HI5020 Corporate Accounting Assignment: Financial Performance Analysis

VerifiedAdded on 2023/04/21

|20

|4549

|497

Report

AI Summary

This report conducts a detailed financial analysis of BHP Billiton, Rio Tinto, and Fortescue Metals Group, all prominent companies within the Australian mining industry. The analysis encompasses a comprehensive review of their financial statements over three fiscal years, focusing on key components such as equity, liabilities, cash flow statements, other comprehensive income statements, and corporate income tax. The report examines the share capital, reserves, retained earnings, and non-controlling interests within the equity section, and further investigates current and non-current liabilities. Key financial metrics, including the debt-to-equity ratio, are calculated and evaluated. The cash flow statements are dissected to understand operating, investing, and financing activities, while the other comprehensive income statements are scrutinized to identify sources of gains and losses. Finally, the report addresses the accounting practices related to corporate income tax. The objective of this assessment is to provide a robust evaluation of the financial performance and position of these companies, providing insights into their operational effectiveness and financial health. The report concludes with an overview of the findings, referencing the financial data obtained from the companies' annual reports.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Authors Note:

Corporate Accounting

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING

1

Executive Summary:

The assessment directly evaluates the performance and financial position of BHP Billiton,

Rio Tinto, and Fortescue Metal Group for three fiscal years. The assessment has relatively

evaluated equity, liability, Cash flow statement, other comprehensive income statement, and

corporate income tax of the three companies. The selected companies mainly fall under the

mining industry of Australia, which helps in analysing their overall performance of the three

companies. The equity, liability, cash flow statement, comprehensive income statement and

corporate income tax of the selected companies are mainly analysed in the assessment for

detecting the level of income, which can be generated from an evaluation.

1

Executive Summary:

The assessment directly evaluates the performance and financial position of BHP Billiton,

Rio Tinto, and Fortescue Metal Group for three fiscal years. The assessment has relatively

evaluated equity, liability, Cash flow statement, other comprehensive income statement, and

corporate income tax of the three companies. The selected companies mainly fall under the

mining industry of Australia, which helps in analysing their overall performance of the three

companies. The equity, liability, cash flow statement, comprehensive income statement and

corporate income tax of the selected companies are mainly analysed in the assessment for

detecting the level of income, which can be generated from an evaluation.

CORPORATE ACCOUNTING

2

Table of Contents

Introduction:...............................................................................................................................3

Equity & Liability:.....................................................................................................................3

Answer to i)................................................................................................................................3

Answer to ii)...............................................................................................................................4

Answer to iii)..............................................................................................................................5

Cash Flow Statement:................................................................................................................5

Answer to iv)..............................................................................................................................5

Answer to v)...............................................................................................................................7

Answer to vi)..............................................................................................................................8

Other comprehensive income statement:...................................................................................9

Answer to vii).............................................................................................................................9

Answer to viii)..........................................................................................................................10

Answer to ix)............................................................................................................................11

Answer to x).............................................................................................................................11

Accounting for Corporate income tax:.....................................................................................12

Answer to xi)............................................................................................................................12

Answer to xii)...........................................................................................................................12

Answer to xiii)..........................................................................................................................13

Answer to xiv)..........................................................................................................................14

Answer to xv)...........................................................................................................................14

Answer to xvi)..........................................................................................................................15

Answer to xvii).........................................................................................................................16

Conclusion:..............................................................................................................................16

Reference and Bibliography:....................................................................................................17

2

Table of Contents

Introduction:...............................................................................................................................3

Equity & Liability:.....................................................................................................................3

Answer to i)................................................................................................................................3

Answer to ii)...............................................................................................................................4

Answer to iii)..............................................................................................................................5

Cash Flow Statement:................................................................................................................5

Answer to iv)..............................................................................................................................5

Answer to v)...............................................................................................................................7

Answer to vi)..............................................................................................................................8

Other comprehensive income statement:...................................................................................9

Answer to vii).............................................................................................................................9

Answer to viii)..........................................................................................................................10

Answer to ix)............................................................................................................................11

Answer to x).............................................................................................................................11

Accounting for Corporate income tax:.....................................................................................12

Answer to xi)............................................................................................................................12

Answer to xii)...........................................................................................................................12

Answer to xiii)..........................................................................................................................13

Answer to xiv)..........................................................................................................................14

Answer to xv)...........................................................................................................................14

Answer to xvi)..........................................................................................................................15

Answer to xvii).........................................................................................................................16

Conclusion:..............................................................................................................................16

Reference and Bibliography:....................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE ACCOUNTING

3

Introduction:

The assessment aims in evaluating the overall financial performance of the

organisation selected for the analysis. BHP Billiton Limited, RIO Tinto Limited, and

Fortescue Metals Group is mainly selected for the assessment, which can eventually help in

evaluating different segments of the financial report. The selected companies mainly fall

under the mining industry of Australia, which helps in analysing their overall performance of

the three companies. The equity, liability, cash flow statement, comprehensive income

statement and corporate income tax of the selected companies are mainly analysed in the

assessment for detecting the level of income, which can be generated from an evaluation.

Equity & Liability:

Answer to i)

Share capital, Reserves, retained earnings, treasury shares, and non-controlling

interest are relatively listed in the equity section of the three-selected organization. The

components of the equity faction directly help in identifying the level of equity capital that is

being used by the organization. Share capital is the overall invested money of the investors,

which is traded in the security exchange. Moreover, reserves are the overall savings that has

been maintained by the organization over the period of its operations. The value of retained

earnings is relatively calculated after deducting the dividends and other expenses from the net

income. Lastly, the Non-controlling interest value is derived from the ownership position of

shareholders who has no control over the management’s decision (Kothari, Ramanna and

Skinner 2015).

Reserves, retained earnings, and non-controlling interest of BHP Billiton have fallen

from 2015 to 2017. However, Rio Tinto share capital, Reserves, and retained earnings have

3

Introduction:

The assessment aims in evaluating the overall financial performance of the

organisation selected for the analysis. BHP Billiton Limited, RIO Tinto Limited, and

Fortescue Metals Group is mainly selected for the assessment, which can eventually help in

evaluating different segments of the financial report. The selected companies mainly fall

under the mining industry of Australia, which helps in analysing their overall performance of

the three companies. The equity, liability, cash flow statement, comprehensive income

statement and corporate income tax of the selected companies are mainly analysed in the

assessment for detecting the level of income, which can be generated from an evaluation.

Equity & Liability:

Answer to i)

Share capital, Reserves, retained earnings, treasury shares, and non-controlling

interest are relatively listed in the equity section of the three-selected organization. The

components of the equity faction directly help in identifying the level of equity capital that is

being used by the organization. Share capital is the overall invested money of the investors,

which is traded in the security exchange. Moreover, reserves are the overall savings that has

been maintained by the organization over the period of its operations. The value of retained

earnings is relatively calculated after deducting the dividends and other expenses from the net

income. Lastly, the Non-controlling interest value is derived from the ownership position of

shareholders who has no control over the management’s decision (Kothari, Ramanna and

Skinner 2015).

Reserves, retained earnings, and non-controlling interest of BHP Billiton have fallen

from 2015 to 2017. However, Rio Tinto share capital, Reserves, and retained earnings have

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING

4

relatively increased, while the non-controlling interest has declined from 2015 to 2017.

Lastly, Fortescue Metals Group contributed equity, and reserves have declined from 2015 to

2017. On the other hand, the retained earnings and non-controlling interest has increased over

the period of three years.

Answer to ii)

The liability section of the three companies relatively holds current liabilities and

noncurrent liabilities, which comprises of several obligations that needs to be fulfilled by the

organization. The current liability section relatively comprises of trade payable, interest

bearing liabilities, current tax payables, provision, deferred income, and other financial

liabilities. On the other hand, non-current liabilities comprises of interest bearing liabilities,

deferred tax liabilities, deferred income, and other financial liabilities of the organization.

Trade payables are the overall payments that need to be conducted by the company

for the product that has been purchased on credit. Interest bearing liabilities are the overall

payments that need to be conducted on the loans that are acquired by the organization to

support with operation. Current tax payables are the tax obligations that need to be paid by

the organization. Provisions are the measures that have been taken by the company for

supporting their future payments. Deferred income is the overall revenues that have been

generated on accrual basis by the organization. Other financial liabilities are the relevant

expenses that have been conducted by the organization the period of time (Schaltegger,

Etxeberria and Ortas 2017).

Total current liabilities of BHP Billiton have declined, while values of Rio Tinto and

Fortescue Metal Group have increased from 2015 to 2017. In the similar instance, the overall

non-current liabilities of BHP Billiton have increased, while values of Rio Tinto and

Fortescue Metal Group have declined from 2015 to 2017.

4

relatively increased, while the non-controlling interest has declined from 2015 to 2017.

Lastly, Fortescue Metals Group contributed equity, and reserves have declined from 2015 to

2017. On the other hand, the retained earnings and non-controlling interest has increased over

the period of three years.

Answer to ii)

The liability section of the three companies relatively holds current liabilities and

noncurrent liabilities, which comprises of several obligations that needs to be fulfilled by the

organization. The current liability section relatively comprises of trade payable, interest

bearing liabilities, current tax payables, provision, deferred income, and other financial

liabilities. On the other hand, non-current liabilities comprises of interest bearing liabilities,

deferred tax liabilities, deferred income, and other financial liabilities of the organization.

Trade payables are the overall payments that need to be conducted by the company

for the product that has been purchased on credit. Interest bearing liabilities are the overall

payments that need to be conducted on the loans that are acquired by the organization to

support with operation. Current tax payables are the tax obligations that need to be paid by

the organization. Provisions are the measures that have been taken by the company for

supporting their future payments. Deferred income is the overall revenues that have been

generated on accrual basis by the organization. Other financial liabilities are the relevant

expenses that have been conducted by the organization the period of time (Schaltegger,

Etxeberria and Ortas 2017).

Total current liabilities of BHP Billiton have declined, while values of Rio Tinto and

Fortescue Metal Group have increased from 2015 to 2017. In the similar instance, the overall

non-current liabilities of BHP Billiton have increased, while values of Rio Tinto and

Fortescue Metal Group have declined from 2015 to 2017.

CORPORATE ACCOUNTING

5

Answer to iii)

Debt to equity ratio 2017 2016 2015

BHP Billiton 0.51 0.64 0.46

Rio Tinto 0.31 0.40 0.54

Fortescue Metals Group 0.46 0.81 1.27

From the overall evaluation, it could be understood that the debt to equity position of

Rio Tinto has a relatively improved over the period of three years in comparison to BHP

Billiton and Fortescue Metals Group. The debt composition of Rio Tinto is at the levels of

0.31 in 2017, as it declined from the levels of 0.54, while other companies overall debt

positions has remained at the levels of 0.46 to 0.51 in 2017.

Cash Flow Statement:

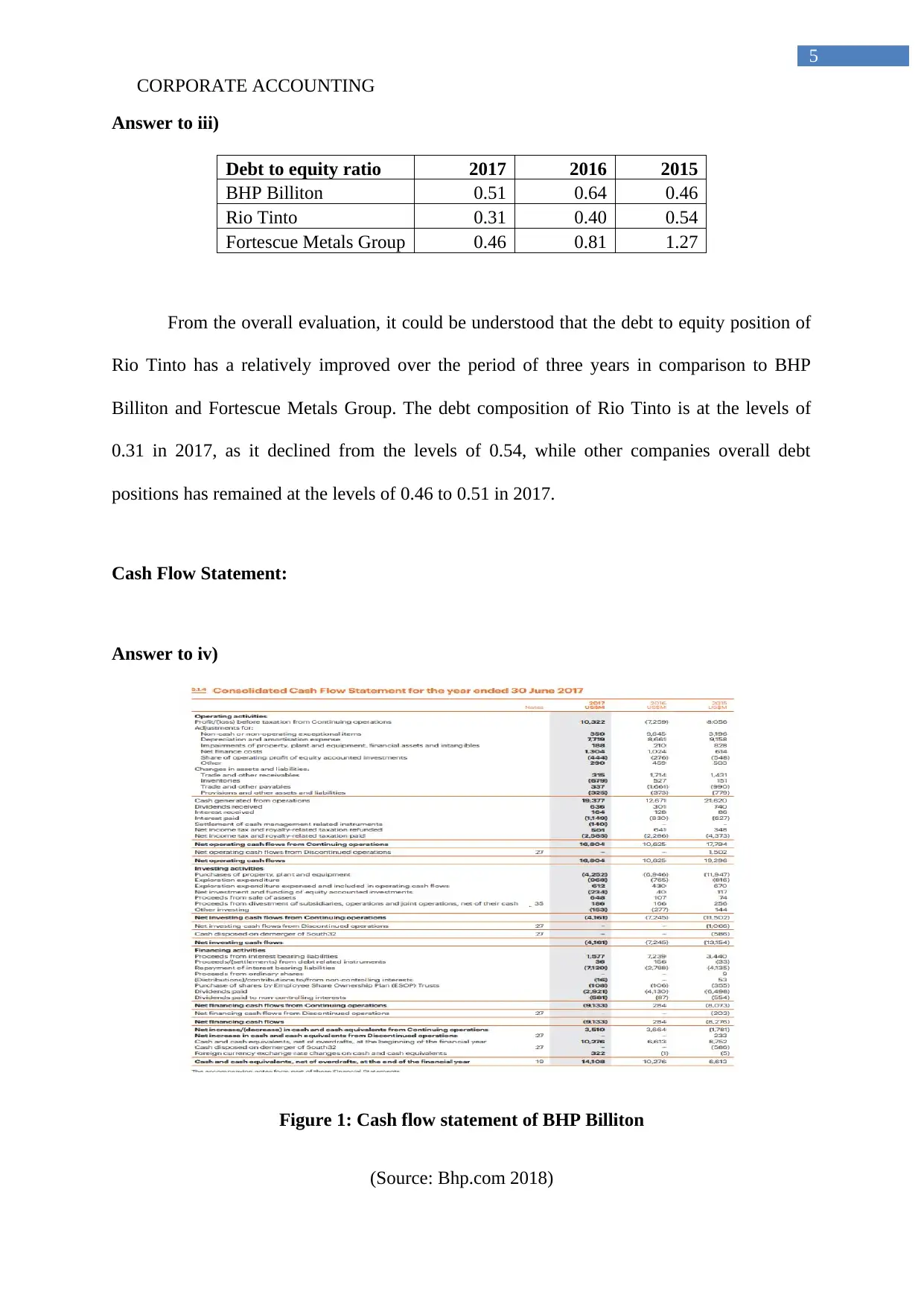

Answer to iv)

Figure 1: Cash flow statement of BHP Billiton

(Source: Bhp.com 2018)

5

Answer to iii)

Debt to equity ratio 2017 2016 2015

BHP Billiton 0.51 0.64 0.46

Rio Tinto 0.31 0.40 0.54

Fortescue Metals Group 0.46 0.81 1.27

From the overall evaluation, it could be understood that the debt to equity position of

Rio Tinto has a relatively improved over the period of three years in comparison to BHP

Billiton and Fortescue Metals Group. The debt composition of Rio Tinto is at the levels of

0.31 in 2017, as it declined from the levels of 0.54, while other companies overall debt

positions has remained at the levels of 0.46 to 0.51 in 2017.

Cash Flow Statement:

Answer to iv)

Figure 1: Cash flow statement of BHP Billiton

(Source: Bhp.com 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE ACCOUNTING

6

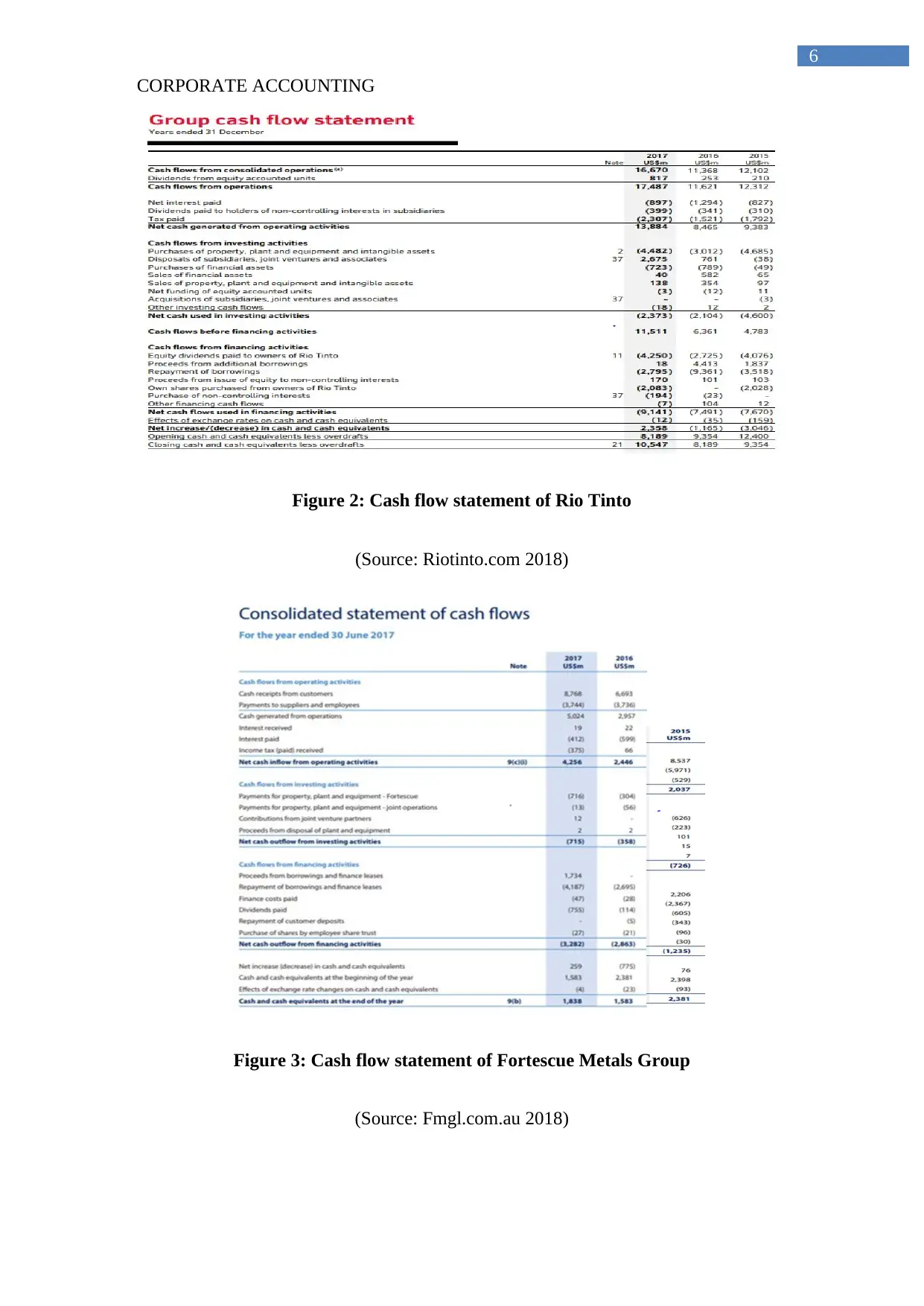

Figure 2: Cash flow statement of Rio Tinto

(Source: Riotinto.com 2018)

Figure 3: Cash flow statement of Fortescue Metals Group

(Source: Fmgl.com.au 2018)

6

Figure 2: Cash flow statement of Rio Tinto

(Source: Riotinto.com 2018)

Figure 3: Cash flow statement of Fortescue Metals Group

(Source: Fmgl.com.au 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING

7

The above figures directly indicate the overall price movement of the cash flows,

which comprises of operating activities, investing activities, and financing activities. The

operating activities relatively identify all the relevant cash inflows and outflows that have

been conducted by the company to support their operations. The investing activities relatively

rely on the oral property, plant and equipment that has purchased and sold by the organization

is relatively list in this section. The overall financing activities relatively rely on the financial

lease, share issue, Bond issue, dividend payments, and other finance cost that has been

incurred by the company during the first year. The cash equivalent of Fortescue metal group

has declined from 2015 to 2017, while both BHP Billiton and Rio Tinto cash position has

relatively increased during the same period. The changes in the values are due to the rising

investing activities and operating activities maintained by the companies (Domino, Wingreen

and Blanton 2015).

Answer to v)

BHP Billiton in Million 2017 2016 2015

Operating activities 16,804 10,625 19,296

Investing activities (4,161) (7,245) (13,154)

Financing activities (9,133) 284 (8,276)

Rio Tinto in Million 2017 2016 2015

Operating activities 13,884 8,465 9,383

Investing activities (2,373) (2,104) (4,600)

Financing activities (9,141) (7,491) (7,670)

Fortescue Metals Group in Million 2017 2016 2015

Operating activities 4,256 2,446 2,037

Investing activities (715) (358) (726)

Financing activities (3,282) (2,863) (1,235)

7

The above figures directly indicate the overall price movement of the cash flows,

which comprises of operating activities, investing activities, and financing activities. The

operating activities relatively identify all the relevant cash inflows and outflows that have

been conducted by the company to support their operations. The investing activities relatively

rely on the oral property, plant and equipment that has purchased and sold by the organization

is relatively list in this section. The overall financing activities relatively rely on the financial

lease, share issue, Bond issue, dividend payments, and other finance cost that has been

incurred by the company during the first year. The cash equivalent of Fortescue metal group

has declined from 2015 to 2017, while both BHP Billiton and Rio Tinto cash position has

relatively increased during the same period. The changes in the values are due to the rising

investing activities and operating activities maintained by the companies (Domino, Wingreen

and Blanton 2015).

Answer to v)

BHP Billiton in Million 2017 2016 2015

Operating activities 16,804 10,625 19,296

Investing activities (4,161) (7,245) (13,154)

Financing activities (9,133) 284 (8,276)

Rio Tinto in Million 2017 2016 2015

Operating activities 13,884 8,465 9,383

Investing activities (2,373) (2,104) (4,600)

Financing activities (9,141) (7,491) (7,670)

Fortescue Metals Group in Million 2017 2016 2015

Operating activities 4,256 2,446 2,037

Investing activities (715) (358) (726)

Financing activities (3,282) (2,863) (1,235)

CORPORATE ACCOUNTING

8

From the evaluation of the above table, cash flow position of BHP Billiton, Rio Tinto,

and Fortescue Metal Group are relatively identified. The value of operating activities and

financing activities has been declined from 2015 to 2017, while the overall investing

activities have improved over the same period. On the other hand, the operating activities and

investing activities of Rio Tinto has improved during the period of 3 years, while its

financing activities have deteriorated. Furthermore, only the operating activities of Fortescue

Metal Group has increased in three years, while both investing activities and financing

activities has deteriorated during the period.

Answer to vi)

The analysis of the above company’s cash flow statement has relatively help in

identifying their cash position and capability to continue their operations. The analysis has

also helped in detecting that both Rio Tinto and BHP Billiton overall cash position has

relatively improved for the period of three years, while deterioration in Fortescue Metal

Group has been witnessed. The operating activities of Rio Tinto has relatively improved

exponentially in three years, while BHP Billiton overall expenses on net investing activities

has reduced exponentially which boosted its closing cash balance. Fortescue Metal Group as

a relatively increased the level of expenses on financing and investing activities, which is the

main reason behind its overall decline in cash and cash equivalent closing balance (Suzuk

2015).

8

From the evaluation of the above table, cash flow position of BHP Billiton, Rio Tinto,

and Fortescue Metal Group are relatively identified. The value of operating activities and

financing activities has been declined from 2015 to 2017, while the overall investing

activities have improved over the same period. On the other hand, the operating activities and

investing activities of Rio Tinto has improved during the period of 3 years, while its

financing activities have deteriorated. Furthermore, only the operating activities of Fortescue

Metal Group has increased in three years, while both investing activities and financing

activities has deteriorated during the period.

Answer to vi)

The analysis of the above company’s cash flow statement has relatively help in

identifying their cash position and capability to continue their operations. The analysis has

also helped in detecting that both Rio Tinto and BHP Billiton overall cash position has

relatively improved for the period of three years, while deterioration in Fortescue Metal

Group has been witnessed. The operating activities of Rio Tinto has relatively improved

exponentially in three years, while BHP Billiton overall expenses on net investing activities

has reduced exponentially which boosted its closing cash balance. Fortescue Metal Group as

a relatively increased the level of expenses on financing and investing activities, which is the

main reason behind its overall decline in cash and cash equivalent closing balance (Suzuk

2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE ACCOUNTING

9

Other comprehensive income statement:

Answer to vii)

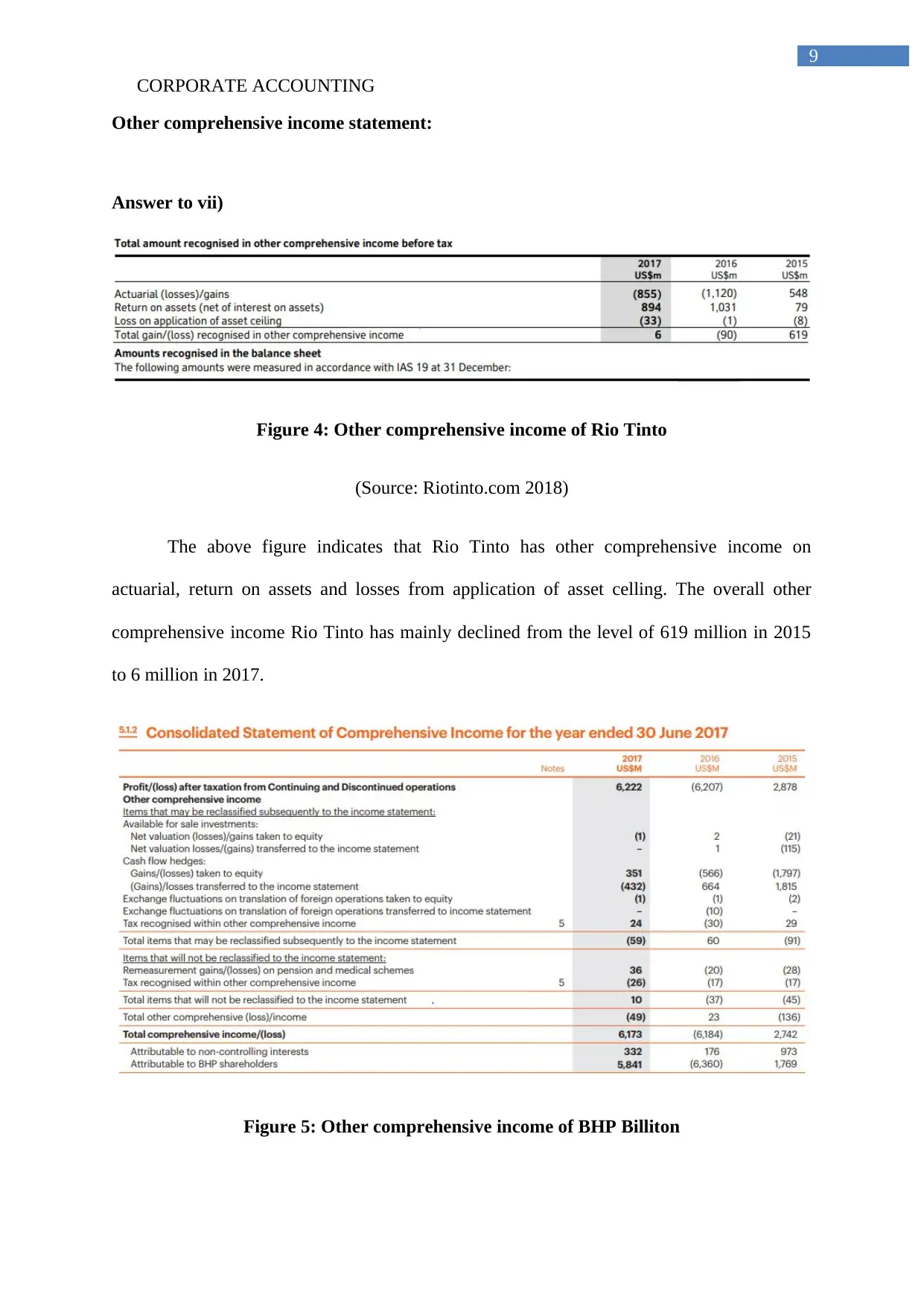

Figure 4: Other comprehensive income of Rio Tinto

(Source: Riotinto.com 2018)

The above figure indicates that Rio Tinto has other comprehensive income on

actuarial, return on assets and losses from application of asset celling. The overall other

comprehensive income Rio Tinto has mainly declined from the level of 619 million in 2015

to 6 million in 2017.

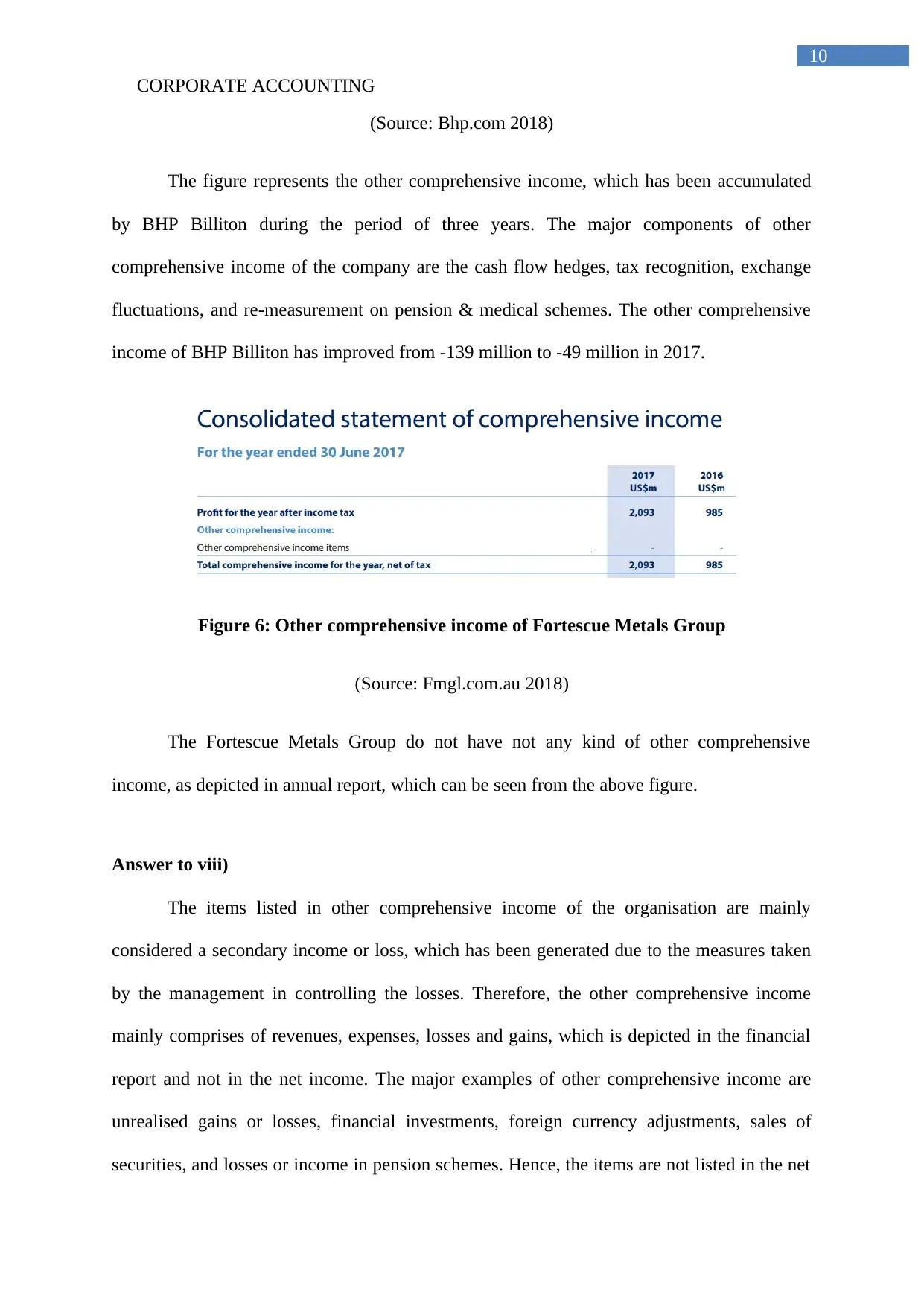

Figure 5: Other comprehensive income of BHP Billiton

9

Other comprehensive income statement:

Answer to vii)

Figure 4: Other comprehensive income of Rio Tinto

(Source: Riotinto.com 2018)

The above figure indicates that Rio Tinto has other comprehensive income on

actuarial, return on assets and losses from application of asset celling. The overall other

comprehensive income Rio Tinto has mainly declined from the level of 619 million in 2015

to 6 million in 2017.

Figure 5: Other comprehensive income of BHP Billiton

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING

10

(Source: Bhp.com 2018)

The figure represents the other comprehensive income, which has been accumulated

by BHP Billiton during the period of three years. The major components of other

comprehensive income of the company are the cash flow hedges, tax recognition, exchange

fluctuations, and re-measurement on pension & medical schemes. The other comprehensive

income of BHP Billiton has improved from -139 million to -49 million in 2017.

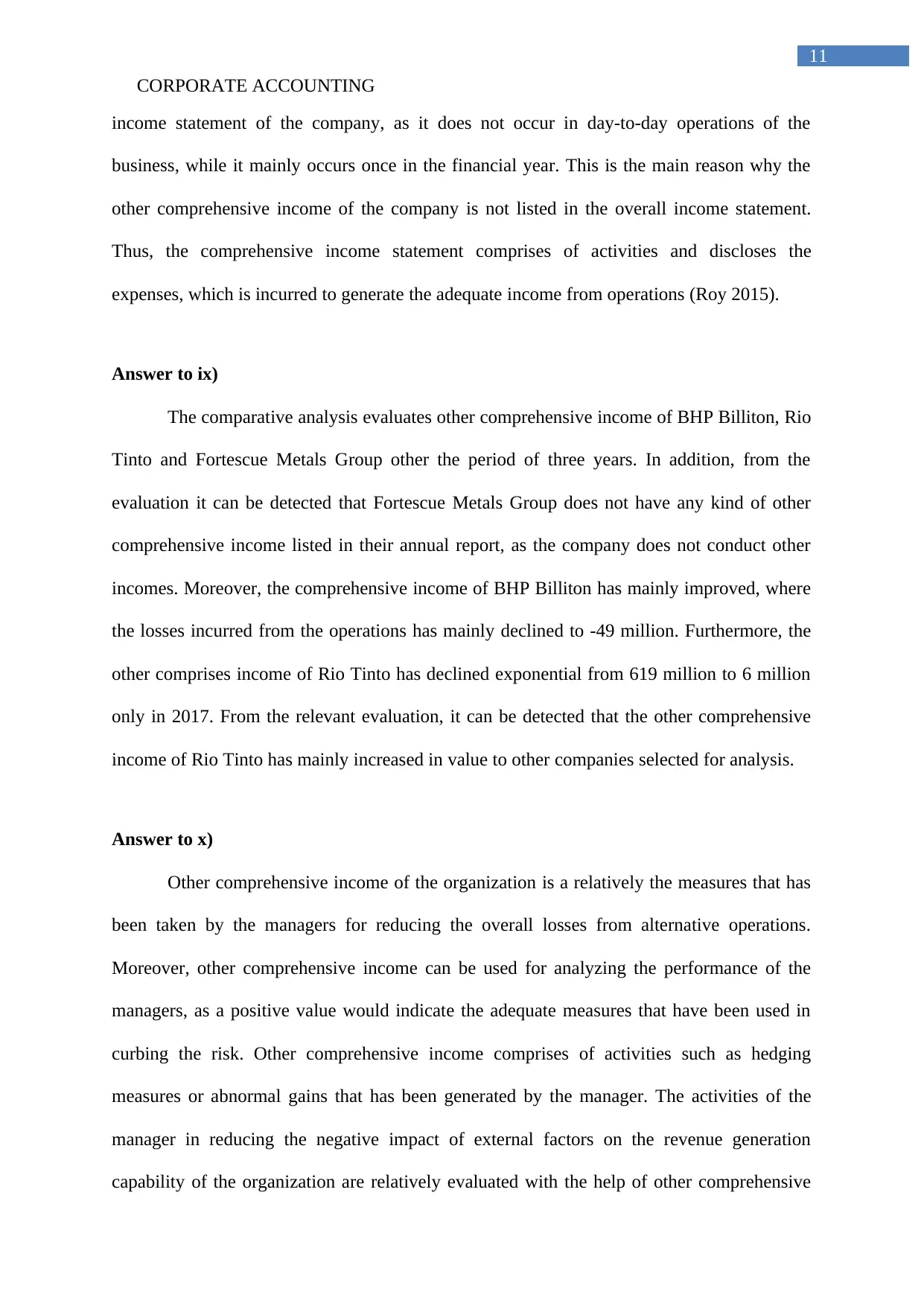

Figure 6: Other comprehensive income of Fortescue Metals Group

(Source: Fmgl.com.au 2018)

The Fortescue Metals Group do not have not any kind of other comprehensive

income, as depicted in annual report, which can be seen from the above figure.

Answer to viii)

The items listed in other comprehensive income of the organisation are mainly

considered a secondary income or loss, which has been generated due to the measures taken

by the management in controlling the losses. Therefore, the other comprehensive income

mainly comprises of revenues, expenses, losses and gains, which is depicted in the financial

report and not in the net income. The major examples of other comprehensive income are

unrealised gains or losses, financial investments, foreign currency adjustments, sales of

securities, and losses or income in pension schemes. Hence, the items are not listed in the net

10

(Source: Bhp.com 2018)

The figure represents the other comprehensive income, which has been accumulated

by BHP Billiton during the period of three years. The major components of other

comprehensive income of the company are the cash flow hedges, tax recognition, exchange

fluctuations, and re-measurement on pension & medical schemes. The other comprehensive

income of BHP Billiton has improved from -139 million to -49 million in 2017.

Figure 6: Other comprehensive income of Fortescue Metals Group

(Source: Fmgl.com.au 2018)

The Fortescue Metals Group do not have not any kind of other comprehensive

income, as depicted in annual report, which can be seen from the above figure.

Answer to viii)

The items listed in other comprehensive income of the organisation are mainly

considered a secondary income or loss, which has been generated due to the measures taken

by the management in controlling the losses. Therefore, the other comprehensive income

mainly comprises of revenues, expenses, losses and gains, which is depicted in the financial

report and not in the net income. The major examples of other comprehensive income are

unrealised gains or losses, financial investments, foreign currency adjustments, sales of

securities, and losses or income in pension schemes. Hence, the items are not listed in the net

CORPORATE ACCOUNTING

11

income statement of the company, as it does not occur in day-to-day operations of the

business, while it mainly occurs once in the financial year. This is the main reason why the

other comprehensive income of the company is not listed in the overall income statement.

Thus, the comprehensive income statement comprises of activities and discloses the

expenses, which is incurred to generate the adequate income from operations (Roy 2015).

Answer to ix)

The comparative analysis evaluates other comprehensive income of BHP Billiton, Rio

Tinto and Fortescue Metals Group other the period of three years. In addition, from the

evaluation it can be detected that Fortescue Metals Group does not have any kind of other

comprehensive income listed in their annual report, as the company does not conduct other

incomes. Moreover, the comprehensive income of BHP Billiton has mainly improved, where

the losses incurred from the operations has mainly declined to -49 million. Furthermore, the

other comprises income of Rio Tinto has declined exponential from 619 million to 6 million

only in 2017. From the relevant evaluation, it can be detected that the other comprehensive

income of Rio Tinto has mainly increased in value to other companies selected for analysis.

Answer to x)

Other comprehensive income of the organization is a relatively the measures that has

been taken by the managers for reducing the overall losses from alternative operations.

Moreover, other comprehensive income can be used for analyzing the performance of the

managers, as a positive value would indicate the adequate measures that have been used in

curbing the risk. Other comprehensive income comprises of activities such as hedging

measures or abnormal gains that has been generated by the manager. The activities of the

manager in reducing the negative impact of external factors on the revenue generation

capability of the organization are relatively evaluated with the help of other comprehensive

11

income statement of the company, as it does not occur in day-to-day operations of the

business, while it mainly occurs once in the financial year. This is the main reason why the

other comprehensive income of the company is not listed in the overall income statement.

Thus, the comprehensive income statement comprises of activities and discloses the

expenses, which is incurred to generate the adequate income from operations (Roy 2015).

Answer to ix)

The comparative analysis evaluates other comprehensive income of BHP Billiton, Rio

Tinto and Fortescue Metals Group other the period of three years. In addition, from the

evaluation it can be detected that Fortescue Metals Group does not have any kind of other

comprehensive income listed in their annual report, as the company does not conduct other

incomes. Moreover, the comprehensive income of BHP Billiton has mainly improved, where

the losses incurred from the operations has mainly declined to -49 million. Furthermore, the

other comprises income of Rio Tinto has declined exponential from 619 million to 6 million

only in 2017. From the relevant evaluation, it can be detected that the other comprehensive

income of Rio Tinto has mainly increased in value to other companies selected for analysis.

Answer to x)

Other comprehensive income of the organization is a relatively the measures that has

been taken by the managers for reducing the overall losses from alternative operations.

Moreover, other comprehensive income can be used for analyzing the performance of the

managers, as a positive value would indicate the adequate measures that have been used in

curbing the risk. Other comprehensive income comprises of activities such as hedging

measures or abnormal gains that has been generated by the manager. The activities of the

manager in reducing the negative impact of external factors on the revenue generation

capability of the organization are relatively evaluated with the help of other comprehensive

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.