Corporate Accounting Report: Rio Tinto and Boral Analysis

VerifiedAdded on 2023/06/05

|17

|4071

|212

Report

AI Summary

This report provides a comprehensive analysis of corporate accounting practices, focusing on the financial statements of Rio Tinto Ltd and Boral Ltd, two companies in the mining industry. The report examines key components such as owner's equity, capital structure decisions, and cash flow statements, offering a comparative study to highlight differences and similarities. It delves into the reporting of comprehensive items and the accounting for taxes, including effective tax rates, deferred tax assets and liabilities, and cash tax rate computations. Numerical calculations and graphical representations are used to enhance the analysis, providing insights into the financial performance and operational structures of both companies. The report concludes with a detailed discussion of the findings, offering a valuable resource for understanding corporate accounting principles and financial statement analysis.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CORPORATE ACCOUNTING

Executive Summary

The assessment considers two company which are engaged in mining business for the purpose of

identifying the operational structure if the business and also look into the sources of funds which

are used by the business. Rio Tinto Ltd and Boral Ltd are considered on the basis of which

significant items of the financial statements are considered. The assessment deals with the

disclosure requirements of complex items which are generally shown in the financial statements

of the company. The assessment effectively sets up a comparative analysis of financial

information which is presented in the annual reports of the business and covers the above

mention items which are shown in the annual reports of the business. The quality of the report is

further enhanced with the help of numerical calculations of taxation for the month.

CORPORATE ACCOUNTING

Executive Summary

The assessment considers two company which are engaged in mining business for the purpose of

identifying the operational structure if the business and also look into the sources of funds which

are used by the business. Rio Tinto Ltd and Boral Ltd are considered on the basis of which

significant items of the financial statements are considered. The assessment deals with the

disclosure requirements of complex items which are generally shown in the financial statements

of the company. The assessment effectively sets up a comparative analysis of financial

information which is presented in the annual reports of the business and covers the above

mention items which are shown in the annual reports of the business. The quality of the report is

further enhanced with the help of numerical calculations of taxation for the month.

2

CORPORATE ACCOUNTING

Table of Contents

Introduction......................................................................................................................................3

Discussions......................................................................................................................................4

Owner’s Equity............................................................................................................................4

Capital Structure Decisions.........................................................................................................5

Analysis of Cash Flow Statement................................................................................................6

Comparative Study of Cash Flow Statement...............................................................................7

Insights of Cash flow Statement................................................................................................11

Reporting for Comprehensive Items..........................................................................................11

Disclosures of Comprehensive Items........................................................................................11

Comparative Analysis of Comprehensive Items.......................................................................12

Accounting for Taxes................................................................................................................12

Effective Tax Rate.....................................................................................................................12

Deferred Tax Assets and Liabilities..........................................................................................13

Cash Tax Rate Computation......................................................................................................13

Difference between Cash Tax rate and Book Tax Rate.............................................................13

Conclusion.....................................................................................................................................14

Reference.......................................................................................................................................15

CORPORATE ACCOUNTING

Table of Contents

Introduction......................................................................................................................................3

Discussions......................................................................................................................................4

Owner’s Equity............................................................................................................................4

Capital Structure Decisions.........................................................................................................5

Analysis of Cash Flow Statement................................................................................................6

Comparative Study of Cash Flow Statement...............................................................................7

Insights of Cash flow Statement................................................................................................11

Reporting for Comprehensive Items..........................................................................................11

Disclosures of Comprehensive Items........................................................................................11

Comparative Analysis of Comprehensive Items.......................................................................12

Accounting for Taxes................................................................................................................12

Effective Tax Rate.....................................................................................................................12

Deferred Tax Assets and Liabilities..........................................................................................13

Cash Tax Rate Computation......................................................................................................13

Difference between Cash Tax rate and Book Tax Rate.............................................................13

Conclusion.....................................................................................................................................14

Reference.......................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CORPORATE ACCOUNTING

Introduction

The role of accounting has enhanced with the changes in the financial structure and

competitiveness in business environment. Most of the business follow a reporting framework

which is approved by one or more accounting bodies such as IASB or ASSB. An ideal reporting

framework consist of all relevant information with appropriate disclosures for the same (Gitman,

Juchau and Flanagan 2015). The assessment proceeds with significant items reported in annual

reports of the companies considered and comment on the changes which have taken place in the

same (Henderson et al. 2015). A brief background of the companies considered is given below

Boral Ltd is engaged in the productions of materials which are used in construction

projects. The company has its headquarters and foundation in Australia however, the business

has expanded and penetrated the markets of Asia and USA (Boral. 2018). The company is

known to supply important building materials which are concrete placings, asphalt, cement to the

customers of the business. The company operates at a large scale and employ around 16000

employees who are working at different operational sites off the business.

Rio Tinto Ltd is one of the largest metal and mining business which has its operations in

Australia and is also listed in ASX. The company was founded in 1873 and has its headquarters

situated in London and therefore the company is also known to be an Anglo-Australian business.

The operations of the company are far and wide spread but the major areas of operations for the

business is in Australia and Canada (Riotinto.com. 2018). The company produces numerous

metals such as aluminum, copper, bauxite, iron ore.

CORPORATE ACCOUNTING

Introduction

The role of accounting has enhanced with the changes in the financial structure and

competitiveness in business environment. Most of the business follow a reporting framework

which is approved by one or more accounting bodies such as IASB or ASSB. An ideal reporting

framework consist of all relevant information with appropriate disclosures for the same (Gitman,

Juchau and Flanagan 2015). The assessment proceeds with significant items reported in annual

reports of the companies considered and comment on the changes which have taken place in the

same (Henderson et al. 2015). A brief background of the companies considered is given below

Boral Ltd is engaged in the productions of materials which are used in construction

projects. The company has its headquarters and foundation in Australia however, the business

has expanded and penetrated the markets of Asia and USA (Boral. 2018). The company is

known to supply important building materials which are concrete placings, asphalt, cement to the

customers of the business. The company operates at a large scale and employ around 16000

employees who are working at different operational sites off the business.

Rio Tinto Ltd is one of the largest metal and mining business which has its operations in

Australia and is also listed in ASX. The company was founded in 1873 and has its headquarters

situated in London and therefore the company is also known to be an Anglo-Australian business.

The operations of the company are far and wide spread but the major areas of operations for the

business is in Australia and Canada (Riotinto.com. 2018). The company produces numerous

metals such as aluminum, copper, bauxite, iron ore.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CORPORATE ACCOUNTING

The report shows computations of tax rates for both companies and analyzes the changes

which have take place in the same. The report also shows contrast between different items which

are shown in the annual reports of both the companies.

Discussions

Owner’s Equity

The owner’s equity is shown in the balance sheet of the company and is considered to be

an important part of the annual report of the business. The components of owner’s equity which

is reflected in the annual report of both the companies are share capital balance, reserves and

retained earnings of the business. The item retained earnings is made out of excessive profits

which are made by the business over the shares and the same represent internal source of finance

for the business. The reserve of the business is made up of accumulated profits which is made on

year to year basis and the same funds can be used by business for specific purpose or even

general purpose. The share capital reflects the capital which is raised by the management of the

company with the help of issue of shares of the business.

Boral ltd ‘s annual report shows that the share capital of the business has increased during

the year and the same is shown to be $ 2361.5 million. The share capital is raised following the

capital requirements of the business for the year. The reserve balance of the company for the

year has shown a decline in value which may be due to set off of previous losses or application

of the reserve amount for a specific purpose which can be purchase of assets of the business. The

retained earnings of the business shows improvement in balances which is due to accumulation

of profits of the business.

CORPORATE ACCOUNTING

The report shows computations of tax rates for both companies and analyzes the changes

which have take place in the same. The report also shows contrast between different items which

are shown in the annual reports of both the companies.

Discussions

Owner’s Equity

The owner’s equity is shown in the balance sheet of the company and is considered to be

an important part of the annual report of the business. The components of owner’s equity which

is reflected in the annual report of both the companies are share capital balance, reserves and

retained earnings of the business. The item retained earnings is made out of excessive profits

which are made by the business over the shares and the same represent internal source of finance

for the business. The reserve of the business is made up of accumulated profits which is made on

year to year basis and the same funds can be used by business for specific purpose or even

general purpose. The share capital reflects the capital which is raised by the management of the

company with the help of issue of shares of the business.

Boral ltd ‘s annual report shows that the share capital of the business has increased during

the year and the same is shown to be $ 2361.5 million. The share capital is raised following the

capital requirements of the business for the year. The reserve balance of the company for the

year has shown a decline in value which may be due to set off of previous losses or application

of the reserve amount for a specific purpose which can be purchase of assets of the business. The

retained earnings of the business shows improvement in balances which is due to accumulation

of profits of the business.

5

CORPORATE ACCOUNTING

In case of Rio Tinto Ltd, the share capital which is shown in the balance sheet is provided

under the breakup of share capital of Rio Tinto Plc and Rio Tinto limited. The management of

the Rio Tinto ltd has issued new shares which causes to increase the capital of the business. The

reserve of the business is shown to have increased during the year and the retained earnings of

the business has also increased during the period. The increase in retained earnings and reserves

demonstrate that the business has financial strength and good financial performance for the year.

The share capital of the business $ 4,140 million for the year 2017. This figure has increased

from previous year analysis.

Capital Structure Decisions

Capital Structure refers to the application of equity and debt capital in handling the

management of the business and also the various operations which are undertaken by the

company during the period. The management of Boral ltd uses an optimal capital structure which

is made up of both share capital and capital accumulated from loans (Dalal 2013). The

management of Boral ltd shows an appropriate capital structure which is made of equity and debt

capital used for financing the activities of the business. The policy and goals of the business is to

attain further expansion and attain sustainable growth in the business which requires the amount

of capital which is raised by Boral Ltd for the year. The debt capital of the business is shown to

be $ 2163.7 million in 2017 which has tremendously increased and the notes to account section

confirms that the business has taken additional loans during the year.

The balance sheet which is prepared by the management of Rio Tinto ltd for the year

2017 shows that the management of the companies utilizes both equity and debt capital for the

purpose of financing the different projects of a business (Jain, Singh and Yadav 2013). The debt

balance of the business for the year 2017 has reduced which is due to the management has repaid

CORPORATE ACCOUNTING

In case of Rio Tinto Ltd, the share capital which is shown in the balance sheet is provided

under the breakup of share capital of Rio Tinto Plc and Rio Tinto limited. The management of

the Rio Tinto ltd has issued new shares which causes to increase the capital of the business. The

reserve of the business is shown to have increased during the year and the retained earnings of

the business has also increased during the period. The increase in retained earnings and reserves

demonstrate that the business has financial strength and good financial performance for the year.

The share capital of the business $ 4,140 million for the year 2017. This figure has increased

from previous year analysis.

Capital Structure Decisions

Capital Structure refers to the application of equity and debt capital in handling the

management of the business and also the various operations which are undertaken by the

company during the period. The management of Boral ltd uses an optimal capital structure which

is made up of both share capital and capital accumulated from loans (Dalal 2013). The

management of Boral ltd shows an appropriate capital structure which is made of equity and debt

capital used for financing the activities of the business. The policy and goals of the business is to

attain further expansion and attain sustainable growth in the business which requires the amount

of capital which is raised by Boral Ltd for the year. The debt capital of the business is shown to

be $ 2163.7 million in 2017 which has tremendously increased and the notes to account section

confirms that the business has taken additional loans during the year.

The balance sheet which is prepared by the management of Rio Tinto ltd for the year

2017 shows that the management of the companies utilizes both equity and debt capital for the

purpose of financing the different projects of a business (Jain, Singh and Yadav 2013). The debt

balance of the business for the year 2017 has reduced which is due to the management has repaid

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CORPORATE ACCOUNTING

a part of loan of the business during the year. The debt balance for the year 2017 is shown to be

$15,148 million which forms a major part of capital structure and the business rarely uses equity-

based capital for the purpose of financing the activities of the business.

The analysis shows that Boral ltd believes in balanced debt equity capital mix as the

business is trying to get the debt capital up to equity standards in order to achieve an optimal

capital structure. The capital structure analysis of Rio Tinto ltd reveals that the debt capital is

used mostly by the business and the management prefers application debt capital for financing

the activities of the business.

Analysis of Cash Flow Statement

The cash flow statement forms a part of the financial reports and the same shows cash

position of the business. The cash flow statement only considers the cash items during the period

and non-cash items of the business are not considered (Call, Chen and Tong 2013). The purpose

of cash flow statement is to evaluate the net cash and cash equivalent balance of the company

which is shown in the balance sheet of the business. The cash flow statement considers the three

main activities of the business which forms part of annual report.

The cash flow statement of the Boral ltd shows cash receipts of the business is through

receipts from sales which is included in the operating activities of the business. The business also

has interest income which is part of the other income of the business. The cash from operating

activities is shown to be positive but the same has reduced from the analysis which is shown for

previous year. The cash from investing activities of the business shows that the business has

purchased entities and business and also properties during the year which is the main reason as to

why cash outflow is more than cash inflow in this section (Mohanram 2014). The cash from

CORPORATE ACCOUNTING

a part of loan of the business during the year. The debt balance for the year 2017 is shown to be

$15,148 million which forms a major part of capital structure and the business rarely uses equity-

based capital for the purpose of financing the activities of the business.

The analysis shows that Boral ltd believes in balanced debt equity capital mix as the

business is trying to get the debt capital up to equity standards in order to achieve an optimal

capital structure. The capital structure analysis of Rio Tinto ltd reveals that the debt capital is

used mostly by the business and the management prefers application debt capital for financing

the activities of the business.

Analysis of Cash Flow Statement

The cash flow statement forms a part of the financial reports and the same shows cash

position of the business. The cash flow statement only considers the cash items during the period

and non-cash items of the business are not considered (Call, Chen and Tong 2013). The purpose

of cash flow statement is to evaluate the net cash and cash equivalent balance of the company

which is shown in the balance sheet of the business. The cash flow statement considers the three

main activities of the business which forms part of annual report.

The cash flow statement of the Boral ltd shows cash receipts of the business is through

receipts from sales which is included in the operating activities of the business. The business also

has interest income which is part of the other income of the business. The cash from operating

activities is shown to be positive but the same has reduced from the analysis which is shown for

previous year. The cash from investing activities of the business shows that the business has

purchased entities and business and also properties during the year which is the main reason as to

why cash outflow is more than cash inflow in this section (Mohanram 2014). The cash from

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE ACCOUNTING

fining activities of the business comprise of net capital which is raised by the business and also

the debt capital which is taken by the company for the year 2017. The net cash from financing

activities of the business is shown to be positive which is due to the excessive cash which has

entered the business during the period.

The cash from operations of Rio Tinto Ltd for the year 2017 is shown to have increased

and the enhanced figure is shown to be $ 16670 million for the year 2017. The increase in cash

flow from operating activities shows strength of the business in managing expenses of the

business. The operating activities of the business comprises of the core business activities related

to the business. The cash from operations of the business mainly comprises of operating

activities of the business and the major cash flows which can be recognized from the cash flow

statement is dividend from equity accounts and tax expenses which are incurred during the year.

The investing activities of the business shows the purchases which is undertaken by the

management of the business (Farshadfar and Monem 2013). The purchases are shown in the

notes to account section of the annual report which comprise of property, plant and equipment

and also intangible assets. This is the major reason for the excessive cash outflow. The cash from

financing activities of the business show that the major cash outflows is from buyback of shares

loan repayments and also dividend which is paid to the investors of the business. The financing

activities of the business represent the loans and share buyback and loan repayment which is

made by the business during the year.

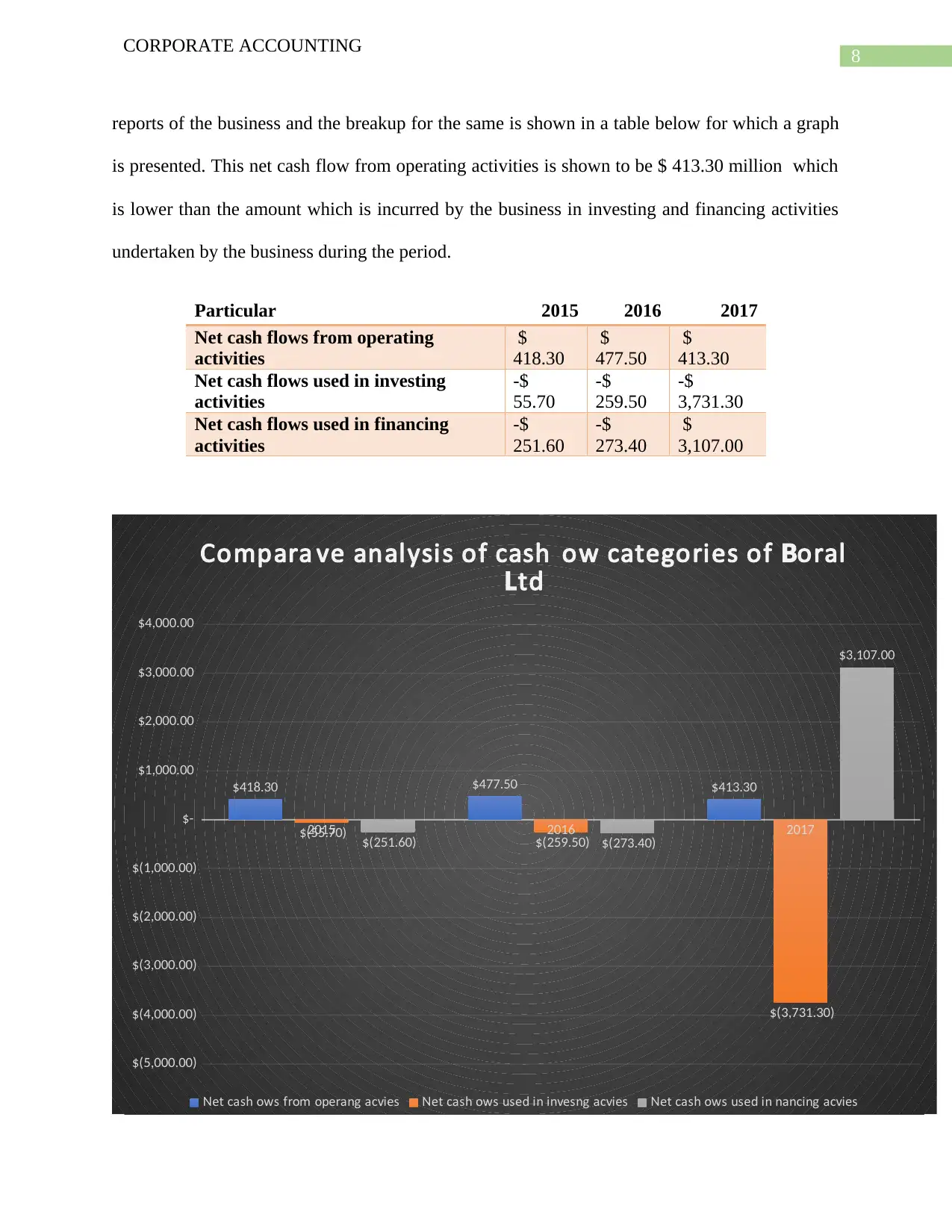

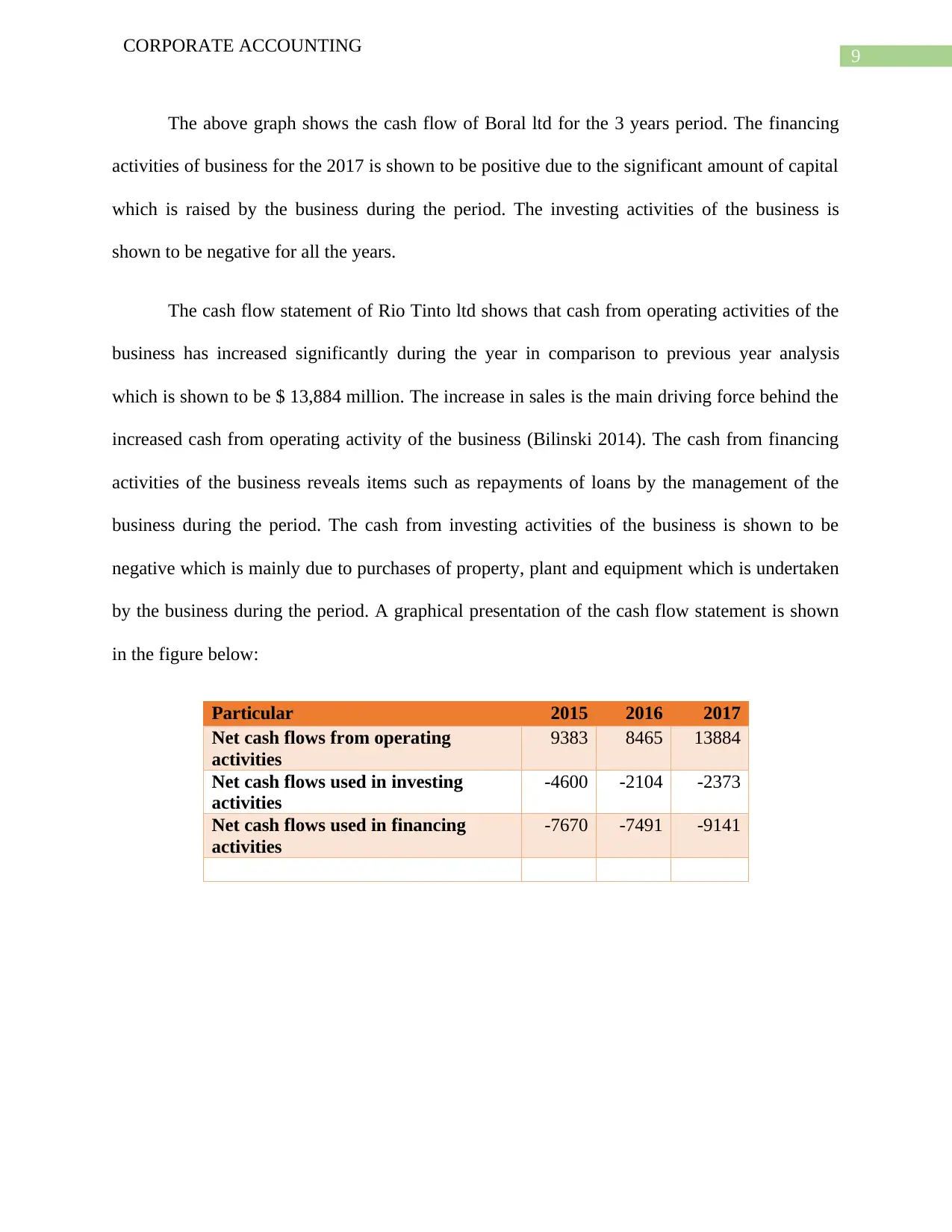

Comparative Study of Cash Flow Statement

The comparative analysis of the cash flow statement which is porepared by both the

companies is effectively presented with the help of graphical presentation of the cash flow

statement is shown in the figure below. The net cash flow of Boral ltd is shown in the annual

CORPORATE ACCOUNTING

fining activities of the business comprise of net capital which is raised by the business and also

the debt capital which is taken by the company for the year 2017. The net cash from financing

activities of the business is shown to be positive which is due to the excessive cash which has

entered the business during the period.

The cash from operations of Rio Tinto Ltd for the year 2017 is shown to have increased

and the enhanced figure is shown to be $ 16670 million for the year 2017. The increase in cash

flow from operating activities shows strength of the business in managing expenses of the

business. The operating activities of the business comprises of the core business activities related

to the business. The cash from operations of the business mainly comprises of operating

activities of the business and the major cash flows which can be recognized from the cash flow

statement is dividend from equity accounts and tax expenses which are incurred during the year.

The investing activities of the business shows the purchases which is undertaken by the

management of the business (Farshadfar and Monem 2013). The purchases are shown in the

notes to account section of the annual report which comprise of property, plant and equipment

and also intangible assets. This is the major reason for the excessive cash outflow. The cash from

financing activities of the business show that the major cash outflows is from buyback of shares

loan repayments and also dividend which is paid to the investors of the business. The financing

activities of the business represent the loans and share buyback and loan repayment which is

made by the business during the year.

Comparative Study of Cash Flow Statement

The comparative analysis of the cash flow statement which is porepared by both the

companies is effectively presented with the help of graphical presentation of the cash flow

statement is shown in the figure below. The net cash flow of Boral ltd is shown in the annual

8

CORPORATE ACCOUNTING

reports of the business and the breakup for the same is shown in a table below for which a graph

is presented. This net cash flow from operating activities is shown to be $ 413.30 million which

is lower than the amount which is incurred by the business in investing and financing activities

undertaken by the business during the period.

Particular 2015 2016 2017

Net cash flows from operating

activities

$

418.30

$

477.50

$

413.30

Net cash flows used in investing

activities

-$

55.70

-$

259.50

-$

3,731.30

Net cash flows used in financing

activities

-$

251.60

-$

273.40

$

3,107.00

2015 2016 2017

$(5,000.00)

$(4,000.00)

$(3,000.00)

$(2,000.00)

$(1,000.00)

$-

$1,000.00

$2,000.00

$3,000.00

$4,000.00

$418.30 $477.50 $413.30

$(55.70) $(259.50)

$(3,731.30)

$(251.60) $(273.40)

$3,107.00

Comparati ve analysis of cash fl ow categories of oralB

tdL

et cash fl ows from operating activitiesN et cash fl ows used in investing activitiesN et cash fl ows used in fi nancing activitiesN

CORPORATE ACCOUNTING

reports of the business and the breakup for the same is shown in a table below for which a graph

is presented. This net cash flow from operating activities is shown to be $ 413.30 million which

is lower than the amount which is incurred by the business in investing and financing activities

undertaken by the business during the period.

Particular 2015 2016 2017

Net cash flows from operating

activities

$

418.30

$

477.50

$

413.30

Net cash flows used in investing

activities

-$

55.70

-$

259.50

-$

3,731.30

Net cash flows used in financing

activities

-$

251.60

-$

273.40

$

3,107.00

2015 2016 2017

$(5,000.00)

$(4,000.00)

$(3,000.00)

$(2,000.00)

$(1,000.00)

$-

$1,000.00

$2,000.00

$3,000.00

$4,000.00

$418.30 $477.50 $413.30

$(55.70) $(259.50)

$(3,731.30)

$(251.60) $(273.40)

$3,107.00

Comparati ve analysis of cash fl ow categories of oralB

tdL

et cash fl ows from operating activitiesN et cash fl ows used in investing activitiesN et cash fl ows used in fi nancing activitiesN

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CORPORATE ACCOUNTING

The above graph shows the cash flow of Boral ltd for the 3 years period. The financing

activities of business for the 2017 is shown to be positive due to the significant amount of capital

which is raised by the business during the period. The investing activities of the business is

shown to be negative for all the years.

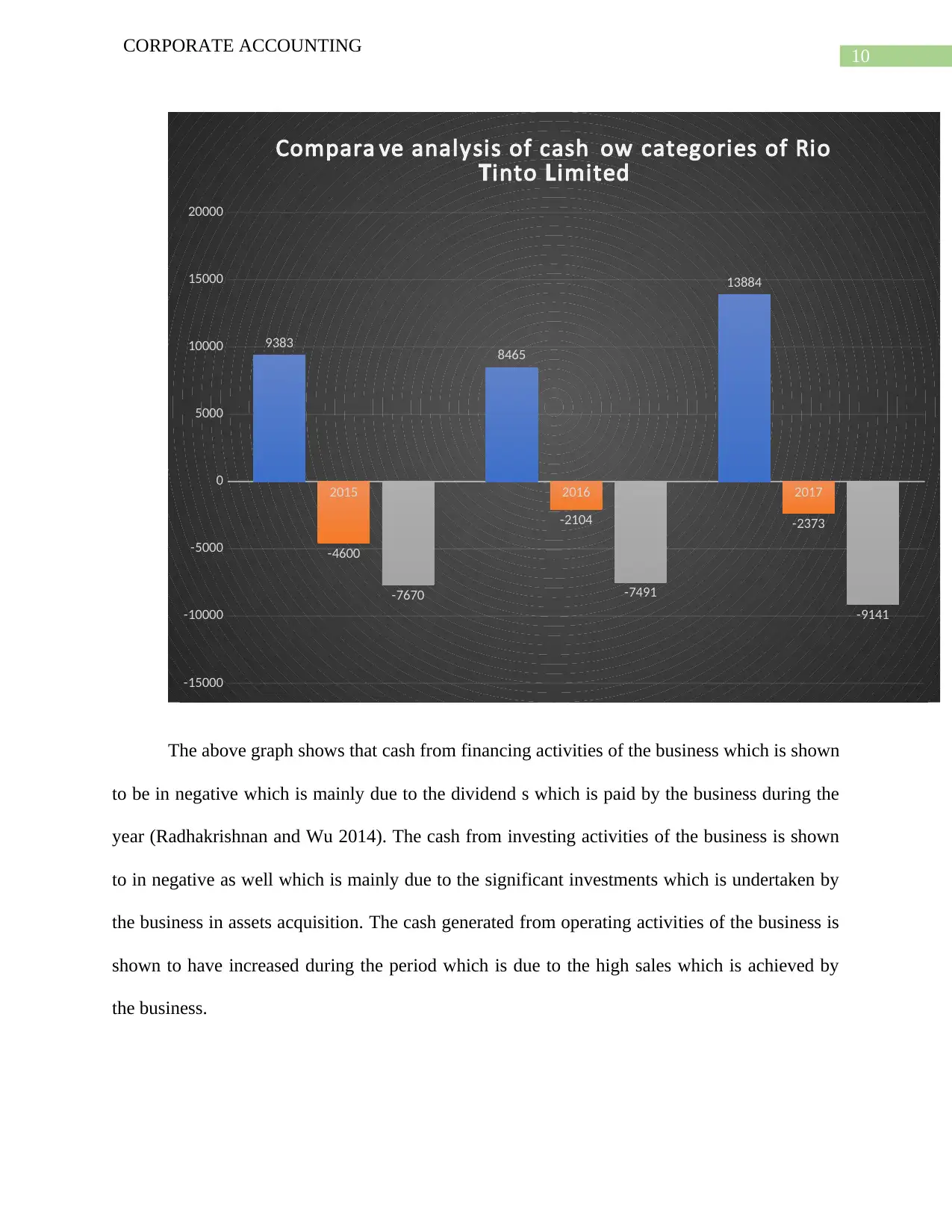

The cash flow statement of Rio Tinto ltd shows that cash from operating activities of the

business has increased significantly during the year in comparison to previous year analysis

which is shown to be $ 13,884 million. The increase in sales is the main driving force behind the

increased cash from operating activity of the business (Bilinski 2014). The cash from financing

activities of the business reveals items such as repayments of loans by the management of the

business during the period. The cash from investing activities of the business is shown to be

negative which is mainly due to purchases of property, plant and equipment which is undertaken

by the business during the period. A graphical presentation of the cash flow statement is shown

in the figure below:

Particular 2015 2016 2017

Net cash flows from operating

activities

9383 8465 13884

Net cash flows used in investing

activities

-4600 -2104 -2373

Net cash flows used in financing

activities

-7670 -7491 -9141

CORPORATE ACCOUNTING

The above graph shows the cash flow of Boral ltd for the 3 years period. The financing

activities of business for the 2017 is shown to be positive due to the significant amount of capital

which is raised by the business during the period. The investing activities of the business is

shown to be negative for all the years.

The cash flow statement of Rio Tinto ltd shows that cash from operating activities of the

business has increased significantly during the year in comparison to previous year analysis

which is shown to be $ 13,884 million. The increase in sales is the main driving force behind the

increased cash from operating activity of the business (Bilinski 2014). The cash from financing

activities of the business reveals items such as repayments of loans by the management of the

business during the period. The cash from investing activities of the business is shown to be

negative which is mainly due to purchases of property, plant and equipment which is undertaken

by the business during the period. A graphical presentation of the cash flow statement is shown

in the figure below:

Particular 2015 2016 2017

Net cash flows from operating

activities

9383 8465 13884

Net cash flows used in investing

activities

-4600 -2104 -2373

Net cash flows used in financing

activities

-7670 -7491 -9141

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CORPORATE ACCOUNTING

2015 2016 2017

-15000

-10000

-5000

0

5000

10000

15000

20000

9383 8465

13884

-4600

-2104 -2373

-7670 -7491

-9141

Comparati ve analysis of cash fl ow categories of Rio

into imitedT L

The above graph shows that cash from financing activities of the business which is shown

to be in negative which is mainly due to the dividend s which is paid by the business during the

year (Radhakrishnan and Wu 2014). The cash from investing activities of the business is shown

to in negative as well which is mainly due to the significant investments which is undertaken by

the business in assets acquisition. The cash generated from operating activities of the business is

shown to have increased during the period which is due to the high sales which is achieved by

the business.

CORPORATE ACCOUNTING

2015 2016 2017

-15000

-10000

-5000

0

5000

10000

15000

20000

9383 8465

13884

-4600

-2104 -2373

-7670 -7491

-9141

Comparati ve analysis of cash fl ow categories of Rio

into imitedT L

The above graph shows that cash from financing activities of the business which is shown

to be in negative which is mainly due to the dividend s which is paid by the business during the

year (Radhakrishnan and Wu 2014). The cash from investing activities of the business is shown

to in negative as well which is mainly due to the significant investments which is undertaken by

the business in assets acquisition. The cash generated from operating activities of the business is

shown to have increased during the period which is due to the high sales which is achieved by

the business.

11

CORPORATE ACCOUNTING

Insights of Cash flow Statement

The cash position of Rio Tinto ltd for the year 2017 is shown to be favorable which

shows that business has operational strength. On the other hand, the operating activities of the

Boral ltd shows that cash generated from operating activities has slightly decreased which needs

to be considered by the management and appropriate strategies needs to be formulated. The cash

from investing activities reveal that Boral ltd has acquired another business in 2017 which is

mainly the reason for the more of cash outflows during the year. On the other hand, the

management of Rio Tinto ltd has purchased significant amount of assets which is the reason for

the negative cash from investing activities of the business. In an overall estimate, it is evident

that cash position of Rio Tinto ltd is much better than the cash position of Boral ltd.

Reporting for Comprehensive Items

The comprehensive items are extraordinary items which are shown in the financial

statements of the business and the annual report of Boral ltd and Rio Tinto ltd show that the

financial statement include comprehensive items. The annual report of Boral ltd shows hedge

contracts and fluctuation of exchange rates of the business. The annual reports of Rio Tinto ltd

also shows the same element and the only addition is the revaluation of assets which is shown in

the annual report of the business.

Disclosures of Comprehensive Items

The extraordinary nature of comprehensive items are important as they determine

whether the same is to be shown in the financial statements or separately in another segment

(Papanikolaou and Wolff 2014). The items are also no-recurring in nature and not regular and

therefore the same is not included in the financial statement of the business.

CORPORATE ACCOUNTING

Insights of Cash flow Statement

The cash position of Rio Tinto ltd for the year 2017 is shown to be favorable which

shows that business has operational strength. On the other hand, the operating activities of the

Boral ltd shows that cash generated from operating activities has slightly decreased which needs

to be considered by the management and appropriate strategies needs to be formulated. The cash

from investing activities reveal that Boral ltd has acquired another business in 2017 which is

mainly the reason for the more of cash outflows during the year. On the other hand, the

management of Rio Tinto ltd has purchased significant amount of assets which is the reason for

the negative cash from investing activities of the business. In an overall estimate, it is evident

that cash position of Rio Tinto ltd is much better than the cash position of Boral ltd.

Reporting for Comprehensive Items

The comprehensive items are extraordinary items which are shown in the financial

statements of the business and the annual report of Boral ltd and Rio Tinto ltd show that the

financial statement include comprehensive items. The annual report of Boral ltd shows hedge

contracts and fluctuation of exchange rates of the business. The annual reports of Rio Tinto ltd

also shows the same element and the only addition is the revaluation of assets which is shown in

the annual report of the business.

Disclosures of Comprehensive Items

The extraordinary nature of comprehensive items are important as they determine

whether the same is to be shown in the financial statements or separately in another segment

(Papanikolaou and Wolff 2014). The items are also no-recurring in nature and not regular and

therefore the same is not included in the financial statement of the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.