Corporate Accounting: Funds, Liabilities, and Asset Measurement

VerifiedAdded on 2022/08/26

|12

|3164

|17

Report

AI Summary

This report provides a comprehensive analysis of corporate accounting practices, focusing on the financial reporting of BHP Billiton Ltd and Boral Ltd, both operating in the mining and material extraction industry. The assessment scrutinizes the companies' sources of funds (equity and debt), their capital structures over a three-year period, and the advantages and disadvantages associated with each funding source. Furthermore, it examines how the businesses report liabilities, provisions, contingent liabilities, and contingent assets, with a specific focus on the application of AASB 137 'Provisions, Contingent Liabilities and Contingent Assets'. The report also covers the classification of assets and the recognition criteria employed by the companies. The analysis includes an examination of the companies' annual reports, providing insights into their financial strategies and compliance with accounting standards.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ACCOUNTING

Abstract

The focus of the assessment is to comment on the reporting process which is followed

by two companies which belong to the same industry. The companies which are

selected are BHP Billiton ltd and Boral Ltd. The assessment compares the sources of

capital which is used by the businesses and relative advantages and disadvantages

associated with the same. The analysis also presents reporting process which is

followed by the management of the company for reporting assets and liabilities of the

businesses. The assessment also shows if the business has appropriately presented

the contingent liabilities and provisions for the business.

Table of Contents

Abstract

The focus of the assessment is to comment on the reporting process which is followed

by two companies which belong to the same industry. The companies which are

selected are BHP Billiton ltd and Boral Ltd. The assessment compares the sources of

capital which is used by the businesses and relative advantages and disadvantages

associated with the same. The analysis also presents reporting process which is

followed by the management of the company for reporting assets and liabilities of the

businesses. The assessment also shows if the business has appropriately presented

the contingent liabilities and provisions for the business.

Table of Contents

2CORPORATE ACCOUNTING

Introduction........................................................................................................................3

Discussion..........................................................................................................................3

Sources of Funds...........................................................................................................3

Changes in the Sources of Funds..................................................................................4

Different Sources of Funds (Percentage)......................................................................5

Advantages and Disadvantages of Different Funds......................................................5

Liabilities of the Businesses...........................................................................................6

Provisions, Contingent Liabilities and Contingent Assets..............................................6

Reporting for AASB 137.................................................................................................7

Classification of Assets..................................................................................................9

Recognition Criteria........................................................................................................9

Conclusion.........................................................................................................................9

Reference........................................................................................................................11

Introduction........................................................................................................................3

Discussion..........................................................................................................................3

Sources of Funds...........................................................................................................3

Changes in the Sources of Funds..................................................................................4

Different Sources of Funds (Percentage)......................................................................5

Advantages and Disadvantages of Different Funds......................................................5

Liabilities of the Businesses...........................................................................................6

Provisions, Contingent Liabilities and Contingent Assets..............................................6

Reporting for AASB 137.................................................................................................7

Classification of Assets..................................................................................................9

Recognition Criteria........................................................................................................9

Conclusion.........................................................................................................................9

Reference........................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ACCOUNTING

Introduction

The assessment considers the businesses of BHP Billiton Ltd and Boral Ltd

which are engaged in mining and material extraction operations and both the

companies belong to the same industry (Bhp.com. 2020). The assessment would be

reviewing the reporting of key items such as assets, liabilities and equities which the

companies have presented in their respective annual reports. For the purpose of

consideration, the most recent annual report for both the companies are considered.

Furthermore, the analysis would also be identifying if there have been any changes in

the capital structure for both the companies over a period of three years and the

reasons which are three for the same. The reporting framework which is used by the

entities for showing provisions would be reviewed and ascertained if the same is

consistent with the provisions which are stated under AASB 137 ‘Provisions, Contingent

Liabilities and Contingent Assets.

Discussion

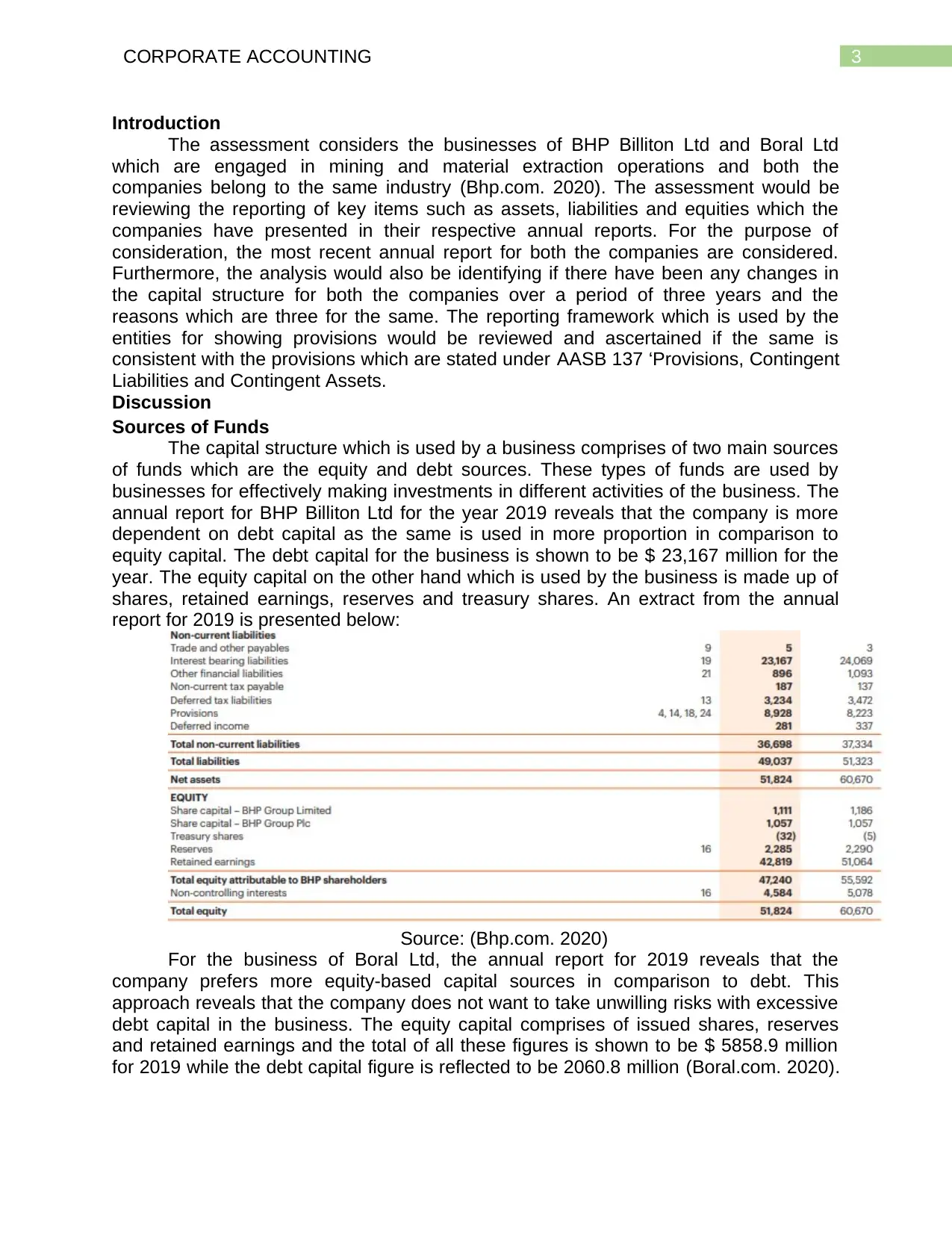

Sources of Funds

The capital structure which is used by a business comprises of two main sources

of funds which are the equity and debt sources. These types of funds are used by

businesses for effectively making investments in different activities of the business. The

annual report for BHP Billiton Ltd for the year 2019 reveals that the company is more

dependent on debt capital as the same is used in more proportion in comparison to

equity capital. The debt capital for the business is shown to be $ 23,167 million for the

year. The equity capital on the other hand which is used by the business is made up of

shares, retained earnings, reserves and treasury shares. An extract from the annual

report for 2019 is presented below:

Source: (Bhp.com. 2020)

For the business of Boral Ltd, the annual report for 2019 reveals that the

company prefers more equity-based capital sources in comparison to debt. This

approach reveals that the company does not want to take unwilling risks with excessive

debt capital in the business. The equity capital comprises of issued shares, reserves

and retained earnings and the total of all these figures is shown to be $ 5858.9 million

for 2019 while the debt capital figure is reflected to be 2060.8 million (Boral.com. 2020).

Introduction

The assessment considers the businesses of BHP Billiton Ltd and Boral Ltd

which are engaged in mining and material extraction operations and both the

companies belong to the same industry (Bhp.com. 2020). The assessment would be

reviewing the reporting of key items such as assets, liabilities and equities which the

companies have presented in their respective annual reports. For the purpose of

consideration, the most recent annual report for both the companies are considered.

Furthermore, the analysis would also be identifying if there have been any changes in

the capital structure for both the companies over a period of three years and the

reasons which are three for the same. The reporting framework which is used by the

entities for showing provisions would be reviewed and ascertained if the same is

consistent with the provisions which are stated under AASB 137 ‘Provisions, Contingent

Liabilities and Contingent Assets.

Discussion

Sources of Funds

The capital structure which is used by a business comprises of two main sources

of funds which are the equity and debt sources. These types of funds are used by

businesses for effectively making investments in different activities of the business. The

annual report for BHP Billiton Ltd for the year 2019 reveals that the company is more

dependent on debt capital as the same is used in more proportion in comparison to

equity capital. The debt capital for the business is shown to be $ 23,167 million for the

year. The equity capital on the other hand which is used by the business is made up of

shares, retained earnings, reserves and treasury shares. An extract from the annual

report for 2019 is presented below:

Source: (Bhp.com. 2020)

For the business of Boral Ltd, the annual report for 2019 reveals that the

company prefers more equity-based capital sources in comparison to debt. This

approach reveals that the company does not want to take unwilling risks with excessive

debt capital in the business. The equity capital comprises of issued shares, reserves

and retained earnings and the total of all these figures is shown to be $ 5858.9 million

for 2019 while the debt capital figure is reflected to be 2060.8 million (Boral.com. 2020).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ACCOUNTING

This shows that the management of the company is trying to maintain an appropriate

balance for the purpose of managing the risks of the business.

Source: (Boral.com. 2020)

Changes in the Sources of Funds

The sources of funds which are used by a company often changes with the

change in strategy of the business or changes in the objectives which is followed by a

business. In the case of BHP Billiton Ltd, the annual report of 2017 shows that the debt

which was used by the business is $ 29,233 million and the same is $ 23,167 million in

2019 which shows that there has been some decline in the debt capital which is used by

the business. Furthermore, there has also been a decline in the equity capital for the

business during the period. This reflects that the management of the company is trying

to reduce the overall capital which is being used considering the current level of

operations of the business (Southern 2016). The overall reserves for the business has

increased over the years which shows that the management of the company is working

on its internal strengths more for maintaining efficiency in the operations of the

business. Over the years, the business has tried to reduce the debt capital which is

mainly for managing the risks which is related to the business.

In the case of Boral Ltd, the annual report for 2017 is also considered for the

purpose of estimating the trend which is there for managing the capital structure of the

business. The management has managed to increase the equity capital of the business

while at the same time reducing the usage of debt capital in the operations of the entity

(Halling, Yu and Zechner 2016). This shows that there has been a shift in the capital

structure which is mainly aimed to control the risks which are related to the capital

structure of the business. The management of Boral Ltd has made positive changes to

the capital structure of the business which is effectively shown in the financial reports

which is formulated by the business.

This shows that the management of the company is trying to maintain an appropriate

balance for the purpose of managing the risks of the business.

Source: (Boral.com. 2020)

Changes in the Sources of Funds

The sources of funds which are used by a company often changes with the

change in strategy of the business or changes in the objectives which is followed by a

business. In the case of BHP Billiton Ltd, the annual report of 2017 shows that the debt

which was used by the business is $ 29,233 million and the same is $ 23,167 million in

2019 which shows that there has been some decline in the debt capital which is used by

the business. Furthermore, there has also been a decline in the equity capital for the

business during the period. This reflects that the management of the company is trying

to reduce the overall capital which is being used considering the current level of

operations of the business (Southern 2016). The overall reserves for the business has

increased over the years which shows that the management of the company is working

on its internal strengths more for maintaining efficiency in the operations of the

business. Over the years, the business has tried to reduce the debt capital which is

mainly for managing the risks which is related to the business.

In the case of Boral Ltd, the annual report for 2017 is also considered for the

purpose of estimating the trend which is there for managing the capital structure of the

business. The management has managed to increase the equity capital of the business

while at the same time reducing the usage of debt capital in the operations of the entity

(Halling, Yu and Zechner 2016). This shows that there has been a shift in the capital

structure which is mainly aimed to control the risks which are related to the capital

structure of the business. The management of Boral Ltd has made positive changes to

the capital structure of the business which is effectively shown in the financial reports

which is formulated by the business.

5CORPORATE ACCOUNTING

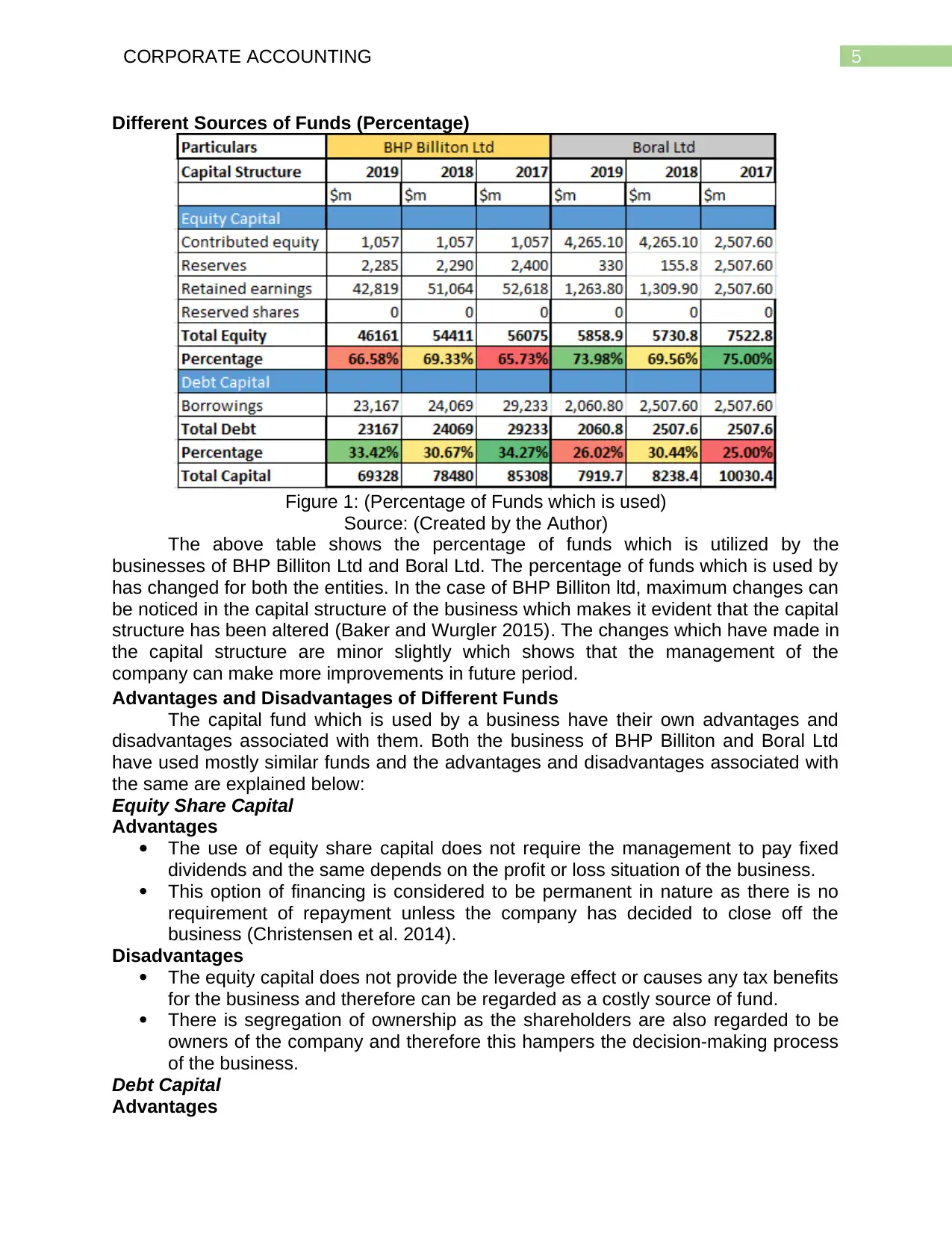

Different Sources of Funds (Percentage)

Figure 1: (Percentage of Funds which is used)

Source: (Created by the Author)

The above table shows the percentage of funds which is utilized by the

businesses of BHP Billiton Ltd and Boral Ltd. The percentage of funds which is used by

has changed for both the entities. In the case of BHP Billiton ltd, maximum changes can

be noticed in the capital structure of the business which makes it evident that the capital

structure has been altered (Baker and Wurgler 2015). The changes which have made in

the capital structure are minor slightly which shows that the management of the

company can make more improvements in future period.

Advantages and Disadvantages of Different Funds

The capital fund which is used by a business have their own advantages and

disadvantages associated with them. Both the business of BHP Billiton and Boral Ltd

have used mostly similar funds and the advantages and disadvantages associated with

the same are explained below:

Equity Share Capital

Advantages

The use of equity share capital does not require the management to pay fixed

dividends and the same depends on the profit or loss situation of the business.

This option of financing is considered to be permanent in nature as there is no

requirement of repayment unless the company has decided to close off the

business (Christensen et al. 2014).

Disadvantages

The equity capital does not provide the leverage effect or causes any tax benefits

for the business and therefore can be regarded as a costly source of fund.

There is segregation of ownership as the shareholders are also regarded to be

owners of the company and therefore this hampers the decision-making process

of the business.

Debt Capital

Advantages

Different Sources of Funds (Percentage)

Figure 1: (Percentage of Funds which is used)

Source: (Created by the Author)

The above table shows the percentage of funds which is utilized by the

businesses of BHP Billiton Ltd and Boral Ltd. The percentage of funds which is used by

has changed for both the entities. In the case of BHP Billiton ltd, maximum changes can

be noticed in the capital structure of the business which makes it evident that the capital

structure has been altered (Baker and Wurgler 2015). The changes which have made in

the capital structure are minor slightly which shows that the management of the

company can make more improvements in future period.

Advantages and Disadvantages of Different Funds

The capital fund which is used by a business have their own advantages and

disadvantages associated with them. Both the business of BHP Billiton and Boral Ltd

have used mostly similar funds and the advantages and disadvantages associated with

the same are explained below:

Equity Share Capital

Advantages

The use of equity share capital does not require the management to pay fixed

dividends and the same depends on the profit or loss situation of the business.

This option of financing is considered to be permanent in nature as there is no

requirement of repayment unless the company has decided to close off the

business (Christensen et al. 2014).

Disadvantages

The equity capital does not provide the leverage effect or causes any tax benefits

for the business and therefore can be regarded as a costly source of fund.

There is segregation of ownership as the shareholders are also regarded to be

owners of the company and therefore this hampers the decision-making process

of the business.

Debt Capital

Advantages

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ACCOUNTING

The usage of debt capital allows a business to take advantage of leverage effect

as well as also enjoy tax deductions which are associated with the interest

payments which is made by the business (Akeem et al. 2014).

There is no change in the ownership in case of debt capital and no segregation

of the same which is the case of equity capital which ensures that decisions are

taken swiftly.

Disadvantages

The business needs to bear regular interest payments irrespective of whether the

business has generated profits or not. This creates a burden on the management

of the business.

The availability of debt capital is difficult as the same depends on the credit

ratings which is associated with a business.

Retained earnings and Reserves

Advantages

These sources are savings which are kept aside by the management of the

company for reinvestment purposes and the same displays internal strength of

the business.

Disadvantage

The application of such form of capital impacts the cash position of the business

and also depletes savings of the business.

Liabilities of the Businesses

The liabilities of a business are shown in the balance sheet of the company and

are formatted as per the integrated reporting framework. The annual report of BHP

Billiton ltd is efficiently presented showing the liabilities under the heads of current and

non-current liabilities. One of the main items which is shown in current liabilities is trade

payables which is shown to be $ 6717 million and the business also has taken a short-

term loan from bank which is shown. In addition to this, the balance sheet also shows

deferred income, current tax payables and other current liabilities. On the other hand,

the non-current liabilities show the long-term debt which the business has taken along

with other financial liabilities of the business (Dichev 2017). The business has also

maintained provisions of long term nature for any anticipated liabilities which is related

to the business.

The financial report for Boral Ltd for the year 2019 shows that the business has

also classified the liabilities in an appropriate manner. The business shows trade

payables and short-term loans which are represented at the values of $ 832.6 million

and $ 339.7 million. There are also employee benefit liabilities which is presented in the

current liabilities side and also shows provisions which is maintained by the business for

meeting short term obligations (Duijm and Wierts 2016). The non-current liabilities

reveal long-term loans and tax liabilities associated with the business. The liabilities for

the business of Boral Ltd has shown to have increased slightly over the years which

may be due to the expansion process which the business is following.

Provisions, Contingent Liabilities and Contingent Assets

As per the outline which is provided by AASB 137 “Provisions, Contingent

Liabilities and Contingent Assets”, contingent assets, liabilities and provisions are to

be recognised in the annual statements following a framework. The reporting should be

accompanied with appropriate disclosures which is associated with the same. It is to be

The usage of debt capital allows a business to take advantage of leverage effect

as well as also enjoy tax deductions which are associated with the interest

payments which is made by the business (Akeem et al. 2014).

There is no change in the ownership in case of debt capital and no segregation

of the same which is the case of equity capital which ensures that decisions are

taken swiftly.

Disadvantages

The business needs to bear regular interest payments irrespective of whether the

business has generated profits or not. This creates a burden on the management

of the business.

The availability of debt capital is difficult as the same depends on the credit

ratings which is associated with a business.

Retained earnings and Reserves

Advantages

These sources are savings which are kept aside by the management of the

company for reinvestment purposes and the same displays internal strength of

the business.

Disadvantage

The application of such form of capital impacts the cash position of the business

and also depletes savings of the business.

Liabilities of the Businesses

The liabilities of a business are shown in the balance sheet of the company and

are formatted as per the integrated reporting framework. The annual report of BHP

Billiton ltd is efficiently presented showing the liabilities under the heads of current and

non-current liabilities. One of the main items which is shown in current liabilities is trade

payables which is shown to be $ 6717 million and the business also has taken a short-

term loan from bank which is shown. In addition to this, the balance sheet also shows

deferred income, current tax payables and other current liabilities. On the other hand,

the non-current liabilities show the long-term debt which the business has taken along

with other financial liabilities of the business (Dichev 2017). The business has also

maintained provisions of long term nature for any anticipated liabilities which is related

to the business.

The financial report for Boral Ltd for the year 2019 shows that the business has

also classified the liabilities in an appropriate manner. The business shows trade

payables and short-term loans which are represented at the values of $ 832.6 million

and $ 339.7 million. There are also employee benefit liabilities which is presented in the

current liabilities side and also shows provisions which is maintained by the business for

meeting short term obligations (Duijm and Wierts 2016). The non-current liabilities

reveal long-term loans and tax liabilities associated with the business. The liabilities for

the business of Boral Ltd has shown to have increased slightly over the years which

may be due to the expansion process which the business is following.

Provisions, Contingent Liabilities and Contingent Assets

As per the outline which is provided by AASB 137 “Provisions, Contingent

Liabilities and Contingent Assets”, contingent assets, liabilities and provisions are to

be recognised in the annual statements following a framework. The reporting should be

accompanied with appropriate disclosures which is associated with the same. It is to be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

noted that provisions are created by the management of the company to recognise any

future losses which is most probable such as contingent liabilities. The standard

requires businesses to disclose any probable losses and make provisions for the same

in the annual report so that some transparency is maintained in the reporting framework

of the business.

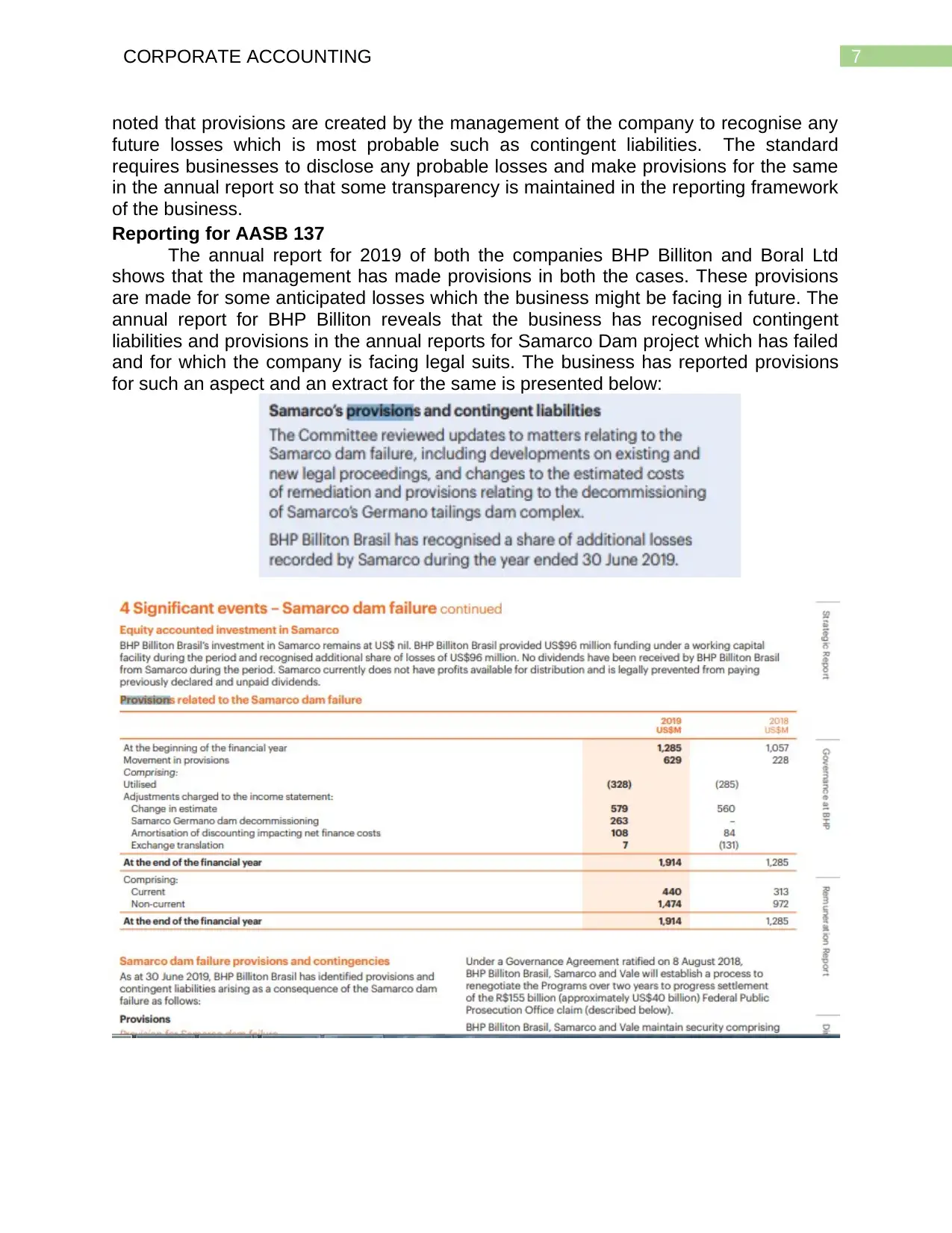

Reporting for AASB 137

The annual report for 2019 of both the companies BHP Billiton and Boral Ltd

shows that the management has made provisions in both the cases. These provisions

are made for some anticipated losses which the business might be facing in future. The

annual report for BHP Billiton reveals that the business has recognised contingent

liabilities and provisions in the annual reports for Samarco Dam project which has failed

and for which the company is facing legal suits. The business has reported provisions

for such an aspect and an extract for the same is presented below:

noted that provisions are created by the management of the company to recognise any

future losses which is most probable such as contingent liabilities. The standard

requires businesses to disclose any probable losses and make provisions for the same

in the annual report so that some transparency is maintained in the reporting framework

of the business.

Reporting for AASB 137

The annual report for 2019 of both the companies BHP Billiton and Boral Ltd

shows that the management has made provisions in both the cases. These provisions

are made for some anticipated losses which the business might be facing in future. The

annual report for BHP Billiton reveals that the business has recognised contingent

liabilities and provisions in the annual reports for Samarco Dam project which has failed

and for which the company is facing legal suits. The business has reported provisions

for such an aspect and an extract for the same is presented below:

8CORPORATE ACCOUNTING

The above extracts show the extensive disclosures which is provided by the

business in the notes to account section. This shows that the management of the

company has appropriately followed the reporting standard of AASB 137 and provided

all information in the annual report of the company thereby providing full disclosures.

In the case if Boral Ltd, the annual report for the company is considered for 2019

for ascertaining the disclosures which is shown by the management (Kulikova,

Grigoryeva and Gubaidullina 2014). The business has made a provision of $ 23.8

million for a restoration project of a limestone quarry and in addition to this, the

company has also made provisions for different losses which the management of the

company anticipates during the period. An extract of the disclosures is provided in the

annual report of the company and the same is presented below:

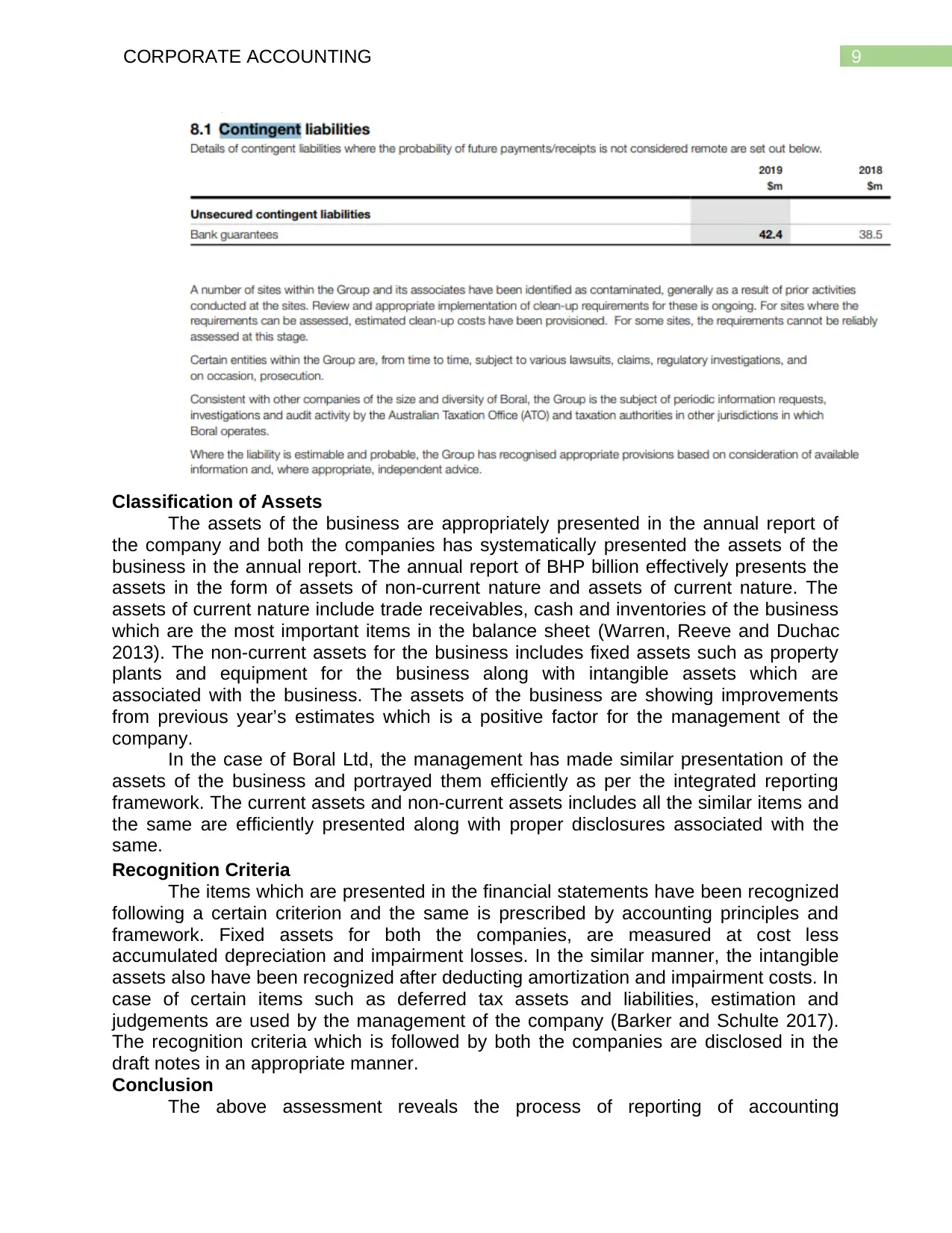

The annual report of the company also shows presence of contingent liabilities

which is generally for the clean-up requirements for areas where there was prior

activities of the business and anticipated losses associated with the same are shown as

disclosures (Sayari and Mugan 2013). An extract for the same is presented below:

The above extracts show the extensive disclosures which is provided by the

business in the notes to account section. This shows that the management of the

company has appropriately followed the reporting standard of AASB 137 and provided

all information in the annual report of the company thereby providing full disclosures.

In the case if Boral Ltd, the annual report for the company is considered for 2019

for ascertaining the disclosures which is shown by the management (Kulikova,

Grigoryeva and Gubaidullina 2014). The business has made a provision of $ 23.8

million for a restoration project of a limestone quarry and in addition to this, the

company has also made provisions for different losses which the management of the

company anticipates during the period. An extract of the disclosures is provided in the

annual report of the company and the same is presented below:

The annual report of the company also shows presence of contingent liabilities

which is generally for the clean-up requirements for areas where there was prior

activities of the business and anticipated losses associated with the same are shown as

disclosures (Sayari and Mugan 2013). An extract for the same is presented below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE ACCOUNTING

Classification of Assets

The assets of the business are appropriately presented in the annual report of

the company and both the companies has systematically presented the assets of the

business in the annual report. The annual report of BHP billion effectively presents the

assets in the form of assets of non-current nature and assets of current nature. The

assets of current nature include trade receivables, cash and inventories of the business

which are the most important items in the balance sheet (Warren, Reeve and Duchac

2013). The non-current assets for the business includes fixed assets such as property

plants and equipment for the business along with intangible assets which are

associated with the business. The assets of the business are showing improvements

from previous year’s estimates which is a positive factor for the management of the

company.

In the case of Boral Ltd, the management has made similar presentation of the

assets of the business and portrayed them efficiently as per the integrated reporting

framework. The current assets and non-current assets includes all the similar items and

the same are efficiently presented along with proper disclosures associated with the

same.

Recognition Criteria

The items which are presented in the financial statements have been recognized

following a certain criterion and the same is prescribed by accounting principles and

framework. Fixed assets for both the companies, are measured at cost less

accumulated depreciation and impairment losses. In the similar manner, the intangible

assets also have been recognized after deducting amortization and impairment costs. In

case of certain items such as deferred tax assets and liabilities, estimation and

judgements are used by the management of the company (Barker and Schulte 2017).

The recognition criteria which is followed by both the companies are disclosed in the

draft notes in an appropriate manner.

Conclusion

The above assessment reveals the process of reporting of accounting

Classification of Assets

The assets of the business are appropriately presented in the annual report of

the company and both the companies has systematically presented the assets of the

business in the annual report. The annual report of BHP billion effectively presents the

assets in the form of assets of non-current nature and assets of current nature. The

assets of current nature include trade receivables, cash and inventories of the business

which are the most important items in the balance sheet (Warren, Reeve and Duchac

2013). The non-current assets for the business includes fixed assets such as property

plants and equipment for the business along with intangible assets which are

associated with the business. The assets of the business are showing improvements

from previous year’s estimates which is a positive factor for the management of the

company.

In the case of Boral Ltd, the management has made similar presentation of the

assets of the business and portrayed them efficiently as per the integrated reporting

framework. The current assets and non-current assets includes all the similar items and

the same are efficiently presented along with proper disclosures associated with the

same.

Recognition Criteria

The items which are presented in the financial statements have been recognized

following a certain criterion and the same is prescribed by accounting principles and

framework. Fixed assets for both the companies, are measured at cost less

accumulated depreciation and impairment losses. In the similar manner, the intangible

assets also have been recognized after deducting amortization and impairment costs. In

case of certain items such as deferred tax assets and liabilities, estimation and

judgements are used by the management of the company (Barker and Schulte 2017).

The recognition criteria which is followed by both the companies are disclosed in the

draft notes in an appropriate manner.

Conclusion

The above assessment reveals the process of reporting of accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE ACCOUNTING

information for BHP Billiton Ltd and Boral Ltd for the year 2019. The discussion firsts

covers the types of capital which is used by both the companies and if any changes

have been made to the capital structure of the business considering the nature of

capital. Furthermore, the discussion further reveals the trend for the past three years

and if changes have been made to the capital structure or not. The analysis further

reveals information regarding different assets and liabilities associated with the

business and how the same are presented in the financial statements.

information for BHP Billiton Ltd and Boral Ltd for the year 2019. The discussion firsts

covers the types of capital which is used by both the companies and if any changes

have been made to the capital structure of the business considering the nature of

capital. Furthermore, the discussion further reveals the trend for the past three years

and if changes have been made to the capital structure or not. The analysis further

reveals information regarding different assets and liabilities associated with the

business and how the same are presented in the financial statements.

11CORPORATE ACCOUNTING

Reference

Akeem, L.B., Terer, E.K., Kiyanjui, M.W. and Kayode, A.M., 2014. Effects of capital

structure on firm’s performance: Empirical study of manufacturing companies in

Nigeria. Journal of Finance and Investment analysis, 3(4), pp.39-57.

Baker, M. and Wurgler, J., 2015. Do strict capital requirements raise the cost of capital?

Bank regulation, capital structure, and the low-risk anomaly. American Economic

Review, 105(5), pp.315-20.

Barker, R. and Schulte, S., 2017. Representing the market perspective: Fair value

measurement for non-financial assets. Accounting, Organizations and Society, 56,

pp.55-67.

Bhp.com. (2020). [online] Available at:

https://www.bhp.com/-/media/documents/investors/annual-reports/2019/

bhpannualreport2019.pdf [Accessed 14 Jan. 2020].

Boral.com. (2020). Annual Reports | Boral. [online] Available at:

https://www.boral.com/news/annual-reports [Accessed 14 Jan. 2020].

Christensen, P.O., Flor, C.R., Lando, D. and Miltersen, K.R., 2014. Dynamic capital

structure with callable debt and debt renegotiations. Journal of Corporate Finance, 29,

pp.644-661.

De Villiers, C., Rinaldi, L. and Unerman, J., 2014. Integrated Reporting: Insights, gaps

and an agenda for future research. Accounting, Auditing & Accountability Journal, 27(7),

pp.1042-1067.

Dichev, I.D., 2017. On the conceptual foundations of financial reporting. Accounting and

Business Research, 47(6), pp.617-632.

Duijm, P. and Wierts, P., 2016. The effects of liquidity regulation on bank assets and

liabilities. International Journal of Central Banking (IJCB).

Halling, M., Yu, J. and Zechner, J., 2016. Leverage dynamics over the business

cycle. Journal of Financial Economics, 122(1), pp.21-41.

Kulikova, L.I., Grigoryeva, L.L. and Gubaidullina, A.R., 2014. The interrelation between

the professional judgment of the accountant and the quality of financial

reporting. Mediterranean Journal of Social Sciences, 5(24), p.61.

Kurshev, A. and Strebulaev, I.A., 2015. Firm size and capital structure. Quarterly

Journal of Finance, 5(03), p.1550008

Nnadi, M., 2015. Stock market reaction, financial reporting quality and International

Financial Reporting Standards (IFRS) convergence of listed firms in China. Global

Business and Economics Review, 17(4), pp.399-416.

Sayari, N. and Mugan, F.C.S., 2013. Cash flow statement as an evidence for financial

distress. Universal Journal of Accounting and Finance, 1(3), pp.95-102.

Southern, L.J., 2016. The status of small business growth and entrepreneurial start-up

capital availability during the current extended economic downturn. Problems and

Perspectives in Management, 14(1), pp.8-15.

Warren, C., Reeve, J.M. and Duchac, J., 2013. Financial & managerial accounting.

Cengage Learning.

Reference

Akeem, L.B., Terer, E.K., Kiyanjui, M.W. and Kayode, A.M., 2014. Effects of capital

structure on firm’s performance: Empirical study of manufacturing companies in

Nigeria. Journal of Finance and Investment analysis, 3(4), pp.39-57.

Baker, M. and Wurgler, J., 2015. Do strict capital requirements raise the cost of capital?

Bank regulation, capital structure, and the low-risk anomaly. American Economic

Review, 105(5), pp.315-20.

Barker, R. and Schulte, S., 2017. Representing the market perspective: Fair value

measurement for non-financial assets. Accounting, Organizations and Society, 56,

pp.55-67.

Bhp.com. (2020). [online] Available at:

https://www.bhp.com/-/media/documents/investors/annual-reports/2019/

bhpannualreport2019.pdf [Accessed 14 Jan. 2020].

Boral.com. (2020). Annual Reports | Boral. [online] Available at:

https://www.boral.com/news/annual-reports [Accessed 14 Jan. 2020].

Christensen, P.O., Flor, C.R., Lando, D. and Miltersen, K.R., 2014. Dynamic capital

structure with callable debt and debt renegotiations. Journal of Corporate Finance, 29,

pp.644-661.

De Villiers, C., Rinaldi, L. and Unerman, J., 2014. Integrated Reporting: Insights, gaps

and an agenda for future research. Accounting, Auditing & Accountability Journal, 27(7),

pp.1042-1067.

Dichev, I.D., 2017. On the conceptual foundations of financial reporting. Accounting and

Business Research, 47(6), pp.617-632.

Duijm, P. and Wierts, P., 2016. The effects of liquidity regulation on bank assets and

liabilities. International Journal of Central Banking (IJCB).

Halling, M., Yu, J. and Zechner, J., 2016. Leverage dynamics over the business

cycle. Journal of Financial Economics, 122(1), pp.21-41.

Kulikova, L.I., Grigoryeva, L.L. and Gubaidullina, A.R., 2014. The interrelation between

the professional judgment of the accountant and the quality of financial

reporting. Mediterranean Journal of Social Sciences, 5(24), p.61.

Kurshev, A. and Strebulaev, I.A., 2015. Firm size and capital structure. Quarterly

Journal of Finance, 5(03), p.1550008

Nnadi, M., 2015. Stock market reaction, financial reporting quality and International

Financial Reporting Standards (IFRS) convergence of listed firms in China. Global

Business and Economics Review, 17(4), pp.399-416.

Sayari, N. and Mugan, F.C.S., 2013. Cash flow statement as an evidence for financial

distress. Universal Journal of Accounting and Finance, 1(3), pp.95-102.

Southern, L.J., 2016. The status of small business growth and entrepreneurial start-up

capital availability during the current extended economic downturn. Problems and

Perspectives in Management, 14(1), pp.8-15.

Warren, C., Reeve, J.M. and Duchac, J., 2013. Financial & managerial accounting.

Cengage Learning.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.