Corporate Accounting and Financial Reporting Analysis

VerifiedAdded on 2023/06/04

|12

|2962

|370

Report

AI Summary

This report provides a comprehensive analysis of corporate accounting, encompassing corporate regulations, the process of setting accounting standards, and detailed examinations of equity components within four publicly listed companies on the ASX: Evolution Mining, BHP Billiton, Rio Tinto, and Altura Mining. The report critically discusses the necessity of regulating financial accounting and reporting versus allowing voluntary disclosure by managers, highlighting the advantages and disadvantages of each approach. It explores the role of the Australian Accounting Standards Board (AASB) in global standard setting, including its contributions to the International Accounting Standards Board (IASB) and the adoption of International Financial Reporting Standards (IFRS). Furthermore, the report delves into the specifics of equity items, such as issued capital, reserves, and accumulated losses, for each of the selected companies. It also provides a comparative analysis of debt and equity, offering a clear understanding of their proportions within the financial structures of the studied entities, which is crucial for investment decisions and assessing financial health.

Running head: CORPORATE ACCOUNTING

Corporate accounting

Name of the student

Name of the university

Student ID

Author note

Corporate accounting

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2CORPORATE ACCOUNTING

Table of Contents

(i) Corporate regulation........................................................................................................3

(ii) Setting of accounting standard........................................................................................5

(iii) Items of equity.................................................................................................................6

(iv) Comparative analysis for debt and equity.....................................................................10

Reference..................................................................................................................................11

Table of Contents

(i) Corporate regulation........................................................................................................3

(ii) Setting of accounting standard........................................................................................5

(iii) Items of equity.................................................................................................................6

(iv) Comparative analysis for debt and equity.....................................................................10

Reference..................................................................................................................................11

3CORPORATE ACCOUNTING

(i) Corporate regulation

In accounting, measurement and identification of elements included in the financial

statement and its impact on the financial status and circumstances shall be defined in the form

of standards and regulation. These regulations are accounting rules for the purpose of

financial accounting as well as reporting. These regulations mention what shall be reported

under the company accounts. Further, these provide guarantees for certain approaches, cases

and requirements those are generally taken into account while preparing the financial

statements (Malsch 2013). Apart from that these regulation assist the potential investors to

make any crucial decision regarding investment. While the accounting standards and

regulations are discussed the 1st thing comes into mind is the accounting report. In accordance

with IASC (International Accounting Standards Committee) the accounting reports are the

documents that represent the entity’s financial position and performance. The report can be

altered on the basis of the material changes in the financial position of the company (Watson

2015). In addition to this, another important aspect of regulating the reporting is accounting

framework. Conceptual framework is the fundamental system and objective that makes the

standard consistent through stating that accounting reports are based on the guidelines. Rules

are the set in accounting standard that can be formulated from the framework. However, in

case of any conflict for interpretation regulation is applied over framework. Various

advantages of regulating the financial reporting and accounting are as follows –

Protecting the investors – regulating the accounting reporting will enhance the

investor’s confidence with regard to investment. the reason behind this is that the

investors are interested in realizing their investment and their interests are assured

through reviewing the authentic and correct information (Newberry 2015)

(i) Corporate regulation

In accounting, measurement and identification of elements included in the financial

statement and its impact on the financial status and circumstances shall be defined in the form

of standards and regulation. These regulations are accounting rules for the purpose of

financial accounting as well as reporting. These regulations mention what shall be reported

under the company accounts. Further, these provide guarantees for certain approaches, cases

and requirements those are generally taken into account while preparing the financial

statements (Malsch 2013). Apart from that these regulation assist the potential investors to

make any crucial decision regarding investment. While the accounting standards and

regulations are discussed the 1st thing comes into mind is the accounting report. In accordance

with IASC (International Accounting Standards Committee) the accounting reports are the

documents that represent the entity’s financial position and performance. The report can be

altered on the basis of the material changes in the financial position of the company (Watson

2015). In addition to this, another important aspect of regulating the reporting is accounting

framework. Conceptual framework is the fundamental system and objective that makes the

standard consistent through stating that accounting reports are based on the guidelines. Rules

are the set in accounting standard that can be formulated from the framework. However, in

case of any conflict for interpretation regulation is applied over framework. Various

advantages of regulating the financial reporting and accounting are as follows –

Protecting the investors – regulating the accounting reporting will enhance the

investor’s confidence with regard to investment. the reason behind this is that the

investors are interested in realizing their investment and their interests are assured

through reviewing the authentic and correct information (Newberry 2015)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4CORPORATE ACCOUNTING

Understandability – this is another advantage of regulating the financial reporting and

accounting. Regulations make it easier to creating the financial statements and

analysing the results. Further, while the financial reports are prepared as per the

regulations some assumptions are made by every entity. Once the assumptions are

realized it helps the users to understand the treatments (Gipper, Lombardi and Skinner

2013).

Guidance – this one is another advantage for regulating the information included in

the financial reports. Preparing the reports through using the regulations is flexibility.

As the financial world is becoming more complex it is becoming more problematic to

create standardized format for entire company. Therefore, the report prepared through

following the regulations will create a standardised format (Mazhambe 2014).

However, irrespective of the above mentioned advantages, some disadvantages are

there in regulating the financial reporting and accounting those can be avoided if the

managers are allowed disclosing the information voluntarily. These disadvantages are –

Cost involvement – using the regulation like accounting standards while preparing the

financial statements requires high costs to be complied with. Further the company is

required to change the procedures that requires large amount of financial investment

including system upgrades, employee training and labour costs. For instance, the

company require some people who will look after correct application of standards and

regulation and some people who will provide training to other employees for adopting

the regulation (Bamber and McMeeking 2016).

Financial statement that includes the balance sheet, profit and loss statement and cash

flow statement requires following step by step process while these are prepared in

compliance with the regulation and accounting standards. However, these steps are

not required if the managers disclose the information voluntarily (Aasb.gov.au 2018).

Understandability – this is another advantage of regulating the financial reporting and

accounting. Regulations make it easier to creating the financial statements and

analysing the results. Further, while the financial reports are prepared as per the

regulations some assumptions are made by every entity. Once the assumptions are

realized it helps the users to understand the treatments (Gipper, Lombardi and Skinner

2013).

Guidance – this one is another advantage for regulating the information included in

the financial reports. Preparing the reports through using the regulations is flexibility.

As the financial world is becoming more complex it is becoming more problematic to

create standardized format for entire company. Therefore, the report prepared through

following the regulations will create a standardised format (Mazhambe 2014).

However, irrespective of the above mentioned advantages, some disadvantages are

there in regulating the financial reporting and accounting those can be avoided if the

managers are allowed disclosing the information voluntarily. These disadvantages are –

Cost involvement – using the regulation like accounting standards while preparing the

financial statements requires high costs to be complied with. Further the company is

required to change the procedures that requires large amount of financial investment

including system upgrades, employee training and labour costs. For instance, the

company require some people who will look after correct application of standards and

regulation and some people who will provide training to other employees for adopting

the regulation (Bamber and McMeeking 2016).

Financial statement that includes the balance sheet, profit and loss statement and cash

flow statement requires following step by step process while these are prepared in

compliance with the regulation and accounting standards. However, these steps are

not required if the managers disclose the information voluntarily (Aasb.gov.au 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5CORPORATE ACCOUNTING

However, it is found from the above discussion that irrespective of some limitations

regulating the financial reporting and accounting will enhance the reporting quality. Further,

it will provide clear and concise information to the users who take any crucial decision based

on the financial report. Therefore, the financial reporting and accounting shall be regulated.

(ii) Setting of accounting standard

AASB taking part in the process of setting the global accounting standard

AASB (Australian accounting standard board) prepares accounting standards for

public, private and not-for-profit sectors and takes part in formulating IAS (international

accounting standards). The below mentioned activities are undertaken by AASB for making

contribution to and taking part in setting the global accounting standards –

Attempting to act as the though leader while contributing in developing the global

standards by IASB and IPSASB (International Public Sector Accounting Standards

Board) and setting up of their priorities and agenda.

Involves itself in considerable projects of IPSASB and IASB as soon as possible

under the procedure through leading projects for research. Further, it takes part in

projecting the panel, providing the technical support, supporting the panel members

and does not wait till the comment is requested through exposure draft and discussion

paper (Preiato, Brown and Tarca 2015).

As an active contributor participates in the activities related to IASB’s meeting for

world standard setters. It further takes part in other national standard setters,

groupings of standard setter, regional grouping for national standards setters like

AOSSG (Asian-Oceanian Standard-Setters Group) and NSS (National Standard

Setters Group).

However, it is found from the above discussion that irrespective of some limitations

regulating the financial reporting and accounting will enhance the reporting quality. Further,

it will provide clear and concise information to the users who take any crucial decision based

on the financial report. Therefore, the financial reporting and accounting shall be regulated.

(ii) Setting of accounting standard

AASB taking part in the process of setting the global accounting standard

AASB (Australian accounting standard board) prepares accounting standards for

public, private and not-for-profit sectors and takes part in formulating IAS (international

accounting standards). The below mentioned activities are undertaken by AASB for making

contribution to and taking part in setting the global accounting standards –

Attempting to act as the though leader while contributing in developing the global

standards by IASB and IPSASB (International Public Sector Accounting Standards

Board) and setting up of their priorities and agenda.

Involves itself in considerable projects of IPSASB and IASB as soon as possible

under the procedure through leading projects for research. Further, it takes part in

projecting the panel, providing the technical support, supporting the panel members

and does not wait till the comment is requested through exposure draft and discussion

paper (Preiato, Brown and Tarca 2015).

As an active contributor participates in the activities related to IASB’s meeting for

world standard setters. It further takes part in other national standard setters,

groupings of standard setter, regional grouping for national standards setters like

AOSSG (Asian-Oceanian Standard-Setters Group) and NSS (National Standard

Setters Group).

6CORPORATE ACCOUNTING

Makes submission on IPSASB and IASB consultative documents those are expected

to be considerable in Australian aspect and and encourages the Australian constitutes

in participating for the due processes of IPSASB and IASB (Henderson et al. 2015).

With regard to Australia’s experience in adopting IFRS, it promotes the IFRS uses

globally which in turn is useful in transitioning the jurisdictions. It is further important

in avoiding wide range of IFRSs national versions.

Reason why IFRS issued by IASB is not compulsory for IASB member countries

IFRS are the set for accounting standard that is issued by IASB (international

accounting standards board). It is becoming global standard for preparing the financial

reports by public companies. Near about 120 countries and the reporting jurisdictions are

required IFRS for its domestic listed entities, however, near about 90 countries are fully

conformed to the IFRS. However, as per the clearance of SEC 2015 was the earliest possible

date for using IFRS by the public companies. However, as per the approved statement issued

on 24th February, SEC stated that if any country is not pursuing for early adoption it can

reconsider the adoption later (Odia and Ogiedu 2013). Therefore, IFRS set by IASB is not

compulsory for the member countries of IASB.

Owner’s equity

4 listed public limited companies on ASX under same industry those will be

considered for this part are Evolution Mining, BHP Billiton, Rio Tinto and Altura Mining.

(iii) Items of equity

Evolution Mining – items listed under equity for Evaluation Mining are as follows –

Issued capital – it is the share capital that is issued to the shareholders. Issued capital

is the part of company’s authorised capital. It is the nominal value of the share held by

Makes submission on IPSASB and IASB consultative documents those are expected

to be considerable in Australian aspect and and encourages the Australian constitutes

in participating for the due processes of IPSASB and IASB (Henderson et al. 2015).

With regard to Australia’s experience in adopting IFRS, it promotes the IFRS uses

globally which in turn is useful in transitioning the jurisdictions. It is further important

in avoiding wide range of IFRSs national versions.

Reason why IFRS issued by IASB is not compulsory for IASB member countries

IFRS are the set for accounting standard that is issued by IASB (international

accounting standards board). It is becoming global standard for preparing the financial

reports by public companies. Near about 120 countries and the reporting jurisdictions are

required IFRS for its domestic listed entities, however, near about 90 countries are fully

conformed to the IFRS. However, as per the clearance of SEC 2015 was the earliest possible

date for using IFRS by the public companies. However, as per the approved statement issued

on 24th February, SEC stated that if any country is not pursuing for early adoption it can

reconsider the adoption later (Odia and Ogiedu 2013). Therefore, IFRS set by IASB is not

compulsory for the member countries of IASB.

Owner’s equity

4 listed public limited companies on ASX under same industry those will be

considered for this part are Evolution Mining, BHP Billiton, Rio Tinto and Altura Mining.

(iii) Items of equity

Evolution Mining – items listed under equity for Evaluation Mining are as follows –

Issued capital – it is the share capital that is issued to the shareholders. Issued capital

is the part of company’s authorised capital. It is the nominal value of the share held by

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7CORPORATE ACCOUNTING

shareholders. Issued share capital forms part of the amount that is invested by the

shareholders in the entity.

Reserves – reserves in the balance sheet is the term used for referring the

shareholder’s equity part excluding the part of basic share capital. Reserves generally

includes the particular part of surplus that are generated from other sources like

increasing the fixed asset’s value, selling stock on premium

Accumulated losses – account balance for retained earnings generally gives positive

credit balance created from accumulation of income over the period of time. The

retained earnings also get affected by the distribution of dividend. However, the

accumulated losses reduce the retained earning into negative balance that is known as

accumulated deficit (Evolutionmining.com.au 2018).

Changes in equity –

Items 2017 2016 2015 2014

Issued capital $21,83,727.00 $17,70,987.00 $12,92,620.00 $10,48,424.00

Reserves $ 38,795.00 $ 29,363.00 $ 27,446.00 $ 18,219.00

Accumulated losses $ -94,270.00 $ 2,48,917.00 $ -1,95,506.00 $ 2,81,339.00

Reason of increase in the amount of issued capital was contributions towards equity

and reasons of accumulated loss was payment of dividends

BHP Billiton – items listed under equity for BHP Billiton are as follows –

Share capital – it is the funds raised through issuing the shares in return of cash or any

other consideration. It is the maximum value of the share that can be issued by a

company.

shareholders. Issued share capital forms part of the amount that is invested by the

shareholders in the entity.

Reserves – reserves in the balance sheet is the term used for referring the

shareholder’s equity part excluding the part of basic share capital. Reserves generally

includes the particular part of surplus that are generated from other sources like

increasing the fixed asset’s value, selling stock on premium

Accumulated losses – account balance for retained earnings generally gives positive

credit balance created from accumulation of income over the period of time. The

retained earnings also get affected by the distribution of dividend. However, the

accumulated losses reduce the retained earning into negative balance that is known as

accumulated deficit (Evolutionmining.com.au 2018).

Changes in equity –

Items 2017 2016 2015 2014

Issued capital $21,83,727.00 $17,70,987.00 $12,92,620.00 $10,48,424.00

Reserves $ 38,795.00 $ 29,363.00 $ 27,446.00 $ 18,219.00

Accumulated losses $ -94,270.00 $ 2,48,917.00 $ -1,95,506.00 $ 2,81,339.00

Reason of increase in the amount of issued capital was contributions towards equity

and reasons of accumulated loss was payment of dividends

BHP Billiton – items listed under equity for BHP Billiton are as follows –

Share capital – it is the funds raised through issuing the shares in return of cash or any

other consideration. It is the maximum value of the share that can be issued by a

company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8CORPORATE ACCOUNTING

Treasury shares – these shares are bought back by issuing entity and it reduces the

number of outstanding shares in open market. However, the treasury shares do not

pay dividends and it does not carry any voting right.

Reserves – reserves in the balance sheet is the term used for referring the

shareholder’s equity part excluding the part of basic share capital. Reserves generally

includes the particular part of surplus that are generated from other sources like

increasing the fixed asset’s value, selling stock on premium (BHP 2018)

Retained earnings – it is the profit earned by the company till date reduced by any

dividends or distribution made to the investors. Amount of retained earnings is

adjusted whenever there takes place any entry that has impact on expenses or revenue

account.

Changes in equity –

Items 2017 ($'m) 2016 ($'m) 2015($'m) 2014 ($'m)

Share capital $ 2,243.00 $ 2,243.00 $ 2,243.00 $ 2,255.00

Treasury shares $ -3.00 $ -33.00 $ -76.00 $ -587.00

Reserves $ 2,400.00 $ 2,538.00 $ 2,557.00 $ 2,927.00

Retained earnings $ 52,618.00 $ 49,542.00 $ 60,044.00 $ 74,548.00

Reason of changes in retained earnings was payment of dividend and reason of

changes in reserves was employee contribution and other adjustments of employees.

Rio Tinto – items listed under equity for Rio Tinto are as follows –

Share capital – as explained above for BHP Billiton

Share premium – share premium is the excess amount that is received by the company

over and above the par value of its share (Riotinto.com 2018).

Other reserves – as explained above for BHP Billiton

Retained earnings - as explained above for BHP Billiton

Treasury shares – these shares are bought back by issuing entity and it reduces the

number of outstanding shares in open market. However, the treasury shares do not

pay dividends and it does not carry any voting right.

Reserves – reserves in the balance sheet is the term used for referring the

shareholder’s equity part excluding the part of basic share capital. Reserves generally

includes the particular part of surplus that are generated from other sources like

increasing the fixed asset’s value, selling stock on premium (BHP 2018)

Retained earnings – it is the profit earned by the company till date reduced by any

dividends or distribution made to the investors. Amount of retained earnings is

adjusted whenever there takes place any entry that has impact on expenses or revenue

account.

Changes in equity –

Items 2017 ($'m) 2016 ($'m) 2015($'m) 2014 ($'m)

Share capital $ 2,243.00 $ 2,243.00 $ 2,243.00 $ 2,255.00

Treasury shares $ -3.00 $ -33.00 $ -76.00 $ -587.00

Reserves $ 2,400.00 $ 2,538.00 $ 2,557.00 $ 2,927.00

Retained earnings $ 52,618.00 $ 49,542.00 $ 60,044.00 $ 74,548.00

Reason of changes in retained earnings was payment of dividend and reason of

changes in reserves was employee contribution and other adjustments of employees.

Rio Tinto – items listed under equity for Rio Tinto are as follows –

Share capital – as explained above for BHP Billiton

Share premium – share premium is the excess amount that is received by the company

over and above the par value of its share (Riotinto.com 2018).

Other reserves – as explained above for BHP Billiton

Retained earnings - as explained above for BHP Billiton

9CORPORATE ACCOUNTING

Changes in equity –

Items 2017 ($'m) 2016 ($'m) 2015($'m) 2014 ($'m)

Share capital $ 4,360.00 $ 4,139.00 $ 4,174.00 $ 4,765.00

Share premium $ 4,306.00 $ 4,304.00 $ 4,300.00 $ 4,288.00

Other reserves $ 12,284.00 $ 9,216.00 $ 9,139.00 $ 11,122.00

Retained earnings $ 23,761.00 $ 21,631.00 $ 19,736.00 $ 26,110.00

Reason of changes in retained earnings was payment of dividend and share buyback.

Further, the reason of changes in the amount of share capital was buyback of shares.

Altura Mining – items listed under equity for Altura Mining are as follows –

Contributed equity – contributed equity that is also known as the paid-in-capital is

cash amount and other assets that have been given by the shareholders in exchange of

the shares. To be more specific, this price is paid by the shareholders in exchange of

their ownership stake (Alturamining.com 2018.).

Reserves – as explained above for BHP Billiton

Accumulated losses – as explained above for Evolution Mining

Changes in equity –

Items 2017 ($'000) 2016 ($'000) 2015($'000) 2014 ($'000)

Contributed equity $ 1,46,556.00 $ 1,05,840.00 $ 78,904.00 $ 74,562.00

Reserves $ 595.00 $ -240.00 $ 179.00 $ 492.00

Accumulated losses $ -90,460.00 $ -84,333.00 $ -53,672.00 $ -23,870.00

Reason of changes in contributed equity is transfer to equity from share based

payment and share issue for bonus payment to employees.

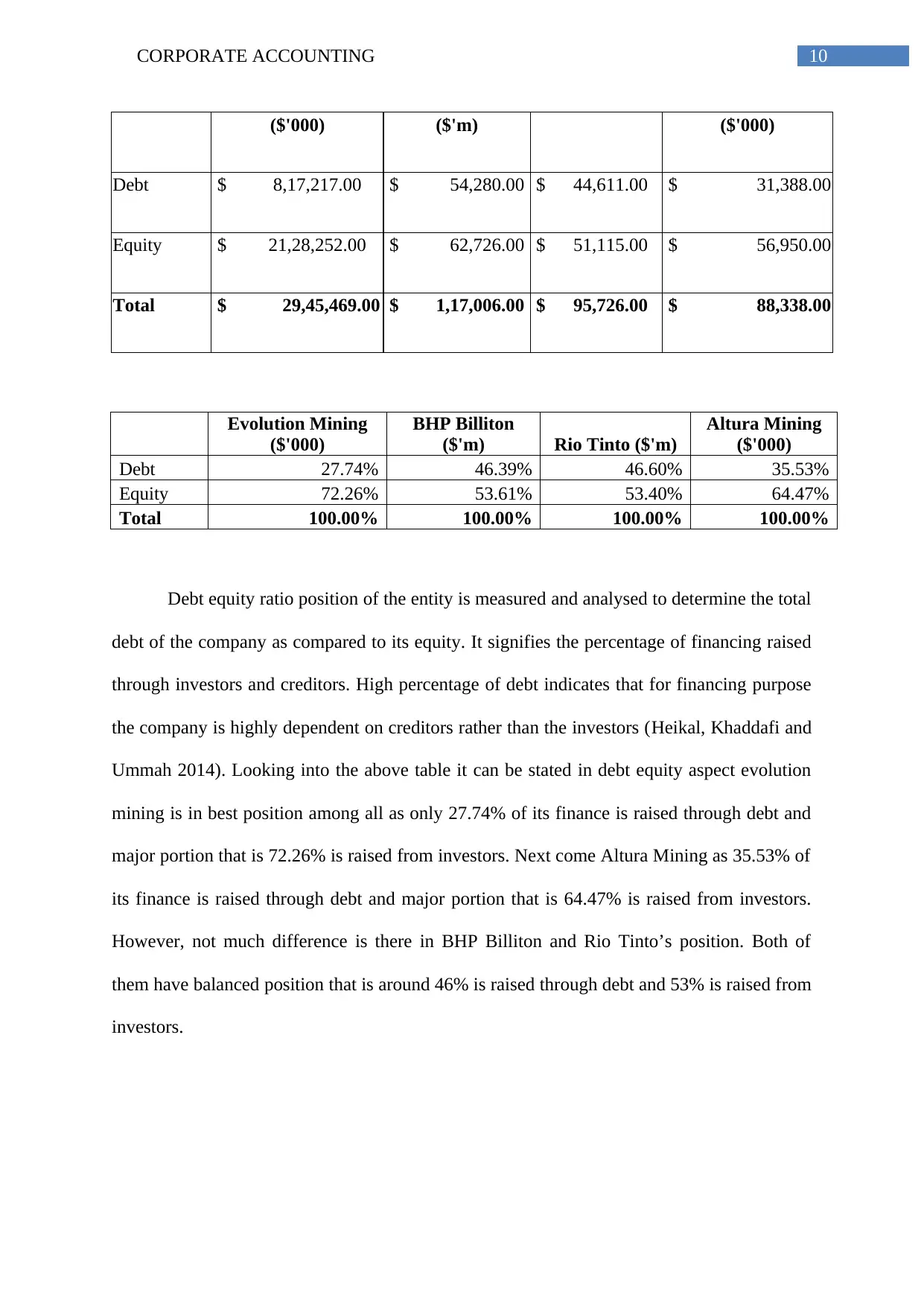

(iv) Comparative analysis for debt and equity

Evolution Mining BHP Billiton Rio Tinto ($'m) Altura Mining

Changes in equity –

Items 2017 ($'m) 2016 ($'m) 2015($'m) 2014 ($'m)

Share capital $ 4,360.00 $ 4,139.00 $ 4,174.00 $ 4,765.00

Share premium $ 4,306.00 $ 4,304.00 $ 4,300.00 $ 4,288.00

Other reserves $ 12,284.00 $ 9,216.00 $ 9,139.00 $ 11,122.00

Retained earnings $ 23,761.00 $ 21,631.00 $ 19,736.00 $ 26,110.00

Reason of changes in retained earnings was payment of dividend and share buyback.

Further, the reason of changes in the amount of share capital was buyback of shares.

Altura Mining – items listed under equity for Altura Mining are as follows –

Contributed equity – contributed equity that is also known as the paid-in-capital is

cash amount and other assets that have been given by the shareholders in exchange of

the shares. To be more specific, this price is paid by the shareholders in exchange of

their ownership stake (Alturamining.com 2018.).

Reserves – as explained above for BHP Billiton

Accumulated losses – as explained above for Evolution Mining

Changes in equity –

Items 2017 ($'000) 2016 ($'000) 2015($'000) 2014 ($'000)

Contributed equity $ 1,46,556.00 $ 1,05,840.00 $ 78,904.00 $ 74,562.00

Reserves $ 595.00 $ -240.00 $ 179.00 $ 492.00

Accumulated losses $ -90,460.00 $ -84,333.00 $ -53,672.00 $ -23,870.00

Reason of changes in contributed equity is transfer to equity from share based

payment and share issue for bonus payment to employees.

(iv) Comparative analysis for debt and equity

Evolution Mining BHP Billiton Rio Tinto ($'m) Altura Mining

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10CORPORATE ACCOUNTING

($'000) ($'m) ($'000)

Debt $ 8,17,217.00 $ 54,280.00 $ 44,611.00 $ 31,388.00

Equity $ 21,28,252.00 $ 62,726.00 $ 51,115.00 $ 56,950.00

Total $ 29,45,469.00 $ 1,17,006.00 $ 95,726.00 $ 88,338.00

Evolution Mining

($'000)

BHP Billiton

($'m) Rio Tinto ($'m)

Altura Mining

($'000)

Debt 27.74% 46.39% 46.60% 35.53%

Equity 72.26% 53.61% 53.40% 64.47%

Total 100.00% 100.00% 100.00% 100.00%

Debt equity ratio position of the entity is measured and analysed to determine the total

debt of the company as compared to its equity. It signifies the percentage of financing raised

through investors and creditors. High percentage of debt indicates that for financing purpose

the company is highly dependent on creditors rather than the investors (Heikal, Khaddafi and

Ummah 2014). Looking into the above table it can be stated in debt equity aspect evolution

mining is in best position among all as only 27.74% of its finance is raised through debt and

major portion that is 72.26% is raised from investors. Next come Altura Mining as 35.53% of

its finance is raised through debt and major portion that is 64.47% is raised from investors.

However, not much difference is there in BHP Billiton and Rio Tinto’s position. Both of

them have balanced position that is around 46% is raised through debt and 53% is raised from

investors.

($'000) ($'m) ($'000)

Debt $ 8,17,217.00 $ 54,280.00 $ 44,611.00 $ 31,388.00

Equity $ 21,28,252.00 $ 62,726.00 $ 51,115.00 $ 56,950.00

Total $ 29,45,469.00 $ 1,17,006.00 $ 95,726.00 $ 88,338.00

Evolution Mining

($'000)

BHP Billiton

($'m) Rio Tinto ($'m)

Altura Mining

($'000)

Debt 27.74% 46.39% 46.60% 35.53%

Equity 72.26% 53.61% 53.40% 64.47%

Total 100.00% 100.00% 100.00% 100.00%

Debt equity ratio position of the entity is measured and analysed to determine the total

debt of the company as compared to its equity. It signifies the percentage of financing raised

through investors and creditors. High percentage of debt indicates that for financing purpose

the company is highly dependent on creditors rather than the investors (Heikal, Khaddafi and

Ummah 2014). Looking into the above table it can be stated in debt equity aspect evolution

mining is in best position among all as only 27.74% of its finance is raised through debt and

major portion that is 72.26% is raised from investors. Next come Altura Mining as 35.53% of

its finance is raised through debt and major portion that is 64.47% is raised from investors.

However, not much difference is there in BHP Billiton and Rio Tinto’s position. Both of

them have balanced position that is around 46% is raised through debt and 53% is raised from

investors.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11CORPORATE ACCOUNTING

Reference

Aasb.gov.au. (2018). [online] Available at:

https://www.aasb.gov.au/admin/file/content102/c3/Policy_Statement_03-11.pdf [Accessed 19

Sep. 2018].

Alturamining.com., 2018. Altura Mining | Charging Forward with Lithium. [online]

Available at: https://alturamining.com/ [Accessed 21 Sep. 2018].

Bamber, M. and McMeeking, K., 2016. An examination of international accounting standard-

setting due process and the implications for legitimacy. The British Accounting

Review, 48(1), pp.59-73.

BHP., 2018. BHP | A leading global resources company. [online] Available at:

https://www.bhp.com/ [Accessed 21 Sep. 2018].

Evolutionmining.com.au., 2018. Evolution Mining – Australian Gold Company. [online]

Available at: https://evolutionmining.com.au/ [Accessed 21 Sep. 2018].

Gipper, B., Lombardi, B.J. and Skinner, D.J., 2013. The politics of accounting standard-

setting: A review of empirical research. Australian Journal of Management, 38(3), pp.523-

551.

Heikal, M., Khaddafi, M. and Ummah, A., 2014. Influence analysis of return on assets

(ROA), return on equity (ROE), net profit margin (NPM), debt to equity ratio (DER), and

current ratio (CR), against corporate profit growth in automotive in Indonesia Stock

Exchange. International Journal of Academic Research in Business and Social

Sciences, 4(12), p.101.

Reference

Aasb.gov.au. (2018). [online] Available at:

https://www.aasb.gov.au/admin/file/content102/c3/Policy_Statement_03-11.pdf [Accessed 19

Sep. 2018].

Alturamining.com., 2018. Altura Mining | Charging Forward with Lithium. [online]

Available at: https://alturamining.com/ [Accessed 21 Sep. 2018].

Bamber, M. and McMeeking, K., 2016. An examination of international accounting standard-

setting due process and the implications for legitimacy. The British Accounting

Review, 48(1), pp.59-73.

BHP., 2018. BHP | A leading global resources company. [online] Available at:

https://www.bhp.com/ [Accessed 21 Sep. 2018].

Evolutionmining.com.au., 2018. Evolution Mining – Australian Gold Company. [online]

Available at: https://evolutionmining.com.au/ [Accessed 21 Sep. 2018].

Gipper, B., Lombardi, B.J. and Skinner, D.J., 2013. The politics of accounting standard-

setting: A review of empirical research. Australian Journal of Management, 38(3), pp.523-

551.

Heikal, M., Khaddafi, M. and Ummah, A., 2014. Influence analysis of return on assets

(ROA), return on equity (ROE), net profit margin (NPM), debt to equity ratio (DER), and

current ratio (CR), against corporate profit growth in automotive in Indonesia Stock

Exchange. International Journal of Academic Research in Business and Social

Sciences, 4(12), p.101.

12CORPORATE ACCOUNTING

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Malsch, B., 2013. Politicizing the expertise of the accounting industry in the realm of

corporate social responsibility. Accounting, Organizations and Society, 38(2), pp.149-168.

Mazhambe, Z., 2014. Review of International Accounting Standards Board (IASB) Proposed

New Conceptual Framework: Discussion Paper (DP/2013/1). Journal of Modern Accounting

and Auditing, 10(8).

Newberry, S., 2015. Public sector accounting: shifting concepts of accountability. Public

Money & Management, 35(5), pp.371-376.

Odia, J.O. and Ogiedu, K.O., 2013. IFRS adoption: Issues, challenges and lessons for Nigeria

and other adopters. Mediterranean Journal of Social Sciences, 4(3), p.389.

Preiato, J., Brown, P. and Tarca, A., 2015. A comparison of between‐country measures of

legal setting and enforcement of accounting standards. Journal of Business Finance &

Accounting, 42(1-2), pp.1-50.

Riotinto.com., 2018. Global home. [online] Available at: https://www.riotinto.com/

[Accessed 21 Sep. 2018].

Watson, L., 2015. Corporate social responsibility research in accounting. Journal of

Accounting Literature, 34, pp.1-16.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Malsch, B., 2013. Politicizing the expertise of the accounting industry in the realm of

corporate social responsibility. Accounting, Organizations and Society, 38(2), pp.149-168.

Mazhambe, Z., 2014. Review of International Accounting Standards Board (IASB) Proposed

New Conceptual Framework: Discussion Paper (DP/2013/1). Journal of Modern Accounting

and Auditing, 10(8).

Newberry, S., 2015. Public sector accounting: shifting concepts of accountability. Public

Money & Management, 35(5), pp.371-376.

Odia, J.O. and Ogiedu, K.O., 2013. IFRS adoption: Issues, challenges and lessons for Nigeria

and other adopters. Mediterranean Journal of Social Sciences, 4(3), p.389.

Preiato, J., Brown, P. and Tarca, A., 2015. A comparison of between‐country measures of

legal setting and enforcement of accounting standards. Journal of Business Finance &

Accounting, 42(1-2), pp.1-50.

Riotinto.com., 2018. Global home. [online] Available at: https://www.riotinto.com/

[Accessed 21 Sep. 2018].

Watson, L., 2015. Corporate social responsibility research in accounting. Journal of

Accounting Literature, 34, pp.1-16.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.