Corporate Accounting Analysis Report: AASB and IFRS Framework

VerifiedAdded on 2023/06/05

|15

|2983

|73

Report

AI Summary

This report provides an executive summary of corporate accounting, focusing on the importance of transparent and reliable financial statements. It references the Australian Accounting Standards Board (AASB) and International Financial Reporting Standards (IFRS), emphasizing the need for detailed corporate disclosures to satisfy stakeholders. The report covers corporate regulations, accounting standard setting, and owner's equity, including contributed equity, reserves, and retained earnings. It analyzes financial data from four public companies: BHP Billiton, Orica Limited, Rio Tinto, and Fortescue, examining their equity and debt instruments. The analysis highlights trends in stockholders' equity, retained earnings, and other financial metrics, offering insights into each company's financial performance and position. The report concludes by emphasizing the significance of financial regulation, transparency, and the adoption of IFRS for global consistency in accounting practices. It also discusses the impact of accounting standards setting on the financial environment.

CORPORATE ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

In today's generation, it has been noticed that organizations have emphasized a lot more on the

quality and quantity of financial statements by using better systems and incorporating more

detailed corporate disclosures so as to provide transparency and reliability to its intended users or

stakeholders. When it comes to investors, the organizations shouldn't take the risk of not

disclosing something as investors expect detailed financial reports so that their analysis could be

based on the best available information. Such reports should also been able to be regulated

within the managerial framework of an entity. The following report has references to Australian

Accounting Standards Board (AASB) and International Financial Reporting Standards (IFRS).

The following report has been prepared along with an analysis of four public companies where

the analysis includes equity and debt instruments.

In today's generation, it has been noticed that organizations have emphasized a lot more on the

quality and quantity of financial statements by using better systems and incorporating more

detailed corporate disclosures so as to provide transparency and reliability to its intended users or

stakeholders. When it comes to investors, the organizations shouldn't take the risk of not

disclosing something as investors expect detailed financial reports so that their analysis could be

based on the best available information. Such reports should also been able to be regulated

within the managerial framework of an entity. The following report has references to Australian

Accounting Standards Board (AASB) and International Financial Reporting Standards (IFRS).

The following report has been prepared along with an analysis of four public companies where

the analysis includes equity and debt instruments.

Contents

CORPORATE REGULATIONS.....................................................................................................3

ACCOUNTING STANDARD SETTING......................................................................................5

OWNER'S EQUITY........................................................................................................................7

Bibliography..................................................................................................................................13

CORPORATE REGULATIONS.....................................................................................................3

ACCOUNTING STANDARD SETTING......................................................................................5

OWNER'S EQUITY........................................................................................................................7

Bibliography..................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE REGULATIONS

An organization's financial statements are analyzed in different ways by different users because

the requirement of information varies from user to user. On the other hand, organizations carry

an objective of keeping their users satisfied with their reporting styles. Therefore, they try to

disclose every possible information including terms and conditions so that users can extract their

required information and use it for making best decisions.

The today's observations show us that the disclosures requirement isn’t sufficient enough to

satisfy the needs of the intended users. The corporate environment is separated into two groups

of users where one set of users are satisfied with the sufficiency of information provided while

the other set of users aren't satisfied and are looking for more information to analyze the reports

in a better way. Hence, it has become important to carry out a regulation of such financial reports

so that whether the entity has made sufficient corporate disclosures or not can be regulated. The

preparation and presentation of such reports along with corporate disclosures are important as it

reflects an organization's image in terms of its financial performance and position (Alvarez,

2013).

All the companies working within the same industry should adopt similar practices and policies

to represent corporate disclosures so as to maintain a consistency among them and have a

common approach towards the reporting requirements (Easton, 2010). However, it is important

for the management to judge the materiality of an information because immaterial information, if

disclosed, can cause damage to the organization as a user may not have the same perception as

the company might be having towards it. An auditor's duty also plays an important role as they

can advice the management regarding disclosures that should be made and disclosures that are

irrelevant. For such requirements, the standard board defines an accounting framework within

which an organization should work as the framework guides the managers regarding corporate

disclosures requirements. Such use of financial regulation helps the intended users to have a

comparative analysis of different companies, whether in the same industry or different industries.

The another important thing an organization should consider is its 'control' and it should keep on

regulating that because stronger the control is, the more reliable the internal sources are and the

better is the quality of the disclosures. The manager should understand that the disclosures of

An organization's financial statements are analyzed in different ways by different users because

the requirement of information varies from user to user. On the other hand, organizations carry

an objective of keeping their users satisfied with their reporting styles. Therefore, they try to

disclose every possible information including terms and conditions so that users can extract their

required information and use it for making best decisions.

The today's observations show us that the disclosures requirement isn’t sufficient enough to

satisfy the needs of the intended users. The corporate environment is separated into two groups

of users where one set of users are satisfied with the sufficiency of information provided while

the other set of users aren't satisfied and are looking for more information to analyze the reports

in a better way. Hence, it has become important to carry out a regulation of such financial reports

so that whether the entity has made sufficient corporate disclosures or not can be regulated. The

preparation and presentation of such reports along with corporate disclosures are important as it

reflects an organization's image in terms of its financial performance and position (Alvarez,

2013).

All the companies working within the same industry should adopt similar practices and policies

to represent corporate disclosures so as to maintain a consistency among them and have a

common approach towards the reporting requirements (Easton, 2010). However, it is important

for the management to judge the materiality of an information because immaterial information, if

disclosed, can cause damage to the organization as a user may not have the same perception as

the company might be having towards it. An auditor's duty also plays an important role as they

can advice the management regarding disclosures that should be made and disclosures that are

irrelevant. For such requirements, the standard board defines an accounting framework within

which an organization should work as the framework guides the managers regarding corporate

disclosures requirements. Such use of financial regulation helps the intended users to have a

comparative analysis of different companies, whether in the same industry or different industries.

The another important thing an organization should consider is its 'control' and it should keep on

regulating that because stronger the control is, the more reliable the internal sources are and the

better is the quality of the disclosures. The manager should understand that the disclosures of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

information shouldn't be made voluntarily but as per the required requirements. The main

objective behind such detailed disclosures is delivering the best possible transparency of such

reports. Hence, we can conclude that the reporting of financial information is idealistic in nature

and the organizations should maintain a control on the disclosures of information. Transparency

doesn't mean disclosing every information and making the reports voluminous in nature. It

means disclosing all the relevant and significant information that discloses the true and fair view

of an entity. Where the management provides information that make their reports look

voluminous, they somewhere divert from their main objective of delivering qualitative reports an

in that case, the organization is suppose to carry out an insensible act.

objective behind such detailed disclosures is delivering the best possible transparency of such

reports. Hence, we can conclude that the reporting of financial information is idealistic in nature

and the organizations should maintain a control on the disclosures of information. Transparency

doesn't mean disclosing every information and making the reports voluminous in nature. It

means disclosing all the relevant and significant information that discloses the true and fair view

of an entity. Where the management provides information that make their reports look

voluminous, they somewhere divert from their main objective of delivering qualitative reports an

in that case, the organization is suppose to carry out an insensible act.

ACCOUNTING STANDARD SETTING

IFRS is a defined framework for preparation and presentation of financial statements having

relevance globally and guides an organization for the collection and presentation of data as per

the regulations prescribed by International Accounting Standards Board (IASB). It is a broader

concept, as observed by AASB and FRC, which is based on strategic implementation, helps

entities to report as per Corporations Act, 2001 and other relevant acts. The adoption of such

reporting methods helps entities to ensure that they are working within the guidelines set by the

AASB framework. The AASB is said to follow a policy of neutrality because what's important is

recording and reporting of every event or transaction, irrespective the entity is a profit making

entity or not for profit making entity.

The AASB is said to have adopted various standards, which are classified as Australian

Accounting Standards now, in order to align with the guidelines and policies set up by the

Financial Reporting Council (FRC). It is important tod discover whether all the organizations

within an industry in Australia are aligning with IFRS system as issued by IASB so as to

maintain a consistency among various financial reports and also, with consistency, the financial

results can be measured & compared reliably. IFRS system is a strong global movement and the

accounting & auditing industry will totally depend on such system having an impact on the

international market.

However, adoption or implementation of IFRS norms haven't been made compulsory yet for all

the entities because IFRS recommends huge changes and for an entity, it is not possible to totally

change its reporting style in one go. Having changes incorporated in the financial sector of the

market is not an easy task because incorporation doesn't need only making changes but also

includes hiring of experts, installation of better IT systems and most importantly, time.

Considering such relevant reasons, the board hasn't make IFRS norms compulsory for all

countries in one go. However, earlier or later, the board has an aim of bringing IFRS standards

into effect globally so as to have a global consistency all over the world. However, we should

consider that pros of such a system when adopted by the accounting sector, that is, it will boost

the economic environment of a country and will provide useful benefits to an organization such

as transparency, better compliances, a good reputation in terms of both national and international

IFRS is a defined framework for preparation and presentation of financial statements having

relevance globally and guides an organization for the collection and presentation of data as per

the regulations prescribed by International Accounting Standards Board (IASB). It is a broader

concept, as observed by AASB and FRC, which is based on strategic implementation, helps

entities to report as per Corporations Act, 2001 and other relevant acts. The adoption of such

reporting methods helps entities to ensure that they are working within the guidelines set by the

AASB framework. The AASB is said to follow a policy of neutrality because what's important is

recording and reporting of every event or transaction, irrespective the entity is a profit making

entity or not for profit making entity.

The AASB is said to have adopted various standards, which are classified as Australian

Accounting Standards now, in order to align with the guidelines and policies set up by the

Financial Reporting Council (FRC). It is important tod discover whether all the organizations

within an industry in Australia are aligning with IFRS system as issued by IASB so as to

maintain a consistency among various financial reports and also, with consistency, the financial

results can be measured & compared reliably. IFRS system is a strong global movement and the

accounting & auditing industry will totally depend on such system having an impact on the

international market.

However, adoption or implementation of IFRS norms haven't been made compulsory yet for all

the entities because IFRS recommends huge changes and for an entity, it is not possible to totally

change its reporting style in one go. Having changes incorporated in the financial sector of the

market is not an easy task because incorporation doesn't need only making changes but also

includes hiring of experts, installation of better IT systems and most importantly, time.

Considering such relevant reasons, the board hasn't make IFRS norms compulsory for all

countries in one go. However, earlier or later, the board has an aim of bringing IFRS standards

into effect globally so as to have a global consistency all over the world. However, we should

consider that pros of such a system when adopted by the accounting sector, that is, it will boost

the economic environment of a country and will provide useful benefits to an organization such

as transparency, better compliances, a good reputation in terms of both national and international

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

status, etc. The countries currently working with the framework defined by General Accepted

Accounting Principles (GAAP) should try getting into the IFRS framework so that the aim of

having uniform principles globally can be achieved and problems regarding convergence cannot

be a problem in the future (Elaine, 2015).

Accounting Principles (GAAP) should try getting into the IFRS framework so that the aim of

having uniform principles globally can be achieved and problems regarding convergence cannot

be a problem in the future (Elaine, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

OWNER'S EQUITY

ITEMS OF EQUITY

The baisc components that together forms equity are :

Equity contributed

Reserves

Retained Earnings

Contributed Equity : As the name suggests, the equity comprises of funds contributed by the

shareholders or investors also known as shareholder's funds. Such shareholders gets shares of the

company in return. This equity also represents the capital of shares owned by the entity itself.

Such equity contributors or shareholders are considered as the owner of the company as there is

no policy of getting dividends or returns or in fact, getting back their money in case of

liquidation (Fridson & Alvarez, 2012). That is why, where an investor is ready to bear so much

of risk, that are given a status of company’s owner to the extent of investment made by them.

The company may issue new shares in the market that increases its equity capital. It may also opt

issuing bonus shares to the shareholders existing at the date of issue after fulfilling of various

other conditions (Taillard, 2013).

Reserves : Various types of reserves are there created according to the needs of an organization

such as hedging reserves, remuneration reserves, general reserves, debenture redemption

reserves, statutory reserves, reserves created due to translation of foreign currencies, etc (Girard,

2014). Hedging reserve is a reserve for protection against the future losses that may be incurred

on the derivative instruments. The remuneration reserve is made so set aside certain amount so as

to make immediate payments of remuneration when calculated appropriately and accurately. The

main reason of not having an accurate calculation of remuneration is the continuous increment or

decrement in the remuneration that changes over the period of time (Skonieczny, 2012).

Similarly, asset revaluation reserve is also prepared by some organizations in order to

compensate for losses that might arise due to revaluations or depreciation or fluctuation in prices

due to fair value measurement or losses due to adverse environmental conditions. General

reserve isn't prepared for any particular reason but in general to save the organization from

ITEMS OF EQUITY

The baisc components that together forms equity are :

Equity contributed

Reserves

Retained Earnings

Contributed Equity : As the name suggests, the equity comprises of funds contributed by the

shareholders or investors also known as shareholder's funds. Such shareholders gets shares of the

company in return. This equity also represents the capital of shares owned by the entity itself.

Such equity contributors or shareholders are considered as the owner of the company as there is

no policy of getting dividends or returns or in fact, getting back their money in case of

liquidation (Fridson & Alvarez, 2012). That is why, where an investor is ready to bear so much

of risk, that are given a status of company’s owner to the extent of investment made by them.

The company may issue new shares in the market that increases its equity capital. It may also opt

issuing bonus shares to the shareholders existing at the date of issue after fulfilling of various

other conditions (Taillard, 2013).

Reserves : Various types of reserves are there created according to the needs of an organization

such as hedging reserves, remuneration reserves, general reserves, debenture redemption

reserves, statutory reserves, reserves created due to translation of foreign currencies, etc (Girard,

2014). Hedging reserve is a reserve for protection against the future losses that may be incurred

on the derivative instruments. The remuneration reserve is made so set aside certain amount so as

to make immediate payments of remuneration when calculated appropriately and accurately. The

main reason of not having an accurate calculation of remuneration is the continuous increment or

decrement in the remuneration that changes over the period of time (Skonieczny, 2012).

Similarly, asset revaluation reserve is also prepared by some organizations in order to

compensate for losses that might arise due to revaluations or depreciation or fluctuation in prices

due to fair value measurement or losses due to adverse environmental conditions. General

reserve isn't prepared for any particular reason but in general to save the organization from

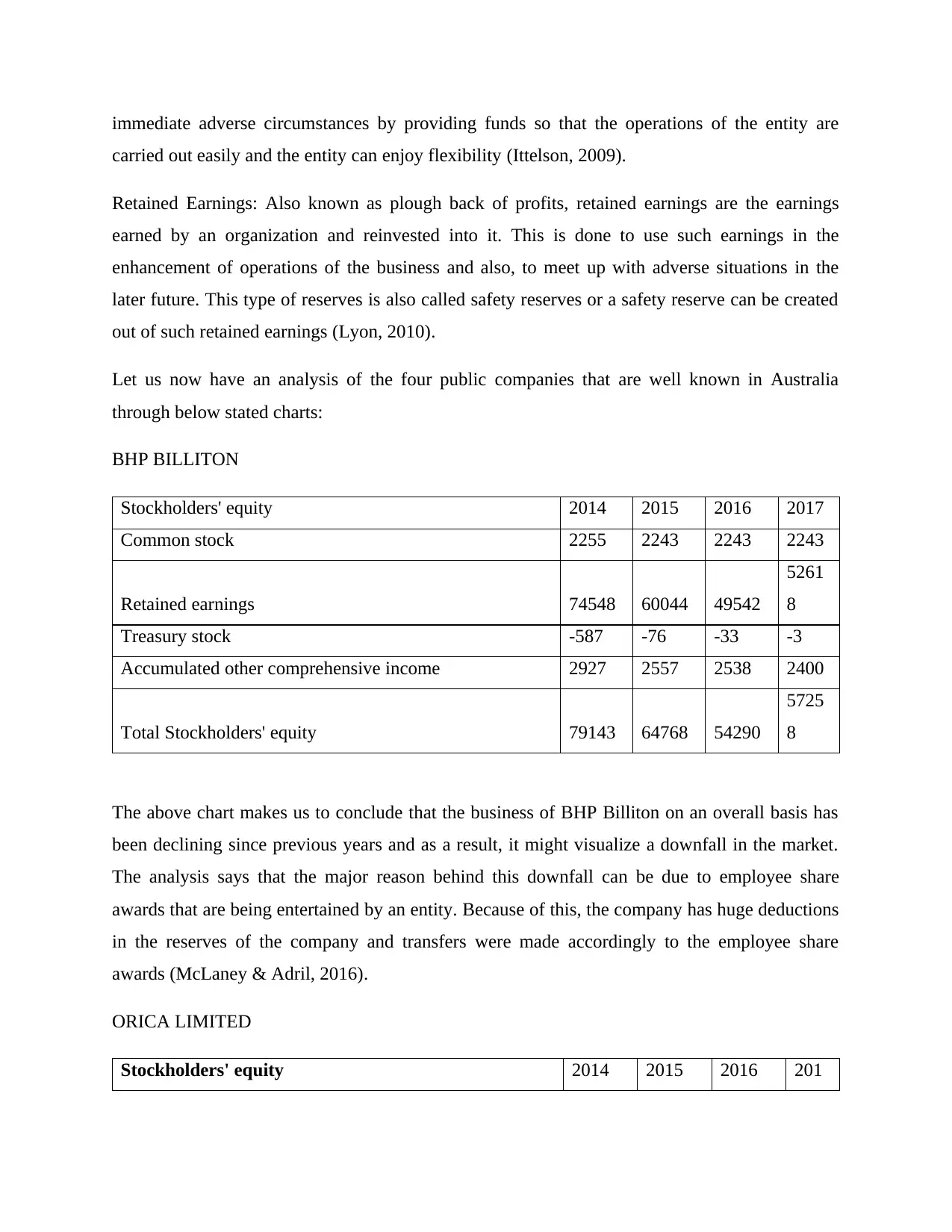

immediate adverse circumstances by providing funds so that the operations of the entity are

carried out easily and the entity can enjoy flexibility (Ittelson, 2009).

Retained Earnings: Also known as plough back of profits, retained earnings are the earnings

earned by an organization and reinvested into it. This is done to use such earnings in the

enhancement of operations of the business and also, to meet up with adverse situations in the

later future. This type of reserves is also called safety reserves or a safety reserve can be created

out of such retained earnings (Lyon, 2010).

Let us now have an analysis of the four public companies that are well known in Australia

through below stated charts:

BHP BILLITON

Stockholders' equity 2014 2015 2016 2017

Common stock 2255 2243 2243 2243

Retained earnings 74548 60044 49542

5261

8

Treasury stock -587 -76 -33 -3

Accumulated other comprehensive income 2927 2557 2538 2400

Total Stockholders' equity 79143 64768 54290

5725

8

The above chart makes us to conclude that the business of BHP Billiton on an overall basis has

been declining since previous years and as a result, it might visualize a downfall in the market.

The analysis says that the major reason behind this downfall can be due to employee share

awards that are being entertained by an entity. Because of this, the company has huge deductions

in the reserves of the company and transfers were made accordingly to the employee share

awards (McLaney & Adril, 2016).

ORICA LIMITED

Stockholders' equity 2014 2015 2016 201

carried out easily and the entity can enjoy flexibility (Ittelson, 2009).

Retained Earnings: Also known as plough back of profits, retained earnings are the earnings

earned by an organization and reinvested into it. This is done to use such earnings in the

enhancement of operations of the business and also, to meet up with adverse situations in the

later future. This type of reserves is also called safety reserves or a safety reserve can be created

out of such retained earnings (Lyon, 2010).

Let us now have an analysis of the four public companies that are well known in Australia

through below stated charts:

BHP BILLITON

Stockholders' equity 2014 2015 2016 2017

Common stock 2255 2243 2243 2243

Retained earnings 74548 60044 49542

5261

8

Treasury stock -587 -76 -33 -3

Accumulated other comprehensive income 2927 2557 2538 2400

Total Stockholders' equity 79143 64768 54290

5725

8

The above chart makes us to conclude that the business of BHP Billiton on an overall basis has

been declining since previous years and as a result, it might visualize a downfall in the market.

The analysis says that the major reason behind this downfall can be due to employee share

awards that are being entertained by an entity. Because of this, the company has huge deductions

in the reserves of the company and transfers were made accordingly to the employee share

awards (McLaney & Adril, 2016).

ORICA LIMITED

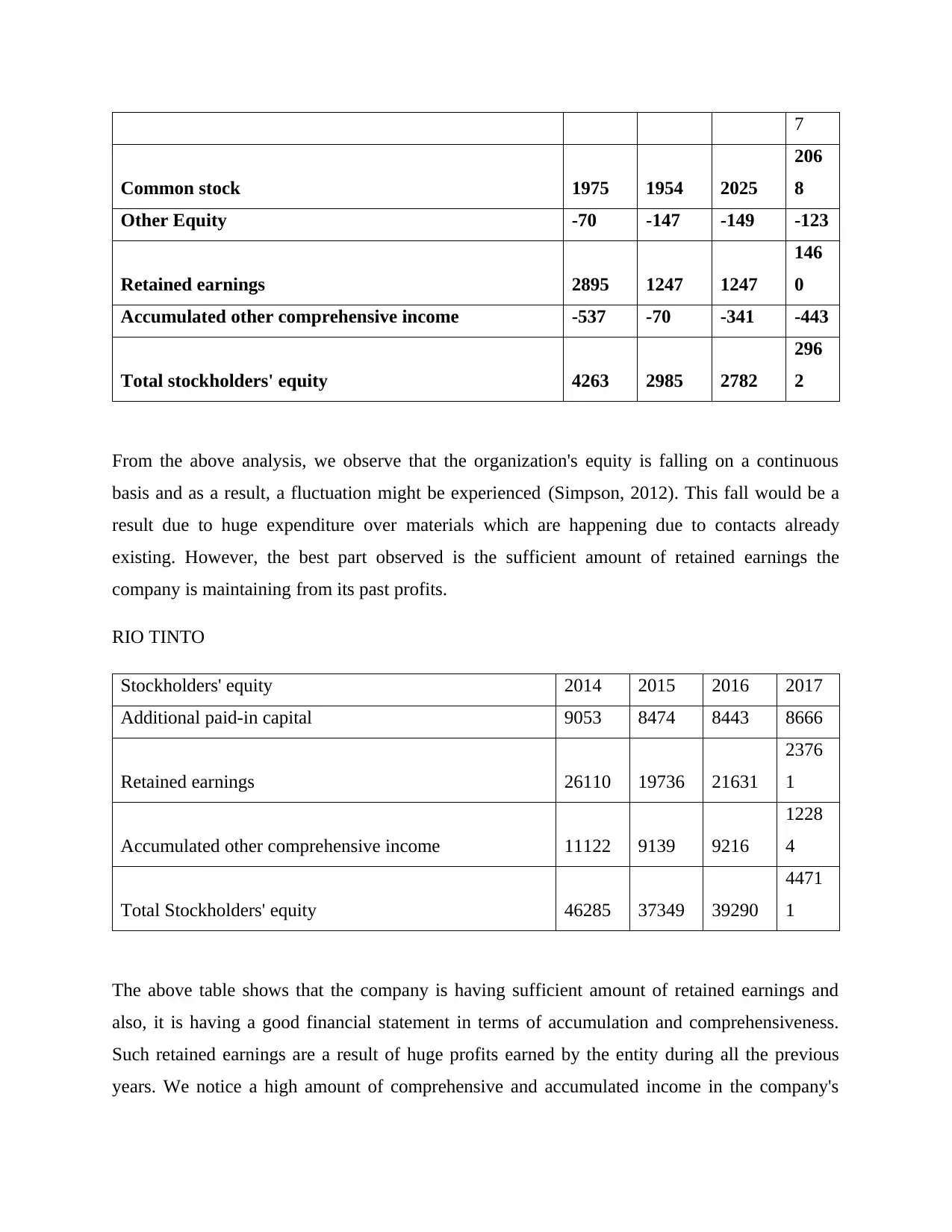

Stockholders' equity 2014 2015 2016 201

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Common stock 1975 1954 2025

206

8

Other Equity -70 -147 -149 -123

Retained earnings 2895 1247 1247

146

0

Accumulated other comprehensive income -537 -70 -341 -443

Total stockholders' equity 4263 2985 2782

296

2

From the above analysis, we observe that the organization's equity is falling on a continuous

basis and as a result, a fluctuation might be experienced (Simpson, 2012). This fall would be a

result due to huge expenditure over materials which are happening due to contacts already

existing. However, the best part observed is the sufficient amount of retained earnings the

company is maintaining from its past profits.

RIO TINTO

Stockholders' equity 2014 2015 2016 2017

Additional paid-in capital 9053 8474 8443 8666

Retained earnings 26110 19736 21631

2376

1

Accumulated other comprehensive income 11122 9139 9216

1228

4

Total Stockholders' equity 46285 37349 39290

4471

1

The above table shows that the company is having sufficient amount of retained earnings and

also, it is having a good financial statement in terms of accumulation and comprehensiveness.

Such retained earnings are a result of huge profits earned by the entity during all the previous

years. We notice a high amount of comprehensive and accumulated income in the company's

Common stock 1975 1954 2025

206

8

Other Equity -70 -147 -149 -123

Retained earnings 2895 1247 1247

146

0

Accumulated other comprehensive income -537 -70 -341 -443

Total stockholders' equity 4263 2985 2782

296

2

From the above analysis, we observe that the organization's equity is falling on a continuous

basis and as a result, a fluctuation might be experienced (Simpson, 2012). This fall would be a

result due to huge expenditure over materials which are happening due to contacts already

existing. However, the best part observed is the sufficient amount of retained earnings the

company is maintaining from its past profits.

RIO TINTO

Stockholders' equity 2014 2015 2016 2017

Additional paid-in capital 9053 8474 8443 8666

Retained earnings 26110 19736 21631

2376

1

Accumulated other comprehensive income 11122 9139 9216

1228

4

Total Stockholders' equity 46285 37349 39290

4471

1

The above table shows that the company is having sufficient amount of retained earnings and

also, it is having a good financial statement in terms of accumulation and comprehensiveness.

Such retained earnings are a result of huge profits earned by the entity during all the previous

years. We notice a high amount of comprehensive and accumulated income in the company's

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

financial reports which somewhere also reflects the strong control over the business environment

by the management of the company (Parrino, 2013).

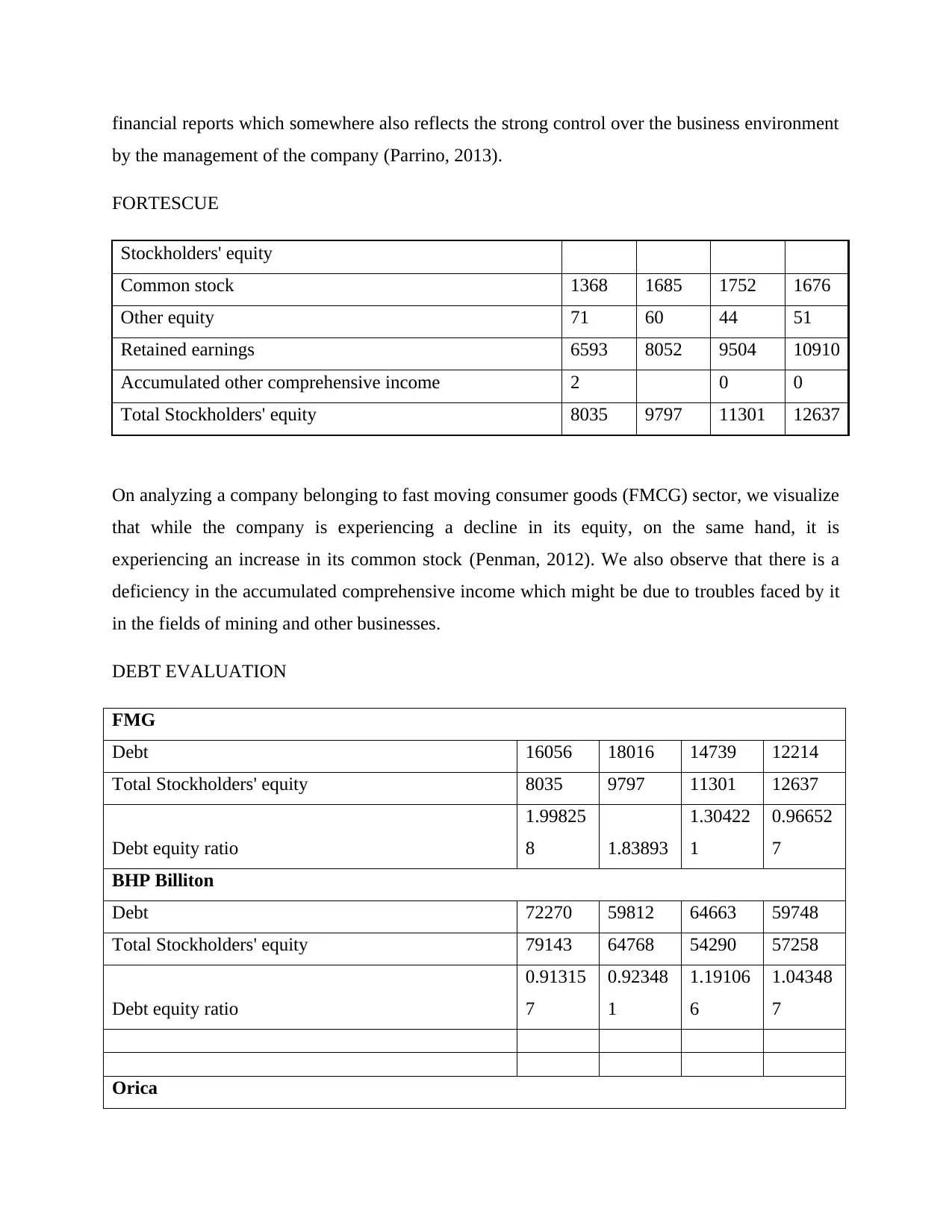

FORTESCUE

Stockholders' equity

Common stock 1368 1685 1752 1676

Other equity 71 60 44 51

Retained earnings 6593 8052 9504 10910

Accumulated other comprehensive income 2 0 0

Total Stockholders' equity 8035 9797 11301 12637

On analyzing a company belonging to fast moving consumer goods (FMCG) sector, we visualize

that while the company is experiencing a decline in its equity, on the same hand, it is

experiencing an increase in its common stock (Penman, 2012). We also observe that there is a

deficiency in the accumulated comprehensive income which might be due to troubles faced by it

in the fields of mining and other businesses.

DEBT EVALUATION

FMG

Debt 16056 18016 14739 12214

Total Stockholders' equity 8035 9797 11301 12637

Debt equity ratio

1.99825

8 1.83893

1.30422

1

0.96652

7

BHP Billiton

Debt 72270 59812 64663 59748

Total Stockholders' equity 79143 64768 54290 57258

Debt equity ratio

0.91315

7

0.92348

1

1.19106

6

1.04348

7

Orica

by the management of the company (Parrino, 2013).

FORTESCUE

Stockholders' equity

Common stock 1368 1685 1752 1676

Other equity 71 60 44 51

Retained earnings 6593 8052 9504 10910

Accumulated other comprehensive income 2 0 0

Total Stockholders' equity 8035 9797 11301 12637

On analyzing a company belonging to fast moving consumer goods (FMCG) sector, we visualize

that while the company is experiencing a decline in its equity, on the same hand, it is

experiencing an increase in its common stock (Penman, 2012). We also observe that there is a

deficiency in the accumulated comprehensive income which might be due to troubles faced by it

in the fields of mining and other businesses.

DEBT EVALUATION

FMG

Debt 16056 18016 14739 12214

Total Stockholders' equity 8035 9797 11301 12637

Debt equity ratio

1.99825

8 1.83893

1.30422

1

0.96652

7

BHP Billiton

Debt 72270 59812 64663 59748

Total Stockholders' equity 79143 64768 54290 57258

Debt equity ratio

0.91315

7

0.92348

1

1.19106

6

1.04348

7

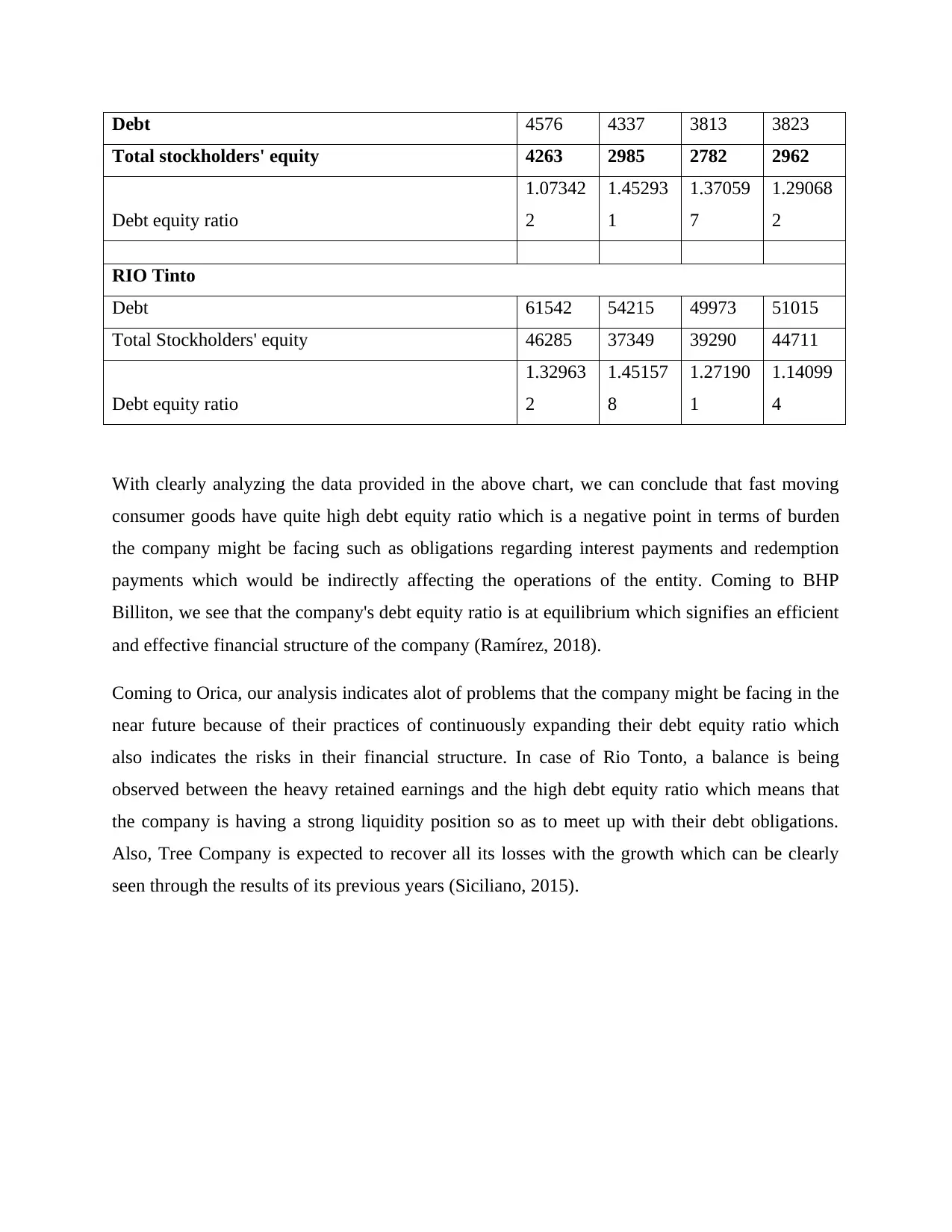

Orica

Debt 4576 4337 3813 3823

Total stockholders' equity 4263 2985 2782 2962

Debt equity ratio

1.07342

2

1.45293

1

1.37059

7

1.29068

2

RIO Tinto

Debt 61542 54215 49973 51015

Total Stockholders' equity 46285 37349 39290 44711

Debt equity ratio

1.32963

2

1.45157

8

1.27190

1

1.14099

4

With clearly analyzing the data provided in the above chart, we can conclude that fast moving

consumer goods have quite high debt equity ratio which is a negative point in terms of burden

the company might be facing such as obligations regarding interest payments and redemption

payments which would be indirectly affecting the operations of the entity. Coming to BHP

Billiton, we see that the company's debt equity ratio is at equilibrium which signifies an efficient

and effective financial structure of the company (Ramírez, 2018).

Coming to Orica, our analysis indicates alot of problems that the company might be facing in the

near future because of their practices of continuously expanding their debt equity ratio which

also indicates the risks in their financial structure. In case of Rio Tonto, a balance is being

observed between the heavy retained earnings and the high debt equity ratio which means that

the company is having a strong liquidity position so as to meet up with their debt obligations.

Also, Tree Company is expected to recover all its losses with the growth which can be clearly

seen through the results of its previous years (Siciliano, 2015).

Total stockholders' equity 4263 2985 2782 2962

Debt equity ratio

1.07342

2

1.45293

1

1.37059

7

1.29068

2

RIO Tinto

Debt 61542 54215 49973 51015

Total Stockholders' equity 46285 37349 39290 44711

Debt equity ratio

1.32963

2

1.45157

8

1.27190

1

1.14099

4

With clearly analyzing the data provided in the above chart, we can conclude that fast moving

consumer goods have quite high debt equity ratio which is a negative point in terms of burden

the company might be facing such as obligations regarding interest payments and redemption

payments which would be indirectly affecting the operations of the entity. Coming to BHP

Billiton, we see that the company's debt equity ratio is at equilibrium which signifies an efficient

and effective financial structure of the company (Ramírez, 2018).

Coming to Orica, our analysis indicates alot of problems that the company might be facing in the

near future because of their practices of continuously expanding their debt equity ratio which

also indicates the risks in their financial structure. In case of Rio Tonto, a balance is being

observed between the heavy retained earnings and the high debt equity ratio which means that

the company is having a strong liquidity position so as to meet up with their debt obligations.

Also, Tree Company is expected to recover all its losses with the growth which can be clearly

seen through the results of its previous years (Siciliano, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.