensuring accurate financial reporting and compliance with relevant standards.

CORPORATE

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...............................................................................................................3

MAIN BODY.......................................................................................................................3

Part (A)..........................................................................................................................3

PART B..............................................................................................................................7

Acquisition analysis at 1 July, 2018:.............................................................................8

Consolidation worksheet entries for Alma Ltd’s group at 30 June 2019:......................8

CONCLUSION...................................................................................................................9

REFERENCES................................................................................................................10

INTRODUCTION...............................................................................................................3

MAIN BODY.......................................................................................................................3

Part (A)..........................................................................................................................3

PART B..............................................................................................................................7

Acquisition analysis at 1 July, 2018:.............................................................................8

Consolidation worksheet entries for Alma Ltd’s group at 30 June 2019:......................8

CONCLUSION...................................................................................................................9

REFERENCES................................................................................................................10

INTRODUCTION

The term corporate accounting can be defined as a way of accounting that deals

with accounting for business entities for preparation of final accounts (Domino and

Blanton, 2015). It is quite crucial field which covers almost whole tasks and activities

concerned with recording and reporting of financial information. Accounting personnels

and financial division of corporation cumulatively establish corporate accounting-

structure. The major distinction here in conventional accounting practices and corporate

accounting practices is that corporate accounting interacts primarily with complying with

accounting practices, principles and regulations in publicly listed entities, not with

normal businesses. Corporate accounting is much wider field which is not limited to

recording to fiscal event but also it support timely and proper compliances of rules,

guidelines and standards prescribed by relevant authorities and bodies. The project

report is categorised into two parts A and B. Part A is about international financial

reporting standard 3 and part B is based on acquisition analysis on the basis of given

data.

MAIN BODY

Part (A)

How to determine whether a transaction is a business combination based on

AASB3/IFRS3.

The international financial reporting standard was reissued on January 2008 and

this is applicable for reporting of annual time frame commencing after 1st of July, 2009

(About AASB 3, 2019). The main objective of this standard is to enhance relevance,

reliability and compatibility of monetary information that is included in the financial

statements. This standard has below mentioned principles which are as follows:

Identifies and assess in its financial statements the recognisable assets

acquired. As well as the liabilities assumed and any non controlling interest in the

acquiree.

Identifies and assess the goodwill acquired in business combination from a

bargain purchase.

The term corporate accounting can be defined as a way of accounting that deals

with accounting for business entities for preparation of final accounts (Domino and

Blanton, 2015). It is quite crucial field which covers almost whole tasks and activities

concerned with recording and reporting of financial information. Accounting personnels

and financial division of corporation cumulatively establish corporate accounting-

structure. The major distinction here in conventional accounting practices and corporate

accounting practices is that corporate accounting interacts primarily with complying with

accounting practices, principles and regulations in publicly listed entities, not with

normal businesses. Corporate accounting is much wider field which is not limited to

recording to fiscal event but also it support timely and proper compliances of rules,

guidelines and standards prescribed by relevant authorities and bodies. The project

report is categorised into two parts A and B. Part A is about international financial

reporting standard 3 and part B is based on acquisition analysis on the basis of given

data.

MAIN BODY

Part (A)

How to determine whether a transaction is a business combination based on

AASB3/IFRS3.

The international financial reporting standard was reissued on January 2008 and

this is applicable for reporting of annual time frame commencing after 1st of July, 2009

(About AASB 3, 2019). The main objective of this standard is to enhance relevance,

reliability and compatibility of monetary information that is included in the financial

statements. This standard has below mentioned principles which are as follows:

Identifies and assess in its financial statements the recognisable assets

acquired. As well as the liabilities assumed and any non controlling interest in the

acquiree.

Identifies and assess the goodwill acquired in business combination from a

bargain purchase.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Assess what types of information is needed in order to disclose and enable

financial statement as well as impacts of business combination.

Identifying business combination:

Entities decide whether a deal or other occurrence is a combination of business

by implementing the concept in IFRS 3 that specifies that the obtained assets and

presumed liability represent a business. If the purchased assets are not a corporation,

then the reporting agency reports as an acquisition of assets for the sale or other

occurrence.

Recognition and measurement-

Every business combination should be responsible for using model of acquisition which

comprises:

Identification of acquirer.

Determination of date of acquisition.

Identifying and measuring goodwill and profits from bargain purchasing.

Identification of acquirer:

The combining entities are characterised as acquirer for every business

combination. Cases in which identification of acquirer is not straightforward consists

following:

In the case when there is combination of more than two corporations where one

of combining corporation should be identified as acquirer (About AASB 3, 2019).

Creation of a new business entity for issuance of equity to impact the business

combination.

Determination of date of acquisition:

The date on which the acquirer get control of acquiree is commonly the date on

that acquirer transfers consideration as well as acquires assets and assumes the

liabilities of acquiree- the closing date. Though, acquirer may acquire control over a

date which is earlier of late than the closing date.

financial statement as well as impacts of business combination.

Identifying business combination:

Entities decide whether a deal or other occurrence is a combination of business

by implementing the concept in IFRS 3 that specifies that the obtained assets and

presumed liability represent a business. If the purchased assets are not a corporation,

then the reporting agency reports as an acquisition of assets for the sale or other

occurrence.

Recognition and measurement-

Every business combination should be responsible for using model of acquisition which

comprises:

Identification of acquirer.

Determination of date of acquisition.

Identifying and measuring goodwill and profits from bargain purchasing.

Identification of acquirer:

The combining entities are characterised as acquirer for every business

combination. Cases in which identification of acquirer is not straightforward consists

following:

In the case when there is combination of more than two corporations where one

of combining corporation should be identified as acquirer (About AASB 3, 2019).

Creation of a new business entity for issuance of equity to impact the business

combination.

Determination of date of acquisition:

The date on which the acquirer get control of acquiree is commonly the date on

that acquirer transfers consideration as well as acquires assets and assumes the

liabilities of acquiree- the closing date. Though, acquirer may acquire control over a

date which is earlier of late than the closing date.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Recognition principle:

In accordance of acquisition date, the acquirer should identify individually from

goodwill, the identifiable assets acquired as well as liabilities which are assumed and

non controlling interest in acquiree.

Recognition conditions:

The recognizable acquisitions obtained and liability inherited must fulfil asset and

liability requirements in the financial statements preparedness and presentation

Framework (as specified by AASB 1048 Understanding of Standards) at the time

of acquisition to qualify for the acknowledgement as part of the acquisition

process. For instance, acquired staff costs are not liability on the date of the

purchase, but they are not required in the future to leave the acquired operation

program or to eliminate jobs and/or transfer the acquired employee.

Further, the recognizable assets obtained and the liabilities assigned must

become part of what can be shared by the acquiree and the retained person (or

former owners), rather than by arising from multiple transactions, for the

purposes of acknowledgement as part of implementation of the acquisition

process. Application of the guide in subsections 51–53 is made in the acquirer to

assess the acquired assets or presumed liabilities are included in the acquisition

exchange and, where any, are the result of multiple transactions that have to be

reported for in compliance with the Australian Accounting Standards relevant to

them.

An acquirer may be able to recognize those assets and liabilities which he had

not historically identified as assets or liabilities in his financial reports by

implementation of the law of identification and condition. For instance, the

purchaser recognizes in his financial reports the obtained accrued liabilities

property, as a brand name, patent or consumer relation, which he did not

recognize as assets because he has created it directly and has paid the

associated costs of the expenditures.

In accordance of acquisition date, the acquirer should identify individually from

goodwill, the identifiable assets acquired as well as liabilities which are assumed and

non controlling interest in acquiree.

Recognition conditions:

The recognizable acquisitions obtained and liability inherited must fulfil asset and

liability requirements in the financial statements preparedness and presentation

Framework (as specified by AASB 1048 Understanding of Standards) at the time

of acquisition to qualify for the acknowledgement as part of the acquisition

process. For instance, acquired staff costs are not liability on the date of the

purchase, but they are not required in the future to leave the acquired operation

program or to eliminate jobs and/or transfer the acquired employee.

Further, the recognizable assets obtained and the liabilities assigned must

become part of what can be shared by the acquiree and the retained person (or

former owners), rather than by arising from multiple transactions, for the

purposes of acknowledgement as part of implementation of the acquisition

process. Application of the guide in subsections 51–53 is made in the acquirer to

assess the acquired assets or presumed liabilities are included in the acquisition

exchange and, where any, are the result of multiple transactions that have to be

reported for in compliance with the Australian Accounting Standards relevant to

them.

An acquirer may be able to recognize those assets and liabilities which he had

not historically identified as assets or liabilities in his financial reports by

implementation of the law of identification and condition. For instance, the

purchaser recognizes in his financial reports the obtained accrued liabilities

property, as a brand name, patent or consumer relation, which he did not

recognize as assets because he has created it directly and has paid the

associated costs of the expenditures.

At that time, the acquirer must, in order to implement more Australian Accounting

Standards, identify or assign the identified acquired assets or the liabilities

presumed as appropriate. In consideration of contract requirements, economic

circumstances, operational or accounting practices and other applicable factors

as they are available at the date of acquisition, the purchaser intend to make any

category or designation.

In some cases, Australian accounting standards provide various accounts based

on the way a particular benefit or liability is categorized or allocated. The acquirer

shall provide descriptions of categories or designations in compliance with the

relevant terms as they occur at the time of acquisition, not necessarily limited:

1. Classification of specific financial assets and liabilities by fair value by gains or

losses or amortized costs or by fair value calculation of other full income in

compliance with AASB 9 standard.

2. Designation of derivative instruments as an instrument of hedging as per the

AASB 9.

3. Analyse of whether a derivative must be individual from a contract of host as per

the AASB 9.

In addition, this standard provides two exception to the principle which are as

follows:

(a) Categorization of contract of lease as an operating and finance lease as per

the standard of lease AASB 117.

(b) Categorization of contract into insurance contract as per the AASB 4.

The acquirer must categorise those contracts which will change its classification at the

time of modification and that time can be acquisition date. The classification should be

done in accordance of terms of contract and other factors.

Measurement principles:

The acquirer should measure identifiable assets acquired and liability which are

presumed on fair value on date of acquisition (Aburous, 2016).

Standards, identify or assign the identified acquired assets or the liabilities

presumed as appropriate. In consideration of contract requirements, economic

circumstances, operational or accounting practices and other applicable factors

as they are available at the date of acquisition, the purchaser intend to make any

category or designation.

In some cases, Australian accounting standards provide various accounts based

on the way a particular benefit or liability is categorized or allocated. The acquirer

shall provide descriptions of categories or designations in compliance with the

relevant terms as they occur at the time of acquisition, not necessarily limited:

1. Classification of specific financial assets and liabilities by fair value by gains or

losses or amortized costs or by fair value calculation of other full income in

compliance with AASB 9 standard.

2. Designation of derivative instruments as an instrument of hedging as per the

AASB 9.

3. Analyse of whether a derivative must be individual from a contract of host as per

the AASB 9.

In addition, this standard provides two exception to the principle which are as

follows:

(a) Categorization of contract of lease as an operating and finance lease as per

the standard of lease AASB 117.

(b) Categorization of contract into insurance contract as per the AASB 4.

The acquirer must categorise those contracts which will change its classification at the

time of modification and that time can be acquisition date. The classification should be

done in accordance of terms of contract and other factors.

Measurement principles:

The acquirer should measure identifiable assets acquired and liability which are

presumed on fair value on date of acquisition (Aburous, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

At the time of the purchase, for each market mix, the acquirer should calculate

UN-controlling interest elements of the acquirer which are present equity

interests and shall be entitled their owners in the case of a wind-up to a

commensurate share of the company's net assets:

(a) Fair value

(b) Current ownership instrument, in proportionate share under identified amount of

identified net assets of acquiree.

All other components of non controlling interest should be measured on their fair values

on acquisition date. Other wise another basis of measurement is needed by Australian

accounting standard.

The range of identified asset and liability which consists item for that this

standard offers limited exception to principle of measurement.

Exception to recognition or principle of measurement:

The standard provides limited exception to recognition and principle of

measurement. It specify both nature of exception and specified item to that

exception is provided (Nulla, 2012). The acquirer must be accountable for those

items by implementation of requirements that will result in some items being:

(a) Identified either by implementing recognition condition or by implementing the

requirement of other Australian accounting standard along with the result which differ

from implementing the terms and condition of recognition.

(b) Measured a value other than their date of acquisition date fair values.

PART B

Combinations of business are combinations created by 2 and sometimes more

corporate units in order to achieve certain mutual goals (particularly the reduction of

competitiveness); these combinations vary from broadest combinations via alliances to

strongest combinations by full consolidations (El-Firjani, Menacere and Pegum, 2014).

Provided Data:

Alma Corporation Ltd →(Acquired shares (ex dividend) → Corporation Davis Ltd

[100%]

UN-controlling interest elements of the acquirer which are present equity

interests and shall be entitled their owners in the case of a wind-up to a

commensurate share of the company's net assets:

(a) Fair value

(b) Current ownership instrument, in proportionate share under identified amount of

identified net assets of acquiree.

All other components of non controlling interest should be measured on their fair values

on acquisition date. Other wise another basis of measurement is needed by Australian

accounting standard.

The range of identified asset and liability which consists item for that this

standard offers limited exception to principle of measurement.

Exception to recognition or principle of measurement:

The standard provides limited exception to recognition and principle of

measurement. It specify both nature of exception and specified item to that

exception is provided (Nulla, 2012). The acquirer must be accountable for those

items by implementation of requirements that will result in some items being:

(a) Identified either by implementing recognition condition or by implementing the

requirement of other Australian accounting standard along with the result which differ

from implementing the terms and condition of recognition.

(b) Measured a value other than their date of acquisition date fair values.

PART B

Combinations of business are combinations created by 2 and sometimes more

corporate units in order to achieve certain mutual goals (particularly the reduction of

competitiveness); these combinations vary from broadest combinations via alliances to

strongest combinations by full consolidations (El-Firjani, Menacere and Pegum, 2014).

Provided Data:

Alma Corporation Ltd →(Acquired shares (ex dividend) → Corporation Davis Ltd

[100%]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

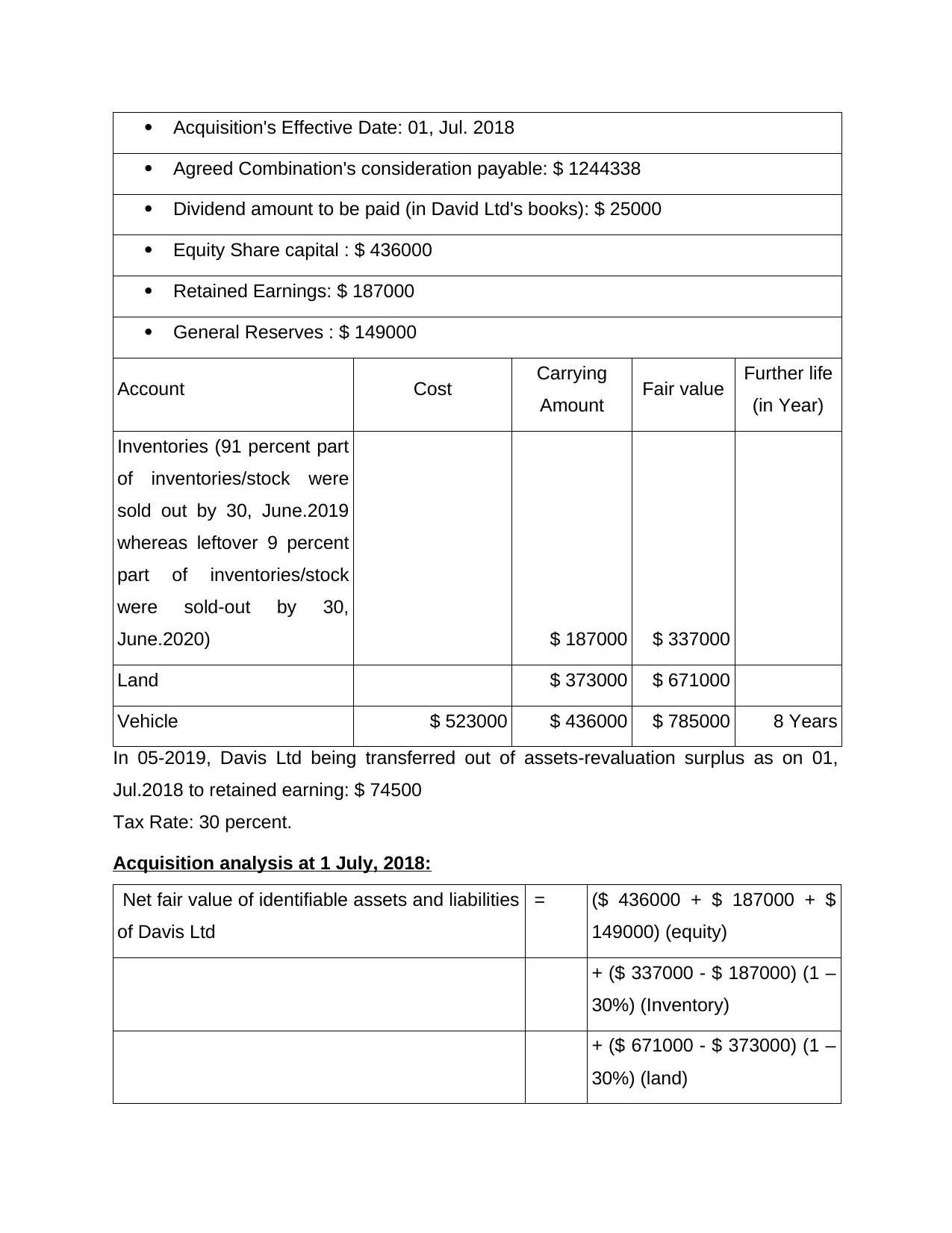

Acquisition's Effective Date: 01, Jul. 2018

Agreed Combination's consideration payable: $ 1244338

Dividend amount to be paid (in David Ltd's books): $ 25000

Equity Share capital : $ 436000

Retained Earnings: $ 187000

General Reserves : $ 149000

Account Cost Carrying

Amount Fair value Further life

(in Year)

Inventories (91 percent part

of inventories/stock were

sold out by 30, June.2019

whereas leftover 9 percent

part of inventories/stock

were sold-out by 30,

June.2020) $ 187000 $ 337000

Land $ 373000 $ 671000

Vehicle $ 523000 $ 436000 $ 785000 8 Years

In 05-2019, Davis Ltd being transferred out of assets-revaluation surplus as on 01,

Jul.2018 to retained earning: $ 74500

Tax Rate: 30 percent.

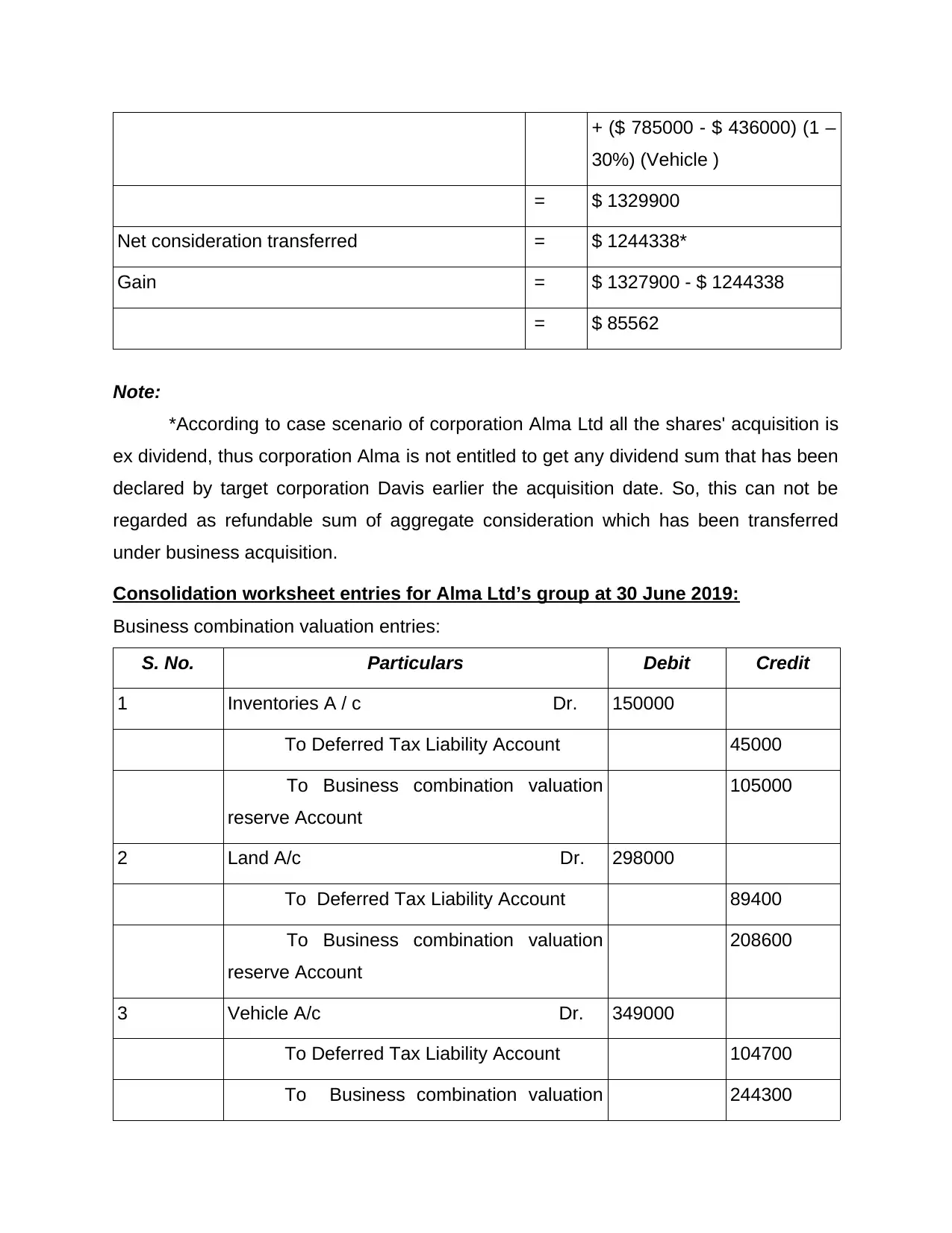

Acquisition analysis at 1 July, 2018:

Net fair value of identifiable assets and liabilities

of Davis Ltd

= ($ 436000 + $ 187000 + $

149000) (equity)

+ ($ 337000 - $ 187000) (1 –

30%) (Inventory)

+ ($ 671000 - $ 373000) (1 –

30%) (land)

Agreed Combination's consideration payable: $ 1244338

Dividend amount to be paid (in David Ltd's books): $ 25000

Equity Share capital : $ 436000

Retained Earnings: $ 187000

General Reserves : $ 149000

Account Cost Carrying

Amount Fair value Further life

(in Year)

Inventories (91 percent part

of inventories/stock were

sold out by 30, June.2019

whereas leftover 9 percent

part of inventories/stock

were sold-out by 30,

June.2020) $ 187000 $ 337000

Land $ 373000 $ 671000

Vehicle $ 523000 $ 436000 $ 785000 8 Years

In 05-2019, Davis Ltd being transferred out of assets-revaluation surplus as on 01,

Jul.2018 to retained earning: $ 74500

Tax Rate: 30 percent.

Acquisition analysis at 1 July, 2018:

Net fair value of identifiable assets and liabilities

of Davis Ltd

= ($ 436000 + $ 187000 + $

149000) (equity)

+ ($ 337000 - $ 187000) (1 –

30%) (Inventory)

+ ($ 671000 - $ 373000) (1 –

30%) (land)

+ ($ 785000 - $ 436000) (1 –

30%) (Vehicle )

= $ 1329900

Net consideration transferred = $ 1244338*

Gain = $ 1327900 - $ 1244338

= $ 85562

Note:

*According to case scenario of corporation Alma Ltd all the shares' acquisition is

ex dividend, thus corporation Alma is not entitled to get any dividend sum that has been

declared by target corporation Davis earlier the acquisition date. So, this can not be

regarded as refundable sum of aggregate consideration which has been transferred

under business acquisition.

Consolidation worksheet entries for Alma Ltd’s group at 30 June 2019:

Business combination valuation entries:

S. No. Particulars Debit Credit

1 Inventories A / c Dr. 150000

To Deferred Tax Liability Account 45000

To Business combination valuation

reserve Account

105000

2 Land A/c Dr. 298000

To Deferred Tax Liability Account 89400

To Business combination valuation

reserve Account

208600

3 Vehicle A/c Dr. 349000

To Deferred Tax Liability Account 104700

To Business combination valuation 244300

30%) (Vehicle )

= $ 1329900

Net consideration transferred = $ 1244338*

Gain = $ 1327900 - $ 1244338

= $ 85562

Note:

*According to case scenario of corporation Alma Ltd all the shares' acquisition is

ex dividend, thus corporation Alma is not entitled to get any dividend sum that has been

declared by target corporation Davis earlier the acquisition date. So, this can not be

regarded as refundable sum of aggregate consideration which has been transferred

under business acquisition.

Consolidation worksheet entries for Alma Ltd’s group at 30 June 2019:

Business combination valuation entries:

S. No. Particulars Debit Credit

1 Inventories A / c Dr. 150000

To Deferred Tax Liability Account 45000

To Business combination valuation

reserve Account

105000

2 Land A/c Dr. 298000

To Deferred Tax Liability Account 89400

To Business combination valuation

reserve Account

208600

3 Vehicle A/c Dr. 349000

To Deferred Tax Liability Account 104700

To Business combination valuation 244300

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

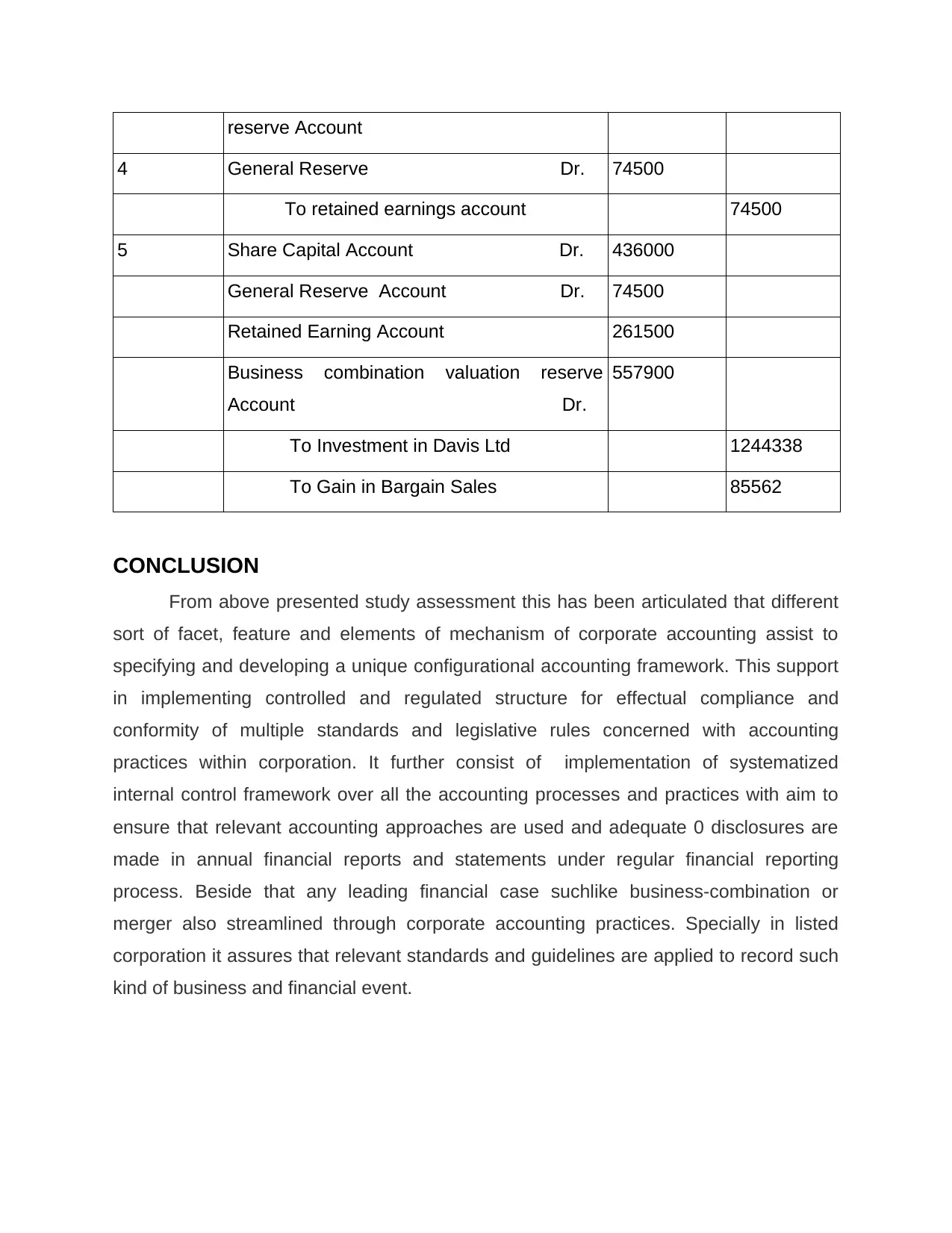

reserve Account

4 General Reserve Dr. 74500

To retained earnings account 74500

5 Share Capital Account Dr. 436000

General Reserve Account Dr. 74500

Retained Earning Account 261500

Business combination valuation reserve

Account Dr.

557900

To Investment in Davis Ltd 1244338

To Gain in Bargain Sales 85562

CONCLUSION

From above presented study assessment this has been articulated that different

sort of facet, feature and elements of mechanism of corporate accounting assist to

specifying and developing a unique configurational accounting framework. This support

in implementing controlled and regulated structure for effectual compliance and

conformity of multiple standards and legislative rules concerned with accounting

practices within corporation. It further consist of implementation of systematized

internal control framework over all the accounting processes and practices with aim to

ensure that relevant accounting approaches are used and adequate 0 disclosures are

made in annual financial reports and statements under regular financial reporting

process. Beside that any leading financial case suchlike business-combination or

merger also streamlined through corporate accounting practices. Specially in listed

corporation it assures that relevant standards and guidelines are applied to record such

kind of business and financial event.

4 General Reserve Dr. 74500

To retained earnings account 74500

5 Share Capital Account Dr. 436000

General Reserve Account Dr. 74500

Retained Earning Account 261500

Business combination valuation reserve

Account Dr.

557900

To Investment in Davis Ltd 1244338

To Gain in Bargain Sales 85562

CONCLUSION

From above presented study assessment this has been articulated that different

sort of facet, feature and elements of mechanism of corporate accounting assist to

specifying and developing a unique configurational accounting framework. This support

in implementing controlled and regulated structure for effectual compliance and

conformity of multiple standards and legislative rules concerned with accounting

practices within corporation. It further consist of implementation of systematized

internal control framework over all the accounting processes and practices with aim to

ensure that relevant accounting approaches are used and adequate 0 disclosures are

made in annual financial reports and statements under regular financial reporting

process. Beside that any leading financial case suchlike business-combination or

merger also streamlined through corporate accounting practices. Specially in listed

corporation it assures that relevant standards and guidelines are applied to record such

kind of business and financial event.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journal:

Domino, M. A., Wingreen, S. C. and Blanton, J. E., 2015. Social cognitive theory: The

antecedents and effects of ethical climate fit on organizational attitudes of

corporate accounting professionals—a reflection of client narcissism and fraud

attitude risk. Journal of Business Ethics. 131(2). pp.453-467.

El-Firjani, E., Menacere, K. and Pegum, R., 2014. Developing corporate accounting

regulation in Libya past and future challenges. Journal of Accounting in

Emerging Economies.

Nulla, Y., 2012. The Study of CEO Compensation System in American Health

Companies: An Analysis between CEO Compensation, Firm Size, Accounting

Performance, and Corporate Accounting Performance. International Journal of

Scientific & Engineering Research, Forthcoming.

Aburous, D., 2016. Understanding cultural capital and habitus in Corporate Accounting:

A postcolonial context. Spanish Journal of Finance and Accounting/Revista

Española de Financiación y Contabilidad. 45(2). pp.154-179.

Online:

About AASB 3, 2019 [online] available

through:<https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf>

Books and journal:

Domino, M. A., Wingreen, S. C. and Blanton, J. E., 2015. Social cognitive theory: The

antecedents and effects of ethical climate fit on organizational attitudes of

corporate accounting professionals—a reflection of client narcissism and fraud

attitude risk. Journal of Business Ethics. 131(2). pp.453-467.

El-Firjani, E., Menacere, K. and Pegum, R., 2014. Developing corporate accounting

regulation in Libya past and future challenges. Journal of Accounting in

Emerging Economies.

Nulla, Y., 2012. The Study of CEO Compensation System in American Health

Companies: An Analysis between CEO Compensation, Firm Size, Accounting

Performance, and Corporate Accounting Performance. International Journal of

Scientific & Engineering Research, Forthcoming.

Aburous, D., 2016. Understanding cultural capital and habitus in Corporate Accounting:

A postcolonial context. Spanish Journal of Finance and Accounting/Revista

Española de Financiación y Contabilidad. 45(2). pp.154-179.

Online:

About AASB 3, 2019 [online] available

through:<https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf>

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.