Corporate Accounting Report: Analysis of Myer's Financials 2018

VerifiedAdded on 2023/03/31

|13

|806

|164

Report

AI Summary

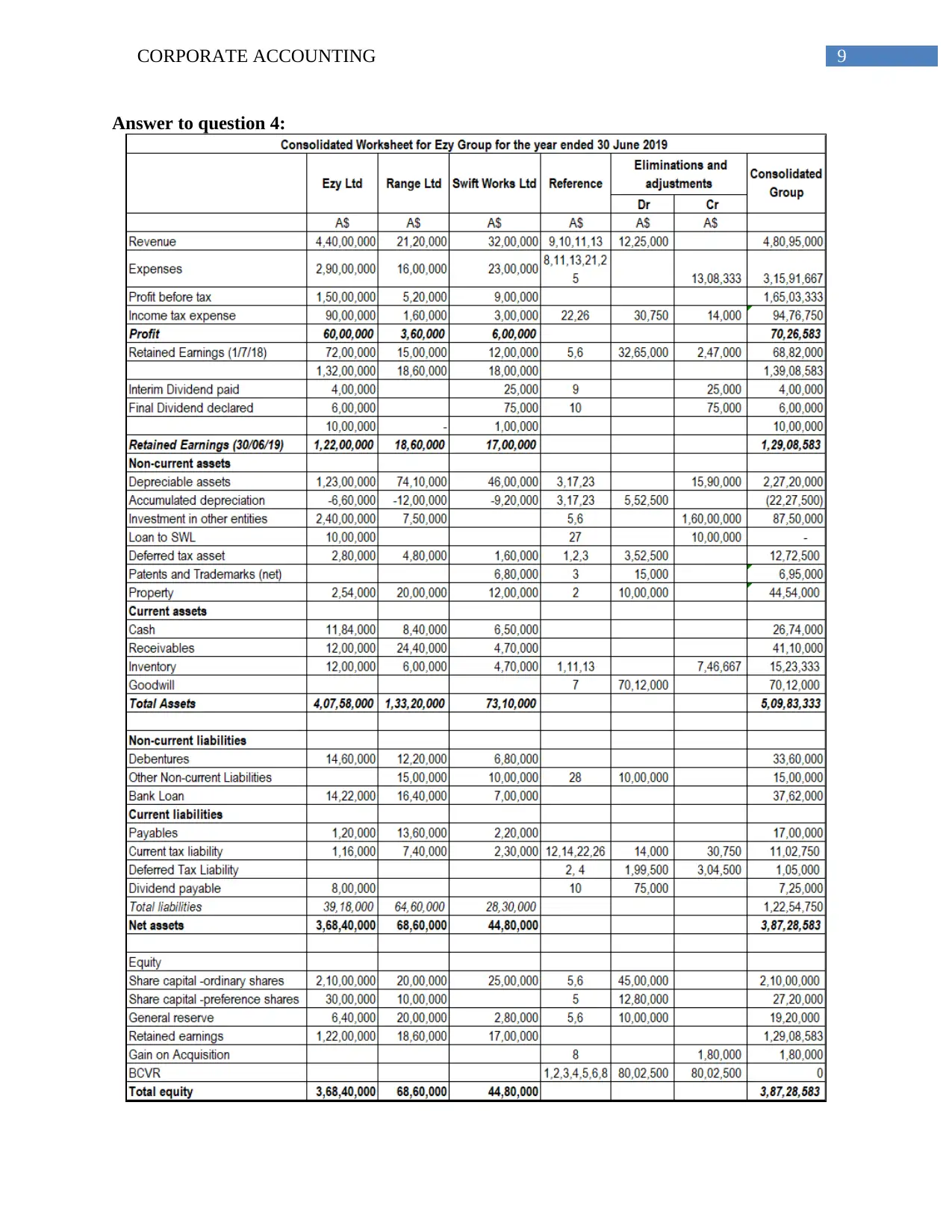

This corporate accounting report analyzes Myer Holdings Limited's 2018 annual report, focusing on key accounting concepts such as impairment testing. The report examines the process of asset impairment, explaining how companies determine the true value of assets and report them in financial statements. It covers the impact of impairment gains and losses on the profit and loss statement and balance sheet. The report uses Myer's 2018 annual report to illustrate the practical application of these concepts, specifically looking at the amortization of goodwill and other assets like brand names and software. It also discusses the role of discount rates in impairment testing and the prohibition of reversing asset impairments under IAS 36. The report provides a comprehensive overview of corporate accounting principles and their practical application through the analysis of Myer's financial data.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.