Corporate Accounting: EZY Manufacturing Analysis Report

VerifiedAdded on 2020/10/23

|11

|3060

|263

Report

AI Summary

This report delves into corporate accounting, examining the financial implications of acquisitions made by EZY Manufacturing Ltd. The analysis covers two key acquisitions: Range PTY Ltd. and Swift Works Ltd. The report details the journal entries for these acquisitions, including share issuance and cash payments, and discusses the calculation of goodwill and purchase consideration. It also addresses dividend payments and receivables, differentiating between dividends received and those declared. Furthermore, the report analyzes the investments made in Range PTY Ltd. and Swift Works Ltd., considering the fair value of assets and the rationale behind specific accounting treatments. The report highlights the importance of vertical integration and its impact on financial reporting, providing a comprehensive overview of corporate accounting principles in the context of these business combinations.

CORPORATE

ACCOUNTING: PART

1

ACCOUNTING: PART

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

QUESTION 1...................................................................................................................................1

1. (a) General Journal Entries in the books of EZY Manufacturing Ltd. for acquisition of

investment:...................................................................................................................................1

(b) Dividend Received or Receivable during the year ended 30th June, 2019............................3

QUESTION 2...................................................................................................................................4

QUESTION 3...................................................................................................................................5

QUESTION 4...................................................................................................................................7

Covered in Excel..........................................................................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

QUESTION 1...................................................................................................................................1

1. (a) General Journal Entries in the books of EZY Manufacturing Ltd. for acquisition of

investment:...................................................................................................................................1

(b) Dividend Received or Receivable during the year ended 30th June, 2019............................3

QUESTION 2...................................................................................................................................4

QUESTION 3...................................................................................................................................5

QUESTION 4...................................................................................................................................7

Covered in Excel..........................................................................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Corporate accounting is a special branch of accounting which can deal with the

accounting for companies (Belal, 2016) . It is a process which can involve different final

accounts of a company like cash flow statement, preparation of their final accounts and After

analysis these results and interpretation of companies financial result in particular accounting

period. These financial results are interpreted specific events such as absorption, amalgamation

and consolidation. In the report consist of Ezy manufacturing limited can acquire of range PTY

LTD and Swift Works Ltd where focused on purchase consideration, business combination and

goodwill. The company basically follow the rules of acquisition analysis because of company

gets growth through analysis. With the help of corporate accounting track all records after that

acquire any other company.

MAIN BODY

Business Combination is a transaction which the acquirer get control of another business

and business combination can provide to way to grow their size as compare to internal activities.

It is not the formation of a joint venture nor does to involve the set of assets which can not

constitute a business. In consolidation, purchase consideration is the cash or stock or other

assets movement by the acquirer to the acquiree or their shareholder in return of the acquirees

assets or their stock. It is an important number which is finding during to business combination

and in the process of price allocation. The value of purchase consideration is higher than the fair

value of net assets of the acquiree (Caskey and Laux, 2016) . Goodwill is a long term asset

classified as an intangible asset and goodwill is recorded when a company has been acquired

another company for growth. If that time purchase price is greater than to fair value of the

tangible and intangible assets acquired after than less amount of liabilities of a company on the

assumption basis. In the context of given case study, the following questions have been answered

and conclusions drawn thereof:

QUESTION 1

1. (a) General Journal Entries in the books of EZY Manufacturing Ltd. for acquisition of

investment:

(i) Range Ltd. as on July 1, 2015:

1

Corporate accounting is a special branch of accounting which can deal with the

accounting for companies (Belal, 2016) . It is a process which can involve different final

accounts of a company like cash flow statement, preparation of their final accounts and After

analysis these results and interpretation of companies financial result in particular accounting

period. These financial results are interpreted specific events such as absorption, amalgamation

and consolidation. In the report consist of Ezy manufacturing limited can acquire of range PTY

LTD and Swift Works Ltd where focused on purchase consideration, business combination and

goodwill. The company basically follow the rules of acquisition analysis because of company

gets growth through analysis. With the help of corporate accounting track all records after that

acquire any other company.

MAIN BODY

Business Combination is a transaction which the acquirer get control of another business

and business combination can provide to way to grow their size as compare to internal activities.

It is not the formation of a joint venture nor does to involve the set of assets which can not

constitute a business. In consolidation, purchase consideration is the cash or stock or other

assets movement by the acquirer to the acquiree or their shareholder in return of the acquirees

assets or their stock. It is an important number which is finding during to business combination

and in the process of price allocation. The value of purchase consideration is higher than the fair

value of net assets of the acquiree (Caskey and Laux, 2016) . Goodwill is a long term asset

classified as an intangible asset and goodwill is recorded when a company has been acquired

another company for growth. If that time purchase price is greater than to fair value of the

tangible and intangible assets acquired after than less amount of liabilities of a company on the

assumption basis. In the context of given case study, the following questions have been answered

and conclusions drawn thereof:

QUESTION 1

1. (a) General Journal Entries in the books of EZY Manufacturing Ltd. for acquisition of

investment:

(i) Range Ltd. as on July 1, 2015:

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

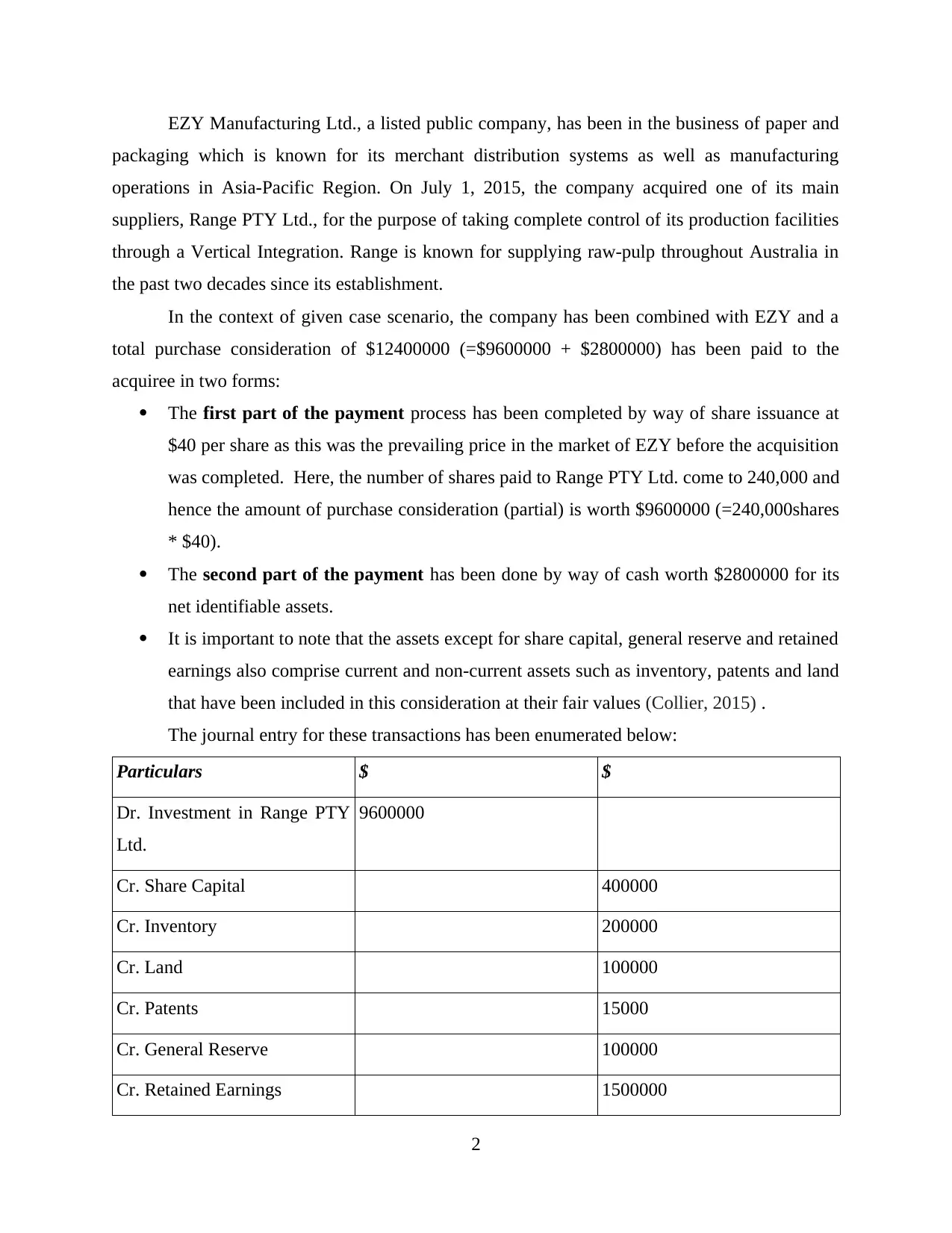

EZY Manufacturing Ltd., a listed public company, has been in the business of paper and

packaging which is known for its merchant distribution systems as well as manufacturing

operations in Asia-Pacific Region. On July 1, 2015, the company acquired one of its main

suppliers, Range PTY Ltd., for the purpose of taking complete control of its production facilities

through a Vertical Integration. Range is known for supplying raw-pulp throughout Australia in

the past two decades since its establishment.

In the context of given case scenario, the company has been combined with EZY and a

total purchase consideration of $12400000 (=$9600000 + $2800000) has been paid to the

acquiree in two forms:

The first part of the payment process has been completed by way of share issuance at

$40 per share as this was the prevailing price in the market of EZY before the acquisition

was completed. Here, the number of shares paid to Range PTY Ltd. come to 240,000 and

hence the amount of purchase consideration (partial) is worth $9600000 (=240,000shares

* $40).

The second part of the payment has been done by way of cash worth $2800000 for its

net identifiable assets.

It is important to note that the assets except for share capital, general reserve and retained

earnings also comprise current and non-current assets such as inventory, patents and land

that have been included in this consideration at their fair values (Collier, 2015) .

The journal entry for these transactions has been enumerated below:

Particulars $ $

Dr. Investment in Range PTY

Ltd.

9600000

Cr. Share Capital 400000

Cr. Inventory 200000

Cr. Land 100000

Cr. Patents 15000

Cr. General Reserve 100000

Cr. Retained Earnings 1500000

2

packaging which is known for its merchant distribution systems as well as manufacturing

operations in Asia-Pacific Region. On July 1, 2015, the company acquired one of its main

suppliers, Range PTY Ltd., for the purpose of taking complete control of its production facilities

through a Vertical Integration. Range is known for supplying raw-pulp throughout Australia in

the past two decades since its establishment.

In the context of given case scenario, the company has been combined with EZY and a

total purchase consideration of $12400000 (=$9600000 + $2800000) has been paid to the

acquiree in two forms:

The first part of the payment process has been completed by way of share issuance at

$40 per share as this was the prevailing price in the market of EZY before the acquisition

was completed. Here, the number of shares paid to Range PTY Ltd. come to 240,000 and

hence the amount of purchase consideration (partial) is worth $9600000 (=240,000shares

* $40).

The second part of the payment has been done by way of cash worth $2800000 for its

net identifiable assets.

It is important to note that the assets except for share capital, general reserve and retained

earnings also comprise current and non-current assets such as inventory, patents and land

that have been included in this consideration at their fair values (Collier, 2015) .

The journal entry for these transactions has been enumerated below:

Particulars $ $

Dr. Investment in Range PTY

Ltd.

9600000

Cr. Share Capital 400000

Cr. Inventory 200000

Cr. Land 100000

Cr. Patents 15000

Cr. General Reserve 100000

Cr. Retained Earnings 1500000

2

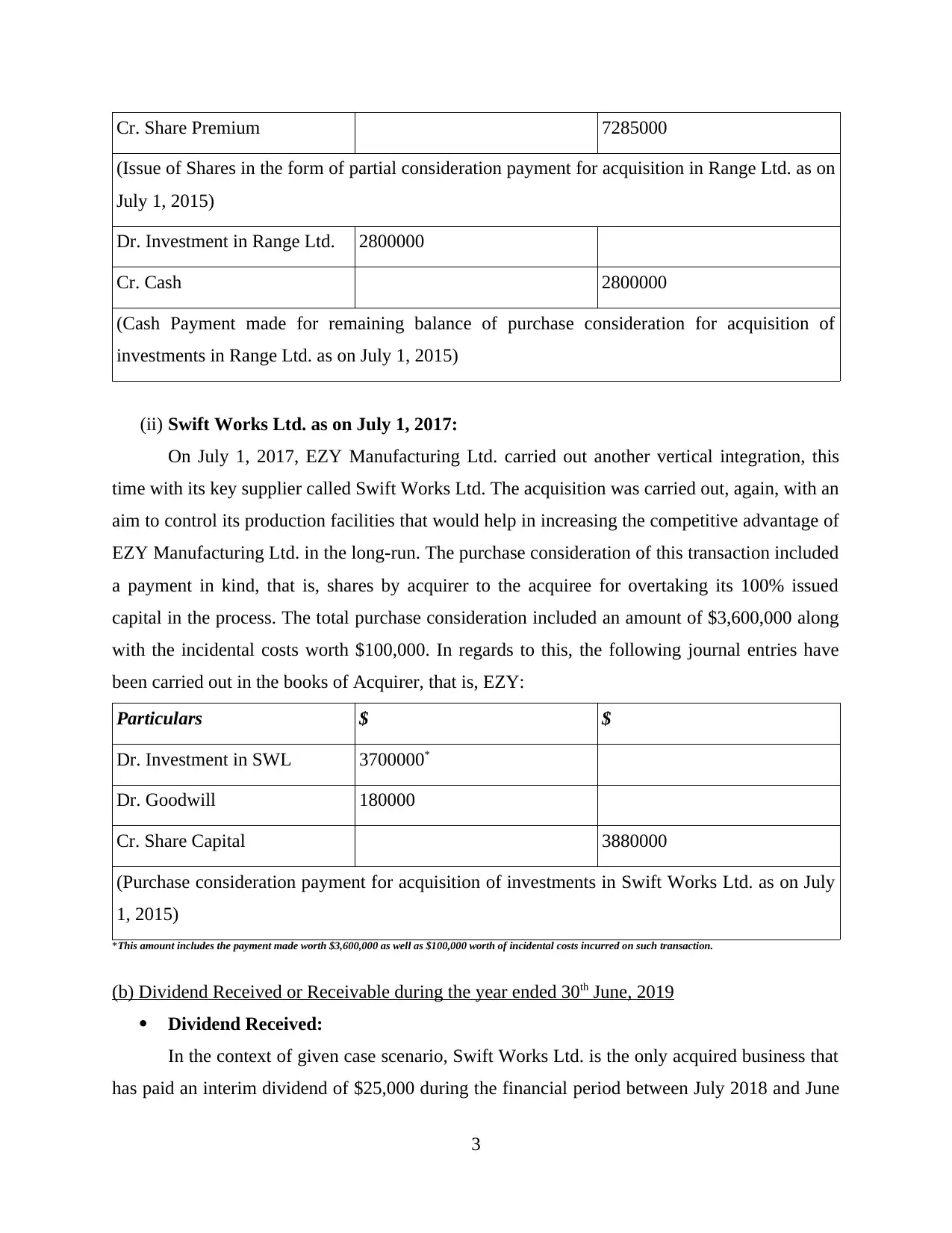

Cr. Share Premium 7285000

(Issue of Shares in the form of partial consideration payment for acquisition in Range Ltd. as on

July 1, 2015)

Dr. Investment in Range Ltd. 2800000

Cr. Cash 2800000

(Cash Payment made for remaining balance of purchase consideration for acquisition of

investments in Range Ltd. as on July 1, 2015)

(ii) Swift Works Ltd. as on July 1, 2017:

On July 1, 2017, EZY Manufacturing Ltd. carried out another vertical integration, this

time with its key supplier called Swift Works Ltd. The acquisition was carried out, again, with an

aim to control its production facilities that would help in increasing the competitive advantage of

EZY Manufacturing Ltd. in the long-run. The purchase consideration of this transaction included

a payment in kind, that is, shares by acquirer to the acquiree for overtaking its 100% issued

capital in the process. The total purchase consideration included an amount of $3,600,000 along

with the incidental costs worth $100,000. In regards to this, the following journal entries have

been carried out in the books of Acquirer, that is, EZY:

Particulars $ $

Dr. Investment in SWL 3700000*

Dr. Goodwill 180000

Cr. Share Capital 3880000

(Purchase consideration payment for acquisition of investments in Swift Works Ltd. as on July

1, 2015)

*This amount includes the payment made worth $3,600,000 as well as $100,000 worth of incidental costs incurred on such transaction.

(b) Dividend Received or Receivable during the year ended 30th June, 2019

Dividend Received:

In the context of given case scenario, Swift Works Ltd. is the only acquired business that

has paid an interim dividend of $25,000 during the financial period between July 2018 and June

3

(Issue of Shares in the form of partial consideration payment for acquisition in Range Ltd. as on

July 1, 2015)

Dr. Investment in Range Ltd. 2800000

Cr. Cash 2800000

(Cash Payment made for remaining balance of purchase consideration for acquisition of

investments in Range Ltd. as on July 1, 2015)

(ii) Swift Works Ltd. as on July 1, 2017:

On July 1, 2017, EZY Manufacturing Ltd. carried out another vertical integration, this

time with its key supplier called Swift Works Ltd. The acquisition was carried out, again, with an

aim to control its production facilities that would help in increasing the competitive advantage of

EZY Manufacturing Ltd. in the long-run. The purchase consideration of this transaction included

a payment in kind, that is, shares by acquirer to the acquiree for overtaking its 100% issued

capital in the process. The total purchase consideration included an amount of $3,600,000 along

with the incidental costs worth $100,000. In regards to this, the following journal entries have

been carried out in the books of Acquirer, that is, EZY:

Particulars $ $

Dr. Investment in SWL 3700000*

Dr. Goodwill 180000

Cr. Share Capital 3880000

(Purchase consideration payment for acquisition of investments in Swift Works Ltd. as on July

1, 2015)

*This amount includes the payment made worth $3,600,000 as well as $100,000 worth of incidental costs incurred on such transaction.

(b) Dividend Received or Receivable during the year ended 30th June, 2019

Dividend Received:

In the context of given case scenario, Swift Works Ltd. is the only acquired business that

has paid an interim dividend of $25,000 during the financial period between July 2018 and June

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2019. As per the given regulations, if one company has been acquired by another with a view to

combine businesses, the assets and liabilities of acquired company are automatically transferred

to the acquiring business entity, that is, EZY Manufacturing Ltd (Epstein, 2018) . On the other

hand, EZY has paid an interim dividend worth $400,000 to their investors. These investors

include both the shareholders of EZY as well as SWL which was previously acquired by the

former company. Since Swift Works has paid $25,000 to the ordinary shareholders this amount

shall be automatically transferred to EZY shareholders who own 100% ordinary share capital of

the acquired company. Hence, the total amount of dividend received by the shareholders of EZY

and SWL combined is $425,000 (=$400,000+$25,000).

Dividend Receivable:

Final Dividend Declared or Dividend Receivable relates to the amount of future

payments that a business enterprise sought to make towards its shareholders in the forthcoming

financial period. In this context, the companies EZY and SWL both have declared a final

dividend payment worth $600,000 and $75,000 respectively. It is important to note that for SWL

this amount shall be paid to the EZY as well as its previous shareholders which have now

become a part of the acquiring company itself. Hence, the total amount of dividend receivable by

the investors as on 30 June, 2019 would be $675,000 (=$600,000 + $75,000).

QUESTION 2

EZY Manufacturing Ltd implemented a policy of vertical integration and invested in two of its

key suppliers as Range Pty Ltd and SWL Pty ltd. The analysis are as follows in terms of both the

suppliers.

Analysis of Investment made by EZY manufacturing in Range Pty Ltd

There is an investment made of acquiring assets and share capital of Range that contains

acquisition of inventory on estimated value of $100000, land recognized as $100000 in respect

of $2000000. Property, plant and equipment contains the range of $750000 as on 1 July 2014

with useful life of 10 years. However, it will be counted as $750000 on 1 July. Due to having no

any recognition in accounting records, the fair value is counted as useful life of 10 years. The

cost of the equipment is not considered in books of accounts because value of equipment become

worthless as on 1 July 2017. As on 1st July 2015 were analyzed with respect of determination of

$2800000 in cash. The as on 1st July 2015 which is share capital 400000 ordinary shares with

4

combine businesses, the assets and liabilities of acquired company are automatically transferred

to the acquiring business entity, that is, EZY Manufacturing Ltd (Epstein, 2018) . On the other

hand, EZY has paid an interim dividend worth $400,000 to their investors. These investors

include both the shareholders of EZY as well as SWL which was previously acquired by the

former company. Since Swift Works has paid $25,000 to the ordinary shareholders this amount

shall be automatically transferred to EZY shareholders who own 100% ordinary share capital of

the acquired company. Hence, the total amount of dividend received by the shareholders of EZY

and SWL combined is $425,000 (=$400,000+$25,000).

Dividend Receivable:

Final Dividend Declared or Dividend Receivable relates to the amount of future

payments that a business enterprise sought to make towards its shareholders in the forthcoming

financial period. In this context, the companies EZY and SWL both have declared a final

dividend payment worth $600,000 and $75,000 respectively. It is important to note that for SWL

this amount shall be paid to the EZY as well as its previous shareholders which have now

become a part of the acquiring company itself. Hence, the total amount of dividend receivable by

the investors as on 30 June, 2019 would be $675,000 (=$600,000 + $75,000).

QUESTION 2

EZY Manufacturing Ltd implemented a policy of vertical integration and invested in two of its

key suppliers as Range Pty Ltd and SWL Pty ltd. The analysis are as follows in terms of both the

suppliers.

Analysis of Investment made by EZY manufacturing in Range Pty Ltd

There is an investment made of acquiring assets and share capital of Range that contains

acquisition of inventory on estimated value of $100000, land recognized as $100000 in respect

of $2000000. Property, plant and equipment contains the range of $750000 as on 1 July 2014

with useful life of 10 years. However, it will be counted as $750000 on 1 July. Due to having no

any recognition in accounting records, the fair value is counted as useful life of 10 years. The

cost of the equipment is not considered in books of accounts because value of equipment become

worthless as on 1 July 2017. As on 1st July 2015 were analyzed with respect of determination of

$2800000 in cash. The as on 1st July 2015 which is share capital 400000 ordinary shares with

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2000000 and preference share @ 8% 2000000, general reserves were counted as 1000000 and

retain earnings were calculated as 1500000.

Analysis of Investment made by EZY manufacturing in SWIFT WORKS LTD (SWL)

There are type of assumptions are considered while investing in SWL Ltd. Values of all

classes of assets are recognized on cost, the inventory’s taken held by SWL taken on cost after

tax. It is assumed that the goodwill will be impaired by 10% every year. The suppliers paper and

the packaging goods are consolidated with cost plus 20%. During the year the cost of stocks are

taken as 14000 for EZY and 40000 for SWL. The annual intragroup purchase is counted as

group purchases. It is assumed that the taxation rate is applicable as 30%. It is realized that the

group is mainly calculated with creative plans and situations. Plant and Equipment in the books

of Ezy limited calculated subject to 1 and 2

In this condition, sound bookkeeping norms ("GAAP") ° give that the hard and fast

expense should be circulated among the advantages proportionately to their individual sensible

characteristics (Henderson and et.al., 2015) . In Speaking to the Purchase of Isolated Assets Not

a Going Concern If SWL ltd were to buy land from SWL ltd Corp. (passed on by EZY on its

books at $35,000) at an expense of $20,000 in genuine cash notwithstanding assumption of a

$80,000 note bearing eagerness at the present market rate, that purchase would be spoken to in

SWl's journal as seeks after: Land $100,0000 Cash $650,000 Note Payable $80,0009 The critical

result to see here is that the acquired asset is showed up at its $1,000,000 cost to SWL, paying

little regard to the $3880,000 book passing on estimation of the dealer, B. In case couple of

individual assets were to be secured from B for a solitary sum in what is as often as possible

suggested as a "container purchase," they in like manner would be passed on Range to their

detriment to A, disregarding the way that an issue would rise concerning distribution of the

particular sum among the couple of things.

QUESTION 3

(a) The carrying value mainly reflect to equity and fair value can reflect to current market price.

The reason of select price that fair value of an assets can be more volatile and their book value

provide possibilities regarding to big discrepancies at the time of measure different values. After

the calculation it is getting that EZY pay to range after the acquisition as two options. First one

in shares amount 96,00,000 and in cash 28,00,000 so total amount pay by EZY to range

1,24,000,000.

5

retain earnings were calculated as 1500000.

Analysis of Investment made by EZY manufacturing in SWIFT WORKS LTD (SWL)

There are type of assumptions are considered while investing in SWL Ltd. Values of all

classes of assets are recognized on cost, the inventory’s taken held by SWL taken on cost after

tax. It is assumed that the goodwill will be impaired by 10% every year. The suppliers paper and

the packaging goods are consolidated with cost plus 20%. During the year the cost of stocks are

taken as 14000 for EZY and 40000 for SWL. The annual intragroup purchase is counted as

group purchases. It is assumed that the taxation rate is applicable as 30%. It is realized that the

group is mainly calculated with creative plans and situations. Plant and Equipment in the books

of Ezy limited calculated subject to 1 and 2

In this condition, sound bookkeeping norms ("GAAP") ° give that the hard and fast

expense should be circulated among the advantages proportionately to their individual sensible

characteristics (Henderson and et.al., 2015) . In Speaking to the Purchase of Isolated Assets Not

a Going Concern If SWL ltd were to buy land from SWL ltd Corp. (passed on by EZY on its

books at $35,000) at an expense of $20,000 in genuine cash notwithstanding assumption of a

$80,000 note bearing eagerness at the present market rate, that purchase would be spoken to in

SWl's journal as seeks after: Land $100,0000 Cash $650,000 Note Payable $80,0009 The critical

result to see here is that the acquired asset is showed up at its $1,000,000 cost to SWL, paying

little regard to the $3880,000 book passing on estimation of the dealer, B. In case couple of

individual assets were to be secured from B for a solitary sum in what is as often as possible

suggested as a "container purchase," they in like manner would be passed on Range to their

detriment to A, disregarding the way that an issue would rise concerning distribution of the

particular sum among the couple of things.

QUESTION 3

(a) The carrying value mainly reflect to equity and fair value can reflect to current market price.

The reason of select price that fair value of an assets can be more volatile and their book value

provide possibilities regarding to big discrepancies at the time of measure different values. After

the calculation it is getting that EZY pay to range after the acquisition as two options. First one

in shares amount 96,00,000 and in cash 28,00,000 so total amount pay by EZY to range

1,24,000,000.

5

(b) The inventory recoded as $100,000 instead of $600000 because of the amount taken fair

value because of firstly analysis that which amount less than fro market value and fair value.

After analysis selected appropriate amount (Maas, Schaltegger and Crutzen, 2016) . Land also

recorded as 200000 rather than to 100000 because of amount will be increased in potential time

so it has been taken increased amount.

(c) Goodwill:

In business the collection that is accounted in order to make purchase, there are many

crucial effect on accounting income of the customer those are preparing to buy goods. It is

observed that when purchase are relevant to the active business firms instead of simply separated

assets, then organization are mainly to ascertained the overall price which are not linked with the

values of single assets. They are basically related to the going-concern value that often related to

the excess of fair values attributable which are linked with value of assets and are equal to net

liabilities for an organisation (Qiu, Shaukat and Tharyan, 2016) In these condition, rather of

distributing the total price of purchase assets that are displayed on the accounting books of SWL

limited, accountants better realize that abstract assets which commonly known as "goodwill,"

must be happen on the books of respective company.

There another difficulty originate is related in concern with allocating of the total

purchase price to those of the acquired assets, which also includes goodwill. To better resolved

the issues of goodwill there is a two-step process which is totally different from the one-step

method that is commonly known as basket purchase of separated assets for company. The

includes two steps such as the purchase price is distributed among the identifiable intangible and

tangible assets which are purchased on the fair value and further it includes any balance is than

debited to the new intangible asset account the named “goodwill”

3. (d) As per the dividend information it is sited that:

On acquisition. As noted previously, on acquisition of the SWL ltd. Shares entered at cost

on in the books of EZY ltd. A debit to an account, which may be labelled “Investments,”

and a credit to cash or whatever, was used to pay the seller.

During the holding of the shares of SWL limited. When the SWL limited Corp. Shares

are accounted for by the equity method, EZY manufacturer must: (i) Recognize EZY's

proportionate share of SWL's post-acquisition earnings by debiting (on SWL's financial

6

value because of firstly analysis that which amount less than fro market value and fair value.

After analysis selected appropriate amount (Maas, Schaltegger and Crutzen, 2016) . Land also

recorded as 200000 rather than to 100000 because of amount will be increased in potential time

so it has been taken increased amount.

(c) Goodwill:

In business the collection that is accounted in order to make purchase, there are many

crucial effect on accounting income of the customer those are preparing to buy goods. It is

observed that when purchase are relevant to the active business firms instead of simply separated

assets, then organization are mainly to ascertained the overall price which are not linked with the

values of single assets. They are basically related to the going-concern value that often related to

the excess of fair values attributable which are linked with value of assets and are equal to net

liabilities for an organisation (Qiu, Shaukat and Tharyan, 2016) In these condition, rather of

distributing the total price of purchase assets that are displayed on the accounting books of SWL

limited, accountants better realize that abstract assets which commonly known as "goodwill,"

must be happen on the books of respective company.

There another difficulty originate is related in concern with allocating of the total

purchase price to those of the acquired assets, which also includes goodwill. To better resolved

the issues of goodwill there is a two-step process which is totally different from the one-step

method that is commonly known as basket purchase of separated assets for company. The

includes two steps such as the purchase price is distributed among the identifiable intangible and

tangible assets which are purchased on the fair value and further it includes any balance is than

debited to the new intangible asset account the named “goodwill”

3. (d) As per the dividend information it is sited that:

On acquisition. As noted previously, on acquisition of the SWL ltd. Shares entered at cost

on in the books of EZY ltd. A debit to an account, which may be labelled “Investments,”

and a credit to cash or whatever, was used to pay the seller.

During the holding of the shares of SWL limited. When the SWL limited Corp. Shares

are accounted for by the equity method, EZY manufacturer must: (i) Recognize EZY's

proportionate share of SWL's post-acquisition earnings by debiting (on SWL's financial

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

statements) "investments" and crediting a revenue account. Any intercompany

transactions must be eliminated, as for consolidated statements.

This will result in Range balance sheet assets. (and consequently net worth) being

increased for profits of SWL, or decreased for losses of SWL, and Range Ltd. income statement

being similarly affected. (ii) Recognize a charge against revenues for certain imputed

depreciation, cost of sales, and amortization expense (Schaltegger, Burritt and Petersen, 2017)..

This is the little known adjustment referred to above which will be explained immediately

following this summary.'

QUESTION 4

Covered in Excel

CONCLUSION

As per the above report it has been concluded that corporate accounting sets new

standards and it is easy to understand. In all financial data apply their approach at the time of

acquisition, amalgamation and other time. There are recording journal entries in the accounting

records because there are keep record of daily activities regrading to business. All details

transactions are recorded in proper formate with date. After that with the help of journal entries

prepare ledgers and track to multiple accounts. Acquisition analysis use to calculate the purchase

price of an acquisition after the exchange of market value of the shares. Strategic analysis more

profitable for the acquisition analysis. There are calculated unrealized profit regarding to

investment and it can show profitable position that has been sold in return for cash. There are

showing position of stock in reference to increase capital gains.

7

transactions must be eliminated, as for consolidated statements.

This will result in Range balance sheet assets. (and consequently net worth) being

increased for profits of SWL, or decreased for losses of SWL, and Range Ltd. income statement

being similarly affected. (ii) Recognize a charge against revenues for certain imputed

depreciation, cost of sales, and amortization expense (Schaltegger, Burritt and Petersen, 2017)..

This is the little known adjustment referred to above which will be explained immediately

following this summary.'

QUESTION 4

Covered in Excel

CONCLUSION

As per the above report it has been concluded that corporate accounting sets new

standards and it is easy to understand. In all financial data apply their approach at the time of

acquisition, amalgamation and other time. There are recording journal entries in the accounting

records because there are keep record of daily activities regrading to business. All details

transactions are recorded in proper formate with date. After that with the help of journal entries

prepare ledgers and track to multiple accounts. Acquisition analysis use to calculate the purchase

price of an acquisition after the exchange of market value of the shares. Strategic analysis more

profitable for the acquisition analysis. There are calculated unrealized profit regarding to

investment and it can show profitable position that has been sold in return for cash. There are

showing position of stock in reference to increase capital gains.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Belal, A. R., 2016. Corporate social responsibility reporting in developing countries: The case

of Bangladesh. Routledge.

Caskey, J. and Laux, V., 2016. Corporate governance, accounting conservatism, and

manipulation. Management Science. 63(2). pp.424-437.

Collier, P. M., 2015. Accounting for managers: Interpreting accounting information for decision

making. John Wiley & Sons.

Epstein, M. J., 2018. Making sustainability work: Best practices in managing and measuring

corporate social, environmental and economic impacts. Routledge.

Henderson, S., and et.al., 2015. Issues in financial accounting. Pearson Higher Education AU.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production. 136.

pp.237-248.

Qiu, Y., Shaukat, A. and Tharyan, R., 2016. Environmental and social disclosures: Link with

corporate financial performance. The British Accounting Review. 48(1). pp.102-116.

Schaltegger, S., Burritt, R. and Petersen, H., 2017. An introduction to corporate environmental

management: Striving for sustainability. Routledge.

8

Books and Journals

Belal, A. R., 2016. Corporate social responsibility reporting in developing countries: The case

of Bangladesh. Routledge.

Caskey, J. and Laux, V., 2016. Corporate governance, accounting conservatism, and

manipulation. Management Science. 63(2). pp.424-437.

Collier, P. M., 2015. Accounting for managers: Interpreting accounting information for decision

making. John Wiley & Sons.

Epstein, M. J., 2018. Making sustainability work: Best practices in managing and measuring

corporate social, environmental and economic impacts. Routledge.

Henderson, S., and et.al., 2015. Issues in financial accounting. Pearson Higher Education AU.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production. 136.

pp.237-248.

Qiu, Y., Shaukat, A. and Tharyan, R., 2016. Environmental and social disclosures: Link with

corporate financial performance. The British Accounting Review. 48(1). pp.102-116.

Schaltegger, S., Burritt, R. and Petersen, H., 2017. An introduction to corporate environmental

management: Striving for sustainability. Routledge.

8

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.