Corporate Accounting Report: Funds Sourcing, Liabilities, and AASB 137

VerifiedAdded on 2022/08/23

|22

|4302

|17

Report

AI Summary

This report provides a detailed analysis of corporate accounting practices, focusing on the funds sourcing strategies of Boral Limited and Brickworks Limited, both operating in the materials sector. The study explores the internal and external sources of funds, including equity, retained earnings, loans, borrowings, and trade credit, evaluating their respective advantages and disadvantages. It examines the changes in these funding sources over a three-year period, supported by financial data. Furthermore, the report assesses the application of AASB 137, provisions, contingent liabilities, and contingent assets, to these companies. The analysis extends to the classification of assets and liabilities, specifically highlighting interest-bearing liabilities. The report also delves into the measurement basis for different asset types reported in the financial statements, offering a comprehensive overview of corporate financial management.

Running head: CORPORATE ACCOUNTING

Corporate accounting

Name of the Student

Name of the University

Author Note

Corporate accounting

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING

Abstract:

The paper aims to develop an understanding of the various sources of the funds which the

company used for financing its business activities. Chosen company for analysis is from

material sector which comprise of Boral Limited and Brickwork limited. Discussion has been

done by identifying the sources of funds and its relative advantages and shortcomings. The

summary of the key concepts of the standard AASB 137 “AASB 137 provisions, contingent

liabilities and contingent assets” has been done and the compliance of the chosen companies

with the requirement of the standard has been assessed. The last section of report elaborates

the measurement basis for the different types of assets reported in the financial report of the

companies.

Abstract:

The paper aims to develop an understanding of the various sources of the funds which the

company used for financing its business activities. Chosen company for analysis is from

material sector which comprise of Boral Limited and Brickwork limited. Discussion has been

done by identifying the sources of funds and its relative advantages and shortcomings. The

summary of the key concepts of the standard AASB 137 “AASB 137 provisions, contingent

liabilities and contingent assets” has been done and the compliance of the chosen companies

with the requirement of the standard has been assessed. The last section of report elaborates

the measurement basis for the different types of assets reported in the financial report of the

companies.

CORPORATE ACCOUNTING

Table of Contents

Introduction:...............................................................................................................................4

Discussion:.................................................................................................................................4

Answer to question i).................................................................................................................4

Answer to question ii)................................................................................................................5

Answer to question iii)...............................................................................................................6

Answer to question iv)...............................................................................................................7

Answer to question v)..............................................................................................................10

Answer to question vi).............................................................................................................11

Answer to question vii)............................................................................................................11

Answer to question viii)...........................................................................................................12

Answer to question ix).............................................................................................................13

Conclusion:..............................................................................................................................14

References list:.........................................................................................................................15

Table of Contents

Introduction:...............................................................................................................................4

Discussion:.................................................................................................................................4

Answer to question i).................................................................................................................4

Answer to question ii)................................................................................................................5

Answer to question iii)...............................................................................................................6

Answer to question iv)...............................................................................................................7

Answer to question v)..............................................................................................................10

Answer to question vi).............................................................................................................11

Answer to question vii)............................................................................................................11

Answer to question viii)...........................................................................................................12

Answer to question ix).............................................................................................................13

Conclusion:..............................................................................................................................14

References list:.........................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE ACCOUNTING

Introduction:

The paper discusses about the various sources of funds used by the organizations by

identifying the relative advantages and drawbacks of the funding used. In this regard, the

chosen companies for evaluating the various funding sources used to raise the funds are Boral

Limited and Brickworks limited operating in material sector. Discussion also incorporates the

assessment of concepts of the standard “AASB 137 provisions, contingent liabilities and

contingent assets”. Every entity has some categories of assets and liabilities disclosed in their

financial statements and such categories of assets are examined along with their basis of

measurement (Pawsey 2017). Furthermore, entity also holds different classes of liabilities and

classification of liabilities are examined in terms of the items that carries interest rates.

Discussion:

Answer to question i)

Funds sourcing can be classified based on ownership, based on periods and on the

source of generation. The discussion on the sourcing of funds would be limited to the funds

that is externally and internally sourced. Boral limited is a multinational company that deals

in supplying and manufacturing of construction and building materials. Sourcing of funds by

Boral limited is done both internally and externally. Funds generated by Boral limited

internally is by issuing of equity shares and investing retained earnings in the business. Some

of the borrowed funds or funds that is sourced externally is loans and borrowings (Fargher et

al. 2019). In addition to this, trade credit is the short term funding based on period. Lease

financing is also used by business that is used for financing the assets.

Introduction:

The paper discusses about the various sources of funds used by the organizations by

identifying the relative advantages and drawbacks of the funding used. In this regard, the

chosen companies for evaluating the various funding sources used to raise the funds are Boral

Limited and Brickworks limited operating in material sector. Discussion also incorporates the

assessment of concepts of the standard “AASB 137 provisions, contingent liabilities and

contingent assets”. Every entity has some categories of assets and liabilities disclosed in their

financial statements and such categories of assets are examined along with their basis of

measurement (Pawsey 2017). Furthermore, entity also holds different classes of liabilities and

classification of liabilities are examined in terms of the items that carries interest rates.

Discussion:

Answer to question i)

Funds sourcing can be classified based on ownership, based on periods and on the

source of generation. The discussion on the sourcing of funds would be limited to the funds

that is externally and internally sourced. Boral limited is a multinational company that deals

in supplying and manufacturing of construction and building materials. Sourcing of funds by

Boral limited is done both internally and externally. Funds generated by Boral limited

internally is by issuing of equity shares and investing retained earnings in the business. Some

of the borrowed funds or funds that is sourced externally is loans and borrowings (Fargher et

al. 2019). In addition to this, trade credit is the short term funding based on period. Lease

financing is also used by business that is used for financing the assets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING

Brickworks limited on other hand is the manufacturers of range of products by

investing and developing activities along with the product lines such as pavers, block and

brick (Brickworks.com.au 2018). It relies on the external as well as internal funds to finance

their business. The externally sourced funds include borrowings and internally sourced funds

include retained earnings and contributed equity. One of the sources of funds for medium

term used by the organization is lease financing.

Answer to question ii)

Changes in the different sources of funds used by the company can be examined by

analysing the figures disclosed in their published financial report. Total amount of issued

capital by Boral Limited has remained same over the years from 2017 to 2019 $ 4265.1

million. Funding using retained earning has increased over the period of three years from $

1156.1 million in year 2017 to $ 1309.9 million in 2018 and further to $ 1263.8 million in

year 2019. Loan and borrowings has increased initially to $ 2507.6 in year 2018 from $

2163.7 million. In current year 2019, borrowings and loans used to fund the business

activities has declined $ 2060.8 million. Funds raised through trade credit has declined in

year 2018 to $ 752 million from $ 825.9 million and has increased to $ 832.6 million in 2019

(Boral.com 2020).

Examination of the financial report of Brickworks limited reveals the evolution of the

sources of funds used by the company and changes over the last three financial years. Shares

issued to raise funds has increased over the time period of three years to $ 351229000 million

in year 2019 from $ 340814000 in year 2017. The figures suggested retained earnings implies

that the funds raised internally through retained earnings is significantly higher than issued

capital. Total amounts of retained earnings invested in the business has increased from $

1317244000 in year 2017 to $ 1416111000 in year 2018 and further to $ 153772000 in year

Brickworks limited on other hand is the manufacturers of range of products by

investing and developing activities along with the product lines such as pavers, block and

brick (Brickworks.com.au 2018). It relies on the external as well as internal funds to finance

their business. The externally sourced funds include borrowings and internally sourced funds

include retained earnings and contributed equity. One of the sources of funds for medium

term used by the organization is lease financing.

Answer to question ii)

Changes in the different sources of funds used by the company can be examined by

analysing the figures disclosed in their published financial report. Total amount of issued

capital by Boral Limited has remained same over the years from 2017 to 2019 $ 4265.1

million. Funding using retained earning has increased over the period of three years from $

1156.1 million in year 2017 to $ 1309.9 million in 2018 and further to $ 1263.8 million in

year 2019. Loan and borrowings has increased initially to $ 2507.6 in year 2018 from $

2163.7 million. In current year 2019, borrowings and loans used to fund the business

activities has declined $ 2060.8 million. Funds raised through trade credit has declined in

year 2018 to $ 752 million from $ 825.9 million and has increased to $ 832.6 million in 2019

(Boral.com 2020).

Examination of the financial report of Brickworks limited reveals the evolution of the

sources of funds used by the company and changes over the last three financial years. Shares

issued to raise funds has increased over the time period of three years to $ 351229000 million

in year 2019 from $ 340814000 in year 2017. The figures suggested retained earnings implies

that the funds raised internally through retained earnings is significantly higher than issued

capital. Total amounts of retained earnings invested in the business has increased from $

1317244000 in year 2017 to $ 1416111000 in year 2018 and further to $ 153772000 in year

CORPORATE ACCOUNTING

2019. Borrowings by Bricks has increased in year 2018 to $ 324105000 from $ 311977000 in

year 2017. However, there has not been increase in the borrowings in year 2019 and the value

stood at $ 324241000. Payable is another externally sourced short term funding that has

reduced from $ 110102000 in year 2017 to $ 107909000 in year 2018. The amount sourced

externally by way of payables has increased in year 2019 to $ 128276000

(Brickworks.com.au 2018).

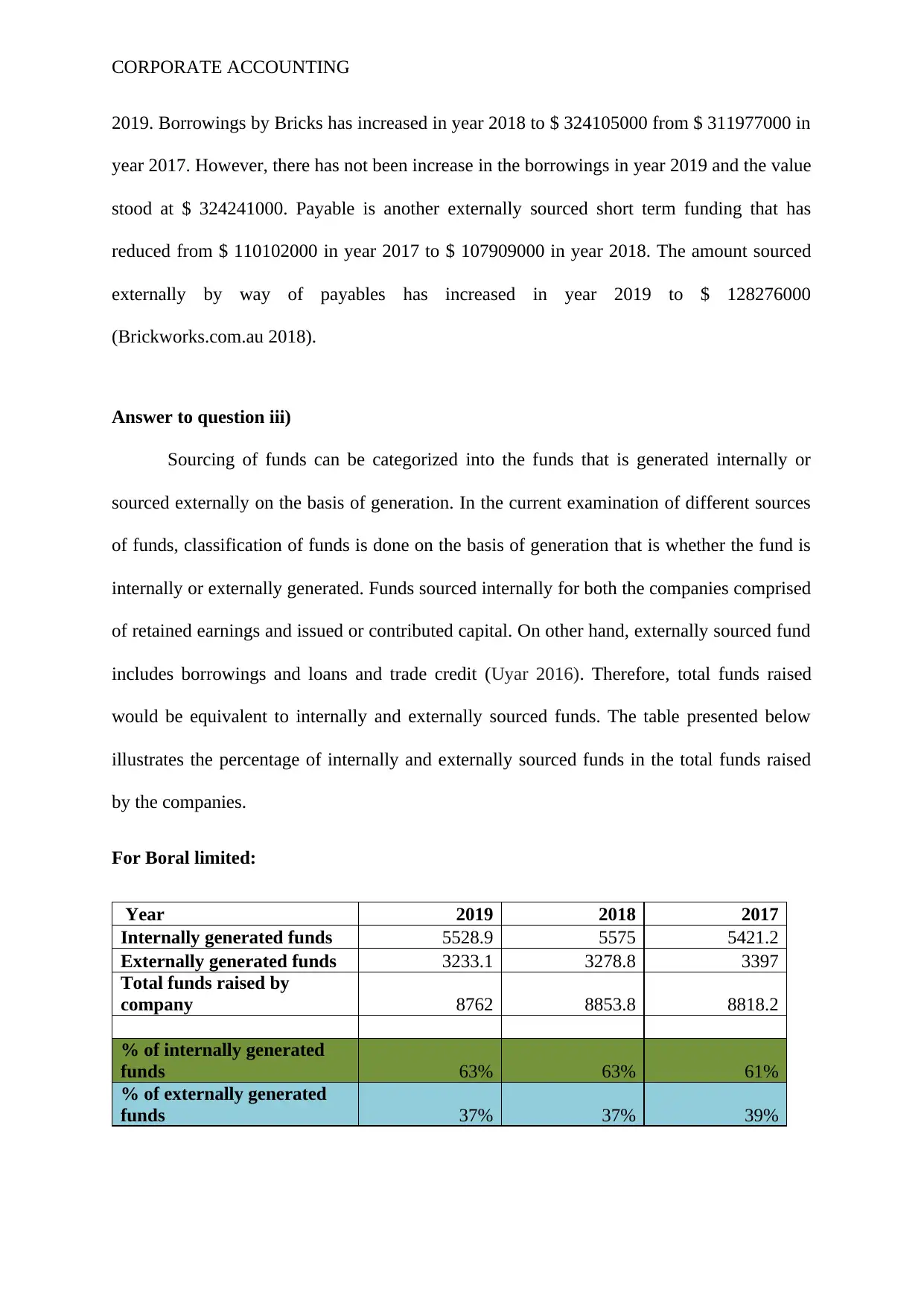

Answer to question iii)

Sourcing of funds can be categorized into the funds that is generated internally or

sourced externally on the basis of generation. In the current examination of different sources

of funds, classification of funds is done on the basis of generation that is whether the fund is

internally or externally generated. Funds sourced internally for both the companies comprised

of retained earnings and issued or contributed capital. On other hand, externally sourced fund

includes borrowings and loans and trade credit (Uyar 2016). Therefore, total funds raised

would be equivalent to internally and externally sourced funds. The table presented below

illustrates the percentage of internally and externally sourced funds in the total funds raised

by the companies.

For Boral limited:

Year 2019 2018 2017

Internally generated funds 5528.9 5575 5421.2

Externally generated funds 3233.1 3278.8 3397

Total funds raised by

company 8762 8853.8 8818.2

% of internally generated

funds 63% 63% 61%

% of externally generated

funds 37% 37% 39%

2019. Borrowings by Bricks has increased in year 2018 to $ 324105000 from $ 311977000 in

year 2017. However, there has not been increase in the borrowings in year 2019 and the value

stood at $ 324241000. Payable is another externally sourced short term funding that has

reduced from $ 110102000 in year 2017 to $ 107909000 in year 2018. The amount sourced

externally by way of payables has increased in year 2019 to $ 128276000

(Brickworks.com.au 2018).

Answer to question iii)

Sourcing of funds can be categorized into the funds that is generated internally or

sourced externally on the basis of generation. In the current examination of different sources

of funds, classification of funds is done on the basis of generation that is whether the fund is

internally or externally generated. Funds sourced internally for both the companies comprised

of retained earnings and issued or contributed capital. On other hand, externally sourced fund

includes borrowings and loans and trade credit (Uyar 2016). Therefore, total funds raised

would be equivalent to internally and externally sourced funds. The table presented below

illustrates the percentage of internally and externally sourced funds in the total funds raised

by the companies.

For Boral limited:

Year 2019 2018 2017

Internally generated funds 5528.9 5575 5421.2

Externally generated funds 3233.1 3278.8 3397

Total funds raised by

company 8762 8853.8 8818.2

% of internally generated

funds 63% 63% 61%

% of externally generated

funds 37% 37% 39%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE ACCOUNTING

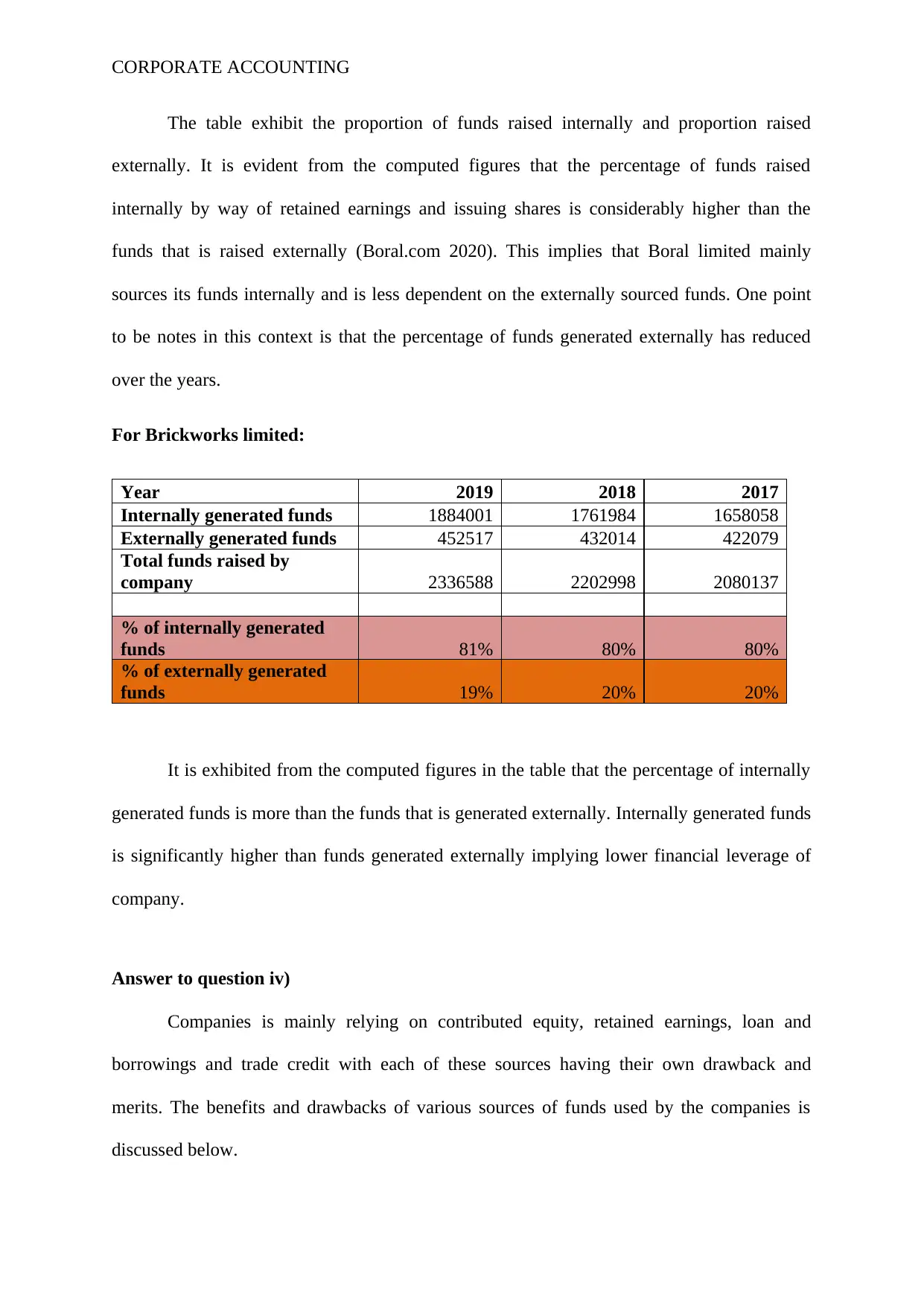

The table exhibit the proportion of funds raised internally and proportion raised

externally. It is evident from the computed figures that the percentage of funds raised

internally by way of retained earnings and issuing shares is considerably higher than the

funds that is raised externally (Boral.com 2020). This implies that Boral limited mainly

sources its funds internally and is less dependent on the externally sourced funds. One point

to be notes in this context is that the percentage of funds generated externally has reduced

over the years.

For Brickworks limited:

Year 2019 2018 2017

Internally generated funds 1884001 1761984 1658058

Externally generated funds 452517 432014 422079

Total funds raised by

company 2336588 2202998 2080137

% of internally generated

funds 81% 80% 80%

% of externally generated

funds 19% 20% 20%

It is exhibited from the computed figures in the table that the percentage of internally

generated funds is more than the funds that is generated externally. Internally generated funds

is significantly higher than funds generated externally implying lower financial leverage of

company.

Answer to question iv)

Companies is mainly relying on contributed equity, retained earnings, loan and

borrowings and trade credit with each of these sources having their own drawback and

merits. The benefits and drawbacks of various sources of funds used by the companies is

discussed below.

The table exhibit the proportion of funds raised internally and proportion raised

externally. It is evident from the computed figures that the percentage of funds raised

internally by way of retained earnings and issuing shares is considerably higher than the

funds that is raised externally (Boral.com 2020). This implies that Boral limited mainly

sources its funds internally and is less dependent on the externally sourced funds. One point

to be notes in this context is that the percentage of funds generated externally has reduced

over the years.

For Brickworks limited:

Year 2019 2018 2017

Internally generated funds 1884001 1761984 1658058

Externally generated funds 452517 432014 422079

Total funds raised by

company 2336588 2202998 2080137

% of internally generated

funds 81% 80% 80%

% of externally generated

funds 19% 20% 20%

It is exhibited from the computed figures in the table that the percentage of internally

generated funds is more than the funds that is generated externally. Internally generated funds

is significantly higher than funds generated externally implying lower financial leverage of

company.

Answer to question iv)

Companies is mainly relying on contributed equity, retained earnings, loan and

borrowings and trade credit with each of these sources having their own drawback and

merits. The benefits and drawbacks of various sources of funds used by the companies is

discussed below.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING

Some of the merits of contributed equity or issued capital are:

Issuing of shares does not burden company about making regular payments as there is

no mandate payment of dividends to the shareholders. Payment of dividend is done

only when adequate profits is generated by the company (Allen et al. 2019).

Risk lover investors is suited when it comes to issuing equity shares as they tend to

bear higher risk for generating higher returns.

Organization is able to enhance its credit worthiness due to issuing capital and

instilling confidence amongst the investors (Drover et al. 2017).

No security is required when it comes to issue share capital and the assets are

mortgage free.

Some of the drawbacks of contributed equity or issued capital are:

Raising funds through any other sources is cheaper than raising funds by issuing

equity shares.

Issuing shares involves some procedural delays and formalities.

The earnings of existing shareholders and voting power is diluted by issuing

additional equity shares (Cornwall et al. 2019).

Merits of retained earnings are as follows:

Funds used by the business using retained earnings is considered to be permanent if it

is available.

Retained earnings do not carry explicit costs such as dividend, interest and cost of

floatation.

Increase in use of retained earnings add to the credibility of business and appreciates

the price of shares in the market.

Some of the merits of contributed equity or issued capital are:

Issuing of shares does not burden company about making regular payments as there is

no mandate payment of dividends to the shareholders. Payment of dividend is done

only when adequate profits is generated by the company (Allen et al. 2019).

Risk lover investors is suited when it comes to issuing equity shares as they tend to

bear higher risk for generating higher returns.

Organization is able to enhance its credit worthiness due to issuing capital and

instilling confidence amongst the investors (Drover et al. 2017).

No security is required when it comes to issue share capital and the assets are

mortgage free.

Some of the drawbacks of contributed equity or issued capital are:

Raising funds through any other sources is cheaper than raising funds by issuing

equity shares.

Issuing shares involves some procedural delays and formalities.

The earnings of existing shareholders and voting power is diluted by issuing

additional equity shares (Cornwall et al. 2019).

Merits of retained earnings are as follows:

Funds used by the business using retained earnings is considered to be permanent if it

is available.

Retained earnings do not carry explicit costs such as dividend, interest and cost of

floatation.

Increase in use of retained earnings add to the credibility of business and appreciates

the price of shares in the market.

CORPORATE ACCOUNTING

Organization can have greater degree of flexibility and operational freedom because

funds are generated internally.

Any unexpected loss can be absorbed by the use of retained earnings in funding.

Some of the drawbacks of retained earnings are:

Many business do not recognize the opportunity costs which retained earnings carries

and consequently causes the funds to not utilize optimally.

Since the profits generated by the business is uncertain and keeps on fluctuating,

retained earnings is considered as uncertain source.

Excessive usage of retained earnings might create dissatisfaction amongst

shareholders as they are paid lower amount of dividends.

Advantages of borrowings:

Raising funds by way of borrowing and loans is preferred by the risk averse investors

seeking fixed return from their investment.

Equity shareholder control on the management of company is not diluted as no voting

rights are carried by borrowings.

Compared to equity capital, raising funds through loan and borrowings is less

expensive as the payment of interest on the total amount borrowed is tax deductible

(Kabir and Rahman 2016).

Borrowings is beneficial to the company when the earnings and sales are moderately

stable

Shortcomings of borrowings:

The borrowing capacity of organization reduces due to borrowing by way of issuing

debentures or loans.

Organization can have greater degree of flexibility and operational freedom because

funds are generated internally.

Any unexpected loss can be absorbed by the use of retained earnings in funding.

Some of the drawbacks of retained earnings are:

Many business do not recognize the opportunity costs which retained earnings carries

and consequently causes the funds to not utilize optimally.

Since the profits generated by the business is uncertain and keeps on fluctuating,

retained earnings is considered as uncertain source.

Excessive usage of retained earnings might create dissatisfaction amongst

shareholders as they are paid lower amount of dividends.

Advantages of borrowings:

Raising funds by way of borrowing and loans is preferred by the risk averse investors

seeking fixed return from their investment.

Equity shareholder control on the management of company is not diluted as no voting

rights are carried by borrowings.

Compared to equity capital, raising funds through loan and borrowings is less

expensive as the payment of interest on the total amount borrowed is tax deductible

(Kabir and Rahman 2016).

Borrowings is beneficial to the company when the earnings and sales are moderately

stable

Shortcomings of borrowings:

The borrowing capacity of organization reduces due to borrowing by way of issuing

debentures or loans.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE ACCOUNTING

Company’s earning is permanently burdened by borrowing and loans due to fixed

charges in the form of interest.

Provision is required to be made for repayment.

Merits of trade credit are as follows:

In event of known credit worthiness of the customers to sellers, the company would

have readily available trade credit.

Trade credit offers a continuous and convenient source of raising funds for short term.

Trade credit helps in promoting the total sales volume indirectly.

Drawbacks of trade credit are as follows:

Trade credit can only raise some limited amounts of funds and greater requirements of

funds in the business cannot be addressed using trade credit.

There is also a risk of firms being involved in overtrading because of flexible and

easily available facilities of trade credit.

Assets are not charged for generating funds from trade credit.

Answer to question v)

Balance sheet of Boral limited discloses various types of liabilities classified as

current and non-current liabilities. Different types of liabilities identified under current

liabilities include trade creditors, provisions, employee benefits liabilities, borrowings and

loans, financial liabilities, current tax liabilities and liabilities that is classified as sale.

Noncurrent liabilities include financial liabilities, provisions, loan and borrowings, deferred

tax liabilities and other liabilities. All the mentioned liabilities do not carry interest expect

loans and borrowings.

Company’s earning is permanently burdened by borrowing and loans due to fixed

charges in the form of interest.

Provision is required to be made for repayment.

Merits of trade credit are as follows:

In event of known credit worthiness of the customers to sellers, the company would

have readily available trade credit.

Trade credit offers a continuous and convenient source of raising funds for short term.

Trade credit helps in promoting the total sales volume indirectly.

Drawbacks of trade credit are as follows:

Trade credit can only raise some limited amounts of funds and greater requirements of

funds in the business cannot be addressed using trade credit.

There is also a risk of firms being involved in overtrading because of flexible and

easily available facilities of trade credit.

Assets are not charged for generating funds from trade credit.

Answer to question v)

Balance sheet of Boral limited discloses various types of liabilities classified as

current and non-current liabilities. Different types of liabilities identified under current

liabilities include trade creditors, provisions, employee benefits liabilities, borrowings and

loans, financial liabilities, current tax liabilities and liabilities that is classified as sale.

Noncurrent liabilities include financial liabilities, provisions, loan and borrowings, deferred

tax liabilities and other liabilities. All the mentioned liabilities do not carry interest expect

loans and borrowings.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING

Total current liabilities and non-current liabilities comprise of total liabilities reported

by Brickworks limited. Items reported under current liabilities include payables, liabilities

held for sale, derivate financial liabilities, current income tax liability, contract liabilities,

provisions and post-employment liabilities. On other hand, items reported under noncurrent

liabilities include derivative financial liabilities, borrowings, provisions, post-employment

liabilities and deferred income tax liability. Interest bearing liabilities is reported under the

section of non-current liabilities that is borrowings and no other items carries interest

(Brickworks.com.au 2018).

Answer to question vi)

The disclosure and accounting treatment for provisions is specified by the Accounting

standard AASB 137 where provision is regarded as the liability of uncertain things or of

uncertain amount. Provision can also be used in context of the items such as doubtful debts,

depreciation and assets impairment. It is ensured by this standard that provisions should be

realized by using appropriate basis of measurement and criteria of recognition. The

restructuring provisions is incorporated in this standard and recognition of provision is done

by the entity when the amount of obligation towards provision can be estimated reliably,

present obligation due to any past events is held by entity and when the settlement of

obligation requires the outflow of resources representing some economic benefits (Michiels

and Molly 2017). In the absence of all such conditions non recognition of provisions should

be done by entities. Provision recognition is done for the obligation that is independent of the

future events of entity and results from any past events. For the settlement of present

obligation, provision recognized should provide the best estimate of the expenditure incurred.

The best estimate of provision is determined by accounting for uncertainties and risks

surrounding around many events and circumstances. Settlement of obligation requires the

Total current liabilities and non-current liabilities comprise of total liabilities reported

by Brickworks limited. Items reported under current liabilities include payables, liabilities

held for sale, derivate financial liabilities, current income tax liability, contract liabilities,

provisions and post-employment liabilities. On other hand, items reported under noncurrent

liabilities include derivative financial liabilities, borrowings, provisions, post-employment

liabilities and deferred income tax liability. Interest bearing liabilities is reported under the

section of non-current liabilities that is borrowings and no other items carries interest

(Brickworks.com.au 2018).

Answer to question vi)

The disclosure and accounting treatment for provisions is specified by the Accounting

standard AASB 137 where provision is regarded as the liability of uncertain things or of

uncertain amount. Provision can also be used in context of the items such as doubtful debts,

depreciation and assets impairment. It is ensured by this standard that provisions should be

realized by using appropriate basis of measurement and criteria of recognition. The

restructuring provisions is incorporated in this standard and recognition of provision is done

by the entity when the amount of obligation towards provision can be estimated reliably,

present obligation due to any past events is held by entity and when the settlement of

obligation requires the outflow of resources representing some economic benefits (Michiels

and Molly 2017). In the absence of all such conditions non recognition of provisions should

be done by entities. Provision recognition is done for the obligation that is independent of the

future events of entity and results from any past events. For the settlement of present

obligation, provision recognized should provide the best estimate of the expenditure incurred.

The best estimate of provision is determined by accounting for uncertainties and risks

surrounding around many events and circumstances. Settlement of obligation requires the

CORPORATE ACCOUNTING

present value of expenditure which gives the provision amount as there is material impact of

time value of money (Aasb.gov.au 2014).

Answer to question vii)

The overall analysis of the financial report of Boral limited leads to conclude the fact

that company has not mentioned anything about its reference to the standard AASB 137 as

the report does not mention about it anywhere. However, when looking at the recognition

criteria and measurement basis of provision, it is easily observed that Boral limited have

satisfied all such condition and have recognised provisions by fulfilling all the listed

recognition criteria as per the standard. Therefore, although, the financial report does not

mention about the standard, the company has made reference to recognize provisions by

meeting the listed recognition criteria. Total amount of provisions has reduced in the current

year.

On other hand, annual report of Brickworks limited clearly reveals that the company

has made reference to the standard “AASB 137 provisions, contingent liabilities and

contingent assets”. Recognition of warrants which the group offers is done under this

particular standard. In addition to this, group also adheres to the recognition criteria and basis

of measurement of accounting provisions (Aasb.gov.au 2014). The amounts depicting

provision is the best estimate of the amount required to settle any uncertainties and

obligations in the present year. Brickworks have made provisions related to remediation,

employee benefits, workers compensation and infrastructure costs.

Answer to question viii)

Assets of reporting entities are categorized into current assets and non-current assets.

Current assets reported by Boral limited in their financial report includes receivables,

present value of expenditure which gives the provision amount as there is material impact of

time value of money (Aasb.gov.au 2014).

Answer to question vii)

The overall analysis of the financial report of Boral limited leads to conclude the fact

that company has not mentioned anything about its reference to the standard AASB 137 as

the report does not mention about it anywhere. However, when looking at the recognition

criteria and measurement basis of provision, it is easily observed that Boral limited have

satisfied all such condition and have recognised provisions by fulfilling all the listed

recognition criteria as per the standard. Therefore, although, the financial report does not

mention about the standard, the company has made reference to recognize provisions by

meeting the listed recognition criteria. Total amount of provisions has reduced in the current

year.

On other hand, annual report of Brickworks limited clearly reveals that the company

has made reference to the standard “AASB 137 provisions, contingent liabilities and

contingent assets”. Recognition of warrants which the group offers is done under this

particular standard. In addition to this, group also adheres to the recognition criteria and basis

of measurement of accounting provisions (Aasb.gov.au 2014). The amounts depicting

provision is the best estimate of the amount required to settle any uncertainties and

obligations in the present year. Brickworks have made provisions related to remediation,

employee benefits, workers compensation and infrastructure costs.

Answer to question viii)

Assets of reporting entities are categorized into current assets and non-current assets.

Current assets reported by Boral limited in their financial report includes receivables,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.