Corporate Accounting and Reporting: IAS 17 and Impairment

VerifiedAdded on 2021/05/30

|9

|1563

|17

Report

AI Summary

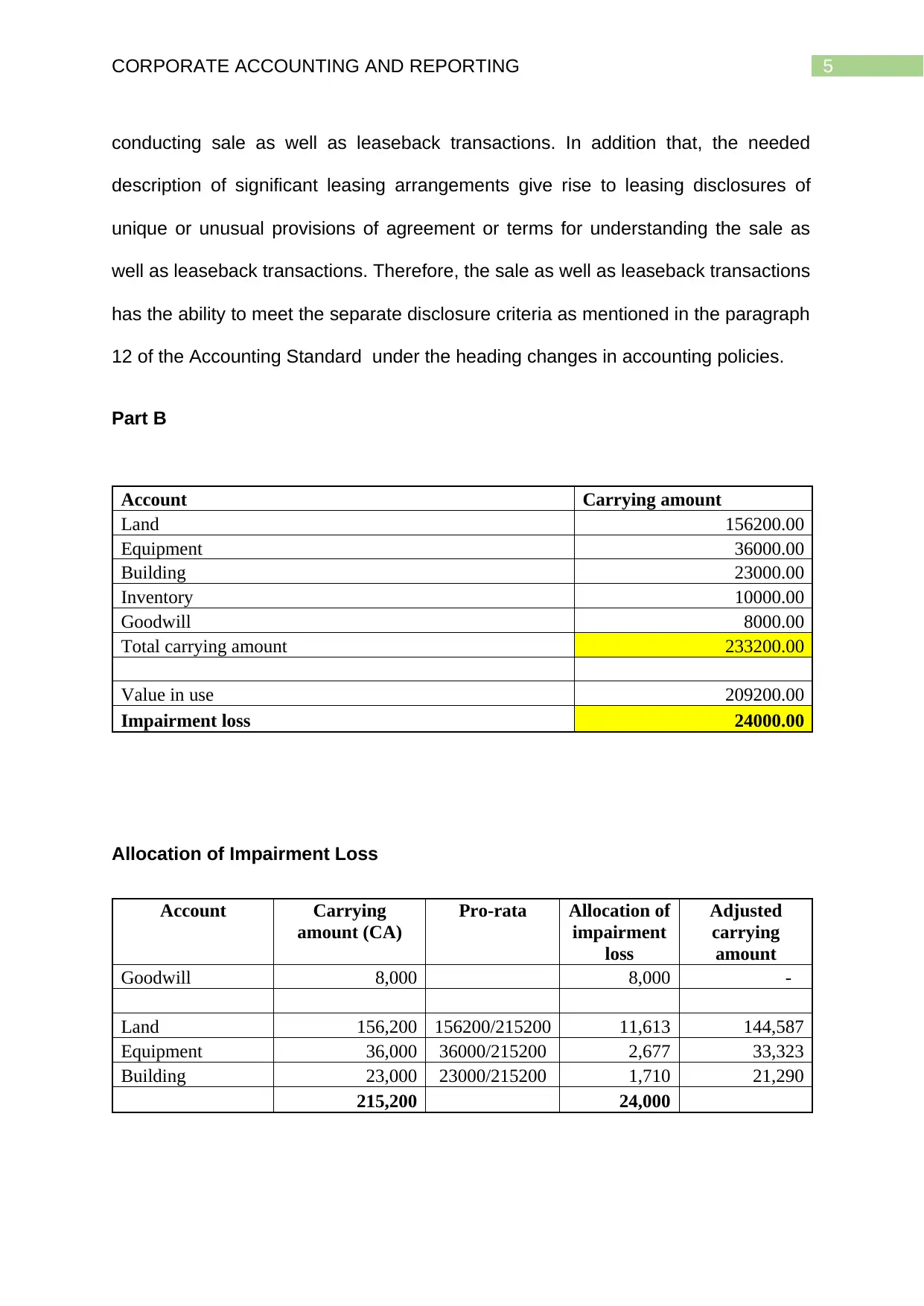

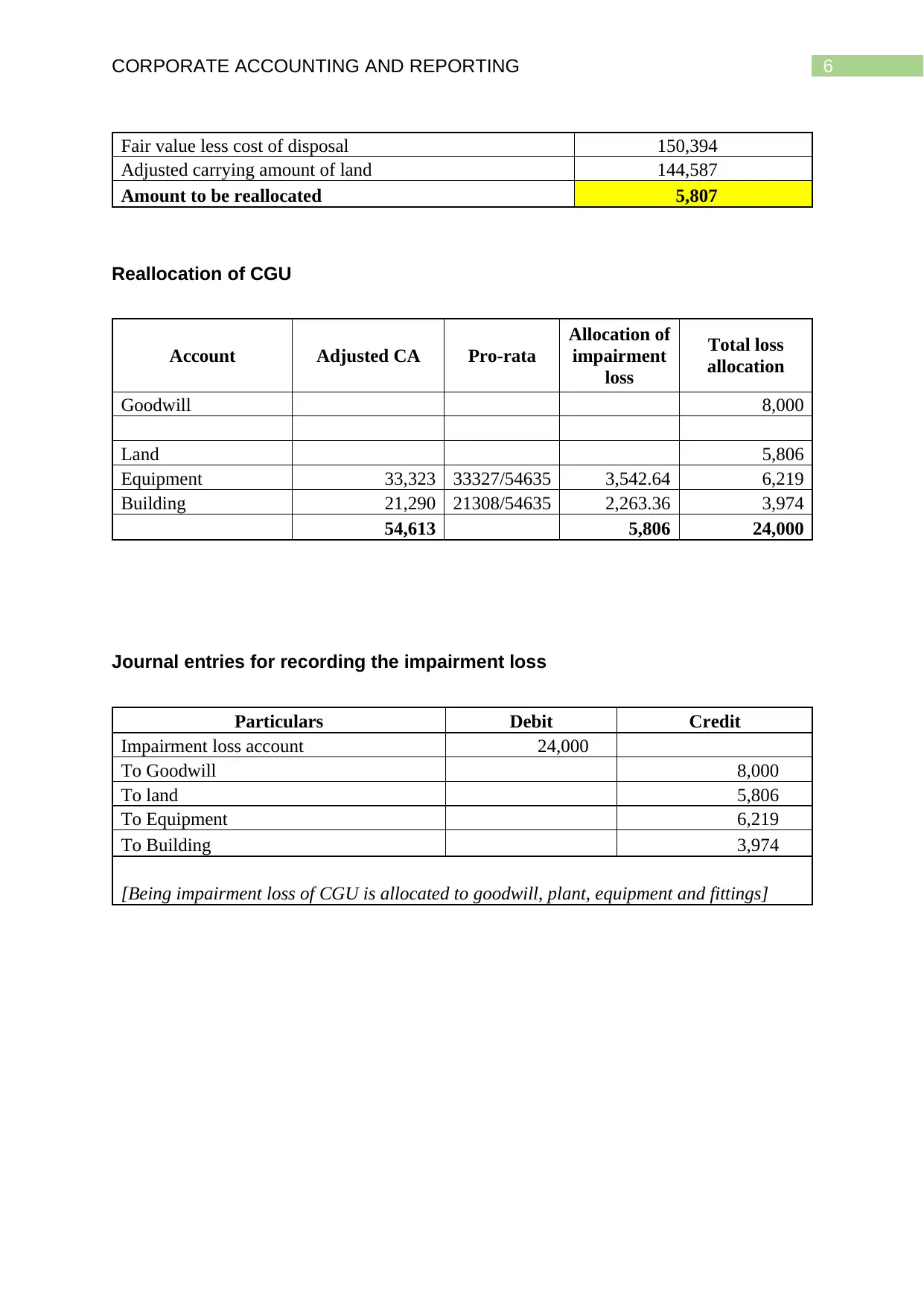

This report provides a detailed analysis of corporate accounting and reporting, focusing on finance leases and impairment losses. It begins with an overview of IAS 17, explaining accounting policies and disclosures for both lessees and lessors. The report highlights the disclosure requirements for finance leases, including the carrying amount of assets, reconciliation of lease payments, and contingent rents. Part A delves into the specifics of finance lease disclosures, while Part B presents a practical application with a case study on impairment loss allocation, including journal entries. The report covers the allocation of impairment loss across various assets, and the subsequent reallocation of the CGU (Cash Generating Unit). The journal entries record the impairment loss allocation to goodwill, land, equipment, and buildings. The analysis includes calculations and tables to illustrate the process. The report concludes by summarizing the key aspects of accounting for finance leases and impairment, providing a comprehensive understanding of the relevant accounting standards. The reference list provides the sources used in the report.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.