Corporate Accounting 1: Cash Flow, Income Tax, and Financial Analysis

VerifiedAdded on 2021/06/16

|10

|2170

|47

Report

AI Summary

This report provides a detailed analysis of Virgin Australia's financial statements, focusing on the cash flow statement, other comprehensive income, and accounting for corporate income tax. The cash flow statement analysis covers operating, investing, and financing activities, examining key items such as staff payments, finance income, and proceeds from property, plant, and equipment. The report evaluates trends in cash flows and discusses the impact of foreign currency, cash flow hedges, and IT benefits on other comprehensive income. Furthermore, it addresses corporate income tax, deferred tax items, and tax assets, highlighting the IT benefit earned by the company and the implications of its tax treatment. The analysis references the company's annual reports from 2014 to 2017, providing a comprehensive overview of its financial performance and accounting practices. The report concludes by summarizing the surprising tax treatment for Virgin Australia and difficulties relating real IT expense paid with the prevailing tax rate of the nation.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ACCOUNTING

Table of Contents

Cash flow statement:........................................................................................................................2

Requirement (i):...........................................................................................................................2

Requirement (ii):..........................................................................................................................4

Other comprehensive income statement:.........................................................................................5

Requirement (iii):.........................................................................................................................5

Requirement (iv):.........................................................................................................................5

Requirement (v):..........................................................................................................................5

Accounting for corporate income tax:.............................................................................................6

Requirement (vi):.........................................................................................................................6

Requirement (vii):........................................................................................................................6

Requirement (viii):.......................................................................................................................6

Requirement (ix):.........................................................................................................................7

Requirement (x):..........................................................................................................................7

Requirement (xi):.........................................................................................................................7

References........................................................................................................................................8

Table of Contents

Cash flow statement:........................................................................................................................2

Requirement (i):...........................................................................................................................2

Requirement (ii):..........................................................................................................................4

Other comprehensive income statement:.........................................................................................5

Requirement (iii):.........................................................................................................................5

Requirement (iv):.........................................................................................................................5

Requirement (v):..........................................................................................................................5

Accounting for corporate income tax:.............................................................................................6

Requirement (vi):.........................................................................................................................6

Requirement (vii):........................................................................................................................6

Requirement (viii):.......................................................................................................................6

Requirement (ix):.........................................................................................................................7

Requirement (x):..........................................................................................................................7

Requirement (xi):.........................................................................................................................7

References........................................................................................................................................8

2CORPORATE ACCOUNTING

Cash flow statement:

Requirement (i):

The various considerations in the report has been included with the various types of the

discussions which are seen to be based on the annual report of Virgin Australia. It is discerned

that the company is registered in the “Australian Securities Exchange (ASX)” as “VAH”. Based

on the depictions of the cash flow statement the different categories are divided as “finance,

operating and investing” activities (Virginaustralia.com, 2018). The main categorization of the

items is discussed as follows:

Cash flows from operating activities:

The important items in this parameter has been seen to be inclusion of the various types

of the factors which are seen to be related to the payment made to the “staff, finance income

recovered and the finance cost” which are paid to the various agencies. In addition to this, the

different types of the increase in the operating cash is evident with “$5,567.40 million in 2016 to

$5,657.10 million 2017”. This has happened due to tightening of the credit policy. The staff

payment and the supplier amounts are further seen to be associated to the various type of the

factors which are associated to the items purchased on credit and salaries of the staff. With

particular reference to the company it needs to be discerned that the different factors which are

associated to the increasing trend identified with the 2017 additional purchases from the

suppliers (Penman & Yehuda, 2015). In addition to this, the depictions based on the finance

income is seen to be net outcome of the various types of the factors which are considered with

the utilisation of the money for repayment on demand at a specified point of time. This increase

is further inferred with the annual report of the 2017 about writing off of the credit sales as

Cash flow statement:

Requirement (i):

The various considerations in the report has been included with the various types of the

discussions which are seen to be based on the annual report of Virgin Australia. It is discerned

that the company is registered in the “Australian Securities Exchange (ASX)” as “VAH”. Based

on the depictions of the cash flow statement the different categories are divided as “finance,

operating and investing” activities (Virginaustralia.com, 2018). The main categorization of the

items is discussed as follows:

Cash flows from operating activities:

The important items in this parameter has been seen to be inclusion of the various types

of the factors which are seen to be related to the payment made to the “staff, finance income

recovered and the finance cost” which are paid to the various agencies. In addition to this, the

different types of the increase in the operating cash is evident with “$5,567.40 million in 2016 to

$5,657.10 million 2017”. This has happened due to tightening of the credit policy. The staff

payment and the supplier amounts are further seen to be associated to the various type of the

factors which are associated to the items purchased on credit and salaries of the staff. With

particular reference to the company it needs to be discerned that the different factors which are

associated to the increasing trend identified with the 2017 additional purchases from the

suppliers (Penman & Yehuda, 2015). In addition to this, the depictions based on the finance

income is seen to be net outcome of the various types of the factors which are considered with

the utilisation of the money for repayment on demand at a specified point of time. This increase

is further inferred with the annual report of the 2017 about writing off of the credit sales as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ACCOUNTING

uncollectible. The various costs under the finance is seen to be included with the various

obligations which are consideration with the decrease in the interest payment on the loans

undertaken (DeFusco et al., 2015).

Cash flows from investing activities:

The significant items in terms of the payments has been considered with the proceeding

from the “property, plant and equipment” and advances to deposits. In addition to this, the

payments considered for the “property, plant and equipment” are the amounts which are

necessary to conduct the business operations. On the contrary, the fixed assets are able to provide

the different types of the economic benefits which are related to the organization which needs to

be considered with the from the proceeds. It needs to be further discerned that the payments

associated to the fixed assets are vital for the business operations. It can be clearly discerned that

Virgin Australia is seen to be involved in different activities to reduce the investment in the cash

from the investing activities. It has also not able to generate sufficient amount of cash flows from

selling of items such as PPE. In addition to this, the proceeds and the payments are associated to

the financial instrument which specifies total time of repayment along with amount of interest

payable. It is further inferred that the deposits in the 2017 is considered due to the higher rate of

interest (Campbell, 2015).

Cash flows from financing activities:

The important items considered under this category is seen to be associated to the various

types of the parameters associated to the different type of the process taken from the equity

distribution, borrowings and several types of the other items. The borrowing have been further

able to signify the various types of the factors which are taken into account on behalf of the

uncollectible. The various costs under the finance is seen to be included with the various

obligations which are consideration with the decrease in the interest payment on the loans

undertaken (DeFusco et al., 2015).

Cash flows from investing activities:

The significant items in terms of the payments has been considered with the proceeding

from the “property, plant and equipment” and advances to deposits. In addition to this, the

payments considered for the “property, plant and equipment” are the amounts which are

necessary to conduct the business operations. On the contrary, the fixed assets are able to provide

the different types of the economic benefits which are related to the organization which needs to

be considered with the from the proceeds. It needs to be further discerned that the payments

associated to the fixed assets are vital for the business operations. It can be clearly discerned that

Virgin Australia is seen to be involved in different activities to reduce the investment in the cash

from the investing activities. It has also not able to generate sufficient amount of cash flows from

selling of items such as PPE. In addition to this, the proceeds and the payments are associated to

the financial instrument which specifies total time of repayment along with amount of interest

payable. It is further inferred that the deposits in the 2017 is considered due to the higher rate of

interest (Campbell, 2015).

Cash flows from financing activities:

The important items considered under this category is seen to be associated to the various

types of the parameters associated to the different type of the process taken from the equity

distribution, borrowings and several types of the other items. The borrowing have been further

able to signify the various types of the factors which are taken into account on behalf of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ACCOUNTING

lenders as per the loan agreement. It needs to be also discerned that the various types of the

observations from the annual report of the company has suggested on the proceeds which has

decreased in the FY 2017. In the same year an increase in the repayment of the borrowings is

evident. The various types of the discussions as per the equity distributions needs to be taken into

account with the shareholders of the organization. The total amount of the cash from the

financing activities are seen to be based on a declining trend as the main emphasis has been paid

on maximising the retained earnings (Robinson et al., 2015).

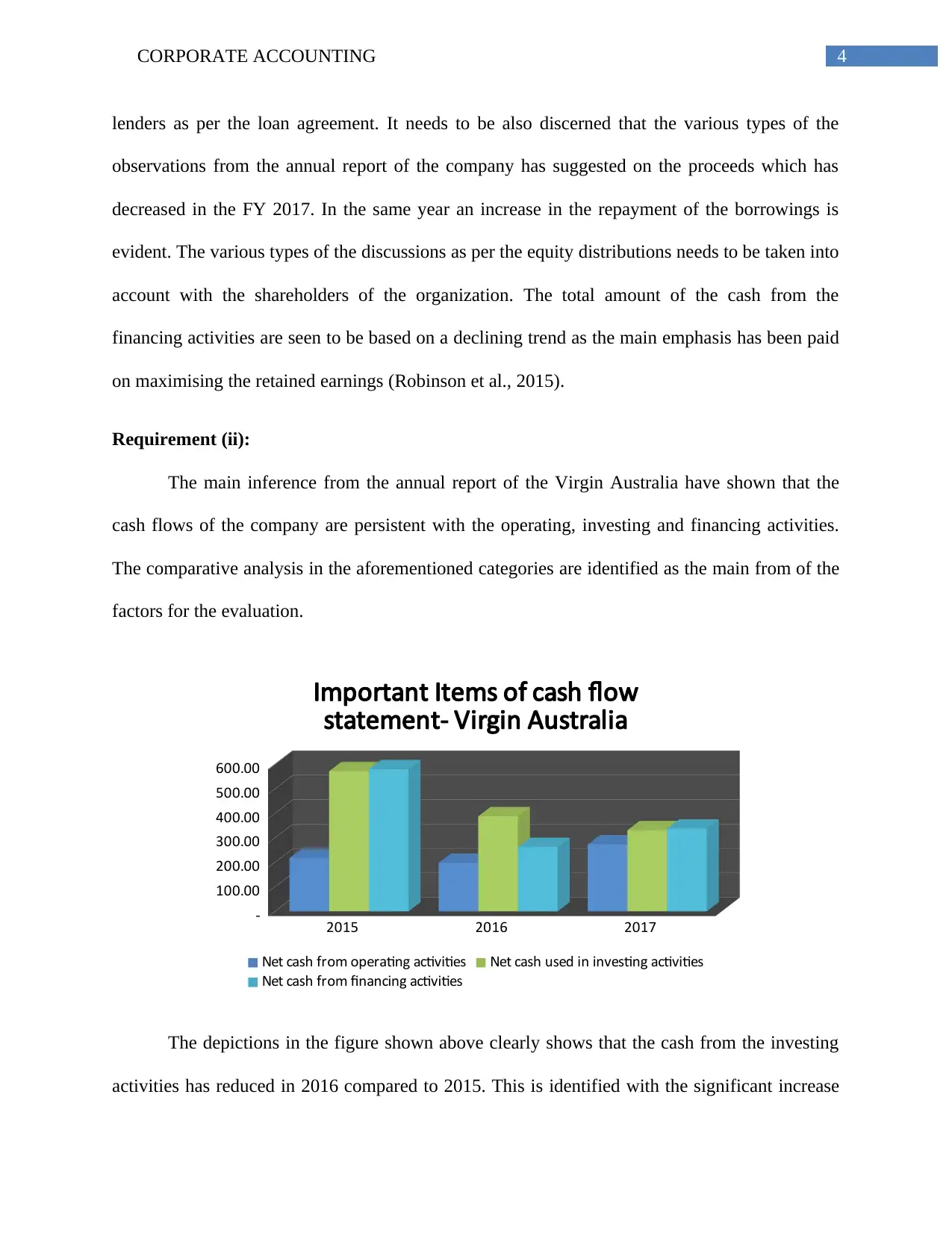

Requirement (ii):

The main inference from the annual report of the Virgin Australia have shown that the

cash flows of the company are persistent with the operating, investing and financing activities.

The comparative analysis in the aforementioned categories are identified as the main from of the

factors for the evaluation.

2015 2016 2017

-

100.00

200.00

300.00

400.00

500.00

600.00

Important Items of cash flow

statement- Virgin Australia

Net cash from operating activities Net cash used in investing activities

Net cash from financing activities

The depictions in the figure shown above clearly shows that the cash from the investing

activities has reduced in 2016 compared to 2015. This is identified with the significant increase

lenders as per the loan agreement. It needs to be also discerned that the various types of the

observations from the annual report of the company has suggested on the proceeds which has

decreased in the FY 2017. In the same year an increase in the repayment of the borrowings is

evident. The various types of the discussions as per the equity distributions needs to be taken into

account with the shareholders of the organization. The total amount of the cash from the

financing activities are seen to be based on a declining trend as the main emphasis has been paid

on maximising the retained earnings (Robinson et al., 2015).

Requirement (ii):

The main inference from the annual report of the Virgin Australia have shown that the

cash flows of the company are persistent with the operating, investing and financing activities.

The comparative analysis in the aforementioned categories are identified as the main from of the

factors for the evaluation.

2015 2016 2017

-

100.00

200.00

300.00

400.00

500.00

600.00

Important Items of cash flow

statement- Virgin Australia

Net cash from operating activities Net cash used in investing activities

Net cash from financing activities

The depictions in the figure shown above clearly shows that the cash from the investing

activities has reduced in 2016 compared to 2015. This is identified with the significant increase

5CORPORATE ACCOUNTING

in the observations taken in 2017 pertaining to higher amount of finance income and customer.

The net cash used in the investing activities are considered with a declining trend over the period

of three years. This has occurred due to reduction in the decreasing investment pertaining to

PPE. Moreover, the cash which is earned from the financing activities are due from the net

proceeds issuance of shares in 2017. Due to this, the main form of the increase in the cash and

cash equivalent units of the company in FY 2017 (Miao, Teoh & Zhu, 2016).

Other comprehensive income statement:

Requirement (iii):

The discourse of the annual report of the company is seen to be considered with the

various depiction which is comprising of the cash flow hedges, currency translation reserve and

IT benefits or expenditures (Virginaustralia.com, 2018).

Requirement (iv):

The application of the foreign currency is seen to e based on the several types o the

factors which are related to the conversion of the outcomes of the subsidiaries taken from the

parent firm to the reporting currency. In addition to this, the use of the cash flow hedge reserve

has reduced the overall exposure of the firm for the variations pertaining to the risk of the

interest rate and floating rate. On the contrary, the IT expense are seen to be based on the

significant consideration taken into account with the PBT of the company (Grant, 2016).

Requirement (v):

The elaborated view of the net income has been conducive in stating the various types of

the assumptions which are taken into consideration with the other comprehensive income. The

airliner is depicted to be providing the necessary information on the values which are seen to be

in the observations taken in 2017 pertaining to higher amount of finance income and customer.

The net cash used in the investing activities are considered with a declining trend over the period

of three years. This has occurred due to reduction in the decreasing investment pertaining to

PPE. Moreover, the cash which is earned from the financing activities are due from the net

proceeds issuance of shares in 2017. Due to this, the main form of the increase in the cash and

cash equivalent units of the company in FY 2017 (Miao, Teoh & Zhu, 2016).

Other comprehensive income statement:

Requirement (iii):

The discourse of the annual report of the company is seen to be considered with the

various depiction which is comprising of the cash flow hedges, currency translation reserve and

IT benefits or expenditures (Virginaustralia.com, 2018).

Requirement (iv):

The application of the foreign currency is seen to e based on the several types o the

factors which are related to the conversion of the outcomes of the subsidiaries taken from the

parent firm to the reporting currency. In addition to this, the use of the cash flow hedge reserve

has reduced the overall exposure of the firm for the variations pertaining to the risk of the

interest rate and floating rate. On the contrary, the IT expense are seen to be based on the

significant consideration taken into account with the PBT of the company (Grant, 2016).

Requirement (v):

The elaborated view of the net income has been conducive in stating the various types of

the assumptions which are taken into consideration with the other comprehensive income. The

airliner is depicted to be providing the necessary information on the values which are seen to be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ACCOUNTING

mentioned in the above items. It is also discerned with various type the consideration of the

items is seen to be based on the significant nature of the discourse which are related to the

various types of the assumptions taken into account with the holistic overview of the cost drivers

related to the operations. These are further seen to be excluded from the disclosure in the income

statement (Virginaustralia.com, 2018).

Accounting for corporate income tax:

Requirement (vi):

The tax expense is discerned in form of the sources such as “federal, municipal and state

governments”. The airliner has not incurred any tax expense, instead procured IT benefit in 2016

and 2017.

Requirement (vii):

The several types of the understanding of the balance sheet have shown the total amount

of LBIT in both 2016 and 2017. The annual report has further shown the total tax rate of 30% on

the PBIT. However, it not possible to identify the tax expense of the airline as 30% tax rate on

PBIT is suggested in the income statement (Virginaustralia.com, 2018).

Requirement (viii):

The items under the differed tax items are seen to be based on the prepayments of the

taxes on the financial assets. The deferred tax of Virgin Australia has seen with “$1,017.6

million in 2017, which were $857.9 million in 2016”. The deferred tax liabilities are depicted

with “$463.4 million in 2017 compared to $434.4 million in 2016” (Virginaustralia.com, 2018).

mentioned in the above items. It is also discerned with various type the consideration of the

items is seen to be based on the significant nature of the discourse which are related to the

various types of the assumptions taken into account with the holistic overview of the cost drivers

related to the operations. These are further seen to be excluded from the disclosure in the income

statement (Virginaustralia.com, 2018).

Accounting for corporate income tax:

Requirement (vi):

The tax expense is discerned in form of the sources such as “federal, municipal and state

governments”. The airliner has not incurred any tax expense, instead procured IT benefit in 2016

and 2017.

Requirement (vii):

The several types of the understanding of the balance sheet have shown the total amount

of LBIT in both 2016 and 2017. The annual report has further shown the total tax rate of 30% on

the PBIT. However, it not possible to identify the tax expense of the airline as 30% tax rate on

PBIT is suggested in the income statement (Virginaustralia.com, 2018).

Requirement (viii):

The items under the differed tax items are seen to be based on the prepayments of the

taxes on the financial assets. The deferred tax of Virgin Australia has seen with “$1,017.6

million in 2017, which were $857.9 million in 2016”. The deferred tax liabilities are depicted

with “$463.4 million in 2017 compared to $434.4 million in 2016” (Virginaustralia.com, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

Requirement (ix):

The main depiction on this category from the annual repot of the company is able to

evaluate the current tax assets which comprises of the expected tax payables or receivable over

the IT loss or gain over a certain period of time. Virgin Australia has earned IT benefit of

“$201.9 million 2016” and “$103.8 million in 2017”. These items are duly included in the

representation of the financial information in the “reconciliation of net loss to net cash from

operations” (Virginaustralia.com, 2018).

Requirement (x):

The significant depictions of the information from the annual report it has been able to

state that the organization has not sustained any IT expense in 2016 and 2017. The earned IT

benefit is main rationale for company’s non-payment of IT included in the cash flow statement

(Virginaustralia.com, 2018).

Requirement (xi):

The vital assertions of the tax treatment for Virgin Australia is seen as a surprising

element which have showed that the company suffered significant amount of loss before IT

expense in both 2016 and 2016. Due to this, the company has earned IT benefit. It is further

difficult for the company to relate the real IT expense paid with the prevailing tax rate of the

nation. Moreover, there is not mention of the IT paid in the cash flow statement of the annual

report (Virginaustralia.com, 2018).

Requirement (ix):

The main depiction on this category from the annual repot of the company is able to

evaluate the current tax assets which comprises of the expected tax payables or receivable over

the IT loss or gain over a certain period of time. Virgin Australia has earned IT benefit of

“$201.9 million 2016” and “$103.8 million in 2017”. These items are duly included in the

representation of the financial information in the “reconciliation of net loss to net cash from

operations” (Virginaustralia.com, 2018).

Requirement (x):

The significant depictions of the information from the annual report it has been able to

state that the organization has not sustained any IT expense in 2016 and 2017. The earned IT

benefit is main rationale for company’s non-payment of IT included in the cash flow statement

(Virginaustralia.com, 2018).

Requirement (xi):

The vital assertions of the tax treatment for Virgin Australia is seen as a surprising

element which have showed that the company suffered significant amount of loss before IT

expense in both 2016 and 2016. Due to this, the company has earned IT benefit. It is further

difficult for the company to relate the real IT expense paid with the prevailing tax rate of the

nation. Moreover, there is not mention of the IT paid in the cash flow statement of the annual

report (Virginaustralia.com, 2018).

8CORPORATE ACCOUNTING

References

Campbell, J. L. (2015). The fair value of cash flow hedges, future profitability, and stock

returns. Contemporary Accounting Research, 32(1), 243-279.

DeFusco, R. A., McLeavey, D. W., Pinto, J. E., Anson, M. J., & Runkle, D. E.

(2015). Quantitative investment analysis. John Wiley & Sons.

Grant, R. M. (2016). Contemporary strategy analysis: Text and cases edition. John Wiley &

Sons.

Miao, B., Teoh, S. H., & Zhu, Z. (2016). Limited attention, statement of cash flow disclosure,

and the valuation of accruals. Review of Accounting Studies, 21(2), 473-515.

Penman, S. H., & Yehuda, N. (2015). A matter of principle: Accounting reports convey both

cash-flow news and discount-rate news.

Robinson, T. R., Henry, E., Pirie, W. L., & Broihahn, M. A. (2015). International financial

statement analysis. John Wiley & Sons.

Virginaustralia.com. (2018). [online] Available at:

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/

webcontent/~edisp/2017-annual-report.pdf [Accessed 20 May 2018].

Virginaustralia.com. (2018). [online] Available at:

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/

webcontent/~edisp/2016-annual-report.pdf [Accessed 20 May 2018].

References

Campbell, J. L. (2015). The fair value of cash flow hedges, future profitability, and stock

returns. Contemporary Accounting Research, 32(1), 243-279.

DeFusco, R. A., McLeavey, D. W., Pinto, J. E., Anson, M. J., & Runkle, D. E.

(2015). Quantitative investment analysis. John Wiley & Sons.

Grant, R. M. (2016). Contemporary strategy analysis: Text and cases edition. John Wiley &

Sons.

Miao, B., Teoh, S. H., & Zhu, Z. (2016). Limited attention, statement of cash flow disclosure,

and the valuation of accruals. Review of Accounting Studies, 21(2), 473-515.

Penman, S. H., & Yehuda, N. (2015). A matter of principle: Accounting reports convey both

cash-flow news and discount-rate news.

Robinson, T. R., Henry, E., Pirie, W. L., & Broihahn, M. A. (2015). International financial

statement analysis. John Wiley & Sons.

Virginaustralia.com. (2018). [online] Available at:

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/

webcontent/~edisp/2017-annual-report.pdf [Accessed 20 May 2018].

Virginaustralia.com. (2018). [online] Available at:

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/

webcontent/~edisp/2016-annual-report.pdf [Accessed 20 May 2018].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE ACCOUNTING

Virginaustralia.com. (2018). [online] Available at:

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/

webcontent/~edisp/2015-annual-report.pdf [Accessed 20 May 2018].

Virginaustralia.com. (2018). [online] Available at:

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/

webcontent/~edisp/2014-annual-report.pdf [Accessed 20 May 2018].

Virginaustralia.com. (2018). Retrieved from

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/

webcontent/~edisp/2017-annual-report.pdf

Virginaustralia.com. (2018). [online] Available at:

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/

webcontent/~edisp/2015-annual-report.pdf [Accessed 20 May 2018].

Virginaustralia.com. (2018). [online] Available at:

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/

webcontent/~edisp/2014-annual-report.pdf [Accessed 20 May 2018].

Virginaustralia.com. (2018). Retrieved from

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/

webcontent/~edisp/2017-annual-report.pdf

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.