BO1COAC318 Corporate Accounting: Acquisition Method Report

VerifiedAdded on 2022/10/11

|9

|1934

|18

Report

AI Summary

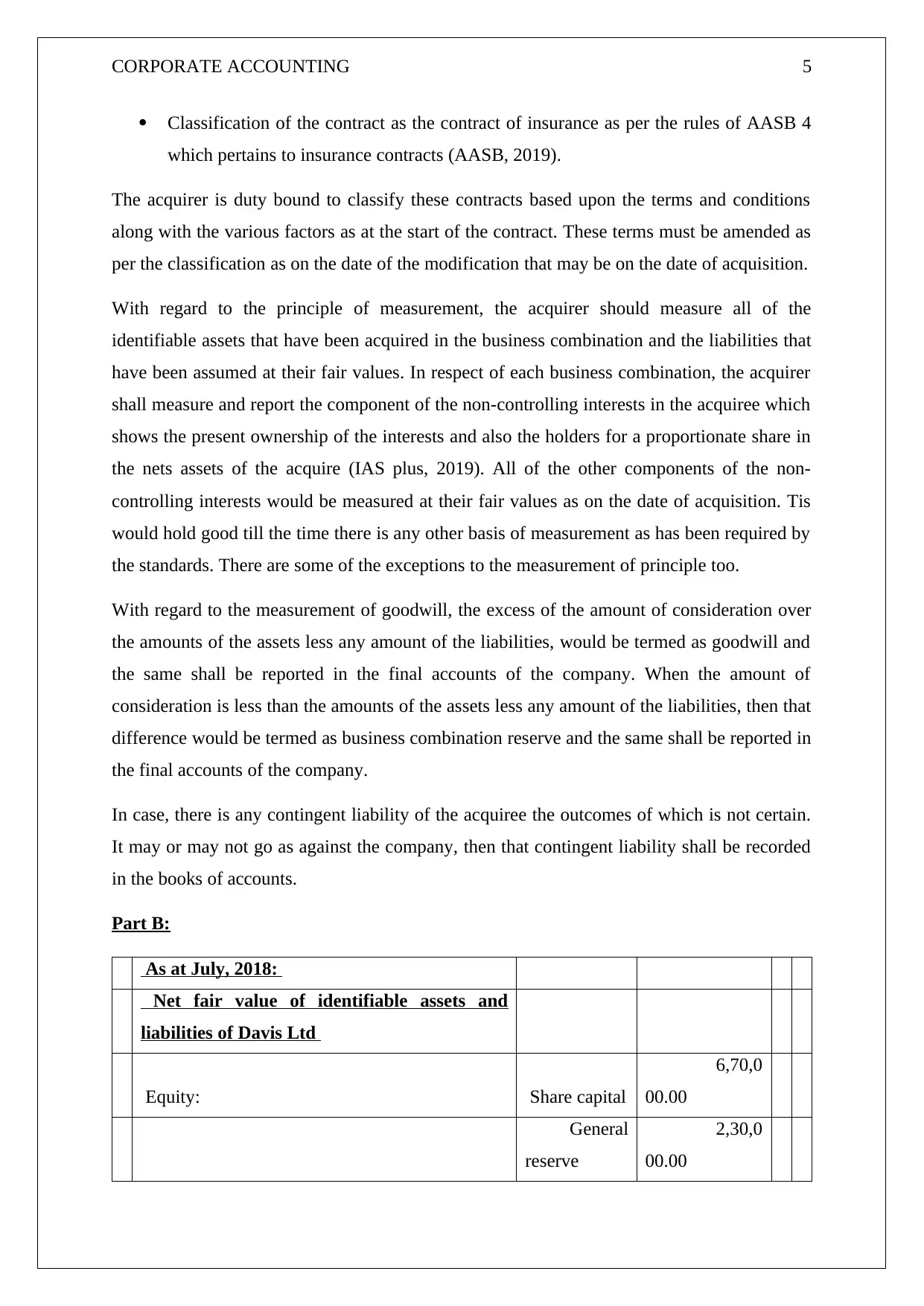

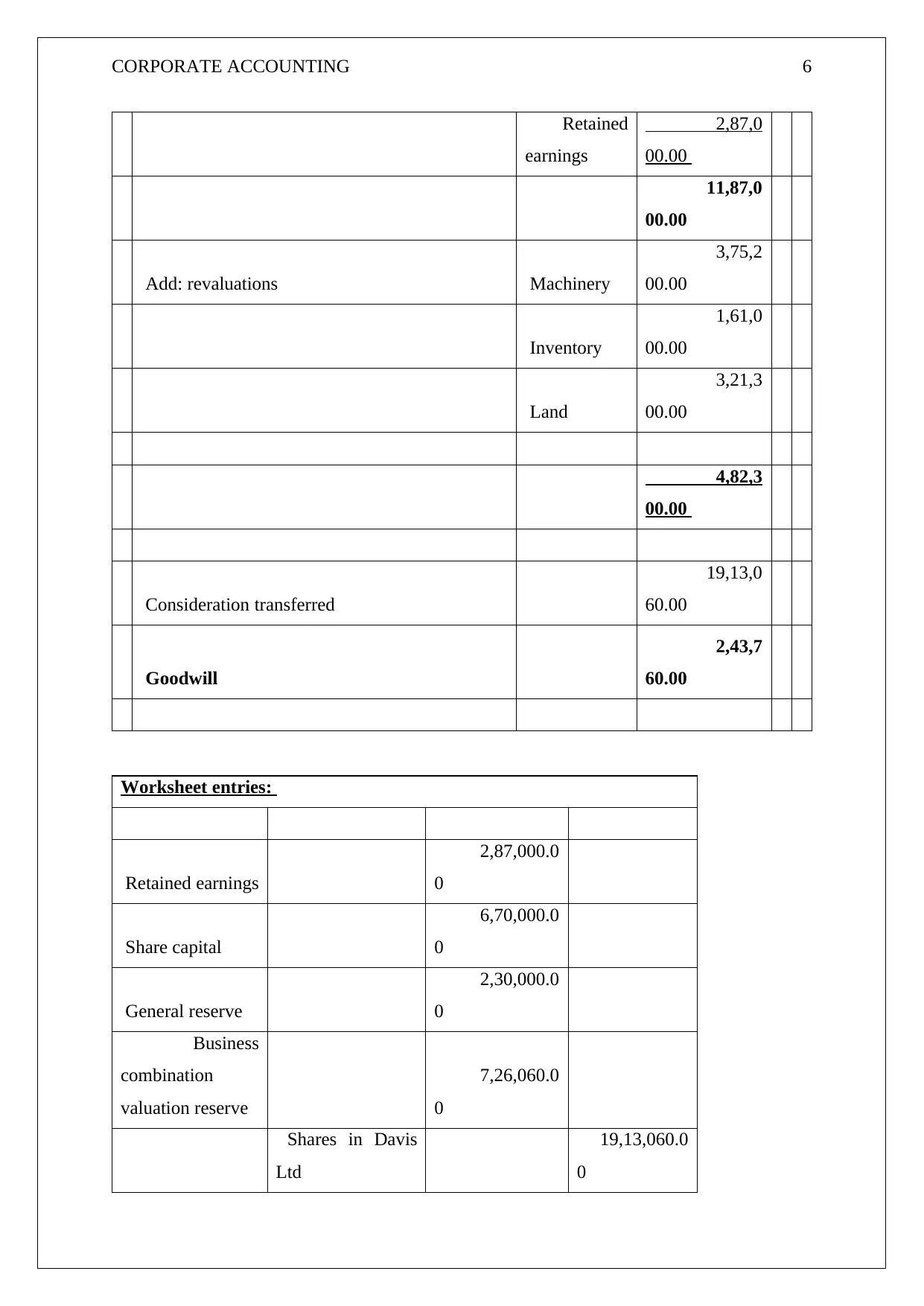

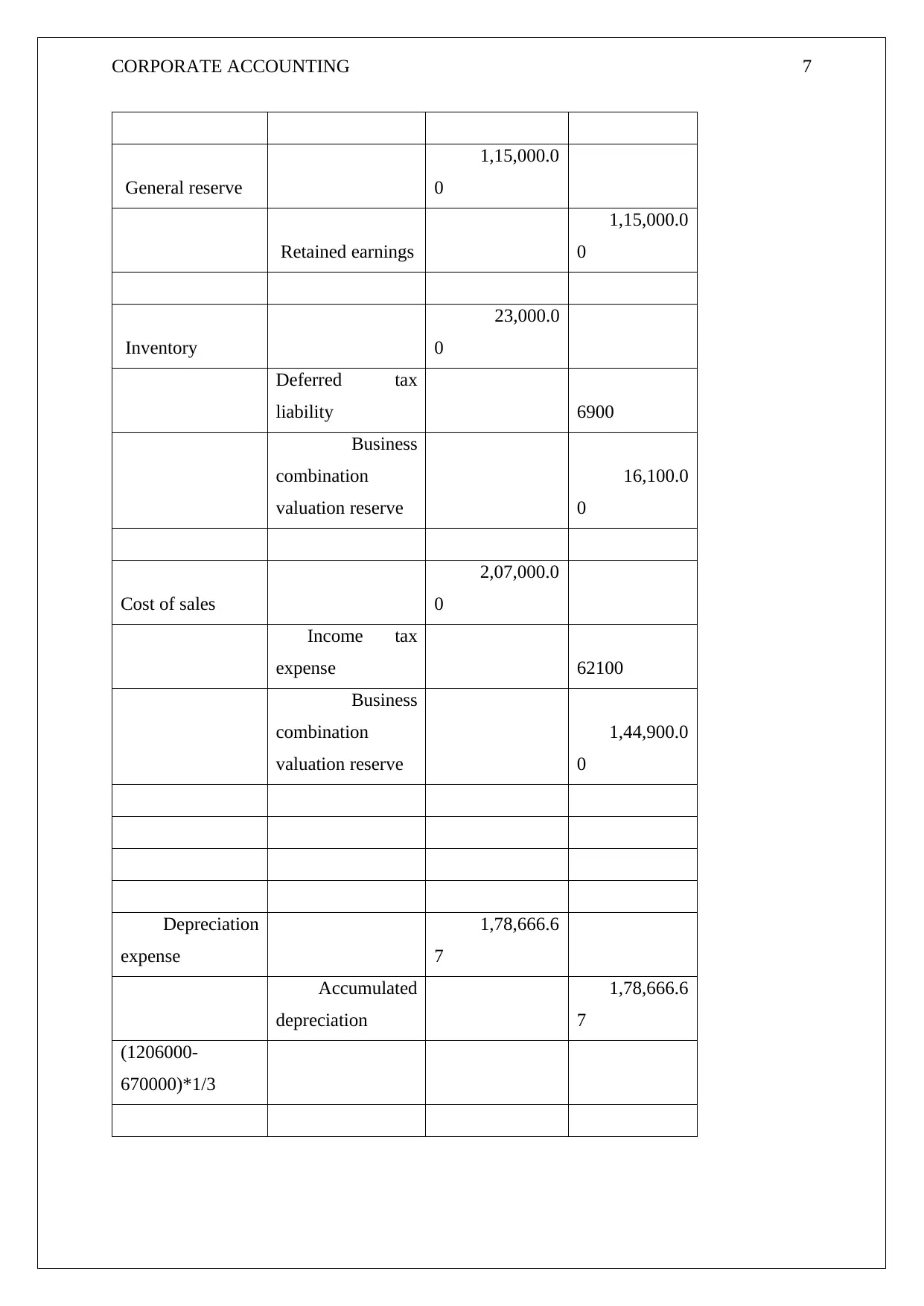

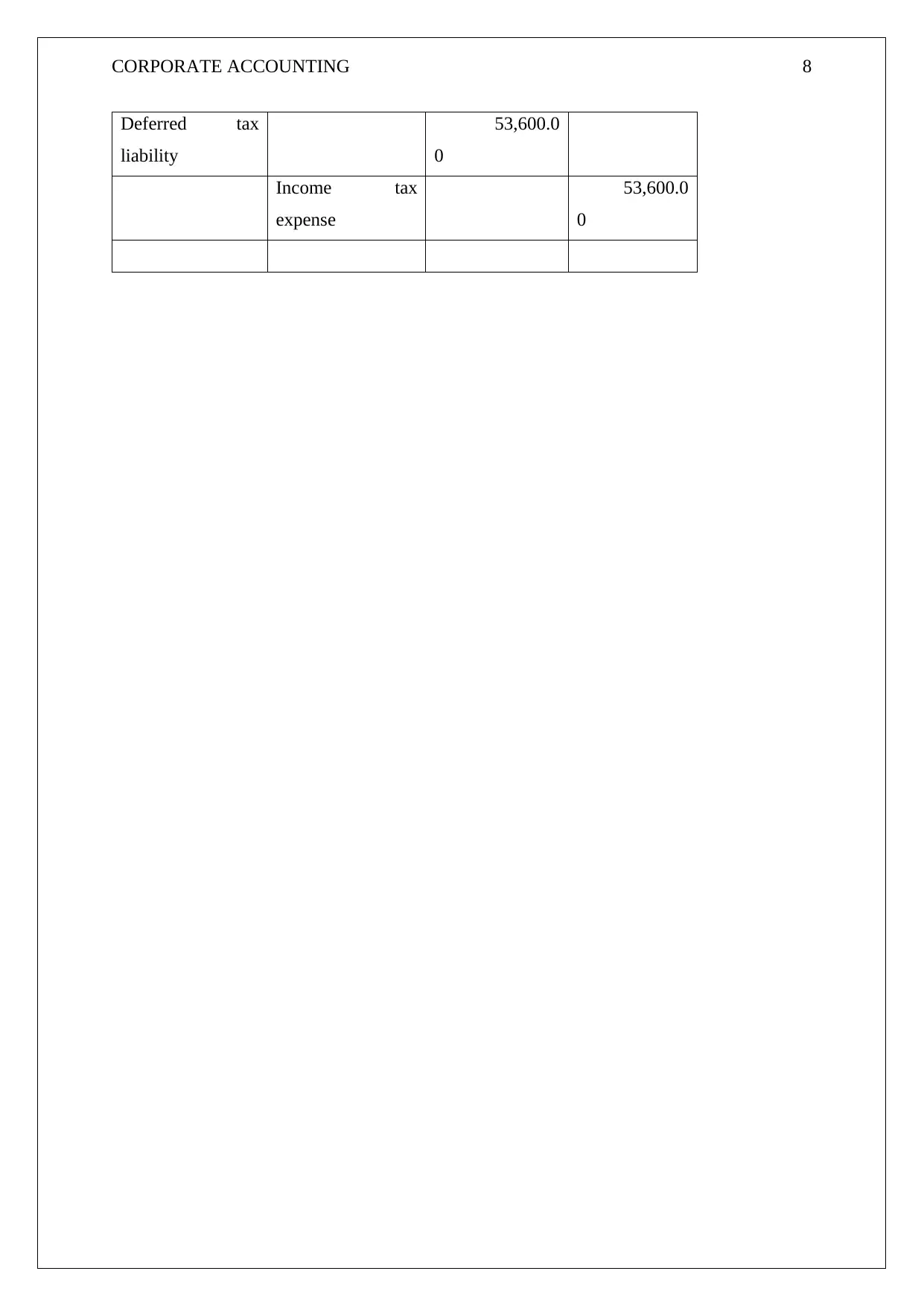

This report delves into the intricacies of corporate accounting, with a primary focus on the acquisition method and business combinations. It meticulously outlines the requirements of the acquisition method, including acquirer identification, recognition and measurement of assets and liabilities, determination of the acquisition date, and the calculation of goodwill. The report references AASB 3 and other relevant accounting standards, providing a detailed explanation of the principles and procedures involved. It also presents a practical application of these concepts through a case study involving Davis Ltd, demonstrating the application of accounting standards in a real-world scenario. The report further includes worksheet entries and financial data to illustrate the accounting treatments for business combinations, providing a comprehensive understanding of the subject matter.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.