Corporate Accounting Report: Investment Analysis and Goodwill

VerifiedAdded on 2020/03/16

|22

|1859

|333

Report

AI Summary

This report delves into corporate accounting, analyzing various investment relationships and their implications under accounting standards. It examines scenarios involving different shareholders and their control over financial activities, referencing AASB 10 and AASB 11. The report assesses the need for consolidation based on the level of control exerted by different stakeholders. Furthermore, it explores goodwill calculations in the context of equity interest acquisition, including the valuation of non-controlling interests and the implications of goodwill on financial statements. The report covers multiple investment scenarios, providing detailed analysis and explanations of accounting treatments, along with references to relevant accounting standards and literature. The report also includes workings and calculations for goodwill and equity interest.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Author Note:

Corporate Accounting

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2CORPORATE ACCOUNTING

Table of Contents

Answer to Question 1:................................................................................................................2

First Investment Relationship....................................................................................................2

Fifth Investment Relationship....................................................................................................5

Question 2..................................................................................................................................5

Question 3..................................................................................................................................9

Question 4................................................................................................................................12

Question 5................................................................................................................................14

References................................................................................................................................20

Table of Contents

Answer to Question 1:................................................................................................................2

First Investment Relationship....................................................................................................2

Fifth Investment Relationship....................................................................................................5

Question 2..................................................................................................................................5

Question 3..................................................................................................................................9

Question 4................................................................................................................................12

Question 5................................................................................................................................14

References................................................................................................................................20

3CORPORATE ACCOUNTING

Answer to Question 1:

First Investment Relationship

According to the given situation, LBX Pty Limited primarily had different shareholders that

had around 25% of shares that was essentially assumed by Millionaires Club along with Pty

Limited whilst the left over shares are possessed by the founder of the company LBX Pty

Limited. Additionally, it is significant to allow for all the evidences as well as situations for

assessing control over financiers. However, Millionaires Club has three different seats in the

Board and has authority to put forward views in some of the central activities that occur

within the business concern. As per the stipulations mentioned under paragraph B-19 of the

standard AASB 10, a financier has the authority to exercise control over the process directing

diverse functionalities of the business concern (Aasb.gov.au, 2017).

Second Investment Relationship

In this case it is imperative to take into consideration that Millionaires Club have the need to

engage in the process of assessment of the rights for the purpose of determination of

consolidation necessities that manage all of the actions. However, the actions that controlled

by a financier necessarily have the protecting rights at the time when they engage in

particular events or else situations. It can be hereby observed that financial exercises of BBT

are essentially controlled by different officials of Millionaires Club for a time period of

around 5 years. Thus, it can be said that the controls primarily remain in the hands of the

officials of Millionaires Club who are responsible to look after diverse financial operations of

the company. In a way, it can be hereby forecasted that consolidation is not required and

cannot be undertaken at the time when different associates of Millionaires Club do not have

position in the Board (Carnegie & O’Connell, 2014).

Answer to Question 1:

First Investment Relationship

According to the given situation, LBX Pty Limited primarily had different shareholders that

had around 25% of shares that was essentially assumed by Millionaires Club along with Pty

Limited whilst the left over shares are possessed by the founder of the company LBX Pty

Limited. Additionally, it is significant to allow for all the evidences as well as situations for

assessing control over financiers. However, Millionaires Club has three different seats in the

Board and has authority to put forward views in some of the central activities that occur

within the business concern. As per the stipulations mentioned under paragraph B-19 of the

standard AASB 10, a financier has the authority to exercise control over the process directing

diverse functionalities of the business concern (Aasb.gov.au, 2017).

Second Investment Relationship

In this case it is imperative to take into consideration that Millionaires Club have the need to

engage in the process of assessment of the rights for the purpose of determination of

consolidation necessities that manage all of the actions. However, the actions that controlled

by a financier necessarily have the protecting rights at the time when they engage in

particular events or else situations. It can be hereby observed that financial exercises of BBT

are essentially controlled by different officials of Millionaires Club for a time period of

around 5 years. Thus, it can be said that the controls primarily remain in the hands of the

officials of Millionaires Club who are responsible to look after diverse financial operations of

the company. In a way, it can be hereby forecasted that consolidation is not required and

cannot be undertaken at the time when different associates of Millionaires Club do not have

position in the Board (Carnegie & O’Connell, 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4CORPORATE ACCOUNTING

Third Investment Relationship

According to the given state of affairs, it can be said that CTL has two different financiers in

which Millionaires Club reflects accountability in delivering loan and BJL for managing the

managerial actions. However, when there are two different financiers engaged in any dealing,

then diverse actions of CTL have the need to be focussed or else controlled by the two

investors collectively and then designed jointly (Carnegie & O’Connell, 2014). In this case,

both the financiers have the need to be in agreement to a specific solution to any difficulty

encountered by the business concern, or else it might prove to be very complicated.

Nonetheless, CTL cannot be properly controlled by a single individual financier. Again, the

concern in CTL can be analysed from specific joint arrangement according to stipulations of

AASB 11 (Aasb.gov.au, 2017).

Fourth Investment Relationship

Analysis of this investment situation reveals that there are three different financiers that are

present in the case. In this case, each of the financiers has identical share of around 33.3%.

However, it can again be observed from this case that daily functionalities of PGH Pty

Limited are directed appropriately by Millionaires Club since they have no more than one

seat in the company’s Board. However, the two shareholders referred to as CCL as well as

GJL possess barely one seat out of the total seats of three existent in the Board, However,

they are considered as passive financiers. Again, it is evidently stipulated in the Paragraph B-

19 of the regulation standard AASB 10 that at the time when a financier demonstrates passive

interest towards corporation, then they predominantly have certain unique association with

the financier (Schaltegger et al., 2017). However, it can be hereby mentioned that

Millionaires Club has ample authority to exercise control over PGH Pty Limited where these

financiers are permitted for certain rights and reflects additional passive concern towards the

Third Investment Relationship

According to the given state of affairs, it can be said that CTL has two different financiers in

which Millionaires Club reflects accountability in delivering loan and BJL for managing the

managerial actions. However, when there are two different financiers engaged in any dealing,

then diverse actions of CTL have the need to be focussed or else controlled by the two

investors collectively and then designed jointly (Carnegie & O’Connell, 2014). In this case,

both the financiers have the need to be in agreement to a specific solution to any difficulty

encountered by the business concern, or else it might prove to be very complicated.

Nonetheless, CTL cannot be properly controlled by a single individual financier. Again, the

concern in CTL can be analysed from specific joint arrangement according to stipulations of

AASB 11 (Aasb.gov.au, 2017).

Fourth Investment Relationship

Analysis of this investment situation reveals that there are three different financiers that are

present in the case. In this case, each of the financiers has identical share of around 33.3%.

However, it can again be observed from this case that daily functionalities of PGH Pty

Limited are directed appropriately by Millionaires Club since they have no more than one

seat in the company’s Board. However, the two shareholders referred to as CCL as well as

GJL possess barely one seat out of the total seats of three existent in the Board, However,

they are considered as passive financiers. Again, it is evidently stipulated in the Paragraph B-

19 of the regulation standard AASB 10 that at the time when a financier demonstrates passive

interest towards corporation, then they predominantly have certain unique association with

the financier (Schaltegger et al., 2017). However, it can be hereby mentioned that

Millionaires Club has ample authority to exercise control over PGH Pty Limited where these

financiers are permitted for certain rights and reflects additional passive concern towards the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5CORPORATE ACCOUNTING

business concern. Thus, engagement of Millionaires Club in actions on a daily basis activities

led to exerting certain control with huge exposure on inconsistency in return (Beekes et al.,

2015).

business concern. Thus, engagement of Millionaires Club in actions on a daily basis activities

led to exerting certain control with huge exposure on inconsistency in return (Beekes et al.,

2015).

6CORPORATE ACCOUNTING

Fifth Investment Relationship

Analysis of the present situation helps in understanding the fact that Millionaires Club is the

possessor of approximately 75% of shares of the company JB Hi-Fi. However, Millionaires

Club does not hold any seat in the Board of the company. Therefore, they are not responsible

for management or else any type of decision making process that is associated to finance as

well as operations. Again, it can be hereby observed that there had taken place consolidation

of company’s assets owing to insufficiency on top of continuous poor as well as unsteady

performance (Henderson et al., 2015). Again, it can be hereby noted that Millionaires Club in

real possesses major fraction of shares of the company JB Hi-Fi in which they do not even

have voting authority. Essentially, it is the authority of a financier to exert control though

they do not possess voting authority according to B-38 of the regulation standard AASB 10.

Again, there had been adequate control that is undertaken by the financiers at the time when

they get involved in the process of management of pertinent actions and maintenance of

contractual necessities. Again, it can be stated that JB Hi-Fi is not involved in the process of

direction of actions that occur in business and therefore control cannot be exerted.

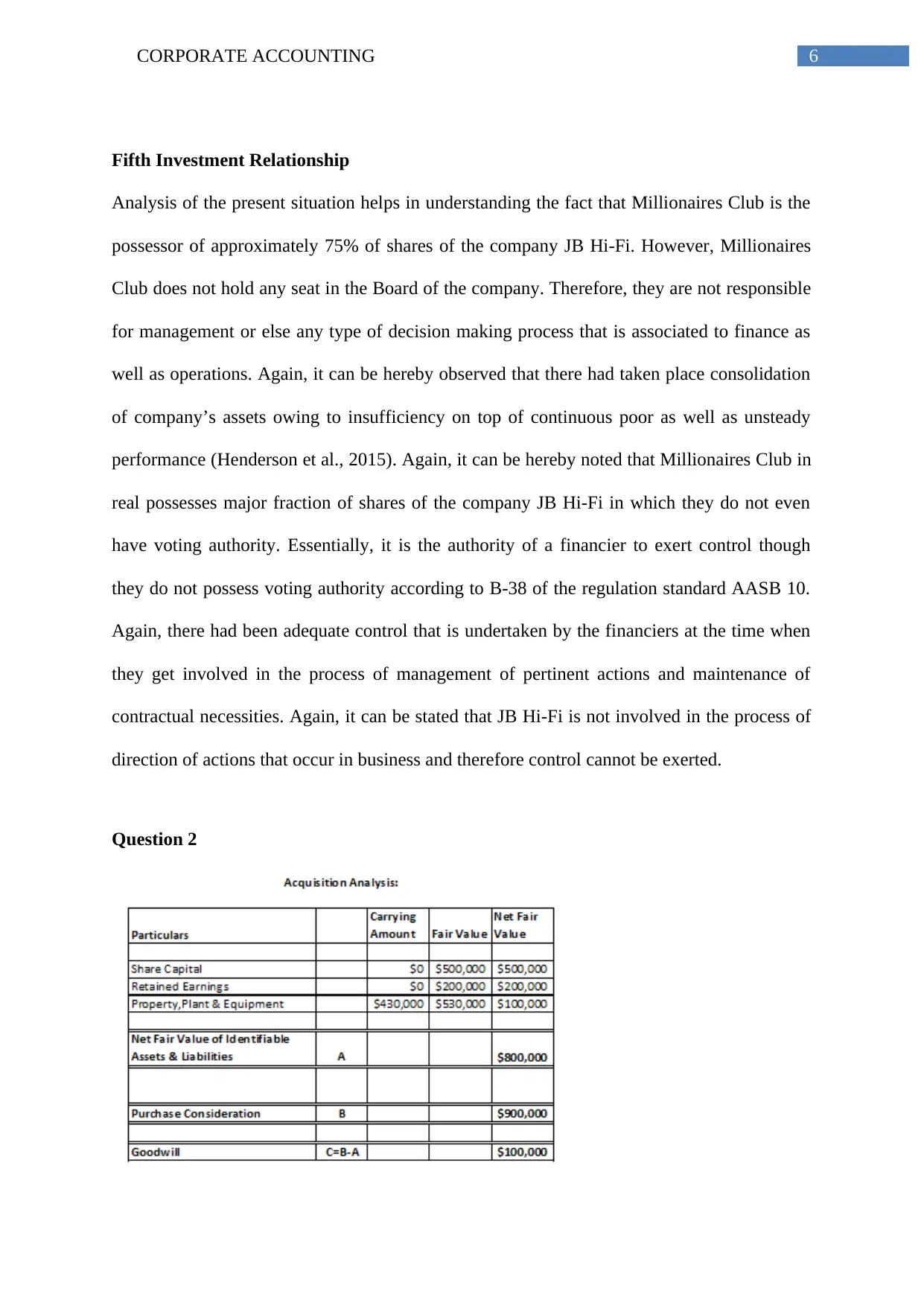

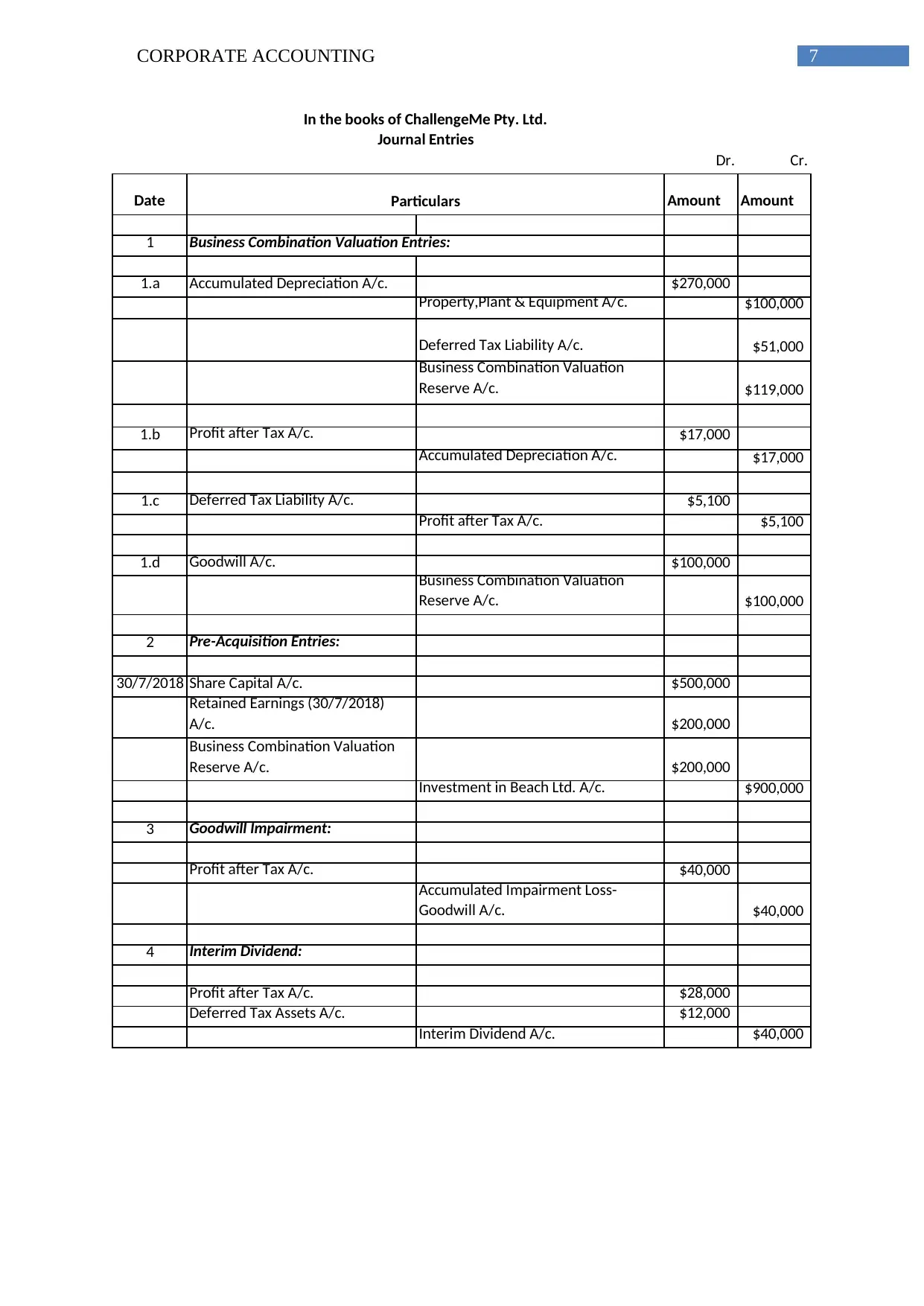

Question 2

Fifth Investment Relationship

Analysis of the present situation helps in understanding the fact that Millionaires Club is the

possessor of approximately 75% of shares of the company JB Hi-Fi. However, Millionaires

Club does not hold any seat in the Board of the company. Therefore, they are not responsible

for management or else any type of decision making process that is associated to finance as

well as operations. Again, it can be hereby observed that there had taken place consolidation

of company’s assets owing to insufficiency on top of continuous poor as well as unsteady

performance (Henderson et al., 2015). Again, it can be hereby noted that Millionaires Club in

real possesses major fraction of shares of the company JB Hi-Fi in which they do not even

have voting authority. Essentially, it is the authority of a financier to exert control though

they do not possess voting authority according to B-38 of the regulation standard AASB 10.

Again, there had been adequate control that is undertaken by the financiers at the time when

they get involved in the process of management of pertinent actions and maintenance of

contractual necessities. Again, it can be stated that JB Hi-Fi is not involved in the process of

direction of actions that occur in business and therefore control cannot be exerted.

Question 2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7CORPORATE ACCOUNTING

Dr. Cr.

Date Amount Amount

1

1.a Accumulated Depreciation A/c. $270,000

Property,Plant & Equipment A/c. $100,000

Deferred Tax Liability A/c. $51,000

Business Combination Valuation

Reserve A/c. $119,000

1.b Profit after Tax A/c. $17,000

Accumulated Depreciation A/c. $17,000

1.c Deferred Tax Liability A/c. $5,100

Profit after Tax A/c. $5,100

1.d Goodwill A/c. $100,000

Business Combination Valuation

Reserve A/c. $100,000

2 Pre-Acquisition Entries:

30/7/2018 Share Capital A/c. $500,000

Retained Earnings (30/7/2018)

A/c. $200,000

Business Combination Valuation

Reserve A/c. $200,000

Investment in Beach Ltd. A/c. $900,000

3 Goodwill Impairment:

Profit after Tax A/c. $40,000

Accumulated Impairment Loss-

Goodwill A/c. $40,000

4 Interim Dividend:

Profit after Tax A/c. $28,000

Deferred Tax Assets A/c. $12,000

Interim Dividend A/c. $40,000

Particulars

Business Combination Valuation Entries:

In the books of ChallengeMe Pty. Ltd.

Journal Entries

Dr. Cr.

Date Amount Amount

1

1.a Accumulated Depreciation A/c. $270,000

Property,Plant & Equipment A/c. $100,000

Deferred Tax Liability A/c. $51,000

Business Combination Valuation

Reserve A/c. $119,000

1.b Profit after Tax A/c. $17,000

Accumulated Depreciation A/c. $17,000

1.c Deferred Tax Liability A/c. $5,100

Profit after Tax A/c. $5,100

1.d Goodwill A/c. $100,000

Business Combination Valuation

Reserve A/c. $100,000

2 Pre-Acquisition Entries:

30/7/2018 Share Capital A/c. $500,000

Retained Earnings (30/7/2018)

A/c. $200,000

Business Combination Valuation

Reserve A/c. $200,000

Investment in Beach Ltd. A/c. $900,000

3 Goodwill Impairment:

Profit after Tax A/c. $40,000

Accumulated Impairment Loss-

Goodwill A/c. $40,000

4 Interim Dividend:

Profit after Tax A/c. $28,000

Deferred Tax Assets A/c. $12,000

Interim Dividend A/c. $40,000

Particulars

Business Combination Valuation Entries:

In the books of ChallengeMe Pty. Ltd.

Journal Entries

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8CORPORATE ACCOUNTING

5 Final Dividend:

5.a Profit after Tax A/c. $35,000

Deferred Tax Assets A/c. $15,000

Final Dividend A/c. $50,000

5.b Dividend Payable A/c. $50,000

Accounts Receivable A/c. $50,000

Particulars

ChallengeMe

Pty. Ltd.

TakeItEasy

Ltd. Debit Credit Group

Profit after Tax $400,000 $190,000

1.b,3.4,5.

a $120,000 $5,100 1.c $475,100

Retained Earnings - 30 June,2018 $300,000 $200,000 2 $200,000 $300,000

Interim Dividend ($90,000) ($40,000) ($40,000) 4 ($90,000)

Final Dividend ($110,000) ($50,000) ($50,000) 5.a ($110,000)

Retained Earnings - 30 June,2019 $500,000 $300,000 $575,100

Share Capital $1,000,000 $500,000 2 $500,000 $1,000,000

Business Combination Valuation Reserve 2 $200,000 $219,000 1.a,1.d $19,000

Total Shareholders' equity $1,500,000 $800,000 $1,594,100

Accounts Payable $100,000 $10,000 $110,000

Dividends Payable $100,000 $50,000 5.b $50,000 $100,000

Deferred Tax Liability 1.c $5,100 $51,000 1.a $45,900

Loan $670,000 $140,000 $810,000

Total Liabilities & equity $2,370,000 $1,000,000 $2,660,000

Cash $80,000 $40,000 $120,000

Accounts Receivable $50,000 $50,000 $50,000 5.b $50,000

Inventory $140,000 $123,000 $263,000

Deferred Tax Assets 4,5.a $27,000 $27,000

Goodwill 1.d $100,000 $100,000

Accumulated Impairment Loss ($40,000) 3 ($40,000)

Land $600,000 $400,000 $1,000,000

Property,Plant & Equipment $900,000 $700,000 $100,000 1.a $1,500,000

Accumulated Depreciation ($300,000) ($313,000) 1.a ($270,000) ($17,000) 1.b ($360,000)

Investment in Beach Ltd. $900,000 $900,000 2 $0

Total Assets $2,370,000 $1,000,000 $2,660,000

Adjustment

Consolidation Worksheet:

5 Final Dividend:

5.a Profit after Tax A/c. $35,000

Deferred Tax Assets A/c. $15,000

Final Dividend A/c. $50,000

5.b Dividend Payable A/c. $50,000

Accounts Receivable A/c. $50,000

Particulars

ChallengeMe

Pty. Ltd.

TakeItEasy

Ltd. Debit Credit Group

Profit after Tax $400,000 $190,000

1.b,3.4,5.

a $120,000 $5,100 1.c $475,100

Retained Earnings - 30 June,2018 $300,000 $200,000 2 $200,000 $300,000

Interim Dividend ($90,000) ($40,000) ($40,000) 4 ($90,000)

Final Dividend ($110,000) ($50,000) ($50,000) 5.a ($110,000)

Retained Earnings - 30 June,2019 $500,000 $300,000 $575,100

Share Capital $1,000,000 $500,000 2 $500,000 $1,000,000

Business Combination Valuation Reserve 2 $200,000 $219,000 1.a,1.d $19,000

Total Shareholders' equity $1,500,000 $800,000 $1,594,100

Accounts Payable $100,000 $10,000 $110,000

Dividends Payable $100,000 $50,000 5.b $50,000 $100,000

Deferred Tax Liability 1.c $5,100 $51,000 1.a $45,900

Loan $670,000 $140,000 $810,000

Total Liabilities & equity $2,370,000 $1,000,000 $2,660,000

Cash $80,000 $40,000 $120,000

Accounts Receivable $50,000 $50,000 $50,000 5.b $50,000

Inventory $140,000 $123,000 $263,000

Deferred Tax Assets 4,5.a $27,000 $27,000

Goodwill 1.d $100,000 $100,000

Accumulated Impairment Loss ($40,000) 3 ($40,000)

Land $600,000 $400,000 $1,000,000

Property,Plant & Equipment $900,000 $700,000 $100,000 1.a $1,500,000

Accumulated Depreciation ($300,000) ($313,000) 1.a ($270,000) ($17,000) 1.b ($360,000)

Investment in Beach Ltd. $900,000 $900,000 2 $0

Total Assets $2,370,000 $1,000,000 $2,660,000

Adjustment

Consolidation Worksheet:

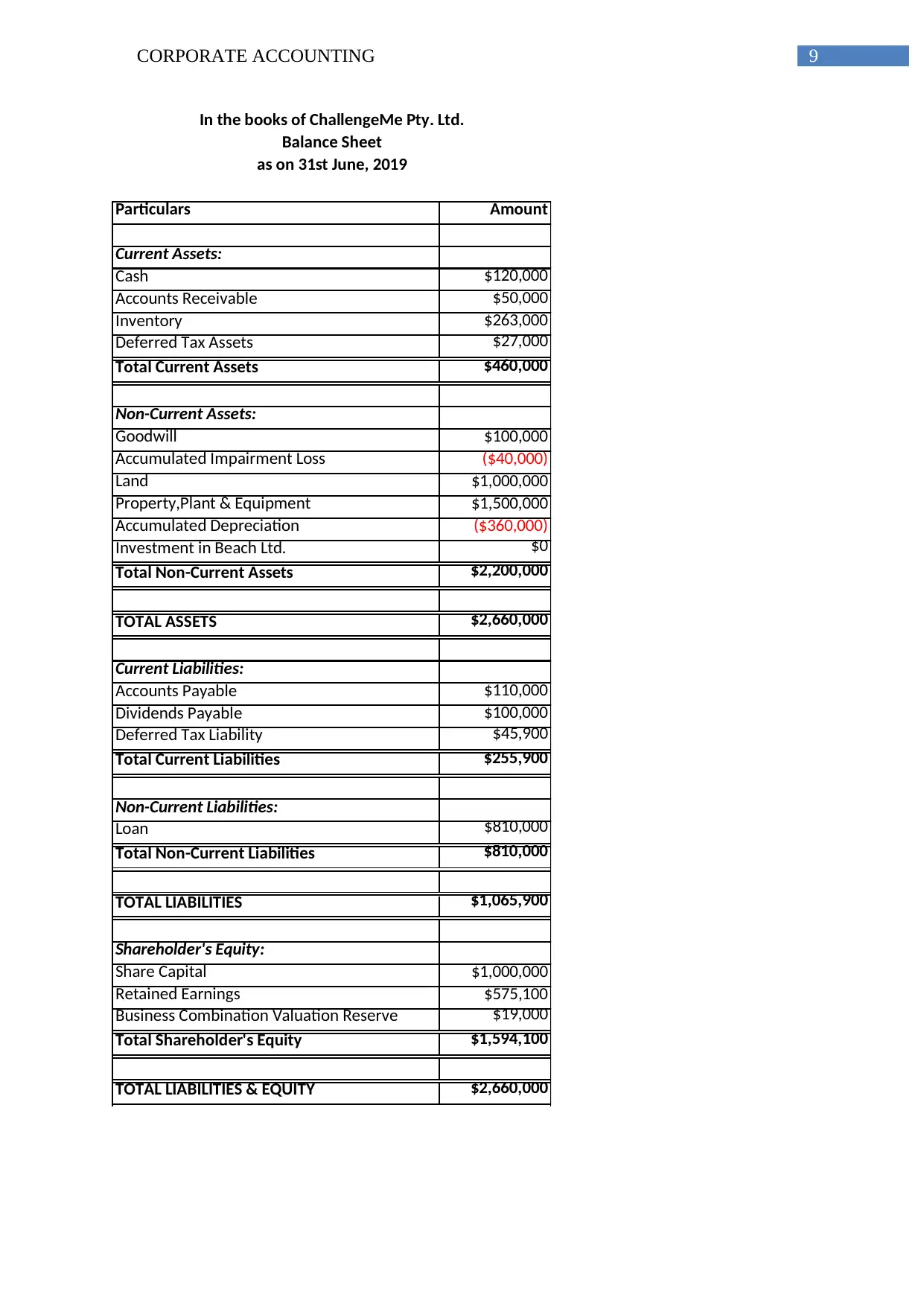

9CORPORATE ACCOUNTING

Particulars Amount

Current Assets:

Cash $120,000

Accounts Receivable $50,000

Inventory $263,000

Deferred Tax Assets $27,000

Total Current Assets $460,000

Non-Current Assets:

Goodwill $100,000

Accumulated Impairment Loss ($40,000)

Land $1,000,000

Property,Plant & Equipment $1,500,000

Accumulated Depreciation ($360,000)

Investment in Beach Ltd. $0

Total Non-Current Assets $2,200,000

TOTAL ASSETS $2,660,000

Current Liabilities:

Accounts Payable $110,000

Dividends Payable $100,000

Deferred Tax Liability $45,900

Total Current Liabilities $255,900

Non-Current Liabilities:

Loan $810,000

Total Non-Current Liabilities $810,000

TOTAL LIABILITIES $1,065,900

Shareholder's Equity:

Share Capital $1,000,000

Retained Earnings $575,100

Business Combination Valuation Reserve $19,000

Total Shareholder's Equity $1,594,100

TOTAL LIABILITIES & EQUITY $2,660,000

In the books of ChallengeMe Pty. Ltd.

Balance Sheet

as on 31st June, 2019

Particulars Amount

Current Assets:

Cash $120,000

Accounts Receivable $50,000

Inventory $263,000

Deferred Tax Assets $27,000

Total Current Assets $460,000

Non-Current Assets:

Goodwill $100,000

Accumulated Impairment Loss ($40,000)

Land $1,000,000

Property,Plant & Equipment $1,500,000

Accumulated Depreciation ($360,000)

Investment in Beach Ltd. $0

Total Non-Current Assets $2,200,000

TOTAL ASSETS $2,660,000

Current Liabilities:

Accounts Payable $110,000

Dividends Payable $100,000

Deferred Tax Liability $45,900

Total Current Liabilities $255,900

Non-Current Liabilities:

Loan $810,000

Total Non-Current Liabilities $810,000

TOTAL LIABILITIES $1,065,900

Shareholder's Equity:

Share Capital $1,000,000

Retained Earnings $575,100

Business Combination Valuation Reserve $19,000

Total Shareholder's Equity $1,594,100

TOTAL LIABILITIES & EQUITY $2,660,000

In the books of ChallengeMe Pty. Ltd.

Balance Sheet

as on 31st June, 2019

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10CORPORATE ACCOUNTING

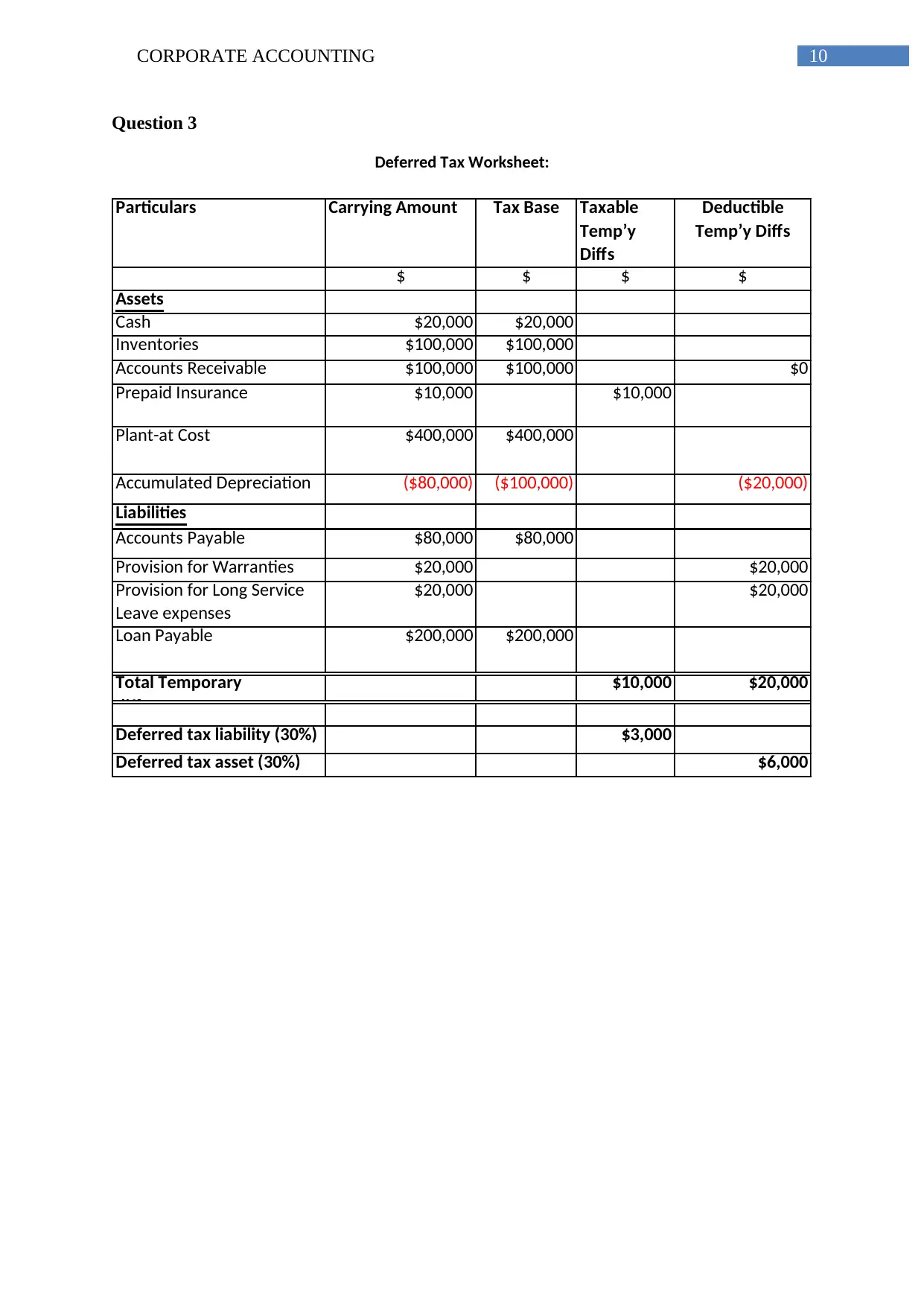

Question 3

Particulars Carrying Amount Tax Base Taxable

Temp’y

Diffs

Deductible

Temp’y Diffs

$ $ $ $

Assets

Cash $20,000 $20,000

Inventories $100,000 $100,000

Accounts Receivable $100,000 $100,000 $0

Prepaid Insurance $10,000 $10,000

Plant-at Cost $400,000 $400,000

Accumulated Depreciation ($80,000) ($100,000) ($20,000)

Liabilities

Accounts Payable $80,000 $80,000

Provision for Warranties $20,000 $20,000

Provision for Long Service

Leave expenses

$20,000 $20,000

Loan Payable $200,000 $200,000

Total Temporary

differences

$10,000 $20,000

Deferred tax liability (30%) $3,000

Deferred tax asset (30%) $6,000

Deferred Tax Worksheet:

Question 3

Particulars Carrying Amount Tax Base Taxable

Temp’y

Diffs

Deductible

Temp’y Diffs

$ $ $ $

Assets

Cash $20,000 $20,000

Inventories $100,000 $100,000

Accounts Receivable $100,000 $100,000 $0

Prepaid Insurance $10,000 $10,000

Plant-at Cost $400,000 $400,000

Accumulated Depreciation ($80,000) ($100,000) ($20,000)

Liabilities

Accounts Payable $80,000 $80,000

Provision for Warranties $20,000 $20,000

Provision for Long Service

Leave expenses

$20,000 $20,000

Loan Payable $200,000 $200,000

Total Temporary

differences

$10,000 $20,000

Deferred tax liability (30%) $3,000

Deferred tax asset (30%) $6,000

Deferred Tax Worksheet:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

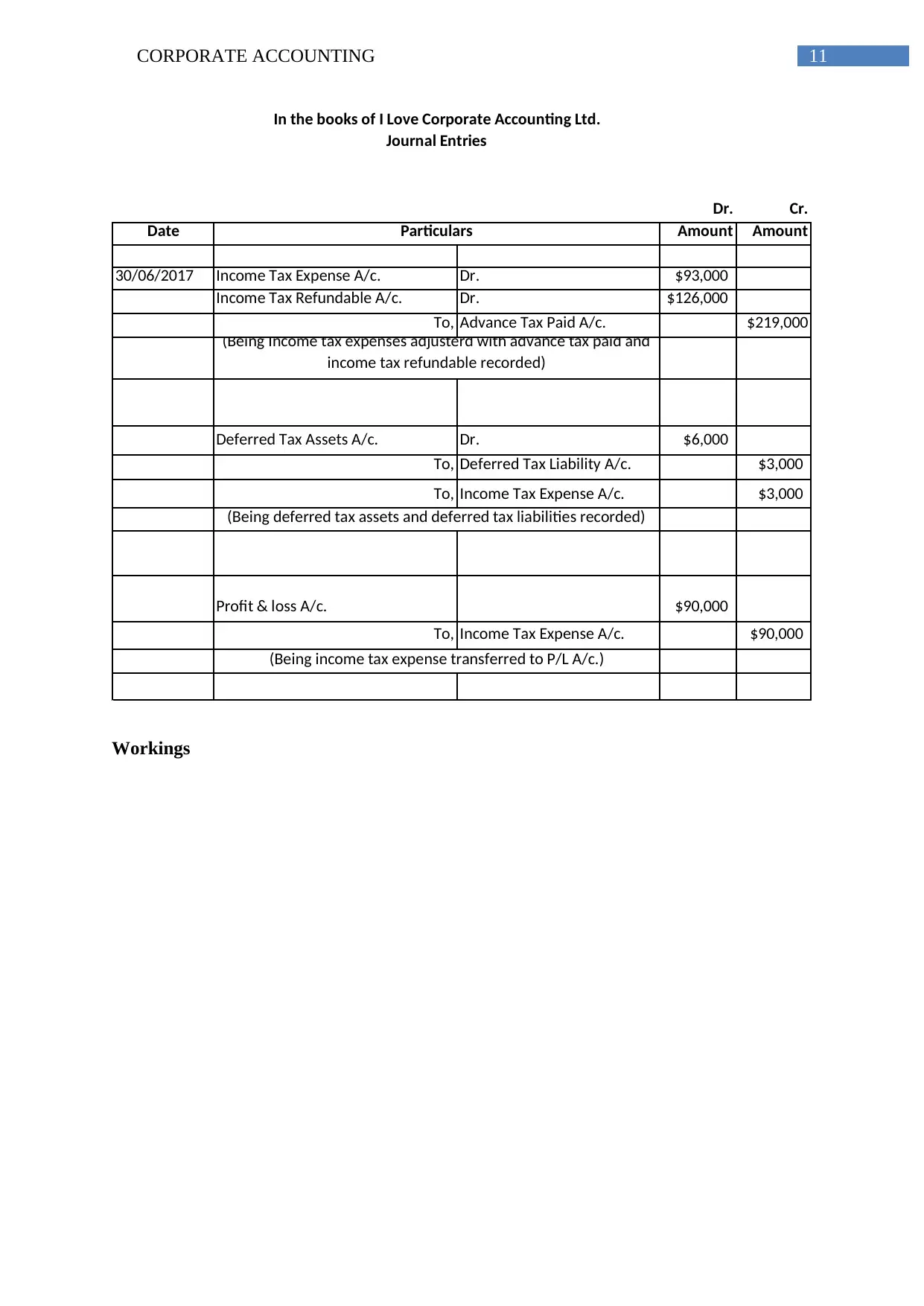

11CORPORATE ACCOUNTING

Dr. Cr.

Date Amount Amount

30/06/2017 Income Tax Expense A/c. Dr. $93,000

Income Tax Refundable A/c. Dr. $126,000

To, Advance Tax Paid A/c. $219,000

Deferred Tax Assets A/c. Dr. $6,000

To, Deferred Tax Liability A/c. $3,000

To, Income Tax Expense A/c. $3,000

Profit & loss A/c. $90,000

To, Income Tax Expense A/c. $90,000

(Being income tax expense transferred to P/L A/c.)

In the books of I Love Corporate Accounting Ltd.

Journal Entries

Particulars

(Being Income tax expenses adjusterd with advance tax paid and

income tax refundable recorded)

(Being deferred tax assets and deferred tax liabilities recorded)

Workings

Dr. Cr.

Date Amount Amount

30/06/2017 Income Tax Expense A/c. Dr. $93,000

Income Tax Refundable A/c. Dr. $126,000

To, Advance Tax Paid A/c. $219,000

Deferred Tax Assets A/c. Dr. $6,000

To, Deferred Tax Liability A/c. $3,000

To, Income Tax Expense A/c. $3,000

Profit & loss A/c. $90,000

To, Income Tax Expense A/c. $90,000

(Being income tax expense transferred to P/L A/c.)

In the books of I Love Corporate Accounting Ltd.

Journal Entries

Particulars

(Being Income tax expenses adjusterd with advance tax paid and

income tax refundable recorded)

(Being deferred tax assets and deferred tax liabilities recorded)

Workings

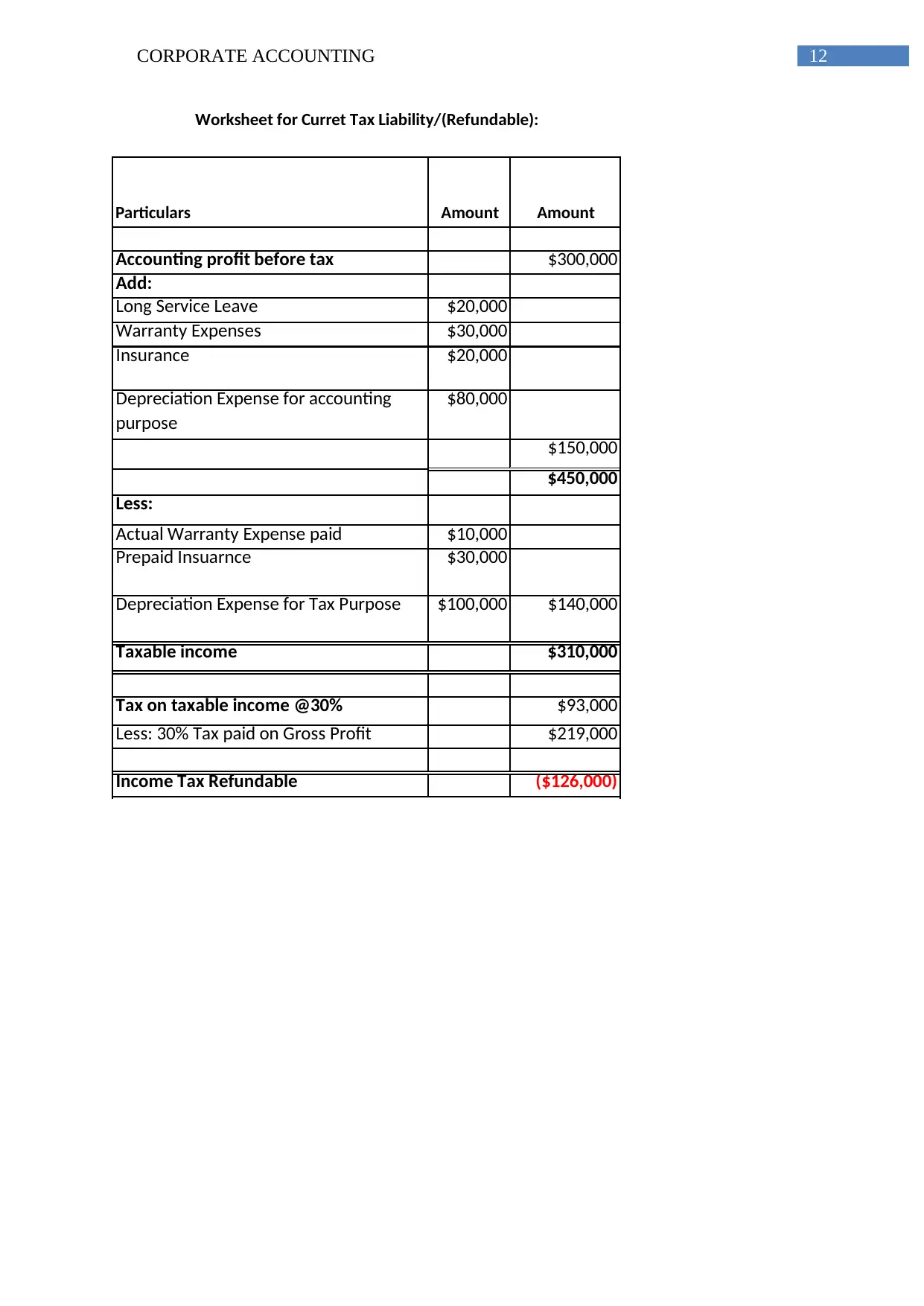

12CORPORATE ACCOUNTING

Particulars Amount Amount

Accounting profit before tax $300,000

Add:

Long Service Leave $20,000

Warranty Expenses $30,000

Insurance $20,000

Depreciation Expense for accounting

purpose

$80,000

$150,000

$450,000

Less:

Actual Warranty Expense paid $10,000

Prepaid Insuarnce $30,000

Depreciation Expense for Tax Purpose $100,000 $140,000

Taxable income $310,000

Tax on taxable income @30% $93,000

Less: 30% Tax paid on Gross Profit $219,000

Income Tax Refundable ($126,000)

Worksheet for Curret Tax Liability/(Refundable):

Particulars Amount Amount

Accounting profit before tax $300,000

Add:

Long Service Leave $20,000

Warranty Expenses $30,000

Insurance $20,000

Depreciation Expense for accounting

purpose

$80,000

$150,000

$450,000

Less:

Actual Warranty Expense paid $10,000

Prepaid Insuarnce $30,000

Depreciation Expense for Tax Purpose $100,000 $140,000

Taxable income $310,000

Tax on taxable income @30% $93,000

Less: 30% Tax paid on Gross Profit $219,000

Income Tax Refundable ($126,000)

Worksheet for Curret Tax Liability/(Refundable):

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.