Corporate Accounting & Reporting: Lease Accounting & Impairment Loss

VerifiedAdded on 2023/06/05

|6

|1394

|189

Report

AI Summary

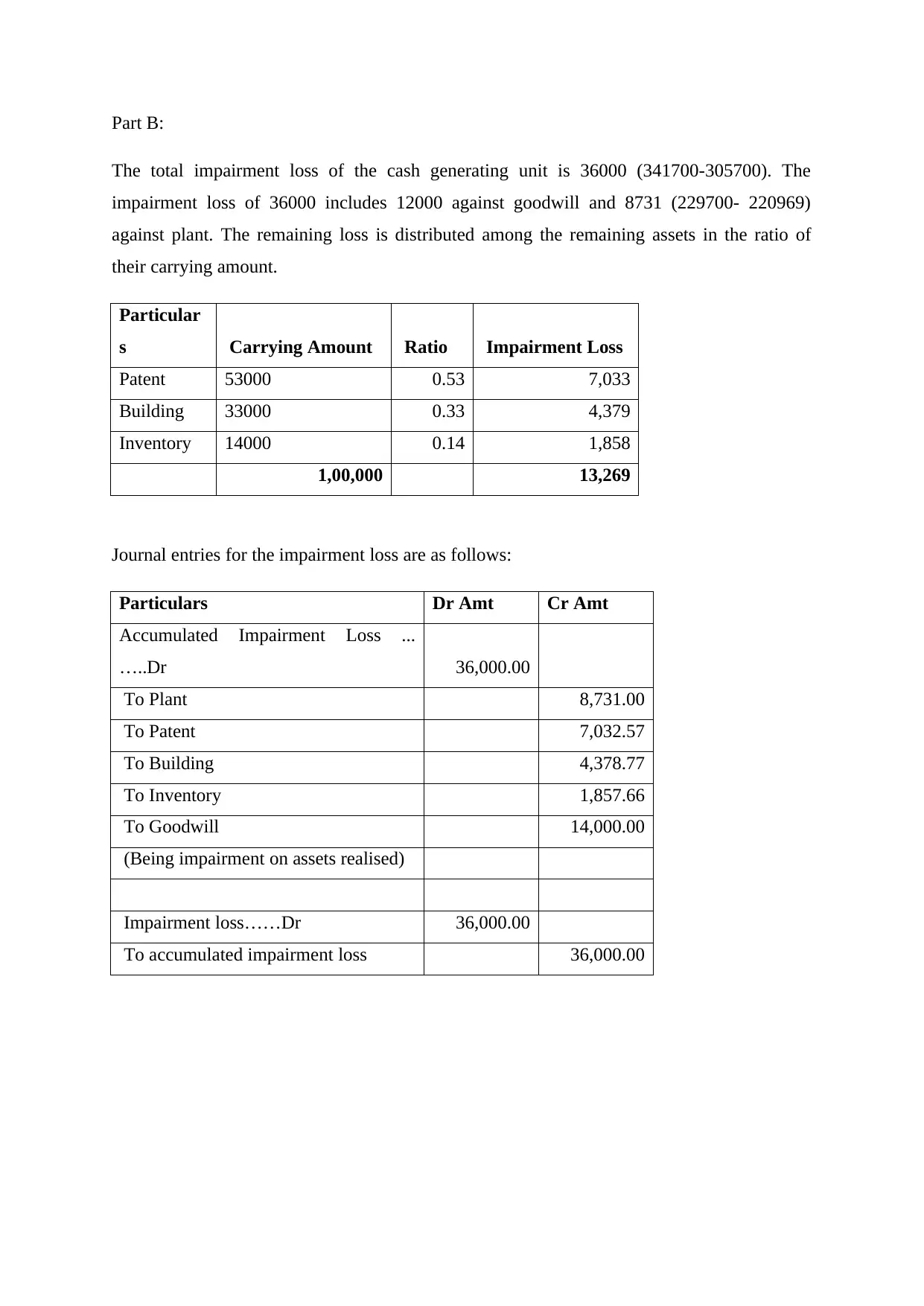

This report provides a detailed analysis of corporate accounting principles, focusing on lease agreements and impairment loss. It defines leases, differentiates between financial and operating leases, and explains the accounting treatment for lessees, including the valuation of right-to-use assets and lease liabilities. It also covers the cost model, depreciation, and adjustments to lease liabilities. The report further addresses the presentation of financial statements, disclosure requirements, and maturity analysis. Additionally, it includes a practical example of impairment loss calculation for a cash-generating unit, demonstrating the allocation of impairment loss across various assets and providing relevant journal entries. Desklib offers similar solved assignments and past papers for students.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.