Corporate Accounting and Reporting: Westfarmers Case Study

VerifiedAdded on 2022/11/26

|13

|3220

|260

Report

AI Summary

This report provides a comprehensive analysis of corporate accounting principles, focusing on the Westfarmers acquisition of Coles Group. It begins with an introduction to goodwill, its calculation, and its treatment after a spin-off. The report clarifies the differences between cum dividend and ex dividend in the context of share acquisitions, and it defines and explains the identification of control in business combinations. It also provides Westfarmers' income and NCI portion for 2018. Furthermore, the report delves into the concept of significant influence and its indicators, followed by a discussion of Westfarmers' associates and their goodwill treatment. Finally, the report includes a case study that encompasses acquisition analysis and the preparation of equity accounting entries in the books of Harvey Ltd. for its investment in Spector Ltd. for the years ended 2021 and 2022, providing a practical application of the concepts discussed throughout the report.

Corporate Accounting and Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction.................................................................................................................................................2

Solution-1....................................................................................................................................................3

(a) Meaning of goodwill....................................................................................................................3

(b) Treatment of previously recognized goodwill..............................................................................3

(c) Difference between cum dividend and ex dividend.....................................................................4

(d) Definition of control and identification of control.......................................................................5

(e) Westfarmers income and NCI portion in 2018.............................................................................5

Solution-2....................................................................................................................................................6

(a) Explanation of term significant influence and its indicators........................................................6

(b) Listing of Westfarmers associates and treatment of goodwill in these investments.....................8

Solution-3....................................................................................................................................................9

(a) Preparation of Acquisition analysis as on 1 July, 2020................................................................9

(b) Equity accounting entries in the books of Harvey Ltd on consolidation for the investment in

Spector Ltd for the year ended 30 June, 2021..........................................................................................9

(b) Equity accounting entries in the books of Harvey Ltd on consolidation for the investment in

Spector Ltd for the year ended 30 June, 2022........................................................................................10

References.................................................................................................................................................12

Introduction.................................................................................................................................................2

Solution-1....................................................................................................................................................3

(a) Meaning of goodwill....................................................................................................................3

(b) Treatment of previously recognized goodwill..............................................................................3

(c) Difference between cum dividend and ex dividend.....................................................................4

(d) Definition of control and identification of control.......................................................................5

(e) Westfarmers income and NCI portion in 2018.............................................................................5

Solution-2....................................................................................................................................................6

(a) Explanation of term significant influence and its indicators........................................................6

(b) Listing of Westfarmers associates and treatment of goodwill in these investments.....................8

Solution-3....................................................................................................................................................9

(a) Preparation of Acquisition analysis as on 1 July, 2020................................................................9

(b) Equity accounting entries in the books of Harvey Ltd on consolidation for the investment in

Spector Ltd for the year ended 30 June, 2021..........................................................................................9

(b) Equity accounting entries in the books of Harvey Ltd on consolidation for the investment in

Spector Ltd for the year ended 30 June, 2022........................................................................................10

References.................................................................................................................................................12

Introduction

The given report is about the Westfarmers acquisition of Coles Group. It lights out the major information

about the aforementioned business combination and explains few important factors. The report has three

major portions.

Solution-1 talks about the Westfarmers acquisition of Coles group alongwith explanation of goodwill and

meaning of control. Further, the net income earned and the NCI portion of Westfarmers for the year 2018

is also provided.

The solution-2 talks about significant influence and its indicators. Further, it includes the list of

Westfarmers associates and accounting of their goodwill.

The last portion, i.e. solution-3 is a case study of accounting for associates and includes the acquisition

analysis and journal entries to record the equity accounting entries in the books of Harvey Ltd. for

investment in Spector Ltd. for the financial years 2021 and 2022.

The given report is about the Westfarmers acquisition of Coles Group. It lights out the major information

about the aforementioned business combination and explains few important factors. The report has three

major portions.

Solution-1 talks about the Westfarmers acquisition of Coles group alongwith explanation of goodwill and

meaning of control. Further, the net income earned and the NCI portion of Westfarmers for the year 2018

is also provided.

The solution-2 talks about significant influence and its indicators. Further, it includes the list of

Westfarmers associates and accounting of their goodwill.

The last portion, i.e. solution-3 is a case study of accounting for associates and includes the acquisition

analysis and journal entries to record the equity accounting entries in the books of Harvey Ltd. for

investment in Spector Ltd. for the financial years 2021 and 2022.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Solution-1

(a) Meaning of goodwill

Goodwill is an intangible asset which has no physical substance but has some future economic

benefits for the entity. These future economic benefits can be in the form of inflow of resource or

any other benefits accruing to the company in direct or indirect form. Generally, goodwill is

recorded at the time of acquisition of another business and represents the excess consideration

paid on business combination. In simple terms, the goodwill is the excess consideration paid over

the net book value of identifiable assets and liabilities. This net book value of assets and liabilities

represents the value of business that is being acquired. For instance, the net book value of assets

& liabilities acquired is $100 and the company has paid $110 to acquire the said company. So, the

goodwill will be $10 ($110 - $100). This goodwill needs to be recorded as an intangible asset in

the books and represents the benefits that will accrue to the company in near future. These

benefits can be monetary or non-monetary.

Para 51 of AASB 3, “Business Combinations” allows the investor company to record and

recognize the goodwill acquired in a business combination and clearly states that goodwill is the

excess of the cost of business combination over the acquirer’s interest in the net fair value of the

identifiable assets, liabilities and contingent liabilities.

Goodwill to be recorded by Westfarmers on acquisition of Coles Group will be approx. 7.17

billion. This is calculated by dividing the acquisition cost with the premium paid on Colus shares.

The Westfarmers has paid $22 billion to acquire Colus group and paid $17 ex dividend per share.

This cost per share represents 48.4% premium. Hence, the excess consideration paid is 48.4%.So,

the goodwill is 7.17 billion.

(b) Treatment of previously recognized goodwill

The goodwill recognized in business combination is never amortised but it is tested for

impairment at every reporting period end. The para 56 of AASB 3, “Business Combinations”,

states that,

(a) Meaning of goodwill

Goodwill is an intangible asset which has no physical substance but has some future economic

benefits for the entity. These future economic benefits can be in the form of inflow of resource or

any other benefits accruing to the company in direct or indirect form. Generally, goodwill is

recorded at the time of acquisition of another business and represents the excess consideration

paid on business combination. In simple terms, the goodwill is the excess consideration paid over

the net book value of identifiable assets and liabilities. This net book value of assets and liabilities

represents the value of business that is being acquired. For instance, the net book value of assets

& liabilities acquired is $100 and the company has paid $110 to acquire the said company. So, the

goodwill will be $10 ($110 - $100). This goodwill needs to be recorded as an intangible asset in

the books and represents the benefits that will accrue to the company in near future. These

benefits can be monetary or non-monetary.

Para 51 of AASB 3, “Business Combinations” allows the investor company to record and

recognize the goodwill acquired in a business combination and clearly states that goodwill is the

excess of the cost of business combination over the acquirer’s interest in the net fair value of the

identifiable assets, liabilities and contingent liabilities.

Goodwill to be recorded by Westfarmers on acquisition of Coles Group will be approx. 7.17

billion. This is calculated by dividing the acquisition cost with the premium paid on Colus shares.

The Westfarmers has paid $22 billion to acquire Colus group and paid $17 ex dividend per share.

This cost per share represents 48.4% premium. Hence, the excess consideration paid is 48.4%.So,

the goodwill is 7.17 billion.

(b) Treatment of previously recognized goodwill

The goodwill recognized in business combination is never amortised but it is tested for

impairment at every reporting period end. The para 56 of AASB 3, “Business Combinations”,

states that,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

“Goodwill acquired in a business combination shall not be amortised. Instead, the acquirer shall

test it for impairment annually, or more frequently if events or changes in circumstances indicate

that it might be impaired, in accordance with AASB 136 Impairment of Assets.”. (2019)

So, the goodwill will continue in the books of Westfarmers, even if Coles has spun off from the

Westfarmers family. However, the Westfarmers is required to test the goodwill for impairment at

every period end, or as and when indicators of impairment is evident.

(c) Difference between cum dividend and ex dividend

The purchase price paid during the business combination plays a vital role as the entire business

combination deals depends on the purchase consideration paid or transferred. Money is the

ultimate important factor for which the businesses run, so taking care of this factor is of utmost

importance.

During the business combination, the investor pays to the shareholders of investee company to

acquire their stake in the investee company. This stake is in the form of shares and the offered

purchase price can be cum dividend or ex divided.

Cum dividend means when the company in near future going to give dividend on its shares, in

other words, the company has declared the dividend, but its payout is still pending. At this stage,

the company has given the notice to the shareholders to pay the dividend but the amount of

dividend to be paid is not finalized, neither the list of shareholders who are going to receive the

dividend is finalized. If at this stage, the investor acquires the shares, then the person / entity

holding the shares will be entitled to the dividends, even though the investor has not earned the

dividend, but he will be going to receive the same since he is holding the shares at the cut-off

date. If the investor purchases the shares at cum dividend stage, then the amount paid by him will

be higher than the normal price, and this higher amount is due to inclusion of dividend in the

purchase cost. ("Cum Dividend Is When a Company Is Gearing up to Pay a Dividend", 2019)

On the other hand, ex-dividend means that the company has finalized the list of names of

shareholders who are going to receive the dividend. Since, the list of the shareholders is identified

and locked, so purchasing the shares at this stage will not entitle the investor company for

test it for impairment annually, or more frequently if events or changes in circumstances indicate

that it might be impaired, in accordance with AASB 136 Impairment of Assets.”. (2019)

So, the goodwill will continue in the books of Westfarmers, even if Coles has spun off from the

Westfarmers family. However, the Westfarmers is required to test the goodwill for impairment at

every period end, or as and when indicators of impairment is evident.

(c) Difference between cum dividend and ex dividend

The purchase price paid during the business combination plays a vital role as the entire business

combination deals depends on the purchase consideration paid or transferred. Money is the

ultimate important factor for which the businesses run, so taking care of this factor is of utmost

importance.

During the business combination, the investor pays to the shareholders of investee company to

acquire their stake in the investee company. This stake is in the form of shares and the offered

purchase price can be cum dividend or ex divided.

Cum dividend means when the company in near future going to give dividend on its shares, in

other words, the company has declared the dividend, but its payout is still pending. At this stage,

the company has given the notice to the shareholders to pay the dividend but the amount of

dividend to be paid is not finalized, neither the list of shareholders who are going to receive the

dividend is finalized. If at this stage, the investor acquires the shares, then the person / entity

holding the shares will be entitled to the dividends, even though the investor has not earned the

dividend, but he will be going to receive the same since he is holding the shares at the cut-off

date. If the investor purchases the shares at cum dividend stage, then the amount paid by him will

be higher than the normal price, and this higher amount is due to inclusion of dividend in the

purchase cost. ("Cum Dividend Is When a Company Is Gearing up to Pay a Dividend", 2019)

On the other hand, ex-dividend means that the company has finalized the list of names of

shareholders who are going to receive the dividend. Since, the list of the shareholders is identified

and locked, so purchasing the shares at this stage will not entitle the investor company for

receiving of dividends and hence, the price paid by the investor to acquire the shares, will include

the shares cost only.

(d) Definition of control and identification of control

Control in general terms means the power to influence another person or events or transactions.

In a business combination, the control means the act of influencing the business or decision of

another entity. It means that the person or company has a right to change or influence the entity’s

decisions. The control over another entity is generally gained by acquiring more than 50% the

shares of the entity. However, the company is said to be under the control of another company

when the controlling company has the power to govern the controlled entities financial, non-

financial and operating decisions or policies to obtain the benefits from its activities.

The control can be identified in a business combination by the following means:

(i) When the controlling company has more than 50% of the voting power in the controlled

entity by virtue of an agreement with the investors. It simply means holding more than

50% of the equity shares of the company.

(ii) When the controlling company has power to govern or operate the financial and

operating policies of the controlled entity.

(iii) When the controlling company has the power to appoint or remove the majority of

directors on the controlled entity board or any other governing body. Since, if the

controlling entity has majority of directors on board, then any decision which the

controlling entity wants can be taken.

(iv) When the controlling company has the power to cast majority of votes at the board of

directors meeting or any other major meetings.

(e) Westfarmers income and NCI portion in 2018

The company’s profit before tax as per company’s 2018 annual report is $3,850 million and profit

after tax is $2,604 million.

There is no NCI portion on company’s portion of 2018 income. (2019)

the shares cost only.

(d) Definition of control and identification of control

Control in general terms means the power to influence another person or events or transactions.

In a business combination, the control means the act of influencing the business or decision of

another entity. It means that the person or company has a right to change or influence the entity’s

decisions. The control over another entity is generally gained by acquiring more than 50% the

shares of the entity. However, the company is said to be under the control of another company

when the controlling company has the power to govern the controlled entities financial, non-

financial and operating decisions or policies to obtain the benefits from its activities.

The control can be identified in a business combination by the following means:

(i) When the controlling company has more than 50% of the voting power in the controlled

entity by virtue of an agreement with the investors. It simply means holding more than

50% of the equity shares of the company.

(ii) When the controlling company has power to govern or operate the financial and

operating policies of the controlled entity.

(iii) When the controlling company has the power to appoint or remove the majority of

directors on the controlled entity board or any other governing body. Since, if the

controlling entity has majority of directors on board, then any decision which the

controlling entity wants can be taken.

(iv) When the controlling company has the power to cast majority of votes at the board of

directors meeting or any other major meetings.

(e) Westfarmers income and NCI portion in 2018

The company’s profit before tax as per company’s 2018 annual report is $3,850 million and profit

after tax is $2,604 million.

There is no NCI portion on company’s portion of 2018 income. (2019)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Solution-2

(a) Explanation of term significant influence and its indicators

Significant influence means having the power and not control to participate in the financial and operating

decisions of the investee company. It means the investor company has power to participate in the business

of the company and can influence the decisions of the investee company, but the investor company can

not control the decisions or can not change the decisions of investee company.

As per AASB 128, “Investments in associates and joint ventures”, para 5, significant influence arises

when the investor company holds more than 20% in the investee company either directly or indirectly. It

is generally presumed that if the investor company has voting power of more than 20% in the investee

company than the investor company has significant influence over the investee company. However, in

every case this does not holds true. On the contrary, if any investor company holds less than 20% of

voting power in an investee company, than it is said that the investor company does not have significant

influence over investee company. This also does not hold true in every case. (2019)

So, the question arises that when it is said that the investor company has significant influence over the

investee company. So, the following situations or circumstances if holds good leads the significant

influence of investor company over investee company.

1. Significant representation or participation on the board of directors – if the investor company has

significant members present on the board of directors of the investee company, and those members

can influence the decisions taken by the investee company’s board of directors, then it is said that

the investor company has significant influence over the investee company.

2. Participation in decision making – If the investor company has right and power to participate in the

decision-making process or policy preparation process of investee company and specifically

decision related to distribution and declaration of dividends or any other appropriation of profits,

then it is said that the investor company has significant influence over the investee company.

3. Major transactions – If there are any major transactions relating to supply of material or sale of

goods or services or any other material transactions between the investee company and investor

company, then it is said that the investor company has significant influence over the investee

company. This is because, if investee company has some material transaction with investor

(a) Explanation of term significant influence and its indicators

Significant influence means having the power and not control to participate in the financial and operating

decisions of the investee company. It means the investor company has power to participate in the business

of the company and can influence the decisions of the investee company, but the investor company can

not control the decisions or can not change the decisions of investee company.

As per AASB 128, “Investments in associates and joint ventures”, para 5, significant influence arises

when the investor company holds more than 20% in the investee company either directly or indirectly. It

is generally presumed that if the investor company has voting power of more than 20% in the investee

company than the investor company has significant influence over the investee company. However, in

every case this does not holds true. On the contrary, if any investor company holds less than 20% of

voting power in an investee company, than it is said that the investor company does not have significant

influence over investee company. This also does not hold true in every case. (2019)

So, the question arises that when it is said that the investor company has significant influence over the

investee company. So, the following situations or circumstances if holds good leads the significant

influence of investor company over investee company.

1. Significant representation or participation on the board of directors – if the investor company has

significant members present on the board of directors of the investee company, and those members

can influence the decisions taken by the investee company’s board of directors, then it is said that

the investor company has significant influence over the investee company.

2. Participation in decision making – If the investor company has right and power to participate in the

decision-making process or policy preparation process of investee company and specifically

decision related to distribution and declaration of dividends or any other appropriation of profits,

then it is said that the investor company has significant influence over the investee company.

3. Major transactions – If there are any major transactions relating to supply of material or sale of

goods or services or any other material transactions between the investee company and investor

company, then it is said that the investor company has significant influence over the investee

company. This is because, if investee company has some material transaction with investor

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company, then at any point of time investor company can disturb the business of investee company.

For instance, the investor company supplies 80% of the raw material required for production to

investee company, in this situation, the investor company has a significant influence over investee

company, because at any point of time the investor company can stop supply of material which will

badly damage the business of investee company.

4. Interchange of managerial personnel – If the investee company and investor company have some

arrangement for interchange of employees involved in the management of the company, then the

investor company has significant influence over investee company, since it have access to

confidential information of investee company, which can be used against the investee company for

influencing the decisions of the investee company in favor of investor company.

5. Access to important technical information – If the investor company has access to important

technical and crucial information of the investee company, then the investor company has significant

influence over the investee company. Because the technical information regarding a company is

most important factor for running the business of the company. Sharing of this information with 3rd

parties, can badly damage the business and image of the company in the market resulting into huge

losses or even shutting off of business.

6. Having 20% of more voting power – If the investor company has more than 20% voting power of

the investee company, then the investor company has significant influence over investee company.

This is so because, in any company the shareholders are the owners who are entitled to take the

major decisions of the company. If the investor company has 20% or more shares in the investee

company, then it means that the investor company has 20% voting power in the decision making of

the investee company and can influence the decisions of the investee company.

7. Having instruments with potential voting rights – If the investor company has voting power of less

than 20% in the investee company but the investor company holds instruments in the investee

company which are going to convert in equity instruments in a future date and such potential

instruments along with equity instruments constitute 20% or more of the total instrument, then also

the investor company has significant influence over the investee company. As in present the investor

company has less than 20% voting power but in the near future the company is going to gain the

20% voting power in the investee company.

For instance, the investor company supplies 80% of the raw material required for production to

investee company, in this situation, the investor company has a significant influence over investee

company, because at any point of time the investor company can stop supply of material which will

badly damage the business of investee company.

4. Interchange of managerial personnel – If the investee company and investor company have some

arrangement for interchange of employees involved in the management of the company, then the

investor company has significant influence over investee company, since it have access to

confidential information of investee company, which can be used against the investee company for

influencing the decisions of the investee company in favor of investor company.

5. Access to important technical information – If the investor company has access to important

technical and crucial information of the investee company, then the investor company has significant

influence over the investee company. Because the technical information regarding a company is

most important factor for running the business of the company. Sharing of this information with 3rd

parties, can badly damage the business and image of the company in the market resulting into huge

losses or even shutting off of business.

6. Having 20% of more voting power – If the investor company has more than 20% voting power of

the investee company, then the investor company has significant influence over investee company.

This is so because, in any company the shareholders are the owners who are entitled to take the

major decisions of the company. If the investor company has 20% or more shares in the investee

company, then it means that the investor company has 20% voting power in the decision making of

the investee company and can influence the decisions of the investee company.

7. Having instruments with potential voting rights – If the investor company has voting power of less

than 20% in the investee company but the investor company holds instruments in the investee

company which are going to convert in equity instruments in a future date and such potential

instruments along with equity instruments constitute 20% or more of the total instrument, then also

the investor company has significant influence over the investee company. As in present the investor

company has less than 20% voting power but in the near future the company is going to gain the

20% voting power in the investee company.

Hence, if any of the above indicator is present in the relation of investor and investee company, then the

investor company has significant influence over the investee company.

(b) Listing of Westfarmers associates and treatment of goodwill in these investments

Westfarmers group is a big group which has diversified investment in many industries. Besides having

subsidiaries, the company has many associates and joint ventures as well. According to the company’s

2018 annual report, the businesses in which Wesfarmers is an associate are:

1. Australian Energy Consortium Pty Ltd

2. Bengalla Coal Sales Company Pty Limited

3. Bengalla Mining Company Pty Limited

4. BWP Trust

5. Gresham Partners Group Limited

6. Gresham Private Equity Funds

7. Queensland Nitrates Management Pty Ltd

8. Queensland Nitrates Pty Ltd

9. Wespine Industries Pty Ltd

Goodwill in these investments relating to associates is included in the carrying amount of the investment

and is not amortised in the profit & loss. The investment is recorded as per the equity method and the

Group determines whether it is necessary to recognise any additional impairment loss with respect to the

Group’s investment. The Group’s income statement reflects the Group’s share of the associate’s result.

(2019)

investor company has significant influence over the investee company.

(b) Listing of Westfarmers associates and treatment of goodwill in these investments

Westfarmers group is a big group which has diversified investment in many industries. Besides having

subsidiaries, the company has many associates and joint ventures as well. According to the company’s

2018 annual report, the businesses in which Wesfarmers is an associate are:

1. Australian Energy Consortium Pty Ltd

2. Bengalla Coal Sales Company Pty Limited

3. Bengalla Mining Company Pty Limited

4. BWP Trust

5. Gresham Partners Group Limited

6. Gresham Private Equity Funds

7. Queensland Nitrates Management Pty Ltd

8. Queensland Nitrates Pty Ltd

9. Wespine Industries Pty Ltd

Goodwill in these investments relating to associates is included in the carrying amount of the investment

and is not amortised in the profit & loss. The investment is recorded as per the equity method and the

Group determines whether it is necessary to recognise any additional impairment loss with respect to the

Group’s investment. The Group’s income statement reflects the Group’s share of the associate’s result.

(2019)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Solution-3

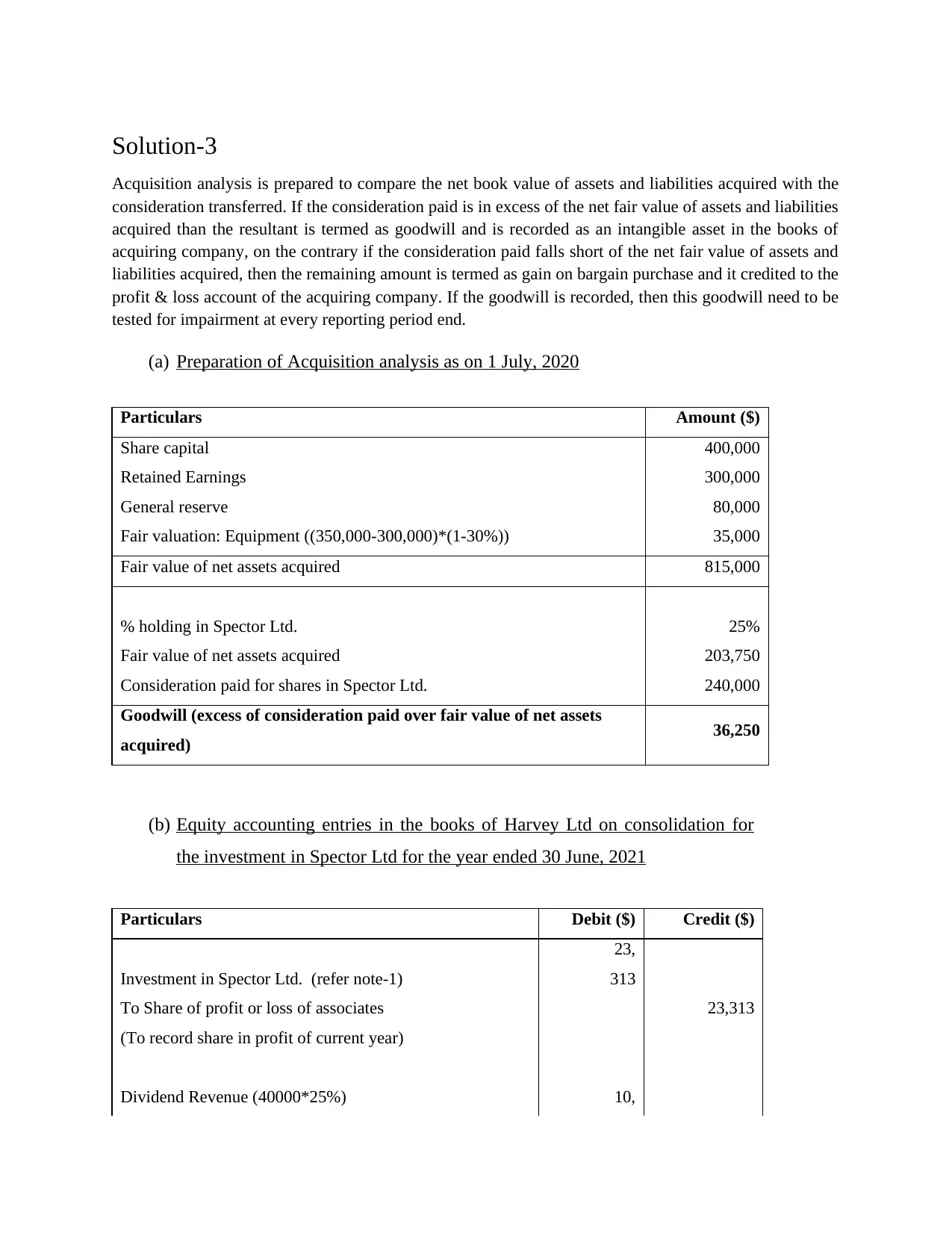

Acquisition analysis is prepared to compare the net book value of assets and liabilities acquired with the

consideration transferred. If the consideration paid is in excess of the net fair value of assets and liabilities

acquired than the resultant is termed as goodwill and is recorded as an intangible asset in the books of

acquiring company, on the contrary if the consideration paid falls short of the net fair value of assets and

liabilities acquired, then the remaining amount is termed as gain on bargain purchase and it credited to the

profit & loss account of the acquiring company. If the goodwill is recorded, then this goodwill need to be

tested for impairment at every reporting period end.

(a) Preparation of Acquisition analysis as on 1 July, 2020

Particulars Amount ($)

Share capital 400,000

Retained Earnings 300,000

General reserve 80,000

Fair valuation: Equipment ((350,000-300,000)*(1-30%)) 35,000

Fair value of net assets acquired 815,000

% holding in Spector Ltd. 25%

Fair value of net assets acquired 203,750

Consideration paid for shares in Spector Ltd. 240,000

Goodwill (excess of consideration paid over fair value of net assets

acquired) 36,250

(b) Equity accounting entries in the books of Harvey Ltd on consolidation for

the investment in Spector Ltd for the year ended 30 June, 2021

Particulars Debit ($) Credit ($)

Investment in Spector Ltd. (refer note-1)

23,

313

To Share of profit or loss of associates 23,313

(To record share in profit of current year)

Dividend Revenue (40000*25%) 10,

Acquisition analysis is prepared to compare the net book value of assets and liabilities acquired with the

consideration transferred. If the consideration paid is in excess of the net fair value of assets and liabilities

acquired than the resultant is termed as goodwill and is recorded as an intangible asset in the books of

acquiring company, on the contrary if the consideration paid falls short of the net fair value of assets and

liabilities acquired, then the remaining amount is termed as gain on bargain purchase and it credited to the

profit & loss account of the acquiring company. If the goodwill is recorded, then this goodwill need to be

tested for impairment at every reporting period end.

(a) Preparation of Acquisition analysis as on 1 July, 2020

Particulars Amount ($)

Share capital 400,000

Retained Earnings 300,000

General reserve 80,000

Fair valuation: Equipment ((350,000-300,000)*(1-30%)) 35,000

Fair value of net assets acquired 815,000

% holding in Spector Ltd. 25%

Fair value of net assets acquired 203,750

Consideration paid for shares in Spector Ltd. 240,000

Goodwill (excess of consideration paid over fair value of net assets

acquired) 36,250

(b) Equity accounting entries in the books of Harvey Ltd on consolidation for

the investment in Spector Ltd for the year ended 30 June, 2021

Particulars Debit ($) Credit ($)

Investment in Spector Ltd. (refer note-1)

23,

313

To Share of profit or loss of associates 23,313

(To record share in profit of current year)

Dividend Revenue (40000*25%) 10,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

000

To Investment in Spector Ltd. 10,000

(To record receipt of dividend paid by Spector Ltd.)

(b) Equity accounting entries in the books of Harvey Ltd on consolidation for

the investment in Spector Ltd for the year ended 30 June, 2022

Particulars Debit ($) Credit ($)

Investment in Spector Ltd. (refer note-2) 1,688

To Share of profit or loss of associates 1,688

(To record share in profit of current year)

Investment in Spector Ltd. (90000*25%) 22,500

To Asset revaluation surplus 22,500

(To record share in revaluation surplus)

Dividend Revenue (30000*25%) 7,500

To Investment in Spector Ltd. 7,500

(To record receipt of dividend paid by Spector Ltd.)

Note-1: Calculation of Share in profit for the year ended 2021

Particulars Amount ($)

Profit for the year 95,000

Adjustments for inter-company transactions:

Depreciation on fair valuation of equipment (50,000/20*(1-30%)) (1,750)

Net Profit 93,250

Investor's share 25%

Investor's share in profit 23,313

To Investment in Spector Ltd. 10,000

(To record receipt of dividend paid by Spector Ltd.)

(b) Equity accounting entries in the books of Harvey Ltd on consolidation for

the investment in Spector Ltd for the year ended 30 June, 2022

Particulars Debit ($) Credit ($)

Investment in Spector Ltd. (refer note-2) 1,688

To Share of profit or loss of associates 1,688

(To record share in profit of current year)

Investment in Spector Ltd. (90000*25%) 22,500

To Asset revaluation surplus 22,500

(To record share in revaluation surplus)

Dividend Revenue (30000*25%) 7,500

To Investment in Spector Ltd. 7,500

(To record receipt of dividend paid by Spector Ltd.)

Note-1: Calculation of Share in profit for the year ended 2021

Particulars Amount ($)

Profit for the year 95,000

Adjustments for inter-company transactions:

Depreciation on fair valuation of equipment (50,000/20*(1-30%)) (1,750)

Net Profit 93,250

Investor's share 25%

Investor's share in profit 23,313

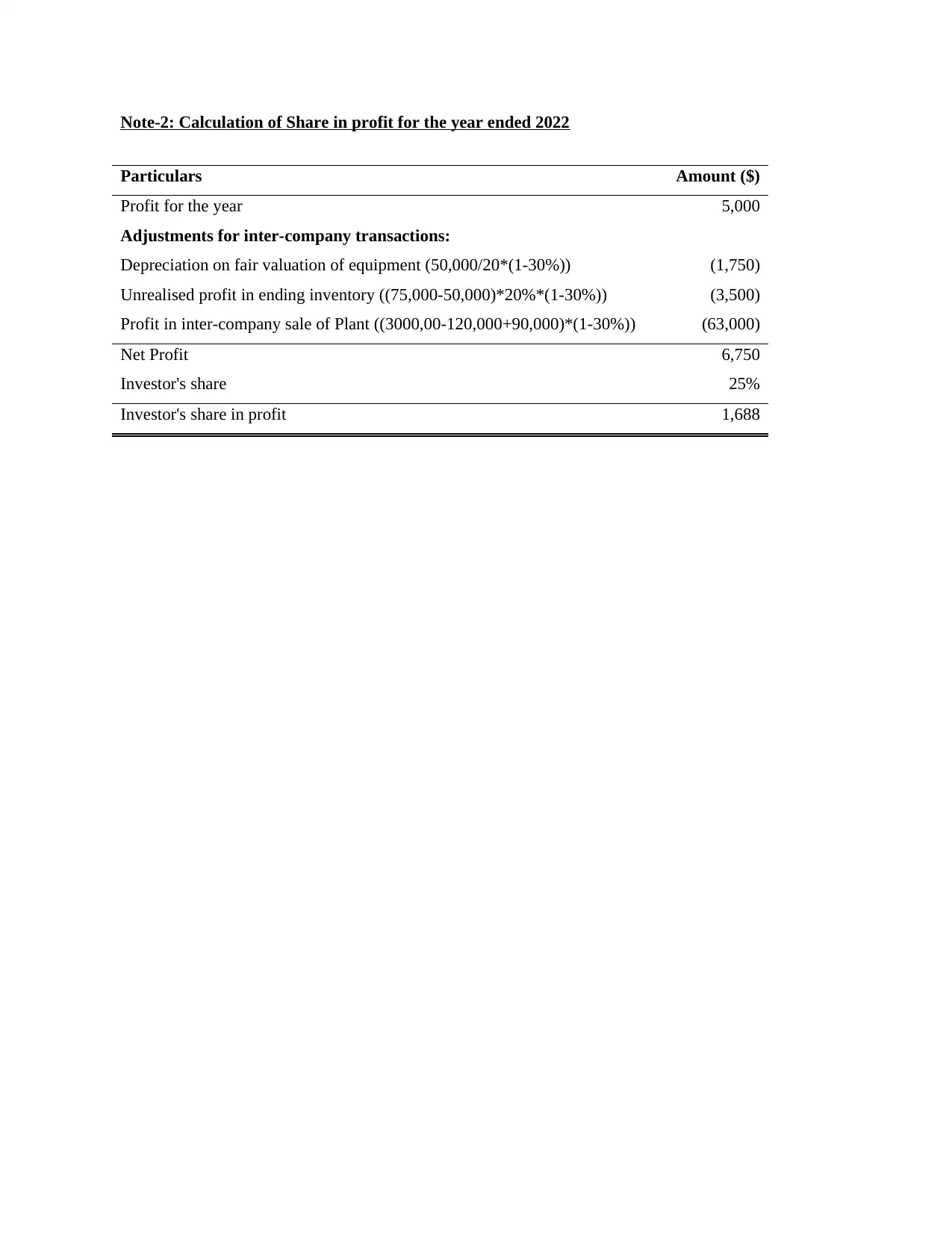

Note-2: Calculation of Share in profit for the year ended 2022

Particulars Amount ($)

Profit for the year 5,000

Adjustments for inter-company transactions:

Depreciation on fair valuation of equipment (50,000/20*(1-30%)) (1,750)

Unrealised profit in ending inventory ((75,000-50,000)*20%*(1-30%)) (3,500)

Profit in inter-company sale of Plant ((3000,00-120,000+90,000)*(1-30%)) (63,000)

Net Profit 6,750

Investor's share 25%

Investor's share in profit 1,688

Particulars Amount ($)

Profit for the year 5,000

Adjustments for inter-company transactions:

Depreciation on fair valuation of equipment (50,000/20*(1-30%)) (1,750)

Unrealised profit in ending inventory ((75,000-50,000)*20%*(1-30%)) (3,500)

Profit in inter-company sale of Plant ((3000,00-120,000+90,000)*(1-30%)) (63,000)

Net Profit 6,750

Investor's share 25%

Investor's share in profit 1,688

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.