Corporate Accounting: Reserves, Dividends, and Impairment Analysis

VerifiedAdded on 2023/03/31

|12

|2453

|187

Report

AI Summary

This corporate accounting assignment provides a detailed analysis of reserves and impairment. The report is divided into two parts. Part A explains the nature of reserves, their movement, including the treatment of dividends, and various types of reserves and their purposes. Part B presents a case study on impairment for Gali Limited, solved according to accounting standards, including journal entries and relevant workings. The assignment covers revenue and capital reserves, fair value reserves, asset revaluation reserves, hedging reserves, foreign currency translation reserves, and statutory reserves. It also discusses dividend distribution and disclosure of reserves in the balance sheet. The impairment analysis includes calculations for goodwill and other assets, adhering to accounting standards.

CORPORATE ACCOUNTING ASSIGNMENT

MAY 27, 2019

Student name

University Name

MAY 27, 2019

Student name

University Name

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 16 May 2019.

1 | P a g e

By student name

Professor

University

Date: 16 May 2019.

1 | P a g e

2

Executive Summary

This report is a Corporate accounting based assignment whereby there are 2 parts. In the first

part, the nature of reserves and the movement in the reserves has been explained in detail

including the treatment of dividend. Various types of reserves and the reason for which they are

formed has been explained in detail. In the second part, a case study on impairment has been

given which has been solved using the rules of impairment as per the accounting standards. The

journal entries and the relevant workings with respect to impairment has also been shown.

2 | P a g e

Executive Summary

This report is a Corporate accounting based assignment whereby there are 2 parts. In the first

part, the nature of reserves and the movement in the reserves has been explained in detail

including the treatment of dividend. Various types of reserves and the reason for which they are

formed has been explained in detail. In the second part, a case study on impairment has been

given which has been solved using the rules of impairment as per the accounting standards. The

journal entries and the relevant workings with respect to impairment has also been shown.

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Table of Contents

Part A: Nature of Reserves and their movement.........................................................................................4

Introduction.................................................................................................................................................4

Description..................................................................................................................................................4

Reserves in Accounting................................................................................................................................7

Dividend......................................................................................................................................................8

Conclusion...................................................................................................................................................9

Disclosure of Reserves in Balance sheet..................................................................................................9

Part B: Calculation for Impairment for Gali Limited.....................................................................................9

References.................................................................................................................................................11

3 | P a g e

Table of Contents

Part A: Nature of Reserves and their movement.........................................................................................4

Introduction.................................................................................................................................................4

Description..................................................................................................................................................4

Reserves in Accounting................................................................................................................................7

Dividend......................................................................................................................................................8

Conclusion...................................................................................................................................................9

Disclosure of Reserves in Balance sheet..................................................................................................9

Part B: Calculation for Impairment for Gali Limited.....................................................................................9

References.................................................................................................................................................11

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Part A: Nature of Reserves and their movement

Introduction

Reserves are profits, which have been set aside for a particular purpose or to expand or

strengthen the financial position of the business. Sometimes reserves are also referred to as

retained earnings. Reserves as a component of financial statement is very important because

amount, which is set aside for reserves, reduces the net profit of the company. Thus, thorough

understanding of reserves, how they are created or made is very much important for the company

(Appelbaum, et al., 2018).

Reserves are kept aside for various purposes such as it can be used for purchase of any fixed

assets, repaying of debts, for payment of bonuses, fund expansions, dividend payments.

Sometimes provisions are misinterpreted as reserves but they are actually not same as a provision

is a liability which is yet to come and whose cost or date is not confirmed. AASB has prescribed

AASB 101 for presentation of financial statement under section 334 of Corporations Act, 2001.

AASB 101 sets out basis for presentation of general-purpose financial statement for making

comparison of company’s financial statement of previous period with that of other entity’s.

Description

Reserves has a credit balance in balance sheet and referred as a part of shareholders equity. A

reserve can be any part of shareholders’ equity except for basic share capital. There are various

types of reserves, which are used, in financial reporting but these reserves are broadly classified

under two types:

1. Revenue Reserves

2. Capital Reserves

Revenue Reserves: Revenue reserves are those reserves, which are retained or set aside

by the company for business expansion or investment in future growth of the company. Revenue

reserves are not distributed to the shareholders in the form of any dividend or bonus. These are

profits, which are earned by company through its normal operations. Revenue reserves are

further classified into two types (Alexander, 2016):

a.) General Reserves: General reserves are those reserves, which are not for any specific or

particular purpose but as the name specifies these are for general purpose including for

general financial strengthening of the entity (Arnott, et al., 2017).

b.) Specific Reserves: As the name specifies, specific reserves are those reserves, which are

kept aside for a specific purpose, which cannot be used for any other purpose except for

the purpose for which it is kept aside. Sometimes specific reserves are also referred to as

special reserves. Examples of various specific reserves are Dividend equalization

reserve, capital redemption reserves, Contingency reserves, Debenture redemption

4 | P a g e

Part A: Nature of Reserves and their movement

Introduction

Reserves are profits, which have been set aside for a particular purpose or to expand or

strengthen the financial position of the business. Sometimes reserves are also referred to as

retained earnings. Reserves as a component of financial statement is very important because

amount, which is set aside for reserves, reduces the net profit of the company. Thus, thorough

understanding of reserves, how they are created or made is very much important for the company

(Appelbaum, et al., 2018).

Reserves are kept aside for various purposes such as it can be used for purchase of any fixed

assets, repaying of debts, for payment of bonuses, fund expansions, dividend payments.

Sometimes provisions are misinterpreted as reserves but they are actually not same as a provision

is a liability which is yet to come and whose cost or date is not confirmed. AASB has prescribed

AASB 101 for presentation of financial statement under section 334 of Corporations Act, 2001.

AASB 101 sets out basis for presentation of general-purpose financial statement for making

comparison of company’s financial statement of previous period with that of other entity’s.

Description

Reserves has a credit balance in balance sheet and referred as a part of shareholders equity. A

reserve can be any part of shareholders’ equity except for basic share capital. There are various

types of reserves, which are used, in financial reporting but these reserves are broadly classified

under two types:

1. Revenue Reserves

2. Capital Reserves

Revenue Reserves: Revenue reserves are those reserves, which are retained or set aside

by the company for business expansion or investment in future growth of the company. Revenue

reserves are not distributed to the shareholders in the form of any dividend or bonus. These are

profits, which are earned by company through its normal operations. Revenue reserves are

further classified into two types (Alexander, 2016):

a.) General Reserves: General reserves are those reserves, which are not for any specific or

particular purpose but as the name specifies these are for general purpose including for

general financial strengthening of the entity (Arnott, et al., 2017).

b.) Specific Reserves: As the name specifies, specific reserves are those reserves, which are

kept aside for a specific purpose, which cannot be used for any other purpose except for

the purpose for which it is kept aside. Sometimes specific reserves are also referred to as

special reserves. Examples of various specific reserves are Dividend equalization

reserve, capital redemption reserves, Contingency reserves, Debenture redemption

4 | P a g e

5

reserves etc. Bad debt reserve is the best example for specific reserve as this is an

amount, which is kept aside in case customer is unable to pay (Belton, 2017).

Creation of revenue reserve from profit: The thing, which should be kept in mind, is that

revenue reserve of a company is just not on the books of the company rather it is actual money,

which is earned, by company out of its real profits. Creation of revenue reserves can be better

explained through example:

Example showing creation of revenue reserves:

5 | P a g e

reserves etc. Bad debt reserve is the best example for specific reserve as this is an

amount, which is kept aside in case customer is unable to pay (Belton, 2017).

Creation of revenue reserve from profit: The thing, which should be kept in mind, is that

revenue reserve of a company is just not on the books of the company rather it is actual money,

which is earned, by company out of its real profits. Creation of revenue reserves can be better

explained through example:

Example showing creation of revenue reserves:

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Here, in this example we can see the net profit of two years which is real money and

which is available in books as well as in cash.

We can see that net profits of 2 years in year 2015 and 2016 are $47000 and $48000

Let us assume 50% of the profits will be transferred to revenue reserves, the amount

would be 48000*50% i.e. $24000 for year 2015 and 47,000*50% i.e. $23500, so total

revenue reserve for the year 2016 will be $23,500+$24,000 = $47,500 (Choy, 2018).

These amounts will be shown in balance sheet under reserves as retained earnings in

shareholders fund.

Uses of Revenue Reserves: Revenue reserves are used for following purposes:

1. Payment of dividend to its shareholders

2. To expand its business operations

3. For the purpose of stabilizing the rate of dividend

Capital Reserves: Capital reserves are those reserves, which are made or created out of

capital profits, and normally they are not available for distribution to shareholders of the

company as dividend. It is to be noted that capital reserves cannot be made or created from the

profits earned from normal trading activities or from its core operations of a company. Capital

reserves are usually set aside for meeting capital losses or helps company in case of

unpredictable events like inflation, business expansion or get into new project (Sithole, et al.,

2017). There are various examples of capital reserves like profit on sale of any fixed assets of the

company, profit on sale of shares of company etc. In case company sells or dispose its assets and

earn some profit out of it then in that case company can transfer that profit to capital reserve.

Suppose if company sells its assets and on sell if there is any capital loss to the company in that

case, company can use capital reserve to mitigate or reduce its loss or any other contingencies.

Capital reserves are not related to any operational activities of the company hence it is nothing to

do with operational efficiency (Lessambo, 2018).

Let us understand capital reserve by taking a practical example: Let us say company want to buy

a machine to increase its operational efficiency for which company needs capital. Moreover,

company do not want to take any loan from outside or financial institution, as the cost of raising

funds will be very high. In that case, company plans to create a capital reserve. Therefore,

company sell out its old machineries or any other assets and money received from sell of those

assets are directly transferred to the capital reserve. In addition, since it is not a free reserve so

6 | P a g e

Here, in this example we can see the net profit of two years which is real money and

which is available in books as well as in cash.

We can see that net profits of 2 years in year 2015 and 2016 are $47000 and $48000

Let us assume 50% of the profits will be transferred to revenue reserves, the amount

would be 48000*50% i.e. $24000 for year 2015 and 47,000*50% i.e. $23500, so total

revenue reserve for the year 2016 will be $23,500+$24,000 = $47,500 (Choy, 2018).

These amounts will be shown in balance sheet under reserves as retained earnings in

shareholders fund.

Uses of Revenue Reserves: Revenue reserves are used for following purposes:

1. Payment of dividend to its shareholders

2. To expand its business operations

3. For the purpose of stabilizing the rate of dividend

Capital Reserves: Capital reserves are those reserves, which are made or created out of

capital profits, and normally they are not available for distribution to shareholders of the

company as dividend. It is to be noted that capital reserves cannot be made or created from the

profits earned from normal trading activities or from its core operations of a company. Capital

reserves are usually set aside for meeting capital losses or helps company in case of

unpredictable events like inflation, business expansion or get into new project (Sithole, et al.,

2017). There are various examples of capital reserves like profit on sale of any fixed assets of the

company, profit on sale of shares of company etc. In case company sells or dispose its assets and

earn some profit out of it then in that case company can transfer that profit to capital reserve.

Suppose if company sells its assets and on sell if there is any capital loss to the company in that

case, company can use capital reserve to mitigate or reduce its loss or any other contingencies.

Capital reserves are not related to any operational activities of the company hence it is nothing to

do with operational efficiency (Lessambo, 2018).

Let us understand capital reserve by taking a practical example: Let us say company want to buy

a machine to increase its operational efficiency for which company needs capital. Moreover,

company do not want to take any loan from outside or financial institution, as the cost of raising

funds will be very high. In that case, company plans to create a capital reserve. Therefore,

company sell out its old machineries or any other assets and money received from sell of those

assets are directly transferred to the capital reserve. In addition, since it is not a free reserve so

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

company to pay any dividend to its shareholders cannot use it. Hence, the amount transferred to

capital reserve can be used to buy machine (Heminway, 2017).

Capital Reserve Exceptions:

a. Company not always create capital reserve for specific project rather sometimes company

create capital reserve for meeting any inflation, recession or excessive competition.

Therefore, for that purpose company can transfer any money received from sell of any

assets and can create a reserve.

b. Profits on sell off assets are not always received in money value sometimes there can be

profit because of revaluation so in that case also profits are transferred to reserve

irrespective of actual receipt of money (Jefferson, 2017).

Reserves in Accounting

While doing the accounting what company do is debit the retained earning accounts and credit

the same amount to reserve account. In case the activity for which reserve was created gets

complete then the entry is reversed and if there is any balancing figure it is transferred to the

retained earnings account.

Apart from two major reserves there are other reserves also which are very important for any

company such as:

Fair value reserves: These reserves are important for businesses like property and Insurance

Company who holds huge amount of fixed income investments. Available for sale assets and

securities are generally included (Gooley, 2016).

Asset Revaluation Reserves: These reserves are created when the adjustment is made in the

value of asset in balance sheet and in need of offsetting the transaction.

Hedging Reserves: company to hedge itself from any volatility in certain costs creates these

reserves.

Foreign currency translation Reserves: These reserves are created by company when there is

change in value of currency in which balance is reported and in which currency assets are held in

balance sheet (Dichev, 2017).

Statutory Reserves: These reserves are those reserves which company creates doe to the

requirement of law or regulation and company cannot pay statutory reserves as dividends.

7 | P a g e

company to pay any dividend to its shareholders cannot use it. Hence, the amount transferred to

capital reserve can be used to buy machine (Heminway, 2017).

Capital Reserve Exceptions:

a. Company not always create capital reserve for specific project rather sometimes company

create capital reserve for meeting any inflation, recession or excessive competition.

Therefore, for that purpose company can transfer any money received from sell of any

assets and can create a reserve.

b. Profits on sell off assets are not always received in money value sometimes there can be

profit because of revaluation so in that case also profits are transferred to reserve

irrespective of actual receipt of money (Jefferson, 2017).

Reserves in Accounting

While doing the accounting what company do is debit the retained earning accounts and credit

the same amount to reserve account. In case the activity for which reserve was created gets

complete then the entry is reversed and if there is any balancing figure it is transferred to the

retained earnings account.

Apart from two major reserves there are other reserves also which are very important for any

company such as:

Fair value reserves: These reserves are important for businesses like property and Insurance

Company who holds huge amount of fixed income investments. Available for sale assets and

securities are generally included (Gooley, 2016).

Asset Revaluation Reserves: These reserves are created when the adjustment is made in the

value of asset in balance sheet and in need of offsetting the transaction.

Hedging Reserves: company to hedge itself from any volatility in certain costs creates these

reserves.

Foreign currency translation Reserves: These reserves are created by company when there is

change in value of currency in which balance is reported and in which currency assets are held in

balance sheet (Dichev, 2017).

Statutory Reserves: These reserves are those reserves which company creates doe to the

requirement of law or regulation and company cannot pay statutory reserves as dividends.

7 | P a g e

8

Dividend

A dividend is not an expense for the company rather it is a distribution of its retained earnings. A

dividend is distributed to shareholders in the proportion of number of shares held by them.

Dividend cannot be paid out of any reserves other than the free reserves (Vieira, et al., 2017).

Below table shows how dividends appear or affect financial statement:

There is no impact on balance sheet before dividend is paid. When dividend is paid, it reduces

the amount of retained earnings in the balance sheet.

As per AASB 101, company shall disclose the following in the notes:

Conclusion

Disclosure of Reserves in Balance sheet

Reserves and surplus are disclosed in balance sheet on liabilities side under the head ‘Equity and

Liabilities’ under sub head ‘Shareholders’ funds.

8 | P a g e

Dividend

A dividend is not an expense for the company rather it is a distribution of its retained earnings. A

dividend is distributed to shareholders in the proportion of number of shares held by them.

Dividend cannot be paid out of any reserves other than the free reserves (Vieira, et al., 2017).

Below table shows how dividends appear or affect financial statement:

There is no impact on balance sheet before dividend is paid. When dividend is paid, it reduces

the amount of retained earnings in the balance sheet.

As per AASB 101, company shall disclose the following in the notes:

Conclusion

Disclosure of Reserves in Balance sheet

Reserves and surplus are disclosed in balance sheet on liabilities side under the head ‘Equity and

Liabilities’ under sub head ‘Shareholders’ funds.

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

As per AASB 101, company shall disclose in either the Balance sheet or statement of changes in

the equity or in the notes to accounts a description or explanation of the nature and the need of

each reserve made or shown in the books (Kim, et al., 2017).

Part B: Calculation for Impairment for Gali Limited

Gali limited is the entity, which has been given in the question. It has identified fine china

division as one of its cash-generating unit for the purpose of the impairment. The carrying values

of the assets of the company as on 30th June 2015 has been given below along with the other

inputs as well:

Gali Ltd.

Impairment calculation as on 30th June, 2015

Account Carrying amount

Plant 190,700

Brand 44,000

Fittings 28,000

Inventory 12,000

Goodwill 10,000

Total carrying amount 284,700

Value in Use of division 254,700

Fair value less cost of disposal of Plant 183,441

Impairment is the amount of the difference between the carrying value of the asset and the fair

value less cost of disposal or the value in use, whichever is lower (Das, 2017). Here since the fair

value less cost of disposal of the entire division has not been given so the value of impairment to

be considered is (carrying value less value in use) = (284700-254700) = $ 30000. As per the

rules laid down in Accounting standard for impairment, the amount of impairment first needs to

be allocated towards goodwill and hence impairment of goodwill here is $ 10000. The remaining

$ 30000 -$ 10000 = $ 20000 will be allocated towards the rest of the assets in the ratio of

carrying values with the exception of inventory since the current assets which are held for the

purpose of selling are not eligible for impairment. The working a calculation for the same has

been shown below:

Account Carrying Amount Pro rata Impairment loss allocated Adjusted CA

Plant 190,700 0.73 14,518 176,182

Brand 44,000 0.17 3,350 40,650

Fittings 28,000 0.11 2,132 25,868

Total CA 262700 1.00 20,000 242700

9 | P a g e

As per AASB 101, company shall disclose in either the Balance sheet or statement of changes in

the equity or in the notes to accounts a description or explanation of the nature and the need of

each reserve made or shown in the books (Kim, et al., 2017).

Part B: Calculation for Impairment for Gali Limited

Gali limited is the entity, which has been given in the question. It has identified fine china

division as one of its cash-generating unit for the purpose of the impairment. The carrying values

of the assets of the company as on 30th June 2015 has been given below along with the other

inputs as well:

Gali Ltd.

Impairment calculation as on 30th June, 2015

Account Carrying amount

Plant 190,700

Brand 44,000

Fittings 28,000

Inventory 12,000

Goodwill 10,000

Total carrying amount 284,700

Value in Use of division 254,700

Fair value less cost of disposal of Plant 183,441

Impairment is the amount of the difference between the carrying value of the asset and the fair

value less cost of disposal or the value in use, whichever is lower (Das, 2017). Here since the fair

value less cost of disposal of the entire division has not been given so the value of impairment to

be considered is (carrying value less value in use) = (284700-254700) = $ 30000. As per the

rules laid down in Accounting standard for impairment, the amount of impairment first needs to

be allocated towards goodwill and hence impairment of goodwill here is $ 10000. The remaining

$ 30000 -$ 10000 = $ 20000 will be allocated towards the rest of the assets in the ratio of

carrying values with the exception of inventory since the current assets which are held for the

purpose of selling are not eligible for impairment. The working a calculation for the same has

been shown below:

Account Carrying Amount Pro rata Impairment loss allocated Adjusted CA

Plant 190,700 0.73 14,518 176,182

Brand 44,000 0.17 3,350 40,650

Fittings 28,000 0.11 2,132 25,868

Total CA 262700 1.00 20,000 242700

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

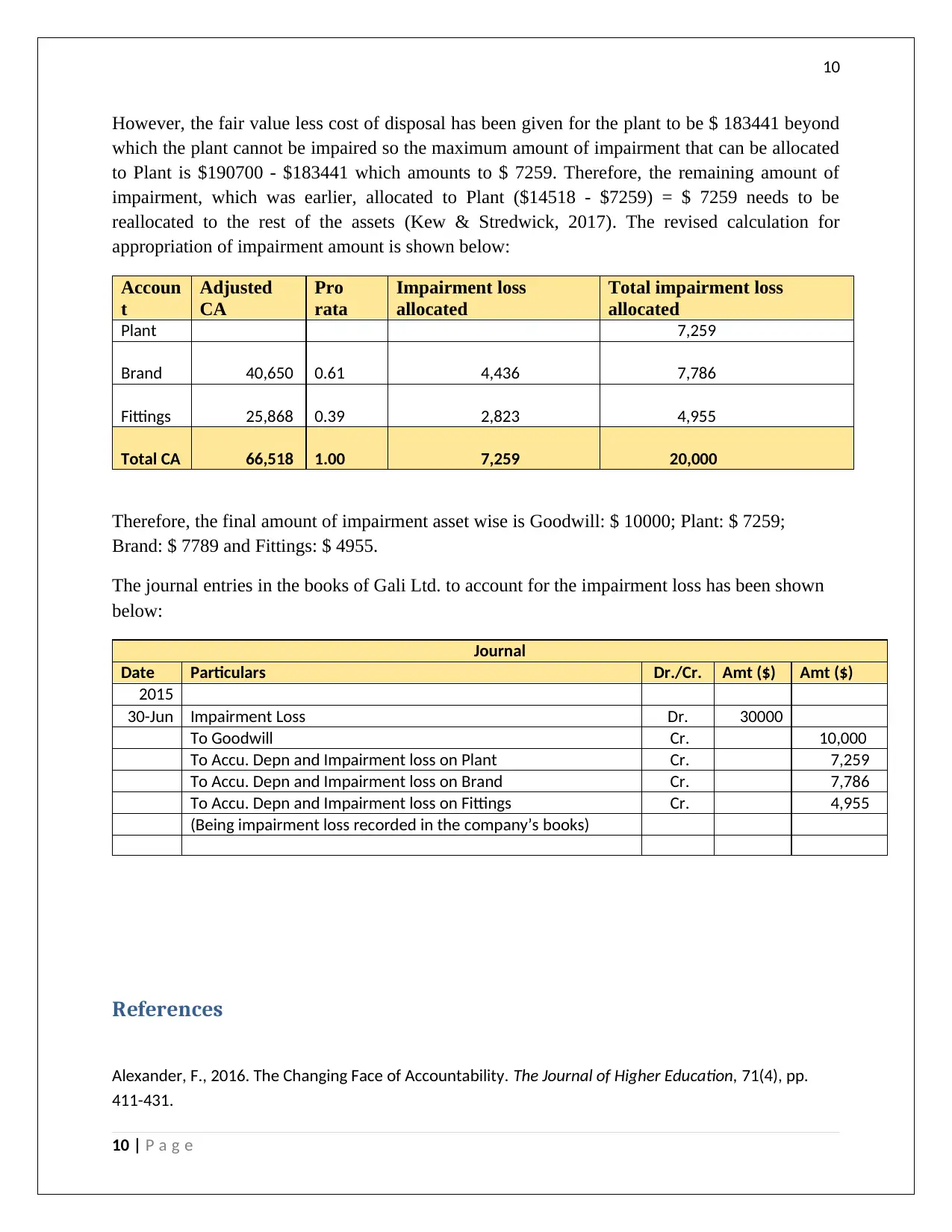

However, the fair value less cost of disposal has been given for the plant to be $ 183441 beyond

which the plant cannot be impaired so the maximum amount of impairment that can be allocated

to Plant is $190700 - $183441 which amounts to $ 7259. Therefore, the remaining amount of

impairment, which was earlier, allocated to Plant ($14518 - $7259) = $ 7259 needs to be

reallocated to the rest of the assets (Kew & Stredwick, 2017). The revised calculation for

appropriation of impairment amount is shown below:

Accoun

t

Adjusted

CA

Pro

rata

Impairment loss

allocated

Total impairment loss

allocated

Plant 7,259

Brand 40,650 0.61 4,436 7,786

Fittings 25,868 0.39 2,823 4,955

Total CA 66,518 1.00 7,259 20,000

Therefore, the final amount of impairment asset wise is Goodwill: $ 10000; Plant: $ 7259;

Brand: $ 7789 and Fittings: $ 4955.

The journal entries in the books of Gali Ltd. to account for the impairment loss has been shown

below:

Journal

Date Particulars Dr./Cr. Amt ($) Amt ($)

2015

30-Jun Impairment Loss Dr. 30000

To Goodwill Cr. 10,000

To Accu. Depn and Impairment loss on Plant Cr. 7,259

To Accu. Depn and Impairment loss on Brand Cr. 7,786

To Accu. Depn and Impairment loss on Fittings Cr. 4,955

(Being impairment loss recorded in the company’s books)

References

Alexander, F., 2016. The Changing Face of Accountability. The Journal of Higher Education, 71(4), pp.

411-431.

10 | P a g e

However, the fair value less cost of disposal has been given for the plant to be $ 183441 beyond

which the plant cannot be impaired so the maximum amount of impairment that can be allocated

to Plant is $190700 - $183441 which amounts to $ 7259. Therefore, the remaining amount of

impairment, which was earlier, allocated to Plant ($14518 - $7259) = $ 7259 needs to be

reallocated to the rest of the assets (Kew & Stredwick, 2017). The revised calculation for

appropriation of impairment amount is shown below:

Accoun

t

Adjusted

CA

Pro

rata

Impairment loss

allocated

Total impairment loss

allocated

Plant 7,259

Brand 40,650 0.61 4,436 7,786

Fittings 25,868 0.39 2,823 4,955

Total CA 66,518 1.00 7,259 20,000

Therefore, the final amount of impairment asset wise is Goodwill: $ 10000; Plant: $ 7259;

Brand: $ 7789 and Fittings: $ 4955.

The journal entries in the books of Gali Ltd. to account for the impairment loss has been shown

below:

Journal

Date Particulars Dr./Cr. Amt ($) Amt ($)

2015

30-Jun Impairment Loss Dr. 30000

To Goodwill Cr. 10,000

To Accu. Depn and Impairment loss on Plant Cr. 7,259

To Accu. Depn and Impairment loss on Brand Cr. 7,786

To Accu. Depn and Impairment loss on Fittings Cr. 4,955

(Being impairment loss recorded in the company’s books)

References

Alexander, F., 2016. The Changing Face of Accountability. The Journal of Higher Education, 71(4), pp.

411-431.

10 | P a g e

11

Appelbaum, D., Kogan, A. & Vasarhelyi, M., 2018. Analytical procedures in external auditing: A

comprehensive literature survey and framework for external audit analytics.. Journal of Accounting

Literature, 40(1), pp. 83-101.

Arnott, D., Lizama, F. & Song, Y., 2017. Patterns of business intelligence systems use in organizations.

Decision Support Systems, Volume 97, pp. 58-68.

Belton, P., 2017. Competitive Strategy: Creating and Sustaining Superior Performance. London: Macat

International ltd.

Choy, Y. K., 2018. Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview Analysis.

Ecological Economics, 3(1), p. 145.

Das, P., 2017. Financing Pattern and Utilization of Fixed Assets - A Study. Asian Journal of Social Science

Studies, 2(2), pp. 10-17.

Dichev, I., 2017. On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), pp. 617-632.

Gooley, J., 2016. Principles of Australian Contract Law. 2 ed. Australia: Lexis Nexis.

Heminway, J., 2017. Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, pp. 1-35.

Jefferson, M., 2017. Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland.

Technological Forecasting and Social Change, pp. 353-354.

Kew, J. & Stredwick, J., 2017. Business Environment: Managing in a Strategic Context. 2nd ed. London:

Chartered Institute of Personnel and Development.

Kim, M., Schmidgall, R. & Damitio, J., 2017. Key Managerial Accounting Skills for Lodging Industry

Managers: The Third Phase of a Repeated Cross-Sectional Study. International Journal of Hospitality &

Tourism Administration, , 18(1), pp. 23-40.

Lessambo, F., 2018. Audit Risks: Identification and Procedures. Auditing, Assurance Services, and

Forensics, 3(1), pp. 183-202.

Sithole, S., Chandler, P., Abeysekera, I. & Paas, F., 2017. Benefits of guided self-management of attention

on learning accounting. Journal of Educational Psychology, 109(2), p. 220.

Vieira, R., O’Dwyer, B. & Schneider, R., 2017. Aligning Strategy and Performance Management Systems.

SAGE Journals, 30(1), pp. 23-48.

11 | P a g e

Appelbaum, D., Kogan, A. & Vasarhelyi, M., 2018. Analytical procedures in external auditing: A

comprehensive literature survey and framework for external audit analytics.. Journal of Accounting

Literature, 40(1), pp. 83-101.

Arnott, D., Lizama, F. & Song, Y., 2017. Patterns of business intelligence systems use in organizations.

Decision Support Systems, Volume 97, pp. 58-68.

Belton, P., 2017. Competitive Strategy: Creating and Sustaining Superior Performance. London: Macat

International ltd.

Choy, Y. K., 2018. Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview Analysis.

Ecological Economics, 3(1), p. 145.

Das, P., 2017. Financing Pattern and Utilization of Fixed Assets - A Study. Asian Journal of Social Science

Studies, 2(2), pp. 10-17.

Dichev, I., 2017. On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), pp. 617-632.

Gooley, J., 2016. Principles of Australian Contract Law. 2 ed. Australia: Lexis Nexis.

Heminway, J., 2017. Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, pp. 1-35.

Jefferson, M., 2017. Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland.

Technological Forecasting and Social Change, pp. 353-354.

Kew, J. & Stredwick, J., 2017. Business Environment: Managing in a Strategic Context. 2nd ed. London:

Chartered Institute of Personnel and Development.

Kim, M., Schmidgall, R. & Damitio, J., 2017. Key Managerial Accounting Skills for Lodging Industry

Managers: The Third Phase of a Repeated Cross-Sectional Study. International Journal of Hospitality &

Tourism Administration, , 18(1), pp. 23-40.

Lessambo, F., 2018. Audit Risks: Identification and Procedures. Auditing, Assurance Services, and

Forensics, 3(1), pp. 183-202.

Sithole, S., Chandler, P., Abeysekera, I. & Paas, F., 2017. Benefits of guided self-management of attention

on learning accounting. Journal of Educational Psychology, 109(2), p. 220.

Vieira, R., O’Dwyer, B. & Schneider, R., 2017. Aligning Strategy and Performance Management Systems.

SAGE Journals, 30(1), pp. 23-48.

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.