HI5020 Corporate Accounting Report: Comparative Company Analysis

VerifiedAdded on 2023/06/03

|14

|3748

|60

Report

AI Summary

This report provides a comparative analysis of the corporate accounting practices of Seafarms and Woolworths Ltd, both listed on the Australian Securities Exchange (ASX). The analysis focuses on key financial statement elements, including owners' equity, statement of cash flow, comprehensive statement of income, and accounting for corporate income tax. The report examines the companies' annual reports to evaluate their performance, comparing their disclosures and identifying significant changes from the previous year. The executive summary highlights the importance of disclosures in decision-making. The report provides insights into the companies' financial positions, including the impact of share issues, reserves, and retained earnings. It also analyzes the cash flow from operating, investing, and financing activities. The comprehensive statement of income is examined, considering the impact of unrealized revenues and expenses. The report aims to determine which company has been more effective in its performance based on the presented financial data. Furthermore, the report also evaluates additional information in the footnotes and notes to the financial statements so that a better understanding can be facilitated.

qwertyuiopasdfghjklzxcvbnmqw

ertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyu

iopasdfghjklzxcvbnmqwertyuio

pasdfghjklzxcvbnmqwertyuiopa

sdfghjklzxcvbnmqwertyuiopasd

fghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklz

xcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnm

qwertyuiopasdfghjklzxcvbnmqw

ertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyu

iopasdfghjklzxcvbnmrtyuiopasd

fghjklzxcvbnmqwertyuiopasdfg

Corporate accounting

ertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyu

iopasdfghjklzxcvbnmqwertyuio

pasdfghjklzxcvbnmqwertyuiopa

sdfghjklzxcvbnmqwertyuiopasd

fghjklzxcvbnmqwertyuiopasdfg

hjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklz

xcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnm

qwertyuiopasdfghjklzxcvbnmqw

ertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyu

iopasdfghjklzxcvbnmrtyuiopasd

fghjklzxcvbnmqwertyuiopasdfg

Corporate accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive summary

Disclosures are significant in the corporate world because it allows users in making relevant

decisions. Furthermore, a comparative analysis between the disclosures of two companies can

assist in highlighting their inclination towards disclosures and organizational performance on

a whole. Therefore, the annual reports of Seafarms and Woolworths Ltd will be studied

through this report so that their different segments can be evaluated and a conclusion can be

derived as to which company has been more effective in its performance. Moreover,

segments like owners’ equity, income tax, comprehensive statement of income, etc will be

taken into due consideration so that any alterations in these areas when compared to the

previous year can be observed and the reasons behind such change can be assessed

thoroughly. The report will also evaluate the additional information in the footnotes and notes

to the financial statements so that a better understanding can be facilitated.

2

Disclosures are significant in the corporate world because it allows users in making relevant

decisions. Furthermore, a comparative analysis between the disclosures of two companies can

assist in highlighting their inclination towards disclosures and organizational performance on

a whole. Therefore, the annual reports of Seafarms and Woolworths Ltd will be studied

through this report so that their different segments can be evaluated and a conclusion can be

derived as to which company has been more effective in its performance. Moreover,

segments like owners’ equity, income tax, comprehensive statement of income, etc will be

taken into due consideration so that any alterations in these areas when compared to the

previous year can be observed and the reasons behind such change can be assessed

thoroughly. The report will also evaluate the additional information in the footnotes and notes

to the financial statements so that a better understanding can be facilitated.

2

Contents

Introduction...........................................................................................................................................3

Owners Equity.......................................................................................................................................3

Statement of cash flow..........................................................................................................................4

Comprehensive statement of income...................................................................................................6

Accounting for Corporate income tax....................................................................................................8

Conclusion...........................................................................................................................................11

References...........................................................................................................................................12

3

Introduction...........................................................................................................................................3

Owners Equity.......................................................................................................................................3

Statement of cash flow..........................................................................................................................4

Comprehensive statement of income...................................................................................................6

Accounting for Corporate income tax....................................................................................................8

Conclusion...........................................................................................................................................11

References...........................................................................................................................................12

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

This report has reflected the different segments of both the companies so that a comparative

analysis can be performed and it can be determined as to which company has witnessed

extreme changes in comparison to the last year. In relation to this, Seafarms Ltd has been

chosen that is listed on the ASX and is a major producer of poultry and other agricultural

products. The company is primarily operating throughout New Zealand and Australia and

intends to diversify its affairs throughout the world. In contrast to this, Woolworths Ltd is a

major retailer that is undertaking its activities on a diversified scale and is also listed on the

ASX.

Owners Equity

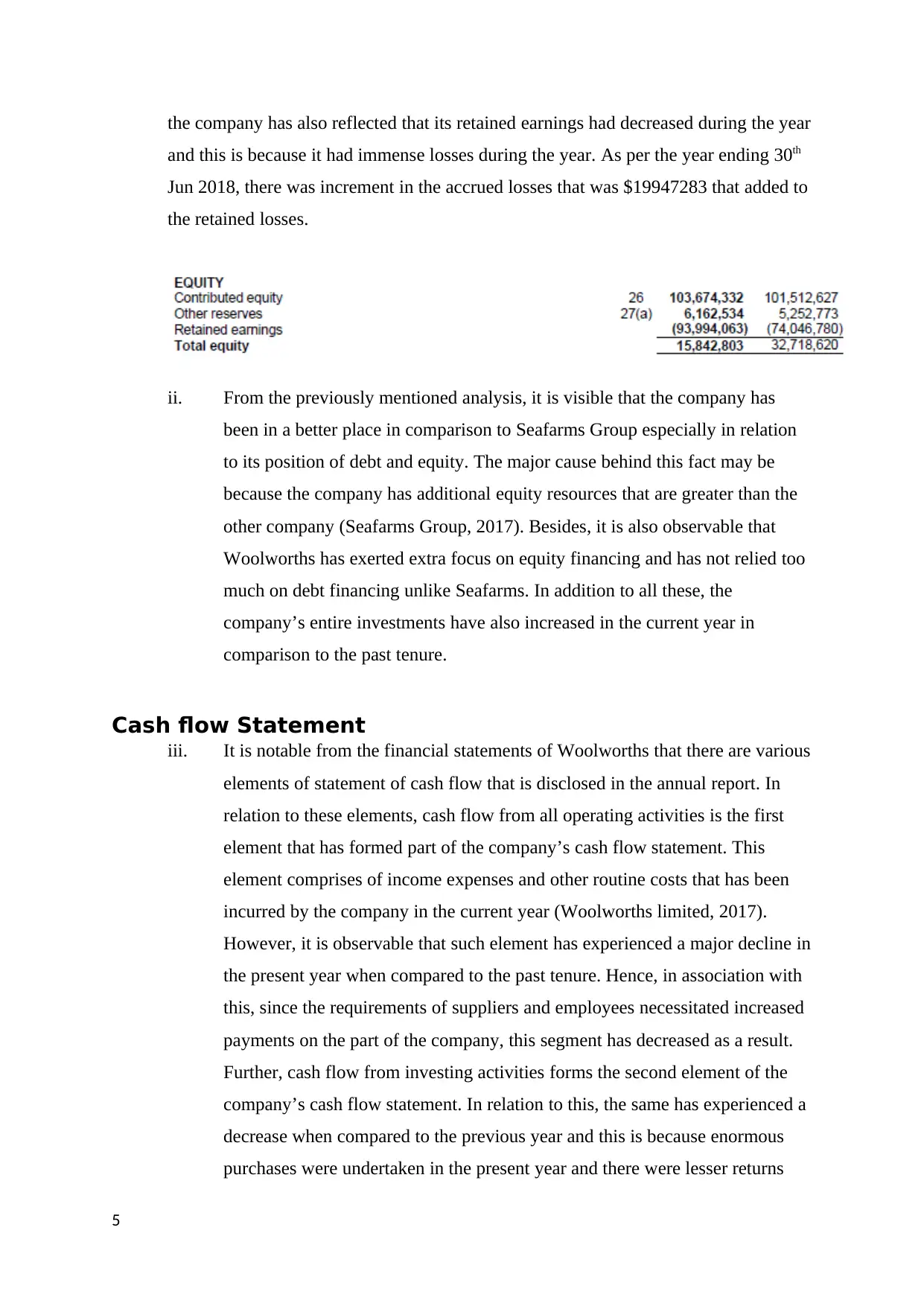

i. It is observable from the companies’ annual reports that the total equity of

Woolworths has been disclosed at $10849 million for the current year. In

contrast to this, such segment reported an amount of $9876 in the previous

year that reflects increment in such segment. This is because Woolworths has

many elements in its financial statements and that can be accounted for by

users in their decision-making process. Nevertheless, the company’s

contributed equity has also experienced an increment in comparison to the last

year and the reason behind this can be attributed to the issue of fresh shares

that has been facilitated in the reinvestment and employees’ long-term

incentives (Needles & Powers, 2013). Nonetheless, the company’s reserves

have also declined owing to the costs associated to the share-based program.

Furthermore, variations in non-controlling interests and retained earnings can

be because of rise in net profits even though dividend payments had been

incurred during the years.

When it comes to Seafarms, the overall equity declined from the range $32718620 in

June 2017 to $ 15842803. The increment is due to the various components of equity

that is contained from the annual report of the company. The increment in the

contributed equity happened due to the share capital issue (Seafarms Group, 2017)

The company’s reserves have experienced a major increment during the year that is a

positive sign of its performance. This is because employees of the company had

attained performance rights, lapsed options, etc that resulted in such increase. Further,

4

This report has reflected the different segments of both the companies so that a comparative

analysis can be performed and it can be determined as to which company has witnessed

extreme changes in comparison to the last year. In relation to this, Seafarms Ltd has been

chosen that is listed on the ASX and is a major producer of poultry and other agricultural

products. The company is primarily operating throughout New Zealand and Australia and

intends to diversify its affairs throughout the world. In contrast to this, Woolworths Ltd is a

major retailer that is undertaking its activities on a diversified scale and is also listed on the

ASX.

Owners Equity

i. It is observable from the companies’ annual reports that the total equity of

Woolworths has been disclosed at $10849 million for the current year. In

contrast to this, such segment reported an amount of $9876 in the previous

year that reflects increment in such segment. This is because Woolworths has

many elements in its financial statements and that can be accounted for by

users in their decision-making process. Nevertheless, the company’s

contributed equity has also experienced an increment in comparison to the last

year and the reason behind this can be attributed to the issue of fresh shares

that has been facilitated in the reinvestment and employees’ long-term

incentives (Needles & Powers, 2013). Nonetheless, the company’s reserves

have also declined owing to the costs associated to the share-based program.

Furthermore, variations in non-controlling interests and retained earnings can

be because of rise in net profits even though dividend payments had been

incurred during the years.

When it comes to Seafarms, the overall equity declined from the range $32718620 in

June 2017 to $ 15842803. The increment is due to the various components of equity

that is contained from the annual report of the company. The increment in the

contributed equity happened due to the share capital issue (Seafarms Group, 2017)

The company’s reserves have experienced a major increment during the year that is a

positive sign of its performance. This is because employees of the company had

attained performance rights, lapsed options, etc that resulted in such increase. Further,

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the company has also reflected that its retained earnings had decreased during the year

and this is because it had immense losses during the year. As per the year ending 30th

Jun 2018, there was increment in the accrued losses that was $19947283 that added to

the retained losses.

ii. From the previously mentioned analysis, it is visible that the company has

been in a better place in comparison to Seafarms Group especially in relation

to its position of debt and equity. The major cause behind this fact may be

because the company has additional equity resources that are greater than the

other company (Seafarms Group, 2017). Besides, it is also observable that

Woolworths has exerted extra focus on equity financing and has not relied too

much on debt financing unlike Seafarms. In addition to all these, the

company’s entire investments have also increased in the current year in

comparison to the past tenure.

Cash flow Statement

iii. It is notable from the financial statements of Woolworths that there are various

elements of statement of cash flow that is disclosed in the annual report. In

relation to these elements, cash flow from all operating activities is the first

element that has formed part of the company’s cash flow statement. This

element comprises of income expenses and other routine costs that has been

incurred by the company in the current year (Woolworths limited, 2017).

However, it is observable that such element has experienced a major decline in

the present year when compared to the past tenure. Hence, in association with

this, since the requirements of suppliers and employees necessitated increased

payments on the part of the company, this segment has decreased as a result.

Further, cash flow from investing activities forms the second element of the

company’s cash flow statement. In relation to this, the same has experienced a

decrease when compared to the previous year and this is because enormous

purchases were undertaken in the present year and there were lesser returns

5

and this is because it had immense losses during the year. As per the year ending 30th

Jun 2018, there was increment in the accrued losses that was $19947283 that added to

the retained losses.

ii. From the previously mentioned analysis, it is visible that the company has

been in a better place in comparison to Seafarms Group especially in relation

to its position of debt and equity. The major cause behind this fact may be

because the company has additional equity resources that are greater than the

other company (Seafarms Group, 2017). Besides, it is also observable that

Woolworths has exerted extra focus on equity financing and has not relied too

much on debt financing unlike Seafarms. In addition to all these, the

company’s entire investments have also increased in the current year in

comparison to the past tenure.

Cash flow Statement

iii. It is notable from the financial statements of Woolworths that there are various

elements of statement of cash flow that is disclosed in the annual report. In

relation to these elements, cash flow from all operating activities is the first

element that has formed part of the company’s cash flow statement. This

element comprises of income expenses and other routine costs that has been

incurred by the company in the current year (Woolworths limited, 2017).

However, it is observable that such element has experienced a major decline in

the present year when compared to the past tenure. Hence, in association with

this, since the requirements of suppliers and employees necessitated increased

payments on the part of the company, this segment has decreased as a result.

Further, cash flow from investing activities forms the second element of the

company’s cash flow statement. In relation to this, the same has experienced a

decrease when compared to the previous year and this is because enormous

purchases were undertaken in the present year and there were lesser returns

5

attained from sale of (PPE) property, plant, and equipments. Further, cash

flow from financing activities forms the third and last element of the

company’s cash flow statement. This element has also declined in the present

year in comparison to the last year. Moreover, even though the company had

undertaken dividend payments in the current year, the outstanding obligations

have not been properly addressed that is a negative indicator and that has

resulted in such deterioration (Deegan, 2011).

When it comes to Seafarm, the cash flow statement comprises of the following:

Cash outflow or inflow from overall operating affairs – Seafarms’ cash flow statement

has portrayed that there are items like general or standard costs that the company has

incurred. In addition, the company has disclosed that its operating activities have

increased in the present scenario that has resulted in the exaggeration of outflow of

cash towards such activities. Besides, it has been reflected that receipts from

customers failed to surpass the expenses that had been undertaken to address the

needs of employees and suppliers.

Outflow of cash for the company’s investing activities has maximized in the current

phase. This is because the company’s expenses towards acquiring fixed assets like PPE

and other machineries had been incurred. Furthermore, there are other assets that have

also incurred extreme costs on the company’s part.

The inflow of cash in association with the company’s financing activities has decreased in

the present year. In addition, the company’s borrowings have also enhanced in this year

when compared to the past tenure. Moreover, the company had also encountered a

maximization of consideration owing to issue of fresh shares in the present scenario.

Therefore, its cash and cash equivalents have deteriorated during the year and that is a

negative indicator of its overall performance.

Comparative analysis

iv. Woolworths Ltd

The net cash from the operating activities of the company have decreased in the present year

because enormous payments were undertaken towards suppliers and employees when

compared to the previous year. In addition, the cash flow from investing activities of the

company had also deteriorated and the major cause behind this can be due to lesser returns

from sale of fixed assets and larger purchases in the current year when compared to the last

6

flow from financing activities forms the third and last element of the

company’s cash flow statement. This element has also declined in the present

year in comparison to the last year. Moreover, even though the company had

undertaken dividend payments in the current year, the outstanding obligations

have not been properly addressed that is a negative indicator and that has

resulted in such deterioration (Deegan, 2011).

When it comes to Seafarm, the cash flow statement comprises of the following:

Cash outflow or inflow from overall operating affairs – Seafarms’ cash flow statement

has portrayed that there are items like general or standard costs that the company has

incurred. In addition, the company has disclosed that its operating activities have

increased in the present scenario that has resulted in the exaggeration of outflow of

cash towards such activities. Besides, it has been reflected that receipts from

customers failed to surpass the expenses that had been undertaken to address the

needs of employees and suppliers.

Outflow of cash for the company’s investing activities has maximized in the current

phase. This is because the company’s expenses towards acquiring fixed assets like PPE

and other machineries had been incurred. Furthermore, there are other assets that have

also incurred extreme costs on the company’s part.

The inflow of cash in association with the company’s financing activities has decreased in

the present year. In addition, the company’s borrowings have also enhanced in this year

when compared to the past tenure. Moreover, the company had also encountered a

maximization of consideration owing to issue of fresh shares in the present scenario.

Therefore, its cash and cash equivalents have deteriorated during the year and that is a

negative indicator of its overall performance.

Comparative analysis

iv. Woolworths Ltd

The net cash from the operating activities of the company have decreased in the present year

because enormous payments were undertaken towards suppliers and employees when

compared to the previous year. In addition, the cash flow from investing activities of the

company had also deteriorated and the major cause behind this can be due to lesser returns

from sale of fixed assets and larger purchases in the current year when compared to the last

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

year. The company has also utilized fewer resources in association with its financing

activities that has resulted in the decline of such segment as well.

v. Insight on such analysis

It is observable from the cash flow statement of the company that it has witnessed

enhancements in its cash equivalent and cash at the end of the year that sheds light on growth

and development on its part.

Comprehensive statement of income

vi. The company has incorporated various items in its statement of

comprehensive income during the year. Firstly, it is observable that there are

significant movements in the equity reserves of the company. Secondly, it is

observable that the fair value of income taxes and hedges of cash flow have

also witnessed potential movements during the year (Kieso et. al, 2010).

Thirdly, it is also notable that the company has disclosed its attempt of foreign

currency translation and income taxes on a whole.

vii. The company has appropriately highlighted the fact that many revenues and

expenses have been failed to be realized by it during the year and the same has

been portrayed in the comprehensive income statement. This highlights the

fact that after realization of these aspects by the company, losses or gains

arising as a result of these will be progressed towards recognition and will be

displayed under the head recognized losses and gains. Thereafter, it is

observable that the same forms part or is adequately disclosed by the company

in its statement of income. Moreover, the company has also reflected that there

are unrealized sales during the year and that has accommodated in its

comprehensive income statement. Nevertheless, if such income had formed

part of the income statement of Woolworths, it will highlight the fact that such

income has not been realized yet (Woolworths limited, 2017). Moreover, as

per the principles or requirements provided by GAAP and IFRS standards, the

company’s net salaries must be properly depicted by it in its financial

statements so that it can be portrayed that there are higher feasibilities of

income that can be accrued in the upcoming time. Overall, these segments

must find place outsides the company’s financial statements (income

statement) and the reason behind this can be attributed to the fact that such

7

activities that has resulted in the decline of such segment as well.

v. Insight on such analysis

It is observable from the cash flow statement of the company that it has witnessed

enhancements in its cash equivalent and cash at the end of the year that sheds light on growth

and development on its part.

Comprehensive statement of income

vi. The company has incorporated various items in its statement of

comprehensive income during the year. Firstly, it is observable that there are

significant movements in the equity reserves of the company. Secondly, it is

observable that the fair value of income taxes and hedges of cash flow have

also witnessed potential movements during the year (Kieso et. al, 2010).

Thirdly, it is also notable that the company has disclosed its attempt of foreign

currency translation and income taxes on a whole.

vii. The company has appropriately highlighted the fact that many revenues and

expenses have been failed to be realized by it during the year and the same has

been portrayed in the comprehensive income statement. This highlights the

fact that after realization of these aspects by the company, losses or gains

arising as a result of these will be progressed towards recognition and will be

displayed under the head recognized losses and gains. Thereafter, it is

observable that the same forms part or is adequately disclosed by the company

in its statement of income. Moreover, the company has also reflected that there

are unrealized sales during the year and that has accommodated in its

comprehensive income statement. Nevertheless, if such income had formed

part of the income statement of Woolworths, it will highlight the fact that such

income has not been realized yet (Woolworths limited, 2017). Moreover, as

per the principles or requirements provided by GAAP and IFRS standards, the

company’s net salaries must be properly depicted by it in its financial

statements so that it can be portrayed that there are higher feasibilities of

income that can be accrued in the upcoming time. Overall, these segments

must find place outsides the company’s financial statements (income

statement) and the reason behind this can be attributed to the fact that such

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

income can be referred as that income which the company has not even

realized in the present scenario.

The aspects or elements that have been disclosed by the company in the previous discussion,

if these were disclosed in the financials, it would cause the attributable profits of the

shareholders to decline. The most important reason behind this issue can be because the

aggregate impact of these transactions can play a major role in the creation of potential losses

on the part of the company and therefore, the shareholders will encounter a major decline in

their attributable profits (Deegan, 2011). Moreover, this sheds light on the fact that the same

will become an ineffective treatment on the company’s affairs and this is because there are

major gains or losses that have been arising owing to the extraordinary transactions that have

not been so particular as their occurrence. Furthermore, this also sheds light on the fact that it

is efficient and appropriate to disclose these amounts outside the scope of the financial

statements of the company.’

viii. The elements that have formed part of the company’s comprehensive

statement of income have not gone through the realization process. In other

words, such items have not been attained in the current year and are yet to be

realized. This highlights the fact that the company has been incapable of

determining that these transactions possess the most feasibility of occurrence

during the year. Besides, these transactions also play a vital role in the

assessment of future feasibility of the company in relation to its statement of

income. Nevertheless, it is already known that a company’s statement of

income can allow users in determining whether it has been capable of

maintaining its financial position during the year.

ix. It has been observed in the case of Seafarms group Limited that there are no

comprehensive incomes during the previous year that can be considered in

order to analyze the differences are the common aspect between the two

companies. Also, there were many items that were detected under the

comprehensive income statements of Woolworths group Limited:

The increase in the exchange of foreign currency differences have also leaded

to an increase in the cost of international operations. They have not planned

transactions because of which the firm can face loss and also they are recorded

outside the income statement because of their short-term nature.

8

realized in the present scenario.

The aspects or elements that have been disclosed by the company in the previous discussion,

if these were disclosed in the financials, it would cause the attributable profits of the

shareholders to decline. The most important reason behind this issue can be because the

aggregate impact of these transactions can play a major role in the creation of potential losses

on the part of the company and therefore, the shareholders will encounter a major decline in

their attributable profits (Deegan, 2011). Moreover, this sheds light on the fact that the same

will become an ineffective treatment on the company’s affairs and this is because there are

major gains or losses that have been arising owing to the extraordinary transactions that have

not been so particular as their occurrence. Furthermore, this also sheds light on the fact that it

is efficient and appropriate to disclose these amounts outside the scope of the financial

statements of the company.’

viii. The elements that have formed part of the company’s comprehensive

statement of income have not gone through the realization process. In other

words, such items have not been attained in the current year and are yet to be

realized. This highlights the fact that the company has been incapable of

determining that these transactions possess the most feasibility of occurrence

during the year. Besides, these transactions also play a vital role in the

assessment of future feasibility of the company in relation to its statement of

income. Nevertheless, it is already known that a company’s statement of

income can allow users in determining whether it has been capable of

maintaining its financial position during the year.

ix. It has been observed in the case of Seafarms group Limited that there are no

comprehensive incomes during the previous year that can be considered in

order to analyze the differences are the common aspect between the two

companies. Also, there were many items that were detected under the

comprehensive income statements of Woolworths group Limited:

The increase in the exchange of foreign currency differences have also leaded

to an increase in the cost of international operations. They have not planned

transactions because of which the firm can face loss and also they are recorded

outside the income statement because of their short-term nature.

8

A rise indicating instrument has been noticed because of the revaluation of

equity securities invested by the organization. Their disposal will lead idea to

gain or loss to the form that will be further transferred to the equity.

The cash flow hedge is depicted using the effective gain or loss of the

derivative financial instrument.

Recognition of actuarial gains and losses can be made on the net defined

benefit liability for the protocol financial year in which they occur with the

help of the comprehensive income statement. They are not generally

reclassified into the income statement (Davies & Crawford, 2012).

• Cash flow hedge is shown about the effective gain or loss on the derivative

financial instrument.

• The company recognises the actuarial gains or losses on the net defined benefit

liability in the year when they occur and are shown in the comprehensive income

statement. These do not get reclassified to Income Statement.

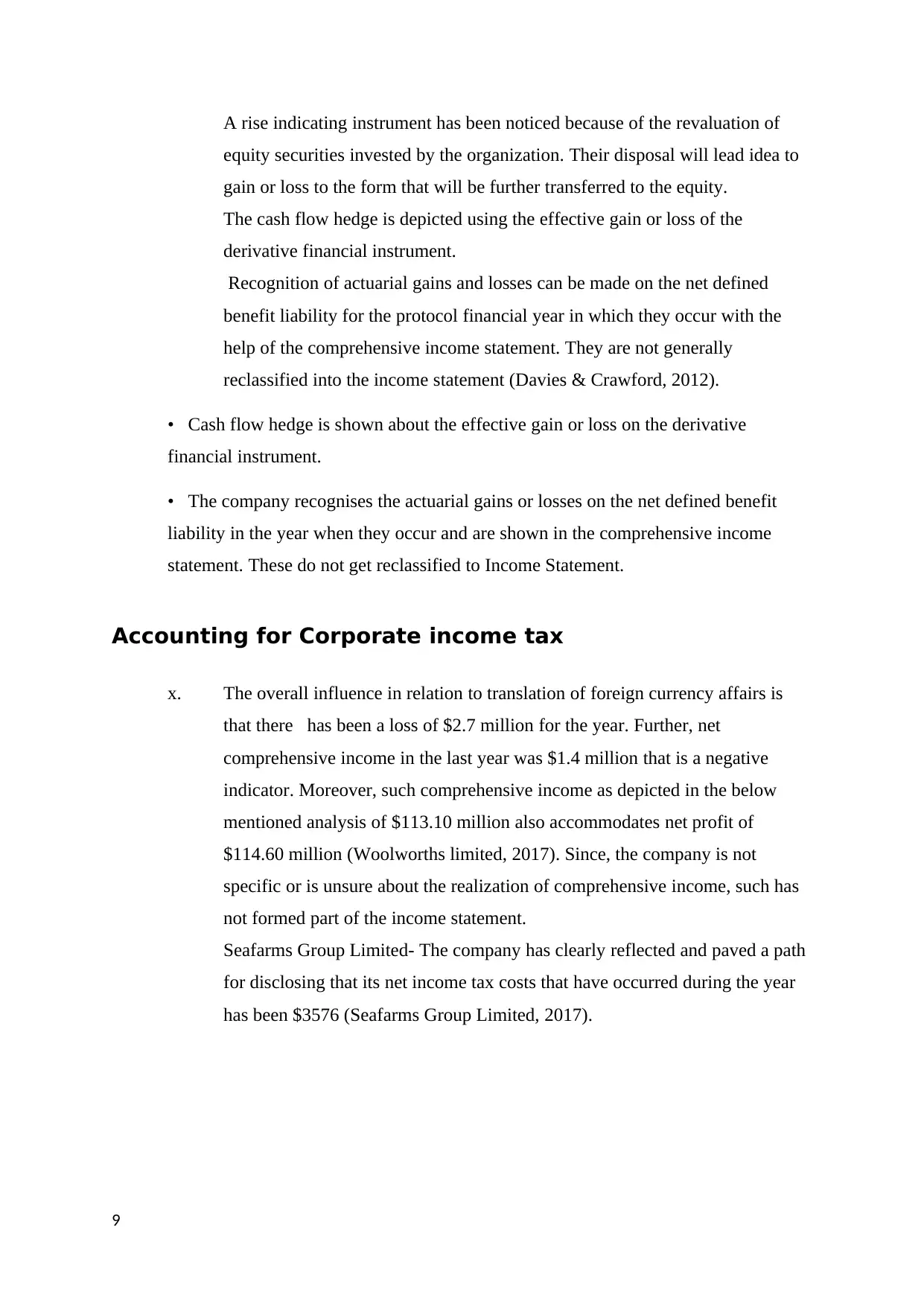

Accounting for Corporate income tax

x. The overall influence in relation to translation of foreign currency affairs is

that there has been a loss of $2.7 million for the year. Further, net

comprehensive income in the last year was $1.4 million that is a negative

indicator. Moreover, such comprehensive income as depicted in the below

mentioned analysis of $113.10 million also accommodates net profit of

$114.60 million (Woolworths limited, 2017). Since, the company is not

specific or is unsure about the realization of comprehensive income, such has

not formed part of the income statement.

Seafarms Group Limited- The company has clearly reflected and paved a path

for disclosing that its net income tax costs that have occurred during the year

has been $3576 (Seafarms Group Limited, 2017).

9

equity securities invested by the organization. Their disposal will lead idea to

gain or loss to the form that will be further transferred to the equity.

The cash flow hedge is depicted using the effective gain or loss of the

derivative financial instrument.

Recognition of actuarial gains and losses can be made on the net defined

benefit liability for the protocol financial year in which they occur with the

help of the comprehensive income statement. They are not generally

reclassified into the income statement (Davies & Crawford, 2012).

• Cash flow hedge is shown about the effective gain or loss on the derivative

financial instrument.

• The company recognises the actuarial gains or losses on the net defined benefit

liability in the year when they occur and are shown in the comprehensive income

statement. These do not get reclassified to Income Statement.

Accounting for Corporate income tax

x. The overall influence in relation to translation of foreign currency affairs is

that there has been a loss of $2.7 million for the year. Further, net

comprehensive income in the last year was $1.4 million that is a negative

indicator. Moreover, such comprehensive income as depicted in the below

mentioned analysis of $113.10 million also accommodates net profit of

$114.60 million (Woolworths limited, 2017). Since, the company is not

specific or is unsure about the realization of comprehensive income, such has

not formed part of the income statement.

Seafarms Group Limited- The company has clearly reflected and paved a path

for disclosing that its net income tax costs that have occurred during the year

has been $3576 (Seafarms Group Limited, 2017).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

xi. The net costs related to tax have been disclosed by the company in its

financials and is being reflected at $718 during the year (Woolworths limited,

2017). Besides, this was $651 million in the previous year. Moreover, the

company’s tax expenses in association with its activities that have been

discontinued have been disclosed at an amount of $74 million.

Seafarms Group Limited-

From the financials, the company has disclosed its PBT to be in negative figure that is

in losses and the income tax costs have been reflected at $3576. In addition, the

effective rate of tax that has been portrayed by the company has arrived at thirty

percent respectively. This clearly depicts that such segment is equivalent betwixt both

the companies.

xii. Computation of effective rate of tax

This can be computed by dividing the company’s income tax costs with its profit before tax

and therefore, since the income tax costs have stood at $714 million in the present year and

profit before tax stood at $2394 million, the effective rate of tax shall come at 30% after

dividing the same. Further, it is notable from the previously mentioned evaluation that there

is a significant deterioration in the company’s deferred tax assets because of mass changes in

time in relation to its liabilities and assets (Peirson et. al, 2015). However, no change is

observable in the scenario of Seafarms Ltd as the same has been reported as nil in both the

years.

10

financials and is being reflected at $718 during the year (Woolworths limited,

2017). Besides, this was $651 million in the previous year. Moreover, the

company’s tax expenses in association with its activities that have been

discontinued have been disclosed at an amount of $74 million.

Seafarms Group Limited-

From the financials, the company has disclosed its PBT to be in negative figure that is

in losses and the income tax costs have been reflected at $3576. In addition, the

effective rate of tax that has been portrayed by the company has arrived at thirty

percent respectively. This clearly depicts that such segment is equivalent betwixt both

the companies.

xii. Computation of effective rate of tax

This can be computed by dividing the company’s income tax costs with its profit before tax

and therefore, since the income tax costs have stood at $714 million in the present year and

profit before tax stood at $2394 million, the effective rate of tax shall come at 30% after

dividing the same. Further, it is notable from the previously mentioned evaluation that there

is a significant deterioration in the company’s deferred tax assets because of mass changes in

time in relation to its liabilities and assets (Peirson et. al, 2015). However, no change is

observable in the scenario of Seafarms Ltd as the same has been reported as nil in both the

years.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Seafarms Group Limited-

Seafarms group Limited depicted a blank balance for the deferred assets in the balance sheet

for the year 2018. The basic function of the deferred tax is to calculate and record the

temporary differences that are present between the assets and liabilities of a company so that

the purpose of transaction recording and taxation can be fulfilled for financial reporting

systems. The differences have been settled in the same financial year itself (Seafarms Group

Limited, 2017).

xiii. Computation of cash tax of Woolworths

Provision of net tax = ($718m)

Decrease in deferred tax assets- $90m

(-) provisions of DTA and accruals- ($44m)

Decrease in deferred tax liabilities = $11m

Therefore, cash tax= $661 m

xiv. It can be noted that the cash tax rate of an organization can be calculated by

dividing its cash tax by its PBT that has incurred during the year. In relation to

Seafarms, the company’s cash tax amount has arrived at 30% but the effective

tax rate of Woolworths has arrived at 27.61% (Woolworths limited, 2017).

This highlights the fact that Seafarms’ effective tax rate is better than that of

Woolworths Ltd (Merchant, 2012).

Seafarms Group Limited:

Provision of tax – ($3576)

Decrease or increase in company’s deferred tax assets- Nil

Less: DTA accruals and provisions during the year - Nil

Net decrease or increase in company’s deferred tax liabilities- Nil

Cash Tax value is equal to- $3576

11

Seafarms group Limited depicted a blank balance for the deferred assets in the balance sheet

for the year 2018. The basic function of the deferred tax is to calculate and record the

temporary differences that are present between the assets and liabilities of a company so that

the purpose of transaction recording and taxation can be fulfilled for financial reporting

systems. The differences have been settled in the same financial year itself (Seafarms Group

Limited, 2017).

xiii. Computation of cash tax of Woolworths

Provision of net tax = ($718m)

Decrease in deferred tax assets- $90m

(-) provisions of DTA and accruals- ($44m)

Decrease in deferred tax liabilities = $11m

Therefore, cash tax= $661 m

xiv. It can be noted that the cash tax rate of an organization can be calculated by

dividing its cash tax by its PBT that has incurred during the year. In relation to

Seafarms, the company’s cash tax amount has arrived at 30% but the effective

tax rate of Woolworths has arrived at 27.61% (Woolworths limited, 2017).

This highlights the fact that Seafarms’ effective tax rate is better than that of

Woolworths Ltd (Merchant, 2012).

Seafarms Group Limited:

Provision of tax – ($3576)

Decrease or increase in company’s deferred tax assets- Nil

Less: DTA accruals and provisions during the year - Nil

Net decrease or increase in company’s deferred tax liabilities- Nil

Cash Tax value is equal to- $3576

11

xv. The amount of cash tax of a company can be ascertained by evaluating their

amount of book tax as depicted in the income tax return and any other

alterations that can be observed in the deferred assets and deferred liabilities

must be also evaluated for the same. Furthermore, users of the company can

utilize such amount to attain self-interest objectives. Besides, such deferred tax

liabilities and assets are also depicted by the company in the annual report so

that the actual payable tax can be determined. In addition, the company has

also disclosed its liability of income tax although it can be undertaken in the

coming reporting period (Gowthrope, 2011).

xvi. both book tax and cash tax are distinct in nature owing to the presence of

deferred tax liabilities and assets together with all the provisions that are

designed for the liabilities of income tax (Madura & Fox, 2011).

12

amount of book tax as depicted in the income tax return and any other

alterations that can be observed in the deferred assets and deferred liabilities

must be also evaluated for the same. Furthermore, users of the company can

utilize such amount to attain self-interest objectives. Besides, such deferred tax

liabilities and assets are also depicted by the company in the annual report so

that the actual payable tax can be determined. In addition, the company has

also disclosed its liability of income tax although it can be undertaken in the

coming reporting period (Gowthrope, 2011).

xvi. both book tax and cash tax are distinct in nature owing to the presence of

deferred tax liabilities and assets together with all the provisions that are

designed for the liabilities of income tax (Madura & Fox, 2011).

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.