Corporate Accounting Report: Acquisition Analysis and Goodwill Methods

VerifiedAdded on 2022/08/20

|9

|765

|15

Report

AI Summary

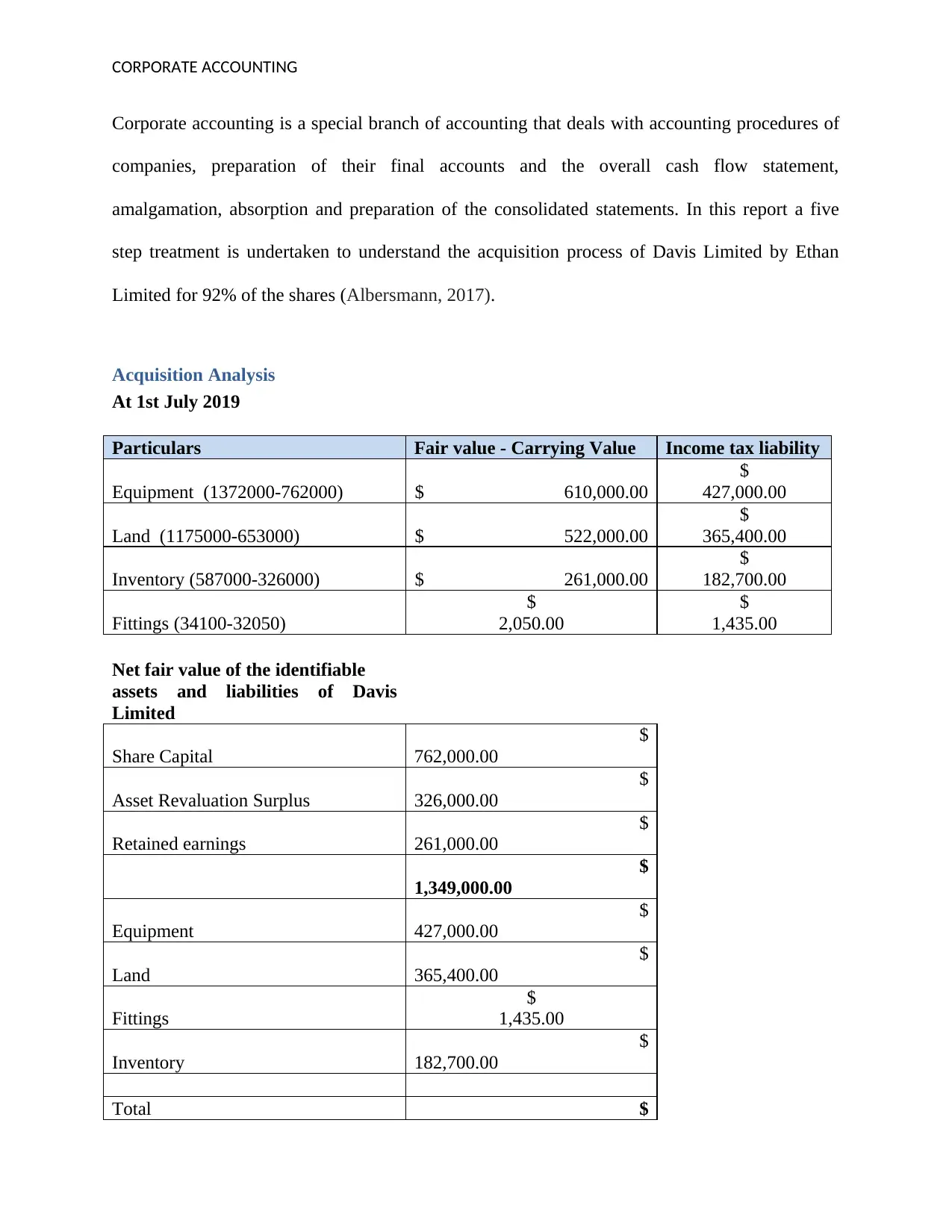

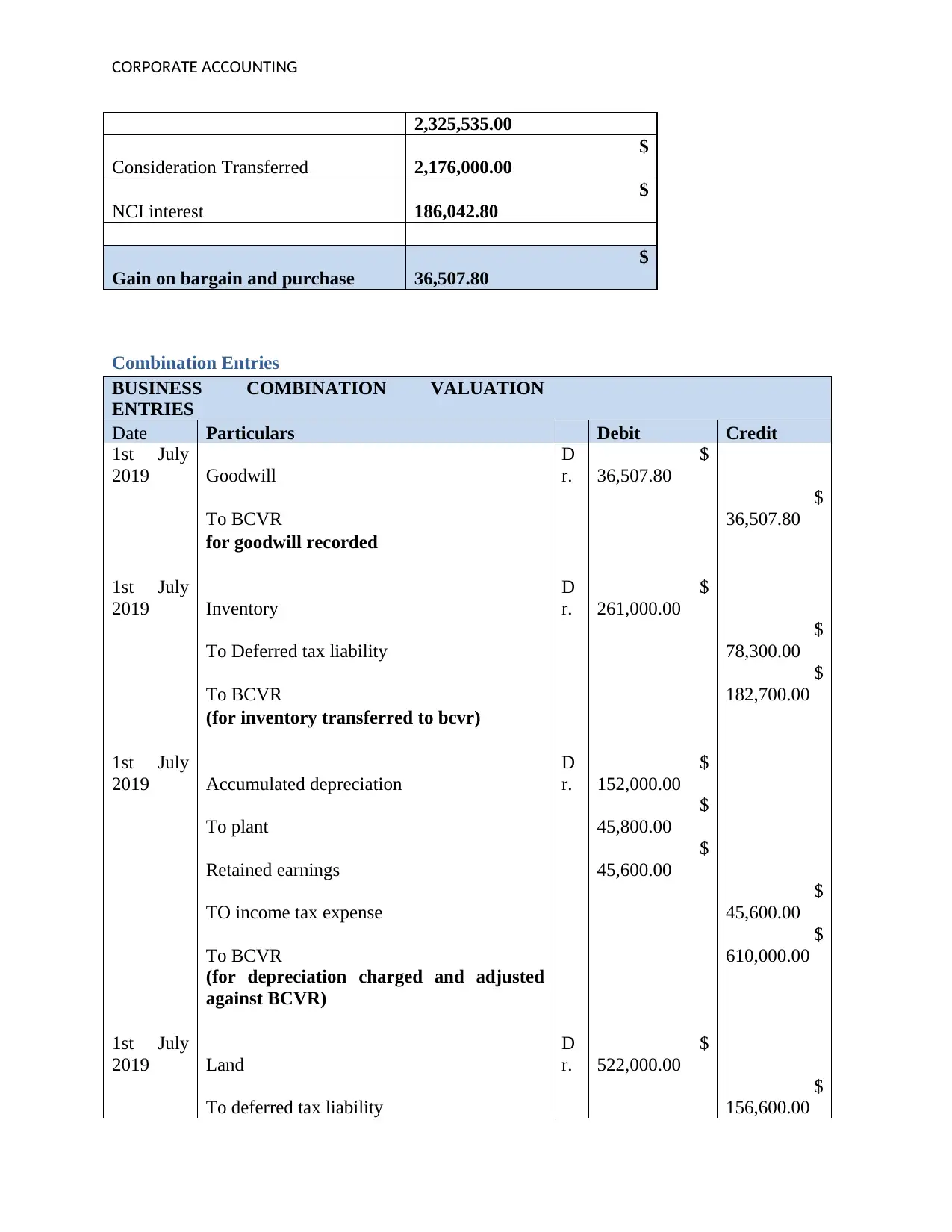

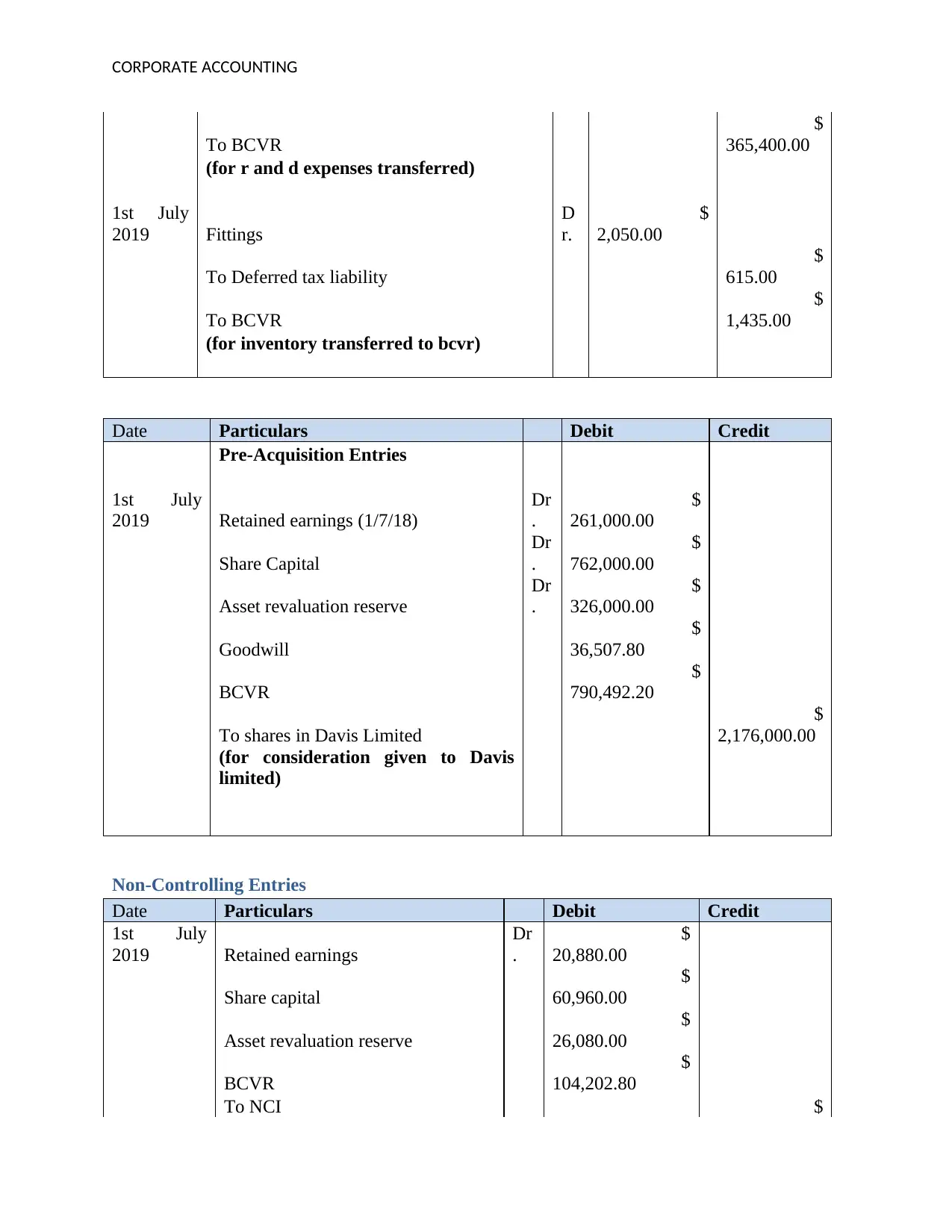

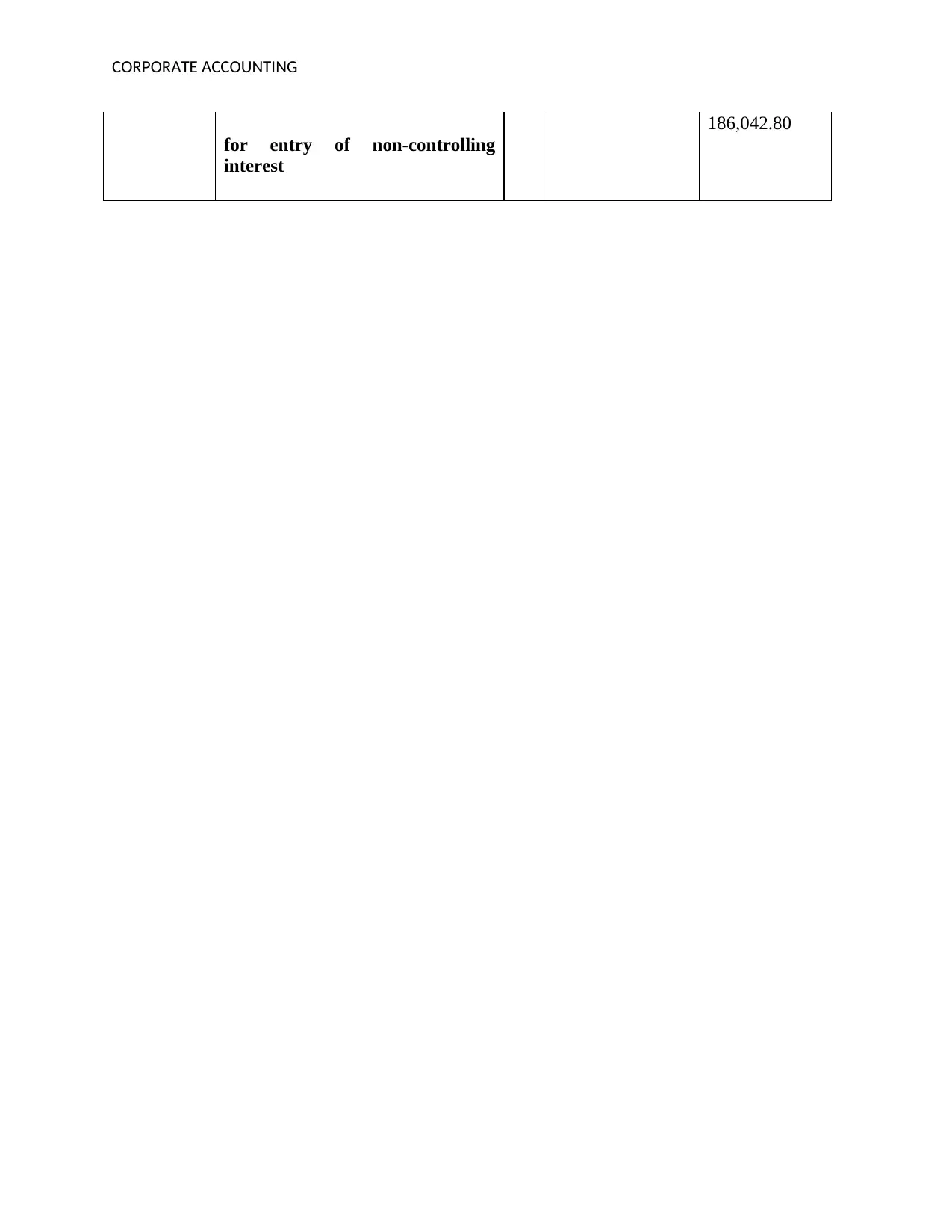

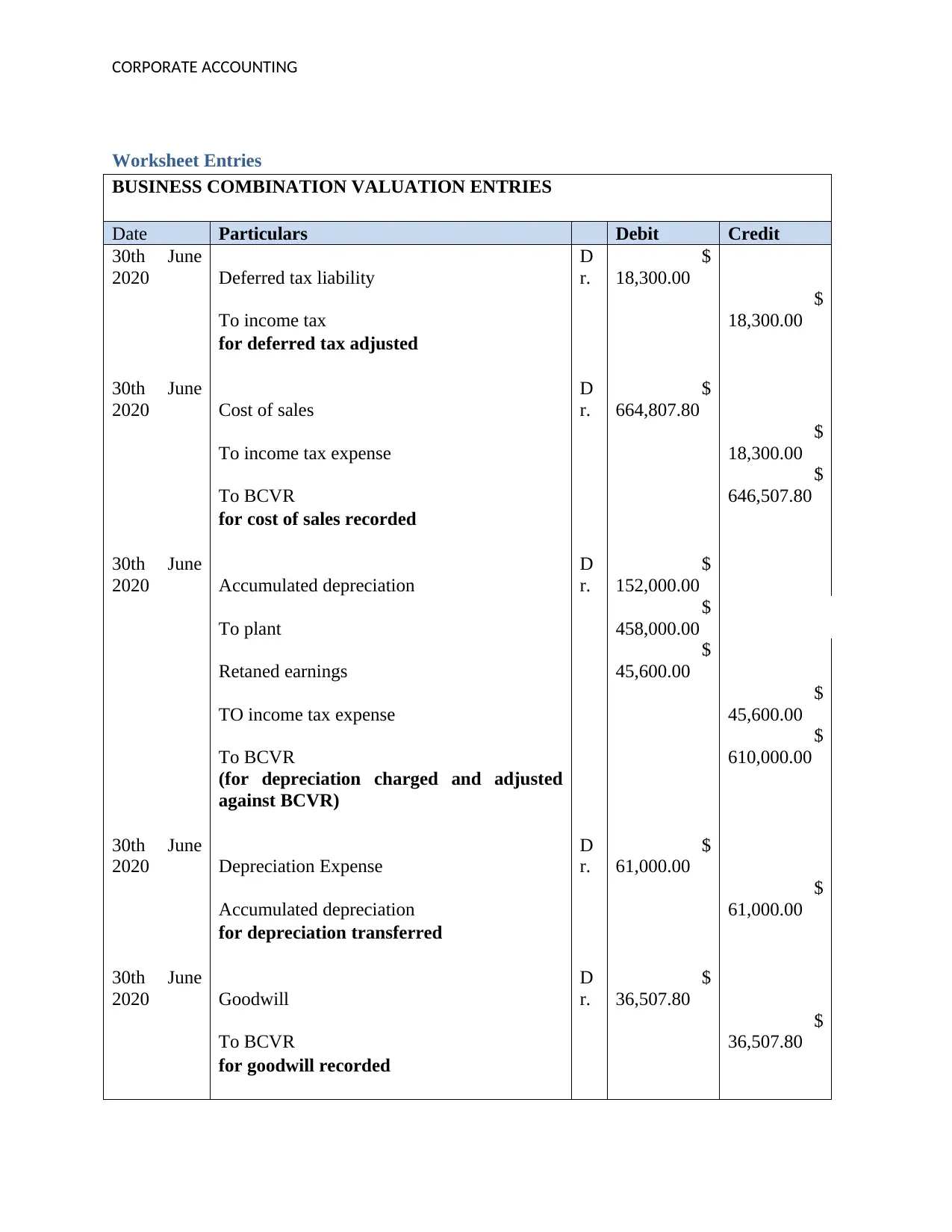

This report delves into the intricacies of corporate accounting, using the acquisition of Davis Limited by Ethan Limited as a case study. It provides a detailed five-step analysis of the acquisition process, including the valuation of assets and liabilities at fair value. The report meticulously outlines the combination entries, non-controlling entries, and worksheet entries necessary to account for the acquisition. Furthermore, it explains the full goodwill method and its implications. The analysis includes the calculation of goodwill and non-controlling interest, offering a comprehensive understanding of the accounting procedures involved in business combinations. The report also references relevant accounting standards and provides insights into the practical application of these principles.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.