Corporate Accounting: Reserves, Impairments, and Financial Reporting

VerifiedAdded on 2022/11/26

|14

|2854

|390

Report

AI Summary

This report delves into the critical aspects of corporate accounting, specifically focusing on reserves and impairments. Part A defines reserves, classifies them into revenue and capital reserves (including general, specific, and secret reserves), and outlines the accounting procedures for reserve accounts. It also covers the importance of reserves in strengthening a company's financial position, funding investments, enhancing its image, increasing working capital, and facilitating financial requirements. Part B assesses Gali Ltd's cash-generating unit (CGU) for impairment, calculating the impairment loss and providing corresponding journal entries. The report highlights the significance of these components in financial accounting, their disclosure in financial statements, and their influence on the financial position of business entities, offering a comprehensive understanding of these key accounting concepts.

Corporate Accounting 1

Corporate accounting

Student Number

Class & Course Code

Trimester Number

Professor

University

The City & State

Date

Corporate accounting

Student Number

Class & Course Code

Trimester Number

Professor

University

The City & State

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting 2

Introduction and study objectives

Reserves and impairments are key components of financial accounting. Both items are

disclosure in the financial statements and significantly influence the financial position of

business entities. Companies tend to retain part of their earnings at the end of a fiscal

year. The retained earnings are referred to as reserves (Fischer, 2015, p. 547).

Likewise, the International Accounting Standards Board (IASB) states that assets and

cash-generating unit (CGU) should be tested for impairment every year or when there

are indications for impairment. Assets should be reported at their fair value (recoverable

amount) and not their carrying amount. An impairment loss is realised when the

recoverable amount is lower than the carrying amount. Moreover, impairment gain is

realised when the recoverable amount is higher than the carrying amount (Amiraslani &

Iatridis, 2013, p. 76).

This study is divided into two parts: Part A and Part B. Part A address reserves as a

component of accounting. The scope of the study covers the definition of reserves,

types of reserves, and the accounting procedures for reserve accounts. Part B evaluates

Gali Ltd’s cash-generating unit (CGU) for impairment. The evaluation entails calculation

for impairments loss and journal entries in respective accounts.

Part A: Reserves in Accounting

Definition and meaning of reserves in accounting

Companies often set aside part of their annual earnings while paying out dividends to

the shareholders. The amount set aside is used to serve several objectives such as

improve the company’s financial position, meet legal requirements, business expansion,

Introduction and study objectives

Reserves and impairments are key components of financial accounting. Both items are

disclosure in the financial statements and significantly influence the financial position of

business entities. Companies tend to retain part of their earnings at the end of a fiscal

year. The retained earnings are referred to as reserves (Fischer, 2015, p. 547).

Likewise, the International Accounting Standards Board (IASB) states that assets and

cash-generating unit (CGU) should be tested for impairment every year or when there

are indications for impairment. Assets should be reported at their fair value (recoverable

amount) and not their carrying amount. An impairment loss is realised when the

recoverable amount is lower than the carrying amount. Moreover, impairment gain is

realised when the recoverable amount is higher than the carrying amount (Amiraslani &

Iatridis, 2013, p. 76).

This study is divided into two parts: Part A and Part B. Part A address reserves as a

component of accounting. The scope of the study covers the definition of reserves,

types of reserves, and the accounting procedures for reserve accounts. Part B evaluates

Gali Ltd’s cash-generating unit (CGU) for impairment. The evaluation entails calculation

for impairments loss and journal entries in respective accounts.

Part A: Reserves in Accounting

Definition and meaning of reserves in accounting

Companies often set aside part of their annual earnings while paying out dividends to

the shareholders. The amount set aside is used to serve several objectives such as

improve the company’s financial position, meet legal requirements, business expansion,

Corporate Accounting 3

fulfilling short term financial obligations, and ensuring a stable repayment if dividends.

The retained portion of the income at the end of a financial year is known as reserves

(Sharma, 2019).

According to the IASB reserves are defined as, “the amount set aside out of profit and

other surpluses, which are not earmarked in any way to meet any particular liability

known to exist on the date of Balance Sheet.” Reserves are added on top of the

shareholder's contribution and are used to meet financial obligations during difficult

periods. It is important to note that reserves are not charged on profit but is instead a

portion of profit during a given year. Therefore, reserves are not recorded in the balance

sheet in case a company incurs a loss (Kennon, 2019).

Moreover, reserves are not set aside to meet particular commitments, liabilities, or

contingencies. Likewise, entities are prohibited from creating reserves after anticipating

the possibility of a loss. However, reserves can be used to meet financial obligations

when a company suffers a loss at the end of a financial year. Lastly, reserves are shown

in the balance sheet and the profit and loss appropriation accounts and not in the profit

and loss account (Thomason, 2017).

Types of reserves

In accounting, reserves are classified into two broad classes of revenue reserves and

capital reserves.

fulfilling short term financial obligations, and ensuring a stable repayment if dividends.

The retained portion of the income at the end of a financial year is known as reserves

(Sharma, 2019).

According to the IASB reserves are defined as, “the amount set aside out of profit and

other surpluses, which are not earmarked in any way to meet any particular liability

known to exist on the date of Balance Sheet.” Reserves are added on top of the

shareholder's contribution and are used to meet financial obligations during difficult

periods. It is important to note that reserves are not charged on profit but is instead a

portion of profit during a given year. Therefore, reserves are not recorded in the balance

sheet in case a company incurs a loss (Kennon, 2019).

Moreover, reserves are not set aside to meet particular commitments, liabilities, or

contingencies. Likewise, entities are prohibited from creating reserves after anticipating

the possibility of a loss. However, reserves can be used to meet financial obligations

when a company suffers a loss at the end of a financial year. Lastly, reserves are shown

in the balance sheet and the profit and loss appropriation accounts and not in the profit

and loss account (Thomason, 2017).

Types of reserves

In accounting, reserves are classified into two broad classes of revenue reserves and

capital reserves.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting 4

I. Revenue reserves

Revenue reserves are realised from the profit realised by a company at the end of a

trading year. Revenue reserve is further classified into the general reserve, specific

reserve, and secret reserve (Davoren, 2018).

i) General reserve

General reserve is created from the profits realised from a financial year. General

reserves are not meant to meet the specific financial purpose. General reserves are

retained to provide extra working capital for a company to strengthen its financial

position. General reserve is referred to as free reserves and contingency reserve

because they are used to meet the unspecific financial purpose

(accountingexplanation.com, 2019). However, they are used to achieve these purposes:

a) Strengthening the financial position of a company.

b) Create additional working capital for the company that can be used anytime by

the management.

c) Meeting contingencies or liabilities arising from unforeseen circumstances.

d) Stabilising the dividend rate offered to the shareholders over the years because

of inadequate profits.

ii) Specific reserve

Unlike general reserves, specific reserves are set aside to meet a particular purpose for

a business. These retained earnings can only be used for the intended purpose and not

any other purpose. However, specific reserves can be used to meet unintended purpose

I. Revenue reserves

Revenue reserves are realised from the profit realised by a company at the end of a

trading year. Revenue reserve is further classified into the general reserve, specific

reserve, and secret reserve (Davoren, 2018).

i) General reserve

General reserve is created from the profits realised from a financial year. General

reserves are not meant to meet the specific financial purpose. General reserves are

retained to provide extra working capital for a company to strengthen its financial

position. General reserve is referred to as free reserves and contingency reserve

because they are used to meet the unspecific financial purpose

(accountingexplanation.com, 2019). However, they are used to achieve these purposes:

a) Strengthening the financial position of a company.

b) Create additional working capital for the company that can be used anytime by

the management.

c) Meeting contingencies or liabilities arising from unforeseen circumstances.

d) Stabilising the dividend rate offered to the shareholders over the years because

of inadequate profits.

ii) Specific reserve

Unlike general reserves, specific reserves are set aside to meet a particular purpose for

a business. These retained earnings can only be used for the intended purpose and not

any other purpose. However, specific reserves can be used to meet unintended purpose

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting 5

at the discretion of the management. Specific reserves can further be classified into five

classes (Bhimani, et al., 2015, p. 102).

a) Dividend stabilizing reserve

Dividend stabilizing reserve is set aside to maintain the rate of dividends paid to

shareholders in case of small profit in the future. When adequate and significant net

income is realised, a potion is transferred into the dividend reserves account. The

created amount is then used to pay dividends when a small profit is realised (Bayoumi,

2012, p. 23).

For journal entries, the amount is debited in the profit and loss appropriation account

and credited to the dividend stabilizing reserve account.

b) Debenture redemption reserve

Debenture redemption reserve assists companies in creating debentures which are then

redeemed at the end of a particular period. Every year a specific amount is retained

from the profit and deposited in the debenture redemption reserve account. The amount

is later invested in market securities (Edmonds, et al., 2015, p. 65).

For journal entries, the amount is debited in the profit and loss appropriation account

and credited to the debenture redemption reserve account.

c) Investment fluctuation reserve

Businesses sometimes engage in external investments in securities, debentures, and

shares. Government policies and market conditions make the price of such investments

to fluctuate. A decrease in the price of such investment would lead to a loss. Therefore,

at the discretion of the management. Specific reserves can further be classified into five

classes (Bhimani, et al., 2015, p. 102).

a) Dividend stabilizing reserve

Dividend stabilizing reserve is set aside to maintain the rate of dividends paid to

shareholders in case of small profit in the future. When adequate and significant net

income is realised, a potion is transferred into the dividend reserves account. The

created amount is then used to pay dividends when a small profit is realised (Bayoumi,

2012, p. 23).

For journal entries, the amount is debited in the profit and loss appropriation account

and credited to the dividend stabilizing reserve account.

b) Debenture redemption reserve

Debenture redemption reserve assists companies in creating debentures which are then

redeemed at the end of a particular period. Every year a specific amount is retained

from the profit and deposited in the debenture redemption reserve account. The amount

is later invested in market securities (Edmonds, et al., 2015, p. 65).

For journal entries, the amount is debited in the profit and loss appropriation account

and credited to the debenture redemption reserve account.

c) Investment fluctuation reserve

Businesses sometimes engage in external investments in securities, debentures, and

shares. Government policies and market conditions make the price of such investments

to fluctuate. A decrease in the price of such investment would lead to a loss. Therefore,

Corporate Accounting 6

part of the profit is set aside as investment fluctuation reserve to meet the loss arising

from the fluctuating value of investments (Kolitz, 2016, p. 82).

For journal entries, the amount is debited in the Accounting for reserve accounts

and credited to the investment fluctuation reserve account.

d) Workmen compensation fund

Companies also set aside part of their earnings to meet workers’ claims in case they get

injured at the workplace or when on duty. The retain earnings meant to meet employees

claims are deposited in the workmen compensation fund account (Deegan, 2013, p. 71).

For journal entries, the amount is debited in the profit and loss appropriation account

and credited to the workmen compensation reserve account.

iii) Secret reserve

The secret reserve is not presented in the balance sheet. Part of profit earned during the

best performance years is retained and reported in the financial statement when the

company performs least. Businesses use different techniques to create secret reserves

(Bayoumi, 2012, p. 33). Some of the techniques are.

a) Undervaluing the stock,

b) Creating extra provisions than required,

c) Changing amounts for capital expenditures to revenue,

d) Reporting contingent liabilities as entities’ actual liabilities.

II. Capital Reserves

part of the profit is set aside as investment fluctuation reserve to meet the loss arising

from the fluctuating value of investments (Kolitz, 2016, p. 82).

For journal entries, the amount is debited in the Accounting for reserve accounts

and credited to the investment fluctuation reserve account.

d) Workmen compensation fund

Companies also set aside part of their earnings to meet workers’ claims in case they get

injured at the workplace or when on duty. The retain earnings meant to meet employees

claims are deposited in the workmen compensation fund account (Deegan, 2013, p. 71).

For journal entries, the amount is debited in the profit and loss appropriation account

and credited to the workmen compensation reserve account.

iii) Secret reserve

The secret reserve is not presented in the balance sheet. Part of profit earned during the

best performance years is retained and reported in the financial statement when the

company performs least. Businesses use different techniques to create secret reserves

(Bayoumi, 2012, p. 33). Some of the techniques are.

a) Undervaluing the stock,

b) Creating extra provisions than required,

c) Changing amounts for capital expenditures to revenue,

d) Reporting contingent liabilities as entities’ actual liabilities.

II. Capital Reserves

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting 7

Capital reserves are apportioned from the capital profits. Companies use capital

reserves to write off their capital losses. Although capital reserves cannot be distributed

to the shareholders as shares, some conditions permit the distribution. First, when

articles of association allow the distribution. Second, the profits are realised in cash from

selling fixed assets. Third, the gain arises from the revaluation of all company assets

and liabilities.

Accounting for reserve accounts

The first procedure for accounting for the reserves is to make journal entries. Cash

should be placed from the cash account into a cash reserve account. Typically, a debit

entry is made into the reserve account while a credit entry of the same amount is made

into the cash account. The reconciliation process is essential to ensure that accurate

information is posted in the general ledgers (Langenderfer & Porter, 2014, p. 89).

All assets are reported in the balance sheet statement. The reserve account is a current

asset. The reserve account appears after the operating cash account under the existing

assets category in the balance sheet. Reserves are created from the retained earnings.

An increase in the reserves account is recorded by debiting the profit and loss

appropriation account and crediting affected general or specific reserve accounts.

Moreover, a decrease in reserves account is recorded by crediting the profit and loss

appropriation account and debiting involved general or specific reserve accounts

(Taschner & Charifzadeh, 2016, p. 171).

Moreover, reduction of reserves can arise from transferring funds from one reserve

account to another. The transaction is recorded by debiting the original account and

Capital reserves are apportioned from the capital profits. Companies use capital

reserves to write off their capital losses. Although capital reserves cannot be distributed

to the shareholders as shares, some conditions permit the distribution. First, when

articles of association allow the distribution. Second, the profits are realised in cash from

selling fixed assets. Third, the gain arises from the revaluation of all company assets

and liabilities.

Accounting for reserve accounts

The first procedure for accounting for the reserves is to make journal entries. Cash

should be placed from the cash account into a cash reserve account. Typically, a debit

entry is made into the reserve account while a credit entry of the same amount is made

into the cash account. The reconciliation process is essential to ensure that accurate

information is posted in the general ledgers (Langenderfer & Porter, 2014, p. 89).

All assets are reported in the balance sheet statement. The reserve account is a current

asset. The reserve account appears after the operating cash account under the existing

assets category in the balance sheet. Reserves are created from the retained earnings.

An increase in the reserves account is recorded by debiting the profit and loss

appropriation account and crediting affected general or specific reserve accounts.

Moreover, a decrease in reserves account is recorded by crediting the profit and loss

appropriation account and debiting involved general or specific reserve accounts

(Taschner & Charifzadeh, 2016, p. 171).

Moreover, reduction of reserves can arise from transferring funds from one reserve

account to another. The transaction is recorded by debiting the original account and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting 8

crediting the new account. Likewise, a reserve account can be reduced by paying

dividends to shareholders using shares and cash withdrawn from such a statement. The

journal entry is made by debiting the concerned reserve account and crediting the

dividend or bonus accounts (Drury, 2013, p. 66).

Lastly, IASB’s conceptual framework for financial reporting states that reports should

show a faithful representation of the business entity. Therefore, companies should make

disclosures to their stakeholders about the creation and use of reserves. In particular,

stakeholders should be informed why the management has decided to retain part of the

profit as reserves instead of payout higher dividends. The disclosure only informs

stakeholders how reserves will be created, the amount to be put aside per annum and

recording and reconciliation of respecting accounts (Hendersen, et al., 2014, p. 213).

Importance of reserves to business entities

As mentioned before, reserve accounts are created to meet either general or specific

needs of a company. First, reserves accounts are meant to strengthen the financial

position of a company. Reserves can be used to fulfill unexpected financial losses in the

future. Second, companies need funds to finance their internal and external investment

activities. Besides relying on loans, the management can set aside part of the annual

profit to fund investments. Therefore, reserves are used as an internal source of

investment funds. Third, reserves are used to enhance a company’s image and

reputation. One method of improving a corporate image is by ensuring a regular

payment of dividends to the investors (accountingexplanation.com, 2019). The amount

of dividends paid to investors should be equalized over time. Therefore, reserves are

crediting the new account. Likewise, a reserve account can be reduced by paying

dividends to shareholders using shares and cash withdrawn from such a statement. The

journal entry is made by debiting the concerned reserve account and crediting the

dividend or bonus accounts (Drury, 2013, p. 66).

Lastly, IASB’s conceptual framework for financial reporting states that reports should

show a faithful representation of the business entity. Therefore, companies should make

disclosures to their stakeholders about the creation and use of reserves. In particular,

stakeholders should be informed why the management has decided to retain part of the

profit as reserves instead of payout higher dividends. The disclosure only informs

stakeholders how reserves will be created, the amount to be put aside per annum and

recording and reconciliation of respecting accounts (Hendersen, et al., 2014, p. 213).

Importance of reserves to business entities

As mentioned before, reserve accounts are created to meet either general or specific

needs of a company. First, reserves accounts are meant to strengthen the financial

position of a company. Reserves can be used to fulfill unexpected financial losses in the

future. Second, companies need funds to finance their internal and external investment

activities. Besides relying on loans, the management can set aside part of the annual

profit to fund investments. Therefore, reserves are used as an internal source of

investment funds. Third, reserves are used to enhance a company’s image and

reputation. One method of improving a corporate image is by ensuring a regular

payment of dividends to the investors (accountingexplanation.com, 2019). The amount

of dividends paid to investors should be equalized over time. Therefore, reserves are

Corporate Accounting 9

used to maintain equalised payment of dividends during the years when profits are

inadequate. Amount from the reserves accounts can be used to supplement benefits

and pay dividends (Davoren, 2018).

Fourth, reserves are used to increase the working capital of an enterprise. During the

periods when a business has performed poorly or during emergencies, companies can

use their reserve accounts to maintain their functions at the recommendable level. Fifth,

reserves are used to facilitate substantial financial requirements, especially when they

are created to meet a specific purpose. For instance, debentures redemption reserve

account are used to pay the debenture holders when a company cannot achieve such

payments. Failure to set reserves aside would force a company to use its working

capital to make debenture payments. Using working capital would adversely affect a

company’s operational efficiency (Davoren, 2018).

Part B: Calculations and Journal entries

Gali Ltd holds a CGU in China. There is adequate evidence showing that the CGU is

impaired. The calculation below seeks to determine the amount of reported impairment

loss based on the information provided by the company. Moreover, the entries have

been made in respective accounts that have been affected by the impairment of the

CGU.

used to maintain equalised payment of dividends during the years when profits are

inadequate. Amount from the reserves accounts can be used to supplement benefits

and pay dividends (Davoren, 2018).

Fourth, reserves are used to increase the working capital of an enterprise. During the

periods when a business has performed poorly or during emergencies, companies can

use their reserve accounts to maintain their functions at the recommendable level. Fifth,

reserves are used to facilitate substantial financial requirements, especially when they

are created to meet a specific purpose. For instance, debentures redemption reserve

account are used to pay the debenture holders when a company cannot achieve such

payments. Failure to set reserves aside would force a company to use its working

capital to make debenture payments. Using working capital would adversely affect a

company’s operational efficiency (Davoren, 2018).

Part B: Calculations and Journal entries

Gali Ltd holds a CGU in China. There is adequate evidence showing that the CGU is

impaired. The calculation below seeks to determine the amount of reported impairment

loss based on the information provided by the company. Moreover, the entries have

been made in respective accounts that have been affected by the impairment of the

CGU.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting 10

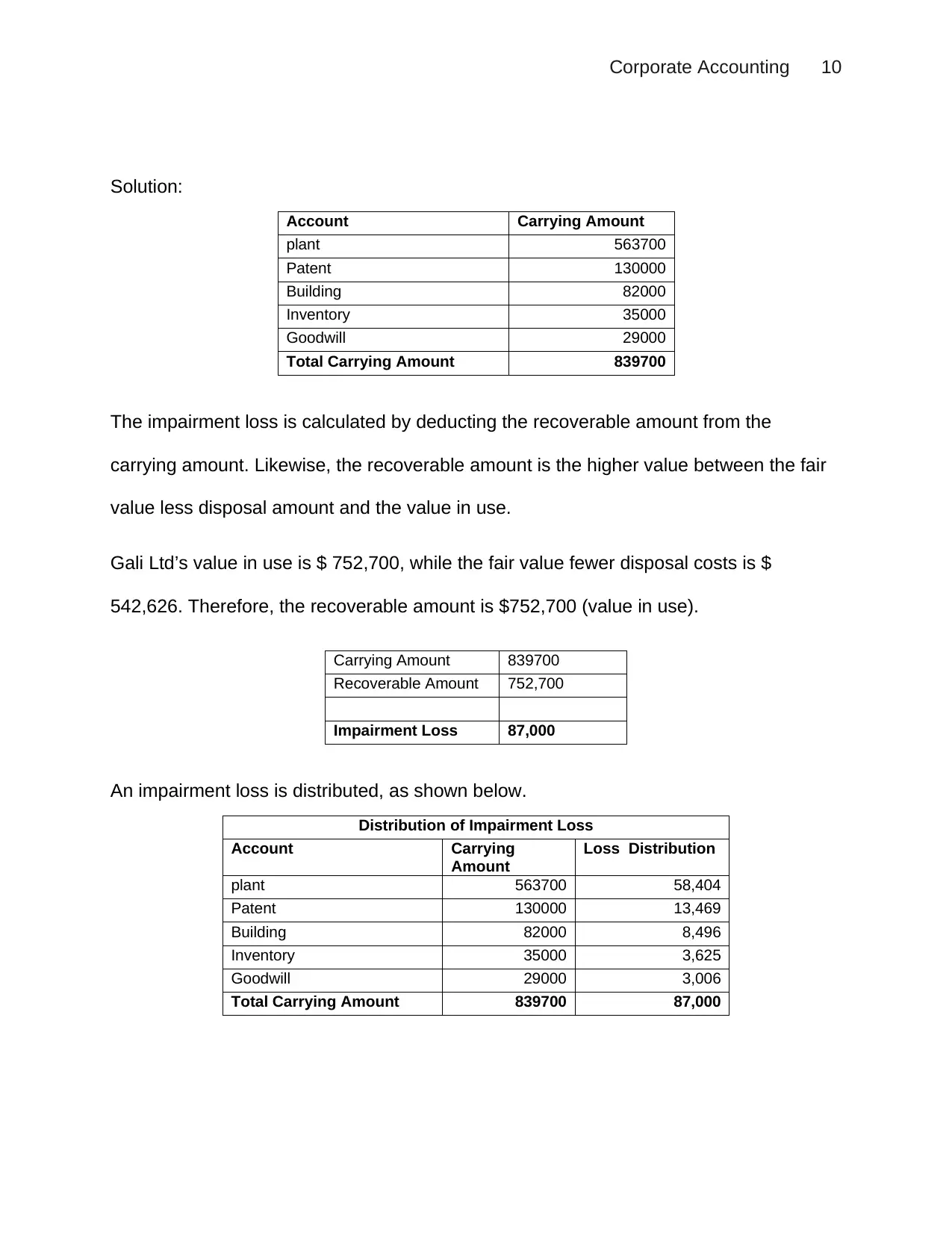

Solution:

Account Carrying Amount

plant 563700

Patent 130000

Building 82000

Inventory 35000

Goodwill 29000

Total Carrying Amount 839700

The impairment loss is calculated by deducting the recoverable amount from the

carrying amount. Likewise, the recoverable amount is the higher value between the fair

value less disposal amount and the value in use.

Gali Ltd’s value in use is $ 752,700, while the fair value fewer disposal costs is $

542,626. Therefore, the recoverable amount is $752,700 (value in use).

Carrying Amount 839700

Recoverable Amount 752,700

Impairment Loss 87,000

An impairment loss is distributed, as shown below.

Distribution of Impairment Loss

Account Carrying

Amount

Loss Distribution

plant 563700 58,404

Patent 130000 13,469

Building 82000 8,496

Inventory 35000 3,625

Goodwill 29000 3,006

Total Carrying Amount 839700 87,000

Solution:

Account Carrying Amount

plant 563700

Patent 130000

Building 82000

Inventory 35000

Goodwill 29000

Total Carrying Amount 839700

The impairment loss is calculated by deducting the recoverable amount from the

carrying amount. Likewise, the recoverable amount is the higher value between the fair

value less disposal amount and the value in use.

Gali Ltd’s value in use is $ 752,700, while the fair value fewer disposal costs is $

542,626. Therefore, the recoverable amount is $752,700 (value in use).

Carrying Amount 839700

Recoverable Amount 752,700

Impairment Loss 87,000

An impairment loss is distributed, as shown below.

Distribution of Impairment Loss

Account Carrying

Amount

Loss Distribution

plant 563700 58,404

Patent 130000 13,469

Building 82000 8,496

Inventory 35000 3,625

Goodwill 29000 3,006

Total Carrying Amount 839700 87,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting 11

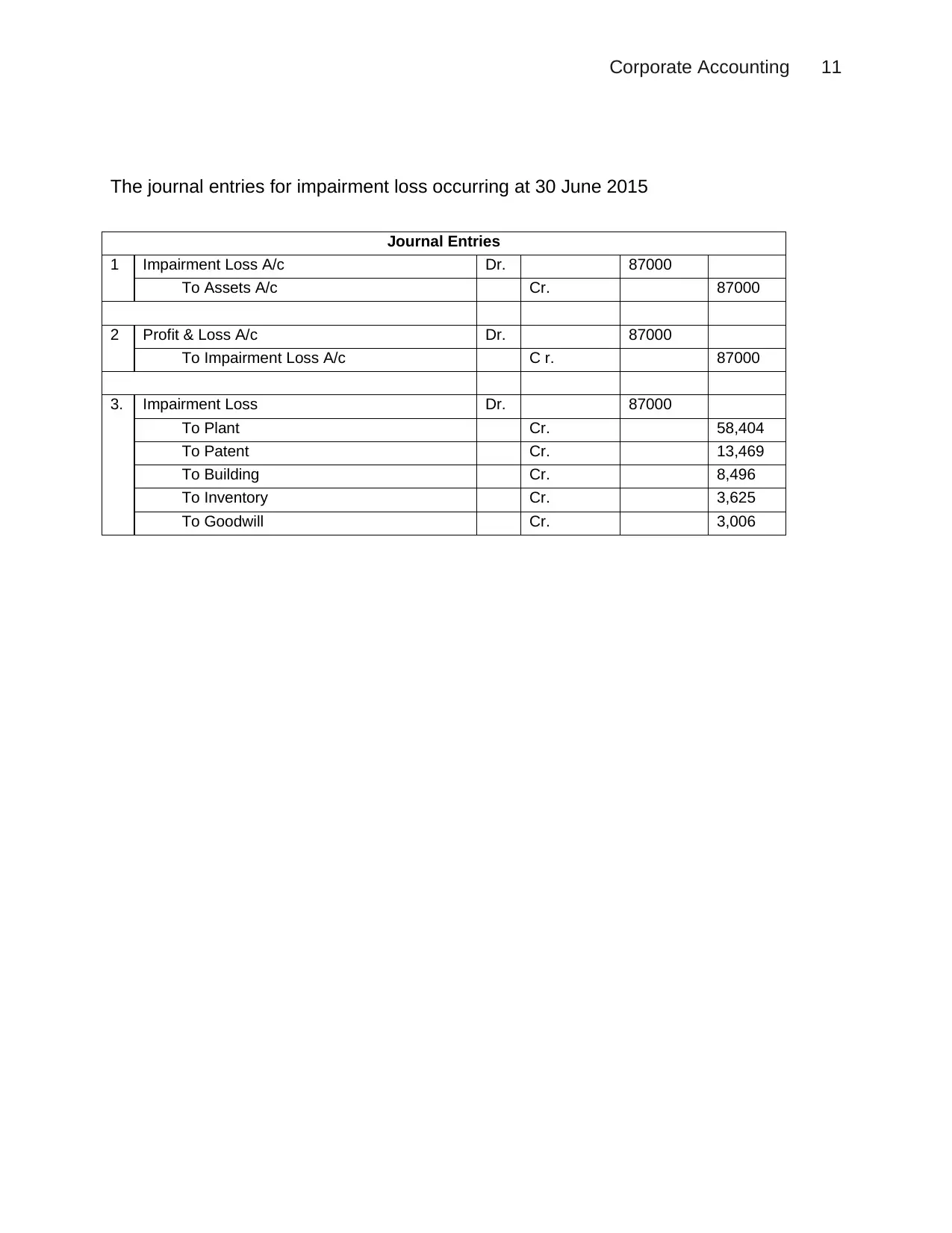

The journal entries for impairment loss occurring at 30 June 2015

Journal Entries

1 Impairment Loss A/c Dr. 87000

To Assets A/c Cr. 87000

2 Profit & Loss A/c Dr. 87000

To Impairment Loss A/c C r. 87000

3. Impairment Loss Dr. 87000

To Plant Cr. 58,404

To Patent Cr. 13,469

To Building Cr. 8,496

To Inventory Cr. 3,625

To Goodwill Cr. 3,006

The journal entries for impairment loss occurring at 30 June 2015

Journal Entries

1 Impairment Loss A/c Dr. 87000

To Assets A/c Cr. 87000

2 Profit & Loss A/c Dr. 87000

To Impairment Loss A/c C r. 87000

3. Impairment Loss Dr. 87000

To Plant Cr. 58,404

To Patent Cr. 13,469

To Building Cr. 8,496

To Inventory Cr. 3,625

To Goodwill Cr. 3,006

Corporate Accounting 12

References List

Accountingexplanation.com, 2019. Reserves. [Online]

Available at: https://www.accountingexplanation.com/reserves.htm

[Accessed 27 May 2019].

Amiraslani, H. & Iatridis, G. E., 2013. Accounting for Asset Impairment: A Test for IFRS

Compliance Across Europe: A Research Report by the Centre for Financial Analysis and

Reporting Research, Cass Business School. Illustrated ed. Bunhill Row, London: City

University Business School.

Bayoumi, T., 2012. Accounting for Reserves. Washington, DC: International Monetary

Fund.

Bhimani, A., Horngren, C. T., Datar, S. M. & Raja, M., 2015. Management and Cost

Accounting. New Delhi: Pearson Education Limited.

Davoren, J., 2018. Accounting Procedures for a Reserve Account. [Online]

Available at: https://yourbusiness.azcentral.com/accounting-procedures-reserve-

account-6850.html

[Accessed 27 May 2019].

Deegan, C., 2013. Financial accounting theory. 4th Edition ed. North Ryde, N.S.W:

McGraw-Hill Education.

Drury, C. M., 2013. Management and Cost Accounting. New York: Springer.

Edmonds, C., Edmonds, T. P., Olds, P. R. & McNair, F. M., 2015. Fundamental

Financial Accounting Concepts. New York: McGraw-Hill Education.

References List

Accountingexplanation.com, 2019. Reserves. [Online]

Available at: https://www.accountingexplanation.com/reserves.htm

[Accessed 27 May 2019].

Amiraslani, H. & Iatridis, G. E., 2013. Accounting for Asset Impairment: A Test for IFRS

Compliance Across Europe: A Research Report by the Centre for Financial Analysis and

Reporting Research, Cass Business School. Illustrated ed. Bunhill Row, London: City

University Business School.

Bayoumi, T., 2012. Accounting for Reserves. Washington, DC: International Monetary

Fund.

Bhimani, A., Horngren, C. T., Datar, S. M. & Raja, M., 2015. Management and Cost

Accounting. New Delhi: Pearson Education Limited.

Davoren, J., 2018. Accounting Procedures for a Reserve Account. [Online]

Available at: https://yourbusiness.azcentral.com/accounting-procedures-reserve-

account-6850.html

[Accessed 27 May 2019].

Deegan, C., 2013. Financial accounting theory. 4th Edition ed. North Ryde, N.S.W:

McGraw-Hill Education.

Drury, C. M., 2013. Management and Cost Accounting. New York: Springer.

Edmonds, C., Edmonds, T. P., Olds, P. R. & McNair, F. M., 2015. Fundamental

Financial Accounting Concepts. New York: McGraw-Hill Education.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.