Corporate Accounting Analysis: Wesfarmers Financial Statements Report

VerifiedAdded on 2021/06/18

|12

|2835

|54

Report

AI Summary

This report provides a comprehensive analysis of corporate accounting principles, focusing on the financial statements of Wesfarmers. It begins with an examination of the cash flow statement, breaking down operating, investing, and financing activities, and offering a comparative analysis of cash flow categories. The report then delves into the other comprehensive income statement, highlighting key items like foreign currency translation reserve, cash flow hedge reserve, and retained earnings. Furthermore, the analysis covers accounting for corporate income tax, including a comparison of reported and standard taxation expenses, deferred tax assets and liabilities, income tax payable, and the differences between tax expenses in the income statement and cash flow statement. The report utilizes Wesfarmers' annual reports to illustrate the application of accounting concepts and provides insights into the company's financial performance and tax strategies.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student

Name of the University

Author’s Note

Corporate Accounting

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ACCOUNTING

Table of Contents

Cash Flow Statement.......................................................................................................................2

Requirement [i]............................................................................................................................2

Requirement [ii]...........................................................................................................................4

Other Comprehensive Income Statement........................................................................................5

Requirement [iii]..........................................................................................................................5

Requirement [iv]..........................................................................................................................5

Requirement [v]...........................................................................................................................6

Accounting for Corporate Income Tax............................................................................................6

Requirement [vi]..........................................................................................................................6

Requirement [vii].........................................................................................................................7

Requirement [viii]........................................................................................................................8

Requirement [ix]..........................................................................................................................8

Requirement [x]...........................................................................................................................9

Requirement [xi]..........................................................................................................................9

References......................................................................................................................................10

Table of Contents

Cash Flow Statement.......................................................................................................................2

Requirement [i]............................................................................................................................2

Requirement [ii]...........................................................................................................................4

Other Comprehensive Income Statement........................................................................................5

Requirement [iii]..........................................................................................................................5

Requirement [iv]..........................................................................................................................5

Requirement [v]...........................................................................................................................6

Accounting for Corporate Income Tax............................................................................................6

Requirement [vi]..........................................................................................................................6

Requirement [vii].........................................................................................................................7

Requirement [viii]........................................................................................................................8

Requirement [ix]..........................................................................................................................8

Requirement [x]...........................................................................................................................9

Requirement [xi]..........................................................................................................................9

References......................................................................................................................................10

2CORPORATE ACCOUNTING

Cash Flow Statement

Requirement [i]

The cash flow statements is considered as a major financial statements that depicts the

major changes in the accounts of balance sheet and income that affect the cash and cash

equivalent of the companies.

Cash Flow from Operating Activities: In Wesfarmers, the major items under Operating

Activities are receipts from the customers, payment to the suppliers, interest received, borrowing

cost and many others. Receipts from the customers refer to the sales proceeds that Wesfarmers

receives from credit sales (Reid and Myddelton 2017).

There is an increase in these receipts in Wesfarmers that is from $74,042 million to

$71,157 million in 2017. Payment to the suppliers refer to the amount that Wesfarmers is

required to pay for their credit purchase; and it has also increased from $66.671 million to

$68,713 million due to increase in purchase (wesfarmers.com.au 2018). Interest received refers

to the amount that Wesfarmers receives from various investments in their company and others.

As a result of the write off of a certain bad debt, there is a decrease in the interest received in

Wesfarmers in 2017 that is $83 million as compared to $131 million in 2016. Borrowing costs

refers to the charges that Wesfarmers has to pay for debt covenant, finance fees and the payment

of interests. There is a decrease in this expense in 2017 from $288 million to $234 million

(wesfarmers.com.au 2018).

Cash Flow from Investing Activities: The most crucial items under Financing Activities of

Wesfarmers are both the payments and proceeds from property, plant, equipment and

Cash Flow Statement

Requirement [i]

The cash flow statements is considered as a major financial statements that depicts the

major changes in the accounts of balance sheet and income that affect the cash and cash

equivalent of the companies.

Cash Flow from Operating Activities: In Wesfarmers, the major items under Operating

Activities are receipts from the customers, payment to the suppliers, interest received, borrowing

cost and many others. Receipts from the customers refer to the sales proceeds that Wesfarmers

receives from credit sales (Reid and Myddelton 2017).

There is an increase in these receipts in Wesfarmers that is from $74,042 million to

$71,157 million in 2017. Payment to the suppliers refer to the amount that Wesfarmers is

required to pay for their credit purchase; and it has also increased from $66.671 million to

$68,713 million due to increase in purchase (wesfarmers.com.au 2018). Interest received refers

to the amount that Wesfarmers receives from various investments in their company and others.

As a result of the write off of a certain bad debt, there is a decrease in the interest received in

Wesfarmers in 2017 that is $83 million as compared to $131 million in 2016. Borrowing costs

refers to the charges that Wesfarmers has to pay for debt covenant, finance fees and the payment

of interests. There is a decrease in this expense in 2017 from $288 million to $234 million

(wesfarmers.com.au 2018).

Cash Flow from Investing Activities: The most crucial items under Financing Activities of

Wesfarmers are both the payments and proceeds from property, plant, equipment and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ACCOUNTING

intangibles; proceeds from sales of businesses and associates; investment in associates and joint

ventures; acquisition of subsidiaries and redemption of loan notes.

The payment for property, plant, equipment and intangible assets refers to the amount

that Wesfarmers is required to pay for the acquisition and purchase of these items. At the same

time, proceeds from these items refer to the monetary benefits received by Wesfarmers by using

these items. As per the cash flow statement, Wesfarmers has reduced their investment in these

items from $1,899 in 2016 to $1,681 in 2017. On the other hand, there is an increase in the

proceeds from $563 million in 2016 to $653 million in 2017 due to sales of these assets.

Wesfarmers realizes the sold or purchased long-term assets as proceeds and investment

respectively (wesfarmers.com.au 2018). In the year 2017, Wesfarmers has gained major

proceeds from sales of businesses. However, the investment remains stagnant in both 2017 and

2016. In Wesfarmers, loan notes refers to a specific financial instrument that puts the obligation

on Wesfarmers to repay the loan along with the interests. Wesfarmers has become able to redeem

$54 milling of loan in the year 2017 (wesfarmers.com.au 2018).

Cash Flow from Financing Activities: The crucial items under Financing Activities of

Wesfarmers are proceeds from borrowing, payment from borrowing and the payment of equity

dividend (Miloš and Jovan 2013).

Borrowing refers to the total disbursed amount that the lenders provide to the borrower

under a specific loan covenant. Due to the extension of the loan terms to the debtors, Wesfarmers

has registers a massive fall in the proceeds from borrowings that is $220 million in 2017 from

$2,360 million in 2016. Moreover, Wesfarmers had to pay large amount to the banks for the

repayment of loans. Equity dividend refers to the yearly cash flow that is provided to the

intangibles; proceeds from sales of businesses and associates; investment in associates and joint

ventures; acquisition of subsidiaries and redemption of loan notes.

The payment for property, plant, equipment and intangible assets refers to the amount

that Wesfarmers is required to pay for the acquisition and purchase of these items. At the same

time, proceeds from these items refer to the monetary benefits received by Wesfarmers by using

these items. As per the cash flow statement, Wesfarmers has reduced their investment in these

items from $1,899 in 2016 to $1,681 in 2017. On the other hand, there is an increase in the

proceeds from $563 million in 2016 to $653 million in 2017 due to sales of these assets.

Wesfarmers realizes the sold or purchased long-term assets as proceeds and investment

respectively (wesfarmers.com.au 2018). In the year 2017, Wesfarmers has gained major

proceeds from sales of businesses. However, the investment remains stagnant in both 2017 and

2016. In Wesfarmers, loan notes refers to a specific financial instrument that puts the obligation

on Wesfarmers to repay the loan along with the interests. Wesfarmers has become able to redeem

$54 milling of loan in the year 2017 (wesfarmers.com.au 2018).

Cash Flow from Financing Activities: The crucial items under Financing Activities of

Wesfarmers are proceeds from borrowing, payment from borrowing and the payment of equity

dividend (Miloš and Jovan 2013).

Borrowing refers to the total disbursed amount that the lenders provide to the borrower

under a specific loan covenant. Due to the extension of the loan terms to the debtors, Wesfarmers

has registers a massive fall in the proceeds from borrowings that is $220 million in 2017 from

$2,360 million in 2016. Moreover, Wesfarmers had to pay large amount to the banks for the

repayment of loans. Equity dividend refers to the yearly cash flow that is provided to the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ACCOUNTING

shareholders of Wesfarmers. Due to the focus on the increase in retained earnings, Wesfarmers

has paid less dividend in 2017 as compared to 2016 (wesfarmers.com.au 2018).

Requirement [ii]

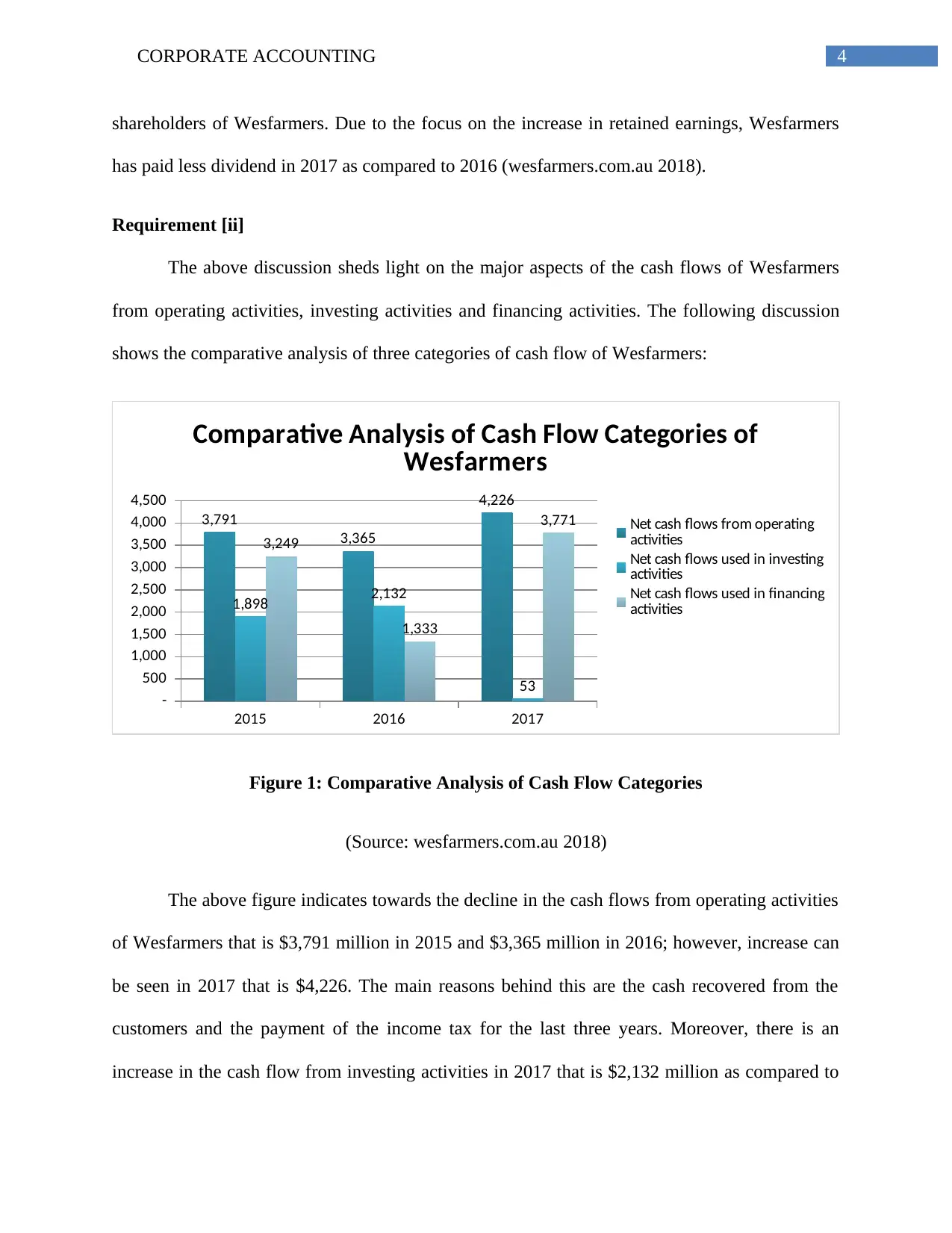

The above discussion sheds light on the major aspects of the cash flows of Wesfarmers

from operating activities, investing activities and financing activities. The following discussion

shows the comparative analysis of three categories of cash flow of Wesfarmers:

2015 2016 2017

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

3,791

3,365

4,226

1,898 2,132

53

3,249

1,333

3,771

Comparative Analysis of Cash Flow Categories of

Wesfarmers

Net cash flows from operating

activities

Net cash flows used in investing

activities

Net cash flows used in financing

activities

Figure 1: Comparative Analysis of Cash Flow Categories

(Source: wesfarmers.com.au 2018)

The above figure indicates towards the decline in the cash flows from operating activities

of Wesfarmers that is $3,791 million in 2015 and $3,365 million in 2016; however, increase can

be seen in 2017 that is $4,226. The main reasons behind this are the cash recovered from the

customers and the payment of the income tax for the last three years. Moreover, there is an

increase in the cash flow from investing activities in 2017 that is $2,132 million as compared to

shareholders of Wesfarmers. Due to the focus on the increase in retained earnings, Wesfarmers

has paid less dividend in 2017 as compared to 2016 (wesfarmers.com.au 2018).

Requirement [ii]

The above discussion sheds light on the major aspects of the cash flows of Wesfarmers

from operating activities, investing activities and financing activities. The following discussion

shows the comparative analysis of three categories of cash flow of Wesfarmers:

2015 2016 2017

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

3,791

3,365

4,226

1,898 2,132

53

3,249

1,333

3,771

Comparative Analysis of Cash Flow Categories of

Wesfarmers

Net cash flows from operating

activities

Net cash flows used in investing

activities

Net cash flows used in financing

activities

Figure 1: Comparative Analysis of Cash Flow Categories

(Source: wesfarmers.com.au 2018)

The above figure indicates towards the decline in the cash flows from operating activities

of Wesfarmers that is $3,791 million in 2015 and $3,365 million in 2016; however, increase can

be seen in 2017 that is $4,226. The main reasons behind this are the cash recovered from the

customers and the payment of the income tax for the last three years. Moreover, there is an

increase in the cash flow from investing activities in 2017 that is $2,132 million as compared to

5CORPORATE ACCOUNTING

$1,898 million in 2016 (wesfarmers.com.au 2018). The main reason behind this is the reduction

in the purchase and acquisition of property, plant, equipment and subsidiaries in Wesfarmers.

Lastly, there is a significant fall in the cash flow from financing activities in 2016 that is 1,333

million as compared to $3,249 million; but, there is a major increase in the year 2017 that is

$3,771 million. The main reason is the clearance of loans. For all these reasons, there is an

increase in the cash and cash equivalent in 2017 that is $1,013 million as compared to $611

million in 2016 (wesfarmers.com.au 2018).

Other Comprehensive Income Statement

Requirement [iii]

It can be seen that Wesfarmers has reported three major items in their comprehensive

income statements. They are Foreign currency translation reserve, Cash flow hedge reserve and

Retained earnings (wesfarmers.com.au 2018).

Requirement [iv]

Business organizations use the foreign currency translation reserve in order to convert the

results of the foreign subsidiaries of the parent companies to the reporting currency. This is

considered as a major portion of the process of consolidation of the financial statements and it

helps in the ascertainment of functional currency of cross-border business entity. With the help

of this aspect, companies use to re-measure the foreign business entity into the reporting

currency of the parent company. The last stage includes the currency translation of recorded

profit and losses (Eaton, Easterday and Rhodes 2013).

Business organizations use to use the cash flow hedge at the time of the planning of the

removal or minimization of the exposures that rose from the change in cash flow of specific

$1,898 million in 2016 (wesfarmers.com.au 2018). The main reason behind this is the reduction

in the purchase and acquisition of property, plant, equipment and subsidiaries in Wesfarmers.

Lastly, there is a significant fall in the cash flow from financing activities in 2016 that is 1,333

million as compared to $3,249 million; but, there is a major increase in the year 2017 that is

$3,771 million. The main reason is the clearance of loans. For all these reasons, there is an

increase in the cash and cash equivalent in 2017 that is $1,013 million as compared to $611

million in 2016 (wesfarmers.com.au 2018).

Other Comprehensive Income Statement

Requirement [iii]

It can be seen that Wesfarmers has reported three major items in their comprehensive

income statements. They are Foreign currency translation reserve, Cash flow hedge reserve and

Retained earnings (wesfarmers.com.au 2018).

Requirement [iv]

Business organizations use the foreign currency translation reserve in order to convert the

results of the foreign subsidiaries of the parent companies to the reporting currency. This is

considered as a major portion of the process of consolidation of the financial statements and it

helps in the ascertainment of functional currency of cross-border business entity. With the help

of this aspect, companies use to re-measure the foreign business entity into the reporting

currency of the parent company. The last stage includes the currency translation of recorded

profit and losses (Eaton, Easterday and Rhodes 2013).

Business organizations use to use the cash flow hedge at the time of the planning of the

removal or minimization of the exposures that rose from the change in cash flow of specific

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ACCOUNTING

assets or liabilities due to the change in the risk rate of the interest on any dent instrument based

on the floating rate of interests (Bratten, Causholli and Khan 2016).

Lastly, retained earnings refers to the portion of the net earnings of the companies that the

businesses do not distribute as dividend to the shareholders as the intention of the companies is

to retain this portion for the payment of debt or reinvestment in the core business activities

(Bertoni and De Rosa 2013).

Requirement [v]

Business organizations use to consider the other comprehensive income as a diversified

of their net profit. In the previous times, business entities use to consider the variations in the

profit as the external factors of their core business operations; and the shareholders use to get

highly volatile equities (Jordan and Clark 2014). However, Wesfarmers uses the other

comprehensive income statement as a tool to provide significant information about the above-

mentioned factors. Comprehensive income is considered as a mixture of standard new income

and other comprehensive income. The main reason behind the reporting of these activities in the

other comprehensive income is to provide the users with the comprehensive and holistic

overview of the major drivers of the business activities and operations as they cannot be reported

in the income statement.

Accounting for Corporate Income Tax

Requirement [vi]

It needs to be mentioned that Wesfarmers is subjected to taxation under Australian

taxation law. According to the annual report of Wesfarmers, the reported taxation expenses for

the company for the years 2017 and 2016 are $1,265 million and $631 million respectively. In

assets or liabilities due to the change in the risk rate of the interest on any dent instrument based

on the floating rate of interests (Bratten, Causholli and Khan 2016).

Lastly, retained earnings refers to the portion of the net earnings of the companies that the

businesses do not distribute as dividend to the shareholders as the intention of the companies is

to retain this portion for the payment of debt or reinvestment in the core business activities

(Bertoni and De Rosa 2013).

Requirement [v]

Business organizations use to consider the other comprehensive income as a diversified

of their net profit. In the previous times, business entities use to consider the variations in the

profit as the external factors of their core business operations; and the shareholders use to get

highly volatile equities (Jordan and Clark 2014). However, Wesfarmers uses the other

comprehensive income statement as a tool to provide significant information about the above-

mentioned factors. Comprehensive income is considered as a mixture of standard new income

and other comprehensive income. The main reason behind the reporting of these activities in the

other comprehensive income is to provide the users with the comprehensive and holistic

overview of the major drivers of the business activities and operations as they cannot be reported

in the income statement.

Accounting for Corporate Income Tax

Requirement [vi]

It needs to be mentioned that Wesfarmers is subjected to taxation under Australian

taxation law. According to the annual report of Wesfarmers, the reported taxation expenses for

the company for the years 2017 and 2016 are $1,265 million and $631 million respectively. In

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

order to carry out the taxation operations, Wesfarmers uses a tax rate of 30%. With the

application of this tax rate, Wesfarmers would have taxation expenses worth $1,241.40 million

($4,138 million*30%) for the year 2017 and $311.40 million ($1,038*30%) for the year 2016.

Hence, in the presence of increased income of the company, the above mentioned figures are the

major taxation related expenses of Wesfarmers (wesfarmers.com.au 2018).

Requirement [vii]

According to the 2017 Annual Report of Wesfarmers, the recorded profit before income

tax for the company for the years 2017 and 2016 are $4,138 million and $1,038 million

respectively; and the taxation rate for these years are 30%. By applying this taxation rate on the

reported profit, the taxation expenses of Wesfarmers would be $1,241.40 million ($4,138 million

x 30%) for the year 2017 and $311.40 million ($1,038 million x 30%) for the year 2016.

However, in the financial statements, the company has reported $1,265 million and $631 million

as the taxation expense for the year 2017 and 2016 respectively (wesfarmers.com.au 2018).

Thus, there is not any resemblance in the reported and standards taxation expenses of

Wesfarmers. The main reason of this differences in the inclusion or exclusion of some taxation

related items in the taxation expenses. Non-deductible expenses required for arriving to the

taxable profit can be considered as one of these items. Change in the rate of taxation for the

taxation operations of subsidiaries of Wesfarmers is considered as another reason; like the tax

rates of Australian and New Zealand are 30% and 208% respectively. Deferred tax is another

crucial item for this difference as Wesfarmers can enjoy tax benefits out of this. Lastly, non-

assessable income can also be held responsible for this difference (Woellner et al. 2016).

order to carry out the taxation operations, Wesfarmers uses a tax rate of 30%. With the

application of this tax rate, Wesfarmers would have taxation expenses worth $1,241.40 million

($4,138 million*30%) for the year 2017 and $311.40 million ($1,038*30%) for the year 2016.

Hence, in the presence of increased income of the company, the above mentioned figures are the

major taxation related expenses of Wesfarmers (wesfarmers.com.au 2018).

Requirement [vii]

According to the 2017 Annual Report of Wesfarmers, the recorded profit before income

tax for the company for the years 2017 and 2016 are $4,138 million and $1,038 million

respectively; and the taxation rate for these years are 30%. By applying this taxation rate on the

reported profit, the taxation expenses of Wesfarmers would be $1,241.40 million ($4,138 million

x 30%) for the year 2017 and $311.40 million ($1,038 million x 30%) for the year 2016.

However, in the financial statements, the company has reported $1,265 million and $631 million

as the taxation expense for the year 2017 and 2016 respectively (wesfarmers.com.au 2018).

Thus, there is not any resemblance in the reported and standards taxation expenses of

Wesfarmers. The main reason of this differences in the inclusion or exclusion of some taxation

related items in the taxation expenses. Non-deductible expenses required for arriving to the

taxable profit can be considered as one of these items. Change in the rate of taxation for the

taxation operations of subsidiaries of Wesfarmers is considered as another reason; like the tax

rates of Australian and New Zealand are 30% and 208% respectively. Deferred tax is another

crucial item for this difference as Wesfarmers can enjoy tax benefits out of this. Lastly, non-

assessable income can also be held responsible for this difference (Woellner et al. 2016).

8CORPORATE ACCOUNTING

Requirement [viii]

Deferred tax assets indicate towards the situation when the company pays advance tax or

high amount of tax. Deferred tax liabilities indicate towards the difference between tax carrying

amount and profit of the companies (Laux 2013). As per the 2017 Annual Report of Wesfarmers,

the amount of deferred tax assets for the year 2017 and 2016 are $971 million and $1,042 million

respectively; and the amount of deferred tax liabilities for 2017 and 2016 are $722 million and

$611 million respectively. The main reason for recording deferred tax assets is the variation in

taxable rate of depreciation and depreciable amount. The reason for deferred tax liabilities is the

difference in profit and the lower payment of taxes in 2017 (wesfarmers.com.au 2018).

Requirement [ix]

Income tax payable is considered as a crucial aspect for the business organizations.

According to the 2017 Annual Report of Wesfarmers, the amounts of income tax payable for

2017 and 2016 are $292 million and $29 million respectively (wesfarmers.com.au 2018).

However, there is difference between the amounts of income tax expenses and income tax

payable and differed tax assets can be considered as the prime reason for this. There are

instances where Wesfarmers has paid additional taxes apart from the actual amount. Thus, the

additional tax payment is the reason for this difference. After that, different regulation for

financial accounting and tax accounting is another major reason and depreciation can be

considered as an example. Due to the difference in the rate of depreciation, variation can be seen

under the taxation accounting and financial accounting and it leads to the increase or decrease in

depreciation expenses (Saad 2014).

Requirement [viii]

Deferred tax assets indicate towards the situation when the company pays advance tax or

high amount of tax. Deferred tax liabilities indicate towards the difference between tax carrying

amount and profit of the companies (Laux 2013). As per the 2017 Annual Report of Wesfarmers,

the amount of deferred tax assets for the year 2017 and 2016 are $971 million and $1,042 million

respectively; and the amount of deferred tax liabilities for 2017 and 2016 are $722 million and

$611 million respectively. The main reason for recording deferred tax assets is the variation in

taxable rate of depreciation and depreciable amount. The reason for deferred tax liabilities is the

difference in profit and the lower payment of taxes in 2017 (wesfarmers.com.au 2018).

Requirement [ix]

Income tax payable is considered as a crucial aspect for the business organizations.

According to the 2017 Annual Report of Wesfarmers, the amounts of income tax payable for

2017 and 2016 are $292 million and $29 million respectively (wesfarmers.com.au 2018).

However, there is difference between the amounts of income tax expenses and income tax

payable and differed tax assets can be considered as the prime reason for this. There are

instances where Wesfarmers has paid additional taxes apart from the actual amount. Thus, the

additional tax payment is the reason for this difference. After that, different regulation for

financial accounting and tax accounting is another major reason and depreciation can be

considered as an example. Due to the difference in the rate of depreciation, variation can be seen

under the taxation accounting and financial accounting and it leads to the increase or decrease in

depreciation expenses (Saad 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE ACCOUNTING

Requirement [x]

In Wesfarmers, $1,261 million and $631 million are the recorded taxation expenses for

2017 and 2016 in the income statement; and, $951 million and $1,009 million are the taxation

expenses for 2017 and 2016 in the cash flow statement (wesfarmers.com.au 2018). Thus, clear

difference can be seen in the amount. The calculation of tax expenses is done after considering

the tax expenses and other aspects. However, the taxation expenses are recorded under operating

expenses in the cash flow statement. It implies that the company has made large income tax

payment for the year and it has been considered as the cash outflow for operations. In the cash

flow statement, reduction in the tax expense implies that use of cash. It implies towards the

elimination of some of the taxation expenses by Wesfarmers before considering them in the

statement of cash flows (Woellner et al. 2016).

Requirement [xi]

The above discussion indicates towards the fact that there is not an surprising or

confusing factors in the taxation treatment of Wesfarmers as the company has complied with the

Australian Taxation Law for carrying out their taxation treatment. In addition, Wesfarmers has

also provided the necessary notes to the financial statements to support their taxation treatment

as they provide the necessary justification and explanation of the taxation treatment. By

observing the taxation treatment of Wesfarmers, one can gain the insight about the taxation

treatment for differed tax, current tax payable and others. These are helpful to gain knowledge to

conduct the taxation treatment of the companies.

Requirement [x]

In Wesfarmers, $1,261 million and $631 million are the recorded taxation expenses for

2017 and 2016 in the income statement; and, $951 million and $1,009 million are the taxation

expenses for 2017 and 2016 in the cash flow statement (wesfarmers.com.au 2018). Thus, clear

difference can be seen in the amount. The calculation of tax expenses is done after considering

the tax expenses and other aspects. However, the taxation expenses are recorded under operating

expenses in the cash flow statement. It implies that the company has made large income tax

payment for the year and it has been considered as the cash outflow for operations. In the cash

flow statement, reduction in the tax expense implies that use of cash. It implies towards the

elimination of some of the taxation expenses by Wesfarmers before considering them in the

statement of cash flows (Woellner et al. 2016).

Requirement [xi]

The above discussion indicates towards the fact that there is not an surprising or

confusing factors in the taxation treatment of Wesfarmers as the company has complied with the

Australian Taxation Law for carrying out their taxation treatment. In addition, Wesfarmers has

also provided the necessary notes to the financial statements to support their taxation treatment

as they provide the necessary justification and explanation of the taxation treatment. By

observing the taxation treatment of Wesfarmers, one can gain the insight about the taxation

treatment for differed tax, current tax payable and others. These are helpful to gain knowledge to

conduct the taxation treatment of the companies.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE ACCOUNTING

References

Bertoni, M. and De Rosa, B., 2013. Comprehensive income, fair value, and conservatism: A

conceptual framework for reporting financial performance.

Bratten, B., Causholli, M. and Khan, U., 2016. Usefulness of fair values for predicting banks’

future earnings: evidence from other comprehensive income and its components. Review of

Accounting Studies, 21(1), pp.280-315.

Eaton, T.V., Easterday, K.E. and Rhodes, M.R., 2013. The presentation of other comprehensive

income. The CPA Journal, 83(3), p.32.

Jordan, C.E. and Clark, S.J., 2014. Reporting preferences under the comprehensive income

standard: Examining its use in practice. The CPA Journal, 84(5), p.34.

Laux, R.C., 2013. The association between deferred tax assets and liabilities and future tax

payments. The Accounting Review, 88(4), pp.1357-1383.

Miloš, P. and Jovan, B., 2013. Cash flow statement. Škola Biznisa, 2013(3-4), pp.129-147.

Reid, W. and Myddelton, D.R., 2017. Cash flow statement. In The Meaning of Company

Accounts (pp. 16-16). Routledge.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia-

Social and Behavioral Sciences, 109, pp.1069-1075.

Wesfarmers.com.au. (2018). 2015 Annual Report. [online] Available at:

http://www.wesfarmers.com.au/docs/default-source/reports/2015-annual-report.pdf?sfvrsn=4

[Accessed 18 May 2018].

References

Bertoni, M. and De Rosa, B., 2013. Comprehensive income, fair value, and conservatism: A

conceptual framework for reporting financial performance.

Bratten, B., Causholli, M. and Khan, U., 2016. Usefulness of fair values for predicting banks’

future earnings: evidence from other comprehensive income and its components. Review of

Accounting Studies, 21(1), pp.280-315.

Eaton, T.V., Easterday, K.E. and Rhodes, M.R., 2013. The presentation of other comprehensive

income. The CPA Journal, 83(3), p.32.

Jordan, C.E. and Clark, S.J., 2014. Reporting preferences under the comprehensive income

standard: Examining its use in practice. The CPA Journal, 84(5), p.34.

Laux, R.C., 2013. The association between deferred tax assets and liabilities and future tax

payments. The Accounting Review, 88(4), pp.1357-1383.

Miloš, P. and Jovan, B., 2013. Cash flow statement. Škola Biznisa, 2013(3-4), pp.129-147.

Reid, W. and Myddelton, D.R., 2017. Cash flow statement. In The Meaning of Company

Accounts (pp. 16-16). Routledge.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia-

Social and Behavioral Sciences, 109, pp.1069-1075.

Wesfarmers.com.au. (2018). 2015 Annual Report. [online] Available at:

http://www.wesfarmers.com.au/docs/default-source/reports/2015-annual-report.pdf?sfvrsn=4

[Accessed 18 May 2018].

11CORPORATE ACCOUNTING

Wesfarmers.com.au. (2018). 2016 Annual Report. [online] Available at:

http://www.wesfarmers.com.au/docs/default-source/reports/2016-annual-report.pdf?sfvrsn=8

[Accessed 18 May 2018].

Wesfarmers.com.au. (2018). 2017 Annual Report. [online] Available at:

http://www.wesfarmers.com.au/docs/default-source/reports/j000901-ar17_interactive_final.pdf?

sfvrsn=4 [Accessed 18 May 2018].

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation Law

2016. OUP Catalogue.

Wesfarmers.com.au. (2018). 2016 Annual Report. [online] Available at:

http://www.wesfarmers.com.au/docs/default-source/reports/2016-annual-report.pdf?sfvrsn=8

[Accessed 18 May 2018].

Wesfarmers.com.au. (2018). 2017 Annual Report. [online] Available at:

http://www.wesfarmers.com.au/docs/default-source/reports/j000901-ar17_interactive_final.pdf?

sfvrsn=4 [Accessed 18 May 2018].

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation Law

2016. OUP Catalogue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.