HI5020 Corporate Accounting: Fund Sources, Liabilities, and Assets

VerifiedAdded on 2022/08/31

|13

|4771

|12

Report

AI Summary

This report, prepared for the HI5020 Corporate Accounting course at Holmes Institute, examines the fund sources, liabilities, and asset measurement practices of Caltex Australia Limited and Woolworths Group. The report begins by identifying and discussing the evolution of these companies' funding sources, including equity and debt, over a specified period. It then analyzes the percentage of internally and externally generated funds, as well as the merits and shortcomings of each funding type. The report further delves into the liabilities shown on the balance sheets of both companies, along with a summary of the key provisions of AASB 137, and whether the companies have made reference to the standard. Finally, the report identifies and examines the different categories of assets recorded by each company and the measurement basis used for each asset class. The analysis provides a comprehensive overview of corporate accounting principles and their practical application in the context of these two Australian companies.

Running Head: CORPORATE ACCOUNTING

CORPORATE ACCOUNTING

Name of the Student

Name of the University

Author Note

CORPORATE ACCOUNTING

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ACCOUNTING

Abstract

Financial records are maintained by the accountants and are they can be specialized

in one or various and finance areas. Corporate accounting aims to communicate

about firm’s assets and liabilities to the users. It helps in offering full suite of the

services for accounting and finance functions on the higher-end offerings, which

drives maximum value all across enterprises. Hence, this report aims to discuss

different fund sources and its evolution, merits and demerits of various fund sources

used by Caltex Australia Limited and Woolworths Group. Further, discussion will be

on AASB 137, its reference to company, categories of assets recorded and its

measurement basis used by both the company. Therefore, this report concludes that

both of the companies have opted equity and debt as their fund sources and both of

them has not made reference to AASB 137, but they have fulfill the condition of this

accounting standard.

Abstract

Financial records are maintained by the accountants and are they can be specialized

in one or various and finance areas. Corporate accounting aims to communicate

about firm’s assets and liabilities to the users. It helps in offering full suite of the

services for accounting and finance functions on the higher-end offerings, which

drives maximum value all across enterprises. Hence, this report aims to discuss

different fund sources and its evolution, merits and demerits of various fund sources

used by Caltex Australia Limited and Woolworths Group. Further, discussion will be

on AASB 137, its reference to company, categories of assets recorded and its

measurement basis used by both the company. Therefore, this report concludes that

both of the companies have opted equity and debt as their fund sources and both of

them has not made reference to AASB 137, but they have fulfill the condition of this

accounting standard.

2CORPORATE ACCOUNTING

Table of Contents

Introduction...................................................................................................................3

Background of Entity.................................................................................................3

Discussion.....................................................................................................................3

Fund Sources............................................................................................................3

Evolution of the Fund Sources..................................................................................4

Percentage of Internally and Externally Generated Funds.......................................4

Merits and Shortcomings of Fund Sources...............................................................5

Equity Fund Source...............................................................................................5

Debt Fund Source.................................................................................................6

Liabilities shown in Balance-Sheet...........................................................................6

Key Provisions under AASB 137..............................................................................6

AASB 137 Reference in Company’s Annual Report.................................................7

Recorded Assets Categories....................................................................................7

Basis of Measurement for Recorded Assets Class..................................................8

Conclusion....................................................................................................................9

Reference...................................................................................................................10

Table of Contents

Introduction...................................................................................................................3

Background of Entity.................................................................................................3

Discussion.....................................................................................................................3

Fund Sources............................................................................................................3

Evolution of the Fund Sources..................................................................................4

Percentage of Internally and Externally Generated Funds.......................................4

Merits and Shortcomings of Fund Sources...............................................................5

Equity Fund Source...............................................................................................5

Debt Fund Source.................................................................................................6

Liabilities shown in Balance-Sheet...........................................................................6

Key Provisions under AASB 137..............................................................................6

AASB 137 Reference in Company’s Annual Report.................................................7

Recorded Assets Categories....................................................................................7

Basis of Measurement for Recorded Assets Class..................................................8

Conclusion....................................................................................................................9

Reference...................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ACCOUNTING

Introduction

Corporate accounting is the accounting process, which is dedicated towards

single company’s operations. The activity of corporate accounting is performed

normally for ascertaining operational and financial status of company. The investors

of company are interested especially in knowing about firm’s financial strength for

making investment. Corporate accounting is performed for ensuring that company’s

financial activities complies with regulations and laws stipulated by the oversight

bodies. It helps in ensuring that activities of business are in tune with the policies of

organization (Avdjiev, Chui and Shin 2014). Hence, this assignment aims to identify

various fund sources and its evolution of Caltex Australia Limited and Woolworths

Group. Further, discussion will be on percentage of internally and externally

generated fund sources, merits and shortcomings of each fund sources, different

types of liabilities shown in selected companies. Moreover, examination of key

provisions under AASB 137 and its reference to the selected company. Lastly,

identification and examination will be of different assets categories and the

measurement basis used by both the companies for each assets class.

Background of Entity

Caltex Australia Limited

Caltex Australia Limited is the Australian convenience retailer and the

transport fuel supplier company. It is engaged in purchases, refines, markets and

distributes products of petroleum in the Australia. The products of Australia are

consisting of motor oil, petroleum, diesel fuel, lubricants and jet fuel. It also operates

service stations, stores of fast food and convenience stores. Caltex Australia Limited

is publicly listed comany that derives revenue from wholesale, refinement and

petroleum retail. It employs approx. 6,600 employees that operates in Singapore,

Australia and New Zealand and is administered from Sydney head office (Caltex.

2020).

Woolworths Group Limited

Woolworths Group is the major listed company of Australia that offers retail

operations. This company is engaged in operating general merchandise

supermarkets and consumer goods as well as it is engaged in the products, liquor

and food procurement. The company also operates in the hotels that are consists of

food, pubs, gaming operations and accommodations. Woolworths Group serves its

customers in the countries of Australia and New Zealand (Woolworthsgroup.com.au.

2020).

Discussion

i)

Fund Sources

The sources of fund are referred to medium with the help of which entity

raises its working capital and long-term capital. The entity can select any fund

sources depending upon requirement and gestation period of project that has to be

financed. Fund is the lifeblood of any organization. There is no business that can live

without having funds. Business organization often require capital funding or external

funding for expanding their business into the new locations or markets for investing

in the research & development of fending off competition (Muritala 2018). Further,

Introduction

Corporate accounting is the accounting process, which is dedicated towards

single company’s operations. The activity of corporate accounting is performed

normally for ascertaining operational and financial status of company. The investors

of company are interested especially in knowing about firm’s financial strength for

making investment. Corporate accounting is performed for ensuring that company’s

financial activities complies with regulations and laws stipulated by the oversight

bodies. It helps in ensuring that activities of business are in tune with the policies of

organization (Avdjiev, Chui and Shin 2014). Hence, this assignment aims to identify

various fund sources and its evolution of Caltex Australia Limited and Woolworths

Group. Further, discussion will be on percentage of internally and externally

generated fund sources, merits and shortcomings of each fund sources, different

types of liabilities shown in selected companies. Moreover, examination of key

provisions under AASB 137 and its reference to the selected company. Lastly,

identification and examination will be of different assets categories and the

measurement basis used by both the companies for each assets class.

Background of Entity

Caltex Australia Limited

Caltex Australia Limited is the Australian convenience retailer and the

transport fuel supplier company. It is engaged in purchases, refines, markets and

distributes products of petroleum in the Australia. The products of Australia are

consisting of motor oil, petroleum, diesel fuel, lubricants and jet fuel. It also operates

service stations, stores of fast food and convenience stores. Caltex Australia Limited

is publicly listed comany that derives revenue from wholesale, refinement and

petroleum retail. It employs approx. 6,600 employees that operates in Singapore,

Australia and New Zealand and is administered from Sydney head office (Caltex.

2020).

Woolworths Group Limited

Woolworths Group is the major listed company of Australia that offers retail

operations. This company is engaged in operating general merchandise

supermarkets and consumer goods as well as it is engaged in the products, liquor

and food procurement. The company also operates in the hotels that are consists of

food, pubs, gaming operations and accommodations. Woolworths Group serves its

customers in the countries of Australia and New Zealand (Woolworthsgroup.com.au.

2020).

Discussion

i)

Fund Sources

The sources of fund are referred to medium with the help of which entity

raises its working capital and long-term capital. The entity can select any fund

sources depending upon requirement and gestation period of project that has to be

financed. Fund is the lifeblood of any organization. There is no business that can live

without having funds. Business organization often require capital funding or external

funding for expanding their business into the new locations or markets for investing

in the research & development of fending off competition (Muritala 2018). Further,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ACCOUNTING

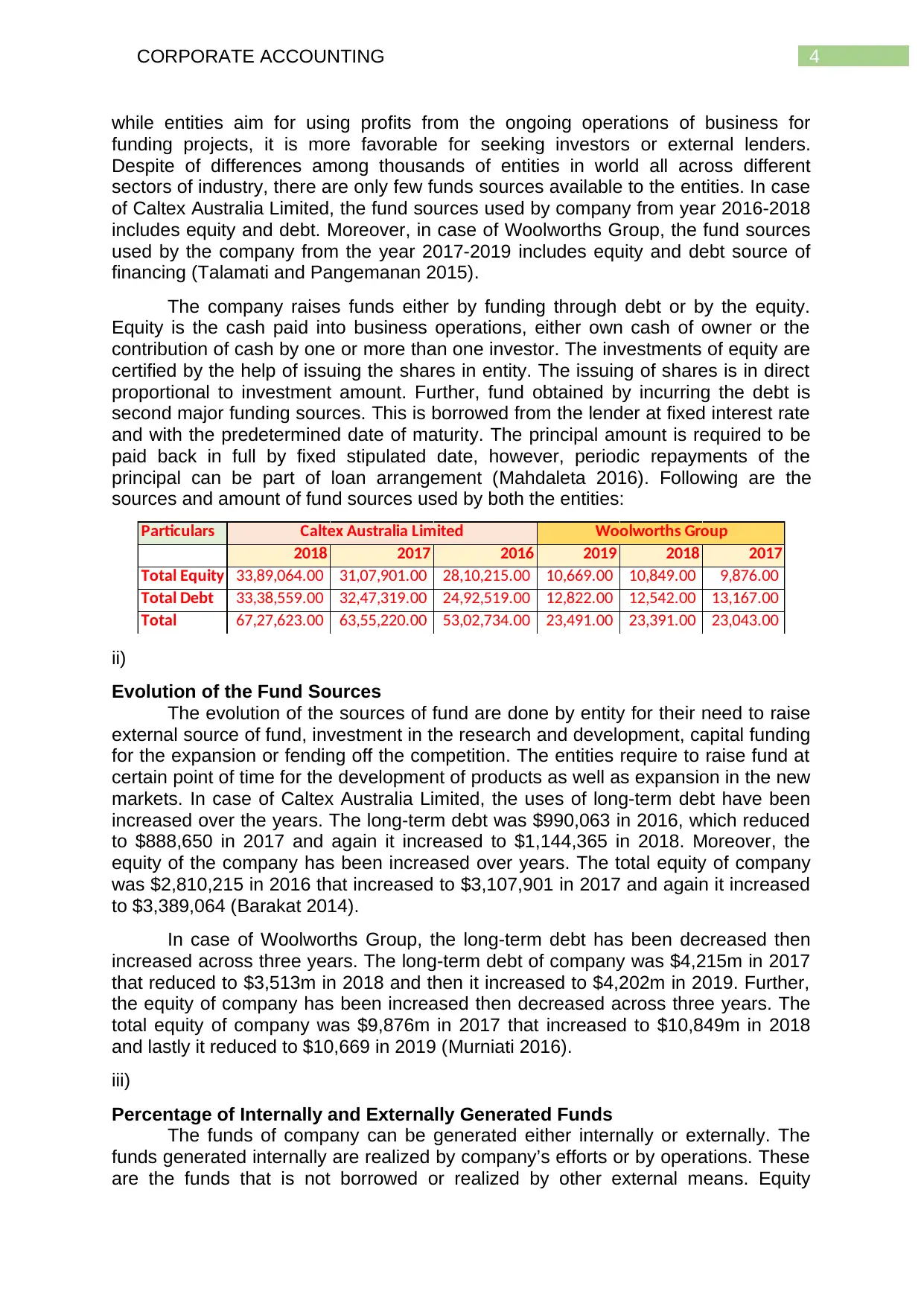

while entities aim for using profits from the ongoing operations of business for

funding projects, it is more favorable for seeking investors or external lenders.

Despite of differences among thousands of entities in world all across different

sectors of industry, there are only few funds sources available to the entities. In case

of Caltex Australia Limited, the fund sources used by company from year 2016-2018

includes equity and debt. Moreover, in case of Woolworths Group, the fund sources

used by the company from the year 2017-2019 includes equity and debt source of

financing (Talamati and Pangemanan 2015).

The company raises funds either by funding through debt or by the equity.

Equity is the cash paid into business operations, either own cash of owner or the

contribution of cash by one or more than one investor. The investments of equity are

certified by the help of issuing the shares in entity. The issuing of shares is in direct

proportional to investment amount. Further, fund obtained by incurring the debt is

second major funding sources. This is borrowed from the lender at fixed interest rate

and with the predetermined date of maturity. The principal amount is required to be

paid back in full by fixed stipulated date, however, periodic repayments of the

principal can be part of loan arrangement (Mahdaleta 2016). Following are the

sources and amount of fund sources used by both the entities:

Particulars

2018 2017 2016 2019 2018 2017

Total Equity 33,89,064.00 31,07,901.00 28,10,215.00 10,669.00 10,849.00 9,876.00

Total Debt 33,38,559.00 32,47,319.00 24,92,519.00 12,822.00 12,542.00 13,167.00

Total 67,27,623.00 63,55,220.00 53,02,734.00 23,491.00 23,391.00 23,043.00

Caltex Australia Limited Woolworths Group

ii)

Evolution of the Fund Sources

The evolution of the sources of fund are done by entity for their need to raise

external source of fund, investment in the research and development, capital funding

for the expansion or fending off the competition. The entities require to raise fund at

certain point of time for the development of products as well as expansion in the new

markets. In case of Caltex Australia Limited, the uses of long-term debt have been

increased over the years. The long-term debt was $990,063 in 2016, which reduced

to $888,650 in 2017 and again it increased to $1,144,365 in 2018. Moreover, the

equity of the company has been increased over years. The total equity of company

was $2,810,215 in 2016 that increased to $3,107,901 in 2017 and again it increased

to $3,389,064 (Barakat 2014).

In case of Woolworths Group, the long-term debt has been decreased then

increased across three years. The long-term debt of company was $4,215m in 2017

that reduced to $3,513m in 2018 and then it increased to $4,202m in 2019. Further,

the equity of company has been increased then decreased across three years. The

total equity of company was $9,876m in 2017 that increased to $10,849m in 2018

and lastly it reduced to $10,669 in 2019 (Murniati 2016).

iii)

Percentage of Internally and Externally Generated Funds

The funds of company can be generated either internally or externally. The

funds generated internally are realized by company’s efforts or by operations. These

are the funds that is not borrowed or realized by other external means. Equity

while entities aim for using profits from the ongoing operations of business for

funding projects, it is more favorable for seeking investors or external lenders.

Despite of differences among thousands of entities in world all across different

sectors of industry, there are only few funds sources available to the entities. In case

of Caltex Australia Limited, the fund sources used by company from year 2016-2018

includes equity and debt. Moreover, in case of Woolworths Group, the fund sources

used by the company from the year 2017-2019 includes equity and debt source of

financing (Talamati and Pangemanan 2015).

The company raises funds either by funding through debt or by the equity.

Equity is the cash paid into business operations, either own cash of owner or the

contribution of cash by one or more than one investor. The investments of equity are

certified by the help of issuing the shares in entity. The issuing of shares is in direct

proportional to investment amount. Further, fund obtained by incurring the debt is

second major funding sources. This is borrowed from the lender at fixed interest rate

and with the predetermined date of maturity. The principal amount is required to be

paid back in full by fixed stipulated date, however, periodic repayments of the

principal can be part of loan arrangement (Mahdaleta 2016). Following are the

sources and amount of fund sources used by both the entities:

Particulars

2018 2017 2016 2019 2018 2017

Total Equity 33,89,064.00 31,07,901.00 28,10,215.00 10,669.00 10,849.00 9,876.00

Total Debt 33,38,559.00 32,47,319.00 24,92,519.00 12,822.00 12,542.00 13,167.00

Total 67,27,623.00 63,55,220.00 53,02,734.00 23,491.00 23,391.00 23,043.00

Caltex Australia Limited Woolworths Group

ii)

Evolution of the Fund Sources

The evolution of the sources of fund are done by entity for their need to raise

external source of fund, investment in the research and development, capital funding

for the expansion or fending off the competition. The entities require to raise fund at

certain point of time for the development of products as well as expansion in the new

markets. In case of Caltex Australia Limited, the uses of long-term debt have been

increased over the years. The long-term debt was $990,063 in 2016, which reduced

to $888,650 in 2017 and again it increased to $1,144,365 in 2018. Moreover, the

equity of the company has been increased over years. The total equity of company

was $2,810,215 in 2016 that increased to $3,107,901 in 2017 and again it increased

to $3,389,064 (Barakat 2014).

In case of Woolworths Group, the long-term debt has been decreased then

increased across three years. The long-term debt of company was $4,215m in 2017

that reduced to $3,513m in 2018 and then it increased to $4,202m in 2019. Further,

the equity of company has been increased then decreased across three years. The

total equity of company was $9,876m in 2017 that increased to $10,849m in 2018

and lastly it reduced to $10,669 in 2019 (Murniati 2016).

iii)

Percentage of Internally and Externally Generated Funds

The funds of company can be generated either internally or externally. The

funds generated internally are realized by company’s efforts or by operations. These

are the funds that is not borrowed or realized by other external means. Equity

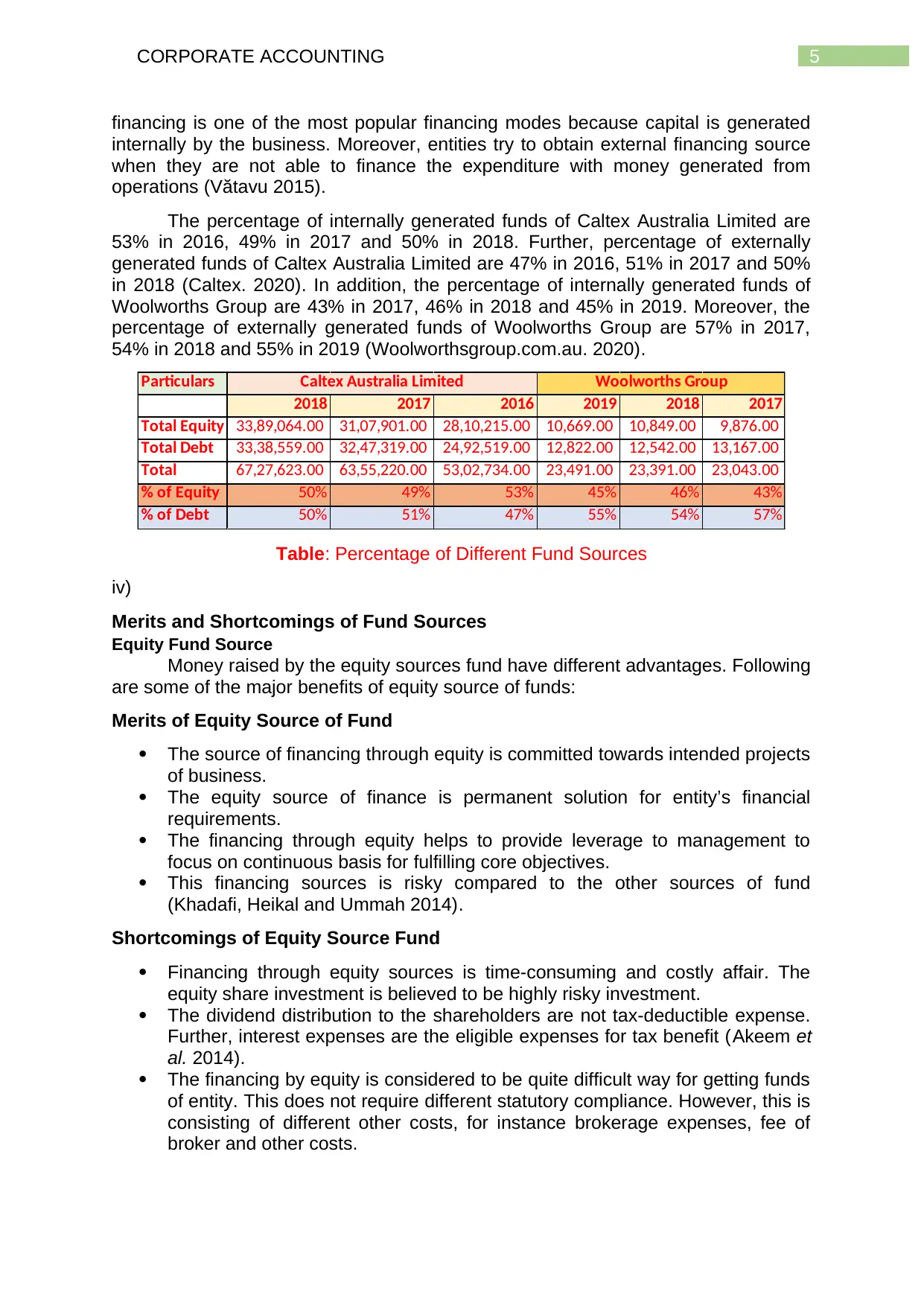

5CORPORATE ACCOUNTING

financing is one of the most popular financing modes because capital is generated

internally by the business. Moreover, entities try to obtain external financing source

when they are not able to finance the expenditure with money generated from

operations (Vătavu 2015).

The percentage of internally generated funds of Caltex Australia Limited are

53% in 2016, 49% in 2017 and 50% in 2018. Further, percentage of externally

generated funds of Caltex Australia Limited are 47% in 2016, 51% in 2017 and 50%

in 2018 (Caltex. 2020). In addition, the percentage of internally generated funds of

Woolworths Group are 43% in 2017, 46% in 2018 and 45% in 2019. Moreover, the

percentage of externally generated funds of Woolworths Group are 57% in 2017,

54% in 2018 and 55% in 2019 (Woolworthsgroup.com.au. 2020).

Particulars

2018 2017 2016 2019 2018 2017

Total Equity 33,89,064.00 31,07,901.00 28,10,215.00 10,669.00 10,849.00 9,876.00

Total Debt 33,38,559.00 32,47,319.00 24,92,519.00 12,822.00 12,542.00 13,167.00

Total 67,27,623.00 63,55,220.00 53,02,734.00 23,491.00 23,391.00 23,043.00

% of Equity 50% 49% 53% 45% 46% 43%

% of Debt 50% 51% 47% 55% 54% 57%

Caltex Australia Limited Woolworths Group

Table: Percentage of Different Fund Sources

iv)

Merits and Shortcomings of Fund Sources

Equity Fund Source

Money raised by the equity sources fund have different advantages. Following

are some of the major benefits of equity source of funds:

Merits of Equity Source of Fund

The source of financing through equity is committed towards intended projects

of business.

The equity source of finance is permanent solution for entity’s financial

requirements.

The financing through equity helps to provide leverage to management to

focus on continuous basis for fulfilling core objectives.

This financing sources is risky compared to the other sources of fund

(Khadafi, Heikal and Ummah 2014).

Shortcomings of Equity Source Fund

Financing through equity sources is time-consuming and costly affair. The

equity share investment is believed to be highly risky investment.

The dividend distribution to the shareholders are not tax-deductible expense.

Further, interest expenses are the eligible expenses for tax benefit (Akeem et

al. 2014).

The financing by equity is considered to be quite difficult way for getting funds

of entity. This does not require different statutory compliance. However, this is

consisting of different other costs, for instance brokerage expenses, fee of

broker and other costs.

financing is one of the most popular financing modes because capital is generated

internally by the business. Moreover, entities try to obtain external financing source

when they are not able to finance the expenditure with money generated from

operations (Vătavu 2015).

The percentage of internally generated funds of Caltex Australia Limited are

53% in 2016, 49% in 2017 and 50% in 2018. Further, percentage of externally

generated funds of Caltex Australia Limited are 47% in 2016, 51% in 2017 and 50%

in 2018 (Caltex. 2020). In addition, the percentage of internally generated funds of

Woolworths Group are 43% in 2017, 46% in 2018 and 45% in 2019. Moreover, the

percentage of externally generated funds of Woolworths Group are 57% in 2017,

54% in 2018 and 55% in 2019 (Woolworthsgroup.com.au. 2020).

Particulars

2018 2017 2016 2019 2018 2017

Total Equity 33,89,064.00 31,07,901.00 28,10,215.00 10,669.00 10,849.00 9,876.00

Total Debt 33,38,559.00 32,47,319.00 24,92,519.00 12,822.00 12,542.00 13,167.00

Total 67,27,623.00 63,55,220.00 53,02,734.00 23,491.00 23,391.00 23,043.00

% of Equity 50% 49% 53% 45% 46% 43%

% of Debt 50% 51% 47% 55% 54% 57%

Caltex Australia Limited Woolworths Group

Table: Percentage of Different Fund Sources

iv)

Merits and Shortcomings of Fund Sources

Equity Fund Source

Money raised by the equity sources fund have different advantages. Following

are some of the major benefits of equity source of funds:

Merits of Equity Source of Fund

The source of financing through equity is committed towards intended projects

of business.

The equity source of finance is permanent solution for entity’s financial

requirements.

The financing through equity helps to provide leverage to management to

focus on continuous basis for fulfilling core objectives.

This financing sources is risky compared to the other sources of fund

(Khadafi, Heikal and Ummah 2014).

Shortcomings of Equity Source Fund

Financing through equity sources is time-consuming and costly affair. The

equity share investment is believed to be highly risky investment.

The dividend distribution to the shareholders are not tax-deductible expense.

Further, interest expenses are the eligible expenses for tax benefit (Akeem et

al. 2014).

The financing by equity is considered to be quite difficult way for getting funds

of entity. This does not require different statutory compliance. However, this is

consisting of different other costs, for instance brokerage expenses, fee of

broker and other costs.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ACCOUNTING

It consists of various legal as well as regulatory issues for the purpose of

compliance. Hence, this is quite hectic process.

The funds raised through equity dilutes the existing shareholders control

(Rouf 2015).

Debt Fund Source

Merits of Debt Fund Source

One of the major benefits of financing through debt is maintaining complete

ownership by the entity. The benefit of maintaining ownership is to have

complete control over the decisions made on the behalf of company (Enekwe,

Agu and Nnagbogu 2014).

The next benefit of financing through debt is receiving deductions by the entity

for interest paid on debt.

The uses of debt source of the financing by company raises capital in the

flexible manner in comparison to financing through equity. This financing

source is considered to be less complicated and expensive (Einiö 2014).

Shortcomings of Debt Fund Source

Even though debt financing is having various benefits but it cannot be denied

that it is having serious shortcomings. The major shortcoming of debt

financing is that entity is obligated to pay back the borrowed principal along

with interest (de Almeida and Eid Jr 2014).

The financing through debt affect the business credit rating. The business

organization is considered to be risky if it has greater amount of debt in

comparison to equity amount.

The business that seeks debt source of finance are required to meet the

lender’s requirement of cash. This means that they require to have good

balance of cash (Dopson 2018).

v)

Liabilities shown in Balance-Sheet

In Caltex Australia Limited, total liabilities of company is classified into two

types, which includes “current liabilities” and “non-current liabilities”. Further, this is

classified into “interest bearing liabilities” and “non-interest-bearing liabilities”. The

“interest bearing liabilities” is comprised of short-term and the long-term “interest

bearing liabilities”. Moreover, “non-interest-bearing liabilities” includes “current tax

liabilities” and short-term and long-term ‘payables”, “employee benefits” and

“provisions” (Caltex. 2020).

In case of Woolworths Group, the total liabilities of entity is divided into two

categories, which includes “current liabilities” and “non-current liabilities”. The

“interest bearing liabilities” is comprised of short-term and the long-term

“borrowings”. Further, the “non-interest-bearing liabilities” includes short-term “trade

and other payables”, “current tax payable”, short-term and the long-term “other

financial liabilities”, short-term and the long-term “provisions” and “other non-current

liabilities” (Woolworthsgroup.com.au. 2020).

vi)

It consists of various legal as well as regulatory issues for the purpose of

compliance. Hence, this is quite hectic process.

The funds raised through equity dilutes the existing shareholders control

(Rouf 2015).

Debt Fund Source

Merits of Debt Fund Source

One of the major benefits of financing through debt is maintaining complete

ownership by the entity. The benefit of maintaining ownership is to have

complete control over the decisions made on the behalf of company (Enekwe,

Agu and Nnagbogu 2014).

The next benefit of financing through debt is receiving deductions by the entity

for interest paid on debt.

The uses of debt source of the financing by company raises capital in the

flexible manner in comparison to financing through equity. This financing

source is considered to be less complicated and expensive (Einiö 2014).

Shortcomings of Debt Fund Source

Even though debt financing is having various benefits but it cannot be denied

that it is having serious shortcomings. The major shortcoming of debt

financing is that entity is obligated to pay back the borrowed principal along

with interest (de Almeida and Eid Jr 2014).

The financing through debt affect the business credit rating. The business

organization is considered to be risky if it has greater amount of debt in

comparison to equity amount.

The business that seeks debt source of finance are required to meet the

lender’s requirement of cash. This means that they require to have good

balance of cash (Dopson 2018).

v)

Liabilities shown in Balance-Sheet

In Caltex Australia Limited, total liabilities of company is classified into two

types, which includes “current liabilities” and “non-current liabilities”. Further, this is

classified into “interest bearing liabilities” and “non-interest-bearing liabilities”. The

“interest bearing liabilities” is comprised of short-term and the long-term “interest

bearing liabilities”. Moreover, “non-interest-bearing liabilities” includes “current tax

liabilities” and short-term and long-term ‘payables”, “employee benefits” and

“provisions” (Caltex. 2020).

In case of Woolworths Group, the total liabilities of entity is divided into two

categories, which includes “current liabilities” and “non-current liabilities”. The

“interest bearing liabilities” is comprised of short-term and the long-term

“borrowings”. Further, the “non-interest-bearing liabilities” includes short-term “trade

and other payables”, “current tax payable”, short-term and the long-term “other

financial liabilities”, short-term and the long-term “provisions” and “other non-current

liabilities” (Woolworthsgroup.com.au. 2020).

vi)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

Key Provisions under AASB 137

The accounting standard provision of AASB 137 is having the objective for

ensuring suitable criteria of the recognition and bases of the measurement are

applied to the contingent assets, provisions and the contingent liabilities as well as

sufficient information level is disclosed in notes to enable the users to understand

nature, amount and timing. The companies are required for applying this standard in

the accounting for contingent assets, provisions and the contingent liabilities, except

for those, which results from executory contracts and also expect, in case of having

onerous contracts and those covered by other standard. Moreover, recognition of the

provision is required to done, when entity have present obligation that is result of

past events (Florina and Iulia 2015). This is probable that the outflow of resources

embodying the economic benefits will be needed to settle down obligations.

Moreover, reliable estimates are required to be done with the amount of obligations.

In case, if these conditions are not fulfilled then provision recognition will not be

done. At the end of each of the period of reporting, revision of provision is required to

be done and adjustment of this should reflect current best estimate. Further, in case

of no probability of requirement of the resource outflow embodying the economic

benefits for settling obligations, there should be reversal of provisions (Aasb.gov.au.

2020).

vii)

AASB 137 Reference in Company’s Annual Report

Both of the companies, Caltex Australia Limited and Woolworths Group has

not made any reference to the accounting standard AASB 137 but both of them have

fulfilled certain conditions of the accounting standard. In case of Caltex Australia

Limited, provision for the impairment loss is raised on the basis of risk matrix for the

expected losses of credit across categories of customer. The recognition of provision

is when there is present constructive or legal obligation as the past event result,

which can be reliably measured and there is probability that future sacrifice of the

economic benefits will be required for settle down obligations, amount or timing of

which is uncertain (Muritala 2018). Further, company discusses certain items that is

either not probable that the company will require making future payments or it will not

be possible to measure amounts of future payments such as legal and other claims,

bank guarantees and deed of the cross guarantee and the class order relief. Further,

in case of Woolworths Group, they define probability as recorded liability where there

includes uncertainty over amount or timing, which will be required to be paid but

expected amount of settlement can be estimated reliably by Group. The major

provisions held by company includes self-insured risks, employee benefits, onerous

contracts, self-insured risk and store exist costs. Moreover, company defines

contingent liabilities as potential future payments of cash but where payment

likelihood is not considered to be probable or cannot be reliably measured

(Woolworthsgroup.com.au. 2020).

viii)

Recorded Assets Categories

The assets categories of Caltex Australia Limited is classified in two major

parts, the first one is “current assets” and second one is “non-current assets”. The

“current assets” includes “cash and cash equivalents”, “receivables”, “inventories”

and “others”. Further, “non-current assets” includes “receivables”, “investment

Key Provisions under AASB 137

The accounting standard provision of AASB 137 is having the objective for

ensuring suitable criteria of the recognition and bases of the measurement are

applied to the contingent assets, provisions and the contingent liabilities as well as

sufficient information level is disclosed in notes to enable the users to understand

nature, amount and timing. The companies are required for applying this standard in

the accounting for contingent assets, provisions and the contingent liabilities, except

for those, which results from executory contracts and also expect, in case of having

onerous contracts and those covered by other standard. Moreover, recognition of the

provision is required to done, when entity have present obligation that is result of

past events (Florina and Iulia 2015). This is probable that the outflow of resources

embodying the economic benefits will be needed to settle down obligations.

Moreover, reliable estimates are required to be done with the amount of obligations.

In case, if these conditions are not fulfilled then provision recognition will not be

done. At the end of each of the period of reporting, revision of provision is required to

be done and adjustment of this should reflect current best estimate. Further, in case

of no probability of requirement of the resource outflow embodying the economic

benefits for settling obligations, there should be reversal of provisions (Aasb.gov.au.

2020).

vii)

AASB 137 Reference in Company’s Annual Report

Both of the companies, Caltex Australia Limited and Woolworths Group has

not made any reference to the accounting standard AASB 137 but both of them have

fulfilled certain conditions of the accounting standard. In case of Caltex Australia

Limited, provision for the impairment loss is raised on the basis of risk matrix for the

expected losses of credit across categories of customer. The recognition of provision

is when there is present constructive or legal obligation as the past event result,

which can be reliably measured and there is probability that future sacrifice of the

economic benefits will be required for settle down obligations, amount or timing of

which is uncertain (Muritala 2018). Further, company discusses certain items that is

either not probable that the company will require making future payments or it will not

be possible to measure amounts of future payments such as legal and other claims,

bank guarantees and deed of the cross guarantee and the class order relief. Further,

in case of Woolworths Group, they define probability as recorded liability where there

includes uncertainty over amount or timing, which will be required to be paid but

expected amount of settlement can be estimated reliably by Group. The major

provisions held by company includes self-insured risks, employee benefits, onerous

contracts, self-insured risk and store exist costs. Moreover, company defines

contingent liabilities as potential future payments of cash but where payment

likelihood is not considered to be probable or cannot be reliably measured

(Woolworthsgroup.com.au. 2020).

viii)

Recorded Assets Categories

The assets categories of Caltex Australia Limited is classified in two major

parts, the first one is “current assets” and second one is “non-current assets”. The

“current assets” includes “cash and cash equivalents”, “receivables”, “inventories”

and “others”. Further, “non-current assets” includes “receivables”, “investment

8CORPORATE ACCOUNTING

accounted for using equity method”, “intangibles”, “plant, property and equipment”,

“deferred tax assets”, “employee benefits” and “others” (Caltex. 2020).

The assets categories of Woolworths Group are divided in two types, which

are “current assets” and “non-current assets”. The “current assets” is consists of

“cash and cash equivalents”, “trade and other receivables”, “inventories” and “other

financial assets”. Further, “non-current assets” is consists of “trade and other

receivables”, “other financial assets”, “plant, property and equipment”, “intangible

assets” and “deferred tax assets” (Woolworthsgroup.com.au. 2020).

ix)

Basis of Measurement for Recorded Assets Class

In case of Caltex Australia Limited, receivable is recognized at the fair value

and it is measured at the amortized cost less the losses of impairment. Measurement

of the inventories are at lower of cost and the net realizable value. The cost is based

on principle of FIFO and it is consisting of direct labor, direct material and suitable

proportion of the fixed and variable overhead expenditure incurred in inventories

acquisition and bringing them into the existing condition and location. Goodwill arises

on subsidiaries acquisition is stated at the cost less any accumulated loss of

impairment. Acquisition of the other intangible assets are done by Group is stated at

the cost less accumulated amortization and the losses of impairment (Maas,

Schaltegger and Crutzen 2016). The amortization is charged up with consolidated

P/L statement on the straight-line method over estimated useful lives of the

intangible assets. Further, measurement of plant, property and equipment are at the

cost less to impairment losses and the accumulated depreciation. The cost is

consisting of expenditure, which is directly attributable to asset’s acquisition. The

self-constructed asset’s costs include direct labor, material costs and appropriate

production overheads proportion. The recognition of deferred tax is by using method

of balance sheet liability, amount used for the purposes of taxation and assets and

the liabilities carrying amounts for the purposes of financial reporting (Watson 2015).

The provided deferred tax amount is based on the expected manner of the

settlement or realization of the assets and liabilities carrying amount by using

enacted tax rates or substantively enacted at date of balance sheet. Lastly, the

unrealized gains that arises from the transactions with the associates and the joint

ventures are being eliminated to the extent of interest of Group in entity. The

unrealized losses that arises from the transactions with the joint ventures and

associates are eliminated in the same way as unrealized gains, however, only to the

extent that there includes no impairment evidence (Caltex. 2020).

In Woolworths Group, the recognition of trade and the other receivables are at

the fair value and the measurement of it is at amortized cost by using effective

method of interest and loss allowance. Generally, they have the terms of thirty days.

The investment of Group in the listed equity securities are designated as the

financial assets and at the fair value by other comprehensive income. The

measurement of investment is at the fair value with any recognized changes in the

other comprehensive income (Al Ani and Al Amri 2015). Further, the initial

recognition off investment in associates are at the cost consisting of costs of

transaction and it is accounted with the help of using equity method and including

profit or loss share of Group and the other associate’s comprehensive income in

investment’s carrying amount until date on which the key influence ceases. The

measurement of plant, property and equipment of Group is done at the cost less

accounted for using equity method”, “intangibles”, “plant, property and equipment”,

“deferred tax assets”, “employee benefits” and “others” (Caltex. 2020).

The assets categories of Woolworths Group are divided in two types, which

are “current assets” and “non-current assets”. The “current assets” is consists of

“cash and cash equivalents”, “trade and other receivables”, “inventories” and “other

financial assets”. Further, “non-current assets” is consists of “trade and other

receivables”, “other financial assets”, “plant, property and equipment”, “intangible

assets” and “deferred tax assets” (Woolworthsgroup.com.au. 2020).

ix)

Basis of Measurement for Recorded Assets Class

In case of Caltex Australia Limited, receivable is recognized at the fair value

and it is measured at the amortized cost less the losses of impairment. Measurement

of the inventories are at lower of cost and the net realizable value. The cost is based

on principle of FIFO and it is consisting of direct labor, direct material and suitable

proportion of the fixed and variable overhead expenditure incurred in inventories

acquisition and bringing them into the existing condition and location. Goodwill arises

on subsidiaries acquisition is stated at the cost less any accumulated loss of

impairment. Acquisition of the other intangible assets are done by Group is stated at

the cost less accumulated amortization and the losses of impairment (Maas,

Schaltegger and Crutzen 2016). The amortization is charged up with consolidated

P/L statement on the straight-line method over estimated useful lives of the

intangible assets. Further, measurement of plant, property and equipment are at the

cost less to impairment losses and the accumulated depreciation. The cost is

consisting of expenditure, which is directly attributable to asset’s acquisition. The

self-constructed asset’s costs include direct labor, material costs and appropriate

production overheads proportion. The recognition of deferred tax is by using method

of balance sheet liability, amount used for the purposes of taxation and assets and

the liabilities carrying amounts for the purposes of financial reporting (Watson 2015).

The provided deferred tax amount is based on the expected manner of the

settlement or realization of the assets and liabilities carrying amount by using

enacted tax rates or substantively enacted at date of balance sheet. Lastly, the

unrealized gains that arises from the transactions with the associates and the joint

ventures are being eliminated to the extent of interest of Group in entity. The

unrealized losses that arises from the transactions with the joint ventures and

associates are eliminated in the same way as unrealized gains, however, only to the

extent that there includes no impairment evidence (Caltex. 2020).

In Woolworths Group, the recognition of trade and the other receivables are at

the fair value and the measurement of it is at amortized cost by using effective

method of interest and loss allowance. Generally, they have the terms of thirty days.

The investment of Group in the listed equity securities are designated as the

financial assets and at the fair value by other comprehensive income. The

measurement of investment is at the fair value with any recognized changes in the

other comprehensive income (Al Ani and Al Amri 2015). Further, the initial

recognition off investment in associates are at the cost consisting of costs of

transaction and it is accounted with the help of using equity method and including

profit or loss share of Group and the other associate’s comprehensive income in

investment’s carrying amount until date on which the key influence ceases. The

measurement of plant, property and equipment of Group is done at the cost less

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE ACCOUNTING

impairment losses, amortization and depreciation. The self-constructed asset’s cost

is consisting of materials costs, overheads proportion and direct labor. The

development properties cost is consisting of holding, borrowing and costs of

development until asset is complete (Woolworthsgroup.com.au. 2020). The

depreciation of assets is based on straight-line basis over their useful lives to the

residual values. When parts of plant, property and equipment’s item have various

useful live then they account for separate assets. The goodwill of company

represents excess of the cost of acquisition over fair value of share of acquired net

identifiable assets (Watson 2015). Its measurement is done at the cost less than

any accumulated losses of impairment. Further, the measurement of other intangible

assets is at cost less impairment losses and amortization. When acquired in the

business combination, the representation of cost is at the fair value at date of

acquisition (Javed, Younas and Imran 2014).

Conclusion

Therefore, the conclusion can be reached from the analysis that both entities

are using debt and equity as their fund sources. Moreover, the long-term debt and

equity of Caltex Australia Limited has been increased over the years. In case of

Woolworths Group, the long-term debt of company has been reduced and then it has

been increased and equity of company has increased and then reduced. Further,

Caltex Australia Limited percentage of internally generated funds are 53%, 49% and

50% from 2016-2018 and percentage of externally generated funds are 47%, 51%

and 50% from 2016-2018. In addition, Woolworths Group’s percentage of internally

generated funds are 43%, 46% and 45% from 2017-2019 and percentage of

externally generated funds are 57%, 54% and 55% from 2017-2019. Further, it has

been discussed that both the debt and equity fund sources have their own merits

and shortcomings. In addition, different assets and liabilities categories as well as

AASB 137 provisions has been discussed. Both of the companies have not made

reference to this accounting standard but they have fulfilled certain conditions of the

standard. The assets class of both of the companies includes short and long-term

assets. Lastly, measurement basis for each of the assets class used by both

companies has been discussed.

impairment losses, amortization and depreciation. The self-constructed asset’s cost

is consisting of materials costs, overheads proportion and direct labor. The

development properties cost is consisting of holding, borrowing and costs of

development until asset is complete (Woolworthsgroup.com.au. 2020). The

depreciation of assets is based on straight-line basis over their useful lives to the

residual values. When parts of plant, property and equipment’s item have various

useful live then they account for separate assets. The goodwill of company

represents excess of the cost of acquisition over fair value of share of acquired net

identifiable assets (Watson 2015). Its measurement is done at the cost less than

any accumulated losses of impairment. Further, the measurement of other intangible

assets is at cost less impairment losses and amortization. When acquired in the

business combination, the representation of cost is at the fair value at date of

acquisition (Javed, Younas and Imran 2014).

Conclusion

Therefore, the conclusion can be reached from the analysis that both entities

are using debt and equity as their fund sources. Moreover, the long-term debt and

equity of Caltex Australia Limited has been increased over the years. In case of

Woolworths Group, the long-term debt of company has been reduced and then it has

been increased and equity of company has increased and then reduced. Further,

Caltex Australia Limited percentage of internally generated funds are 53%, 49% and

50% from 2016-2018 and percentage of externally generated funds are 47%, 51%

and 50% from 2016-2018. In addition, Woolworths Group’s percentage of internally

generated funds are 43%, 46% and 45% from 2017-2019 and percentage of

externally generated funds are 57%, 54% and 55% from 2017-2019. Further, it has

been discussed that both the debt and equity fund sources have their own merits

and shortcomings. In addition, different assets and liabilities categories as well as

AASB 137 provisions has been discussed. Both of the companies have not made

reference to this accounting standard but they have fulfilled certain conditions of the

standard. The assets class of both of the companies includes short and long-term

assets. Lastly, measurement basis for each of the assets class used by both

companies has been discussed.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE ACCOUNTING

Reference

Aasb.gov.au. 2020. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB137_08-15.pdf [Accessed 9

Jan. 2020].

Akeem, L.B., Terer, E.K., Kiyanjui, M.W. and Kayode, A.M., 2014. Effects of capital

structure on firm’s performance: Empirical study of manufacturing companies in

Nigeria. Journal of Finance and Investment analysis, 3(4), pp.39-57.

Al Ani, M. and Al Amri, M., 2015. The determinants of capital structure: an empirical

study of Omani listed industrial companies. Business: Theory and Practice, 16,

p.159.

Avdjiev, S., Chui, M.K. and Shin, H.S., 2014. Non-financial corporations from

emerging market economies and capital flows. BIS Quarterly Review December.

Barakat, A., 2014. The impact of financial structure, financial leverage and

profitability on industrial companies shares value (applied study on a sample of

Saudi industrial companies). Research Journal of Finance and Accounting, 5(1),

pp.55-66.

Caltex. 2020. Annual Reports & Reviews | Caltex Australia. [online] Available at:

https://www.caltex.com.au/our-company/investor-centre/annual-reports-and-reviews

[Accessed 19 Jan. 2020].

de Almeida, J.R. and Eid Jr, W., 2014. Access to finance, working capital

management and company value: Evidences from Brazilian companies listed on

BM&FBOVESPA. Journal of Business Research, 67(5), pp.924-934.

Dopson, C., 2018. New Funding sources. Fizier, 35(3), pp.14-16.

Einiö, E., 2014. R&D subsidies and company performance: Evidence from

geographic variation in government funding based on the ERDF population-density

rule. Review of Economics and Statistics, 96(4), pp.710-728.

Enekwe, C.I., Agu, C.I. and Nnagbogu, E.K., 2014. The effect of financial leverage

on financial performance: Evidence of quoted pharmaceutical companies in

Nigeria. Journal of Economics and Finance, 5(3), pp.17-25.

Florina, M. and Iulia, I.I., 2015. The Analysis of the Correlation Between the Sources

of Funding, Performance and Risk Exposure of a Company. Ovidius University

Annals, Series Economic Sciences, 15(1).

Javed, T., Younas, W. and Imran, M., 2014. Impact of capital structure on firm

performance: Evidence from Pakistani firms. International Journal of Academic

Research in Economics and Management Sciences, 3(5), p.28.

Khadafi, M., Heikal, M. and Ummah, A., 2014. Influence analysis of return on assets

(ROA), return on equity (ROE), net profit margin (NPM), debt to equity ratio (DER),

and current ratio (CR), against corporate profit growth in automotive in Indonesia

Stock Exchange. International Journal of Academic Research in Business and Social

Sciences, 4(12).

Reference

Aasb.gov.au. 2020. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB137_08-15.pdf [Accessed 9

Jan. 2020].

Akeem, L.B., Terer, E.K., Kiyanjui, M.W. and Kayode, A.M., 2014. Effects of capital

structure on firm’s performance: Empirical study of manufacturing companies in

Nigeria. Journal of Finance and Investment analysis, 3(4), pp.39-57.

Al Ani, M. and Al Amri, M., 2015. The determinants of capital structure: an empirical

study of Omani listed industrial companies. Business: Theory and Practice, 16,

p.159.

Avdjiev, S., Chui, M.K. and Shin, H.S., 2014. Non-financial corporations from

emerging market economies and capital flows. BIS Quarterly Review December.

Barakat, A., 2014. The impact of financial structure, financial leverage and

profitability on industrial companies shares value (applied study on a sample of

Saudi industrial companies). Research Journal of Finance and Accounting, 5(1),

pp.55-66.

Caltex. 2020. Annual Reports & Reviews | Caltex Australia. [online] Available at:

https://www.caltex.com.au/our-company/investor-centre/annual-reports-and-reviews

[Accessed 19 Jan. 2020].

de Almeida, J.R. and Eid Jr, W., 2014. Access to finance, working capital

management and company value: Evidences from Brazilian companies listed on

BM&FBOVESPA. Journal of Business Research, 67(5), pp.924-934.

Dopson, C., 2018. New Funding sources. Fizier, 35(3), pp.14-16.

Einiö, E., 2014. R&D subsidies and company performance: Evidence from

geographic variation in government funding based on the ERDF population-density

rule. Review of Economics and Statistics, 96(4), pp.710-728.

Enekwe, C.I., Agu, C.I. and Nnagbogu, E.K., 2014. The effect of financial leverage

on financial performance: Evidence of quoted pharmaceutical companies in

Nigeria. Journal of Economics and Finance, 5(3), pp.17-25.

Florina, M. and Iulia, I.I., 2015. The Analysis of the Correlation Between the Sources

of Funding, Performance and Risk Exposure of a Company. Ovidius University

Annals, Series Economic Sciences, 15(1).

Javed, T., Younas, W. and Imran, M., 2014. Impact of capital structure on firm

performance: Evidence from Pakistani firms. International Journal of Academic

Research in Economics and Management Sciences, 3(5), p.28.

Khadafi, M., Heikal, M. and Ummah, A., 2014. Influence analysis of return on assets

(ROA), return on equity (ROE), net profit margin (NPM), debt to equity ratio (DER),

and current ratio (CR), against corporate profit growth in automotive in Indonesia

Stock Exchange. International Journal of Academic Research in Business and Social

Sciences, 4(12).

11CORPORATE ACCOUNTING

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability

assessment, management accounting, control, and reporting. Journal of Cleaner

Production, 136, pp.237-248.

Mahdaleta, E., 2016. Effects of capital structure and profitability on corporate value

with company size as the moderating variable of manufacturing companies listed on

Indonesia Stock Exchange.

Muritala, T.A., 2018. An empirical analysis of capital structure on firms’ performance

in Nigeria. IJAME.

Murniati, S., 2016. Effect of Capital Structure, Company Size and Profitability on the

Stock Price of Food and Beverage Companies Listed on the Indonesia Stock

Exchange. Information Management and Business Review, 8(1), pp.23-29.

Rouf, D., 2015. Capital structure and firm performance of listed non-financial

companies in Bangladesh. The International Journal of Applied Economics and

Finance, 9(1), pp.25-32.

Talamati, M.R. and Pangemanan, S.S., 2015. The Effect Of Earnings Per Share

(EPS) & Return On Equity (ROE) On Stock Price Of Banking Company Listed In

Indonesia Stock Exchange (Idx) 2010-2014. Jurnal EMBA: Jurnal Riset Ekonomi,

Manajemen, Bisnis dan Akuntansi, 3(2).

Vătavu, S., 2015. The impact of capital structure on financial performance in

Romanian listed companies. Procedia Economics and Finance, 32, pp.1314-1322.

Watson, L., 2015. Corporate social responsibility research in accounting. Journal of

Accounting Literature, 34, pp.1-16.

Woolworthsgroup.com.au. 2020. [online] Available at:

https://www.woolworthsgroup.com.au/icms_docs/195582_annual-report-2019.pdf

[Accessed 19 Jan. 2020].

Woolworthsgroup.com.au. 2020. [online] Available at:

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf

[Accessed 19 Jan. 2020].

Woolworthsgroup.com.au. 2020. [online] Available at:

https://www.woolworthsgroup.com.au/icms_docs/188795_annual-report-2017.pdf

[Accessed 19 Jan. 2020].

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability

assessment, management accounting, control, and reporting. Journal of Cleaner

Production, 136, pp.237-248.

Mahdaleta, E., 2016. Effects of capital structure and profitability on corporate value

with company size as the moderating variable of manufacturing companies listed on

Indonesia Stock Exchange.

Muritala, T.A., 2018. An empirical analysis of capital structure on firms’ performance

in Nigeria. IJAME.

Murniati, S., 2016. Effect of Capital Structure, Company Size and Profitability on the

Stock Price of Food and Beverage Companies Listed on the Indonesia Stock

Exchange. Information Management and Business Review, 8(1), pp.23-29.

Rouf, D., 2015. Capital structure and firm performance of listed non-financial

companies in Bangladesh. The International Journal of Applied Economics and

Finance, 9(1), pp.25-32.

Talamati, M.R. and Pangemanan, S.S., 2015. The Effect Of Earnings Per Share

(EPS) & Return On Equity (ROE) On Stock Price Of Banking Company Listed In

Indonesia Stock Exchange (Idx) 2010-2014. Jurnal EMBA: Jurnal Riset Ekonomi,

Manajemen, Bisnis dan Akuntansi, 3(2).

Vătavu, S., 2015. The impact of capital structure on financial performance in

Romanian listed companies. Procedia Economics and Finance, 32, pp.1314-1322.

Watson, L., 2015. Corporate social responsibility research in accounting. Journal of

Accounting Literature, 34, pp.1-16.

Woolworthsgroup.com.au. 2020. [online] Available at:

https://www.woolworthsgroup.com.au/icms_docs/195582_annual-report-2019.pdf

[Accessed 19 Jan. 2020].

Woolworthsgroup.com.au. 2020. [online] Available at:

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf

[Accessed 19 Jan. 2020].

Woolworthsgroup.com.au. 2020. [online] Available at:

https://www.woolworthsgroup.com.au/icms_docs/188795_annual-report-2017.pdf

[Accessed 19 Jan. 2020].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.