Corporate Accounting Report: Funds, Liabilities, and Assets

VerifiedAdded on 2022/08/20

|13

|3245

|12

Report

AI Summary

This report provides a comprehensive analysis of corporate accounting practices, focusing on the sources of funds, asset classification, and liabilities of two major companies: Rio Tinto and BHP Billiton. The report begins by exploring the different methods companies utilize to raise capital, categorizing them into internal and external sources. It then delves into the specific funding strategies employed by Rio Tinto and BHP Billiton, examining their reliance on retained earnings, long-term borrowings, and shareholder equity. The evolution of these funding sources over a three-year period is discussed, highlighting shifts from external to internal financing. Furthermore, the report provides an overview of AASB 137, focusing on provisions, contingent liabilities, and contingent assets, and how these standards are applied by the chosen companies. It also details the classification of assets and liabilities in the financial statements of Rio Tinto and BHP Billiton, including current and non-current assets and liabilities. Finally, the report concludes with an analysis of the asset measurement bases employed by both companies.

RUNNING HEAD: CORPORATE ACCOUNTING 0

Corporate Accounting

Report

Corporate Accounting

Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting 1

Abstract

There are different sources of raising funds, the choice of source depend on various

factors such as cost of raising fund, time and ownership. In order to understand the

concept of sources of raising funds two companies are chosen that are Rio Tinto and BHP

Billiton both the companies operate in metal and petroleum industry. The report highlights

the different sources that are available for companies and the sources they used in order

to raise funds. After that a brief overview of AASB 137 standard is given and asset and

liabilities classification of both the companies are given. At last, asset measurement use

by both the companies is disclosed. It is concluded from report that both the companies

witch to internal sources to raise funds that are retained earnings and reserves.

Abstract

There are different sources of raising funds, the choice of source depend on various

factors such as cost of raising fund, time and ownership. In order to understand the

concept of sources of raising funds two companies are chosen that are Rio Tinto and BHP

Billiton both the companies operate in metal and petroleum industry. The report highlights

the different sources that are available for companies and the sources they used in order

to raise funds. After that a brief overview of AASB 137 standard is given and asset and

liabilities classification of both the companies are given. At last, asset measurement use

by both the companies is disclosed. It is concluded from report that both the companies

witch to internal sources to raise funds that are retained earnings and reserves.

Corporate Accounting 2

Table of Contents

Introduction............................................................................................................................3

Different sources of Funds.....................................................................................................3

Evolution................................................................................................................................4

Demerits and merits...............................................................................................................4

Liabilities classification...........................................................................................................5

Assets classification...............................................................................................................5

AASB137................................................................................................................................6

Conclusion.............................................................................................................................7

References.............................................................................................................................8

Appendix................................................................................................................................9

Table of Contents

Introduction............................................................................................................................3

Different sources of Funds.....................................................................................................3

Evolution................................................................................................................................4

Demerits and merits...............................................................................................................4

Liabilities classification...........................................................................................................5

Assets classification...............................................................................................................5

AASB137................................................................................................................................6

Conclusion.............................................................................................................................7

References.............................................................................................................................8

Appendix................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting 3

Introduction

There are different sources that are used by the companies to raise funds. The main

sources of funds are divided into two categories; external sources and internal sources.

Funds are raised by the organizations to grow and expand in the market by investing in its

products or services. Companies use different source for raising funds in order to reduce

its cost and to gain maximum return with minimum risk. Companies mainly raise funds

through two sources that are equity and debt. Both the sources have some advantage and

disadvantage (Cornwall et.al, 2019). This report includes different sources of funds used

by BHP Billiton and Rio Tinto. Both these companies operate in the same segment.

Further, report includes evolution of sources by analyzing last 3 years financial statement

of companies. At last, asset classification and liabilities classification are disclosed by

considering AASB 137 “provisions contingent liabilities and contingent assets”. At last,

analyses of both the companies are done followed by conclusion.

Rio Tinto

Rio Tinto is Australian multinational company that operates in metal and mining segment.

In 2018, the company had turnover of US$ 40,522 billion with net income of US$ 13,925

billion. It is analysed from the balance sheet that the company mainly depend on two

sources of funds that are retained earnings and long term borrowings. In 2018, long term

borrowings of the company were $12,847 and retained earnings was $27,025. This

indicates that the company keep aside most of its profits in order to expand and grow in

the market. The company mainly depend on debts as compare to shareholder equity as

total shareholders’ equity in 2018 was $3,688. From the information taken from company’s

balance sheet it can be said that Rio Tinto mainly depend on internal sources of funds and

from external sources portion of debt in the capital structure is greater ( Rio Tinto, 2018).

BHP Billiton

BHP group limited operates in mining, petroleum and metal industry. The company was

established in 1885 and headquartered in Melbourne, Australia. BHP Billiton was formed

when BHP and Billiton merged in 2001. The annual turnover of the company in 2018 was

US$43,638 billion and net income was US$4,823 billion. It is analysed that the company

expanded its operations from last 3 years and due to that raise funds from different

sources. The capital structure of the company consists of both internal and external

sources. The external sources include debt and equity, debt of BHP Billiton in 2018 was

$24,069 and equity was $2,243. This indicates that the company mainly raise funds

through debts. The internal sources include retained earnings and reserve of the company

and retained earnings of the company in 2018 was $51,064 and reserve was $2,290 (BHP

Billiton, 2018). In a nutshell, BHP Billiton depends on internal sources for expansion and

growth in the market.

Different sources of Funds

There are many sources of raising funds but some of the most common sources that are

used organizations are long term loans, borrowings, equity, venture capital, reserves,

debentures and retained earnings. The choice of source depends on the company and

includes various factors such as cost of raising funds, time period and control. It is

essential for the companies to evaluate all the sources and opt for the source that benefit

the company by getting maximum return with minimum expenses. It became challenging

Introduction

There are different sources that are used by the companies to raise funds. The main

sources of funds are divided into two categories; external sources and internal sources.

Funds are raised by the organizations to grow and expand in the market by investing in its

products or services. Companies use different source for raising funds in order to reduce

its cost and to gain maximum return with minimum risk. Companies mainly raise funds

through two sources that are equity and debt. Both the sources have some advantage and

disadvantage (Cornwall et.al, 2019). This report includes different sources of funds used

by BHP Billiton and Rio Tinto. Both these companies operate in the same segment.

Further, report includes evolution of sources by analyzing last 3 years financial statement

of companies. At last, asset classification and liabilities classification are disclosed by

considering AASB 137 “provisions contingent liabilities and contingent assets”. At last,

analyses of both the companies are done followed by conclusion.

Rio Tinto

Rio Tinto is Australian multinational company that operates in metal and mining segment.

In 2018, the company had turnover of US$ 40,522 billion with net income of US$ 13,925

billion. It is analysed from the balance sheet that the company mainly depend on two

sources of funds that are retained earnings and long term borrowings. In 2018, long term

borrowings of the company were $12,847 and retained earnings was $27,025. This

indicates that the company keep aside most of its profits in order to expand and grow in

the market. The company mainly depend on debts as compare to shareholder equity as

total shareholders’ equity in 2018 was $3,688. From the information taken from company’s

balance sheet it can be said that Rio Tinto mainly depend on internal sources of funds and

from external sources portion of debt in the capital structure is greater ( Rio Tinto, 2018).

BHP Billiton

BHP group limited operates in mining, petroleum and metal industry. The company was

established in 1885 and headquartered in Melbourne, Australia. BHP Billiton was formed

when BHP and Billiton merged in 2001. The annual turnover of the company in 2018 was

US$43,638 billion and net income was US$4,823 billion. It is analysed that the company

expanded its operations from last 3 years and due to that raise funds from different

sources. The capital structure of the company consists of both internal and external

sources. The external sources include debt and equity, debt of BHP Billiton in 2018 was

$24,069 and equity was $2,243. This indicates that the company mainly raise funds

through debts. The internal sources include retained earnings and reserve of the company

and retained earnings of the company in 2018 was $51,064 and reserve was $2,290 (BHP

Billiton, 2018). In a nutshell, BHP Billiton depends on internal sources for expansion and

growth in the market.

Different sources of Funds

There are many sources of raising funds but some of the most common sources that are

used organizations are long term loans, borrowings, equity, venture capital, reserves,

debentures and retained earnings. The choice of source depends on the company and

includes various factors such as cost of raising funds, time period and control. It is

essential for the companies to evaluate all the sources and opt for the source that benefit

the company by getting maximum return with minimum expenses. It became challenging

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting 4

situation for large organizations to choose the right source of raising fund as business

operations of the organizations get affected because of its capital structure. In order to

understand the impact of different sources on capital structure, Rio Tinto and BHP Billiton

capital structures are analysed (Beiki and Elizaie,2016).

Rio Tinto raises funds through internal sources that are retained earnings and reserves.

The total internal fund available with the company in 2018 was $35,686 and fundraised

from external sources amounted for $16,535 that included debt of $12,487 and equity of

$3,688. It can be said that mainly the company depend on internal sources of funds as

69% of funds in the company raised through internal sources that means by keeping the

profits aside to invest in future growth and development and remaining 31% funds are

generated from external sources. (Rio Tinto,2018).

BHP Billiton also raises funds through internal sources that include retained earnings and

reserves. The company’s internal fund amounted in 2018 was $53,354 and external fund

amounted was $26,312. This indicates that BHP Billiton use internal funds for expansion

and growth as the ratio of internal funds in the organization was double the external funds

or the company generate 67% of funds through internal sources and remaining 33% from

external sources. Hence, both the companies depend on internal sources of fund (BHP

Billiton,2018).

Evolution

Rio Tinto source of raising funds changed from external sources to internal sources.

External sources include equity and debts, shareholders’ equity of the company reduced

from $4,139 in 2016 to $3,688 in 2018 (Rio Tinto, 2018). Further, the company paid off its

borrowings due to that its debts reduced from $17,470 in 2016 to $12,847 in 2018. This

indicates that Rio Tinto shifts to internal sources from external sources, as internal sources

increased by 25% (Rio Tinto,2017). Hence, the company changes or evolved its

fundraising sources from external to internal

BHP Billiton capital structure mainly have major portion of but the company paid most of

its debt from last three years as in 2016 debt of the company was $31,768 and in 2018

debt of the company was $24,069 (BHP Billiton, 2018). Further, the equity portion of the

company remains the same from last 3 years. BHP Billiton shifted its focus to internal

sources and reduced its external sources percentage in the company capital structure. As

the retained earnings of the company in 2016 was $49,542 and in 2018 the retained

earnings was $51,064 that indicate that the company reduce its debts because of its

profitable situation in last two years due to that retained earnings were increased and debt

was paid off by the company (BHP Billiton, 2017).

Demerits and merits

There are different sources of fund and each source has some merit and demerit.

Borrowings and equity are the most used sources. When the companies raise funds

through debentures it increases the cost of capital as interest to be paid on timely basis to

debenture holders. Further, merits of raising fund through this source include tax benefits

and no such control of lender on the business operations. On the other side, shareholders

equity is one of the ways that companies prefer most as it is less risky and the company

only obliged to pay the amount to shareholders when the business is going to wind up.

The company pay dividend to its equity holders as a reward of the amount that the

company is using. This source also has some drawbacks such as more control of equity

situation for large organizations to choose the right source of raising fund as business

operations of the organizations get affected because of its capital structure. In order to

understand the impact of different sources on capital structure, Rio Tinto and BHP Billiton

capital structures are analysed (Beiki and Elizaie,2016).

Rio Tinto raises funds through internal sources that are retained earnings and reserves.

The total internal fund available with the company in 2018 was $35,686 and fundraised

from external sources amounted for $16,535 that included debt of $12,487 and equity of

$3,688. It can be said that mainly the company depend on internal sources of funds as

69% of funds in the company raised through internal sources that means by keeping the

profits aside to invest in future growth and development and remaining 31% funds are

generated from external sources. (Rio Tinto,2018).

BHP Billiton also raises funds through internal sources that include retained earnings and

reserves. The company’s internal fund amounted in 2018 was $53,354 and external fund

amounted was $26,312. This indicates that BHP Billiton use internal funds for expansion

and growth as the ratio of internal funds in the organization was double the external funds

or the company generate 67% of funds through internal sources and remaining 33% from

external sources. Hence, both the companies depend on internal sources of fund (BHP

Billiton,2018).

Evolution

Rio Tinto source of raising funds changed from external sources to internal sources.

External sources include equity and debts, shareholders’ equity of the company reduced

from $4,139 in 2016 to $3,688 in 2018 (Rio Tinto, 2018). Further, the company paid off its

borrowings due to that its debts reduced from $17,470 in 2016 to $12,847 in 2018. This

indicates that Rio Tinto shifts to internal sources from external sources, as internal sources

increased by 25% (Rio Tinto,2017). Hence, the company changes or evolved its

fundraising sources from external to internal

BHP Billiton capital structure mainly have major portion of but the company paid most of

its debt from last three years as in 2016 debt of the company was $31,768 and in 2018

debt of the company was $24,069 (BHP Billiton, 2018). Further, the equity portion of the

company remains the same from last 3 years. BHP Billiton shifted its focus to internal

sources and reduced its external sources percentage in the company capital structure. As

the retained earnings of the company in 2016 was $49,542 and in 2018 the retained

earnings was $51,064 that indicate that the company reduce its debts because of its

profitable situation in last two years due to that retained earnings were increased and debt

was paid off by the company (BHP Billiton, 2017).

Demerits and merits

There are different sources of fund and each source has some merit and demerit.

Borrowings and equity are the most used sources. When the companies raise funds

through debentures it increases the cost of capital as interest to be paid on timely basis to

debenture holders. Further, merits of raising fund through this source include tax benefits

and no such control of lender on the business operations. On the other side, shareholders

equity is one of the ways that companies prefer most as it is less risky and the company

only obliged to pay the amount to shareholders when the business is going to wind up.

The company pay dividend to its equity holders as a reward of the amount that the

company is using. This source also has some drawbacks such as more control of equity

Corporate Accounting 5

owners in decision making, and with the majority votes changes can be made in the

business plan in order to maximize the wealth of shareholder (Vermimmen et.al,2014).

Retained earnings are the safest source of raising funds as it is the part of profits.

Companies keep this aside accordance with their future expansion and growth plans. This

source is safest because there is no cost of raising funds. But on the other side, if the

companies kept huge amount of their profits aside this leads to opportunity cost, that

means the company can invest this amount in some profitable ventures in order to get

higher return as the ideal amount is the burden for the companies (Arnold,2012).

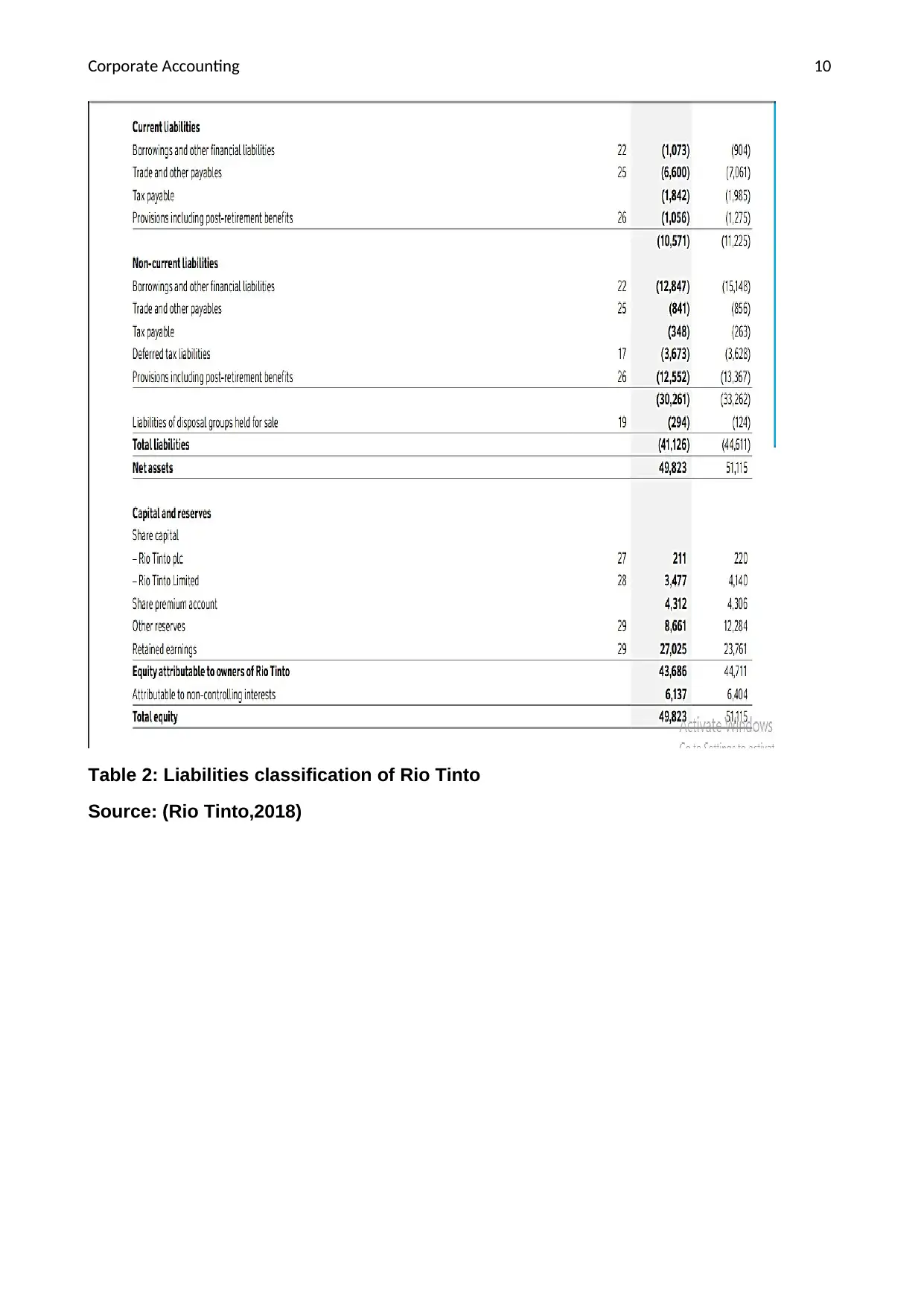

Liabilities classification

The liabilities of the companies are classified in three categories that are non-current

liabilities, current liabilities and contingent liabilities ( Bauman and Shaw,2016). Rio Tinto

balance sheet showed liabilities classification as the same mentioned above. Under the

current liabilities the company includes short term borrowings, trade payables, tax payable

and provisions that need to pay within the one year. Under the head of non-current

liabilities the company includes long term borrowings, trade payable, tax payable, deferred

tax liabilities, provisions and all these liabilities are paid after one year by the company.

This indicates that the company classify its liabilities on the basis of time period. Further,

the contingent liabilities are not includes in the balance sheet rather, showed in the notes

or appendix of financial statements (table 2).

BHP Billiton liabilities classification is based on the time period also as the company

categorized its liabilities as “current liabilities and non-current liabilities”. Under the head of

current liabilities all the liabilities that are paid off after one year is included such as long

term trade payables, liabilities that are interest bearing, other financial liabilities, current tax

payable under head of non-current liabilities, deferred tax, provisions related to uncertain

events. The change that can be seen in the classification of long term liabilities is its

bifurcation as interest-bearing liabilities and non-interest bearing liabilities. Further, under

the head of current liabilities all the liabilities that are need to pay within 1 year are

included such as trade payable, short term liabilities that are interest bearing, liabilities that

are held for sales, and provisions related to current tax payable. (table 4).

Assets classification

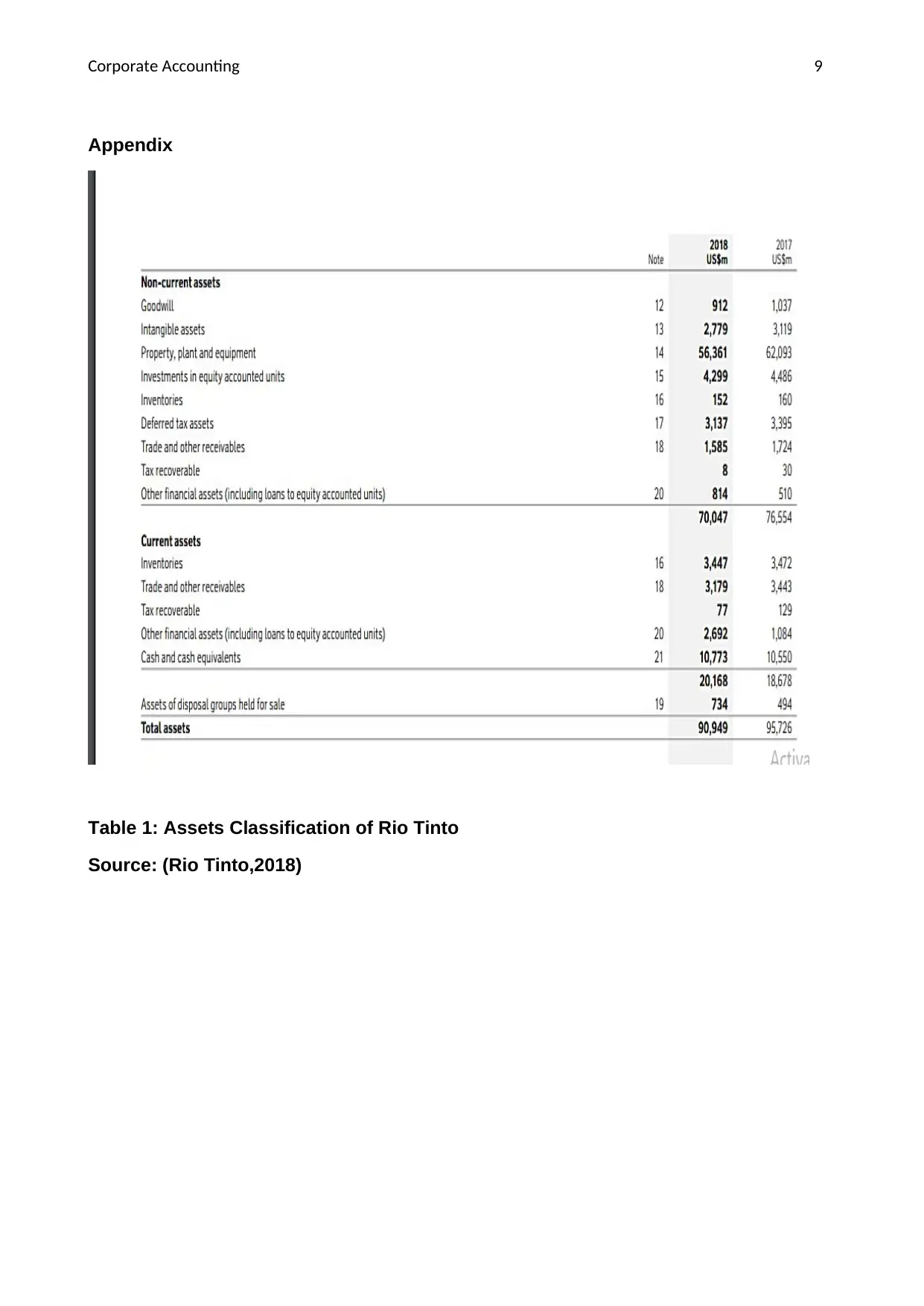

Assets classification includes classification as intangible assets and tangible assets,

assets that are current or non-current, operating assets and non-operating assets (Weil

et.al,2013). Rio Tinto classifies its assets as non-current assets and current assets. Under

the head of non-current assets following items are include by the company that are

goodwill, intangible assets, property, investments, inventories, deferred tax assets, “trade

receivables, tax recoverable, and other financial assets”. The company includes intangible

assets in its head of non-current assets. On the other side, under the head of current

assets items are inventories, account receivables, other financial assets and tax recovery

and cash equivalent. The company included inventories in both the head as there are

inventories such as metal that cannot be transformed into finished goods i9n one year it

might require more than one year (table 1).

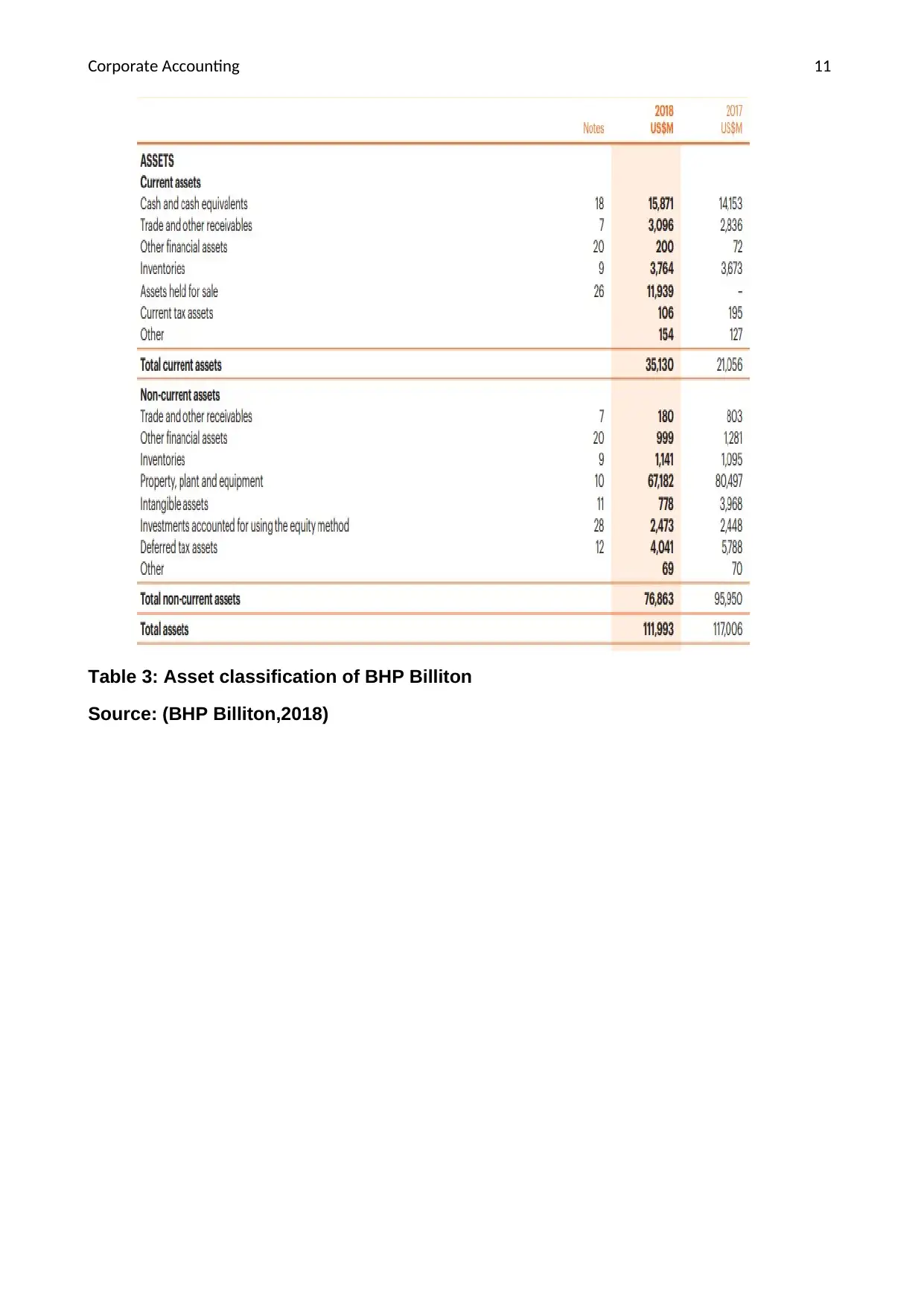

BHP Billiton also classifies its assets as “current assets and non-current assets”. Thus

classification helps the companies to identify assets that can be transformed into cash

within one year and assets that can be give return for long term. Under the current assets

the items are cash and bank, account receivables, other financial assets, raw material or

owners in decision making, and with the majority votes changes can be made in the

business plan in order to maximize the wealth of shareholder (Vermimmen et.al,2014).

Retained earnings are the safest source of raising funds as it is the part of profits.

Companies keep this aside accordance with their future expansion and growth plans. This

source is safest because there is no cost of raising funds. But on the other side, if the

companies kept huge amount of their profits aside this leads to opportunity cost, that

means the company can invest this amount in some profitable ventures in order to get

higher return as the ideal amount is the burden for the companies (Arnold,2012).

Liabilities classification

The liabilities of the companies are classified in three categories that are non-current

liabilities, current liabilities and contingent liabilities ( Bauman and Shaw,2016). Rio Tinto

balance sheet showed liabilities classification as the same mentioned above. Under the

current liabilities the company includes short term borrowings, trade payables, tax payable

and provisions that need to pay within the one year. Under the head of non-current

liabilities the company includes long term borrowings, trade payable, tax payable, deferred

tax liabilities, provisions and all these liabilities are paid after one year by the company.

This indicates that the company classify its liabilities on the basis of time period. Further,

the contingent liabilities are not includes in the balance sheet rather, showed in the notes

or appendix of financial statements (table 2).

BHP Billiton liabilities classification is based on the time period also as the company

categorized its liabilities as “current liabilities and non-current liabilities”. Under the head of

current liabilities all the liabilities that are paid off after one year is included such as long

term trade payables, liabilities that are interest bearing, other financial liabilities, current tax

payable under head of non-current liabilities, deferred tax, provisions related to uncertain

events. The change that can be seen in the classification of long term liabilities is its

bifurcation as interest-bearing liabilities and non-interest bearing liabilities. Further, under

the head of current liabilities all the liabilities that are need to pay within 1 year are

included such as trade payable, short term liabilities that are interest bearing, liabilities that

are held for sales, and provisions related to current tax payable. (table 4).

Assets classification

Assets classification includes classification as intangible assets and tangible assets,

assets that are current or non-current, operating assets and non-operating assets (Weil

et.al,2013). Rio Tinto classifies its assets as non-current assets and current assets. Under

the head of non-current assets following items are include by the company that are

goodwill, intangible assets, property, investments, inventories, deferred tax assets, “trade

receivables, tax recoverable, and other financial assets”. The company includes intangible

assets in its head of non-current assets. On the other side, under the head of current

assets items are inventories, account receivables, other financial assets and tax recovery

and cash equivalent. The company included inventories in both the head as there are

inventories such as metal that cannot be transformed into finished goods i9n one year it

might require more than one year (table 1).

BHP Billiton also classifies its assets as “current assets and non-current assets”. Thus

classification helps the companies to identify assets that can be transformed into cash

within one year and assets that can be give return for long term. Under the current assets

the items are cash and bank, account receivables, other financial assets, raw material or

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting 6

stock, assets that are for sales, assets as current tax and other assets. All these assets

can be converted into cash within one year. Further, under the head of non-current assets

following items are included such as long term financial assets, account receivables, stock,

building and equipment, assets that are intangible, investments, and deferred tax.. BHP

Billiton and Rio Tinto use same classification type in order to classify their assets rather

than classifying it on the basis of tangible and intangible assets (table 3).

AASB137

AASB 137 is Australian accounting standard that focus on a set of standard that should be

meet by all the companies in Australia in order to make its “provisions contingent liabilities

and assets”. Further, AASB 137 standard ensures that the companies use appropriate

criteria to disclose information about their provisions related to contingent assets and

contingent liabilities. As per this standard companies maintain provision as a liability that

indicates outflow of resources from the company. On the other side, contingent assets are

gains for the companies due to unplanned events (Wang,2019).

BHP Billiton classify its contingent liabilities on the basis of AASB 137 standard, as

contingent liabilities of the company in 2017 was US$ 3,610 that included tax and other

matters and amount of subsidiaries and joint operations of BHP Billiton . Further, items

include uncertain tax, royalty matters, demerger of South32 and bank guarantees (BHP

Billiton, 2018).

Rio Tinto follow IAS 37 for “provisions of assets and liabilities”, accordance with

international standard “a contract under which the unavoidable costs of meeting the

obligations under the contract exceed the economic benefits expected to receive “. On the

other side, provisions are made “when assets dedicated to the contract are fully impaired

or the contract becomes stranded as a result of business decision”. As per this accounting

standard contingent liabilities of Rio Tinto in 2018 was US$317 million. Hence, by

analysing both the companies accounting standard criteria it is found that BHP Billiton use

AASB 137 criteria for disclosing information related to contingent liabilities and assets and

Rio Tinto use IAS 37 to disclose its information (Rio Tinto,2018).

Measurements

Different companies have different measurement techniques, Rio Tinto classify and

measure its assets in the following ways; some assets are measured at the fair value and

some to be measured at amortized cost . The company measure its debt at the amortized

value, trade receivables of the company are measure at their transaction price. Remaining

financial assets are measured at fair value in the initial stage and after that transaction

cost is added in the amount. The equity investment was measured on the basis of fair

value losses or gains. Hence, an asset measurement by Rio Tinto is done by on the basis

of two measurement first is fair value second is on the basis of amortized cost (Rio

Tinto,2018).

BHP Billiton measure trade receivables at fair value at the initial stage and after that

subsequently at amortized cost using effective interest method. Inventories of the

company measured at the lower cost and net realizable value. Further, plant, equipment

and property measured at cost less impairment charges and accumulated depreciation.

Goodwill measure at the present value of the future cash flows and fair value less cost of

disposal is used to measure the amount of minerals and petroleum. Hence from the

stock, assets that are for sales, assets as current tax and other assets. All these assets

can be converted into cash within one year. Further, under the head of non-current assets

following items are included such as long term financial assets, account receivables, stock,

building and equipment, assets that are intangible, investments, and deferred tax.. BHP

Billiton and Rio Tinto use same classification type in order to classify their assets rather

than classifying it on the basis of tangible and intangible assets (table 3).

AASB137

AASB 137 is Australian accounting standard that focus on a set of standard that should be

meet by all the companies in Australia in order to make its “provisions contingent liabilities

and assets”. Further, AASB 137 standard ensures that the companies use appropriate

criteria to disclose information about their provisions related to contingent assets and

contingent liabilities. As per this standard companies maintain provision as a liability that

indicates outflow of resources from the company. On the other side, contingent assets are

gains for the companies due to unplanned events (Wang,2019).

BHP Billiton classify its contingent liabilities on the basis of AASB 137 standard, as

contingent liabilities of the company in 2017 was US$ 3,610 that included tax and other

matters and amount of subsidiaries and joint operations of BHP Billiton . Further, items

include uncertain tax, royalty matters, demerger of South32 and bank guarantees (BHP

Billiton, 2018).

Rio Tinto follow IAS 37 for “provisions of assets and liabilities”, accordance with

international standard “a contract under which the unavoidable costs of meeting the

obligations under the contract exceed the economic benefits expected to receive “. On the

other side, provisions are made “when assets dedicated to the contract are fully impaired

or the contract becomes stranded as a result of business decision”. As per this accounting

standard contingent liabilities of Rio Tinto in 2018 was US$317 million. Hence, by

analysing both the companies accounting standard criteria it is found that BHP Billiton use

AASB 137 criteria for disclosing information related to contingent liabilities and assets and

Rio Tinto use IAS 37 to disclose its information (Rio Tinto,2018).

Measurements

Different companies have different measurement techniques, Rio Tinto classify and

measure its assets in the following ways; some assets are measured at the fair value and

some to be measured at amortized cost . The company measure its debt at the amortized

value, trade receivables of the company are measure at their transaction price. Remaining

financial assets are measured at fair value in the initial stage and after that transaction

cost is added in the amount. The equity investment was measured on the basis of fair

value losses or gains. Hence, an asset measurement by Rio Tinto is done by on the basis

of two measurement first is fair value second is on the basis of amortized cost (Rio

Tinto,2018).

BHP Billiton measure trade receivables at fair value at the initial stage and after that

subsequently at amortized cost using effective interest method. Inventories of the

company measured at the lower cost and net realizable value. Further, plant, equipment

and property measured at cost less impairment charges and accumulated depreciation.

Goodwill measure at the present value of the future cash flows and fair value less cost of

disposal is used to measure the amount of minerals and petroleum. Hence from the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting 7

analysis of assets measurement of BHP Billiton it is found that mainly the company

measure its assets using fair value method (BHP Billiton, 2018).

Conclusion

The analyses of both the companies are done from the analysis it is concluded that Rio

Tinto mainly depend on two sources that are retained earnings and long term borrowings

for growth and expansion in the market. On the other side, BHP Billiton mainly focus on

internal sources for raising funds as the company reduced its debt amount in the capital

structure and increased its retained earnings. It is concluded that both the companies

operates in same segment in Australia market but use different accounting standards to

disclose information related to “provisions of contingent liabilities and contingent assets”.

As Rio Tinto use IAS 37 standard in order to disclose and measure amount of provisions

and on the other side BHP Billiton follow AASB 137 standard for disclosing its provisions.

At last, it can be said that there are many sources available with companies to raise funds

and it is important to evaluate each source in order to get higher return by reducing the

cost of capital and by making effective capital structure for long term growth and

profitability.

analysis of assets measurement of BHP Billiton it is found that mainly the company

measure its assets using fair value method (BHP Billiton, 2018).

Conclusion

The analyses of both the companies are done from the analysis it is concluded that Rio

Tinto mainly depend on two sources that are retained earnings and long term borrowings

for growth and expansion in the market. On the other side, BHP Billiton mainly focus on

internal sources for raising funds as the company reduced its debt amount in the capital

structure and increased its retained earnings. It is concluded that both the companies

operates in same segment in Australia market but use different accounting standards to

disclose information related to “provisions of contingent liabilities and contingent assets”.

As Rio Tinto use IAS 37 standard in order to disclose and measure amount of provisions

and on the other side BHP Billiton follow AASB 137 standard for disclosing its provisions.

At last, it can be said that there are many sources available with companies to raise funds

and it is important to evaluate each source in order to get higher return by reducing the

cost of capital and by making effective capital structure for long term growth and

profitability.

Corporate Accounting 8

References

Arnold, G., 2012. Corporate financial management. Pearson Education.

Bauman, M.P. and Shaw, K.W., 2016. Balance sheet classification and the valuation of

deferred taxes. Research in Accounting Regulation, 28(2), pp.77-85.\

BHP Billiton, 2018. Annual Report 2018. Accessed From:

https://www.bhp.com/-/media/documents/investors/annual-reports/2018/

bhpannualreport2018.pdf?la=en

BHP Billiton,2017, Annual Report 2017. Accessed From:

https://www.bhp.com/-/media/documents/investors/annual-reports/2017/

bhpannualreport2017.pdf

Cornwall, J.R., Vang, D.O. and Hartman, J.M., 2019. Entrepreneurial financial

management: An applied approach. Routledge.

Rio Tinto, 2017. Annual Report 2017. Accessed From:

https://www.asx.com.au/asxpdf/20180302/pdf/43s3gt12q9npd5.pdf

Rio Tinto, 2018. Annual Report 2018. Accessed From:

http://www.annualreports.com/HostedData/AnnualReports/PDF/LSE_RIOA_2018.pdf

Vernimmen, P., Quiry, P., Dallocchio, M., Le Fur, Y. and Salvi, A., 2014. Corporate

finance: theory and practice. John Wiley & Sons.

Wang, X., 2019. Compliance Over Time by Australian Firms with IFRS Disclosure

Requirements. Australian Accounting Review, 29(4), pp.679-691.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

References

Arnold, G., 2012. Corporate financial management. Pearson Education.

Bauman, M.P. and Shaw, K.W., 2016. Balance sheet classification and the valuation of

deferred taxes. Research in Accounting Regulation, 28(2), pp.77-85.\

BHP Billiton, 2018. Annual Report 2018. Accessed From:

https://www.bhp.com/-/media/documents/investors/annual-reports/2018/

bhpannualreport2018.pdf?la=en

BHP Billiton,2017, Annual Report 2017. Accessed From:

https://www.bhp.com/-/media/documents/investors/annual-reports/2017/

bhpannualreport2017.pdf

Cornwall, J.R., Vang, D.O. and Hartman, J.M., 2019. Entrepreneurial financial

management: An applied approach. Routledge.

Rio Tinto, 2017. Annual Report 2017. Accessed From:

https://www.asx.com.au/asxpdf/20180302/pdf/43s3gt12q9npd5.pdf

Rio Tinto, 2018. Annual Report 2018. Accessed From:

http://www.annualreports.com/HostedData/AnnualReports/PDF/LSE_RIOA_2018.pdf

Vernimmen, P., Quiry, P., Dallocchio, M., Le Fur, Y. and Salvi, A., 2014. Corporate

finance: theory and practice. John Wiley & Sons.

Wang, X., 2019. Compliance Over Time by Australian Firms with IFRS Disclosure

Requirements. Australian Accounting Review, 29(4), pp.679-691.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting 9

Appendix

Table 1: Assets Classification of Rio Tinto

Source: (Rio Tinto,2018)

Appendix

Table 1: Assets Classification of Rio Tinto

Source: (Rio Tinto,2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting 10

Table 2: Liabilities classification of Rio Tinto

Source: (Rio Tinto,2018)

Table 2: Liabilities classification of Rio Tinto

Source: (Rio Tinto,2018)

Corporate Accounting 11

Table 3: Asset classification of BHP Billiton

Source: (BHP Billiton,2018)

Table 3: Asset classification of BHP Billiton

Source: (BHP Billiton,2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.