Corporate Financial Accounting Report: Corporate Regulation & Equity

VerifiedAdded on 2023/06/07

|13

|3180

|477

Report

AI Summary

This report provides a comprehensive analysis of corporate financial accounting, focusing on corporate regulations, accounting standards, and owners' equity. The report begins with an executive summary, followed by an in-depth examination of corporate regulations governing accounting information disclosure in Australia, emphasizing the importance of regulations in ensuring accurate and reliable financial reporting. The report then delves into the Australian Accounting Standards Board's (AASB) participation in global accounting standard settings, its impact on International Financial Reporting Standards (IFRS), and its influence on constituent users. Finally, the report analyzes owners' equity for four listed companies in the energy sector on the Australian Stock Exchange, providing a comparative assessment of their financial performance over several years. The report highlights key financial metrics and trends, offering valuable insights into the financial health and performance of these companies.

CORPORATE FINANCIAL ACCOUNTING

CORPORATE REGULATION, ACCOUNTING STANDARDS AND OWNERS EQUITY

ANALYSIS

Course:

Professor’s Name

Institution

City

Date

CORPORATE REGULATION, ACCOUNTING STANDARDS AND OWNERS EQUITY

ANALYSIS

Course:

Professor’s Name

Institution

City

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCIAL ACCOUNTING

Table of Content:

1. Titles and addresses…………………... ...Pg1

2. Table of Content……………………..… .Pg2

3.Executive Summary………………………Pg2

3. Corporate Regulation Report……...Pgs3,4,5

4. Accounting Setting Process…………..Pg6,7

5. Owners Equity Analysis…… .Pgs8,9,10,11

6. References…........................................Pg12,13

Executive Summary;

Query (i) entails analysis on how International Accounting Standard Board and

International Financial Reporting Standard Board is involved in reporting of financial and

accounting information to the users of this information who are investors, lenders, creditors, and

general public as a general purpose objective has improved and boosted the accounting business

sector, since it has given all relevant information for decision making.

The query (ii) involves analysis on accounting setting process tests and seek

confirmation on whether indeed the Australian Board Of Accounting participates in setting,

amending and improving international accounting standards like IFRS and its scope of users.

In query (iii) owners’ equity in finance perspective is the owners’ investment share in

the business less any draws or redemption done, while mathematically it means the amount of

owners’ equity fewer liabilities, likewise it is explained as the balance value claimed on business

asset since the responsibilities are higher for claim (Needles, Powers, and Crosson, 2013.P.36.)

(i)

Table of Content:

1. Titles and addresses…………………... ...Pg1

2. Table of Content……………………..… .Pg2

3.Executive Summary………………………Pg2

3. Corporate Regulation Report……...Pgs3,4,5

4. Accounting Setting Process…………..Pg6,7

5. Owners Equity Analysis…… .Pgs8,9,10,11

6. References…........................................Pg12,13

Executive Summary;

Query (i) entails analysis on how International Accounting Standard Board and

International Financial Reporting Standard Board is involved in reporting of financial and

accounting information to the users of this information who are investors, lenders, creditors, and

general public as a general purpose objective has improved and boosted the accounting business

sector, since it has given all relevant information for decision making.

The query (ii) involves analysis on accounting setting process tests and seek

confirmation on whether indeed the Australian Board Of Accounting participates in setting,

amending and improving international accounting standards like IFRS and its scope of users.

In query (iii) owners’ equity in finance perspective is the owners’ investment share in

the business less any draws or redemption done, while mathematically it means the amount of

owners’ equity fewer liabilities, likewise it is explained as the balance value claimed on business

asset since the responsibilities are higher for claim (Needles, Powers, and Crosson, 2013.P.36.)

(i)

CORPORATE FINANCIAL ACCOUNTING

The Report on Corporate Regulations Governing Accounting Information Disclosure in

Australia.

Financial information regulation is a restrictive supervision requirement that has

provided guidelines that restricts and protect the integrity disclosure of the financial information

adhere for the safety of the integrity of any information that may affect the users directly or

indirectly (Bamber, Jiang and Wang,2010.Pg.1160.) In any prospect operations and success,

knowledge is power hence before attending on any matter that is deemed of essence the fact

notion of information is whether the info is relevant to the case in the subject. Wrongful

disclosure of financial information is therefore, curbed by the outlined regulations that ensure

that every data is disclosed in a disciplined manner, i.e., in the correct way, at the proper time, to

the right people and finally the correct place.

I do not oppose disclosure of company information by the managers to the users;

however, the main point of concern is the effect of that disclosure. The accounting business

environment according to the below three concerned issues raised and discussed by Australian

accounting scholars, i.e., the question of the subjectivity of the information and disclosure, biases

in reporting and finally own self-personal, informational damage expect and require the high

level of confidentiality and integrity in operations(Nobes, 2014, Pg.17.)

It should be known that in a company the regulation in company act, as well as auditing

and accounting standards, except that all material relevant information is disclosed to only the

intended user confidently. Ideally, it should be known that whenever information is prepared,

scrutinized, shared and reveal the aspect of company interest safety should prevail to ensure that

no adverse repercussion will befall the company after disclosure of information (Kirkpatrick,

2009.Pg.21.)

The Report on Corporate Regulations Governing Accounting Information Disclosure in

Australia.

Financial information regulation is a restrictive supervision requirement that has

provided guidelines that restricts and protect the integrity disclosure of the financial information

adhere for the safety of the integrity of any information that may affect the users directly or

indirectly (Bamber, Jiang and Wang,2010.Pg.1160.) In any prospect operations and success,

knowledge is power hence before attending on any matter that is deemed of essence the fact

notion of information is whether the info is relevant to the case in the subject. Wrongful

disclosure of financial information is therefore, curbed by the outlined regulations that ensure

that every data is disclosed in a disciplined manner, i.e., in the correct way, at the proper time, to

the right people and finally the correct place.

I do not oppose disclosure of company information by the managers to the users;

however, the main point of concern is the effect of that disclosure. The accounting business

environment according to the below three concerned issues raised and discussed by Australian

accounting scholars, i.e., the question of the subjectivity of the information and disclosure, biases

in reporting and finally own self-personal, informational damage expect and require the high

level of confidentiality and integrity in operations(Nobes, 2014, Pg.17.)

It should be known that in a company the regulation in company act, as well as auditing

and accounting standards, except that all material relevant information is disclosed to only the

intended user confidently. Ideally, it should be known that whenever information is prepared,

scrutinized, shared and reveal the aspect of company interest safety should prevail to ensure that

no adverse repercussion will befall the company after disclosure of information (Kirkpatrick,

2009.Pg.21.)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCIAL ACCOUNTING

The regulation on financial news is so sure that it ensures that only subjective matters of

relevance are disclosed and in this case is those which are material in context, and likewise it

provides that due diligence and competency is exercised while revealing information to the user.

Users of financial information determine what information they need and who is to disclose the

information. It is through this that the concern in question is raised, i.e., whether managers are to

be regulated on what to reveal (Chan and Watson, 2011.Pg.50.) Allow me to say that there is no

harm in reporting and disclosing any information as long as it is done in the right manner and to

the intended users.

Company managers are persons who oversee day to day operations of the business.

Therefore, they are expected to know all financial information that contributes to and boosts their

decision-making process. This, thus, mandates them to access only that information that

concerns his operation. However, since every user of information should access and utilize the

information for the benefit of the company thus the need to regulate on how the data is disclosed,

i.e., by who and to who.

The main concern is whether the manager should be allowed to disclose financial

information or regulates (Lai and Shan, 2013.Pg.33.) I wish to say that for purposes of company

interest, the manager should be restricted to reveal only that information that entails business

operation for instance on profitability, cash flows and liquidity so that he can share the info to the

employees and department for operational decision making.

A manager is however restricted by ethical principles only to disclose that information

that is deemed relevant to the user who in this case is the internal user. A manager is constrained

to withhold confidentiality and exercise due diligence while disclosing company information to

The regulation on financial news is so sure that it ensures that only subjective matters of

relevance are disclosed and in this case is those which are material in context, and likewise it

provides that due diligence and competency is exercised while revealing information to the user.

Users of financial information determine what information they need and who is to disclose the

information. It is through this that the concern in question is raised, i.e., whether managers are to

be regulated on what to reveal (Chan and Watson, 2011.Pg.50.) Allow me to say that there is no

harm in reporting and disclosing any information as long as it is done in the right manner and to

the intended users.

Company managers are persons who oversee day to day operations of the business.

Therefore, they are expected to know all financial information that contributes to and boosts their

decision-making process. This, thus, mandates them to access only that information that

concerns his operation. However, since every user of information should access and utilize the

information for the benefit of the company thus the need to regulate on how the data is disclosed,

i.e., by who and to who.

The main concern is whether the manager should be allowed to disclose financial

information or regulates (Lai and Shan, 2013.Pg.33.) I wish to say that for purposes of company

interest, the manager should be restricted to reveal only that information that entails business

operation for instance on profitability, cash flows and liquidity so that he can share the info to the

employees and department for operational decision making.

A manager is however restricted by ethical principles only to disclose that information

that is deemed relevant to the user who in this case is the internal user. A manager is constrained

to withhold confidentiality and exercise due diligence while disclosing company information to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCIAL ACCOUNTING

the user to safeguard the interest of the company hence he is only limited by the law to disclose

information to only internal users who in this case is the company.

The regulation bars him from disclosing financial information to external parties

because of fear of the unknown. It does this to prevent the company from potential self-damage

whereby the competitors may get the info and use it to exploit the market. This might also cost

the company on litigation grounds whereby information may link to the persons using the

company hence making the company lose. It is therefore straight that there is the need to regulate

the information disclosed by not only the manager but even other parties who disclose

information to their intended uses.

Conclusion;

It is therefore apparent that financial and accounting information should be regulated to

ensure that only personal, relevant information is reported by the legally allowed parties and of

course, the intended user to avoid blames and mitigate risks that might put the interest of the

company down. This should be done by outlining what material information is to reach the

intended user and who is to disclose the info and finally how is that info going to be revealed.

Professional ethics code of conduct and principles the likes of objectivity, subjection to

materiality, due diligence care, integrity, honesty, professional competency, confidentiality and

self-responsibility is of very importance since this is what is to guide and direct both the users

and the persons disclosing information on how they are to utilize and effect the info without

inflicting any damage to the company. Company interest should always come first while

revealing any information.

(ii)

the user to safeguard the interest of the company hence he is only limited by the law to disclose

information to only internal users who in this case is the company.

The regulation bars him from disclosing financial information to external parties

because of fear of the unknown. It does this to prevent the company from potential self-damage

whereby the competitors may get the info and use it to exploit the market. This might also cost

the company on litigation grounds whereby information may link to the persons using the

company hence making the company lose. It is therefore straight that there is the need to regulate

the information disclosed by not only the manager but even other parties who disclose

information to their intended uses.

Conclusion;

It is therefore apparent that financial and accounting information should be regulated to

ensure that only personal, relevant information is reported by the legally allowed parties and of

course, the intended user to avoid blames and mitigate risks that might put the interest of the

company down. This should be done by outlining what material information is to reach the

intended user and who is to disclose the info and finally how is that info going to be revealed.

Professional ethics code of conduct and principles the likes of objectivity, subjection to

materiality, due diligence care, integrity, honesty, professional competency, confidentiality and

self-responsibility is of very importance since this is what is to guide and direct both the users

and the persons disclosing information on how they are to utilize and effect the info without

inflicting any damage to the company. Company interest should always come first while

revealing any information.

(ii)

CORPORATE FINANCIAL ACCOUNTING

Report on Australian Accounting Standard Board Participation In Global Accounting

Standard Settings And Its Impact On IFRS And Constituent Users Analysis.

Accounting standard setting is a process that indeed involves teamwork since one party

can’t do it alone in any case the parties involved in the background are not the final users of the

standards hence need to engage all concerned parties in context, and that is why AASB is always

dashed in.

Australia is a country which the Internal Accounting Setting Body has never left aside

especially when it comes to matters relating setting accounting international standards. It is

among the G4+1 country together with Canada, US and United Kingdom whose contribution and

research has never been neglected on matters accounting standard. The sole reason why they are

always involved in this setting process and especially Australia is because of their pre-eminent

advanced national standard-setting bodies of competent, sound minded, intellectual personnel

who have expertise in standard settings due to their upgraded forums and workshop meetings

where they exchange ideas as they brainstorm.

Australia influence in standard setting is highly contributed by its corresponding change

in economic scale mainly as a result of high profile body that has high level intellectual

experienced individuals who have mastered in different fields (Arnold, 2009.Pg.805.) AASB is

highly involved in the setting process since they are first consulted for input by International

Accounting Standard Board in return they identify the issue, i.e. AASB and research by

participating individuals and local Australian organization wherein return they get feedback and

call for discussion with IASB. Hence AASB contributes to its study for documentation to a point

whereby they concurrently reveal IASB research (Deegan, 2013.Pg.7.)

Report on Australian Accounting Standard Board Participation In Global Accounting

Standard Settings And Its Impact On IFRS And Constituent Users Analysis.

Accounting standard setting is a process that indeed involves teamwork since one party

can’t do it alone in any case the parties involved in the background are not the final users of the

standards hence need to engage all concerned parties in context, and that is why AASB is always

dashed in.

Australia is a country which the Internal Accounting Setting Body has never left aside

especially when it comes to matters relating setting accounting international standards. It is

among the G4+1 country together with Canada, US and United Kingdom whose contribution and

research has never been neglected on matters accounting standard. The sole reason why they are

always involved in this setting process and especially Australia is because of their pre-eminent

advanced national standard-setting bodies of competent, sound minded, intellectual personnel

who have expertise in standard settings due to their upgraded forums and workshop meetings

where they exchange ideas as they brainstorm.

Australia influence in standard setting is highly contributed by its corresponding change

in economic scale mainly as a result of high profile body that has high level intellectual

experienced individuals who have mastered in different fields (Arnold, 2009.Pg.805.) AASB is

highly involved in the setting process since they are first consulted for input by International

Accounting Standard Board in return they identify the issue, i.e. AASB and research by

participating individuals and local Australian organization wherein return they get feedback and

call for discussion with IASB. Hence AASB contributes to its study for documentation to a point

whereby they concurrently reveal IASB research (Deegan, 2013.Pg.7.)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCIAL ACCOUNTING

After that, the final standard or rather a pronouncement is made by AASB to IASB for

awareness and education enrichment awaiting post-implementation review. Generally AASB

task on accounting standard is accepting the strategic oversight directives then identify the issue

in query, do research and consider the problem of course engaging both IASB and other

Australian local organization as well as specialist, then provide documentation of the findings to

form standard reporting that is made aware to the user as IASB does the final review.AASB is

entirely considered in standard process setting (Durocher, Fortin and Côté, 2007.Pg.33.)

Countries that are members of IASB are seen not to use IFRS mainly because most of

IFRS is the adoption of GAAPS and local known accounting standards hence no need of using

IFRS because you will be having the application of similar regulation than the one you have

since this is an upgrade of GAAPS that was found earlier than IFRS. Likewise let it be known

that it is so expensive to shift from GAAPS or any other standard to IFRS especially on training

cost, system installation and maintenance cost. The other primary reason why it is not used is

that it is based on principle and not rules hence a loophole for controls and efficiency (Ahmed,

Neel and Wang, 2013.Pg. 1350.)

IFRS are somehow viewed by these countries that do not need them too far below the

level of the current present used standards hence find no reason of shifting. It is therefore clear

that member states of IASB do not trust and are not contempt with what IFRS offer considers

hence no reason for adopting it (Soderstrom and Sun,2007.Pg.700.) It does not mean that it is by

default that IFRS’s are adopted no, it is because does not meet the need of the users hence if it is

upgraded these people with other standards would opt to choose it. It is similarly expected if

there were any other regulations whose rules supersedes that of GAAPS.

After that, the final standard or rather a pronouncement is made by AASB to IASB for

awareness and education enrichment awaiting post-implementation review. Generally AASB

task on accounting standard is accepting the strategic oversight directives then identify the issue

in query, do research and consider the problem of course engaging both IASB and other

Australian local organization as well as specialist, then provide documentation of the findings to

form standard reporting that is made aware to the user as IASB does the final review.AASB is

entirely considered in standard process setting (Durocher, Fortin and Côté, 2007.Pg.33.)

Countries that are members of IASB are seen not to use IFRS mainly because most of

IFRS is the adoption of GAAPS and local known accounting standards hence no need of using

IFRS because you will be having the application of similar regulation than the one you have

since this is an upgrade of GAAPS that was found earlier than IFRS. Likewise let it be known

that it is so expensive to shift from GAAPS or any other standard to IFRS especially on training

cost, system installation and maintenance cost. The other primary reason why it is not used is

that it is based on principle and not rules hence a loophole for controls and efficiency (Ahmed,

Neel and Wang, 2013.Pg. 1350.)

IFRS are somehow viewed by these countries that do not need them too far below the

level of the current present used standards hence find no reason of shifting. It is therefore clear

that member states of IASB do not trust and are not contempt with what IFRS offer considers

hence no reason for adopting it (Soderstrom and Sun,2007.Pg.700.) It does not mean that it is by

default that IFRS’s are adopted no, it is because does not meet the need of the users hence if it is

upgraded these people with other standards would opt to choose it. It is similarly expected if

there were any other regulations whose rules supersedes that of GAAPS.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCIAL ACCOUNTING

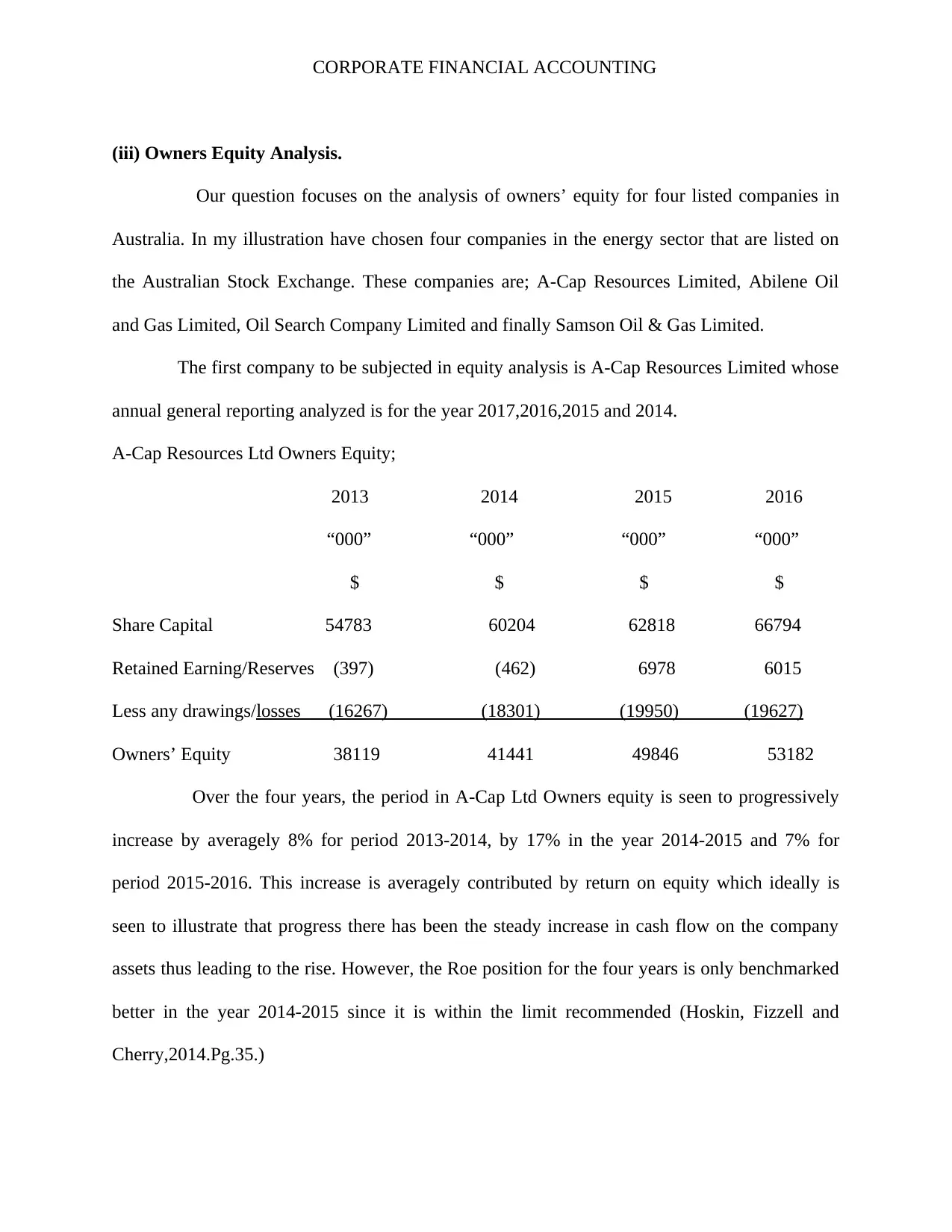

(iii) Owners Equity Analysis.

Our question focuses on the analysis of owners’ equity for four listed companies in

Australia. In my illustration have chosen four companies in the energy sector that are listed on

the Australian Stock Exchange. These companies are; A-Cap Resources Limited, Abilene Oil

and Gas Limited, Oil Search Company Limited and finally Samson Oil & Gas Limited.

The first company to be subjected in equity analysis is A-Cap Resources Limited whose

annual general reporting analyzed is for the year 2017,2016,2015 and 2014.

A-Cap Resources Ltd Owners Equity;

2013 2014 2015 2016

“000” “000” “000” “000”

$ $ $ $

Share Capital 54783 60204 62818 66794

Retained Earning/Reserves (397) (462) 6978 6015

Less any drawings/losses (16267) (18301) (19950) (19627)

Owners’ Equity 38119 41441 49846 53182

Over the four years, the period in A-Cap Ltd Owners equity is seen to progressively

increase by averagely 8% for period 2013-2014, by 17% in the year 2014-2015 and 7% for

period 2015-2016. This increase is averagely contributed by return on equity which ideally is

seen to illustrate that progress there has been the steady increase in cash flow on the company

assets thus leading to the rise. However, the Roe position for the four years is only benchmarked

better in the year 2014-2015 since it is within the limit recommended (Hoskin, Fizzell and

Cherry,2014.Pg.35.)

(iii) Owners Equity Analysis.

Our question focuses on the analysis of owners’ equity for four listed companies in

Australia. In my illustration have chosen four companies in the energy sector that are listed on

the Australian Stock Exchange. These companies are; A-Cap Resources Limited, Abilene Oil

and Gas Limited, Oil Search Company Limited and finally Samson Oil & Gas Limited.

The first company to be subjected in equity analysis is A-Cap Resources Limited whose

annual general reporting analyzed is for the year 2017,2016,2015 and 2014.

A-Cap Resources Ltd Owners Equity;

2013 2014 2015 2016

“000” “000” “000” “000”

$ $ $ $

Share Capital 54783 60204 62818 66794

Retained Earning/Reserves (397) (462) 6978 6015

Less any drawings/losses (16267) (18301) (19950) (19627)

Owners’ Equity 38119 41441 49846 53182

Over the four years, the period in A-Cap Ltd Owners equity is seen to progressively

increase by averagely 8% for period 2013-2014, by 17% in the year 2014-2015 and 7% for

period 2015-2016. This increase is averagely contributed by return on equity which ideally is

seen to illustrate that progress there has been the steady increase in cash flow on the company

assets thus leading to the rise. However, the Roe position for the four years is only benchmarked

better in the year 2014-2015 since it is within the limit recommended (Hoskin, Fizzell and

Cherry,2014.Pg.35.)

CORPORATE FINANCIAL ACCOUNTING

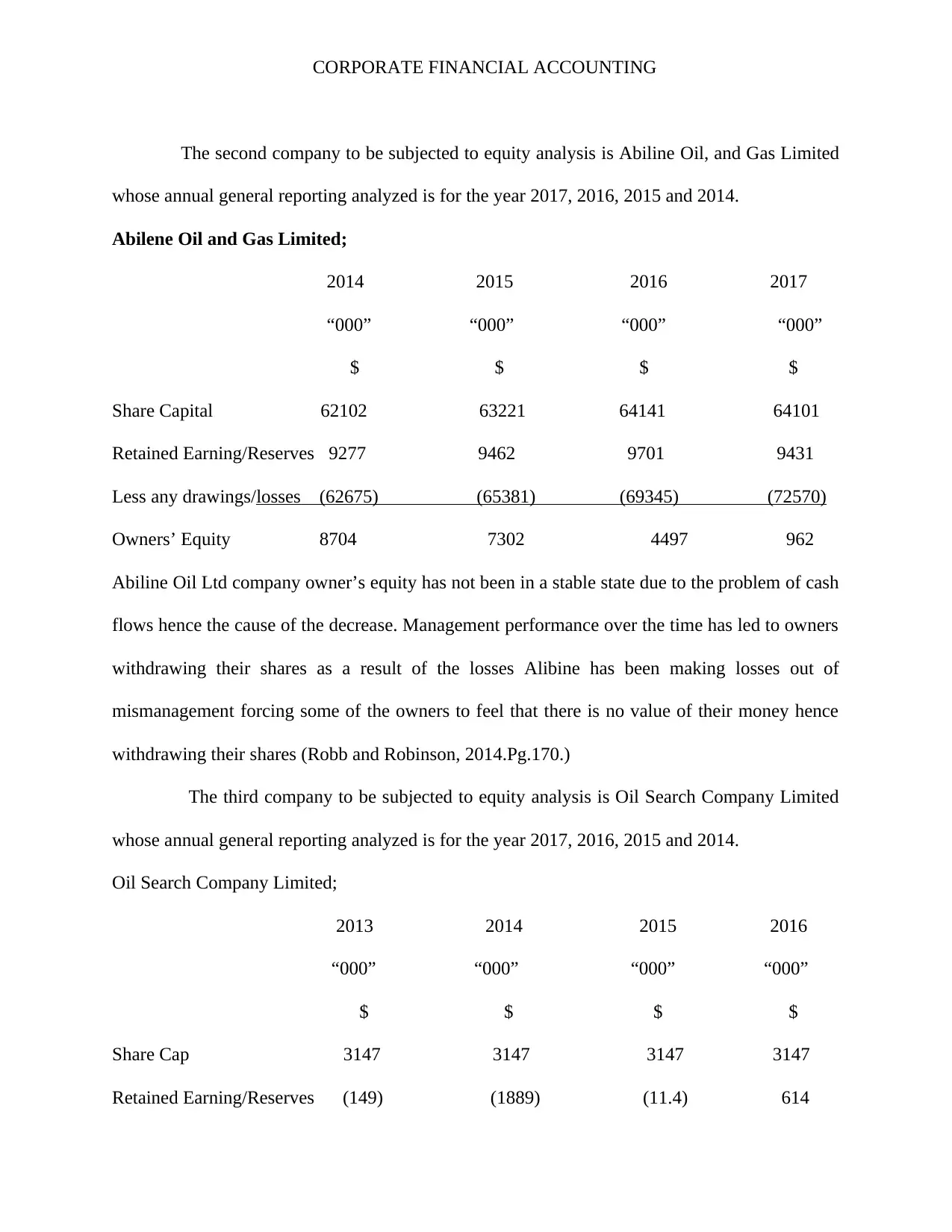

The second company to be subjected to equity analysis is Abiline Oil, and Gas Limited

whose annual general reporting analyzed is for the year 2017, 2016, 2015 and 2014.

Abilene Oil and Gas Limited;

2014 2015 2016 2017

“000” “000” “000” “000”

$ $ $ $

Share Capital 62102 63221 64141 64101

Retained Earning/Reserves 9277 9462 9701 9431

Less any drawings/losses (62675) (65381) (69345) (72570)

Owners’ Equity 8704 7302 4497 962

Abiline Oil Ltd company owner’s equity has not been in a stable state due to the problem of cash

flows hence the cause of the decrease. Management performance over the time has led to owners

withdrawing their shares as a result of the losses Alibine has been making losses out of

mismanagement forcing some of the owners to feel that there is no value of their money hence

withdrawing their shares (Robb and Robinson, 2014.Pg.170.)

The third company to be subjected to equity analysis is Oil Search Company Limited

whose annual general reporting analyzed is for the year 2017, 2016, 2015 and 2014.

Oil Search Company Limited;

2013 2014 2015 2016

“000” “000” “000” “000”

$ $ $ $

Share Cap 3147 3147 3147 3147

Retained Earning/Reserves (149) (1889) (11.4) 614

The second company to be subjected to equity analysis is Abiline Oil, and Gas Limited

whose annual general reporting analyzed is for the year 2017, 2016, 2015 and 2014.

Abilene Oil and Gas Limited;

2014 2015 2016 2017

“000” “000” “000” “000”

$ $ $ $

Share Capital 62102 63221 64141 64101

Retained Earning/Reserves 9277 9462 9701 9431

Less any drawings/losses (62675) (65381) (69345) (72570)

Owners’ Equity 8704 7302 4497 962

Abiline Oil Ltd company owner’s equity has not been in a stable state due to the problem of cash

flows hence the cause of the decrease. Management performance over the time has led to owners

withdrawing their shares as a result of the losses Alibine has been making losses out of

mismanagement forcing some of the owners to feel that there is no value of their money hence

withdrawing their shares (Robb and Robinson, 2014.Pg.170.)

The third company to be subjected to equity analysis is Oil Search Company Limited

whose annual general reporting analyzed is for the year 2017, 2016, 2015 and 2014.

Oil Search Company Limited;

2013 2014 2015 2016

“000” “000” “000” “000”

$ $ $ $

Share Cap 3147 3147 3147 3147

Retained Earning/Reserves (149) (1889) (11.4) 614

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCIAL ACCOUNTING

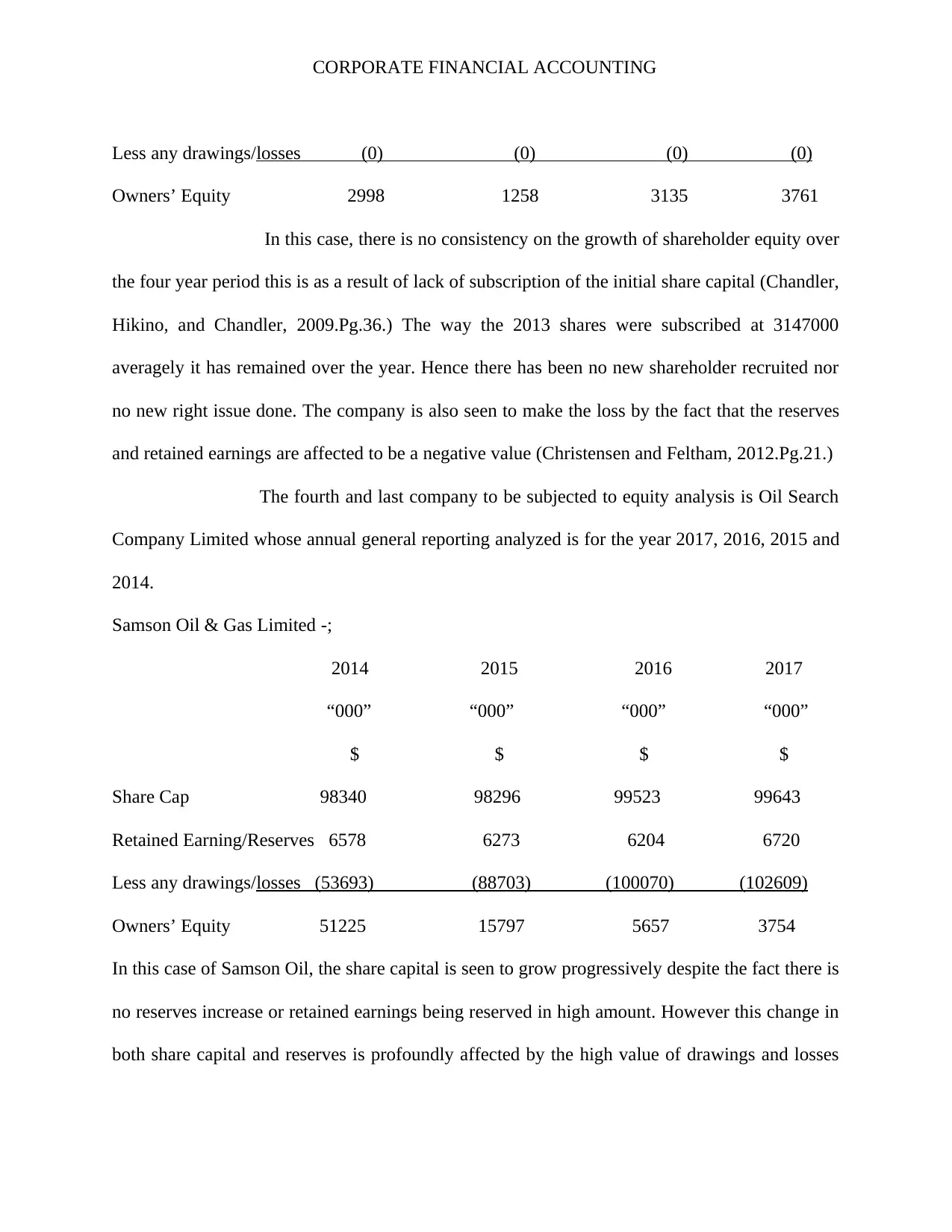

Less any drawings/losses (0) (0) (0) (0)

Owners’ Equity 2998 1258 3135 3761

In this case, there is no consistency on the growth of shareholder equity over

the four year period this is as a result of lack of subscription of the initial share capital (Chandler,

Hikino, and Chandler, 2009.Pg.36.) The way the 2013 shares were subscribed at 3147000

averagely it has remained over the year. Hence there has been no new shareholder recruited nor

no new right issue done. The company is also seen to make the loss by the fact that the reserves

and retained earnings are affected to be a negative value (Christensen and Feltham, 2012.Pg.21.)

The fourth and last company to be subjected to equity analysis is Oil Search

Company Limited whose annual general reporting analyzed is for the year 2017, 2016, 2015 and

2014.

Samson Oil & Gas Limited -;

2014 2015 2016 2017

“000” “000” “000” “000”

$ $ $ $

Share Cap 98340 98296 99523 99643

Retained Earning/Reserves 6578 6273 6204 6720

Less any drawings/losses (53693) (88703) (100070) (102609)

Owners’ Equity 51225 15797 5657 3754

In this case of Samson Oil, the share capital is seen to grow progressively despite the fact there is

no reserves increase or retained earnings being reserved in high amount. However this change in

both share capital and reserves is profoundly affected by the high value of drawings and losses

Less any drawings/losses (0) (0) (0) (0)

Owners’ Equity 2998 1258 3135 3761

In this case, there is no consistency on the growth of shareholder equity over

the four year period this is as a result of lack of subscription of the initial share capital (Chandler,

Hikino, and Chandler, 2009.Pg.36.) The way the 2013 shares were subscribed at 3147000

averagely it has remained over the year. Hence there has been no new shareholder recruited nor

no new right issue done. The company is also seen to make the loss by the fact that the reserves

and retained earnings are affected to be a negative value (Christensen and Feltham, 2012.Pg.21.)

The fourth and last company to be subjected to equity analysis is Oil Search

Company Limited whose annual general reporting analyzed is for the year 2017, 2016, 2015 and

2014.

Samson Oil & Gas Limited -;

2014 2015 2016 2017

“000” “000” “000” “000”

$ $ $ $

Share Cap 98340 98296 99523 99643

Retained Earning/Reserves 6578 6273 6204 6720

Less any drawings/losses (53693) (88703) (100070) (102609)

Owners’ Equity 51225 15797 5657 3754

In this case of Samson Oil, the share capital is seen to grow progressively despite the fact there is

no reserves increase or retained earnings being reserved in high amount. However this change in

both share capital and reserves is profoundly affected by the high value of drawings and losses

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCIAL ACCOUNTING

done with its climax being the year 2016 and 2017 thus reducing the owner's equity drastically

(Dyrda and Pugsley, 2018. Pg.13.)

done with its climax being the year 2016 and 2017 thus reducing the owner's equity drastically

(Dyrda and Pugsley, 2018. Pg.13.)

CORPORATE FINANCIAL ACCOUNTING

References;

Ahmed, A.S., Neel, M. and Wang, D., 2013. Does mandatory adoption of IFRS improve

accounting quality? Preliminary evidence. Contemporary Accounting Research, 30(4), pp.1344-

1372.

Arnold, P.J., 2009. Global financial crisis: The challenge to accounting research. Accounting,

organizations and society,34(6-7), pp.803-809

Bamber, L.S., Jiang, J. and Wang, I.Y., 2010. What’s my style? The influence of top managers

on voluntary corporate financial disclosure. The accounting review, 85(4), pp.1131-1162.

Chan, M.C. and Watson, J., 2011. Voluntary disclosure of segment information in a regulated

environment: Australian evidence. Eurasian Business Review, 1(1), pp.37-53.

Chandler, A.D., Hikino, T. and Chandler, A.D., 2009. Scale and scope: The dynamics of

industrial capitalism. Harvard University Press.

Christensen, P.O. and Feltham, G., 2012. Economics of Accounting: Information in

markets (Vol. 1). Springer.

Deegan, C., 2013. Financial accounting theory. McGraw-Hill Education Australia.

Durocher, S., Fortin, A. and Côté, L., 2007. Users’ participation in the accounting standard-

setting process: A theory-building study. Accounting, Organizations and Society,32(1-2), pp.29-

59.

Dyrda, S. and Pugsley, B.W., 2018. Taxes, private equity and evolution of income inequality in

the us. Working paper.

Hoskin, R.E., Fizzell, M.R. and Cherry, D.C., 2014. Financial Accounting: a user perspective.

Wiley Global Education.

References;

Ahmed, A.S., Neel, M. and Wang, D., 2013. Does mandatory adoption of IFRS improve

accounting quality? Preliminary evidence. Contemporary Accounting Research, 30(4), pp.1344-

1372.

Arnold, P.J., 2009. Global financial crisis: The challenge to accounting research. Accounting,

organizations and society,34(6-7), pp.803-809

Bamber, L.S., Jiang, J. and Wang, I.Y., 2010. What’s my style? The influence of top managers

on voluntary corporate financial disclosure. The accounting review, 85(4), pp.1131-1162.

Chan, M.C. and Watson, J., 2011. Voluntary disclosure of segment information in a regulated

environment: Australian evidence. Eurasian Business Review, 1(1), pp.37-53.

Chandler, A.D., Hikino, T. and Chandler, A.D., 2009. Scale and scope: The dynamics of

industrial capitalism. Harvard University Press.

Christensen, P.O. and Feltham, G., 2012. Economics of Accounting: Information in

markets (Vol. 1). Springer.

Deegan, C., 2013. Financial accounting theory. McGraw-Hill Education Australia.

Durocher, S., Fortin, A. and Côté, L., 2007. Users’ participation in the accounting standard-

setting process: A theory-building study. Accounting, Organizations and Society,32(1-2), pp.29-

59.

Dyrda, S. and Pugsley, B.W., 2018. Taxes, private equity and evolution of income inequality in

the us. Working paper.

Hoskin, R.E., Fizzell, M.R. and Cherry, D.C., 2014. Financial Accounting: a user perspective.

Wiley Global Education.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.