Corporate Accounting Report: Capital Structure and Liability Analysis

VerifiedAdded on 2022/08/18

|11

|3477

|12

Report

AI Summary

This report analyzes the corporate accounting practices of Australian Vintage Ltd and Domino's Pizza Enterprises. It examines their capital sources, including equity and debt, and their respective trends over a period, presenting a table of capital mix. The report assesses the companies' reporting of assets and liabilities, evaluating consistency with Australian reporting frameworks. It further discusses asset recognition criteria and explores the advantages and disadvantages of different funding sources, including equity, debt, and retained earnings. The analysis includes a review of liabilities, provisions, contingent liabilities, and contingent assets, along with the application of AASB 137. The report also covers the classification and recognition criteria of assets, providing a comprehensive overview of the companies' financial reporting processes. The report concludes by summarizing key findings and providing references for further reading.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CORPORATE ACCOUNTING

Executive Summary

The discussion would be related to two companies reporting process for the period

for which annual report of the considered companies would be reviewed. The

companies which are considered are Australian Vintage ltd and Domino’s Pizza

Enterprises. The capital sources and its respective trends would be the main focus of

the discussion in the initial stages for which a table showing trend is also presented.

The assessment shows the reporting process of assets and liabilities for both the

company and also comment on whether the same are consistent with the reporting

framework which is followed in Australia. The analysis further includes discussion on

recognition criteria which is followed for reporting assets of the business.

CORPORATE ACCOUNTING

Executive Summary

The discussion would be related to two companies reporting process for the period

for which annual report of the considered companies would be reviewed. The

companies which are considered are Australian Vintage ltd and Domino’s Pizza

Enterprises. The capital sources and its respective trends would be the main focus of

the discussion in the initial stages for which a table showing trend is also presented.

The assessment shows the reporting process of assets and liabilities for both the

company and also comment on whether the same are consistent with the reporting

framework which is followed in Australia. The analysis further includes discussion on

recognition criteria which is followed for reporting assets of the business.

2

CORPORATE ACCOUNTING

Table of Contents

Introduction...................................................................................................................3

Discussion....................................................................................................................3

Options for accumulating of Funds...........................................................................3

Changes in the Capital Mix.......................................................................................4

Percentage of Different Sources of Funds................................................................4

Pros and Cons of Different Sources of Business.....................................................5

Liabilities of the Businesses......................................................................................7

Provisions, Contingent Liabilities and Contingent Assets........................................7

Reporting for AASB 137............................................................................................8

Classification of Assets.............................................................................................9

Recognition Criteria...................................................................................................9

Conclusion....................................................................................................................9

Reference...................................................................................................................10

CORPORATE ACCOUNTING

Table of Contents

Introduction...................................................................................................................3

Discussion....................................................................................................................3

Options for accumulating of Funds...........................................................................3

Changes in the Capital Mix.......................................................................................4

Percentage of Different Sources of Funds................................................................4

Pros and Cons of Different Sources of Business.....................................................5

Liabilities of the Businesses......................................................................................7

Provisions, Contingent Liabilities and Contingent Assets........................................7

Reporting for AASB 137............................................................................................8

Classification of Assets.............................................................................................9

Recognition Criteria...................................................................................................9

Conclusion....................................................................................................................9

Reference...................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CORPORATE ACCOUNTING

Introduction

The accounting framework which is used by a business for the purpose of

presenting the financial statement follows conceptual framework and relevant

accounting standards so that all necessary information and disclosures can be

included. The accounting information also includes aspects of capital sources which

is utilized by a business along with the assets and liabilities which the business

possess at the end of a financial year. The assessment would be considering two

companies which are listed in same industry and provide similar products. The

companies which are considered for the purpose of analysis are Australian Vintage

ltd and Domino’s Pizza Enterprises. The capital sources which is used by the

businesses and also the trend which can be identified regarding the changes in

capital sources would also be discussed in the analysis. Further, the reporting

process and disclosures which the respective businesses show regarding assets and

liabilities are projected in the financial reports (Tschopp and Nastanski 2014). In

addition to this, the analysis would also identify if any contingent liabilities or assets

or provisions are disclosed in the financial report or not and whether appropriate

disclosure is provided in this respect. The recognition criteria which are followed by

the respective companies are also shows covered in the assessment and the same

are obtained from draft notes.

Discussion

Options for accumulating of Funds

In a business, numerous projects and activities are undertaken for the motive

of generating profits and expanding the operations. In order to conduct all these

projects and activities, funds are required and the same needs to be acquired from a

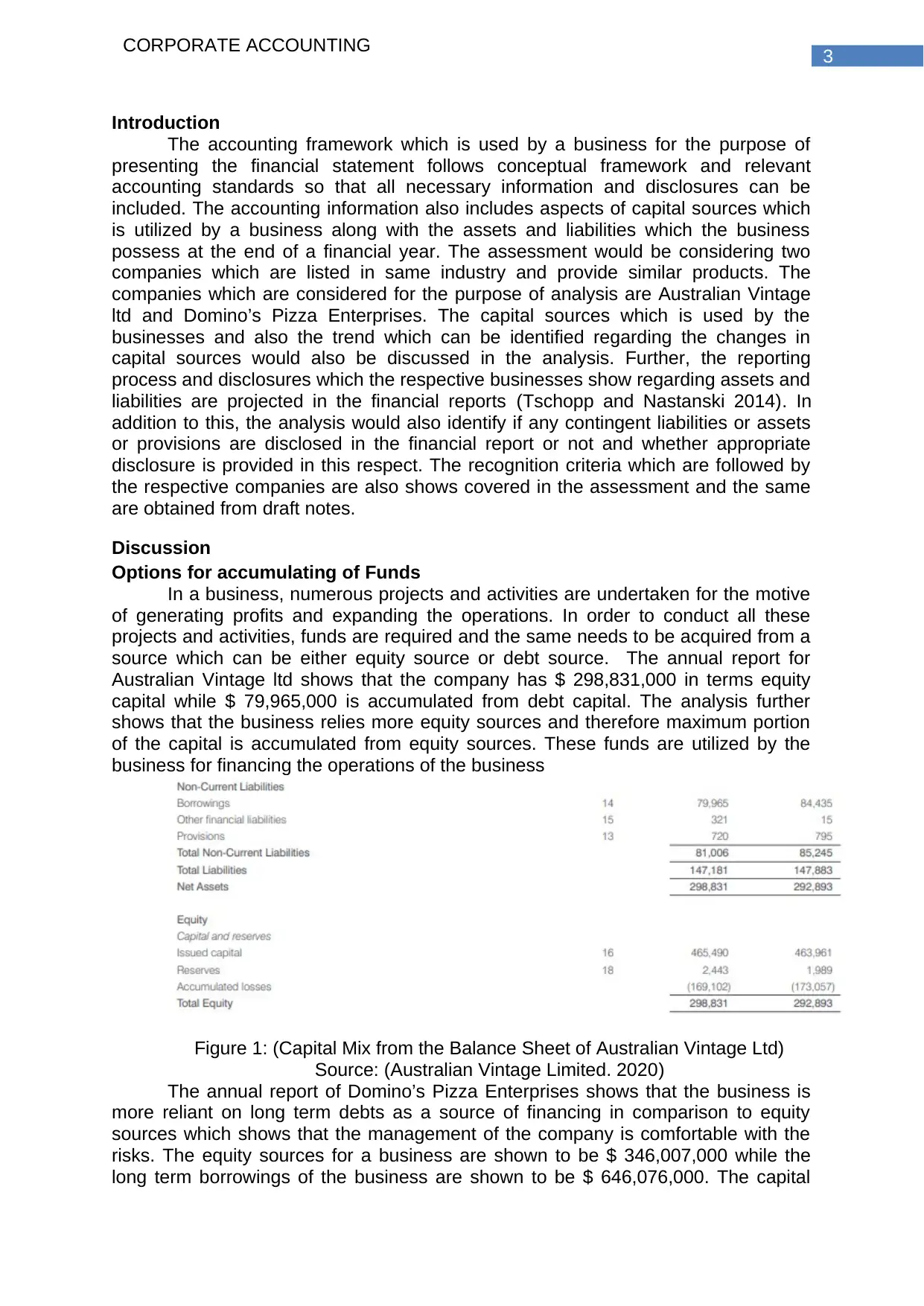

source which can be either equity source or debt source. The annual report for

Australian Vintage ltd shows that the company has $ 298,831,000 in terms equity

capital while $ 79,965,000 is accumulated from debt capital. The analysis further

shows that the business relies more equity sources and therefore maximum portion

of the capital is accumulated from equity sources. These funds are utilized by the

business for financing the operations of the business

Figure 1: (Capital Mix from the Balance Sheet of Australian Vintage Ltd)

Source: (Australian Vintage Limited. 2020)

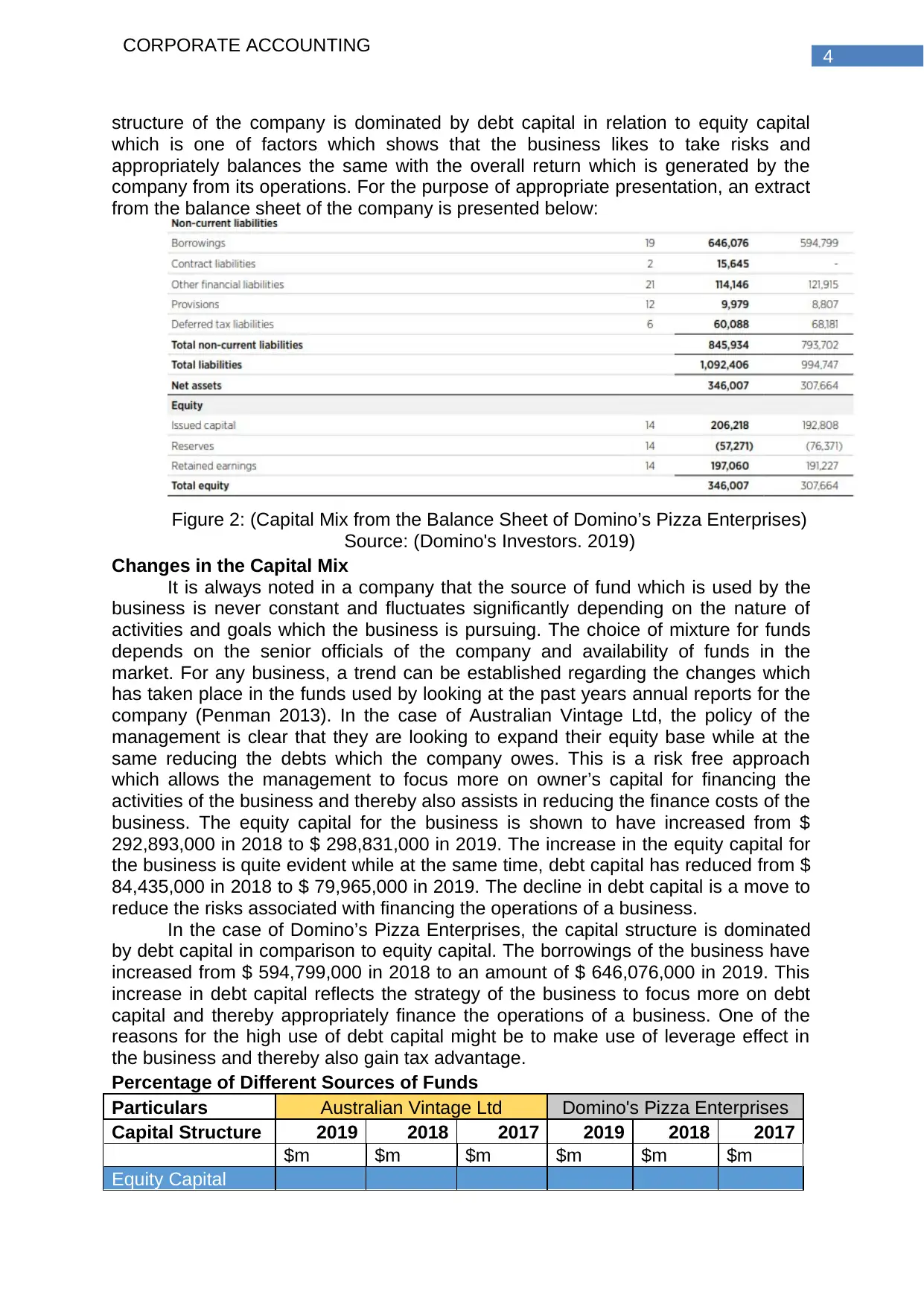

The annual report of Domino’s Pizza Enterprises shows that the business is

more reliant on long term debts as a source of financing in comparison to equity

sources which shows that the management of the company is comfortable with the

risks. The equity sources for a business are shown to be $ 346,007,000 while the

long term borrowings of the business are shown to be $ 646,076,000. The capital

CORPORATE ACCOUNTING

Introduction

The accounting framework which is used by a business for the purpose of

presenting the financial statement follows conceptual framework and relevant

accounting standards so that all necessary information and disclosures can be

included. The accounting information also includes aspects of capital sources which

is utilized by a business along with the assets and liabilities which the business

possess at the end of a financial year. The assessment would be considering two

companies which are listed in same industry and provide similar products. The

companies which are considered for the purpose of analysis are Australian Vintage

ltd and Domino’s Pizza Enterprises. The capital sources which is used by the

businesses and also the trend which can be identified regarding the changes in

capital sources would also be discussed in the analysis. Further, the reporting

process and disclosures which the respective businesses show regarding assets and

liabilities are projected in the financial reports (Tschopp and Nastanski 2014). In

addition to this, the analysis would also identify if any contingent liabilities or assets

or provisions are disclosed in the financial report or not and whether appropriate

disclosure is provided in this respect. The recognition criteria which are followed by

the respective companies are also shows covered in the assessment and the same

are obtained from draft notes.

Discussion

Options for accumulating of Funds

In a business, numerous projects and activities are undertaken for the motive

of generating profits and expanding the operations. In order to conduct all these

projects and activities, funds are required and the same needs to be acquired from a

source which can be either equity source or debt source. The annual report for

Australian Vintage ltd shows that the company has $ 298,831,000 in terms equity

capital while $ 79,965,000 is accumulated from debt capital. The analysis further

shows that the business relies more equity sources and therefore maximum portion

of the capital is accumulated from equity sources. These funds are utilized by the

business for financing the operations of the business

Figure 1: (Capital Mix from the Balance Sheet of Australian Vintage Ltd)

Source: (Australian Vintage Limited. 2020)

The annual report of Domino’s Pizza Enterprises shows that the business is

more reliant on long term debts as a source of financing in comparison to equity

sources which shows that the management of the company is comfortable with the

risks. The equity sources for a business are shown to be $ 346,007,000 while the

long term borrowings of the business are shown to be $ 646,076,000. The capital

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CORPORATE ACCOUNTING

structure of the company is dominated by debt capital in relation to equity capital

which is one of factors which shows that the business likes to take risks and

appropriately balances the same with the overall return which is generated by the

company from its operations. For the purpose of appropriate presentation, an extract

from the balance sheet of the company is presented below:

Figure 2: (Capital Mix from the Balance Sheet of Domino’s Pizza Enterprises)

Source: (Domino's Investors. 2019)

Changes in the Capital Mix

It is always noted in a company that the source of fund which is used by the

business is never constant and fluctuates significantly depending on the nature of

activities and goals which the business is pursuing. The choice of mixture for funds

depends on the senior officials of the company and availability of funds in the

market. For any business, a trend can be established regarding the changes which

has taken place in the funds used by looking at the past years annual reports for the

company (Penman 2013). In the case of Australian Vintage Ltd, the policy of the

management is clear that they are looking to expand their equity base while at the

same reducing the debts which the company owes. This is a risk free approach

which allows the management to focus more on owner’s capital for financing the

activities of the business and thereby also assists in reducing the finance costs of the

business. The equity capital for the business is shown to have increased from $

292,893,000 in 2018 to $ 298,831,000 in 2019. The increase in the equity capital for

the business is quite evident while at the same time, debt capital has reduced from $

84,435,000 in 2018 to $ 79,965,000 in 2019. The decline in debt capital is a move to

reduce the risks associated with financing the operations of a business.

In the case of Domino’s Pizza Enterprises, the capital structure is dominated

by debt capital in comparison to equity capital. The borrowings of the business have

increased from $ 594,799,000 in 2018 to an amount of $ 646,076,000 in 2019. This

increase in debt capital reflects the strategy of the business to focus more on debt

capital and thereby appropriately finance the operations of a business. One of the

reasons for the high use of debt capital might be to make use of leverage effect in

the business and thereby also gain tax advantage.

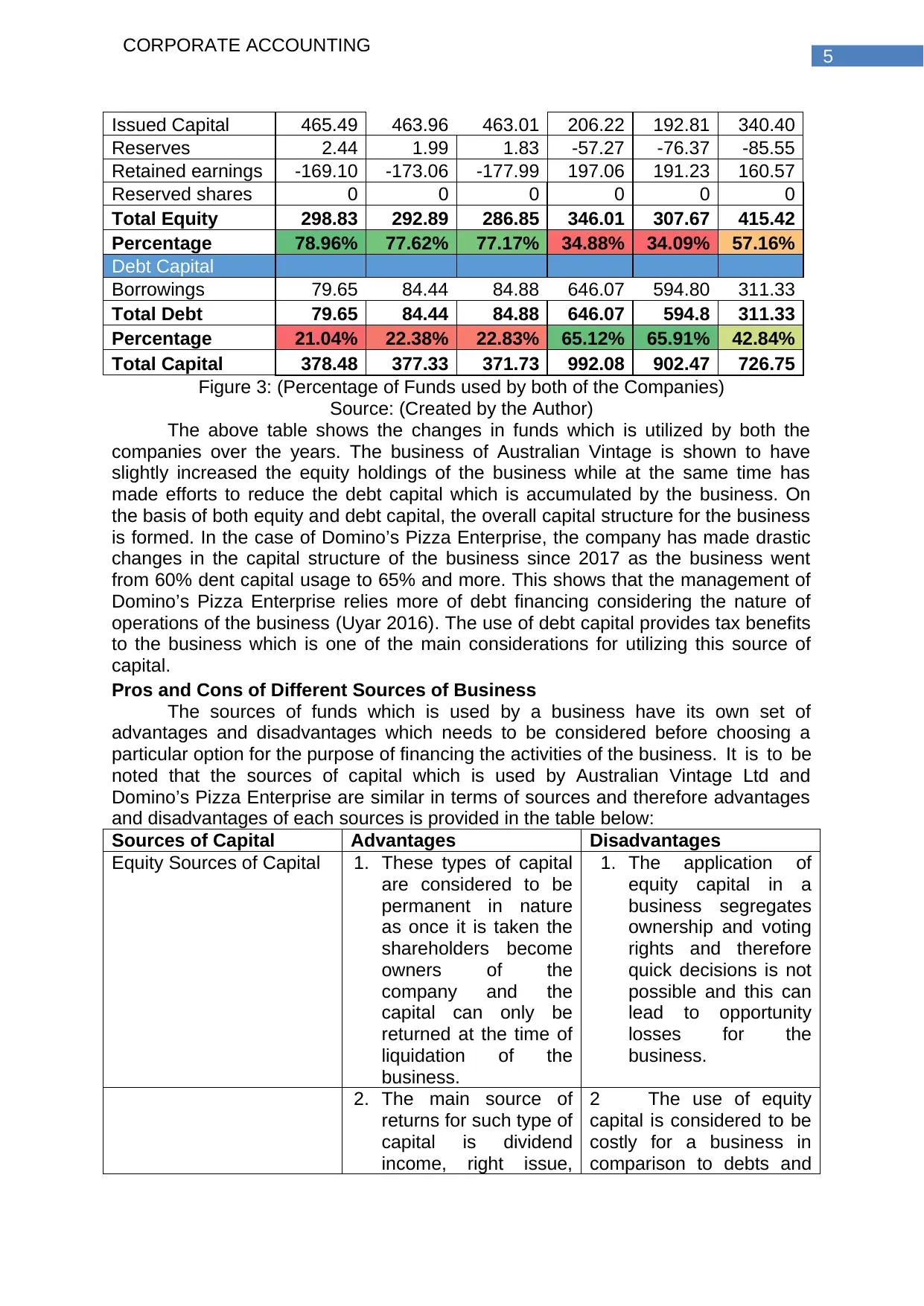

Percentage of Different Sources of Funds

Particulars Australian Vintage Ltd Domino's Pizza Enterprises

Capital Structure 2019 2018 2017 2019 2018 2017

$m $m $m $m $m $m

Equity Capital

CORPORATE ACCOUNTING

structure of the company is dominated by debt capital in relation to equity capital

which is one of factors which shows that the business likes to take risks and

appropriately balances the same with the overall return which is generated by the

company from its operations. For the purpose of appropriate presentation, an extract

from the balance sheet of the company is presented below:

Figure 2: (Capital Mix from the Balance Sheet of Domino’s Pizza Enterprises)

Source: (Domino's Investors. 2019)

Changes in the Capital Mix

It is always noted in a company that the source of fund which is used by the

business is never constant and fluctuates significantly depending on the nature of

activities and goals which the business is pursuing. The choice of mixture for funds

depends on the senior officials of the company and availability of funds in the

market. For any business, a trend can be established regarding the changes which

has taken place in the funds used by looking at the past years annual reports for the

company (Penman 2013). In the case of Australian Vintage Ltd, the policy of the

management is clear that they are looking to expand their equity base while at the

same reducing the debts which the company owes. This is a risk free approach

which allows the management to focus more on owner’s capital for financing the

activities of the business and thereby also assists in reducing the finance costs of the

business. The equity capital for the business is shown to have increased from $

292,893,000 in 2018 to $ 298,831,000 in 2019. The increase in the equity capital for

the business is quite evident while at the same time, debt capital has reduced from $

84,435,000 in 2018 to $ 79,965,000 in 2019. The decline in debt capital is a move to

reduce the risks associated with financing the operations of a business.

In the case of Domino’s Pizza Enterprises, the capital structure is dominated

by debt capital in comparison to equity capital. The borrowings of the business have

increased from $ 594,799,000 in 2018 to an amount of $ 646,076,000 in 2019. This

increase in debt capital reflects the strategy of the business to focus more on debt

capital and thereby appropriately finance the operations of a business. One of the

reasons for the high use of debt capital might be to make use of leverage effect in

the business and thereby also gain tax advantage.

Percentage of Different Sources of Funds

Particulars Australian Vintage Ltd Domino's Pizza Enterprises

Capital Structure 2019 2018 2017 2019 2018 2017

$m $m $m $m $m $m

Equity Capital

5

CORPORATE ACCOUNTING

Issued Capital 465.49 463.96 463.01 206.22 192.81 340.40

Reserves 2.44 1.99 1.83 -57.27 -76.37 -85.55

Retained earnings -169.10 -173.06 -177.99 197.06 191.23 160.57

Reserved shares 0 0 0 0 0 0

Total Equity 298.83 292.89 286.85 346.01 307.67 415.42

Percentage 78.96% 77.62% 77.17% 34.88% 34.09% 57.16%

Debt Capital

Borrowings 79.65 84.44 84.88 646.07 594.80 311.33

Total Debt 79.65 84.44 84.88 646.07 594.8 311.33

Percentage 21.04% 22.38% 22.83% 65.12% 65.91% 42.84%

Total Capital 378.48 377.33 371.73 992.08 902.47 726.75

Figure 3: (Percentage of Funds used by both of the Companies)

Source: (Created by the Author)

The above table shows the changes in funds which is utilized by both the

companies over the years. The business of Australian Vintage is shown to have

slightly increased the equity holdings of the business while at the same time has

made efforts to reduce the debt capital which is accumulated by the business. On

the basis of both equity and debt capital, the overall capital structure for the business

is formed. In the case of Domino’s Pizza Enterprise, the company has made drastic

changes in the capital structure of the business since 2017 as the business went

from 60% dent capital usage to 65% and more. This shows that the management of

Domino’s Pizza Enterprise relies more of debt financing considering the nature of

operations of the business (Uyar 2016). The use of debt capital provides tax benefits

to the business which is one of the main considerations for utilizing this source of

capital.

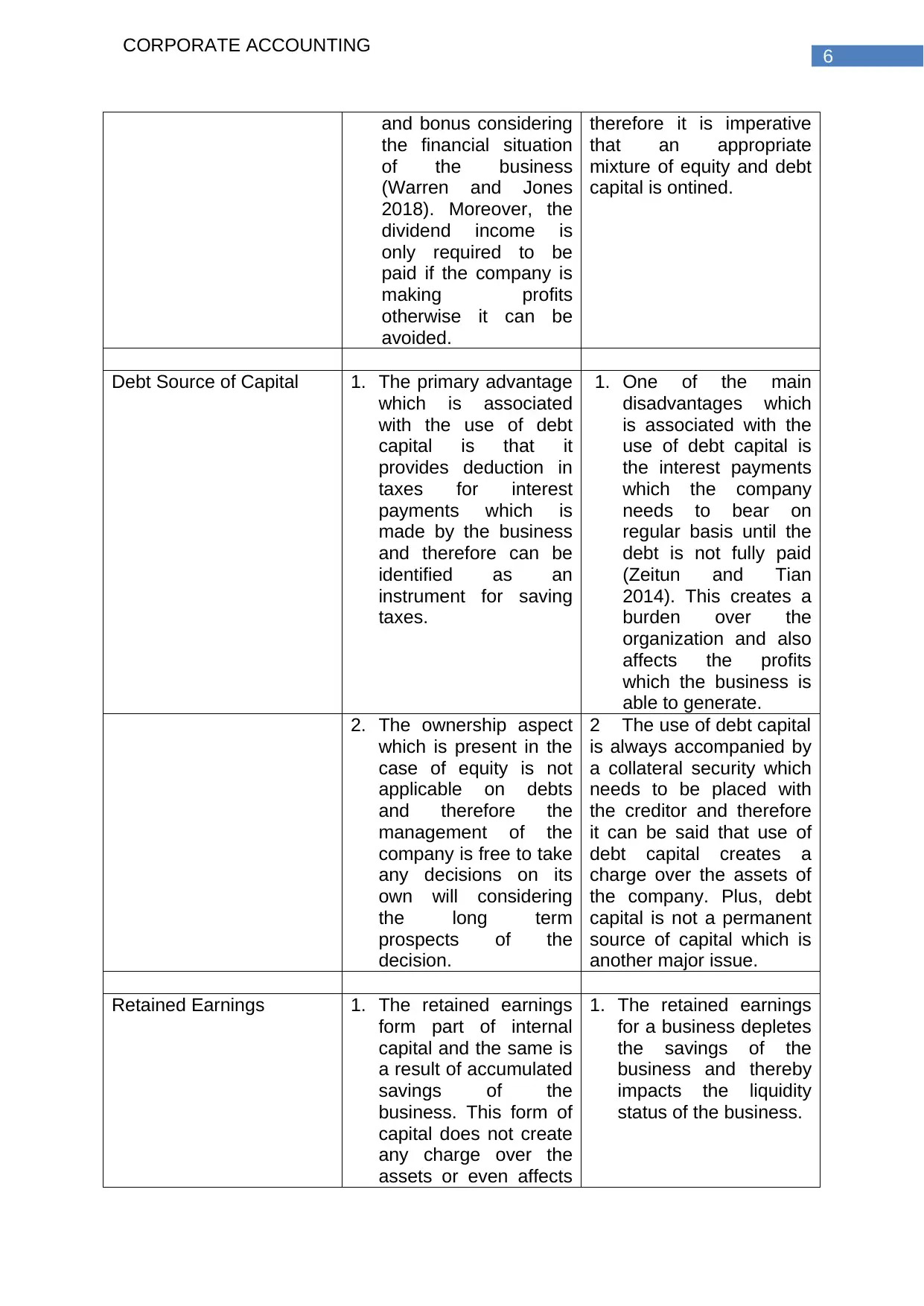

Pros and Cons of Different Sources of Business

The sources of funds which is used by a business have its own set of

advantages and disadvantages which needs to be considered before choosing a

particular option for the purpose of financing the activities of the business. It is to be

noted that the sources of capital which is used by Australian Vintage Ltd and

Domino’s Pizza Enterprise are similar in terms of sources and therefore advantages

and disadvantages of each sources is provided in the table below:

Sources of Capital Advantages Disadvantages

Equity Sources of Capital 1. These types of capital

are considered to be

permanent in nature

as once it is taken the

shareholders become

owners of the

company and the

capital can only be

returned at the time of

liquidation of the

business.

1. The application of

equity capital in a

business segregates

ownership and voting

rights and therefore

quick decisions is not

possible and this can

lead to opportunity

losses for the

business.

2. The main source of

returns for such type of

capital is dividend

income, right issue,

2 The use of equity

capital is considered to be

costly for a business in

comparison to debts and

CORPORATE ACCOUNTING

Issued Capital 465.49 463.96 463.01 206.22 192.81 340.40

Reserves 2.44 1.99 1.83 -57.27 -76.37 -85.55

Retained earnings -169.10 -173.06 -177.99 197.06 191.23 160.57

Reserved shares 0 0 0 0 0 0

Total Equity 298.83 292.89 286.85 346.01 307.67 415.42

Percentage 78.96% 77.62% 77.17% 34.88% 34.09% 57.16%

Debt Capital

Borrowings 79.65 84.44 84.88 646.07 594.80 311.33

Total Debt 79.65 84.44 84.88 646.07 594.8 311.33

Percentage 21.04% 22.38% 22.83% 65.12% 65.91% 42.84%

Total Capital 378.48 377.33 371.73 992.08 902.47 726.75

Figure 3: (Percentage of Funds used by both of the Companies)

Source: (Created by the Author)

The above table shows the changes in funds which is utilized by both the

companies over the years. The business of Australian Vintage is shown to have

slightly increased the equity holdings of the business while at the same time has

made efforts to reduce the debt capital which is accumulated by the business. On

the basis of both equity and debt capital, the overall capital structure for the business

is formed. In the case of Domino’s Pizza Enterprise, the company has made drastic

changes in the capital structure of the business since 2017 as the business went

from 60% dent capital usage to 65% and more. This shows that the management of

Domino’s Pizza Enterprise relies more of debt financing considering the nature of

operations of the business (Uyar 2016). The use of debt capital provides tax benefits

to the business which is one of the main considerations for utilizing this source of

capital.

Pros and Cons of Different Sources of Business

The sources of funds which is used by a business have its own set of

advantages and disadvantages which needs to be considered before choosing a

particular option for the purpose of financing the activities of the business. It is to be

noted that the sources of capital which is used by Australian Vintage Ltd and

Domino’s Pizza Enterprise are similar in terms of sources and therefore advantages

and disadvantages of each sources is provided in the table below:

Sources of Capital Advantages Disadvantages

Equity Sources of Capital 1. These types of capital

are considered to be

permanent in nature

as once it is taken the

shareholders become

owners of the

company and the

capital can only be

returned at the time of

liquidation of the

business.

1. The application of

equity capital in a

business segregates

ownership and voting

rights and therefore

quick decisions is not

possible and this can

lead to opportunity

losses for the

business.

2. The main source of

returns for such type of

capital is dividend

income, right issue,

2 The use of equity

capital is considered to be

costly for a business in

comparison to debts and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CORPORATE ACCOUNTING

and bonus considering

the financial situation

of the business

(Warren and Jones

2018). Moreover, the

dividend income is

only required to be

paid if the company is

making profits

otherwise it can be

avoided.

therefore it is imperative

that an appropriate

mixture of equity and debt

capital is ontined.

Debt Source of Capital 1. The primary advantage

which is associated

with the use of debt

capital is that it

provides deduction in

taxes for interest

payments which is

made by the business

and therefore can be

identified as an

instrument for saving

taxes.

1. One of the main

disadvantages which

is associated with the

use of debt capital is

the interest payments

which the company

needs to bear on

regular basis until the

debt is not fully paid

(Zeitun and Tian

2014). This creates a

burden over the

organization and also

affects the profits

which the business is

able to generate.

2. The ownership aspect

which is present in the

case of equity is not

applicable on debts

and therefore the

management of the

company is free to take

any decisions on its

own will considering

the long term

prospects of the

decision.

2 The use of debt capital

is always accompanied by

a collateral security which

needs to be placed with

the creditor and therefore

it can be said that use of

debt capital creates a

charge over the assets of

the company. Plus, debt

capital is not a permanent

source of capital which is

another major issue.

Retained Earnings 1. The retained earnings

form part of internal

capital and the same is

a result of accumulated

savings of the

business. This form of

capital does not create

any charge over the

assets or even affects

1. The retained earnings

for a business depletes

the savings of the

business and thereby

impacts the liquidity

status of the business.

CORPORATE ACCOUNTING

and bonus considering

the financial situation

of the business

(Warren and Jones

2018). Moreover, the

dividend income is

only required to be

paid if the company is

making profits

otherwise it can be

avoided.

therefore it is imperative

that an appropriate

mixture of equity and debt

capital is ontined.

Debt Source of Capital 1. The primary advantage

which is associated

with the use of debt

capital is that it

provides deduction in

taxes for interest

payments which is

made by the business

and therefore can be

identified as an

instrument for saving

taxes.

1. One of the main

disadvantages which

is associated with the

use of debt capital is

the interest payments

which the company

needs to bear on

regular basis until the

debt is not fully paid

(Zeitun and Tian

2014). This creates a

burden over the

organization and also

affects the profits

which the business is

able to generate.

2. The ownership aspect

which is present in the

case of equity is not

applicable on debts

and therefore the

management of the

company is free to take

any decisions on its

own will considering

the long term

prospects of the

decision.

2 The use of debt capital

is always accompanied by

a collateral security which

needs to be placed with

the creditor and therefore

it can be said that use of

debt capital creates a

charge over the assets of

the company. Plus, debt

capital is not a permanent

source of capital which is

another major issue.

Retained Earnings 1. The retained earnings

form part of internal

capital and the same is

a result of accumulated

savings of the

business. This form of

capital does not create

any charge over the

assets or even affects

1. The retained earnings

for a business depletes

the savings of the

business and thereby

impacts the liquidity

status of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE ACCOUNTING

the ownership status of

the company. The use

of such capital

demonstrates strength

on the part of the

management.

Liabilities of the Businesses

The liabilities of a business are covered in the balance sheet and the same

shows what the business owes to external parties. The liabilities need to be

appropriately presented in the financial statement so that investors have a clear idea

regarding all the liabilities of the business. The total of the liabilities and equities of a

business equals the total of the asset side of the business. As per the reporting

framework which is adopted by Australia Vintage Ltd for the year 2019 shows that

the management has effectively shows the sub-parts of current and non-current

liabilities so that it can be effectively determined which liabilities are short term and

which are long term in nature (Aversano and Christiaens 2014). The current liabilities

include short term borrowings, trade payables and provisions which are maintained

by the organization for the period. On the other hand, non-current liabilities include

the long term borrowings which the business has undertaken during the period for

the purpose of financing the operations of the business. In an overall analysis, it can

be said that the management of Australia Vintage Ltd has appropriately managed

the liabilities of the business and provided appropriate disclosures in this respect in

the financial statements. In case of debts which form a major part of the non-current

liabilities, the management is trying to reduce the same so that the risks which are

associated with the use of debt capital can be minimized.

In the case of Domino’s Pizza Enterprise, the management of the company

has also properly represented the reporting aspects of liabilities so that appropriate

financial position can be available to the investors of a business. The annual reports

shows that the business has a material amount of deferred tax liabilities as well as

provisions which has increased from previous year estimates (Demartini and Paoloni

2013). The non-current liabilities for the business show an increase which is mainly

due to the increase in borrowings of the business which also creates interest burden

over the management of the company. One new item which is presented in the

liability side of the company is contract liabilities which are also shown for a

significant amount and the same needs to be controlled by the senior officials of the

business.

Provisions, Contingent Liabilities and Contingent Assets

The provisions which is stated in by AASB 137 “Provisions, Contingent

Liabilities and Contingent Assets”, requires businesses to appropriately disclose

items which needs to be represented in the financial statements of the entity. The

standard requires businesses to appropriately disclose all losses or provisions which

are created by the business during the period (Ioana and Adriana 2013). The

purpose for which the provision was created should also be disclosed in the annual

reports note section. Every company which has provisions or contingent liabilities

needs to follow this standard for providing appropriate disclosure in the financial

reports of the business.

CORPORATE ACCOUNTING

the ownership status of

the company. The use

of such capital

demonstrates strength

on the part of the

management.

Liabilities of the Businesses

The liabilities of a business are covered in the balance sheet and the same

shows what the business owes to external parties. The liabilities need to be

appropriately presented in the financial statement so that investors have a clear idea

regarding all the liabilities of the business. The total of the liabilities and equities of a

business equals the total of the asset side of the business. As per the reporting

framework which is adopted by Australia Vintage Ltd for the year 2019 shows that

the management has effectively shows the sub-parts of current and non-current

liabilities so that it can be effectively determined which liabilities are short term and

which are long term in nature (Aversano and Christiaens 2014). The current liabilities

include short term borrowings, trade payables and provisions which are maintained

by the organization for the period. On the other hand, non-current liabilities include

the long term borrowings which the business has undertaken during the period for

the purpose of financing the operations of the business. In an overall analysis, it can

be said that the management of Australia Vintage Ltd has appropriately managed

the liabilities of the business and provided appropriate disclosures in this respect in

the financial statements. In case of debts which form a major part of the non-current

liabilities, the management is trying to reduce the same so that the risks which are

associated with the use of debt capital can be minimized.

In the case of Domino’s Pizza Enterprise, the management of the company

has also properly represented the reporting aspects of liabilities so that appropriate

financial position can be available to the investors of a business. The annual reports

shows that the business has a material amount of deferred tax liabilities as well as

provisions which has increased from previous year estimates (Demartini and Paoloni

2013). The non-current liabilities for the business show an increase which is mainly

due to the increase in borrowings of the business which also creates interest burden

over the management of the company. One new item which is presented in the

liability side of the company is contract liabilities which are also shown for a

significant amount and the same needs to be controlled by the senior officials of the

business.

Provisions, Contingent Liabilities and Contingent Assets

The provisions which is stated in by AASB 137 “Provisions, Contingent

Liabilities and Contingent Assets”, requires businesses to appropriately disclose

items which needs to be represented in the financial statements of the entity. The

standard requires businesses to appropriately disclose all losses or provisions which

are created by the business during the period (Ioana and Adriana 2013). The

purpose for which the provision was created should also be disclosed in the annual

reports note section. Every company which has provisions or contingent liabilities

needs to follow this standard for providing appropriate disclosure in the financial

reports of the business.

8

CORPORATE ACCOUNTING

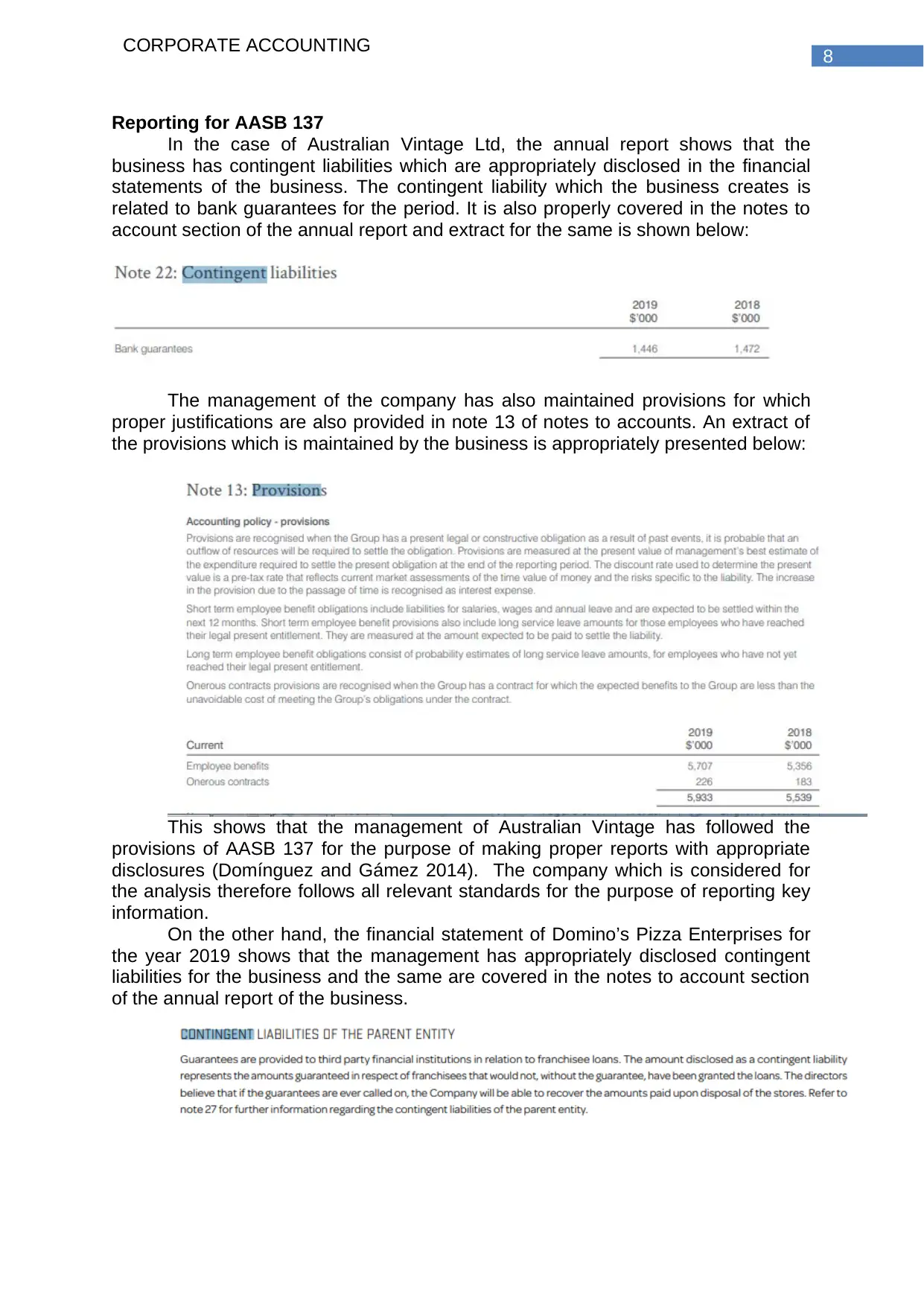

Reporting for AASB 137

In the case of Australian Vintage Ltd, the annual report shows that the

business has contingent liabilities which are appropriately disclosed in the financial

statements of the business. The contingent liability which the business creates is

related to bank guarantees for the period. It is also properly covered in the notes to

account section of the annual report and extract for the same is shown below:

The management of the company has also maintained provisions for which

proper justifications are also provided in note 13 of notes to accounts. An extract of

the provisions which is maintained by the business is appropriately presented below:

This shows that the management of Australian Vintage has followed the

provisions of AASB 137 for the purpose of making proper reports with appropriate

disclosures (Domínguez and Gámez 2014). The company which is considered for

the analysis therefore follows all relevant standards for the purpose of reporting key

information.

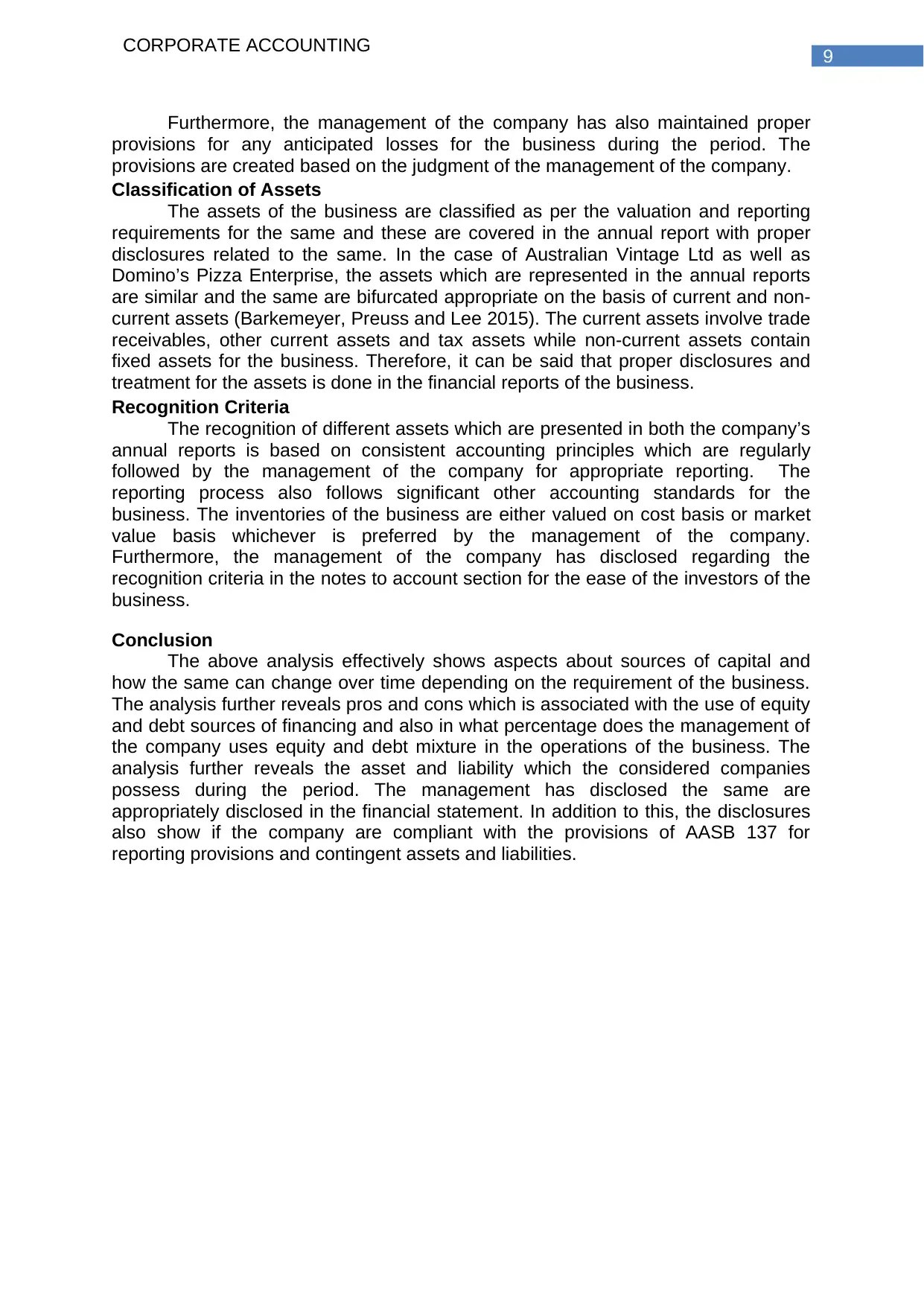

On the other hand, the financial statement of Domino’s Pizza Enterprises for

the year 2019 shows that the management has appropriately disclosed contingent

liabilities for the business and the same are covered in the notes to account section

of the annual report of the business.

CORPORATE ACCOUNTING

Reporting for AASB 137

In the case of Australian Vintage Ltd, the annual report shows that the

business has contingent liabilities which are appropriately disclosed in the financial

statements of the business. The contingent liability which the business creates is

related to bank guarantees for the period. It is also properly covered in the notes to

account section of the annual report and extract for the same is shown below:

The management of the company has also maintained provisions for which

proper justifications are also provided in note 13 of notes to accounts. An extract of

the provisions which is maintained by the business is appropriately presented below:

This shows that the management of Australian Vintage has followed the

provisions of AASB 137 for the purpose of making proper reports with appropriate

disclosures (Domínguez and Gámez 2014). The company which is considered for

the analysis therefore follows all relevant standards for the purpose of reporting key

information.

On the other hand, the financial statement of Domino’s Pizza Enterprises for

the year 2019 shows that the management has appropriately disclosed contingent

liabilities for the business and the same are covered in the notes to account section

of the annual report of the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CORPORATE ACCOUNTING

Furthermore, the management of the company has also maintained proper

provisions for any anticipated losses for the business during the period. The

provisions are created based on the judgment of the management of the company.

Classification of Assets

The assets of the business are classified as per the valuation and reporting

requirements for the same and these are covered in the annual report with proper

disclosures related to the same. In the case of Australian Vintage Ltd as well as

Domino’s Pizza Enterprise, the assets which are represented in the annual reports

are similar and the same are bifurcated appropriate on the basis of current and non-

current assets (Barkemeyer, Preuss and Lee 2015). The current assets involve trade

receivables, other current assets and tax assets while non-current assets contain

fixed assets for the business. Therefore, it can be said that proper disclosures and

treatment for the assets is done in the financial reports of the business.

Recognition Criteria

The recognition of different assets which are presented in both the company’s

annual reports is based on consistent accounting principles which are regularly

followed by the management of the company for appropriate reporting. The

reporting process also follows significant other accounting standards for the

business. The inventories of the business are either valued on cost basis or market

value basis whichever is preferred by the management of the company.

Furthermore, the management of the company has disclosed regarding the

recognition criteria in the notes to account section for the ease of the investors of the

business.

Conclusion

The above analysis effectively shows aspects about sources of capital and

how the same can change over time depending on the requirement of the business.

The analysis further reveals pros and cons which is associated with the use of equity

and debt sources of financing and also in what percentage does the management of

the company uses equity and debt mixture in the operations of the business. The

analysis further reveals the asset and liability which the considered companies

possess during the period. The management has disclosed the same are

appropriately disclosed in the financial statement. In addition to this, the disclosures

also show if the company are compliant with the provisions of AASB 137 for

reporting provisions and contingent assets and liabilities.

CORPORATE ACCOUNTING

Furthermore, the management of the company has also maintained proper

provisions for any anticipated losses for the business during the period. The

provisions are created based on the judgment of the management of the company.

Classification of Assets

The assets of the business are classified as per the valuation and reporting

requirements for the same and these are covered in the annual report with proper

disclosures related to the same. In the case of Australian Vintage Ltd as well as

Domino’s Pizza Enterprise, the assets which are represented in the annual reports

are similar and the same are bifurcated appropriate on the basis of current and non-

current assets (Barkemeyer, Preuss and Lee 2015). The current assets involve trade

receivables, other current assets and tax assets while non-current assets contain

fixed assets for the business. Therefore, it can be said that proper disclosures and

treatment for the assets is done in the financial reports of the business.

Recognition Criteria

The recognition of different assets which are presented in both the company’s

annual reports is based on consistent accounting principles which are regularly

followed by the management of the company for appropriate reporting. The

reporting process also follows significant other accounting standards for the

business. The inventories of the business are either valued on cost basis or market

value basis whichever is preferred by the management of the company.

Furthermore, the management of the company has disclosed regarding the

recognition criteria in the notes to account section for the ease of the investors of the

business.

Conclusion

The above analysis effectively shows aspects about sources of capital and

how the same can change over time depending on the requirement of the business.

The analysis further reveals pros and cons which is associated with the use of equity

and debt sources of financing and also in what percentage does the management of

the company uses equity and debt mixture in the operations of the business. The

analysis further reveals the asset and liability which the considered companies

possess during the period. The management has disclosed the same are

appropriately disclosed in the financial statement. In addition to this, the disclosures

also show if the company are compliant with the provisions of AASB 137 for

reporting provisions and contingent assets and liabilities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CORPORATE ACCOUNTING

Reference

Australian Vintage Limited. (2020). Investors - Australian Vintage Limited. [online]

Available at: https://www.australianvintage.com.au/investors/ [Accessed 31 Jan.

2020].

Aversano, N. and Christiaens, J., 2014. Governmental financial reporting of heritage

assets from a user needs perspective. Financial Accountability &

Management, 30(2), pp.150-174.

Barkemeyer, R., Preuss, L. and Lee, L., 2015, December. Corporate reporting on

corruption: An international comparison. In Accounting Forum (Vol. 39, No. 4, pp.

349-365). Taylor & Francis.

Demartini, P. and Paoloni, P., 2013. Awareness of your own intangible

assets. Journal of Intellectual Capital.

Domínguez, L.R. and Gámez, L.C.N., 2014. Corporate reporting on risks: Evidence

from Spanish companies. Revista de Contabilidad, 17(2), pp.116-129.

Domino's Investors. (2019). Annual Reports — Domino's Investors. [online] Available

at: https://investors.dominos.com.au/annual-reports [Accessed 31 Jan. 2020].

Ioana, D. and Adriana, T., 2013. New corporate reporting trends. Analysis on the

evolution of integrated reporting. Annals of the University of Oradea, Economic

Science Series, 22(1), pp.1221-1228.

Penman, S.H., 2013. Financial statement analysis and security valuation. McGraw-

Hill.

Tschopp, D. and Nastanski, M., 2014. The harmonization and convergence of

corporate social responsibility reporting standards. Journal of Business

Ethics, 125(1), pp.147-162.

Uyar, A., 2016. Evolution of corporate reporting and emerging trends. Journal of

Corporate Accounting & Finance, 27(4), pp.27-30.

Warren, C. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Zeitun, R. and Tian, G.G., 2014. Capital structure and corporate performance:

evidence from Jordan. Australasian Accounting Business & Finance Journal,

Forthcoming.

CORPORATE ACCOUNTING

Reference

Australian Vintage Limited. (2020). Investors - Australian Vintage Limited. [online]

Available at: https://www.australianvintage.com.au/investors/ [Accessed 31 Jan.

2020].

Aversano, N. and Christiaens, J., 2014. Governmental financial reporting of heritage

assets from a user needs perspective. Financial Accountability &

Management, 30(2), pp.150-174.

Barkemeyer, R., Preuss, L. and Lee, L., 2015, December. Corporate reporting on

corruption: An international comparison. In Accounting Forum (Vol. 39, No. 4, pp.

349-365). Taylor & Francis.

Demartini, P. and Paoloni, P., 2013. Awareness of your own intangible

assets. Journal of Intellectual Capital.

Domínguez, L.R. and Gámez, L.C.N., 2014. Corporate reporting on risks: Evidence

from Spanish companies. Revista de Contabilidad, 17(2), pp.116-129.

Domino's Investors. (2019). Annual Reports — Domino's Investors. [online] Available

at: https://investors.dominos.com.au/annual-reports [Accessed 31 Jan. 2020].

Ioana, D. and Adriana, T., 2013. New corporate reporting trends. Analysis on the

evolution of integrated reporting. Annals of the University of Oradea, Economic

Science Series, 22(1), pp.1221-1228.

Penman, S.H., 2013. Financial statement analysis and security valuation. McGraw-

Hill.

Tschopp, D. and Nastanski, M., 2014. The harmonization and convergence of

corporate social responsibility reporting standards. Journal of Business

Ethics, 125(1), pp.147-162.

Uyar, A., 2016. Evolution of corporate reporting and emerging trends. Journal of

Corporate Accounting & Finance, 27(4), pp.27-30.

Warren, C. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Zeitun, R. and Tian, G.G., 2014. Capital structure and corporate performance:

evidence from Jordan. Australasian Accounting Business & Finance Journal,

Forthcoming.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.