Corporate Accounting Report: Financial Reporting and Equity Analysis

VerifiedAdded on 2023/06/04

|14

|2590

|456

Report

AI Summary

This report provides a comprehensive overview of corporate accounting, focusing on the relevance of International Financial Reporting Standards (IFRS) and the role of the Australian Accounting Standards Board (AASB). It examines voluntary disclosure practices and the importance of IFRS in ensuring transparency and comparability in financial reporting. The report delves into the analysis of equity components, including issued capital, retained earnings, and reserves, for four companies listed on the Australian Securities Exchange: Ramsay Health Care Limited, Capitol Health Limited, SDI Ltd, and Virtus Health Limited. Furthermore, it compares the debt-to-equity ratios of these companies, providing insights into their financial stability. The report concludes with a summary of findings, emphasizing the importance of adhering to financial accounting and reporting frameworks for effective corporate governance.

1

Corporate Accounting

Corporate Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Executive Summary

Today, the pace and impact of globalization have created a stronger connectivity among the

financial markets at international level. As a result, it has become necessary for the companies to

strictly comply with the international accounting standards while preparing their financial

statements. The IFRS has established a series of regulations and codes which are applicable to

the framework of corporate reporting for every country to disclose their material information.

From the report, it has been found that a sound corporate reporting system facilitates economic

development of a country by reinforcing shareholders' confidence and enhancing transparency,

comparability as well as financial stability. Moreover, it was observed that an effective reporting

structure also enables worldwide sharing of financial resources along with economy integration.

AASB also supports this for minimizing mis-utilization of resources, and corruption. In addition,

the AASB has also been found to promote compliance and that that management should not be

provided absolute freedom to decide what accounting information should be incorporated in the

financial statements in order to control information irregularity.

Executive Summary

Today, the pace and impact of globalization have created a stronger connectivity among the

financial markets at international level. As a result, it has become necessary for the companies to

strictly comply with the international accounting standards while preparing their financial

statements. The IFRS has established a series of regulations and codes which are applicable to

the framework of corporate reporting for every country to disclose their material information.

From the report, it has been found that a sound corporate reporting system facilitates economic

development of a country by reinforcing shareholders' confidence and enhancing transparency,

comparability as well as financial stability. Moreover, it was observed that an effective reporting

structure also enables worldwide sharing of financial resources along with economy integration.

AASB also supports this for minimizing mis-utilization of resources, and corruption. In addition,

the AASB has also been found to promote compliance and that that management should not be

provided absolute freedom to decide what accounting information should be incorporated in the

financial statements in order to control information irregularity.

3

Table of Contents

Introduction......................................................................................................................................3

Financial Reporting and Voluntary Disclosure...............................................................................4

AASB & IASB................................................................................................................................5

Participation of AASB in setting IFRS........................................................................................5

Non-compulsion of IFRS for IASB members..............................................................................6

Discussion on items of equity..........................................................................................................8

Comparison of debt and equity for the four companies................................................................10

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

Table of Contents

Introduction......................................................................................................................................3

Financial Reporting and Voluntary Disclosure...............................................................................4

AASB & IASB................................................................................................................................5

Participation of AASB in setting IFRS........................................................................................5

Non-compulsion of IFRS for IASB members..............................................................................6

Discussion on items of equity..........................................................................................................8

Comparison of debt and equity for the four companies................................................................10

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Introduction

The following report is designed to provide an understanding of corporate accounting concepts

and its relevance for companies in the preparation and disclosure of their financial statements.

The report discusses the relevance of disclosing financial information by the managers as per

IFRS or voluntarily. Along with this, emphasize has been made on the role of AASB in the

setting process of IFRS on global level, and the reasons why the associate countries of IASB are

not required to follow the IFRS framework. In this context, the report also analyses the financial

statements, and debt-equity position of four companies listed on Australian Securities Exchange:

Ransay healthcare limited, Capitil health limited, SDI limited and Vtrus Health Limited.

Introduction

The following report is designed to provide an understanding of corporate accounting concepts

and its relevance for companies in the preparation and disclosure of their financial statements.

The report discusses the relevance of disclosing financial information by the managers as per

IFRS or voluntarily. Along with this, emphasize has been made on the role of AASB in the

setting process of IFRS on global level, and the reasons why the associate countries of IASB are

not required to follow the IFRS framework. In this context, the report also analyses the financial

statements, and debt-equity position of four companies listed on Australian Securities Exchange:

Ransay healthcare limited, Capitil health limited, SDI limited and Vtrus Health Limited.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

Financial Reporting and Voluntary Disclosure

Voluntary disclosure of financial information refers to the practice of incorporating information

by the companies' management outside the principles of International Financial Reporting

Structure (IFRS), and Securities Exchange Commission requirements. Many companies believe

that voluntary disclosure is relevant for enabling effective decision making by the users of

financial statements (Newberry, 2015). Managers also adopts voluntary disclosure in addition to

the mandatory reporting system in order to communicate their entity's performance to the

stakeholders.

However, in comparison to voluntary disclosure, IFRS reporting principles proves to be more

systematic and authentic. The true and fair scenario of a company's performance sometimes

become hard to determine when managers follow voluntary disclosure system thereby hurting

the decision making process of the customers, banks, government and the society as a whole.

When annual reports are prepared by the managers according to IFRS rules, it enables them to

give more relevant and timely information to the investors for predicting future income.

Moreover, the adoption of voluntary disclosure of information may lead to presentation of

manipulated information by the management, resulting in inaccurate picture of financial state of

the entity, no exemption from liabilities, increased cost, reputation harm, and penalties for the

undisclosed details in the reports (Newberry, 2015).

In addition to this, the growing complexity and volume of financial statements in today's

competitive businesses, the risk of non-uniformity in the information and exclusion of material

items in the annual reports is high. IFRS facilitates managers to comply effectively with the

Financial Reporting and Voluntary Disclosure

Voluntary disclosure of financial information refers to the practice of incorporating information

by the companies' management outside the principles of International Financial Reporting

Structure (IFRS), and Securities Exchange Commission requirements. Many companies believe

that voluntary disclosure is relevant for enabling effective decision making by the users of

financial statements (Newberry, 2015). Managers also adopts voluntary disclosure in addition to

the mandatory reporting system in order to communicate their entity's performance to the

stakeholders.

However, in comparison to voluntary disclosure, IFRS reporting principles proves to be more

systematic and authentic. The true and fair scenario of a company's performance sometimes

become hard to determine when managers follow voluntary disclosure system thereby hurting

the decision making process of the customers, banks, government and the society as a whole.

When annual reports are prepared by the managers according to IFRS rules, it enables them to

give more relevant and timely information to the investors for predicting future income.

Moreover, the adoption of voluntary disclosure of information may lead to presentation of

manipulated information by the management, resulting in inaccurate picture of financial state of

the entity, no exemption from liabilities, increased cost, reputation harm, and penalties for the

undisclosed details in the reports (Newberry, 2015).

In addition to this, the growing complexity and volume of financial statements in today's

competitive businesses, the risk of non-uniformity in the information and exclusion of material

items in the annual reports is high. IFRS facilitates managers to comply effectively with the

6

accounting standards and other relevant laws . IFRS acts as a common international language for

discussing business matters in a comparable and understandable form throughout the worldwide

boundaries. Furthermore, the adoption of IFRS is important for managers while dealing with

numerous countries to increase global trade and shareholding (Hellman et al., 2018). The

principles of IFRS develop a set of clear, cost-effective, and high quality information which is

enforceable and accepted at the global level.

AASB & IASB

Participation of AASB in setting IFRS

The policies and procedures of Australian Accounting Standards Board (AASB) define the

functions and powers of AASB. It sets out the nature and type of financial statements to be made

by the companies required to report as per the guidelines issued by Australian Accounting

Standards. The AASB also takes part in ensuring the appropriateness of the proposed standards

for various kinds of companies in accordance with the Australian Securities and Investments

Commission Act 2001 (Ipino, and Parbonetti, 2017). In addition to this, the AASB also confirms

the development, issuance and maintenance of external guidance and standards, along with the

Australian based rules that fulfill the user needs and improve the consistency of external

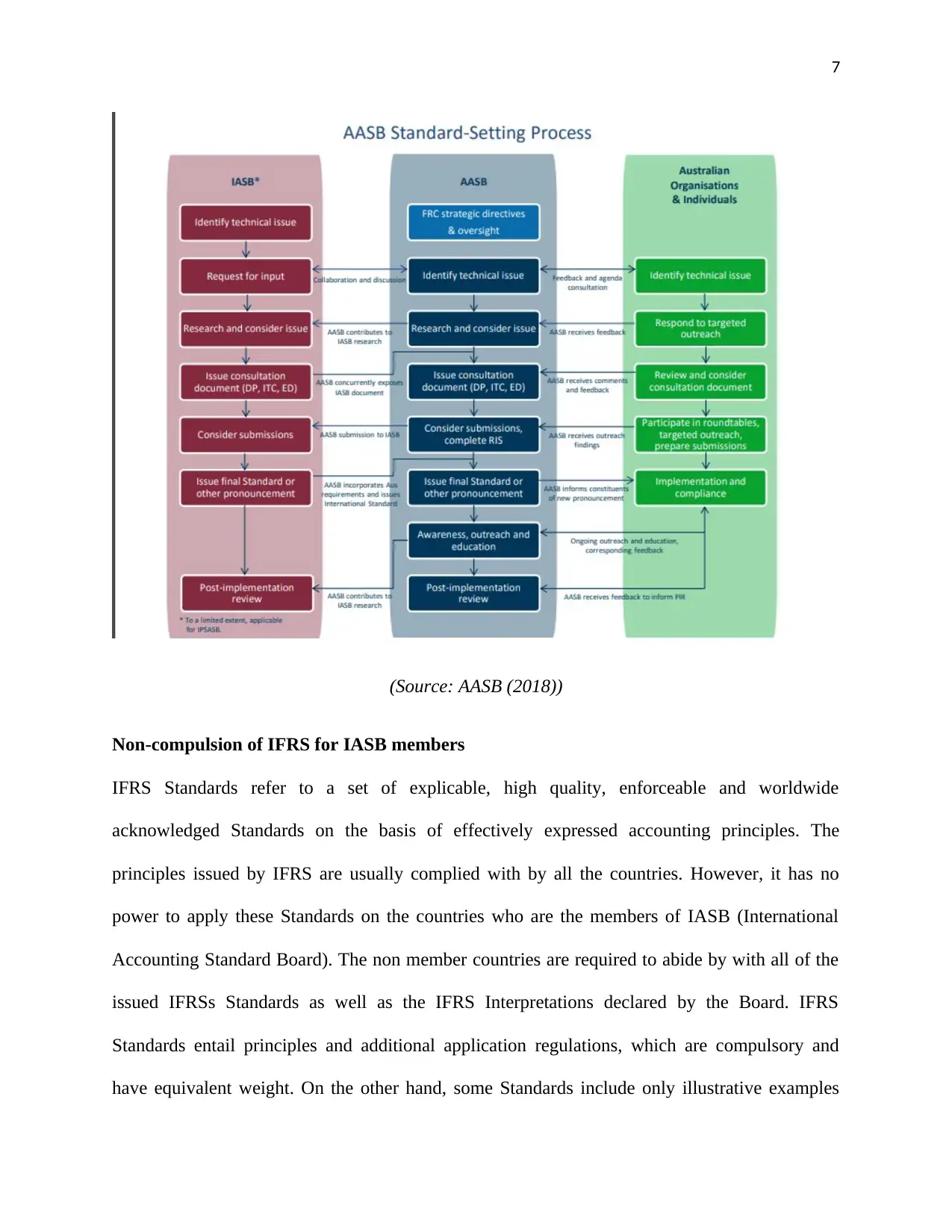

reporting and its quality. The underneath diagram provides the process of the standard-setting

process.

accounting standards and other relevant laws . IFRS acts as a common international language for

discussing business matters in a comparable and understandable form throughout the worldwide

boundaries. Furthermore, the adoption of IFRS is important for managers while dealing with

numerous countries to increase global trade and shareholding (Hellman et al., 2018). The

principles of IFRS develop a set of clear, cost-effective, and high quality information which is

enforceable and accepted at the global level.

AASB & IASB

Participation of AASB in setting IFRS

The policies and procedures of Australian Accounting Standards Board (AASB) define the

functions and powers of AASB. It sets out the nature and type of financial statements to be made

by the companies required to report as per the guidelines issued by Australian Accounting

Standards. The AASB also takes part in ensuring the appropriateness of the proposed standards

for various kinds of companies in accordance with the Australian Securities and Investments

Commission Act 2001 (Ipino, and Parbonetti, 2017). In addition to this, the AASB also confirms

the development, issuance and maintenance of external guidance and standards, along with the

Australian based rules that fulfill the user needs and improve the consistency of external

reporting and its quality. The underneath diagram provides the process of the standard-setting

process.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

(Source: AASB (2018))

Non-compulsion of IFRS for IASB members

IFRS Standards refer to a set of explicable, high quality, enforceable and worldwide

acknowledged Standards on the basis of effectively expressed accounting principles. The

principles issued by IFRS are usually complied with by all the countries. However, it has no

power to apply these Standards on the countries who are the members of IASB (International

Accounting Standard Board). The non member countries are required to abide by with all of the

issued IFRSs Standards as well as the IFRS Interpretations declared by the Board. IFRS

Standards entail principles and additional application regulations, which are compulsory and

have equivalent weight. On the other hand, some Standards include only illustrative examples

(Source: AASB (2018))

Non-compulsion of IFRS for IASB members

IFRS Standards refer to a set of explicable, high quality, enforceable and worldwide

acknowledged Standards on the basis of effectively expressed accounting principles. The

principles issued by IFRS are usually complied with by all the countries. However, it has no

power to apply these Standards on the countries who are the members of IASB (International

Accounting Standard Board). The non member countries are required to abide by with all of the

issued IFRSs Standards as well as the IFRS Interpretations declared by the Board. IFRS

Standards entail principles and additional application regulations, which are compulsory and

have equivalent weight. On the other hand, some Standards include only illustrative examples

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

which are not mandatory for the member countries of IASB. In addition to this, some Standards

and Interpretation provide just the conclusions for fulfilling the particular requirements.

Therefore, these are also not compulsory for the member countries of IASB (Hellman et al.,

2018). Apart from this, the reliability and accuracy of the financial statements made by the

member countries automatically go through the processes of IFRS, which does not force them to

comply with the IFRS.

which are not mandatory for the member countries of IASB. In addition to this, some Standards

and Interpretation provide just the conclusions for fulfilling the particular requirements.

Therefore, these are also not compulsory for the member countries of IASB (Hellman et al.,

2018). Apart from this, the reliability and accuracy of the financial statements made by the

member countries automatically go through the processes of IFRS, which does not force them to

comply with the IFRS.

9

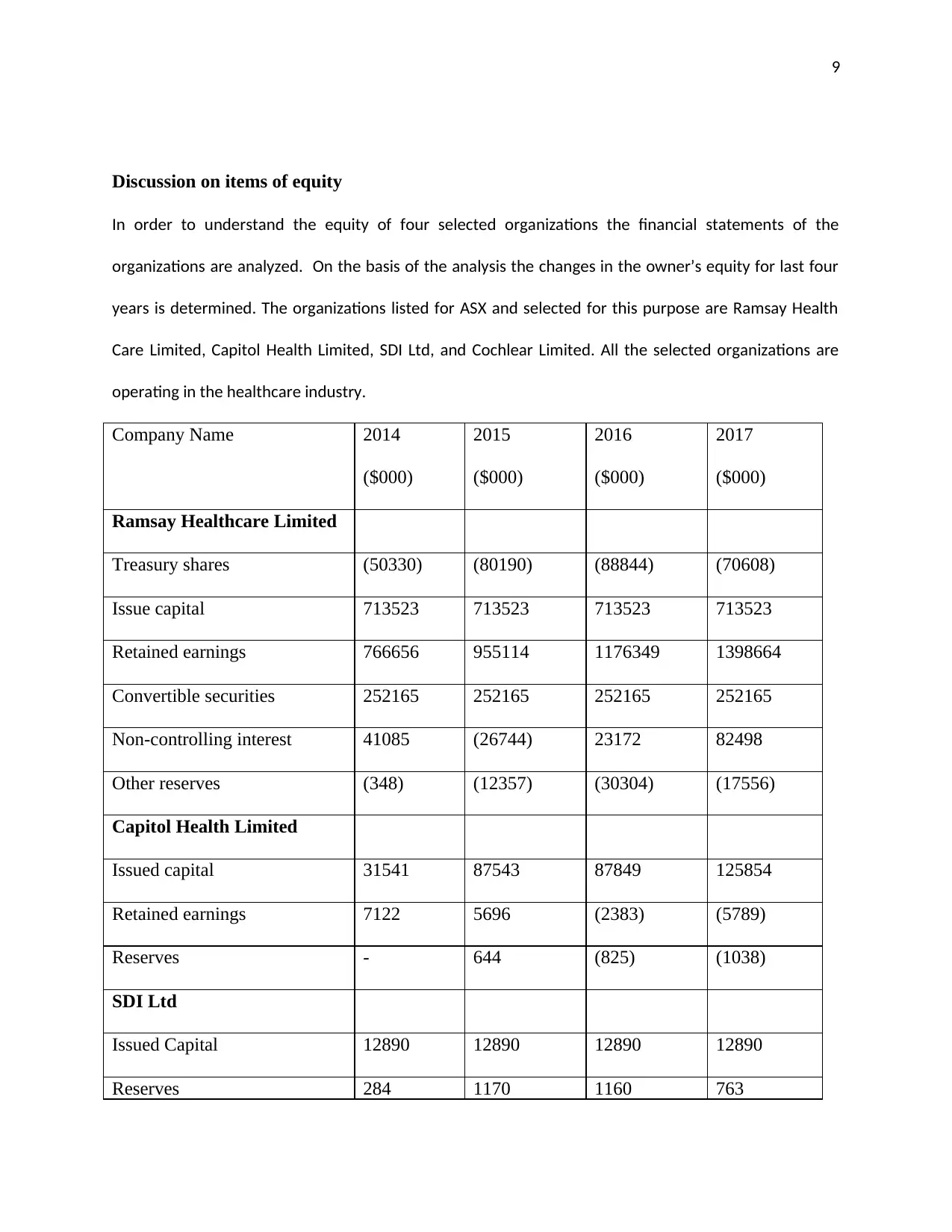

Discussion on items of equity

In order to understand the equity of four selected organizations the financial statements of the

organizations are analyzed. On the basis of the analysis the changes in the owner’s equity for last four

years is determined. The organizations listed for ASX and selected for this purpose are Ramsay Health

Care Limited, Capitol Health Limited, SDI Ltd, and Cochlear Limited. All the selected organizations are

operating in the healthcare industry.

Company Name 2014

($000)

2015

($000)

2016

($000)

2017

($000)

Ramsay Healthcare Limited

Treasury shares (50330) (80190) (88844) (70608)

Issue capital 713523 713523 713523 713523

Retained earnings 766656 955114 1176349 1398664

Convertible securities 252165 252165 252165 252165

Non-controlling interest 41085 (26744) 23172 82498

Other reserves (348) (12357) (30304) (17556)

Capitol Health Limited

Issued capital 31541 87543 87849 125854

Retained earnings 7122 5696 (2383) (5789)

Reserves - 644 (825) (1038)

SDI Ltd

Issued Capital 12890 12890 12890 12890

Reserves 284 1170 1160 763

Discussion on items of equity

In order to understand the equity of four selected organizations the financial statements of the

organizations are analyzed. On the basis of the analysis the changes in the owner’s equity for last four

years is determined. The organizations listed for ASX and selected for this purpose are Ramsay Health

Care Limited, Capitol Health Limited, SDI Ltd, and Cochlear Limited. All the selected organizations are

operating in the healthcare industry.

Company Name 2014

($000)

2015

($000)

2016

($000)

2017

($000)

Ramsay Healthcare Limited

Treasury shares (50330) (80190) (88844) (70608)

Issue capital 713523 713523 713523 713523

Retained earnings 766656 955114 1176349 1398664

Convertible securities 252165 252165 252165 252165

Non-controlling interest 41085 (26744) 23172 82498

Other reserves (348) (12357) (30304) (17556)

Capitol Health Limited

Issued capital 31541 87543 87849 125854

Retained earnings 7122 5696 (2383) (5789)

Reserves - 644 (825) (1038)

SDI Ltd

Issued Capital 12890 12890 12890 12890

Reserves 284 1170 1160 763

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

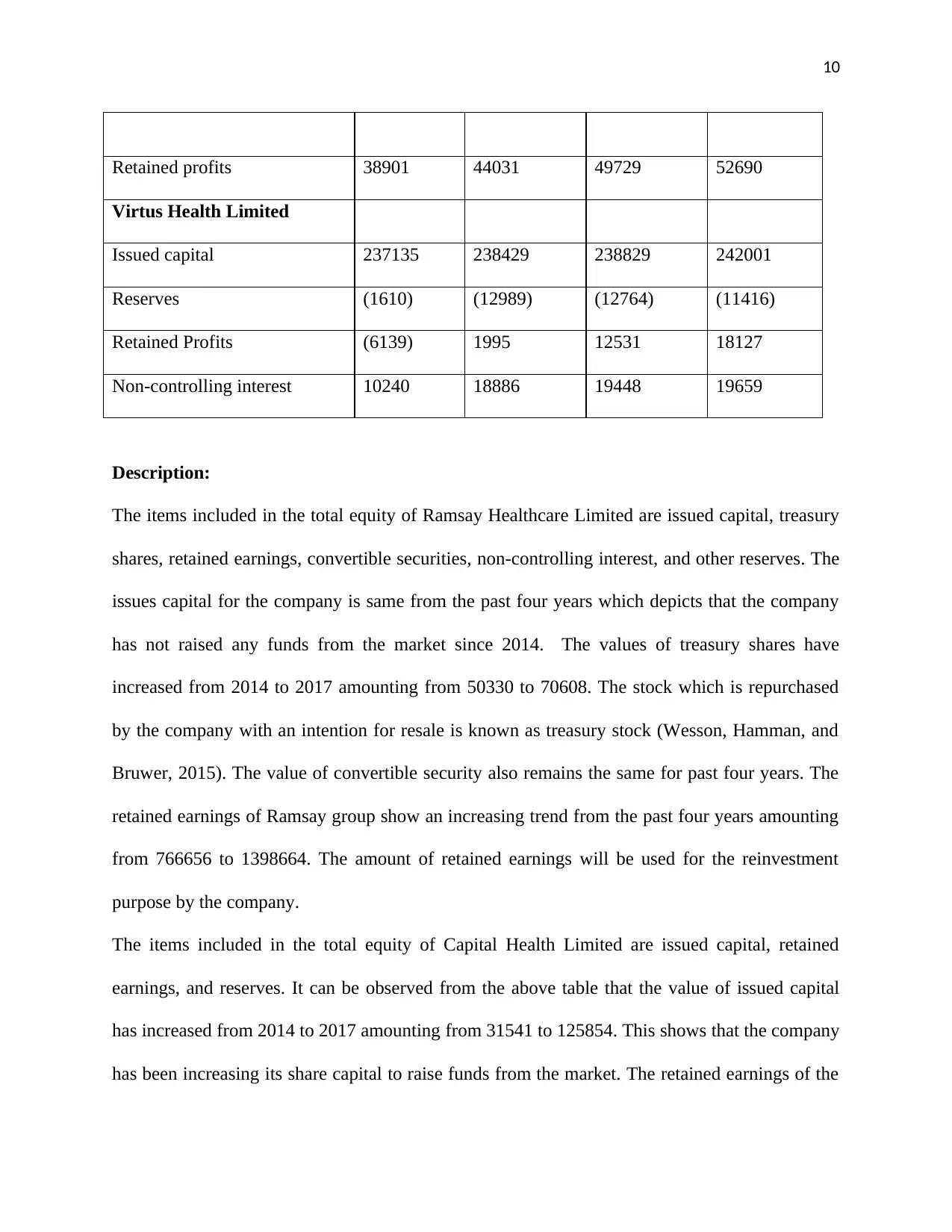

Retained profits 38901 44031 49729 52690

Virtus Health Limited

Issued capital 237135 238429 238829 242001

Reserves (1610) (12989) (12764) (11416)

Retained Profits (6139) 1995 12531 18127

Non-controlling interest 10240 18886 19448 19659

Description:

The items included in the total equity of Ramsay Healthcare Limited are issued capital, treasury

shares, retained earnings, convertible securities, non-controlling interest, and other reserves. The

issues capital for the company is same from the past four years which depicts that the company

has not raised any funds from the market since 2014. The values of treasury shares have

increased from 2014 to 2017 amounting from 50330 to 70608. The stock which is repurchased

by the company with an intention for resale is known as treasury stock (Wesson, Hamman, and

Bruwer, 2015). The value of convertible security also remains the same for past four years. The

retained earnings of Ramsay group show an increasing trend from the past four years amounting

from 766656 to 1398664. The amount of retained earnings will be used for the reinvestment

purpose by the company.

The items included in the total equity of Capital Health Limited are issued capital, retained

earnings, and reserves. It can be observed from the above table that the value of issued capital

has increased from 2014 to 2017 amounting from 31541 to 125854. This shows that the company

has been increasing its share capital to raise funds from the market. The retained earnings of the

Retained profits 38901 44031 49729 52690

Virtus Health Limited

Issued capital 237135 238429 238829 242001

Reserves (1610) (12989) (12764) (11416)

Retained Profits (6139) 1995 12531 18127

Non-controlling interest 10240 18886 19448 19659

Description:

The items included in the total equity of Ramsay Healthcare Limited are issued capital, treasury

shares, retained earnings, convertible securities, non-controlling interest, and other reserves. The

issues capital for the company is same from the past four years which depicts that the company

has not raised any funds from the market since 2014. The values of treasury shares have

increased from 2014 to 2017 amounting from 50330 to 70608. The stock which is repurchased

by the company with an intention for resale is known as treasury stock (Wesson, Hamman, and

Bruwer, 2015). The value of convertible security also remains the same for past four years. The

retained earnings of Ramsay group show an increasing trend from the past four years amounting

from 766656 to 1398664. The amount of retained earnings will be used for the reinvestment

purpose by the company.

The items included in the total equity of Capital Health Limited are issued capital, retained

earnings, and reserves. It can be observed from the above table that the value of issued capital

has increased from 2014 to 2017 amounting from 31541 to 125854. This shows that the company

has been increasing its share capital to raise funds from the market. The retained earnings of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

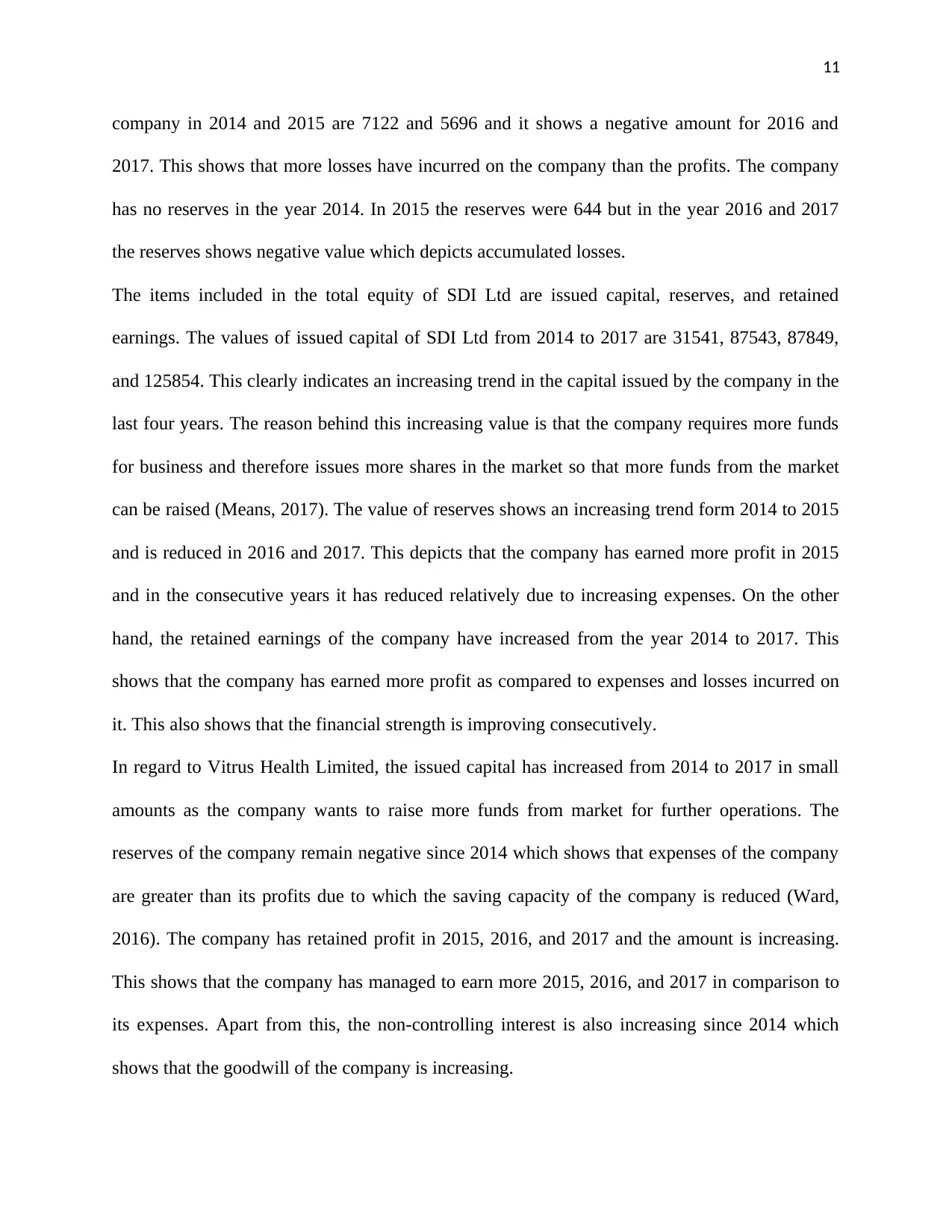

company in 2014 and 2015 are 7122 and 5696 and it shows a negative amount for 2016 and

2017. This shows that more losses have incurred on the company than the profits. The company

has no reserves in the year 2014. In 2015 the reserves were 644 but in the year 2016 and 2017

the reserves shows negative value which depicts accumulated losses.

The items included in the total equity of SDI Ltd are issued capital, reserves, and retained

earnings. The values of issued capital of SDI Ltd from 2014 to 2017 are 31541, 87543, 87849,

and 125854. This clearly indicates an increasing trend in the capital issued by the company in the

last four years. The reason behind this increasing value is that the company requires more funds

for business and therefore issues more shares in the market so that more funds from the market

can be raised (Means, 2017). The value of reserves shows an increasing trend form 2014 to 2015

and is reduced in 2016 and 2017. This depicts that the company has earned more profit in 2015

and in the consecutive years it has reduced relatively due to increasing expenses. On the other

hand, the retained earnings of the company have increased from the year 2014 to 2017. This

shows that the company has earned more profit as compared to expenses and losses incurred on

it. This also shows that the financial strength is improving consecutively.

In regard to Vitrus Health Limited, the issued capital has increased from 2014 to 2017 in small

amounts as the company wants to raise more funds from market for further operations. The

reserves of the company remain negative since 2014 which shows that expenses of the company

are greater than its profits due to which the saving capacity of the company is reduced (Ward,

2016). The company has retained profit in 2015, 2016, and 2017 and the amount is increasing.

This shows that the company has managed to earn more 2015, 2016, and 2017 in comparison to

its expenses. Apart from this, the non-controlling interest is also increasing since 2014 which

shows that the goodwill of the company is increasing.

company in 2014 and 2015 are 7122 and 5696 and it shows a negative amount for 2016 and

2017. This shows that more losses have incurred on the company than the profits. The company

has no reserves in the year 2014. In 2015 the reserves were 644 but in the year 2016 and 2017

the reserves shows negative value which depicts accumulated losses.

The items included in the total equity of SDI Ltd are issued capital, reserves, and retained

earnings. The values of issued capital of SDI Ltd from 2014 to 2017 are 31541, 87543, 87849,

and 125854. This clearly indicates an increasing trend in the capital issued by the company in the

last four years. The reason behind this increasing value is that the company requires more funds

for business and therefore issues more shares in the market so that more funds from the market

can be raised (Means, 2017). The value of reserves shows an increasing trend form 2014 to 2015

and is reduced in 2016 and 2017. This depicts that the company has earned more profit in 2015

and in the consecutive years it has reduced relatively due to increasing expenses. On the other

hand, the retained earnings of the company have increased from the year 2014 to 2017. This

shows that the company has earned more profit as compared to expenses and losses incurred on

it. This also shows that the financial strength is improving consecutively.

In regard to Vitrus Health Limited, the issued capital has increased from 2014 to 2017 in small

amounts as the company wants to raise more funds from market for further operations. The

reserves of the company remain negative since 2014 which shows that expenses of the company

are greater than its profits due to which the saving capacity of the company is reduced (Ward,

2016). The company has retained profit in 2015, 2016, and 2017 and the amount is increasing.

This shows that the company has managed to earn more 2015, 2016, and 2017 in comparison to

its expenses. Apart from this, the non-controlling interest is also increasing since 2014 which

shows that the goodwill of the company is increasing.

12

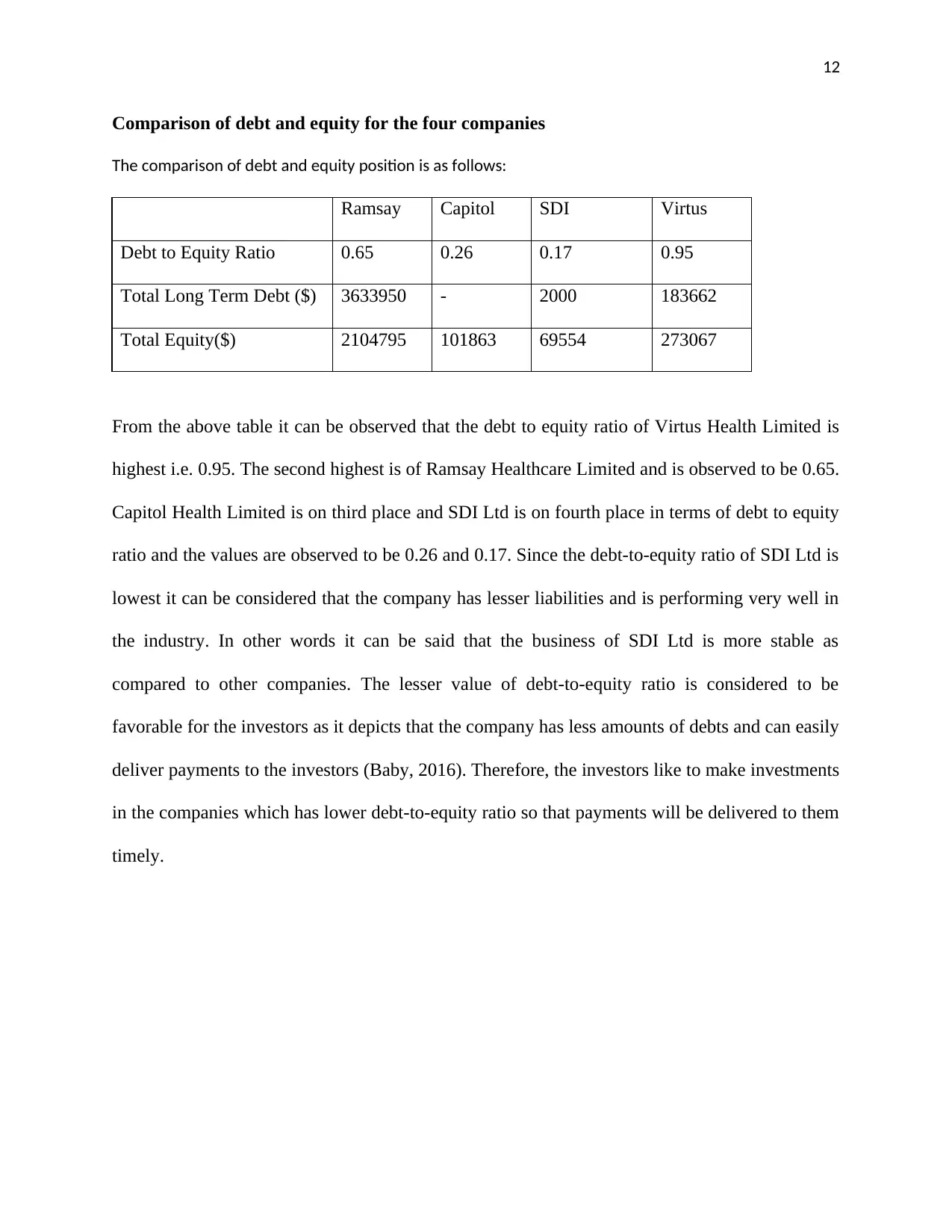

Comparison of debt and equity for the four companies

The comparison of debt and equity position is as follows:

Ramsay Capitol SDI Virtus

Debt to Equity Ratio 0.65 0.26 0.17 0.95

Total Long Term Debt ($) 3633950 - 2000 183662

Total Equity($) 2104795 101863 69554 273067

From the above table it can be observed that the debt to equity ratio of Virtus Health Limited is

highest i.e. 0.95. The second highest is of Ramsay Healthcare Limited and is observed to be 0.65.

Capitol Health Limited is on third place and SDI Ltd is on fourth place in terms of debt to equity

ratio and the values are observed to be 0.26 and 0.17. Since the debt-to-equity ratio of SDI Ltd is

lowest it can be considered that the company has lesser liabilities and is performing very well in

the industry. In other words it can be said that the business of SDI Ltd is more stable as

compared to other companies. The lesser value of debt-to-equity ratio is considered to be

favorable for the investors as it depicts that the company has less amounts of debts and can easily

deliver payments to the investors (Baby, 2016). Therefore, the investors like to make investments

in the companies which has lower debt-to-equity ratio so that payments will be delivered to them

timely.

Comparison of debt and equity for the four companies

The comparison of debt and equity position is as follows:

Ramsay Capitol SDI Virtus

Debt to Equity Ratio 0.65 0.26 0.17 0.95

Total Long Term Debt ($) 3633950 - 2000 183662

Total Equity($) 2104795 101863 69554 273067

From the above table it can be observed that the debt to equity ratio of Virtus Health Limited is

highest i.e. 0.95. The second highest is of Ramsay Healthcare Limited and is observed to be 0.65.

Capitol Health Limited is on third place and SDI Ltd is on fourth place in terms of debt to equity

ratio and the values are observed to be 0.26 and 0.17. Since the debt-to-equity ratio of SDI Ltd is

lowest it can be considered that the company has lesser liabilities and is performing very well in

the industry. In other words it can be said that the business of SDI Ltd is more stable as

compared to other companies. The lesser value of debt-to-equity ratio is considered to be

favorable for the investors as it depicts that the company has less amounts of debts and can easily

deliver payments to the investors (Baby, 2016). Therefore, the investors like to make investments

in the companies which has lower debt-to-equity ratio so that payments will be delivered to them

timely.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.