Corporate Accounting Report: Adelaide Brighton and Alumina Analysis

VerifiedAdded on 2022/10/17

|16

|2922

|16

Report

AI Summary

This report undertakes a comparative analysis of the financial performance of Adelaide Brighton Ltd and Alumina Ltd, both listed on the ASX, over a three-year period. The analysis focuses on the movement of items within the balance sheet, specifically examining owners' equity and liabilities. The report details the components of owners' equity (share capital, reserves, retained earnings) and liabilities (trade payables, borrowings, provisions, etc.) for both companies, explaining the trends and fluctuations in these items. The advantages and disadvantages of each company's sources of funding are also assessed. Furthermore, the report provides a critical examination of the concepts of small proprietary companies, large proprietary companies, and reporting entities, including the implications of each classification. The report concludes with a summary of the key findings and insights derived from the financial analysis and entity classifications.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student

Name of the University

Authors Note

Course ID

Corporate Accounting

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ACCOUNTING

Executive Summary:

The report here focuses on companies taken from the materials sector. The companies

selected in this report is Adelaide Brighton Ltd and Alumina Ltd that are listed in the top 200

of the ASX. The report would consider the last three years’ period of both the companies to

understand the movement of its balance sheet items. Apart from this, a critical examination of

the concepts of small proprietary firm, large proprietary firm and reporting entity will be also

considered as well. The financial performance of the both the companies along with the

movement in the owners’ equity and liabilities will also be considered as well.

Executive Summary:

The report here focuses on companies taken from the materials sector. The companies

selected in this report is Adelaide Brighton Ltd and Alumina Ltd that are listed in the top 200

of the ASX. The report would consider the last three years’ period of both the companies to

understand the movement of its balance sheet items. Apart from this, a critical examination of

the concepts of small proprietary firm, large proprietary firm and reporting entity will be also

considered as well. The financial performance of the both the companies along with the

movement in the owners’ equity and liabilities will also be considered as well.

2CORPORATE ACCOUNTING

Table of Contents

Introduction:...............................................................................................................................4

Part A:........................................................................................................................................4

Items recorded under owners’ equity section:.......................................................................4

Movement of each item under owner equity:........................................................................7

Items recorded under liabilities section:................................................................................7

Movements in each item recorded in liabilities section:........................................................9

Advantage or disadvantage of sources of fund:...................................................................10

Part B:.......................................................................................................................................11

Critical examination of concepts of small proprietary company, large proprietary company

and reporting entity:.............................................................................................................11

Implications of being classified as any one of the companies:............................................12

Conclusion:..............................................................................................................................13

References:...............................................................................................................................14

Table of Contents

Introduction:...............................................................................................................................4

Part A:........................................................................................................................................4

Items recorded under owners’ equity section:.......................................................................4

Movement of each item under owner equity:........................................................................7

Items recorded under liabilities section:................................................................................7

Movements in each item recorded in liabilities section:........................................................9

Advantage or disadvantage of sources of fund:...................................................................10

Part B:.......................................................................................................................................11

Critical examination of concepts of small proprietary company, large proprietary company

and reporting entity:.............................................................................................................11

Implications of being classified as any one of the companies:............................................12

Conclusion:..............................................................................................................................13

References:...............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ACCOUNTING

Introduction:

Corporate accounting is regarded as the special branch of accounting that is associated

with the bookkeeping for businesses, preparing the financial accounts and the cash flow

reports. The corporate accounting is also associated with the analysis, interpretation of the

businesses financial outcomes and preparing the consolidated balance sheets (Williams and

Dobelman 2017). The corporate accounting facilitates the comparative analysis of the

financial statement that provides the users with the information for assessing the change in

direction of business. The financial performance is viewed as measuring the overall financial

condition of the company over the given time period.

The present report is based on two ASX listed companies namely the Adelaide

Brighton Ltd, Alumina Ltd. The report would consider the last three years’ period of both the

companies to understand the movement of its balance sheet items. Apart from this, a critical

examination of the concepts of small proprietary firm, large proprietary firm and reporting

entity will be also considered as well.

Part A:

Items recorded under owners’ equity section:

The owners’ equity is viewed as investment of the owner’s in their business less the

owner’s withdrawal from the business plus the total amount of net income from the time

when the business commenced (Crowther 2018). It is regarded as one of the three main

sections of an organization’s balance sheet. It mainly comprises of equity capital, general

reserve and retained earnings.

Adelaide Brighton –

Introduction:

Corporate accounting is regarded as the special branch of accounting that is associated

with the bookkeeping for businesses, preparing the financial accounts and the cash flow

reports. The corporate accounting is also associated with the analysis, interpretation of the

businesses financial outcomes and preparing the consolidated balance sheets (Williams and

Dobelman 2017). The corporate accounting facilitates the comparative analysis of the

financial statement that provides the users with the information for assessing the change in

direction of business. The financial performance is viewed as measuring the overall financial

condition of the company over the given time period.

The present report is based on two ASX listed companies namely the Adelaide

Brighton Ltd, Alumina Ltd. The report would consider the last three years’ period of both the

companies to understand the movement of its balance sheet items. Apart from this, a critical

examination of the concepts of small proprietary firm, large proprietary firm and reporting

entity will be also considered as well.

Part A:

Items recorded under owners’ equity section:

The owners’ equity is viewed as investment of the owner’s in their business less the

owner’s withdrawal from the business plus the total amount of net income from the time

when the business commenced (Crowther 2018). It is regarded as one of the three main

sections of an organization’s balance sheet. It mainly comprises of equity capital, general

reserve and retained earnings.

Adelaide Brighton –

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ACCOUNTING

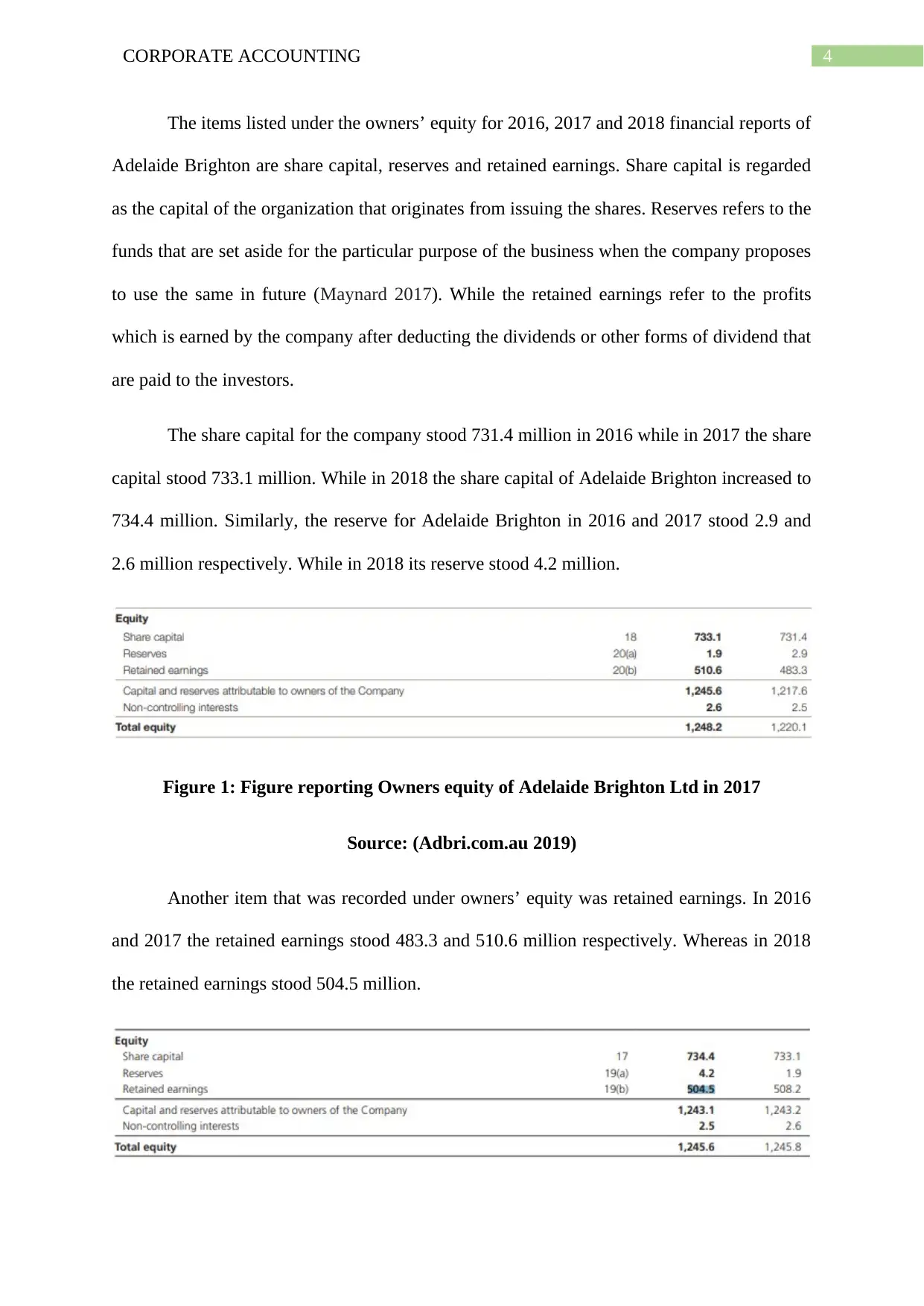

The items listed under the owners’ equity for 2016, 2017 and 2018 financial reports of

Adelaide Brighton are share capital, reserves and retained earnings. Share capital is regarded

as the capital of the organization that originates from issuing the shares. Reserves refers to the

funds that are set aside for the particular purpose of the business when the company proposes

to use the same in future (Maynard 2017). While the retained earnings refer to the profits

which is earned by the company after deducting the dividends or other forms of dividend that

are paid to the investors.

The share capital for the company stood 731.4 million in 2016 while in 2017 the share

capital stood 733.1 million. While in 2018 the share capital of Adelaide Brighton increased to

734.4 million. Similarly, the reserve for Adelaide Brighton in 2016 and 2017 stood 2.9 and

2.6 million respectively. While in 2018 its reserve stood 4.2 million.

Figure 1: Figure reporting Owners equity of Adelaide Brighton Ltd in 2017

Source: (Adbri.com.au 2019)

Another item that was recorded under owners’ equity was retained earnings. In 2016

and 2017 the retained earnings stood 483.3 and 510.6 million respectively. Whereas in 2018

the retained earnings stood 504.5 million.

The items listed under the owners’ equity for 2016, 2017 and 2018 financial reports of

Adelaide Brighton are share capital, reserves and retained earnings. Share capital is regarded

as the capital of the organization that originates from issuing the shares. Reserves refers to the

funds that are set aside for the particular purpose of the business when the company proposes

to use the same in future (Maynard 2017). While the retained earnings refer to the profits

which is earned by the company after deducting the dividends or other forms of dividend that

are paid to the investors.

The share capital for the company stood 731.4 million in 2016 while in 2017 the share

capital stood 733.1 million. While in 2018 the share capital of Adelaide Brighton increased to

734.4 million. Similarly, the reserve for Adelaide Brighton in 2016 and 2017 stood 2.9 and

2.6 million respectively. While in 2018 its reserve stood 4.2 million.

Figure 1: Figure reporting Owners equity of Adelaide Brighton Ltd in 2017

Source: (Adbri.com.au 2019)

Another item that was recorded under owners’ equity was retained earnings. In 2016

and 2017 the retained earnings stood 483.3 and 510.6 million respectively. Whereas in 2018

the retained earnings stood 504.5 million.

5CORPORATE ACCOUNTING

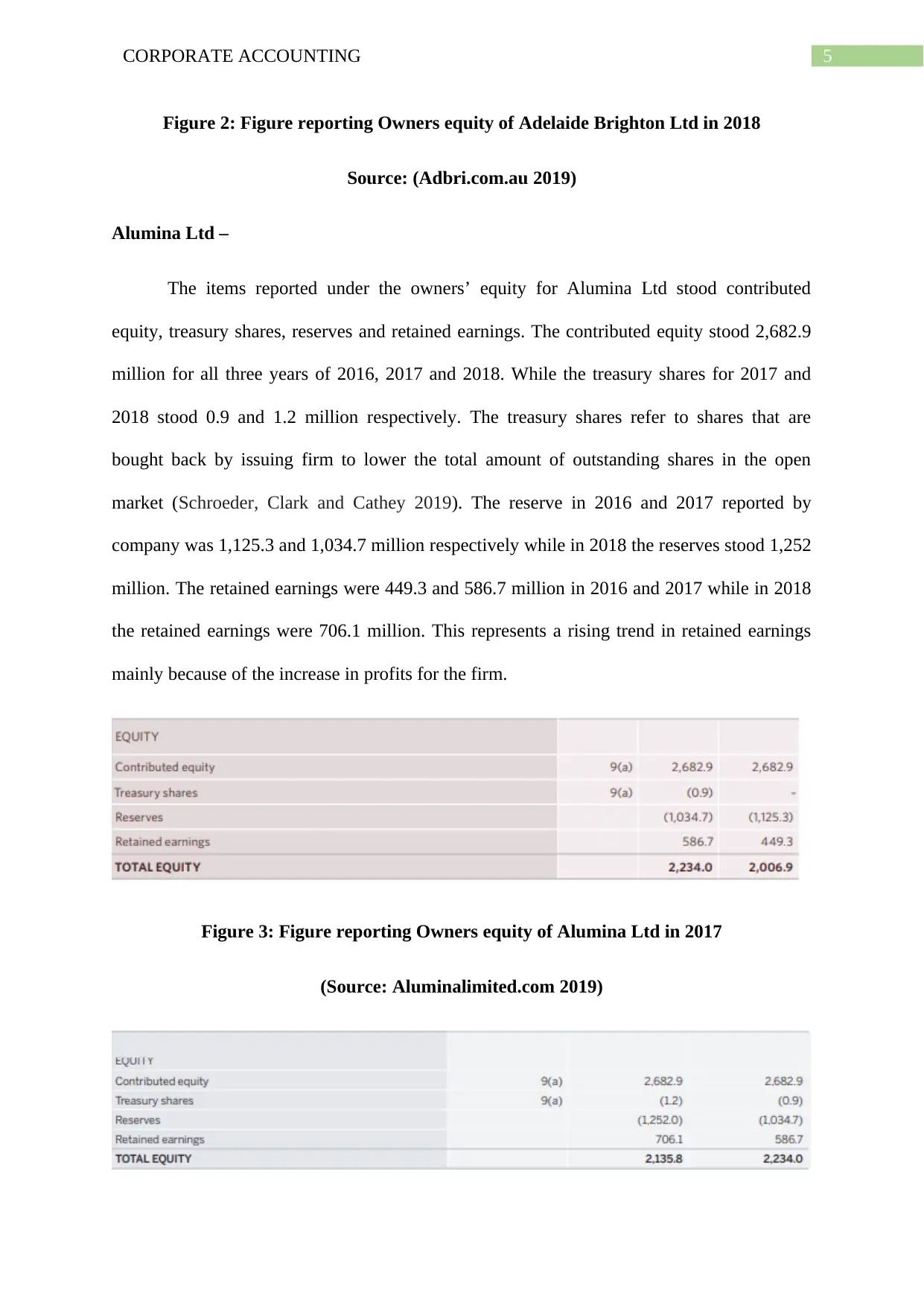

Figure 2: Figure reporting Owners equity of Adelaide Brighton Ltd in 2018

Source: (Adbri.com.au 2019)

Alumina Ltd –

The items reported under the owners’ equity for Alumina Ltd stood contributed

equity, treasury shares, reserves and retained earnings. The contributed equity stood 2,682.9

million for all three years of 2016, 2017 and 2018. While the treasury shares for 2017 and

2018 stood 0.9 and 1.2 million respectively. The treasury shares refer to shares that are

bought back by issuing firm to lower the total amount of outstanding shares in the open

market (Schroeder, Clark and Cathey 2019). The reserve in 2016 and 2017 reported by

company was 1,125.3 and 1,034.7 million respectively while in 2018 the reserves stood 1,252

million. The retained earnings were 449.3 and 586.7 million in 2016 and 2017 while in 2018

the retained earnings were 706.1 million. This represents a rising trend in retained earnings

mainly because of the increase in profits for the firm.

Figure 3: Figure reporting Owners equity of Alumina Ltd in 2017

(Source: Aluminalimited.com 2019)

Figure 2: Figure reporting Owners equity of Adelaide Brighton Ltd in 2018

Source: (Adbri.com.au 2019)

Alumina Ltd –

The items reported under the owners’ equity for Alumina Ltd stood contributed

equity, treasury shares, reserves and retained earnings. The contributed equity stood 2,682.9

million for all three years of 2016, 2017 and 2018. While the treasury shares for 2017 and

2018 stood 0.9 and 1.2 million respectively. The treasury shares refer to shares that are

bought back by issuing firm to lower the total amount of outstanding shares in the open

market (Schroeder, Clark and Cathey 2019). The reserve in 2016 and 2017 reported by

company was 1,125.3 and 1,034.7 million respectively while in 2018 the reserves stood 1,252

million. The retained earnings were 449.3 and 586.7 million in 2016 and 2017 while in 2018

the retained earnings were 706.1 million. This represents a rising trend in retained earnings

mainly because of the increase in profits for the firm.

Figure 3: Figure reporting Owners equity of Alumina Ltd in 2017

(Source: Aluminalimited.com 2019)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ACCOUNTING

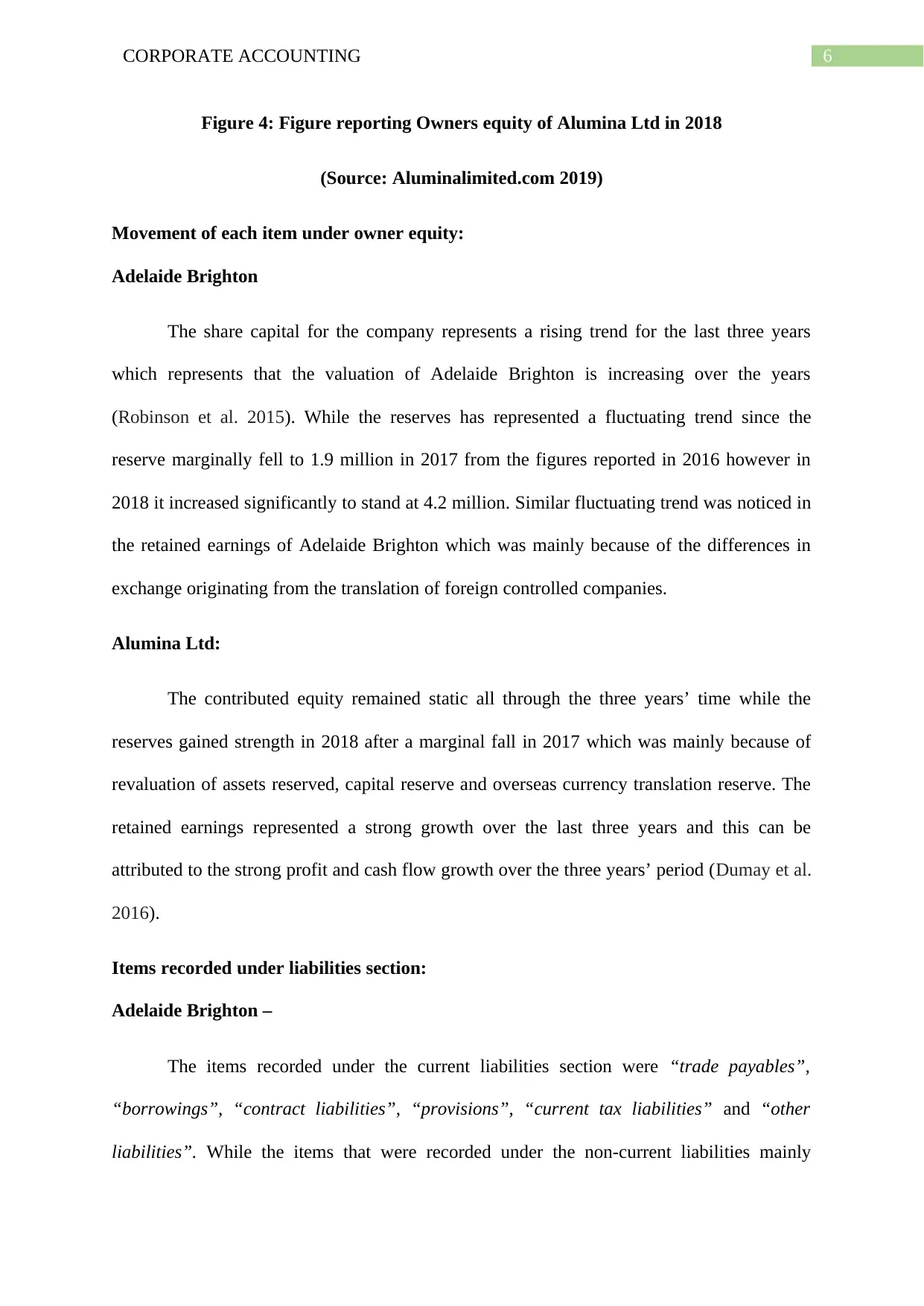

Figure 4: Figure reporting Owners equity of Alumina Ltd in 2018

(Source: Aluminalimited.com 2019)

Movement of each item under owner equity:

Adelaide Brighton

The share capital for the company represents a rising trend for the last three years

which represents that the valuation of Adelaide Brighton is increasing over the years

(Robinson et al. 2015). While the reserves has represented a fluctuating trend since the

reserve marginally fell to 1.9 million in 2017 from the figures reported in 2016 however in

2018 it increased significantly to stand at 4.2 million. Similar fluctuating trend was noticed in

the retained earnings of Adelaide Brighton which was mainly because of the differences in

exchange originating from the translation of foreign controlled companies.

Alumina Ltd:

The contributed equity remained static all through the three years’ time while the

reserves gained strength in 2018 after a marginal fall in 2017 which was mainly because of

revaluation of assets reserved, capital reserve and overseas currency translation reserve. The

retained earnings represented a strong growth over the last three years and this can be

attributed to the strong profit and cash flow growth over the three years’ period (Dumay et al.

2016).

Items recorded under liabilities section:

Adelaide Brighton –

The items recorded under the current liabilities section were “trade payables”,

“borrowings”, “contract liabilities”, “provisions”, “current tax liabilities” and “other

liabilities”. While the items that were recorded under the non-current liabilities mainly

Figure 4: Figure reporting Owners equity of Alumina Ltd in 2018

(Source: Aluminalimited.com 2019)

Movement of each item under owner equity:

Adelaide Brighton

The share capital for the company represents a rising trend for the last three years

which represents that the valuation of Adelaide Brighton is increasing over the years

(Robinson et al. 2015). While the reserves has represented a fluctuating trend since the

reserve marginally fell to 1.9 million in 2017 from the figures reported in 2016 however in

2018 it increased significantly to stand at 4.2 million. Similar fluctuating trend was noticed in

the retained earnings of Adelaide Brighton which was mainly because of the differences in

exchange originating from the translation of foreign controlled companies.

Alumina Ltd:

The contributed equity remained static all through the three years’ time while the

reserves gained strength in 2018 after a marginal fall in 2017 which was mainly because of

revaluation of assets reserved, capital reserve and overseas currency translation reserve. The

retained earnings represented a strong growth over the last three years and this can be

attributed to the strong profit and cash flow growth over the three years’ period (Dumay et al.

2016).

Items recorded under liabilities section:

Adelaide Brighton –

The items recorded under the current liabilities section were “trade payables”,

“borrowings”, “contract liabilities”, “provisions”, “current tax liabilities” and “other

liabilities”. While the items that were recorded under the non-current liabilities mainly

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

included the “borrowings”, “provisions, deferred tax liabilities” and “other non-current

liabilities”.

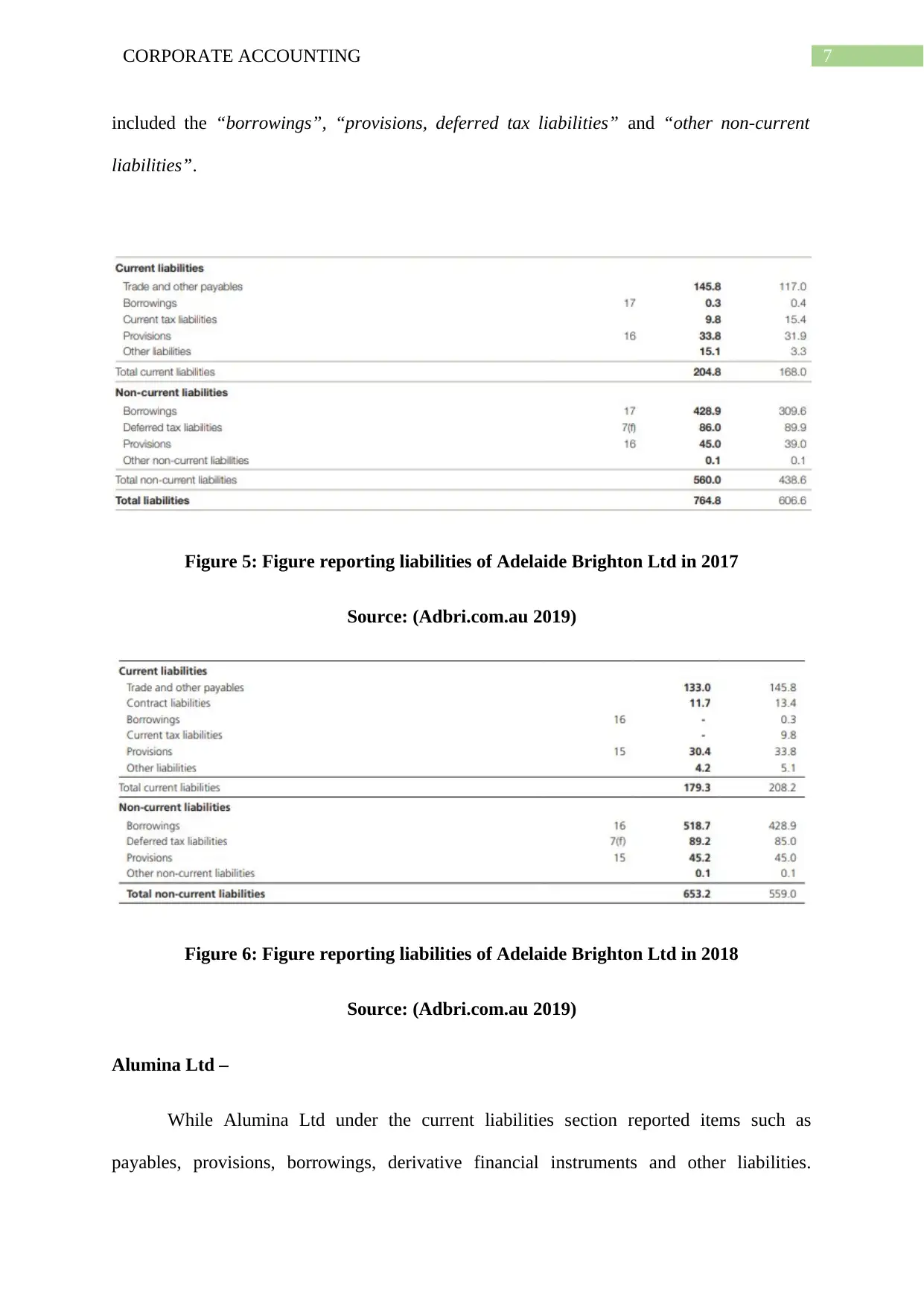

Figure 5: Figure reporting liabilities of Adelaide Brighton Ltd in 2017

Source: (Adbri.com.au 2019)

Figure 6: Figure reporting liabilities of Adelaide Brighton Ltd in 2018

Source: (Adbri.com.au 2019)

Alumina Ltd –

While Alumina Ltd under the current liabilities section reported items such as

payables, provisions, borrowings, derivative financial instruments and other liabilities.

included the “borrowings”, “provisions, deferred tax liabilities” and “other non-current

liabilities”.

Figure 5: Figure reporting liabilities of Adelaide Brighton Ltd in 2017

Source: (Adbri.com.au 2019)

Figure 6: Figure reporting liabilities of Adelaide Brighton Ltd in 2018

Source: (Adbri.com.au 2019)

Alumina Ltd –

While Alumina Ltd under the current liabilities section reported items such as

payables, provisions, borrowings, derivative financial instruments and other liabilities.

8CORPORATE ACCOUNTING

Whereas the non-current liabilities section includes the reported items such as “borrowings”,

“derivative financial instrument” and “provisions”.

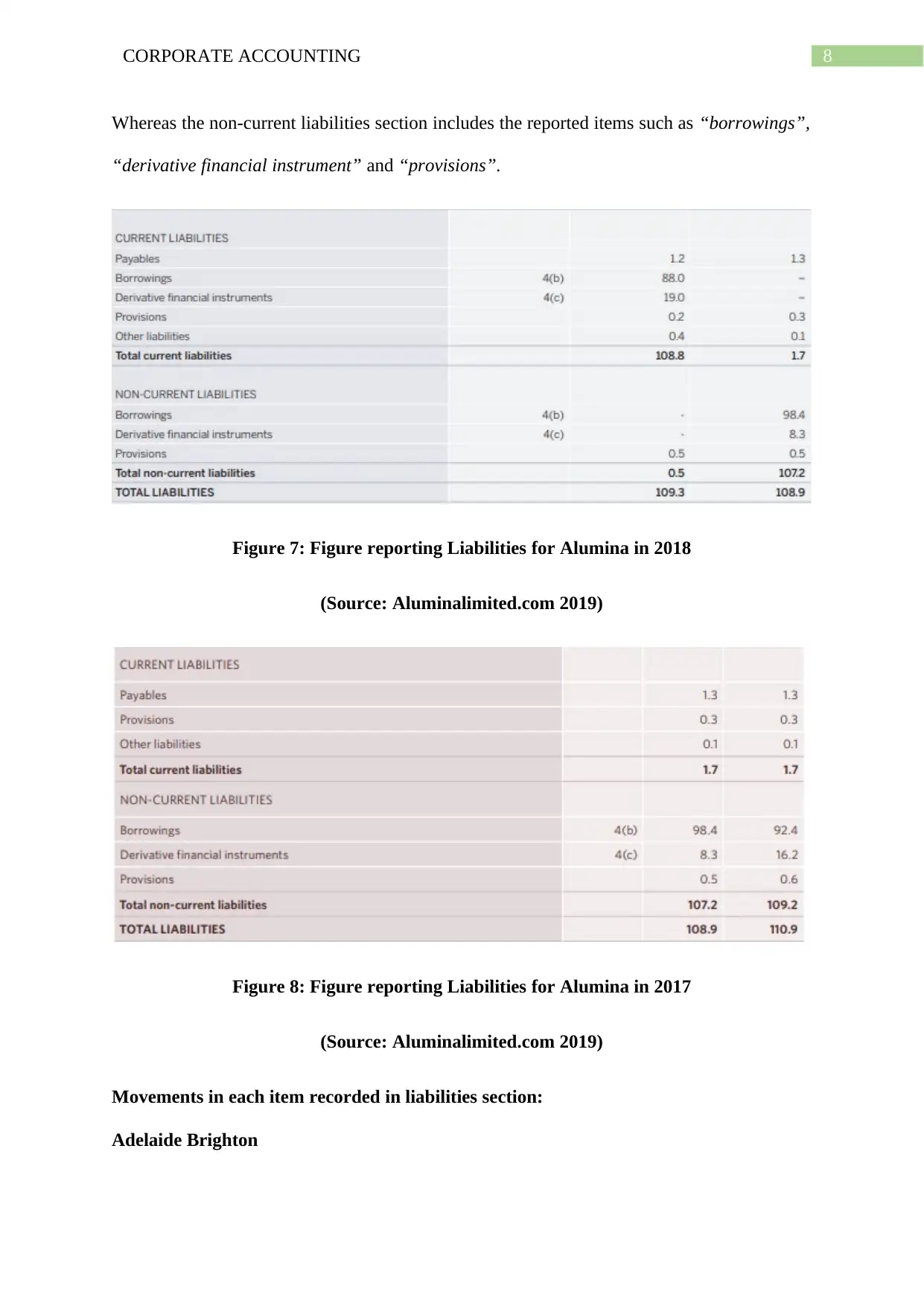

Figure 7: Figure reporting Liabilities for Alumina in 2018

(Source: Aluminalimited.com 2019)

Figure 8: Figure reporting Liabilities for Alumina in 2017

(Source: Aluminalimited.com 2019)

Movements in each item recorded in liabilities section:

Adelaide Brighton

Whereas the non-current liabilities section includes the reported items such as “borrowings”,

“derivative financial instrument” and “provisions”.

Figure 7: Figure reporting Liabilities for Alumina in 2018

(Source: Aluminalimited.com 2019)

Figure 8: Figure reporting Liabilities for Alumina in 2017

(Source: Aluminalimited.com 2019)

Movements in each item recorded in liabilities section:

Adelaide Brighton

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE ACCOUNTING

The current liabilities for the company in 2016 stood 168 million while in 2017 it

increased to 204.8 million. This is mainly because of the increase in the trade and other

payables which significantly increased to 145.8 in 2017 from the previous year figure of

117.0 million. In 2018 the current liabilities declined to 179.3 million and this can be

attributed to the fall in trade payables which improved to 133.0 million in 2018.

The non-current liabilities in 2016 stood 438.6 whereas in 2017 it significantly

increased to 560.0 million this is mainly because of the increased borrowings of the company.

The borrowings reported in 2016 stood 309.6 while it increased to 428.9 in 2017.

Furthermore, in 2018 the non-current liabilities reported by the company stood 653.2 The rise

in borrowing is because of its increase in the net finance cost which resulted a significant

increase in the borrowing margins (Schroeder, Clark and Cathey 2019).

Alumina Ltd:

The current liabilities for Alumina Ltd for both 2016 and 2017 stood same as the

figures reported stood 1.7 million for both the years. While in 2018 there has been a

significant rise in the total current liabilities as it stood 108.8 million. The rise in current

liabilities can be attributed to the borrowings which stood $88 million while derivative

financial instrument stood $19 million (Henderson et al. 2015). The borrowings represent

Alumina Ltd unconditional rights of deferring the settlement of liability for a minimum of 12

months.

While the non-current liabilities in 2016 stood 109.2 which marginally declined to

107.2 million in 2017. This can be largely attributable due to fall in derivative financial

instruments. These instruments were only used for economic hedging purpose (Kimmel et al.

2016). While in 2018 the non-current liabilities stood 0.5 million only. The company has

recognized redemption amount in the profit and loss account for the borrowings.

The current liabilities for the company in 2016 stood 168 million while in 2017 it

increased to 204.8 million. This is mainly because of the increase in the trade and other

payables which significantly increased to 145.8 in 2017 from the previous year figure of

117.0 million. In 2018 the current liabilities declined to 179.3 million and this can be

attributed to the fall in trade payables which improved to 133.0 million in 2018.

The non-current liabilities in 2016 stood 438.6 whereas in 2017 it significantly

increased to 560.0 million this is mainly because of the increased borrowings of the company.

The borrowings reported in 2016 stood 309.6 while it increased to 428.9 in 2017.

Furthermore, in 2018 the non-current liabilities reported by the company stood 653.2 The rise

in borrowing is because of its increase in the net finance cost which resulted a significant

increase in the borrowing margins (Schroeder, Clark and Cathey 2019).

Alumina Ltd:

The current liabilities for Alumina Ltd for both 2016 and 2017 stood same as the

figures reported stood 1.7 million for both the years. While in 2018 there has been a

significant rise in the total current liabilities as it stood 108.8 million. The rise in current

liabilities can be attributed to the borrowings which stood $88 million while derivative

financial instrument stood $19 million (Henderson et al. 2015). The borrowings represent

Alumina Ltd unconditional rights of deferring the settlement of liability for a minimum of 12

months.

While the non-current liabilities in 2016 stood 109.2 which marginally declined to

107.2 million in 2017. This can be largely attributable due to fall in derivative financial

instruments. These instruments were only used for economic hedging purpose (Kimmel et al.

2016). While in 2018 the non-current liabilities stood 0.5 million only. The company has

recognized redemption amount in the profit and loss account for the borrowings.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE ACCOUNTING

Advantage or disadvantage of sources of fund:

Adelaide Brighton:

The company mainly uses share capital as its main source of fund. While fund is

considered advantageous because the company would not be required to pay interest or

repaying the equity investors initial investment (Narayanaswamy 2017). The equity capital is

advantageous because it helps the company in keeping majority of its profits and grants better

flexibility in spending. While the equity capital also serves as a disadvantage for Adelaide

Brighton because it will be having greater burden of cost to company.

Adelaide Brighton also uses the reserve as its main sources of finance. The fund can

be advantageous in recovering the future contingencies of the business and it is also helpful

in meeting any kind of future loss and liabilities (Narayanaswamy 2017).

Alumina Ltd:

The main sources of fund for Alumina Ltd is the contributed equity. The advantage of

the fund is that the company has no obligation to repay the investors based on their initial

investment. Furthermore, it also has lower risks of bankruptcy (Caruana et al. 2019). While

the reserve fund is advantageous in expanding the business activities of Alumina Ltd and also

forms the major sources of financing for the company.

The disadvantage of the contributed equity for Alumina Ltd is that there is a dilution

of ownership for the company and the company may face loss of control on the company

activities.

Advantage or disadvantage of sources of fund:

Adelaide Brighton:

The company mainly uses share capital as its main source of fund. While fund is

considered advantageous because the company would not be required to pay interest or

repaying the equity investors initial investment (Narayanaswamy 2017). The equity capital is

advantageous because it helps the company in keeping majority of its profits and grants better

flexibility in spending. While the equity capital also serves as a disadvantage for Adelaide

Brighton because it will be having greater burden of cost to company.

Adelaide Brighton also uses the reserve as its main sources of finance. The fund can

be advantageous in recovering the future contingencies of the business and it is also helpful

in meeting any kind of future loss and liabilities (Narayanaswamy 2017).

Alumina Ltd:

The main sources of fund for Alumina Ltd is the contributed equity. The advantage of

the fund is that the company has no obligation to repay the investors based on their initial

investment. Furthermore, it also has lower risks of bankruptcy (Caruana et al. 2019). While

the reserve fund is advantageous in expanding the business activities of Alumina Ltd and also

forms the major sources of financing for the company.

The disadvantage of the contributed equity for Alumina Ltd is that there is a dilution

of ownership for the company and the company may face loss of control on the company

activities.

11CORPORATE ACCOUNTING

Part B:

Critical examination of concepts of small proprietary company, large proprietary

company and reporting entity:

The small proprietary company refers to those company that has assets of lower than

$12.5 million at the end of financial year (Kieso, Weygandt and Warfield 2019). These type

of company generally has fewer employees of around 50 persons at the end of the year and

has the gross revenue of not greater than $25 million for year.

The large proprietary company generally refers to those company that has the

consolidated revenue during the financial year of $50 million or more (Asic.gov.au 2019).

Furthermore, a large proprietary company generally represents the value of consolidated

gross assets of $25 million or more at the end of financial year. The large proprietary

company at the end of financial year generally has employee strength of more than 100.

Reporting entity is defined as the entity where it become reasonable to anticipate that

there are users that are reliant on the general purpose financial reporting (GPFR) to obtain the

understanding of the financial position and performance of the company and to take the

decision on the basis of financial and other information (Asic.gov.au 2019). The users can be

either the shareholders, members, employees, creditors, lenders or probable investors.

Therefore, it becomes vital for those are assigned with the governance to file whether the

company has users reliant on the GPFR which allow them to define the company as either the

reporting or non-reporting company.

Implications of being classified as any one of the companies:

The implications of being classified as a large proprietary company would require the

company to prepare as well as lodge the financial report and a director’s report for every

financial year. The accounts of the large companies are audited on regularly basis unless the

Part B:

Critical examination of concepts of small proprietary company, large proprietary

company and reporting entity:

The small proprietary company refers to those company that has assets of lower than

$12.5 million at the end of financial year (Kieso, Weygandt and Warfield 2019). These type

of company generally has fewer employees of around 50 persons at the end of the year and

has the gross revenue of not greater than $25 million for year.

The large proprietary company generally refers to those company that has the

consolidated revenue during the financial year of $50 million or more (Asic.gov.au 2019).

Furthermore, a large proprietary company generally represents the value of consolidated

gross assets of $25 million or more at the end of financial year. The large proprietary

company at the end of financial year generally has employee strength of more than 100.

Reporting entity is defined as the entity where it become reasonable to anticipate that

there are users that are reliant on the general purpose financial reporting (GPFR) to obtain the

understanding of the financial position and performance of the company and to take the

decision on the basis of financial and other information (Asic.gov.au 2019). The users can be

either the shareholders, members, employees, creditors, lenders or probable investors.

Therefore, it becomes vital for those are assigned with the governance to file whether the

company has users reliant on the GPFR which allow them to define the company as either the

reporting or non-reporting company.

Implications of being classified as any one of the companies:

The implications of being classified as a large proprietary company would require the

company to prepare as well as lodge the financial report and a director’s report for every

financial year. The accounts of the large companies are audited on regularly basis unless the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.