Corporate Takeover Decision and Consolidation Accounting Report

VerifiedAdded on 2022/11/13

|13

|3718

|320

Report

AI Summary

This report provides an executive summary and in-depth analysis of corporate and financial accounting principles, specifically focusing on AASB standards and their application to business combinations, intragroup transactions, and non-controlling interests. The report delves into the differences between equity accounting and consolidation accounting, examining the implications of AASB 128 Investments in Associates and AASB 3 Business Combinations. It explains the treatment of intragroup transactions according to AASB 127 Consolidated and Separate Financial Statements and AASB 10 Consolidated Financial Statements, and discusses the influence of disclosure requirements for non-controlling interests. The report includes practical examples, such as the consolidation of financial statements and the calculation of non-controlling interests in subsidiary profits. It also references relevant accounting standards and provides a comprehensive understanding of the key concepts.

Running head: Corporate and Financial Accounting

Corporate and Financial Accounting

Corporate and Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate and Financial Accounting 1

Executive Summary

AASB 101 Preparation of Financial Statements was formed with the aim to make sure that the

financial statements of an entity with regards to the previous periods and with the other

entities should be comparable. They set the requirements for presenting the financial

statements, the framework of their structure and requirements which are minimum for their

content. Whereas AASB 3 Business Combinations was developed for improving the

significance, dependability and comparability of the information furnished by the corporation in

its financial statements with reference to its various business combinations and their impact.

So, this report deliberates upon the issue of various business combinations, non –controlling

interests, intragroup transactions and acquisition methods along with the applicability of

accounting standards on various case studies which are mentioned hereunder.

Executive Summary

AASB 101 Preparation of Financial Statements was formed with the aim to make sure that the

financial statements of an entity with regards to the previous periods and with the other

entities should be comparable. They set the requirements for presenting the financial

statements, the framework of their structure and requirements which are minimum for their

content. Whereas AASB 3 Business Combinations was developed for improving the

significance, dependability and comparability of the information furnished by the corporation in

its financial statements with reference to its various business combinations and their impact.

So, this report deliberates upon the issue of various business combinations, non –controlling

interests, intragroup transactions and acquisition methods along with the applicability of

accounting standards on various case studies which are mentioned hereunder.

Corporate and Financial Accounting 2

Contents

Introduction.................................................................................................................................3

Part A..........................................................................................................................................3

Part B..........................................................................................................................................5

Part C..........................................................................................................................................8

Recommendations/Conclusion.................................................................................................10

References................................................................................................................................11

Contents

Introduction.................................................................................................................................3

Part A..........................................................................................................................................3

Part B..........................................................................................................................................5

Part C..........................................................................................................................................8

Recommendations/Conclusion.................................................................................................10

References................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate and Financial Accounting 3

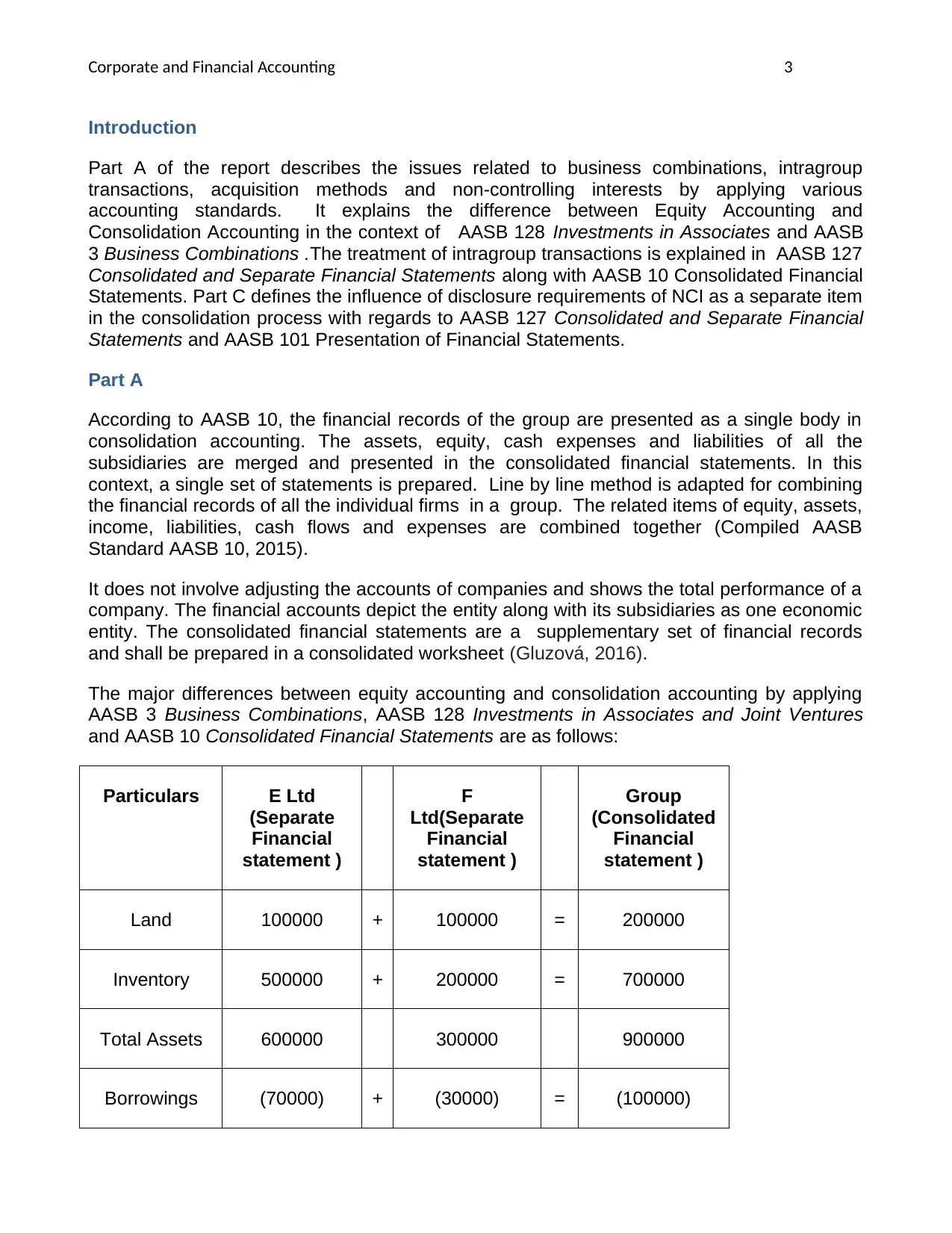

Introduction

Part A of the report describes the issues related to business combinations, intragroup

transactions, acquisition methods and non-controlling interests by applying various

accounting standards. It explains the difference between Equity Accounting and

Consolidation Accounting in the context of AASB 128 Investments in Associates and AASB

3 Business Combinations .The treatment of intragroup transactions is explained in AASB 127

Consolidated and Separate Financial Statements along with AASB 10 Consolidated Financial

Statements. Part C defines the influence of disclosure requirements of NCI as a separate item

in the consolidation process with regards to AASB 127 Consolidated and Separate Financial

Statements and AASB 101 Presentation of Financial Statements.

Part A

According to AASB 10, the financial records of the group are presented as a single body in

consolidation accounting. The assets, equity, cash expenses and liabilities of all the

subsidiaries are merged and presented in the consolidated financial statements. In this

context, a single set of statements is prepared. Line by line method is adapted for combining

the financial records of all the individual firms in a group. The related items of equity, assets,

income, liabilities, cash flows and expenses are combined together (Compiled AASB

Standard AASB 10, 2015).

It does not involve adjusting the accounts of companies and shows the total performance of a

company. The financial accounts depict the entity along with its subsidiaries as one economic

entity. The consolidated financial statements are a supplementary set of financial records

and shall be prepared in a consolidated worksheet (Gluzová, 2016).

The major differences between equity accounting and consolidation accounting by applying

AASB 3 Business Combinations, AASB 128 Investments in Associates and Joint Ventures

and AASB 10 Consolidated Financial Statements are as follows:

Particulars E Ltd

(Separate

Financial

statement )

F

Ltd(Separate

Financial

statement )

Group

(Consolidated

Financial

statement )

Land 100000 + 100000 = 200000

Inventory 500000 + 200000 = 700000

Total Assets 600000 300000 900000

Borrowings (70000) + (30000) = (100000)

Introduction

Part A of the report describes the issues related to business combinations, intragroup

transactions, acquisition methods and non-controlling interests by applying various

accounting standards. It explains the difference between Equity Accounting and

Consolidation Accounting in the context of AASB 128 Investments in Associates and AASB

3 Business Combinations .The treatment of intragroup transactions is explained in AASB 127

Consolidated and Separate Financial Statements along with AASB 10 Consolidated Financial

Statements. Part C defines the influence of disclosure requirements of NCI as a separate item

in the consolidation process with regards to AASB 127 Consolidated and Separate Financial

Statements and AASB 101 Presentation of Financial Statements.

Part A

According to AASB 10, the financial records of the group are presented as a single body in

consolidation accounting. The assets, equity, cash expenses and liabilities of all the

subsidiaries are merged and presented in the consolidated financial statements. In this

context, a single set of statements is prepared. Line by line method is adapted for combining

the financial records of all the individual firms in a group. The related items of equity, assets,

income, liabilities, cash flows and expenses are combined together (Compiled AASB

Standard AASB 10, 2015).

It does not involve adjusting the accounts of companies and shows the total performance of a

company. The financial accounts depict the entity along with its subsidiaries as one economic

entity. The consolidated financial statements are a supplementary set of financial records

and shall be prepared in a consolidated worksheet (Gluzová, 2016).

The major differences between equity accounting and consolidation accounting by applying

AASB 3 Business Combinations, AASB 128 Investments in Associates and Joint Ventures

and AASB 10 Consolidated Financial Statements are as follows:

Particulars E Ltd

(Separate

Financial

statement )

F

Ltd(Separate

Financial

statement )

Group

(Consolidated

Financial

statement )

Land 100000 + 100000 = 200000

Inventory 500000 + 200000 = 700000

Total Assets 600000 300000 900000

Borrowings (70000) + (30000) = (100000)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate and Financial Accounting 4

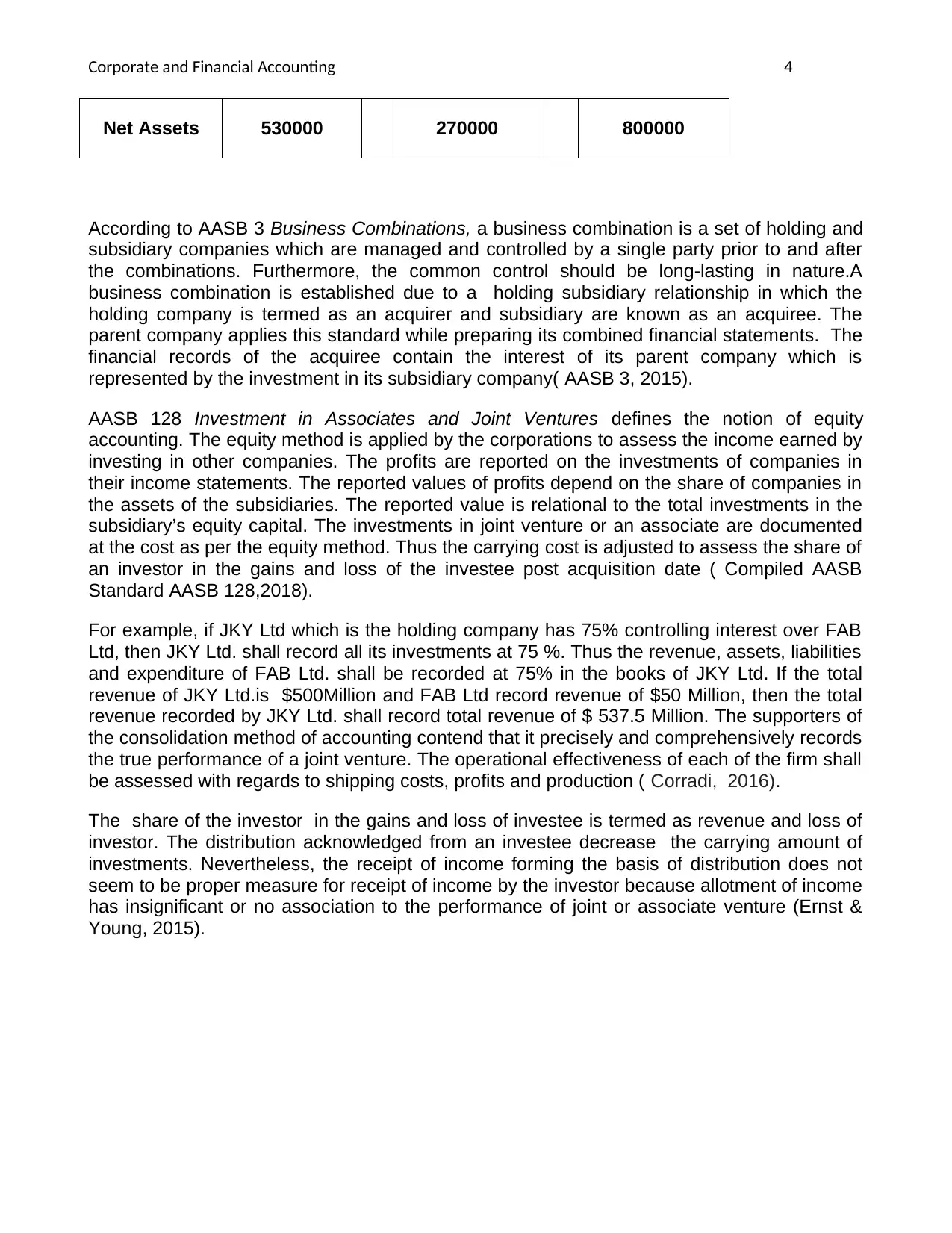

Net Assets 530000 270000 800000

According to AASB 3 Business Combinations, a business combination is a set of holding and

subsidiary companies which are managed and controlled by a single party prior to and after

the combinations. Furthermore, the common control should be long-lasting in nature.A

business combination is established due to a holding subsidiary relationship in which the

holding company is termed as an acquirer and subsidiary are known as an acquiree. The

parent company applies this standard while preparing its combined financial statements. The

financial records of the acquiree contain the interest of its parent company which is

represented by the investment in its subsidiary company( AASB 3, 2015).

AASB 128 Investment in Associates and Joint Ventures defines the notion of equity

accounting. The equity method is applied by the corporations to assess the income earned by

investing in other companies. The profits are reported on the investments of companies in

their income statements. The reported values of profits depend on the share of companies in

the assets of the subsidiaries. The reported value is relational to the total investments in the

subsidiary’s equity capital. The investments in joint venture or an associate are documented

at the cost as per the equity method. Thus the carrying cost is adjusted to assess the share of

an investor in the gains and loss of the investee post acquisition date ( Compiled AASB

Standard AASB 128,2018).

For example, if JKY Ltd which is the holding company has 75% controlling interest over FAB

Ltd, then JKY Ltd. shall record all its investments at 75 %. Thus the revenue, assets, liabilities

and expenditure of FAB Ltd. shall be recorded at 75% in the books of JKY Ltd. If the total

revenue of JKY Ltd.is $500Million and FAB Ltd record revenue of $50 Million, then the total

revenue recorded by JKY Ltd. shall record total revenue of $ 537.5 Million. The supporters of

the consolidation method of accounting contend that it precisely and comprehensively records

the true performance of a joint venture. The operational effectiveness of each of the firm shall

be assessed with regards to shipping costs, profits and production ( Corradi, 2016).

The share of the investor in the gains and loss of investee is termed as revenue and loss of

investor. The distribution acknowledged from an investee decrease the carrying amount of

investments. Nevertheless, the receipt of income forming the basis of distribution does not

seem to be proper measure for receipt of income by the investor because allotment of income

has insignificant or no association to the performance of joint or associate venture (Ernst &

Young, 2015).

Net Assets 530000 270000 800000

According to AASB 3 Business Combinations, a business combination is a set of holding and

subsidiary companies which are managed and controlled by a single party prior to and after

the combinations. Furthermore, the common control should be long-lasting in nature.A

business combination is established due to a holding subsidiary relationship in which the

holding company is termed as an acquirer and subsidiary are known as an acquiree. The

parent company applies this standard while preparing its combined financial statements. The

financial records of the acquiree contain the interest of its parent company which is

represented by the investment in its subsidiary company( AASB 3, 2015).

AASB 128 Investment in Associates and Joint Ventures defines the notion of equity

accounting. The equity method is applied by the corporations to assess the income earned by

investing in other companies. The profits are reported on the investments of companies in

their income statements. The reported values of profits depend on the share of companies in

the assets of the subsidiaries. The reported value is relational to the total investments in the

subsidiary’s equity capital. The investments in joint venture or an associate are documented

at the cost as per the equity method. Thus the carrying cost is adjusted to assess the share of

an investor in the gains and loss of the investee post acquisition date ( Compiled AASB

Standard AASB 128,2018).

For example, if JKY Ltd which is the holding company has 75% controlling interest over FAB

Ltd, then JKY Ltd. shall record all its investments at 75 %. Thus the revenue, assets, liabilities

and expenditure of FAB Ltd. shall be recorded at 75% in the books of JKY Ltd. If the total

revenue of JKY Ltd.is $500Million and FAB Ltd record revenue of $50 Million, then the total

revenue recorded by JKY Ltd. shall record total revenue of $ 537.5 Million. The supporters of

the consolidation method of accounting contend that it precisely and comprehensively records

the true performance of a joint venture. The operational effectiveness of each of the firm shall

be assessed with regards to shipping costs, profits and production ( Corradi, 2016).

The share of the investor in the gains and loss of investee is termed as revenue and loss of

investor. The distribution acknowledged from an investee decrease the carrying amount of

investments. Nevertheless, the receipt of income forming the basis of distribution does not

seem to be proper measure for receipt of income by the investor because allotment of income

has insignificant or no association to the performance of joint or associate venture (Ernst &

Young, 2015).

Corporate and Financial Accounting 5

Part B

According to AASB 127 Consolidated and Separate Financial Statements, the intragroup

balances and transactions including expenses, dividends and income should be fully

eliminated.The losses occurring in intragroup transactions might connote an impairment

which is required to be stated in the combined financial statements. Thus the profit and losses

occurring due to the intragroup transactions arising due to the transfer of assets should be

eliminated in full. In case the financial records of the subsidiaries are prepared on a date

which is different from that of the financial records of holding company, then the important

transactions arising between the two dates shall be adjusted accordingly (AASB 127, 2015).

Thus the gap between the ending of two reporting periods shall not be more than 3 months.

The reporting periods and the gap between the two shall be the same for all time frames.

The consolidated financial reports shall be made by using similar accounting policies for the

similar dealings happening during the same period. The profits and losses of all the

subordinate companies shall be assimilated in the combined financial reports from the

acquisition date as discussed in AASB 3 (Compiled AASB Standard AASB 3, 2015).

Thus the assessment of revenues and losses shall be obtained from the liabilities and assets

stated in combined financial reports of the holding company as on the acquisition date. For

example, the depreciation expenses incurred on the assets post acquisition date shall be

obtained from the fair value of assets in the combined financial statements as on the

acquisition date. In this case, the gains and losses along with other components of income

shall be related to the non-controlling interests and parent entity.

The non-controlling interests pertain to the interest of minority with a position of equity

ownership in a subordinate company not related to the holding company. The holding

company should have a controlling interest of greater than 50% but lower than 100%.

Consequent to this, financial records of both the companies are combined together in the

form of combined financial statements. According to AASB 10 Consolidated Financial

Statements, the non-controlling interests of the holding company are shown in the combined

financial statements by the subsidiary corporation. So, as discussed in this case ,if the

partially owned subsidiary is providing professional services and transfers inventory at a

profit to the holding company , then it should be treated in a same way as the parent

company treats any other dealing in its routine course of business at an arm’s length

price( Casajus and Labrenz, 2017).

The key principle elucidating the way in which intragroup transactions should be treated can

be explained with the help of an example. 50% ownership of the subordinate company is held

by the parent entity and $50000 has been reported as an annual profit by the subordinate

company including the profits obtained from transferring of inventory and provision of

professional services to the holding company. The holding company JKY Ltd. shall debit

$25000(50% of $50000) as Intercorporate Investment and credit the Investment revenue for $

25000. This transaction should be recognized in advance in order to prepare the combined

financial statements.

These may include the sale of assets and providing services apart from sale transactions,

accounts payable and receivable arising between the subsidiary and holding company. In the

case of sale of assets to the parent company and retained earnings which are identified are to

Part B

According to AASB 127 Consolidated and Separate Financial Statements, the intragroup

balances and transactions including expenses, dividends and income should be fully

eliminated.The losses occurring in intragroup transactions might connote an impairment

which is required to be stated in the combined financial statements. Thus the profit and losses

occurring due to the intragroup transactions arising due to the transfer of assets should be

eliminated in full. In case the financial records of the subsidiaries are prepared on a date

which is different from that of the financial records of holding company, then the important

transactions arising between the two dates shall be adjusted accordingly (AASB 127, 2015).

Thus the gap between the ending of two reporting periods shall not be more than 3 months.

The reporting periods and the gap between the two shall be the same for all time frames.

The consolidated financial reports shall be made by using similar accounting policies for the

similar dealings happening during the same period. The profits and losses of all the

subordinate companies shall be assimilated in the combined financial reports from the

acquisition date as discussed in AASB 3 (Compiled AASB Standard AASB 3, 2015).

Thus the assessment of revenues and losses shall be obtained from the liabilities and assets

stated in combined financial reports of the holding company as on the acquisition date. For

example, the depreciation expenses incurred on the assets post acquisition date shall be

obtained from the fair value of assets in the combined financial statements as on the

acquisition date. In this case, the gains and losses along with other components of income

shall be related to the non-controlling interests and parent entity.

The non-controlling interests pertain to the interest of minority with a position of equity

ownership in a subordinate company not related to the holding company. The holding

company should have a controlling interest of greater than 50% but lower than 100%.

Consequent to this, financial records of both the companies are combined together in the

form of combined financial statements. According to AASB 10 Consolidated Financial

Statements, the non-controlling interests of the holding company are shown in the combined

financial statements by the subsidiary corporation. So, as discussed in this case ,if the

partially owned subsidiary is providing professional services and transfers inventory at a

profit to the holding company , then it should be treated in a same way as the parent

company treats any other dealing in its routine course of business at an arm’s length

price( Casajus and Labrenz, 2017).

The key principle elucidating the way in which intragroup transactions should be treated can

be explained with the help of an example. 50% ownership of the subordinate company is held

by the parent entity and $50000 has been reported as an annual profit by the subordinate

company including the profits obtained from transferring of inventory and provision of

professional services to the holding company. The holding company JKY Ltd. shall debit

$25000(50% of $50000) as Intercorporate Investment and credit the Investment revenue for $

25000. This transaction should be recognized in advance in order to prepare the combined

financial statements.

These may include the sale of assets and providing services apart from sale transactions,

accounts payable and receivable arising between the subsidiary and holding company. In the

case of sale of assets to the parent company and retained earnings which are identified are to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate and Financial Accounting 6

be debited and consolidated inventory at the closing date shall be credited. It should be

associated with the value of transfers. If the value of the stock is $40000 and it was

transferred from parent to subsidiary company, then the statements shall record debt of

$40000 to retained earnings and $40000 to consolidated stock (Gardini and Grossi, 2014).

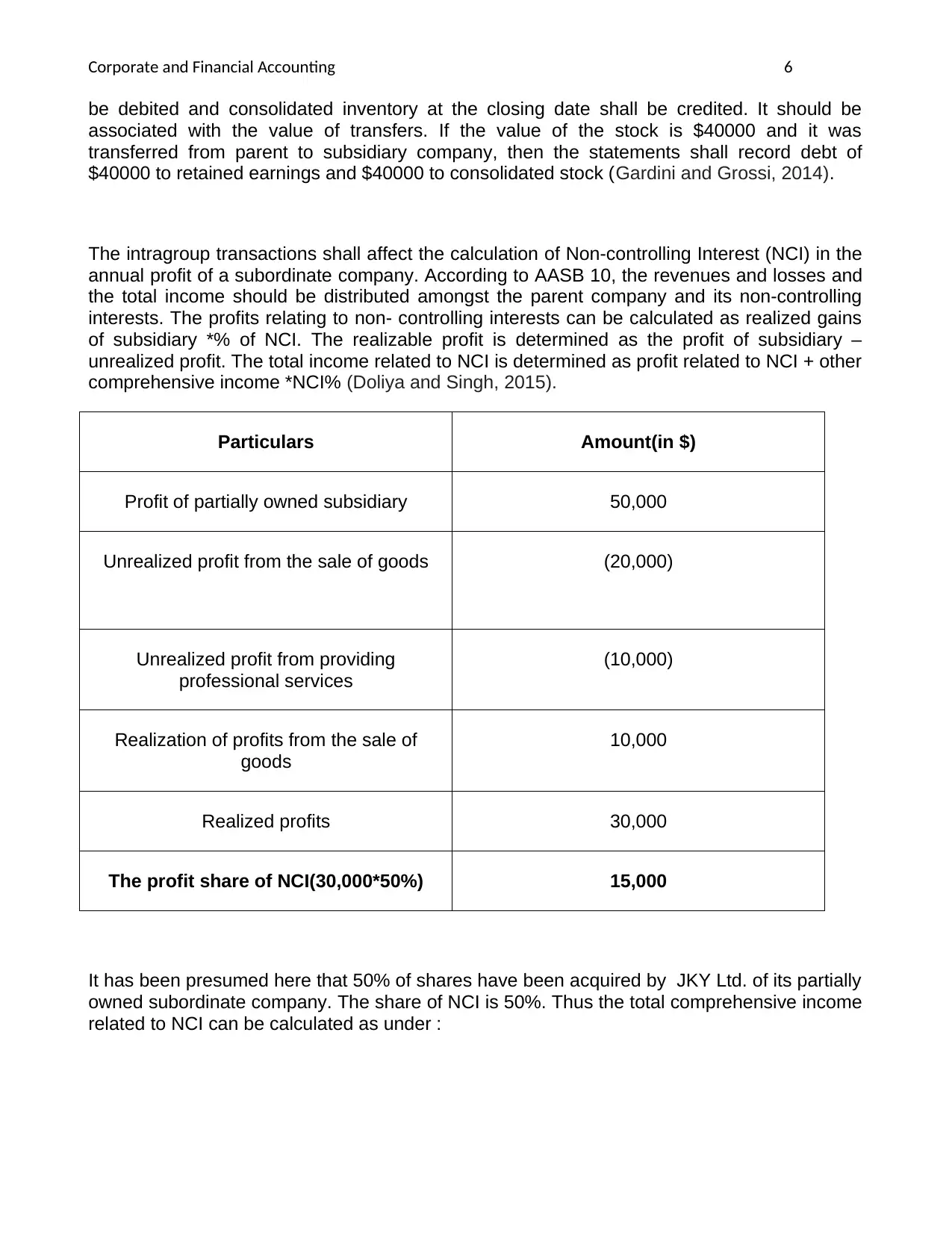

The intragroup transactions shall affect the calculation of Non-controlling Interest (NCI) in the

annual profit of a subordinate company. According to AASB 10, the revenues and losses and

the total income should be distributed amongst the parent company and its non-controlling

interests. The profits relating to non- controlling interests can be calculated as realized gains

of subsidiary *% of NCI. The realizable profit is determined as the profit of subsidiary –

unrealized profit. The total income related to NCI is determined as profit related to NCI + other

comprehensive income *NCI% (Doliya and Singh, 2015).

Particulars Amount(in $)

Profit of partially owned subsidiary 50,000

Unrealized profit from the sale of goods (20,000)

Unrealized profit from providing

professional services

(10,000)

Realization of profits from the sale of

goods

10,000

Realized profits 30,000

The profit share of NCI(30,000*50%) 15,000

It has been presumed here that 50% of shares have been acquired by JKY Ltd. of its partially

owned subordinate company. The share of NCI is 50%. Thus the total comprehensive income

related to NCI can be calculated as under :

be debited and consolidated inventory at the closing date shall be credited. It should be

associated with the value of transfers. If the value of the stock is $40000 and it was

transferred from parent to subsidiary company, then the statements shall record debt of

$40000 to retained earnings and $40000 to consolidated stock (Gardini and Grossi, 2014).

The intragroup transactions shall affect the calculation of Non-controlling Interest (NCI) in the

annual profit of a subordinate company. According to AASB 10, the revenues and losses and

the total income should be distributed amongst the parent company and its non-controlling

interests. The profits relating to non- controlling interests can be calculated as realized gains

of subsidiary *% of NCI. The realizable profit is determined as the profit of subsidiary –

unrealized profit. The total income related to NCI is determined as profit related to NCI + other

comprehensive income *NCI% (Doliya and Singh, 2015).

Particulars Amount(in $)

Profit of partially owned subsidiary 50,000

Unrealized profit from the sale of goods (20,000)

Unrealized profit from providing

professional services

(10,000)

Realization of profits from the sale of

goods

10,000

Realized profits 30,000

The profit share of NCI(30,000*50%) 15,000

It has been presumed here that 50% of shares have been acquired by JKY Ltd. of its partially

owned subordinate company. The share of NCI is 50%. Thus the total comprehensive income

related to NCI can be calculated as under :

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate and Financial Accounting 7

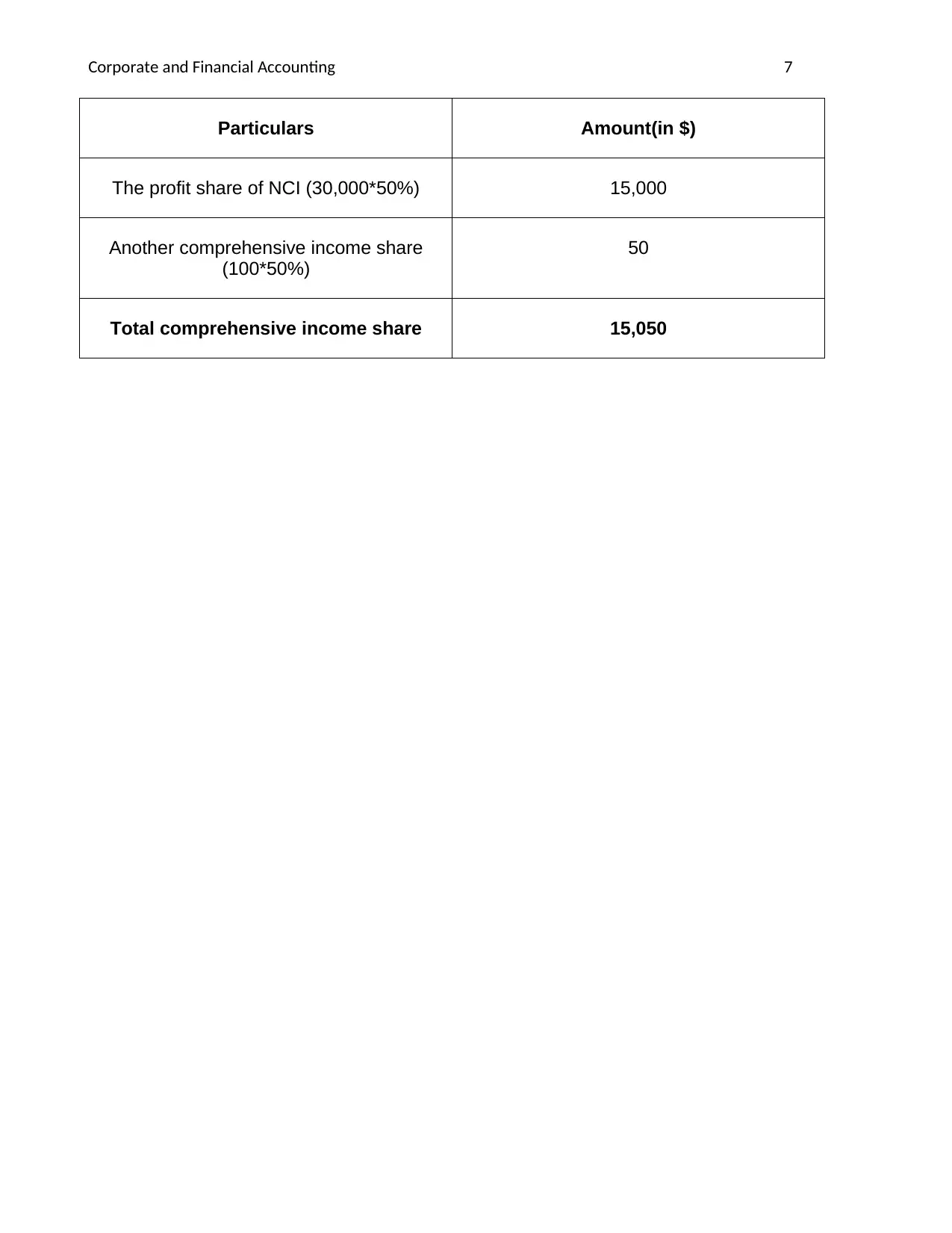

Particulars Amount(in $)

The profit share of NCI (30,000*50%) 15,000

Another comprehensive income share

(100*50%)

50

Total comprehensive income share 15,050

Particulars Amount(in $)

The profit share of NCI (30,000*50%) 15,000

Another comprehensive income share

(100*50%)

50

Total comprehensive income share 15,050

Corporate and Financial Accounting 8

Part C

According to AASB 127 Consolidated and Separate Financial Statements and AASB 101

Presentation of Financial Statements, substantial NCI of each and every subordinate

company shall be disclosed by the holding company in the consolidation process. The

requirements of disclosure shall be met by the holding company by illustrating the

disaggregated information from the monetary worth encompassed in the consolidated

financial statements of the holding company. The process shall also be executed with regards

to subordinate companies having a substantial NCI to the holding company. The reporting

company shall apply its discretion for determining the worth of disaggregated data in case the

holding company furnishing the data about the subordinate company has a material

controlling interest (Compiled AASB Standard AASB 101,2017).

In the context of requirements of disclosure of NCI as a separate item in the consolidation

process, the substantiality shall be assessed by the holding company in the consolidated

financial reports. The holding company shall consider both the quantitative aspects and the

qualitative aspect of the subsidiary. The qualitative aspect shall pertain to the nature of the

subsidiary and the qualitative aspect is related to the size of the subordinate

company.According to the disclosure requirement, the holding company shall present the

information which can help stakeholders to know more about the commercial activities

conducted by the group. It should also help them to understand the stake held by the non-

controlling interests in the transactions of the group apart from its cash flows(Compiled AASB

Standard AASB 101, 2015b).

The required information is stated on the basis of the nature of the subsidiary. Moreover, in

order to meet the requirements of disclosure, the information about the subsidiaries should be

segregated. It should be presented regarding the subsidiaries having a substantial non-

controlling interest in the group. The parent entity shall present the summarized balance

sheet with other financial reports about the liabilities, assets, cash flows and profits of the

subordinate companies which are having a non-controlling interest in the commercial

activities of the group apart from the cash flows ( Lemus, 2016).

The holding company shall classify and assess the profits in the consolidated financial

records on the basis of their economic materiality. The profits earned should be categorized

as non-controlling interests in the financial records of the holding company. If the revenues

earned are not of material nature, then they would not be categorized as non-controlling

interests. In such cases, the holding company shall classify the comprehensive profit as a

profit-sharing system rather than a non-controlling interest. In the context of asset valuation,

AASB 101 Presentation of Financial Statements suggests that the entity shall evaluate the fair

value of liabilities and assets according to AASB 13 Fair Value Measurement (Ernst &

Young, 2018).

The fair value measurement assesses the capability of participants of using their assets in the

best possible way in the market. In case any asset is recategorized from the class of

amortized cost measurement, then, in that case, it is analyzed at the fair value through

revenues and losses and any incurred profits arising due to the differences between the

previous amortized costs to the financial assets and their fair values. They should be

recorded at the values prevalent at the reclassification date. The assets of the subordinate

Part C

According to AASB 127 Consolidated and Separate Financial Statements and AASB 101

Presentation of Financial Statements, substantial NCI of each and every subordinate

company shall be disclosed by the holding company in the consolidation process. The

requirements of disclosure shall be met by the holding company by illustrating the

disaggregated information from the monetary worth encompassed in the consolidated

financial statements of the holding company. The process shall also be executed with regards

to subordinate companies having a substantial NCI to the holding company. The reporting

company shall apply its discretion for determining the worth of disaggregated data in case the

holding company furnishing the data about the subordinate company has a material

controlling interest (Compiled AASB Standard AASB 101,2017).

In the context of requirements of disclosure of NCI as a separate item in the consolidation

process, the substantiality shall be assessed by the holding company in the consolidated

financial reports. The holding company shall consider both the quantitative aspects and the

qualitative aspect of the subsidiary. The qualitative aspect shall pertain to the nature of the

subsidiary and the qualitative aspect is related to the size of the subordinate

company.According to the disclosure requirement, the holding company shall present the

information which can help stakeholders to know more about the commercial activities

conducted by the group. It should also help them to understand the stake held by the non-

controlling interests in the transactions of the group apart from its cash flows(Compiled AASB

Standard AASB 101, 2015b).

The required information is stated on the basis of the nature of the subsidiary. Moreover, in

order to meet the requirements of disclosure, the information about the subsidiaries should be

segregated. It should be presented regarding the subsidiaries having a substantial non-

controlling interest in the group. The parent entity shall present the summarized balance

sheet with other financial reports about the liabilities, assets, cash flows and profits of the

subordinate companies which are having a non-controlling interest in the commercial

activities of the group apart from the cash flows ( Lemus, 2016).

The holding company shall classify and assess the profits in the consolidated financial

records on the basis of their economic materiality. The profits earned should be categorized

as non-controlling interests in the financial records of the holding company. If the revenues

earned are not of material nature, then they would not be categorized as non-controlling

interests. In such cases, the holding company shall classify the comprehensive profit as a

profit-sharing system rather than a non-controlling interest. In the context of asset valuation,

AASB 101 Presentation of Financial Statements suggests that the entity shall evaluate the fair

value of liabilities and assets according to AASB 13 Fair Value Measurement (Ernst &

Young, 2018).

The fair value measurement assesses the capability of participants of using their assets in the

best possible way in the market. In case any asset is recategorized from the class of

amortized cost measurement, then, in that case, it is analyzed at the fair value through

revenues and losses and any incurred profits arising due to the differences between the

previous amortized costs to the financial assets and their fair values. They should be

recorded at the values prevalent at the reclassification date. The assets of the subordinate

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate and Financial Accounting 9

company shall be recorded at the fair values in the consolidated financial statements (Cîrstea,

Nistor and Tiron Tudor, 2017).

AASB 127 Consolidated and Separate Financial Statements suggest that NCI shall be

mentioned as a distinct item to the owner’s equity and other comprehensive income should be

apportioned to NCI. The categorization of non-controlling interests as equity capital can affect

the criteria of financial performance apart from the equity of the entire group. In this context,

the other comprehensive income shall include the profits and gains which are excluded from

the net profits according to the income statement. The earnings and gains encompassed in

the other comprehensive profits are associated with the unrealized income.

The capital of the group shall be allocated according to the interest held by the holding

company and its shareholders apart from the non-controlling interests. The apportionment of

the equity capital of subordinate companies shall be related to the apportionment of the total

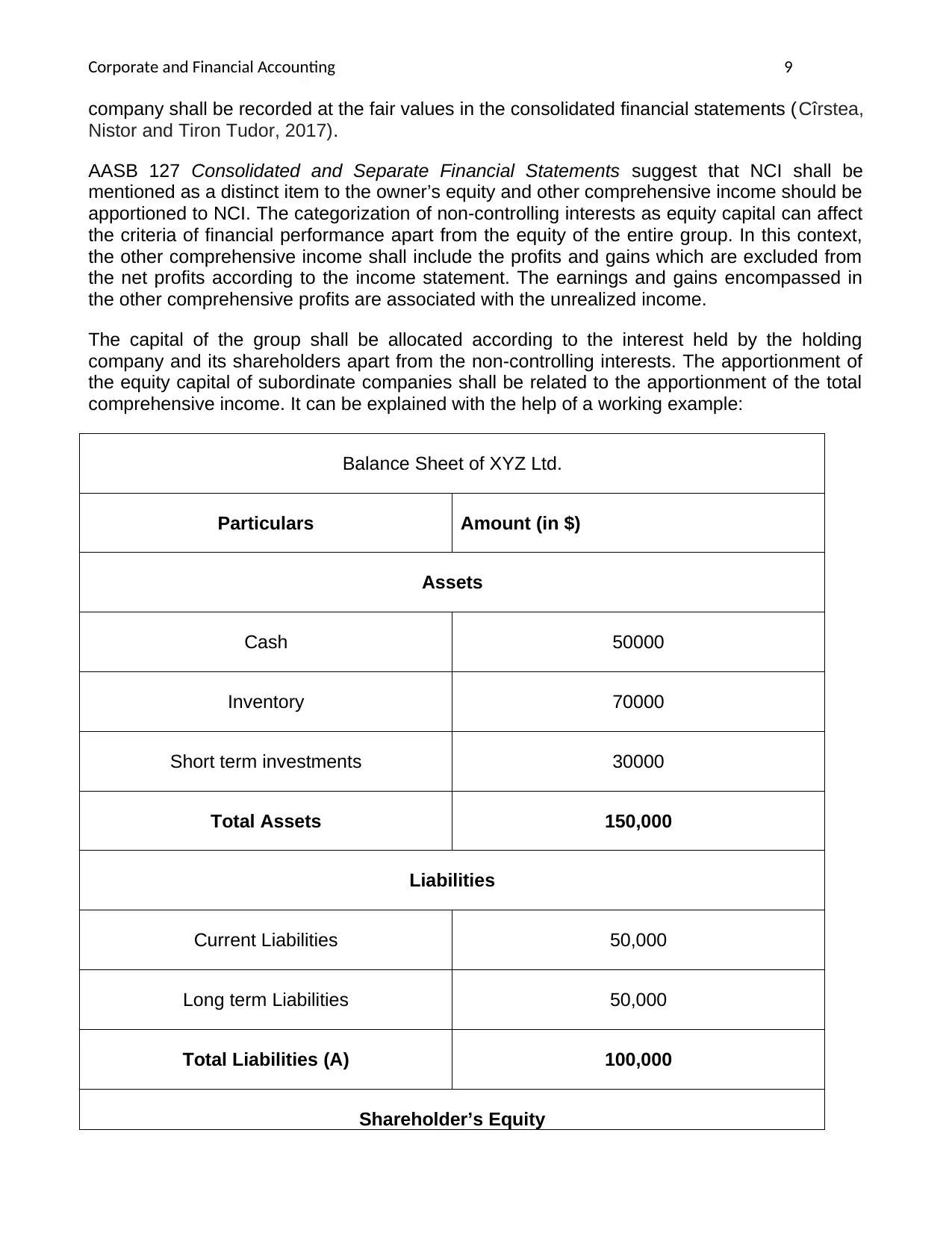

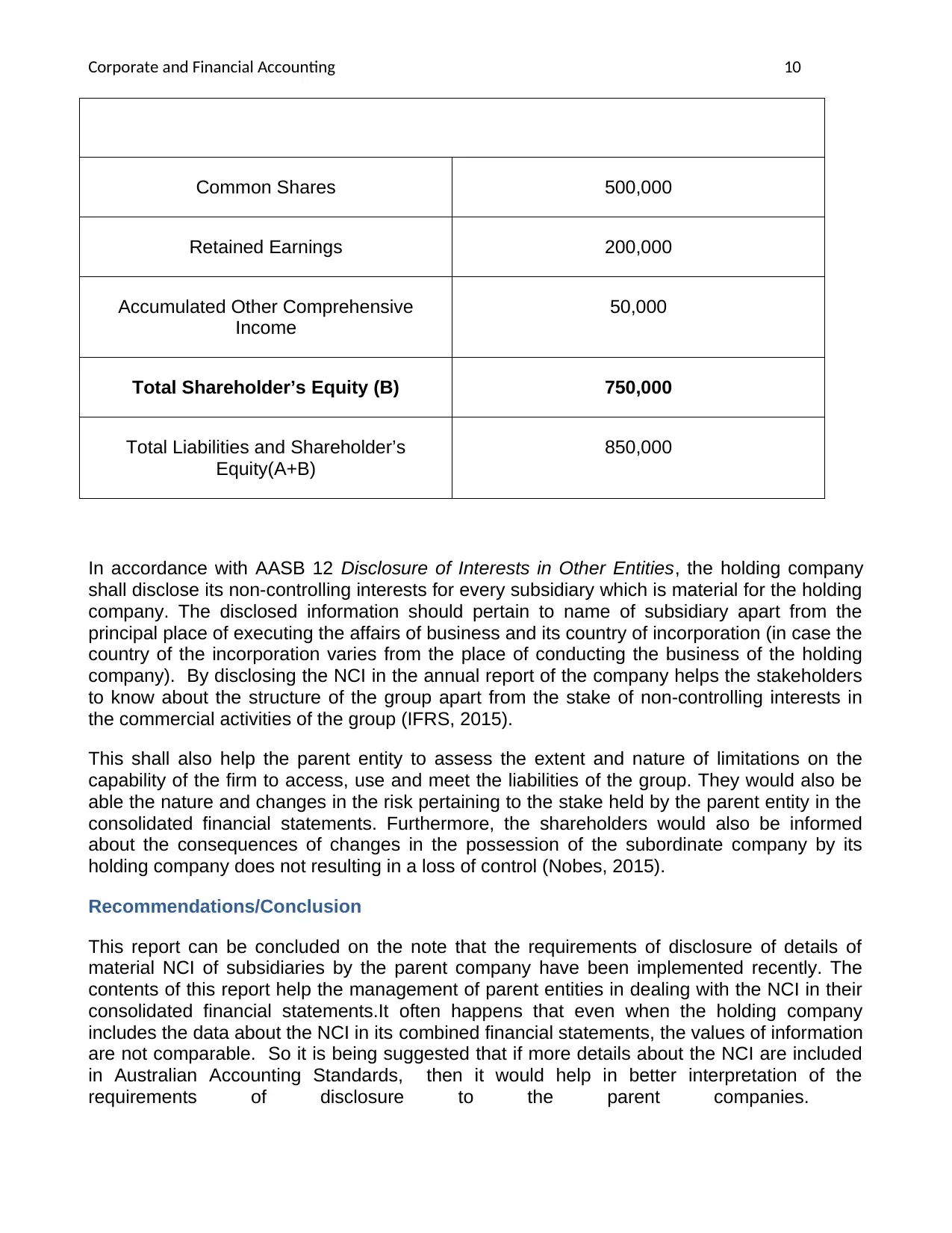

comprehensive income. It can be explained with the help of a working example:

Balance Sheet of XYZ Ltd.

Particulars Amount (in $)

Assets

Cash 50000

Inventory 70000

Short term investments 30000

Total Assets 150,000

Liabilities

Current Liabilities 50,000

Long term Liabilities 50,000

Total Liabilities (A) 100,000

Shareholder’s Equity

company shall be recorded at the fair values in the consolidated financial statements (Cîrstea,

Nistor and Tiron Tudor, 2017).

AASB 127 Consolidated and Separate Financial Statements suggest that NCI shall be

mentioned as a distinct item to the owner’s equity and other comprehensive income should be

apportioned to NCI. The categorization of non-controlling interests as equity capital can affect

the criteria of financial performance apart from the equity of the entire group. In this context,

the other comprehensive income shall include the profits and gains which are excluded from

the net profits according to the income statement. The earnings and gains encompassed in

the other comprehensive profits are associated with the unrealized income.

The capital of the group shall be allocated according to the interest held by the holding

company and its shareholders apart from the non-controlling interests. The apportionment of

the equity capital of subordinate companies shall be related to the apportionment of the total

comprehensive income. It can be explained with the help of a working example:

Balance Sheet of XYZ Ltd.

Particulars Amount (in $)

Assets

Cash 50000

Inventory 70000

Short term investments 30000

Total Assets 150,000

Liabilities

Current Liabilities 50,000

Long term Liabilities 50,000

Total Liabilities (A) 100,000

Shareholder’s Equity

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate and Financial Accounting 10

Common Shares 500,000

Retained Earnings 200,000

Accumulated Other Comprehensive

Income

50,000

Total Shareholder’s Equity (B) 750,000

Total Liabilities and Shareholder’s

Equity(A+B)

850,000

In accordance with AASB 12 Disclosure of Interests in Other Entities, the holding company

shall disclose its non-controlling interests for every subsidiary which is material for the holding

company. The disclosed information should pertain to name of subsidiary apart from the

principal place of executing the affairs of business and its country of incorporation (in case the

country of the incorporation varies from the place of conducting the business of the holding

company). By disclosing the NCI in the annual report of the company helps the stakeholders

to know about the structure of the group apart from the stake of non-controlling interests in

the commercial activities of the group (IFRS, 2015).

This shall also help the parent entity to assess the extent and nature of limitations on the

capability of the firm to access, use and meet the liabilities of the group. They would also be

able the nature and changes in the risk pertaining to the stake held by the parent entity in the

consolidated financial statements. Furthermore, the shareholders would also be informed

about the consequences of changes in the possession of the subordinate company by its

holding company does not resulting in a loss of control (Nobes, 2015).

Recommendations/Conclusion

This report can be concluded on the note that the requirements of disclosure of details of

material NCI of subsidiaries by the parent company have been implemented recently. The

contents of this report help the management of parent entities in dealing with the NCI in their

consolidated financial statements.It often happens that even when the holding company

includes the data about the NCI in its combined financial statements, the values of information

are not comparable. So it is being suggested that if more details about the NCI are included

in Australian Accounting Standards, then it would help in better interpretation of the

requirements of disclosure to the parent companies.

Common Shares 500,000

Retained Earnings 200,000

Accumulated Other Comprehensive

Income

50,000

Total Shareholder’s Equity (B) 750,000

Total Liabilities and Shareholder’s

Equity(A+B)

850,000

In accordance with AASB 12 Disclosure of Interests in Other Entities, the holding company

shall disclose its non-controlling interests for every subsidiary which is material for the holding

company. The disclosed information should pertain to name of subsidiary apart from the

principal place of executing the affairs of business and its country of incorporation (in case the

country of the incorporation varies from the place of conducting the business of the holding

company). By disclosing the NCI in the annual report of the company helps the stakeholders

to know about the structure of the group apart from the stake of non-controlling interests in

the commercial activities of the group (IFRS, 2015).

This shall also help the parent entity to assess the extent and nature of limitations on the

capability of the firm to access, use and meet the liabilities of the group. They would also be

able the nature and changes in the risk pertaining to the stake held by the parent entity in the

consolidated financial statements. Furthermore, the shareholders would also be informed

about the consequences of changes in the possession of the subordinate company by its

holding company does not resulting in a loss of control (Nobes, 2015).

Recommendations/Conclusion

This report can be concluded on the note that the requirements of disclosure of details of

material NCI of subsidiaries by the parent company have been implemented recently. The

contents of this report help the management of parent entities in dealing with the NCI in their

consolidated financial statements.It often happens that even when the holding company

includes the data about the NCI in its combined financial statements, the values of information

are not comparable. So it is being suggested that if more details about the NCI are included

in Australian Accounting Standards, then it would help in better interpretation of the

requirements of disclosure to the parent companies.

Corporate and Financial Accounting 11

References

AASB 127(2015) Separate Financial Statements [online]. Available from:

https://jade.io/article/500101?at.hl=aasb+127 [Accessed 28th May 2019].

AASB 3(2015) Business Combinations [online]. Available from: https://jade.io/j/?

a=outline&id=500098 [Accessed 28th May 2019].

Casajus, A. and Labrenz, H.(2017) Recognition of Non-Controlling Interest in Consolidated

Financial Statements Based on Property Rights. Review of Law & Economics, 13(3),pp.1-23.

Cîrstea, A., Nistor, C.S. and Tiron Tudor, A.( 2017) Consolidated financial statements–a new

challenge for the public sector administration. Journal of Economic and Administrative

Sciences. 33(1), pp.46-65.

Compiled AASB Standard AASB 10 (2015) Consolidated Financial Statements[online].

Available from: https://jade.io/j/?a=outline&id=584708 [Accessed 28th May 2019].

Compiled AASB Standard AASB 101(2015) Consolidated Financial Statements[online].

Available from: https://jade.io/j/?a=outline&id=503698 [Accessed 28th May 2019].

Compiled AASB Standard AASB 101(2017) Presentation of Financial Statements [online].

Available from: https://jade.io/article/588436 [Accessed 28th May 2019].

Compiled AASB Standard AASB 128(2018) Investments in Associates and Joint

Ventures[online]. Available from:

https://www.aasb.gov.au/admin/file/content105/c9/AASB128_08-15_NFP_COMPdec17_01-

18.pdf [Accessed 28th May 2019].

Compiled AASB Standard AASB 3 (2015) Business Combinations [online]. Available from:

https://www.aasb.gov.au/admin/file/content105/c9/AASB3_03-08_COMPjan15_01-16.pdf

[Accessed 28th May 2019].

Corradi, M.C.( 2016) Bridging the Gap in the Shifting Sands of Non-controlling Financial

Holdings?. World Competition. 39(2), pp.239-265.

Doliya, P. and Singh, J.P.( 2015) On the Implications of Fair Value Based Merger

Accounting. Procedia-Social and Behavioral Sciences. 189(2015), pp.356-361.

Ernst & Young (2015) Consolidated and other financial statements[online]. Available from:

https://www.ey.com/Publication/vwLUAssets/FinancialReportingDevelopments_BB1577_Con

solidatedFinancialStatements_8December2015/$FILE/

FinancialReportingDevelopments_BB1577_ConsolidatedFinancialStatements_8December20

15.pdf [Accessed 28th May 2019].

References

AASB 127(2015) Separate Financial Statements [online]. Available from:

https://jade.io/article/500101?at.hl=aasb+127 [Accessed 28th May 2019].

AASB 3(2015) Business Combinations [online]. Available from: https://jade.io/j/?

a=outline&id=500098 [Accessed 28th May 2019].

Casajus, A. and Labrenz, H.(2017) Recognition of Non-Controlling Interest in Consolidated

Financial Statements Based on Property Rights. Review of Law & Economics, 13(3),pp.1-23.

Cîrstea, A., Nistor, C.S. and Tiron Tudor, A.( 2017) Consolidated financial statements–a new

challenge for the public sector administration. Journal of Economic and Administrative

Sciences. 33(1), pp.46-65.

Compiled AASB Standard AASB 10 (2015) Consolidated Financial Statements[online].

Available from: https://jade.io/j/?a=outline&id=584708 [Accessed 28th May 2019].

Compiled AASB Standard AASB 101(2015) Consolidated Financial Statements[online].

Available from: https://jade.io/j/?a=outline&id=503698 [Accessed 28th May 2019].

Compiled AASB Standard AASB 101(2017) Presentation of Financial Statements [online].

Available from: https://jade.io/article/588436 [Accessed 28th May 2019].

Compiled AASB Standard AASB 128(2018) Investments in Associates and Joint

Ventures[online]. Available from:

https://www.aasb.gov.au/admin/file/content105/c9/AASB128_08-15_NFP_COMPdec17_01-

18.pdf [Accessed 28th May 2019].

Compiled AASB Standard AASB 3 (2015) Business Combinations [online]. Available from:

https://www.aasb.gov.au/admin/file/content105/c9/AASB3_03-08_COMPjan15_01-16.pdf

[Accessed 28th May 2019].

Corradi, M.C.( 2016) Bridging the Gap in the Shifting Sands of Non-controlling Financial

Holdings?. World Competition. 39(2), pp.239-265.

Doliya, P. and Singh, J.P.( 2015) On the Implications of Fair Value Based Merger

Accounting. Procedia-Social and Behavioral Sciences. 189(2015), pp.356-361.

Ernst & Young (2015) Consolidated and other financial statements[online]. Available from:

https://www.ey.com/Publication/vwLUAssets/FinancialReportingDevelopments_BB1577_Con

solidatedFinancialStatements_8December2015/$FILE/

FinancialReportingDevelopments_BB1577_ConsolidatedFinancialStatements_8December20

15.pdf [Accessed 28th May 2019].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.