Corporate Accounting HI5020 Assessment 2: Retail Food Group Analysis

VerifiedAdded on 2021/05/27

|9

|2078

|102

Report

AI Summary

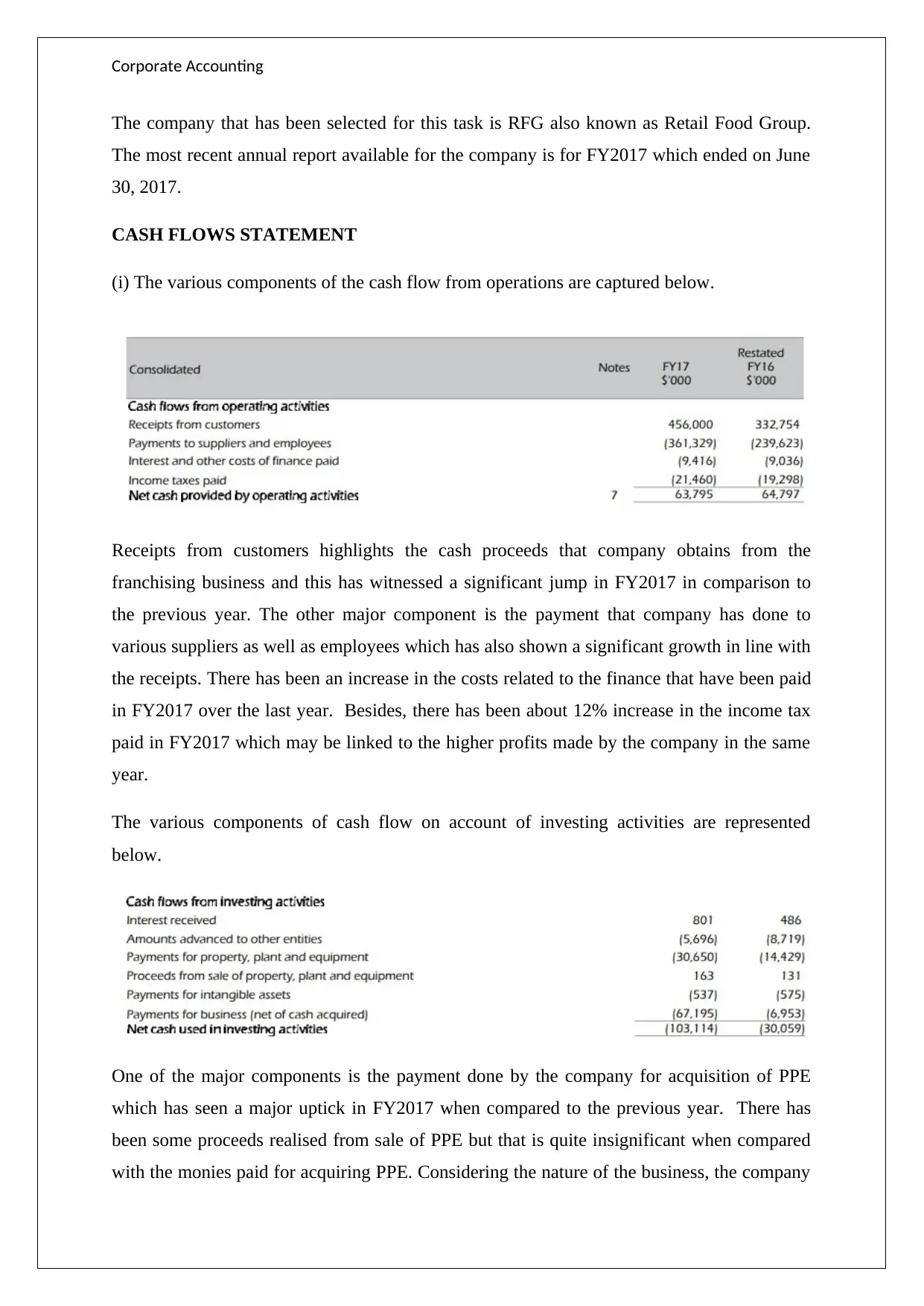

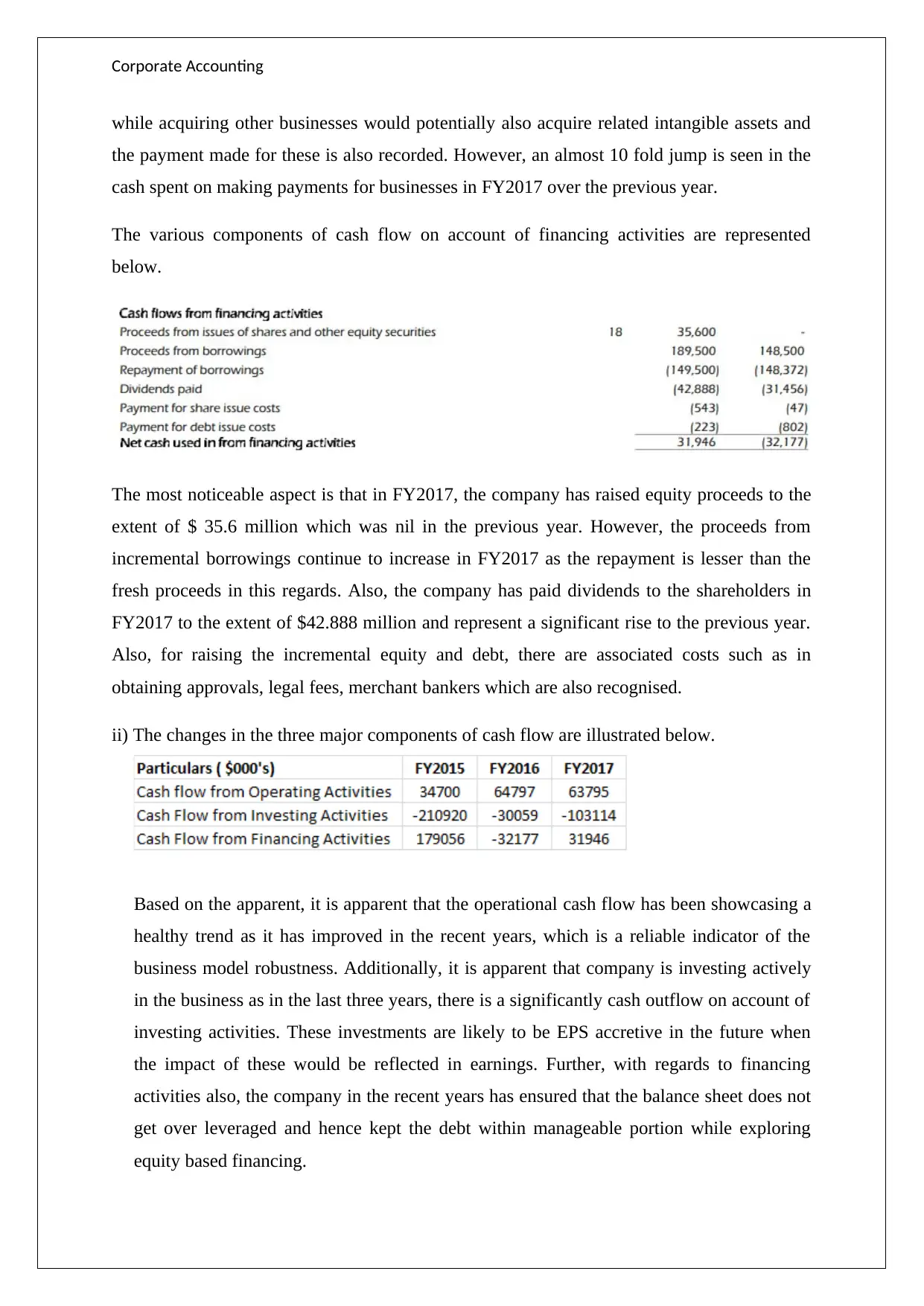

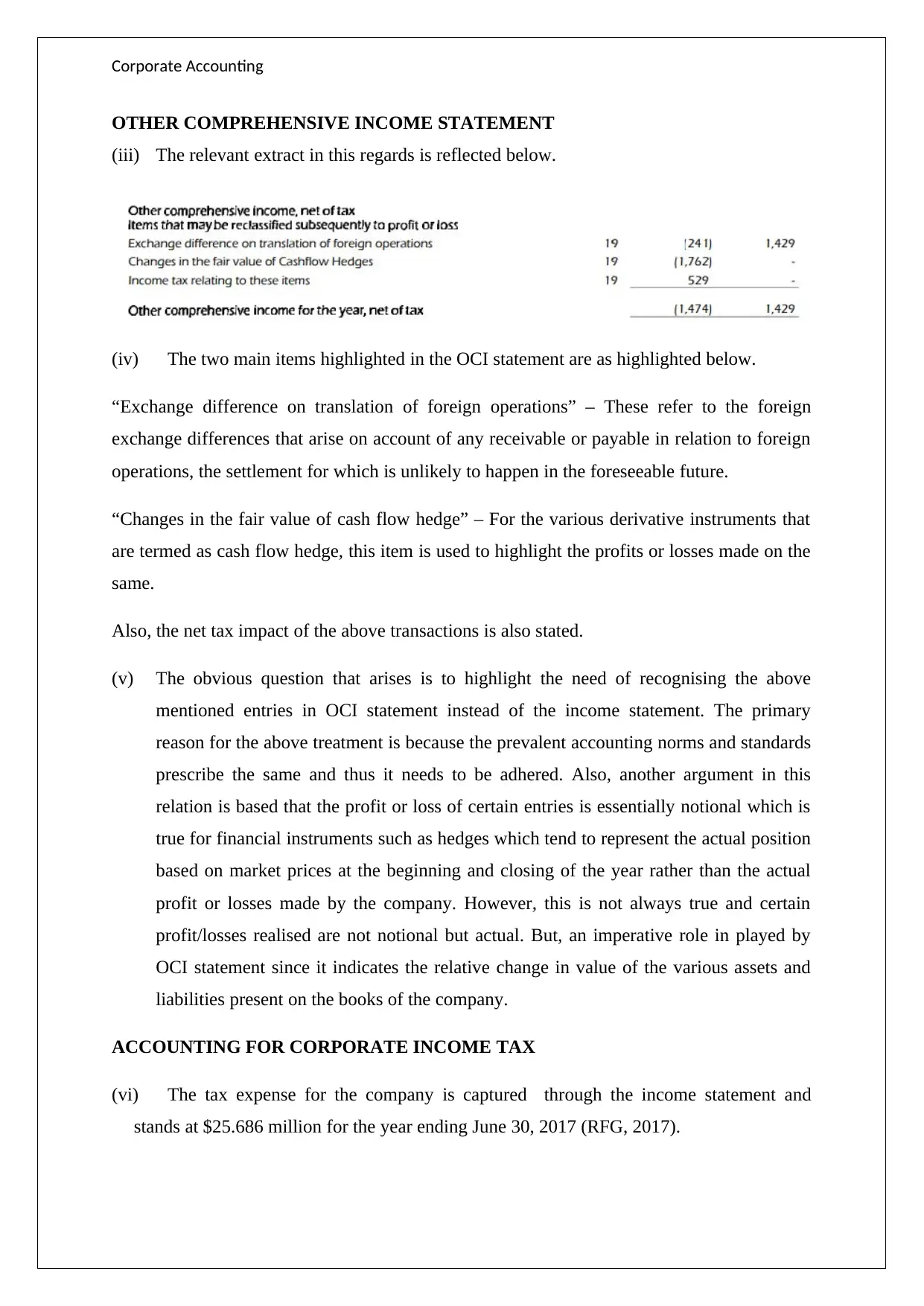

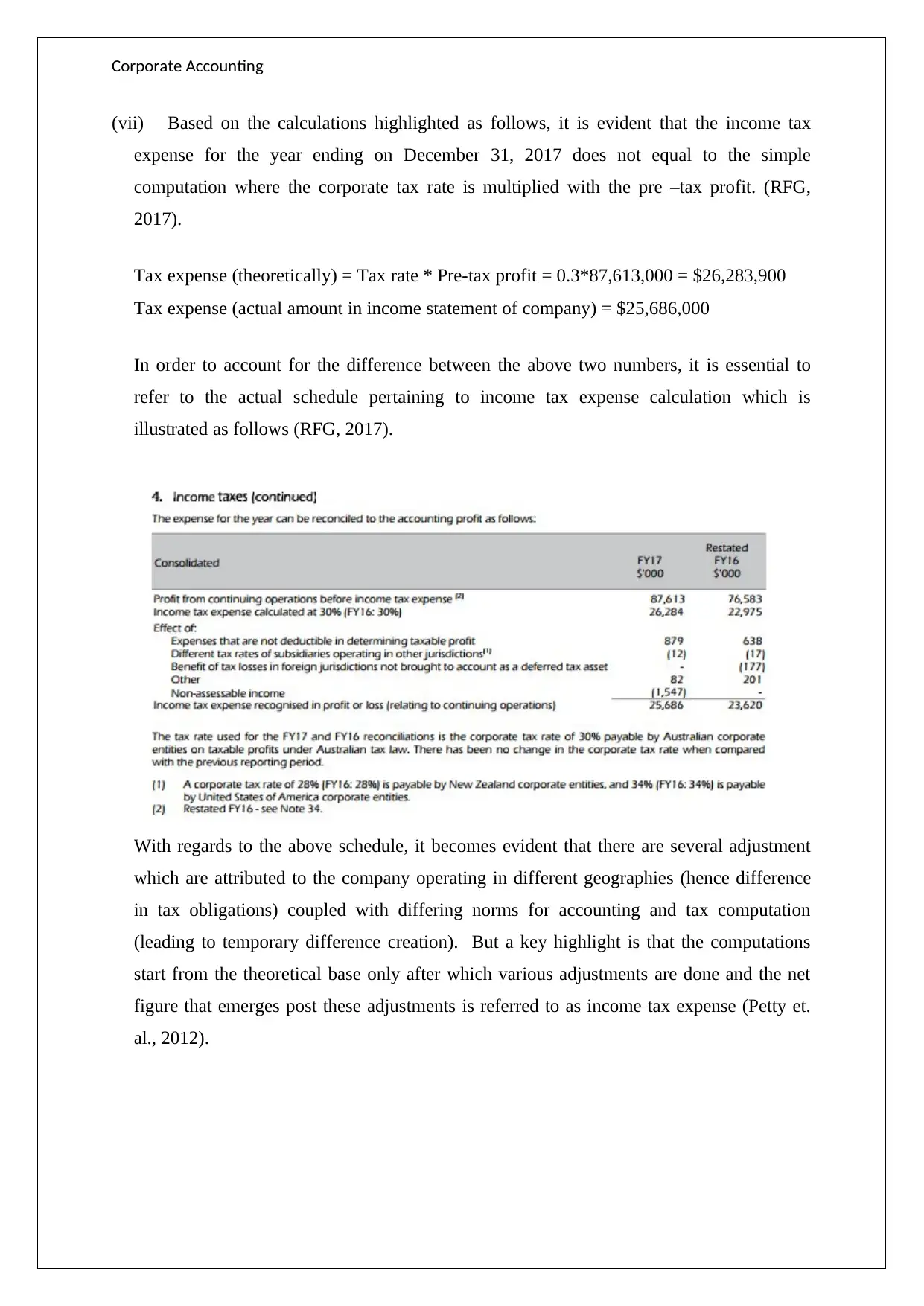

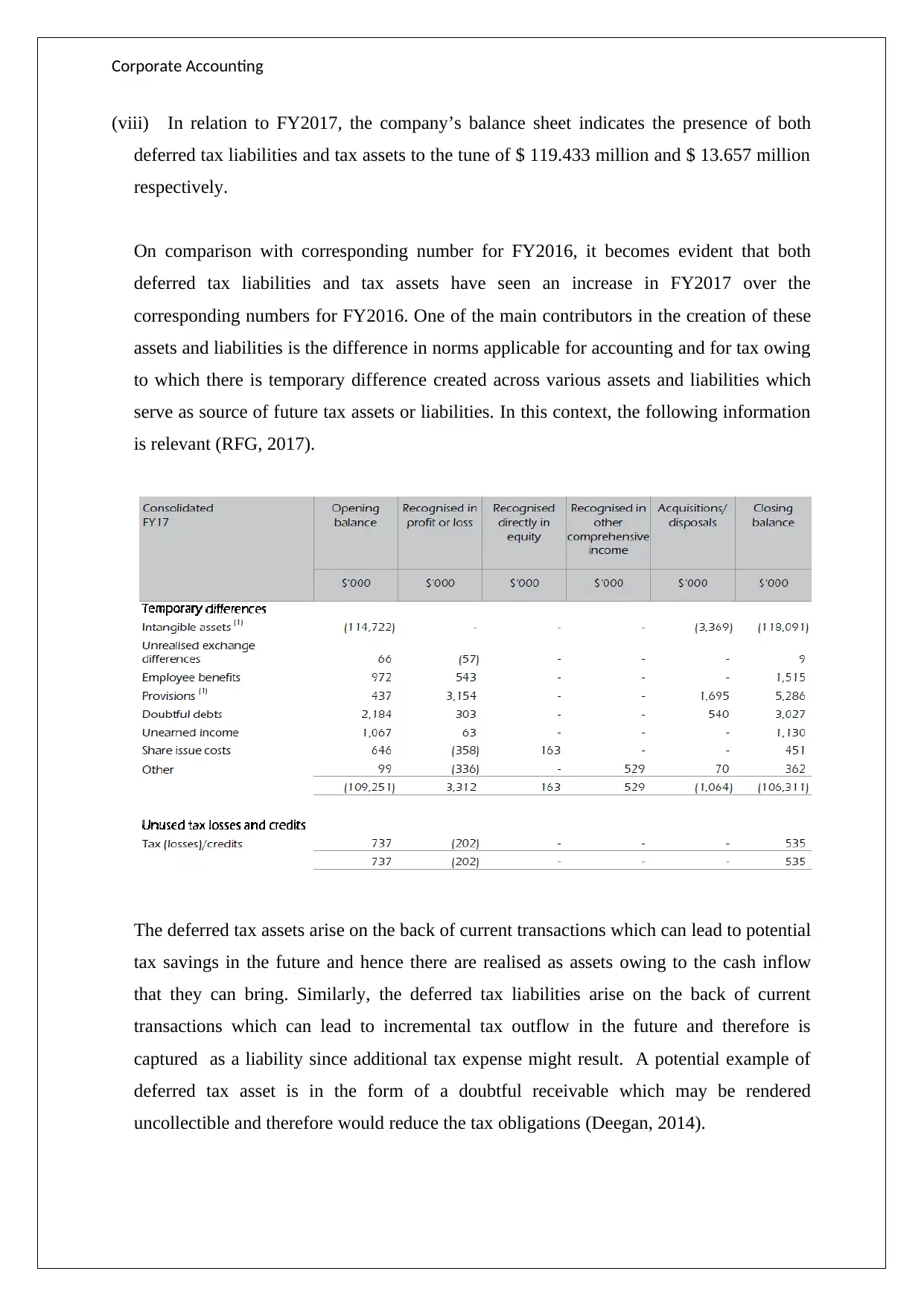

This report provides a comprehensive analysis of Retail Food Group's (RFG) financial statements for FY2017. It examines the cash flow statement, detailing receipts from customers, payments to suppliers and employees, and financing activities, highlighting the company's investments and financing strategies, including equity proceeds, borrowings, and dividend payments. The report also explores the other comprehensive income (OCI) statement, focusing on exchange differences and changes in the fair value of cash flow hedges, and discusses the rationale for recognizing these items in OCI. Furthermore, it delves into the accounting for corporate income tax, comparing the theoretical tax expense with the actual amount, analyzing deferred tax assets and liabilities, and explaining the differences between tax expense and tax payable. The analysis highlights the complexities of tax computation, the impact of accounting and tax norms, and the practical application of theoretical concepts, emphasizing the challenges in managing deferred tax assets and liabilities and the differences between accrual and cash accounting.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.